Financial Management for Hotel Industry

VerifiedAdded on 2023/01/09

|8

|1257

|98

AI Summary

This document provides a cash budget and profit budget forecast for a hotel in the hotel industry. It includes calculations for cash collection and payments to suppliers, as well as an analysis of the cash flow and profit projections. The document also explains the importance of cash and profit budgets in financial management.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL MANAGEMENT

FOR HOTEL INDUSTRY

FOR HOTEL INDUSTRY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

TASK 1............................................................................................................................................1

Cash Budget of Hotel for January to December 2020.................................................................1

TASK 2............................................................................................................................................5

Profit Budget Forecast for January to June 2020.........................................................................5

TABLE OF CONTENTS................................................................................................................2

TASK 1............................................................................................................................................1

Cash Budget of Hotel for January to December 2020.................................................................1

TASK 2............................................................................................................................................5

Profit Budget Forecast for January to June 2020.........................................................................5

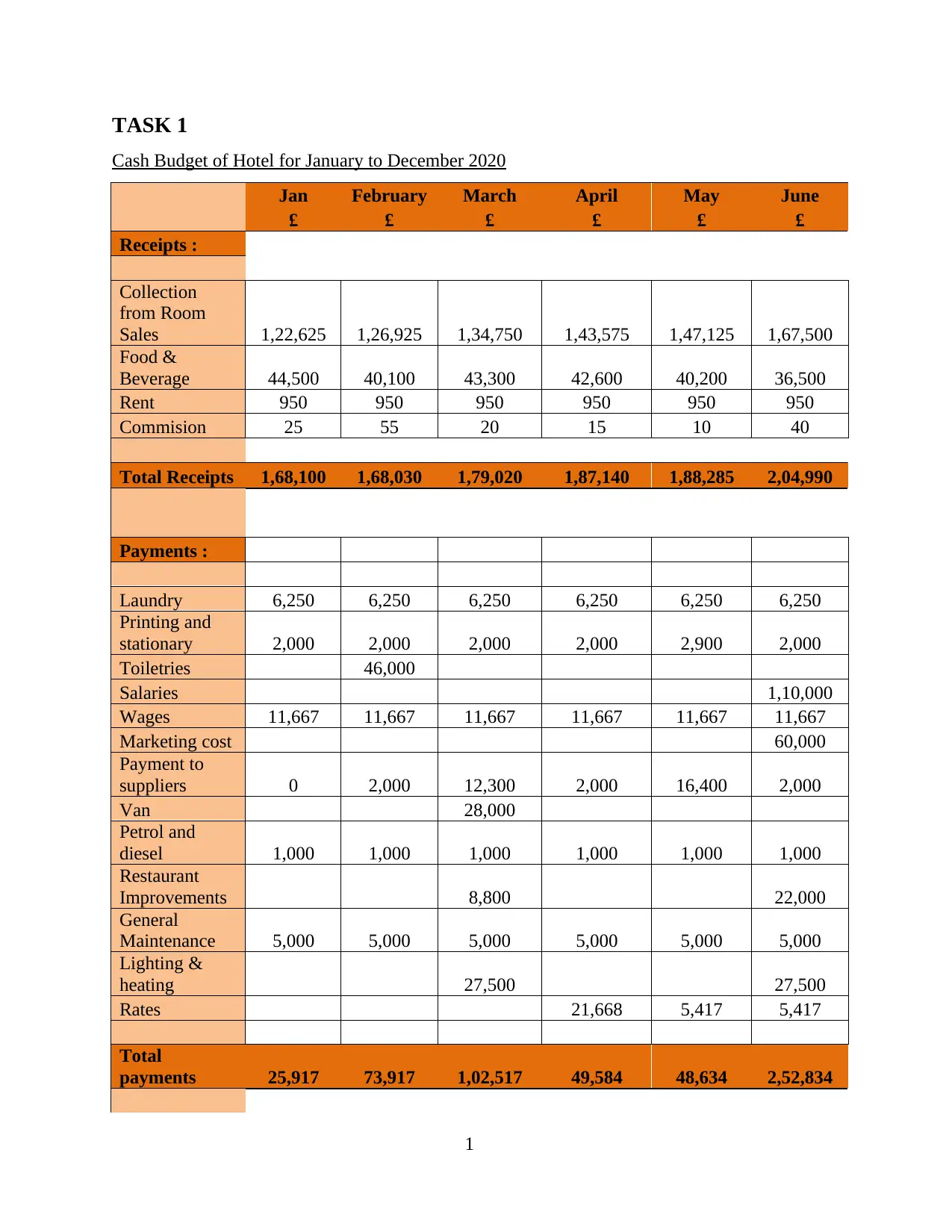

TASK 1

Cash Budget of Hotel for January to December 2020

Jan February March April May June

£ £ £ £ £ £

Receipts :

Collection

from Room

Sales 1,22,625 1,26,925 1,34,750 1,43,575 1,47,125 1,67,500

Food &

Beverage 44,500 40,100 43,300 42,600 40,200 36,500

Rent 950 950 950 950 950 950

Commision 25 55 20 15 10 40

Total Receipts 1,68,100 1,68,030 1,79,020 1,87,140 1,88,285 2,04,990

Payments :

Laundry 6,250 6,250 6,250 6,250 6,250 6,250

Printing and

stationary 2,000 2,000 2,000 2,000 2,900 2,000

Toiletries 46,000

Salaries 1,10,000

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Marketing cost 60,000

Payment to

suppliers 0 2,000 12,300 2,000 16,400 2,000

Van 28,000

Petrol and

diesel 1,000 1,000 1,000 1,000 1,000 1,000

Restaurant

Improvements 8,800 22,000

General

Maintenance 5,000 5,000 5,000 5,000 5,000 5,000

Lighting &

heating 27,500 27,500

Rates 21,668 5,417 5,417

Total

payments 25,917 73,917 1,02,517 49,584 48,634 2,52,834

1

Cash Budget of Hotel for January to December 2020

Jan February March April May June

£ £ £ £ £ £

Receipts :

Collection

from Room

Sales 1,22,625 1,26,925 1,34,750 1,43,575 1,47,125 1,67,500

Food &

Beverage 44,500 40,100 43,300 42,600 40,200 36,500

Rent 950 950 950 950 950 950

Commision 25 55 20 15 10 40

Total Receipts 1,68,100 1,68,030 1,79,020 1,87,140 1,88,285 2,04,990

Payments :

Laundry 6,250 6,250 6,250 6,250 6,250 6,250

Printing and

stationary 2,000 2,000 2,000 2,000 2,900 2,000

Toiletries 46,000

Salaries 1,10,000

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Marketing cost 60,000

Payment to

suppliers 0 2,000 12,300 2,000 16,400 2,000

Van 28,000

Petrol and

diesel 1,000 1,000 1,000 1,000 1,000 1,000

Restaurant

Improvements 8,800 22,000

General

Maintenance 5,000 5,000 5,000 5,000 5,000 5,000

Lighting &

heating 27,500 27,500

Rates 21,668 5,417 5,417

Total

payments 25,917 73,917 1,02,517 49,584 48,634 2,52,834

1

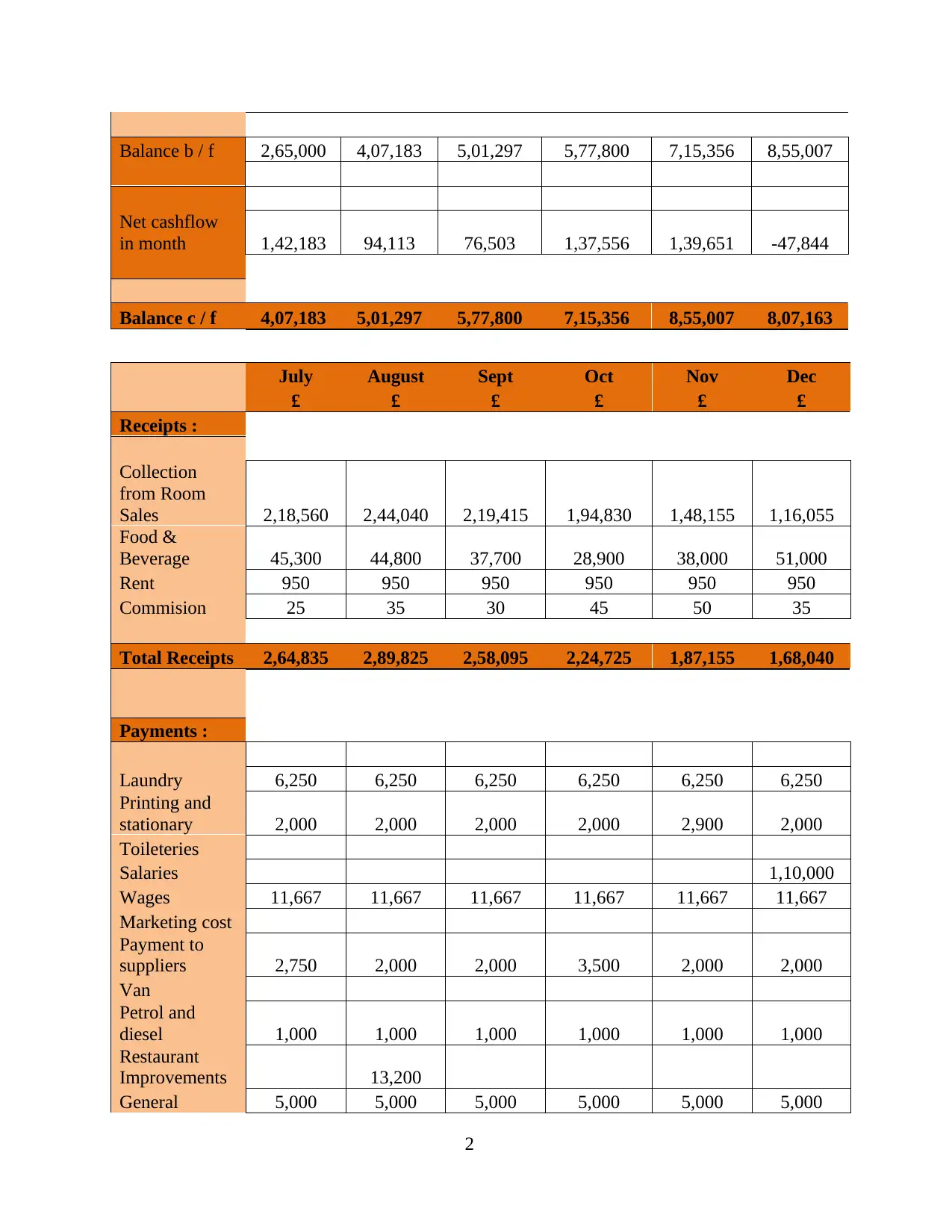

Balance b / f 2,65,000 4,07,183 5,01,297 5,77,800 7,15,356 8,55,007

Net cashflow

in month 1,42,183 94,113 76,503 1,37,556 1,39,651 -47,844

Balance c / f 4,07,183 5,01,297 5,77,800 7,15,356 8,55,007 8,07,163

July August Sept Oct Nov Dec

£ £ £ £ £ £

Receipts :

Collection

from Room

Sales 2,18,560 2,44,040 2,19,415 1,94,830 1,48,155 1,16,055

Food &

Beverage 45,300 44,800 37,700 28,900 38,000 51,000

Rent 950 950 950 950 950 950

Commision 25 35 30 45 50 35

Total Receipts 2,64,835 2,89,825 2,58,095 2,24,725 1,87,155 1,68,040

Payments :

Laundry 6,250 6,250 6,250 6,250 6,250 6,250

Printing and

stationary 2,000 2,000 2,000 2,000 2,900 2,000

Toileteries

Salaries 1,10,000

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Marketing cost

Payment to

suppliers 2,750 2,000 2,000 3,500 2,000 2,000

Van

Petrol and

diesel 1,000 1,000 1,000 1,000 1,000 1,000

Restaurant

Improvements 13,200

General 5,000 5,000 5,000 5,000 5,000 5,000

2

Net cashflow

in month 1,42,183 94,113 76,503 1,37,556 1,39,651 -47,844

Balance c / f 4,07,183 5,01,297 5,77,800 7,15,356 8,55,007 8,07,163

July August Sept Oct Nov Dec

£ £ £ £ £ £

Receipts :

Collection

from Room

Sales 2,18,560 2,44,040 2,19,415 1,94,830 1,48,155 1,16,055

Food &

Beverage 45,300 44,800 37,700 28,900 38,000 51,000

Rent 950 950 950 950 950 950

Commision 25 35 30 45 50 35

Total Receipts 2,64,835 2,89,825 2,58,095 2,24,725 1,87,155 1,68,040

Payments :

Laundry 6,250 6,250 6,250 6,250 6,250 6,250

Printing and

stationary 2,000 2,000 2,000 2,000 2,900 2,000

Toileteries

Salaries 1,10,000

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Marketing cost

Payment to

suppliers 2,750 2,000 2,000 3,500 2,000 2,000

Van

Petrol and

diesel 1,000 1,000 1,000 1,000 1,000 1,000

Restaurant

Improvements 13,200

General 5,000 5,000 5,000 5,000 5,000 5,000

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

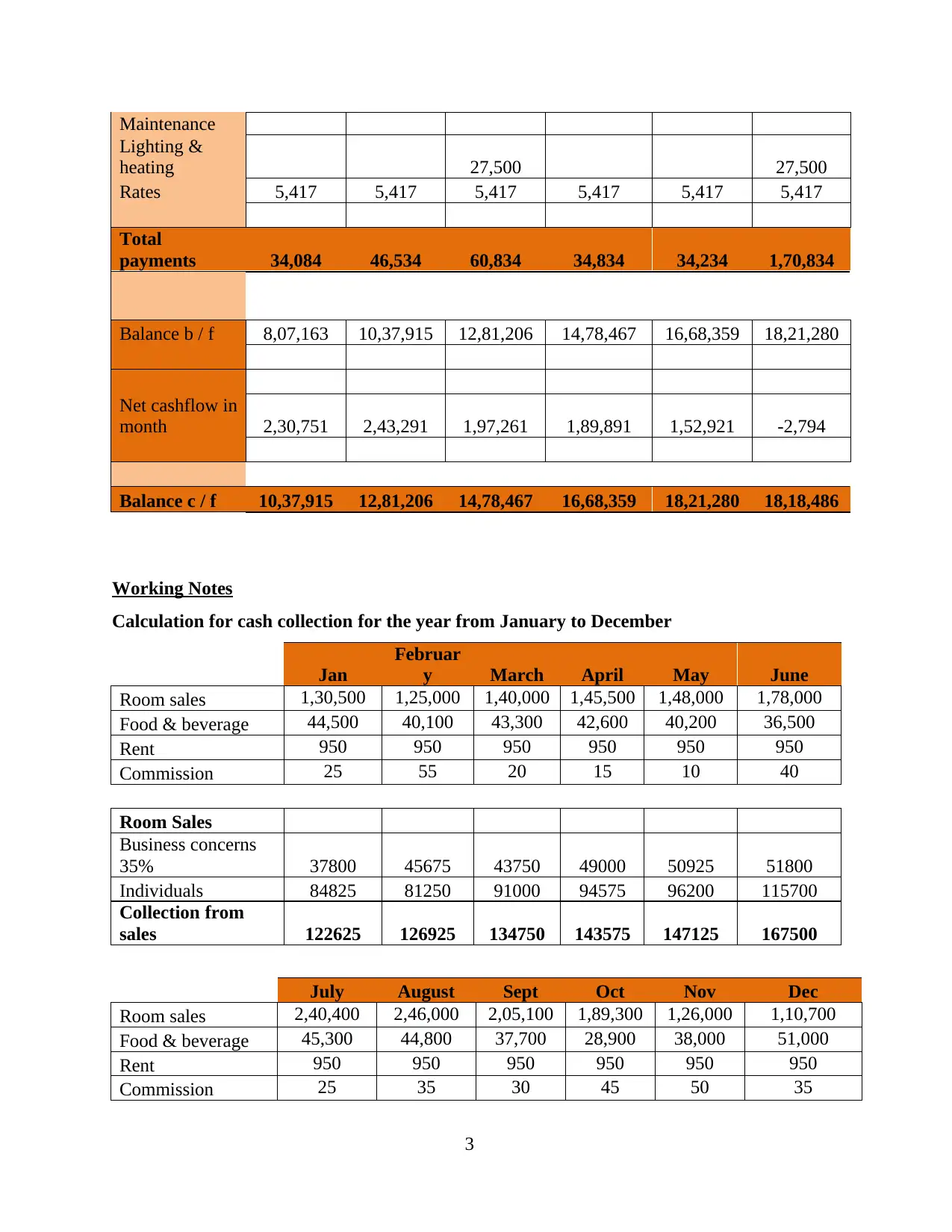

Maintenance

Lighting &

heating 27,500 27,500

Rates 5,417 5,417 5,417 5,417 5,417 5,417

Total

payments 34,084 46,534 60,834 34,834 34,234 1,70,834

Balance b / f 8,07,163 10,37,915 12,81,206 14,78,467 16,68,359 18,21,280

Net cashflow in

month 2,30,751 2,43,291 1,97,261 1,89,891 1,52,921 -2,794

Balance c / f 10,37,915 12,81,206 14,78,467 16,68,359 18,21,280 18,18,486

Working Notes

Calculation for cash collection for the year from January to December

Jan

Februar

y March April May June

Room sales 1,30,500 1,25,000 1,40,000 1,45,500 1,48,000 1,78,000

Food & beverage 44,500 40,100 43,300 42,600 40,200 36,500

Rent 950 950 950 950 950 950

Commission 25 55 20 15 10 40

Room Sales

Business concerns

35% 37800 45675 43750 49000 50925 51800

Individuals 84825 81250 91000 94575 96200 115700

Collection from

sales 122625 126925 134750 143575 147125 167500

July August Sept Oct Nov Dec

Room sales 2,40,400 2,46,000 2,05,100 1,89,300 1,26,000 1,10,700

Food & beverage 45,300 44,800 37,700 28,900 38,000 51,000

Rent 950 950 950 950 950 950

Commission 25 35 30 45 50 35

3

Lighting &

heating 27,500 27,500

Rates 5,417 5,417 5,417 5,417 5,417 5,417

Total

payments 34,084 46,534 60,834 34,834 34,234 1,70,834

Balance b / f 8,07,163 10,37,915 12,81,206 14,78,467 16,68,359 18,21,280

Net cashflow in

month 2,30,751 2,43,291 1,97,261 1,89,891 1,52,921 -2,794

Balance c / f 10,37,915 12,81,206 14,78,467 16,68,359 18,21,280 18,18,486

Working Notes

Calculation for cash collection for the year from January to December

Jan

Februar

y March April May June

Room sales 1,30,500 1,25,000 1,40,000 1,45,500 1,48,000 1,78,000

Food & beverage 44,500 40,100 43,300 42,600 40,200 36,500

Rent 950 950 950 950 950 950

Commission 25 55 20 15 10 40

Room Sales

Business concerns

35% 37800 45675 43750 49000 50925 51800

Individuals 84825 81250 91000 94575 96200 115700

Collection from

sales 122625 126925 134750 143575 147125 167500

July August Sept Oct Nov Dec

Room sales 2,40,400 2,46,000 2,05,100 1,89,300 1,26,000 1,10,700

Food & beverage 45,300 44,800 37,700 28,900 38,000 51,000

Rent 950 950 950 950 950 950

Commission 25 35 30 45 50 35

3

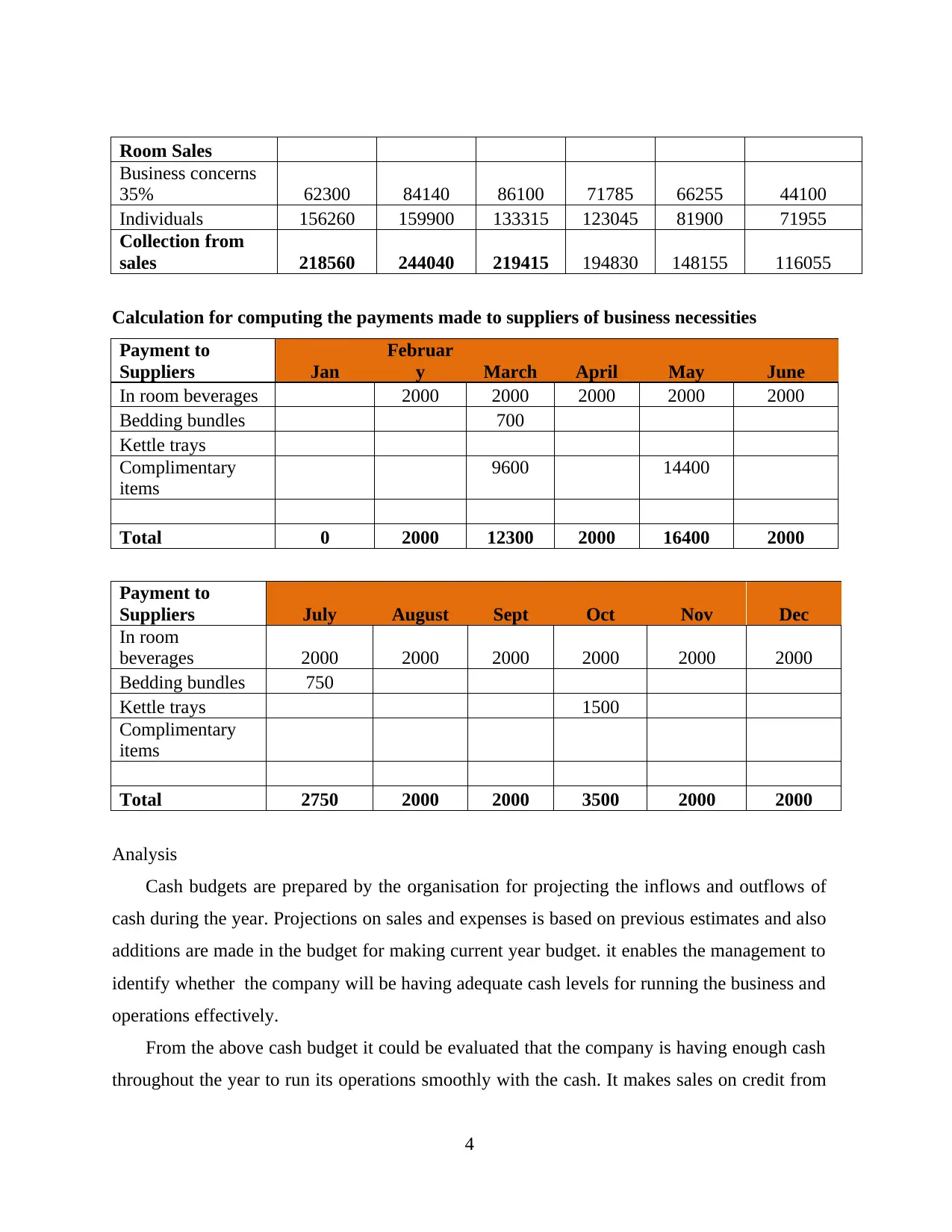

Room Sales

Business concerns

35% 62300 84140 86100 71785 66255 44100

Individuals 156260 159900 133315 123045 81900 71955

Collection from

sales 218560 244040 219415 194830 148155 116055

Calculation for computing the payments made to suppliers of business necessities

Payment to

Suppliers Jan

Februar

y March April May June

In room beverages 2000 2000 2000 2000 2000

Bedding bundles 700

Kettle trays

Complimentary

items

9600 14400

Total 0 2000 12300 2000 16400 2000

Payment to

Suppliers July August Sept Oct Nov Dec

In room

beverages 2000 2000 2000 2000 2000 2000

Bedding bundles 750

Kettle trays 1500

Complimentary

items

Total 2750 2000 2000 3500 2000 2000

Analysis

Cash budgets are prepared by the organisation for projecting the inflows and outflows of

cash during the year. Projections on sales and expenses is based on previous estimates and also

additions are made in the budget for making current year budget. it enables the management to

identify whether the company will be having adequate cash levels for running the business and

operations effectively.

From the above cash budget it could be evaluated that the company is having enough cash

throughout the year to run its operations smoothly with the cash. It makes sales on credit from

4

Business concerns

35% 62300 84140 86100 71785 66255 44100

Individuals 156260 159900 133315 123045 81900 71955

Collection from

sales 218560 244040 219415 194830 148155 116055

Calculation for computing the payments made to suppliers of business necessities

Payment to

Suppliers Jan

Februar

y March April May June

In room beverages 2000 2000 2000 2000 2000

Bedding bundles 700

Kettle trays

Complimentary

items

9600 14400

Total 0 2000 12300 2000 16400 2000

Payment to

Suppliers July August Sept Oct Nov Dec

In room

beverages 2000 2000 2000 2000 2000 2000

Bedding bundles 750

Kettle trays 1500

Complimentary

items

Total 2750 2000 2000 3500 2000 2000

Analysis

Cash budgets are prepared by the organisation for projecting the inflows and outflows of

cash during the year. Projections on sales and expenses is based on previous estimates and also

additions are made in the budget for making current year budget. it enables the management to

identify whether the company will be having adequate cash levels for running the business and

operations effectively.

From the above cash budget it could be evaluated that the company is having enough cash

throughout the year to run its operations smoothly with the cash. It makes sales on credit from

4

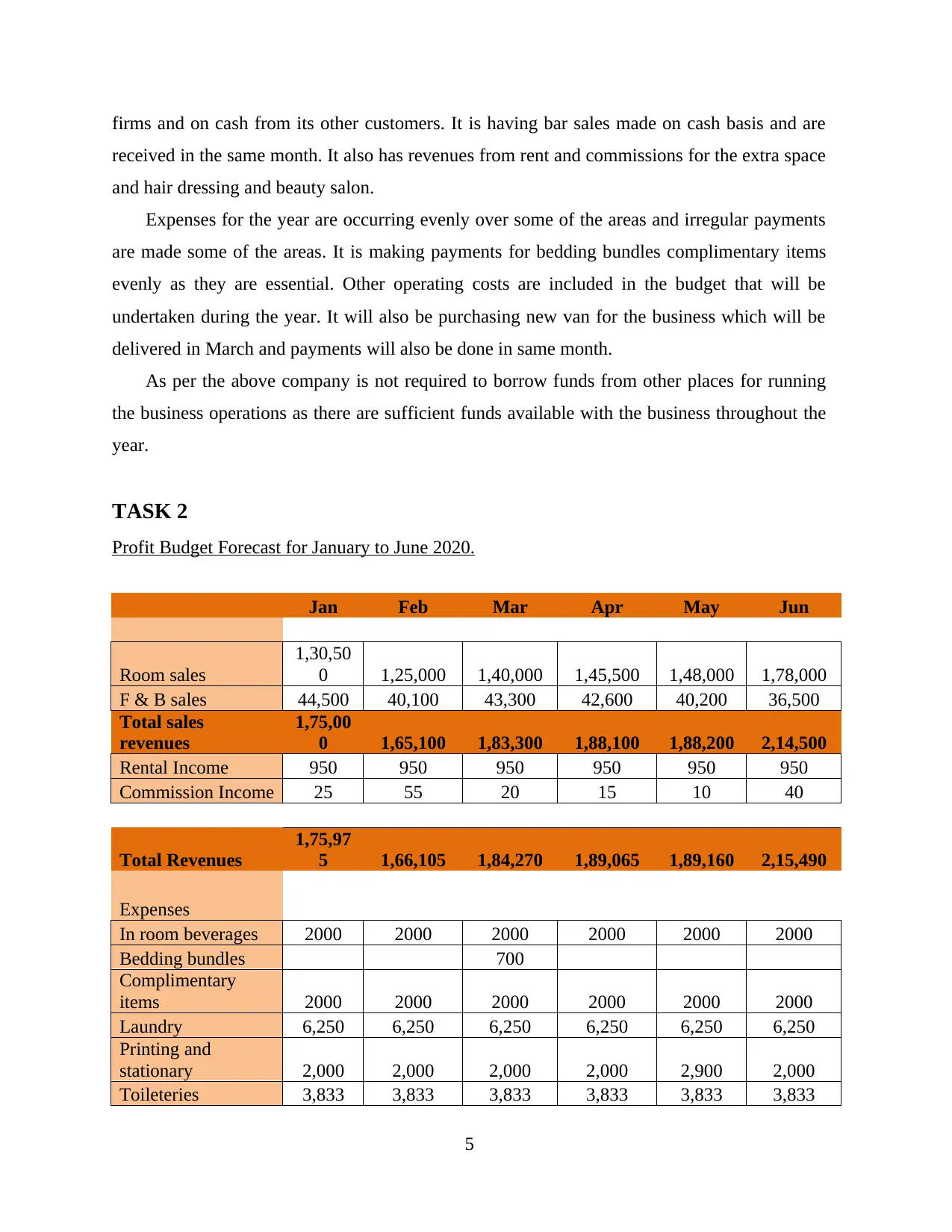

firms and on cash from its other customers. It is having bar sales made on cash basis and are

received in the same month. It also has revenues from rent and commissions for the extra space

and hair dressing and beauty salon.

Expenses for the year are occurring evenly over some of the areas and irregular payments

are made some of the areas. It is making payments for bedding bundles complimentary items

evenly as they are essential. Other operating costs are included in the budget that will be

undertaken during the year. It will also be purchasing new van for the business which will be

delivered in March and payments will also be done in same month.

As per the above company is not required to borrow funds from other places for running

the business operations as there are sufficient funds available with the business throughout the

year.

TASK 2

Profit Budget Forecast for January to June 2020.

Jan Feb Mar Apr May Jun

Room sales

1,30,50

0 1,25,000 1,40,000 1,45,500 1,48,000 1,78,000

F & B sales 44,500 40,100 43,300 42,600 40,200 36,500

Total sales

revenues

1,75,00

0 1,65,100 1,83,300 1,88,100 1,88,200 2,14,500

Rental Income 950 950 950 950 950 950

Commission Income 25 55 20 15 10 40

Total Revenues

1,75,97

5 1,66,105 1,84,270 1,89,065 1,89,160 2,15,490

Expenses

In room beverages 2000 2000 2000 2000 2000 2000

Bedding bundles 700

Complimentary

items 2000 2000 2000 2000 2000 2000

Laundry 6,250 6,250 6,250 6,250 6,250 6,250

Printing and

stationary 2,000 2,000 2,000 2,000 2,900 2,000

Toileteries 3,833 3,833 3,833 3,833 3,833 3,833

5

received in the same month. It also has revenues from rent and commissions for the extra space

and hair dressing and beauty salon.

Expenses for the year are occurring evenly over some of the areas and irregular payments

are made some of the areas. It is making payments for bedding bundles complimentary items

evenly as they are essential. Other operating costs are included in the budget that will be

undertaken during the year. It will also be purchasing new van for the business which will be

delivered in March and payments will also be done in same month.

As per the above company is not required to borrow funds from other places for running

the business operations as there are sufficient funds available with the business throughout the

year.

TASK 2

Profit Budget Forecast for January to June 2020.

Jan Feb Mar Apr May Jun

Room sales

1,30,50

0 1,25,000 1,40,000 1,45,500 1,48,000 1,78,000

F & B sales 44,500 40,100 43,300 42,600 40,200 36,500

Total sales

revenues

1,75,00

0 1,65,100 1,83,300 1,88,100 1,88,200 2,14,500

Rental Income 950 950 950 950 950 950

Commission Income 25 55 20 15 10 40

Total Revenues

1,75,97

5 1,66,105 1,84,270 1,89,065 1,89,160 2,15,490

Expenses

In room beverages 2000 2000 2000 2000 2000 2000

Bedding bundles 700

Complimentary

items 2000 2000 2000 2000 2000 2000

Laundry 6,250 6,250 6,250 6,250 6,250 6,250

Printing and

stationary 2,000 2,000 2,000 2,000 2,900 2,000

Toileteries 3,833 3,833 3,833 3,833 3,833 3,833

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

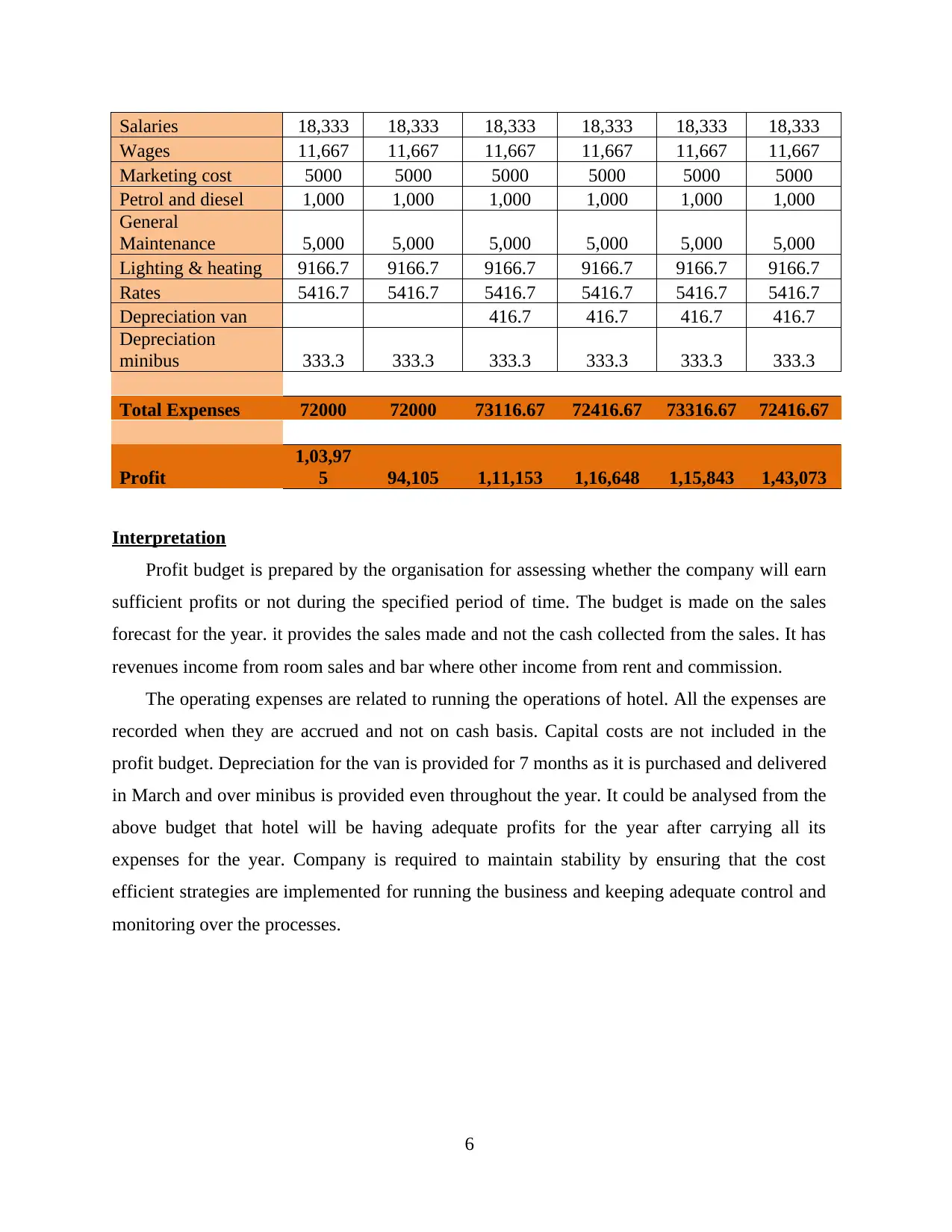

Salaries 18,333 18,333 18,333 18,333 18,333 18,333

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Marketing cost 5000 5000 5000 5000 5000 5000

Petrol and diesel 1,000 1,000 1,000 1,000 1,000 1,000

General

Maintenance 5,000 5,000 5,000 5,000 5,000 5,000

Lighting & heating 9166.7 9166.7 9166.7 9166.7 9166.7 9166.7

Rates 5416.7 5416.7 5416.7 5416.7 5416.7 5416.7

Depreciation van 416.7 416.7 416.7 416.7

Depreciation

minibus 333.3 333.3 333.3 333.3 333.3 333.3

Total Expenses 72000 72000 73116.67 72416.67 73316.67 72416.67

Profit

1,03,97

5 94,105 1,11,153 1,16,648 1,15,843 1,43,073

Interpretation

Profit budget is prepared by the organisation for assessing whether the company will earn

sufficient profits or not during the specified period of time. The budget is made on the sales

forecast for the year. it provides the sales made and not the cash collected from the sales. It has

revenues income from room sales and bar where other income from rent and commission.

The operating expenses are related to running the operations of hotel. All the expenses are

recorded when they are accrued and not on cash basis. Capital costs are not included in the

profit budget. Depreciation for the van is provided for 7 months as it is purchased and delivered

in March and over minibus is provided even throughout the year. It could be analysed from the

above budget that hotel will be having adequate profits for the year after carrying all its

expenses for the year. Company is required to maintain stability by ensuring that the cost

efficient strategies are implemented for running the business and keeping adequate control and

monitoring over the processes.

6

Wages 11,667 11,667 11,667 11,667 11,667 11,667

Marketing cost 5000 5000 5000 5000 5000 5000

Petrol and diesel 1,000 1,000 1,000 1,000 1,000 1,000

General

Maintenance 5,000 5,000 5,000 5,000 5,000 5,000

Lighting & heating 9166.7 9166.7 9166.7 9166.7 9166.7 9166.7

Rates 5416.7 5416.7 5416.7 5416.7 5416.7 5416.7

Depreciation van 416.7 416.7 416.7 416.7

Depreciation

minibus 333.3 333.3 333.3 333.3 333.3 333.3

Total Expenses 72000 72000 73116.67 72416.67 73316.67 72416.67

Profit

1,03,97

5 94,105 1,11,153 1,16,648 1,15,843 1,43,073

Interpretation

Profit budget is prepared by the organisation for assessing whether the company will earn

sufficient profits or not during the specified period of time. The budget is made on the sales

forecast for the year. it provides the sales made and not the cash collected from the sales. It has

revenues income from room sales and bar where other income from rent and commission.

The operating expenses are related to running the operations of hotel. All the expenses are

recorded when they are accrued and not on cash basis. Capital costs are not included in the

profit budget. Depreciation for the van is provided for 7 months as it is purchased and delivered

in March and over minibus is provided even throughout the year. It could be analysed from the

above budget that hotel will be having adequate profits for the year after carrying all its

expenses for the year. Company is required to maintain stability by ensuring that the cost

efficient strategies are implemented for running the business and keeping adequate control and

monitoring over the processes.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.