Financial Management: Costing, Budgeting and Variance Analysis

VerifiedAdded on 2022/12/28

|12

|2225

|1

Report

AI Summary

This financial management report analyzes various costing methods, including absorption costing and activity-based costing, to determine product profitability for lip gloss, lipstick, and lip balm. It compares the results of both methods, highlighting the impact of overhead allocation on profit margins. The report further explores variance analysis, calculating material usage, mix, and yield variances to assess production efficiency. Additionally, it examines zero-based budgeting and incremental budgeting approaches, outlining their merits and demerits. Finally, the report discusses the role of sensitivity analysis in managing uncertainties and its importance in evaluating the impact of changing variables on a company's financial performance, such as in cost-volume-profit analysis.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY...................................................................................................................................3

Q.1................................................................................................................................................3

Q.2................................................................................................................................................6

Q.3................................................................................................................................................8

REFERENCES................................................................................................................................1

MAIN BODY...................................................................................................................................3

Q.1................................................................................................................................................3

Q.2................................................................................................................................................6

Q.3................................................................................................................................................8

REFERENCES................................................................................................................................1

MAIN BODY

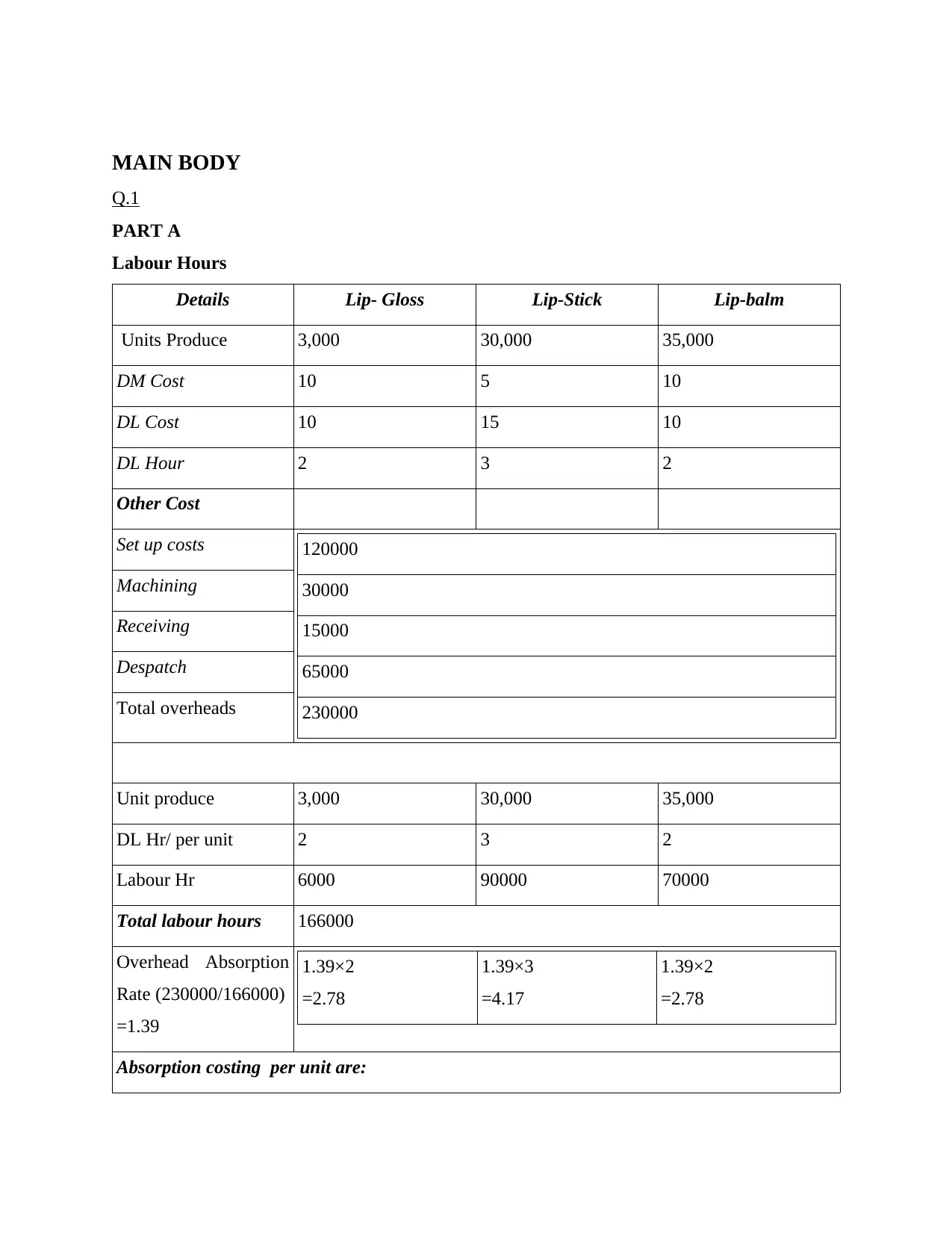

Q.1

PART A

Labour Hours

Details Lip- Gloss Lip-Stick Lip-balm

Units Produce 3,000 30,000 35,000

DM Cost 10 5 10

DL Cost 10 15 10

DL Hour 2 3 2

Other Cost

Set up costs 120000

30000

15000

65000

230000

Machining

Receiving

Despatch

Total overheads

Unit produce 3,000 30,000 35,000

DL Hr/ per unit 2 3 2

Labour Hr 6000 90000 70000

Total labour hours 166000

Overhead Absorption

Rate (230000/166000)

=1.39

1.39×2

=2.78

1.39×3

=4.17

1.39×2

=2.78

Absorption costing per unit are:

Q.1

PART A

Labour Hours

Details Lip- Gloss Lip-Stick Lip-balm

Units Produce 3,000 30,000 35,000

DM Cost 10 5 10

DL Cost 10 15 10

DL Hour 2 3 2

Other Cost

Set up costs 120000

30000

15000

65000

230000

Machining

Receiving

Despatch

Total overheads

Unit produce 3,000 30,000 35,000

DL Hr/ per unit 2 3 2

Labour Hr 6000 90000 70000

Total labour hours 166000

Overhead Absorption

Rate (230000/166000)

=1.39

1.39×2

=2.78

1.39×3

=4.17

1.39×2

=2.78

Absorption costing per unit are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

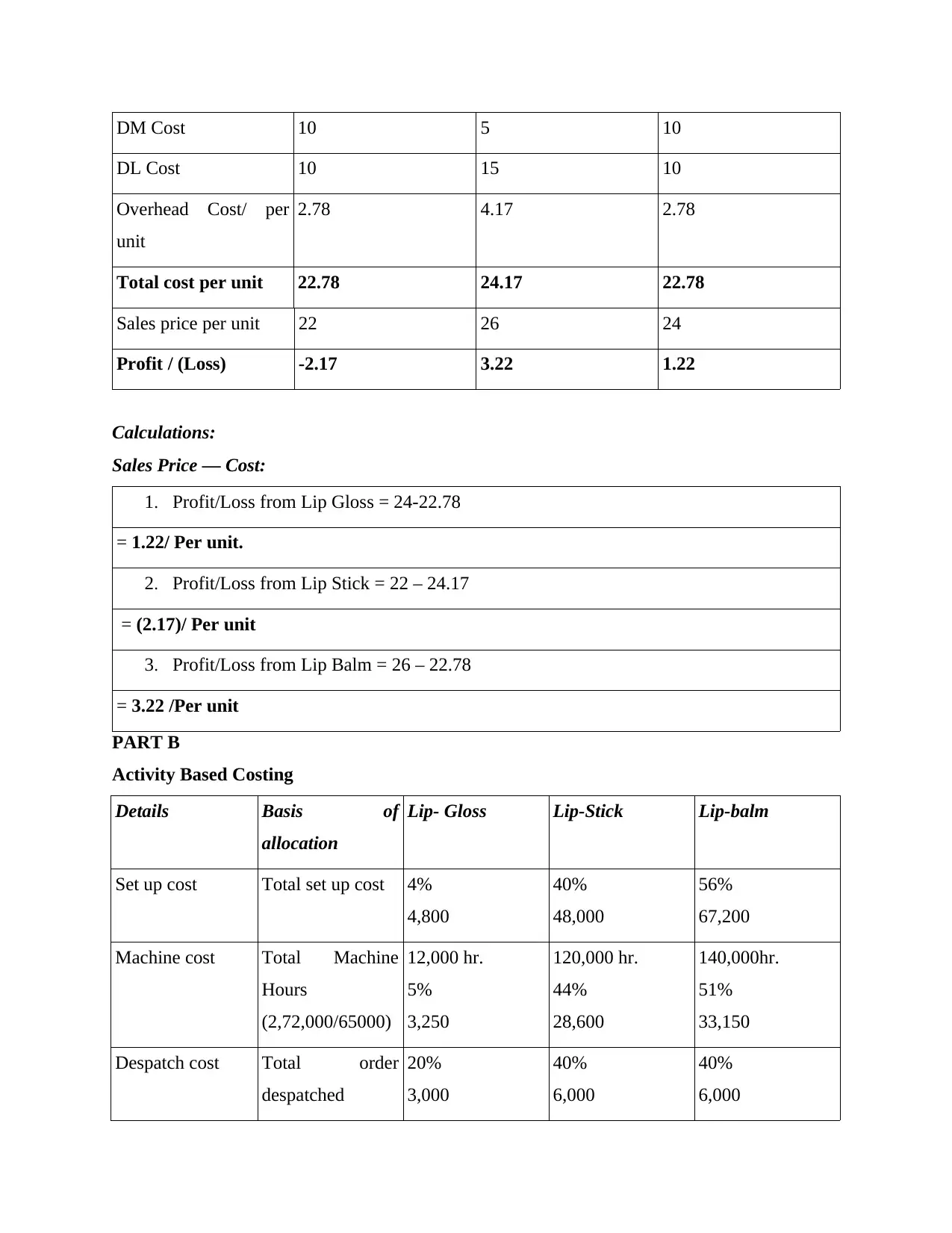

DM Cost 10 5 10

DL Cost 10 15 10

Overhead Cost/ per

unit

2.78 4.17 2.78

Total cost per unit 22.78 24.17 22.78

Sales price per unit 22 26 24

Profit / (Loss) -2.17 3.22 1.22

Calculations:

Sales Price — Cost:

1. Profit/Loss from Lip Gloss = 24-22.78

= 1.22/ Per unit.

2. Profit/Loss from Lip Stick = 22 – 24.17

= (2.17)/ Per unit

3. Profit/Loss from Lip Balm = 26 – 22.78

= 3.22 /Per unit

PART B

Activity Based Costing

Details Basis of

allocation

Lip- Gloss Lip-Stick Lip-balm

Set up cost Total set up cost 4%

4,800

40%

48,000

56%

67,200

Machine cost Total Machine

Hours

(2,72,000/65000)

12,000 hr.

5%

3,250

120,000 hr.

44%

28,600

140,000hr.

51%

33,150

Despatch cost Total order

despatched

20%

3,000

40%

6,000

40%

6,000

DL Cost 10 15 10

Overhead Cost/ per

unit

2.78 4.17 2.78

Total cost per unit 22.78 24.17 22.78

Sales price per unit 22 26 24

Profit / (Loss) -2.17 3.22 1.22

Calculations:

Sales Price — Cost:

1. Profit/Loss from Lip Gloss = 24-22.78

= 1.22/ Per unit.

2. Profit/Loss from Lip Stick = 22 – 24.17

= (2.17)/ Per unit

3. Profit/Loss from Lip Balm = 26 – 22.78

= 3.22 /Per unit

PART B

Activity Based Costing

Details Basis of

allocation

Lip- Gloss Lip-Stick Lip-balm

Set up cost Total set up cost 4%

4,800

40%

48,000

56%

67,200

Machine cost Total Machine

Hours

(2,72,000/65000)

12,000 hr.

5%

3,250

120,000 hr.

44%

28,600

140,000hr.

51%

33,150

Despatch cost Total order

despatched

20%

3,000

40%

6,000

40%

6,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

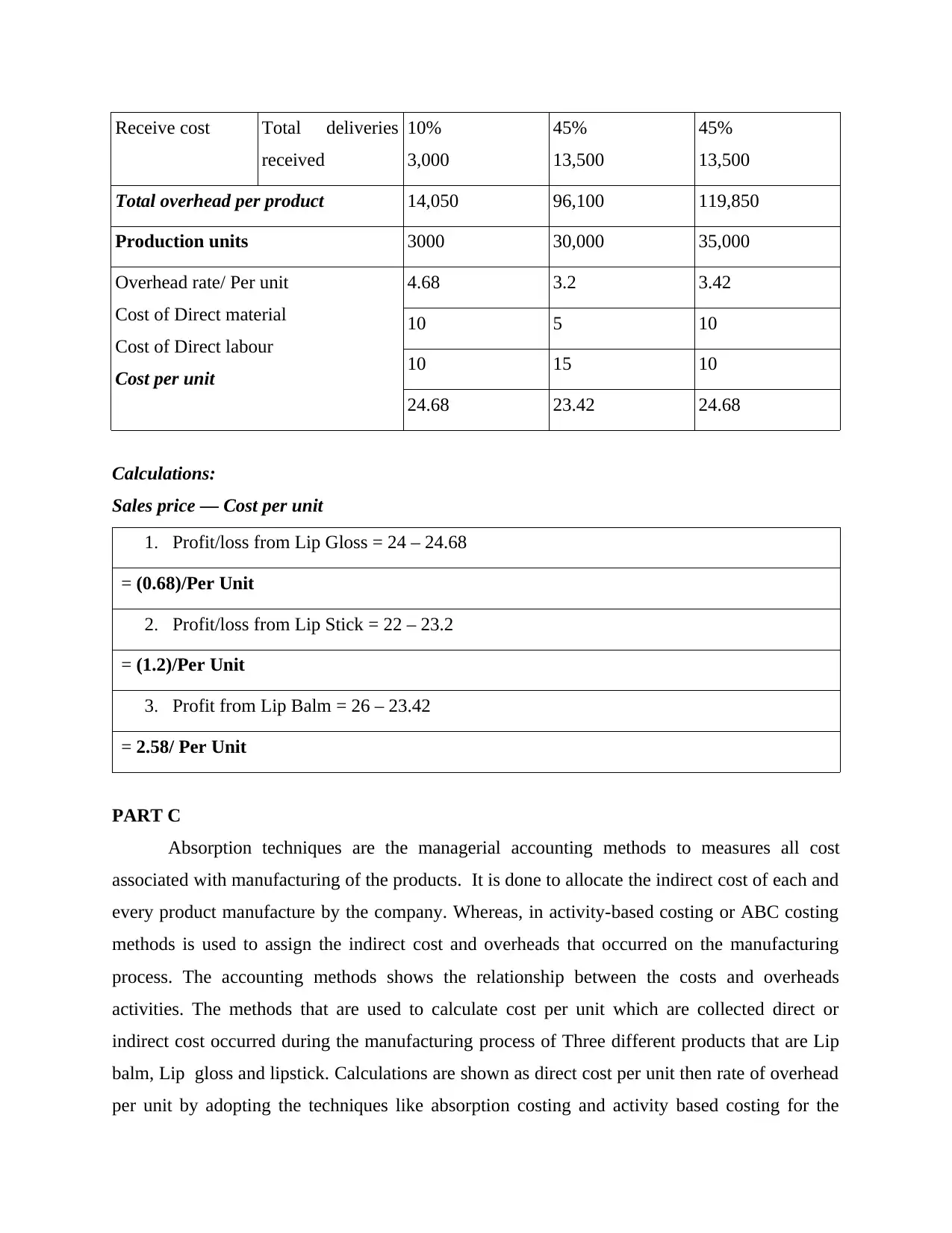

Receive cost Total deliveries

received

10%

3,000

45%

13,500

45%

13,500

Total overhead per product 14,050 96,100 119,850

Production units 3000 30,000 35,000

Overhead rate/ Per unit

Cost of Direct material

Cost of Direct labour

Cost per unit

4.68 3.2 3.42

10 5 10

10 15 10

24.68 23.42 24.68

Calculations:

Sales price — Cost per unit

1. Profit/loss from Lip Gloss = 24 – 24.68

= (0.68)/Per Unit

2. Profit/loss from Lip Stick = 22 – 23.2

= (1.2)/Per Unit

3. Profit from Lip Balm = 26 – 23.42

= 2.58/ Per Unit

PART C

Absorption techniques are the managerial accounting methods to measures all cost

associated with manufacturing of the products. It is done to allocate the indirect cost of each and

every product manufacture by the company. Whereas, in activity-based costing or ABC costing

methods is used to assign the indirect cost and overheads that occurred on the manufacturing

process. The accounting methods shows the relationship between the costs and overheads

activities. The methods that are used to calculate cost per unit which are collected direct or

indirect cost occurred during the manufacturing process of Three different products that are Lip

balm, Lip gloss and lipstick. Calculations are shown as direct cost per unit then rate of overhead

per unit by adopting the techniques like absorption costing and activity based costing for the

received

10%

3,000

45%

13,500

45%

13,500

Total overhead per product 14,050 96,100 119,850

Production units 3000 30,000 35,000

Overhead rate/ Per unit

Cost of Direct material

Cost of Direct labour

Cost per unit

4.68 3.2 3.42

10 5 10

10 15 10

24.68 23.42 24.68

Calculations:

Sales price — Cost per unit

1. Profit/loss from Lip Gloss = 24 – 24.68

= (0.68)/Per Unit

2. Profit/loss from Lip Stick = 22 – 23.2

= (1.2)/Per Unit

3. Profit from Lip Balm = 26 – 23.42

= 2.58/ Per Unit

PART C

Absorption techniques are the managerial accounting methods to measures all cost

associated with manufacturing of the products. It is done to allocate the indirect cost of each and

every product manufacture by the company. Whereas, in activity-based costing or ABC costing

methods is used to assign the indirect cost and overheads that occurred on the manufacturing

process. The accounting methods shows the relationship between the costs and overheads

activities. The methods that are used to calculate cost per unit which are collected direct or

indirect cost occurred during the manufacturing process of Three different products that are Lip

balm, Lip gloss and lipstick. Calculations are shown as direct cost per unit then rate of overhead

per unit by adopting the techniques like absorption costing and activity based costing for the

calculation. On the basis of labour hours worked for production, we have analysed that by using

the absorption costing, it is been seen that the firm is earning quite good profit margin where all

the cost of overheads are divided in the three products (Akeem, L.B., 2017).

On the other hand, through activity based costing the profit margin had shown in only in

one product Lip Balm, while other two products lip gloss and lipstick are shown in loss with 0.68

and 1.2 per unit receptively. By using absorption costing technique, all direct cost are collected

and then divide the indirect cost on the basis of allocation relevant to each other. Hence, by

going with profitability factor, absorption costing techniques must be used by the company. But

if company need to know the activity performed without minimizing the cost related to each

activity in order to reduce the cost per unit, activity based costing must be selected to analysis the

cost. However, the difference can be seen in the Lip gloss where, By absorption costing it shows

the profit of 1.22 per unit whereas in the activity based costing It can be seen that Lip Gloss

found in loss by (0.68) per unit due to over costing and under costing of the product.

PART D

Role of sensitive analysis to cop up with uncertainties:

Sensitive analysis is the tool used in accounting to help the management of the

organization to analysis the situations related to what if arises to company. Sensitive analysis

help to analyse uncertainty in the mathematical (Bariska, M., Pásztory, Z. and Koloszár, L.,

2019). The technique is used for the specific boundaries that are depended on the one or more

input variables. It helps manager to know the company operating income changes in case of

prediction is correct or not. The manager predicts on the selling price, variable cost, fixed cost

and variable of cost, volume of sales are calculated in order to measure the break even point of

the company goods and services. The sensitive analysis also helps the company to analysis the

what-if situation to develop the internals and external management of the company.

Margin of safety is the point to protect the business from decreasing before fixed cost

incurred. Margin of safety is very important component part for sensitive analysis as it measure

the level of risk. At above break even point all sales are considered as a Margin of safety.

However, it helps company to know the fixed cost of the company and not remain constant and

affect the Margin safety. The affect of cost volume profit analysis and help manager to know the

cost structure of the company. Also, it helps to know the relation between fixed cost and variable

cost of the company and also include operating leverage into sensitive analysis to measure the

the absorption costing, it is been seen that the firm is earning quite good profit margin where all

the cost of overheads are divided in the three products (Akeem, L.B., 2017).

On the other hand, through activity based costing the profit margin had shown in only in

one product Lip Balm, while other two products lip gloss and lipstick are shown in loss with 0.68

and 1.2 per unit receptively. By using absorption costing technique, all direct cost are collected

and then divide the indirect cost on the basis of allocation relevant to each other. Hence, by

going with profitability factor, absorption costing techniques must be used by the company. But

if company need to know the activity performed without minimizing the cost related to each

activity in order to reduce the cost per unit, activity based costing must be selected to analysis the

cost. However, the difference can be seen in the Lip gloss where, By absorption costing it shows

the profit of 1.22 per unit whereas in the activity based costing It can be seen that Lip Gloss

found in loss by (0.68) per unit due to over costing and under costing of the product.

PART D

Role of sensitive analysis to cop up with uncertainties:

Sensitive analysis is the tool used in accounting to help the management of the

organization to analysis the situations related to what if arises to company. Sensitive analysis

help to analyse uncertainty in the mathematical (Bariska, M., Pásztory, Z. and Koloszár, L.,

2019). The technique is used for the specific boundaries that are depended on the one or more

input variables. It helps manager to know the company operating income changes in case of

prediction is correct or not. The manager predicts on the selling price, variable cost, fixed cost

and variable of cost, volume of sales are calculated in order to measure the break even point of

the company goods and services. The sensitive analysis also helps the company to analysis the

what-if situation to develop the internals and external management of the company.

Margin of safety is the point to protect the business from decreasing before fixed cost

incurred. Margin of safety is very important component part for sensitive analysis as it measure

the level of risk. At above break even point all sales are considered as a Margin of safety.

However, it helps company to know the fixed cost of the company and not remain constant and

affect the Margin safety. The affect of cost volume profit analysis and help manager to know the

cost structure of the company. Also, it helps to know the relation between fixed cost and variable

cost of the company and also include operating leverage into sensitive analysis to measure the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

impact of cost structure on company's profit (alagatti, V.D., 2020). It helps Manager to interpret

the performance of the company.

Q.2

PART 1

Material usage variance

Standard Quality:

(Standard quality-actual quality)×standard price /per unit

Omega Standard quantity Total producing = 4600 kg

Alpha = 40 / 100 × 4600 = 1840

Beta = 60 / 100 × 4600 = 2760

Gamma = 20 / 100 ×4600 = 920

Alpha

Standard Actual

(46 × 40)

=1840

(1840-

2200)×2

=-720

Beta

Standard Actual

(46 × 60)

= 2760

(2760 –

2500) ×5

=1300

Gama

Standard Actual

(46 × 20)

= 920

(920 –

920) × 1

=0

In Total

=1300-720

=580 F

Material mix variance.

(Revised Standard Quantity — Actual Quantity) * Standard price

Revised Standard Quantity of Alpha = 40 / 120 × 5620

= 1873.33

Revised Standard Quantity of Beta = 60 / 120 × 5620

= 2810

Revised Standard quantity of gamma = 20 / 120 × 5620

= 936.67

Details Revised

Standard

Quantity

Actual

Quantity

Quantitative

difference

Standard

Rate/kg

Variances

the performance of the company.

Q.2

PART 1

Material usage variance

Standard Quality:

(Standard quality-actual quality)×standard price /per unit

Omega Standard quantity Total producing = 4600 kg

Alpha = 40 / 100 × 4600 = 1840

Beta = 60 / 100 × 4600 = 2760

Gamma = 20 / 100 ×4600 = 920

Alpha

Standard Actual

(46 × 40)

=1840

(1840-

2200)×2

=-720

Beta

Standard Actual

(46 × 60)

= 2760

(2760 –

2500) ×5

=1300

Gama

Standard Actual

(46 × 20)

= 920

(920 –

920) × 1

=0

In Total

=1300-720

=580 F

Material mix variance.

(Revised Standard Quantity — Actual Quantity) * Standard price

Revised Standard Quantity of Alpha = 40 / 120 × 5620

= 1873.33

Revised Standard Quantity of Beta = 60 / 120 × 5620

= 2810

Revised Standard quantity of gamma = 20 / 120 × 5620

= 936.67

Details Revised

Standard

Quantity

Actual

Quantity

Quantitative

difference

Standard

Rate/kg

Variances

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alpha 1873.33 2200 326.67 (A) 2 653.34 (A)

Beta 2810 2500 310 (F) 5 1550 (F)

Gama 936.67 920 16.67(F) 1 16.67 (F)

Total 5620 5620 913.33 (F)

Total material yield variance.

(Standard Quantity — Revised Standard Quantity)× Standard Price

Particulars Standard

Quantity

Revised

Standard

Quantity

Quantitative

Difference

Standard

Rate/kg

Variance

Alpha 1840 1873.33 33.33 (A) 2 66.66 (A)

Beta 2760 2810 50 (A) 5 250 (A)

Gamma 920 936.67 16.67 (A) 1 16.67 (A)

Total 5520 5620 333.33 (A)

PART 2

Standard costing is a practise of substitute cost of expected cost for an actual cost in the

accounting records. It is a difference between expected and actual cost (Fliedner, G., 2018).

The report of raw material price variance are mostly out of control of production manager

control and more of Purchasing manager are responsible. Here production manager had no

involvement of setting standard mix. Production manager had no appearance in the planning

variance. Quality and price of materials are volatile using before price and usage standard and

provide contorted view of yield and mix variance. Decreasing in non isolated planning variance

are demotivated.

The standard mix of product are not changed in five-year instead of change in price and

quality of products. It helps production manager to control action on variance calculated from

standard. However, kappa company is not accessing the required importance towards the various

variance occurred. It leads to production manager over sighting the higher cost incurred which

Beta 2810 2500 310 (F) 5 1550 (F)

Gama 936.67 920 16.67(F) 1 16.67 (F)

Total 5620 5620 913.33 (F)

Total material yield variance.

(Standard Quantity — Revised Standard Quantity)× Standard Price

Particulars Standard

Quantity

Revised

Standard

Quantity

Quantitative

Difference

Standard

Rate/kg

Variance

Alpha 1840 1873.33 33.33 (A) 2 66.66 (A)

Beta 2760 2810 50 (A) 5 250 (A)

Gamma 920 936.67 16.67 (A) 1 16.67 (A)

Total 5520 5620 333.33 (A)

PART 2

Standard costing is a practise of substitute cost of expected cost for an actual cost in the

accounting records. It is a difference between expected and actual cost (Fliedner, G., 2018).

The report of raw material price variance are mostly out of control of production manager

control and more of Purchasing manager are responsible. Here production manager had no

involvement of setting standard mix. Production manager had no appearance in the planning

variance. Quality and price of materials are volatile using before price and usage standard and

provide contorted view of yield and mix variance. Decreasing in non isolated planning variance

are demotivated.

The standard mix of product are not changed in five-year instead of change in price and

quality of products. It helps production manager to control action on variance calculated from

standard. However, kappa company is not accessing the required importance towards the various

variance occurred. It leads to production manager over sighting the higher cost incurred which

was not healthy towards the performance of kappa co. The manager will not be motivated

towards control in cost to satisfy and affect the company adversely. In the above calculations the

overall usage of variance shows at 580 favourable which show the good performance of the

company. If, the usage of variance is taken in more details through yield and mix variance, it

seen that mix had been changed. It shows the direct relationship between the material mix and

material yield variance by applying mix material which is different from standard.

Q.3

Zero based budgeting is applied from the zero level i.e. from scratch. It is the method

where expenses are need to be justified for new period. The starting of the process is done

through zero based and every function is analysed for need and cost. The previous year revenue

is assumed to be zero and compute the cost which are included in the all products to know the

cost involved. Incremental Budgeting refers to incremental increases occurred on the previous

budgets with increase in spending (Wegmann, G., 2019). This budget analysis only new

expenditure and budget is prepared on the basis of actual performance of the company.

Zero based budgeting also had merit and demerit in the methods:

Merits

The incremental budgeting is useful because it promotes the accuracy to estimate forecast

and help to solve grievances of different departments of require funds.

The method is rigid which help management to make the friendly budget and strict

guidelines to address. The line approach is a long process but help to assess in current

demand of product for their budgets (Hughes, P., 2020). It helps company to spend on product category wise which gives good return.

Demerits

Zero based budgeting is subjective in nature to calculate each expense while it is not easy

to calculate each one of them. This approach may help in short run only and cannot be

taken for long run by the company.

There is a rigidity in the budget where it makes company to stick on the one budget for

longer period. Also, incremental budgeting allow company to change only few changes

with the changing situation (brahim, M.M., 2019).

towards control in cost to satisfy and affect the company adversely. In the above calculations the

overall usage of variance shows at 580 favourable which show the good performance of the

company. If, the usage of variance is taken in more details through yield and mix variance, it

seen that mix had been changed. It shows the direct relationship between the material mix and

material yield variance by applying mix material which is different from standard.

Q.3

Zero based budgeting is applied from the zero level i.e. from scratch. It is the method

where expenses are need to be justified for new period. The starting of the process is done

through zero based and every function is analysed for need and cost. The previous year revenue

is assumed to be zero and compute the cost which are included in the all products to know the

cost involved. Incremental Budgeting refers to incremental increases occurred on the previous

budgets with increase in spending (Wegmann, G., 2019). This budget analysis only new

expenditure and budget is prepared on the basis of actual performance of the company.

Zero based budgeting also had merit and demerit in the methods:

Merits

The incremental budgeting is useful because it promotes the accuracy to estimate forecast

and help to solve grievances of different departments of require funds.

The method is rigid which help management to make the friendly budget and strict

guidelines to address. The line approach is a long process but help to assess in current

demand of product for their budgets (Hughes, P., 2020). It helps company to spend on product category wise which gives good return.

Demerits

Zero based budgeting is subjective in nature to calculate each expense while it is not easy

to calculate each one of them. This approach may help in short run only and cannot be

taken for long run by the company.

There is a rigidity in the budget where it makes company to stick on the one budget for

longer period. Also, incremental budgeting allow company to change only few changes

with the changing situation (brahim, M.M., 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Zero based budgeting is long and time-consuming process as every line of various

product category are been assessed and incremental budgeting does not calculate

complex calculations.

It is been required of managerial training for zero based budgeting implementation and it

takes time and cost of company. The staff is need to be trained to use these methods.

Traditional budget cannot consider the changing market factors and does not take future

change which may occurred.

product category are been assessed and incremental budgeting does not calculate

complex calculations.

It is been required of managerial training for zero based budgeting implementation and it

takes time and cost of company. The staff is need to be trained to use these methods.

Traditional budget cannot consider the changing market factors and does not take future

change which may occurred.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Akeem, L.B., 2017. Effect of cost control and cost reduction techniques in organizational

performance. International business and management. 14(3). pp.19-26.

Bariska, M., Pásztory, Z. and Koloszár, L., 2019. The Efficiency Based Costing Method–Using a

Sawmill as Example. EUROPEAN RESEARCH STUDIES: AN INTERNATIONAL

MULTIDISCIPLINARY JOURNAL WITH TOPICS IN EUROPEAN INTEGRATION. 22(2),

pp.229-243.

Fliedner, G., 2018. Lean Accounting: Current State and Future Needs Assessment. Journal of

Accounting & Finance (2158-3625). 18(3).

Hughes, P., 2020. Discover the power of zero-based budgeting. Farmer’s Weekly, 2020(20032),

pp.30-30.

Ibrahim, M.M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Malagatti, V.D., 2020. Costing for the Service Industry. Cambridge Scholars Publishing.

Wegmann, G., 2019. A typology of cost accounting practices based on Activity-Based Costing-a

strategic cost management approach. Asia-Pacific Management Accounting Journal. 14. pp.161-

184.

Online

[Online]. Available through: <>

1

Books and journals

Akeem, L.B., 2017. Effect of cost control and cost reduction techniques in organizational

performance. International business and management. 14(3). pp.19-26.

Bariska, M., Pásztory, Z. and Koloszár, L., 2019. The Efficiency Based Costing Method–Using a

Sawmill as Example. EUROPEAN RESEARCH STUDIES: AN INTERNATIONAL

MULTIDISCIPLINARY JOURNAL WITH TOPICS IN EUROPEAN INTEGRATION. 22(2),

pp.229-243.

Fliedner, G., 2018. Lean Accounting: Current State and Future Needs Assessment. Journal of

Accounting & Finance (2158-3625). 18(3).

Hughes, P., 2020. Discover the power of zero-based budgeting. Farmer’s Weekly, 2020(20032),

pp.30-30.

Ibrahim, M.M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Malagatti, V.D., 2020. Costing for the Service Industry. Cambridge Scholars Publishing.

Wegmann, G., 2019. A typology of cost accounting practices based on Activity-Based Costing-a

strategic cost management approach. Asia-Pacific Management Accounting Journal. 14. pp.161-

184.

Online

[Online]. Available through: <>

1

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.