Financial Management Report: Investment Appraisal and WACC Analysis

VerifiedAdded on 2023/01/12

|19

|4149

|46

Report

AI Summary

This financial management report analyzes Kadlex Plc's financial performance, focusing on the computation of market and book value cost of capital (WACC), and the impact of capital structure adjustments. It delves into investment appraisal techniques, including payback period, ARR, NPV, and IRR, evaluating their benefits and limitations. The report also examines the effects of short-termism on agency problems and bankruptcy, providing a comprehensive overview of financial management principles. The report concludes with an in-depth analysis of WACC minimization through sensible gearing and capital structure integration, offering valuable insights for financial decision-making. The student assignment offers detailed calculations and discussions on the application of various financial concepts and techniques.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

a. Computation of market and book value cost of capital.......................................................................3

b. Recalculation of cost of capital of company........................................................................................6

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible level of

gearing in to the capital structure...........................................................................................................7

d. Effects of short-termism on agency problem and bankruptcy.............................................................7

QUESTION 3.................................................................................................................................................8

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV and IRR

.................................................................................................................................................................8

B. Limitations and benefits of different investment appraisal techniques............................................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

a. Computation of market and book value cost of capital.......................................................................3

b. Recalculation of cost of capital of company........................................................................................6

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible level of

gearing in to the capital structure...........................................................................................................7

d. Effects of short-termism on agency problem and bankruptcy.............................................................7

QUESTION 3.................................................................................................................................................8

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV and IRR

.................................................................................................................................................................8

B. Limitations and benefits of different investment appraisal techniques............................................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

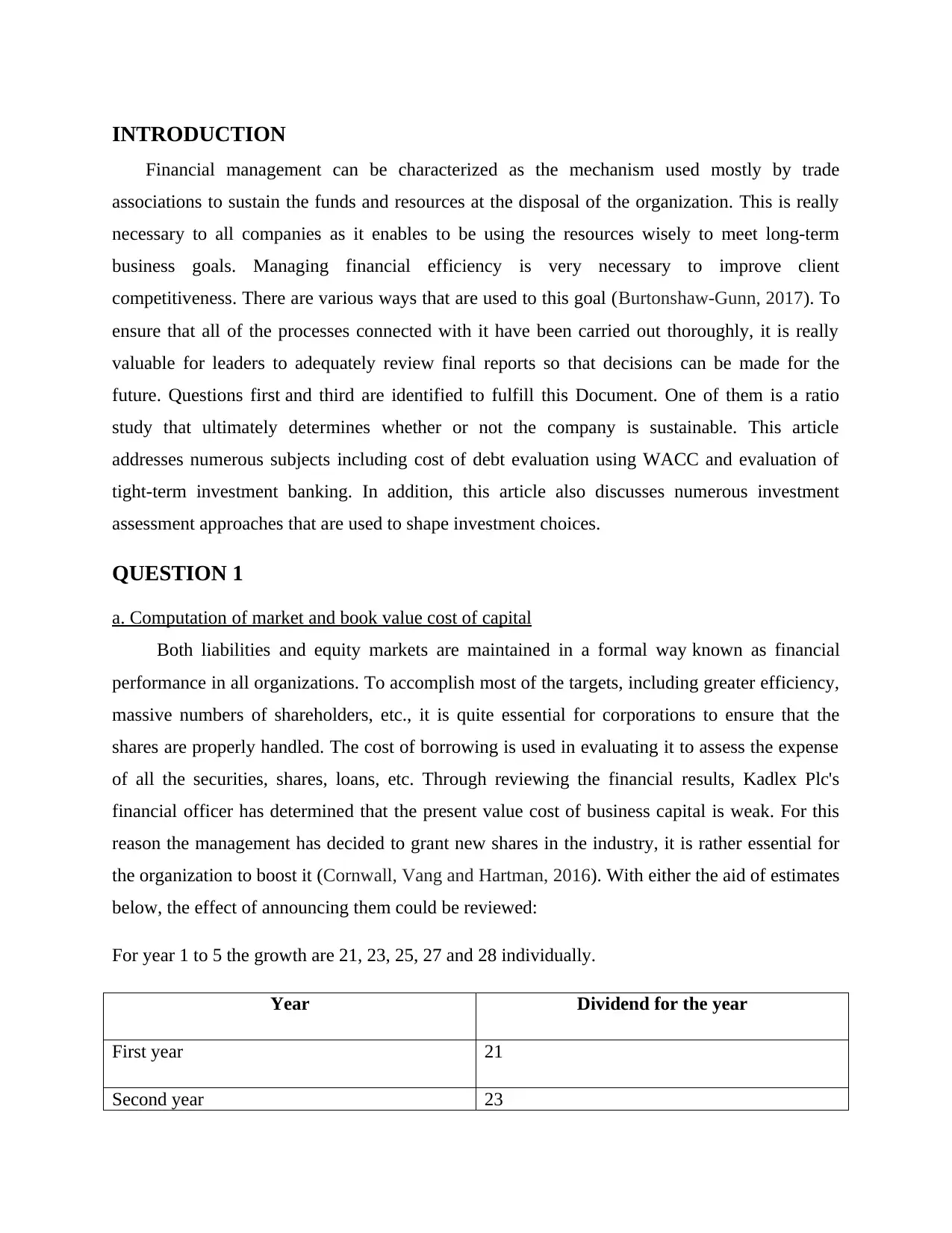

INTRODUCTION

Financial management can be characterized as the mechanism used mostly by trade

associations to sustain the funds and resources at the disposal of the organization. This is really

necessary to all companies as it enables to be using the resources wisely to meet long-term

business goals. Managing financial efficiency is very necessary to improve client

competitiveness. There are various ways that are used to this goal (Burtonshaw-Gunn, 2017). To

ensure that all of the processes connected with it have been carried out thoroughly, it is really

valuable for leaders to adequately review final reports so that decisions can be made for the

future. Questions first and third are identified to fulfill this Document. One of them is a ratio

study that ultimately determines whether or not the company is sustainable. This article

addresses numerous subjects including cost of debt evaluation using WACC and evaluation of

tight-term investment banking. In addition, this article also discusses numerous investment

assessment approaches that are used to shape investment choices.

QUESTION 1

a. Computation of market and book value cost of capital

Both liabilities and equity markets are maintained in a formal way known as financial

performance in all organizations. To accomplish most of the targets, including greater efficiency,

massive numbers of shareholders, etc., it is quite essential for corporations to ensure that the

shares are properly handled. The cost of borrowing is used in evaluating it to assess the expense

of all the securities, shares, loans, etc. Through reviewing the financial results, Kadlex Plc's

financial officer has determined that the present value cost of business capital is weak. For this

reason the management has decided to grant new shares in the industry, it is rather essential for

the organization to boost it (Cornwall, Vang and Hartman, 2016). With either the aid of estimates

below, the effect of announcing them could be reviewed:

For year 1 to 5 the growth are 21, 23, 25, 27 and 28 individually.

Year Dividend for the year

First year 21

Second year 23

Financial management can be characterized as the mechanism used mostly by trade

associations to sustain the funds and resources at the disposal of the organization. This is really

necessary to all companies as it enables to be using the resources wisely to meet long-term

business goals. Managing financial efficiency is very necessary to improve client

competitiveness. There are various ways that are used to this goal (Burtonshaw-Gunn, 2017). To

ensure that all of the processes connected with it have been carried out thoroughly, it is really

valuable for leaders to adequately review final reports so that decisions can be made for the

future. Questions first and third are identified to fulfill this Document. One of them is a ratio

study that ultimately determines whether or not the company is sustainable. This article

addresses numerous subjects including cost of debt evaluation using WACC and evaluation of

tight-term investment banking. In addition, this article also discusses numerous investment

assessment approaches that are used to shape investment choices.

QUESTION 1

a. Computation of market and book value cost of capital

Both liabilities and equity markets are maintained in a formal way known as financial

performance in all organizations. To accomplish most of the targets, including greater efficiency,

massive numbers of shareholders, etc., it is quite essential for corporations to ensure that the

shares are properly handled. The cost of borrowing is used in evaluating it to assess the expense

of all the securities, shares, loans, etc. Through reviewing the financial results, Kadlex Plc's

financial officer has determined that the present value cost of business capital is weak. For this

reason the management has decided to grant new shares in the industry, it is rather essential for

the organization to boost it (Cornwall, Vang and Hartman, 2016). With either the aid of estimates

below, the effect of announcing them could be reviewed:

For year 1 to 5 the growth are 21, 23, 25, 27 and 28 individually.

Year Dividend for the year

First year 21

Second year 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

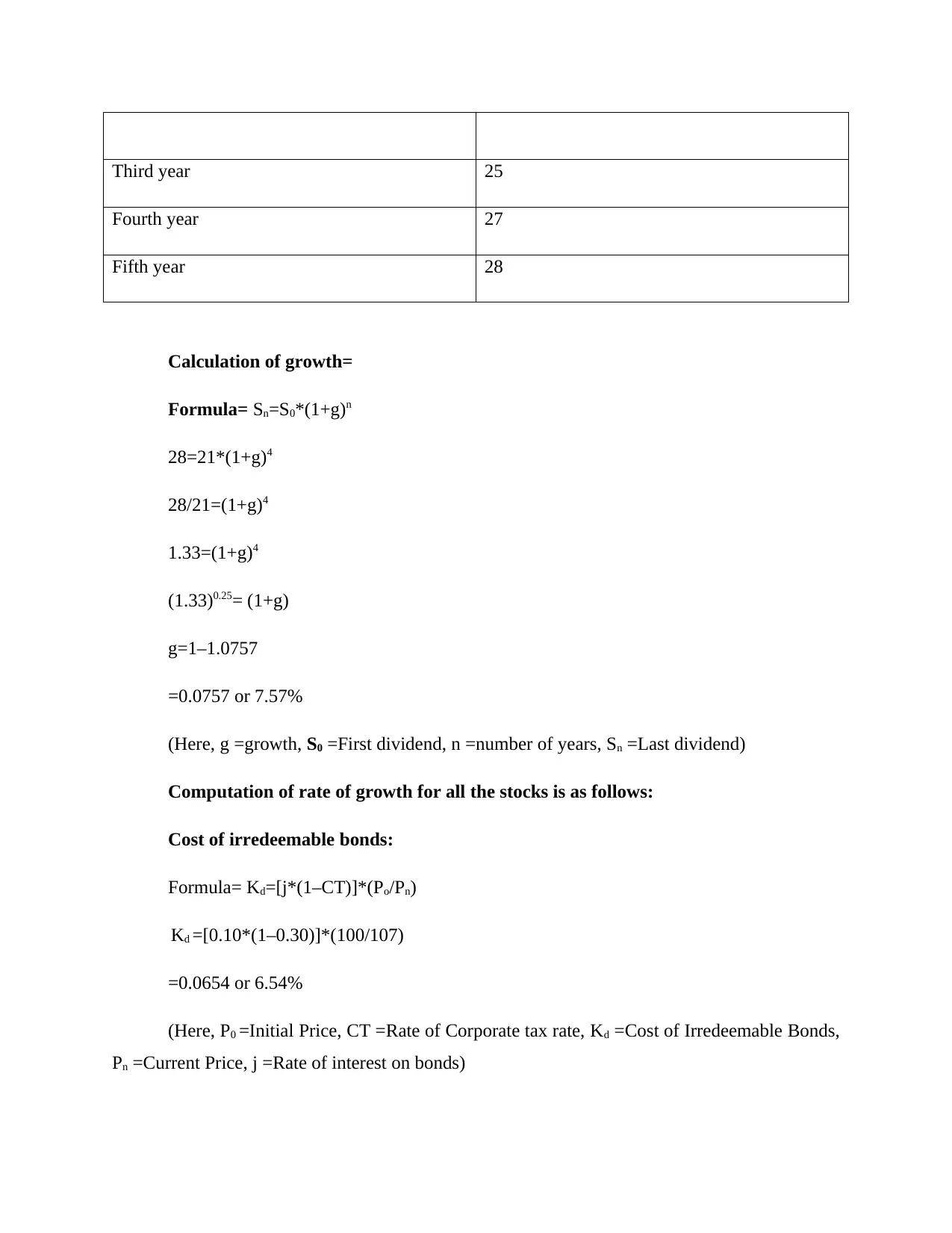

Third year 25

Fourth year 27

Fifth year 28

Calculation of growth=

Formula= Sn=S0*(1+g)n

28=21*(1+g)4

28/21=(1+g)4

1.33=(1+g)4

(1.33)0.25= (1+g)

g=1–1.0757

=0.0757 or 7.57%

(Here, g =growth, S0 =First dividend, n =number of years, Sn =Last dividend)

Computation of rate of growth for all the stocks is as follows:

Cost of irredeemable bonds:

Formula= Kd=[j*(1–CT)]*(Po/Pn)

Kd =[0.10*(1–0.30)]*(100/107)

=0.0654 or 6.54%

(Here, P0 =Initial Price, CT =Rate of Corporate tax rate, Kd =Cost of Irredeemable Bonds,

Pn =Current Price, j =Rate of interest on bonds)

Fourth year 27

Fifth year 28

Calculation of growth=

Formula= Sn=S0*(1+g)n

28=21*(1+g)4

28/21=(1+g)4

1.33=(1+g)4

(1.33)0.25= (1+g)

g=1–1.0757

=0.0757 or 7.57%

(Here, g =growth, S0 =First dividend, n =number of years, Sn =Last dividend)

Computation of rate of growth for all the stocks is as follows:

Cost of irredeemable bonds:

Formula= Kd=[j*(1–CT)]*(Po/Pn)

Kd =[0.10*(1–0.30)]*(100/107)

=0.0654 or 6.54%

(Here, P0 =Initial Price, CT =Rate of Corporate tax rate, Kd =Cost of Irredeemable Bonds,

Pn =Current Price, j =Rate of interest on bonds)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of equities:

Formula= Ke =[Sn*(1+g)+g ])/P0

Ke =[28*(1+0.075)+0.075]/2.65

=(28*1.15)/2.65

=12.15%

(Here, Sn =First dividend, P0 =Current share price of equity shares excluding dividend, Ke

=Cost of Equity, g =Growth rate, )

Cost of preference share:

Formula= Kp=(j)/Pf

= 7/75

= 0.0933 or 9.33%

(Here, Pf =Current price of preference share excluding dividend, j =Dividend on

preference shares, Kp =Total cost of Preference Shares)

Calculation of total average business and market value operating costs is as obeys:

Formula= Ke =[Sn*(1+g)+g ])/P0

Ke =[28*(1+0.075)+0.075]/2.65

=(28*1.15)/2.65

=12.15%

(Here, Sn =First dividend, P0 =Current share price of equity shares excluding dividend, Ke

=Cost of Equity, g =Growth rate, )

Cost of preference share:

Formula= Kp=(j)/Pf

= 7/75

= 0.0933 or 9.33%

(Here, Pf =Current price of preference share excluding dividend, j =Dividend on

preference shares, Kp =Total cost of Preference Shares)

Calculation of total average business and market value operating costs is as obeys:

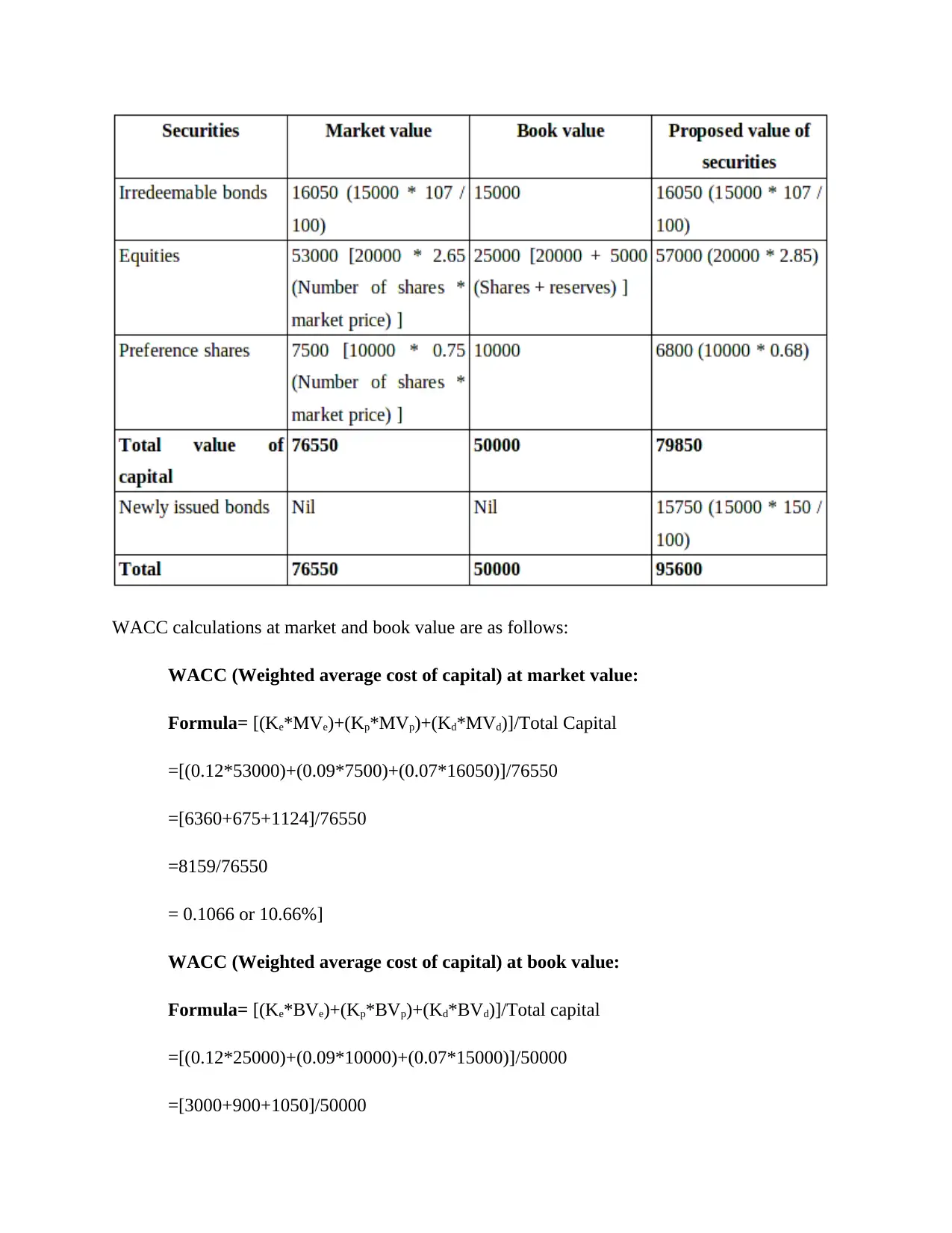

WACC calculations at market and book value are as follows:

WACC (Weighted average cost of capital) at market value:

Formula= [(Ke*MVe)+(Kp*MVp)+(Kd*MVd)]/Total Capital

=[(0.12*53000)+(0.09*7500)+(0.07*16050)]/76550

=[6360+675+1124]/76550

=8159/76550

= 0.1066 or 10.66%]

WACC (Weighted average cost of capital) at book value:

Formula= [(Ke*BVe)+(Kp*BVp)+(Kd*BVd)]/Total capital

=[(0.12*25000)+(0.09*10000)+(0.07*15000)]/50000

=[3000+900+1050]/50000

WACC (Weighted average cost of capital) at market value:

Formula= [(Ke*MVe)+(Kp*MVp)+(Kd*MVd)]/Total Capital

=[(0.12*53000)+(0.09*7500)+(0.07*16050)]/76550

=[6360+675+1124]/76550

=8159/76550

= 0.1066 or 10.66%]

WACC (Weighted average cost of capital) at book value:

Formula= [(Ke*BVe)+(Kp*BVp)+(Kd*BVd)]/Total capital

=[(0.12*25000)+(0.09*10000)+(0.07*15000)]/50000

=[3000+900+1050]/50000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=4950/50000

=0.099 or 9.9%

There are defined descriptions of all the variables that are mentioned in the formulas such as:

MVp =Market value of all the preference shares

Kd =Total cost of debts before applying changes

BVd =Actual book value of debts for the organisation

Total capital = Book + market value of all the securities

Kp =Total cost of preference shares before making changes

Mvd =Market value of debts of organisation

Bve =Actual book value of equities

Ke =Total cost of equity before making changes

MVe =Market value of total equities

BVp =Actual book values of preference shares

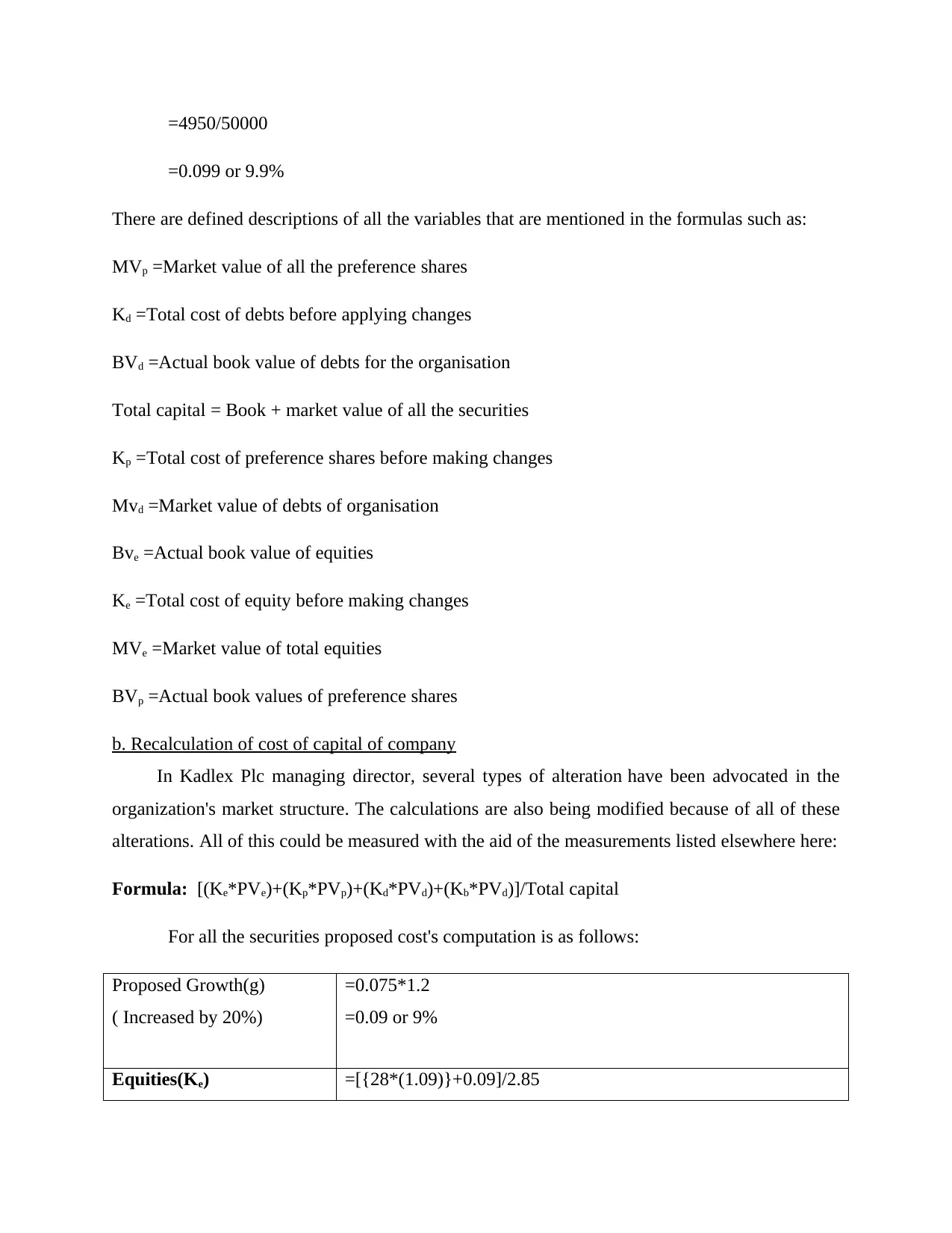

b. Recalculation of cost of capital of company

In Kadlex Plc managing director, several types of alteration have been advocated in the

organization's market structure. The calculations are also being modified because of all of these

alterations. All of this could be measured with the aid of the measurements listed elsewhere here:

Formula: [(Ke*PVe)+(Kp*PVp)+(Kd*PVd)+(Kb*PVd)]/Total capital

For all the securities proposed cost's computation is as follows:

Proposed Growth(g)

( Increased by 20%)

=0.075*1.2

=0.09 or 9%

Equities(Ke) =[{28*(1.09)}+0.09]/2.85

=0.099 or 9.9%

There are defined descriptions of all the variables that are mentioned in the formulas such as:

MVp =Market value of all the preference shares

Kd =Total cost of debts before applying changes

BVd =Actual book value of debts for the organisation

Total capital = Book + market value of all the securities

Kp =Total cost of preference shares before making changes

Mvd =Market value of debts of organisation

Bve =Actual book value of equities

Ke =Total cost of equity before making changes

MVe =Market value of total equities

BVp =Actual book values of preference shares

b. Recalculation of cost of capital of company

In Kadlex Plc managing director, several types of alteration have been advocated in the

organization's market structure. The calculations are also being modified because of all of these

alterations. All of this could be measured with the aid of the measurements listed elsewhere here:

Formula: [(Ke*PVe)+(Kp*PVp)+(Kd*PVd)+(Kb*PVd)]/Total capital

For all the securities proposed cost's computation is as follows:

Proposed Growth(g)

( Increased by 20%)

=0.075*1.2

=0.09 or 9%

Equities(Ke) =[{28*(1.09)}+0.09]/2.85

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

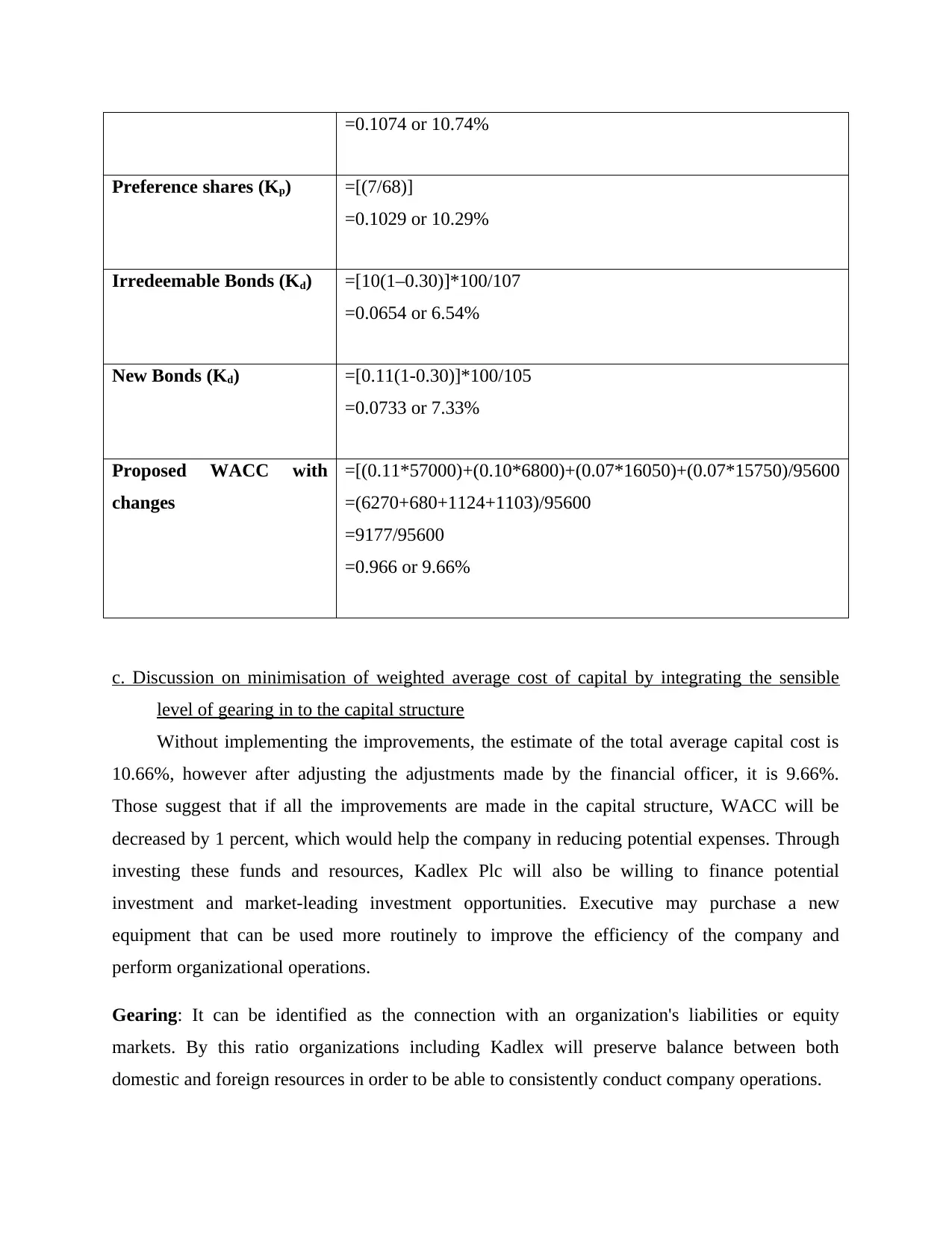

=0.1074 or 10.74%

Preference shares (Kp) =[(7/68)]

=0.1029 or 10.29%

Irredeemable Bonds (Kd) =[10(1–0.30)]*100/107

=0.0654 or 6.54%

New Bonds (Kd) =[0.11(1-0.30)]*100/105

=0.0733 or 7.33%

Proposed WACC with

changes

=[(0.11*57000)+(0.10*6800)+(0.07*16050)+(0.07*15750)/95600

=(6270+680+1124+1103)/95600

=9177/95600

=0.966 or 9.66%

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible

level of gearing in to the capital structure

Without implementing the improvements, the estimate of the total average capital cost is

10.66%, however after adjusting the adjustments made by the financial officer, it is 9.66%.

Those suggest that if all the improvements are made in the capital structure, WACC will be

decreased by 1 percent, which would help the company in reducing potential expenses. Through

investing these funds and resources, Kadlex Plc will also be willing to finance potential

investment and market-leading investment opportunities. Executive may purchase a new

equipment that can be used more routinely to improve the efficiency of the company and

perform organizational operations.

Gearing: It can be identified as the connection with an organization's liabilities or equity

markets. By this ratio organizations including Kadlex will preserve balance between both

domestic and foreign resources in order to be able to consistently conduct company operations.

Preference shares (Kp) =[(7/68)]

=0.1029 or 10.29%

Irredeemable Bonds (Kd) =[10(1–0.30)]*100/107

=0.0654 or 6.54%

New Bonds (Kd) =[0.11(1-0.30)]*100/105

=0.0733 or 7.33%

Proposed WACC with

changes

=[(0.11*57000)+(0.10*6800)+(0.07*16050)+(0.07*15750)/95600

=(6270+680+1124+1103)/95600

=9177/95600

=0.966 or 9.66%

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible

level of gearing in to the capital structure

Without implementing the improvements, the estimate of the total average capital cost is

10.66%, however after adjusting the adjustments made by the financial officer, it is 9.66%.

Those suggest that if all the improvements are made in the capital structure, WACC will be

decreased by 1 percent, which would help the company in reducing potential expenses. Through

investing these funds and resources, Kadlex Plc will also be willing to finance potential

investment and market-leading investment opportunities. Executive may purchase a new

equipment that can be used more routinely to improve the efficiency of the company and

perform organizational operations.

Gearing: It can be identified as the connection with an organization's liabilities or equity

markets. By this ratio organizations including Kadlex will preserve balance between both

domestic and foreign resources in order to be able to consistently conduct company operations.

Weighted average cost of capital: This can be characterized as a rate of interest or payout that

must be charged to its investors including stock holders with an entity. It is determined primarily

by the foreign economy, but rather by the executives. When it is measured varying equity prices,

preferential securities and liabilities are determined.

Capital structure: It is the structure that an organization follows for the participatory

management of its loans and equity markets. This helps an company to evaluate the resources it

needs in order to achieve development and execute organizational activities. In other words, the

percentage where liabilities, equity markets as well as other bonds are attempted could be

described as (Dunham-Taylor and Pinczuk, 2014).

d. Effects of short-termism on agency problem and bankruptcy

Shorter-terms can be described as unreasonable corporate emphasis instead of just hard-

term approaches on quick-term outcomes. This is centered on companies where the company is

under heavy pressure from stakeholders to get higher profits. Development of this sort of

scenario leads to increased quarterly profits and neglect the implementation of initiatives that

that seek to produce successful outcomes in the future era.

The concern with the corporation is the constitutional violation from a company's owners

and management. Management functions as an employee of protection owners in all

organizations and it is their duty to devise these plans that would provide them with greater

yields. And from the other side, restructuring can be described as procedure where an

organization, caused by lack of properties and private properties, becomes delinquent. vIf the

organization actually listens to brief-termism then it will lead in issues with the business and

default as only quick-term vantages will be gained for this. It will build the circumstance of lack

of resources for the potential that will lead to no payout to stakeholders and no funding to carried

about ongoing operations. If the condition of quick-terms arises then it'll be quite challenging for

the corporations to pay the protection shareholders good yields for this, lengthy-term income

could not be produced.

must be charged to its investors including stock holders with an entity. It is determined primarily

by the foreign economy, but rather by the executives. When it is measured varying equity prices,

preferential securities and liabilities are determined.

Capital structure: It is the structure that an organization follows for the participatory

management of its loans and equity markets. This helps an company to evaluate the resources it

needs in order to achieve development and execute organizational activities. In other words, the

percentage where liabilities, equity markets as well as other bonds are attempted could be

described as (Dunham-Taylor and Pinczuk, 2014).

d. Effects of short-termism on agency problem and bankruptcy

Shorter-terms can be described as unreasonable corporate emphasis instead of just hard-

term approaches on quick-term outcomes. This is centered on companies where the company is

under heavy pressure from stakeholders to get higher profits. Development of this sort of

scenario leads to increased quarterly profits and neglect the implementation of initiatives that

that seek to produce successful outcomes in the future era.

The concern with the corporation is the constitutional violation from a company's owners

and management. Management functions as an employee of protection owners in all

organizations and it is their duty to devise these plans that would provide them with greater

yields. And from the other side, restructuring can be described as procedure where an

organization, caused by lack of properties and private properties, becomes delinquent. vIf the

organization actually listens to brief-termism then it will lead in issues with the business and

default as only quick-term vantages will be gained for this. It will build the circumstance of lack

of resources for the potential that will lead to no payout to stakeholders and no funding to carried

about ongoing operations. If the condition of quick-terms arises then it'll be quite challenging for

the corporations to pay the protection shareholders good yields for this, lengthy-term income

could not be produced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 3

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV

and IRR

Companies need to invest in income-creating resources to refresh, enhance, or substitute

the medium through which the carry on the sector. Investment enables corporations to keep

producing cash flows or sustain the competitiveness of company's current operations in the

potential. Investment capital ventures will usually involve large cash inflows at the outset, and

will then generate cash inflows across various times (Finkler, Smith and Calabrese, 2018).

Investment capital ventures need careful consideration, as they have to collect and spend very

significant quantities of money, and as they will decide if the business will be successful in the

long run. For this apply various types of methods to get effective results. Such as Lovewell apply

various methods to analysis that the project investment is good or not.

Particulars Details

Initial outlay of project 275000

Inflows of funds 85000

Outflow of funds for six years 12500

Actual cash inflow (85000 - 12500) 72500

Total life of project 6 years

Residual value of machine (275000 *

15% = 41250)

15% of machine's

original cost

Depreciation (275000 – 41250 / 6) 38958

Cost of capital 12%

R1` 14%

R2 18%

Payback period: The payback time is the amount of periods it is projected to continue to

return from those in the total net profits arising from an investment capital plan, the initial

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV

and IRR

Companies need to invest in income-creating resources to refresh, enhance, or substitute

the medium through which the carry on the sector. Investment enables corporations to keep

producing cash flows or sustain the competitiveness of company's current operations in the

potential. Investment capital ventures will usually involve large cash inflows at the outset, and

will then generate cash inflows across various times (Finkler, Smith and Calabrese, 2018).

Investment capital ventures need careful consideration, as they have to collect and spend very

significant quantities of money, and as they will decide if the business will be successful in the

long run. For this apply various types of methods to get effective results. Such as Lovewell apply

various methods to analysis that the project investment is good or not.

Particulars Details

Initial outlay of project 275000

Inflows of funds 85000

Outflow of funds for six years 12500

Actual cash inflow (85000 - 12500) 72500

Total life of project 6 years

Residual value of machine (275000 *

15% = 41250)

15% of machine's

original cost

Depreciation (275000 – 41250 / 6) 38958

Cost of capital 12%

R1` 14%

R2 18%

Payback period: The payback time is the amount of periods it is projected to continue to

return from those in the total net profits arising from an investment capital plan, the initial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenditure. By applying this approach to assess projects the determination principle is to

approve a proposal if the repayment duration is comparable to or above a defined minimum

value. An estimation of the repayment period to many integers can be obtained if dividend

payments are expected to take place equally during every period, but a greater level of precision

is not ideal in measuring the time horizon because it does not provide knowledge that is

particularly effective. Formula of it is follows:

Pay back period = I / C

I = Initial investment

C = Cash Inflow

Calculation of it is as follows:

Payback period= 275000/ 72500

= 3.79 years

Accounting rate of return: There are alternate meanings of the return on equity worked

(ROCE), which is often named the return on the investment (ROI) and the rate of interest on

accounting (ARR). All meanings apply to accounting income of a certain proportion of the

resources engaged in a construction project. One broadly-used concept is: The rate of return to

contract is the estimated rate of return on the investment. The estimate is the plan's financial

benefit, separated by both the original project expenditure (Martin, 2016). Someone will approve

a venture if the calculation produces an amount that reaches the same level of challenge that the

business considers as its guaranteed return on investment. The calculation for the rate of return to

payment is:

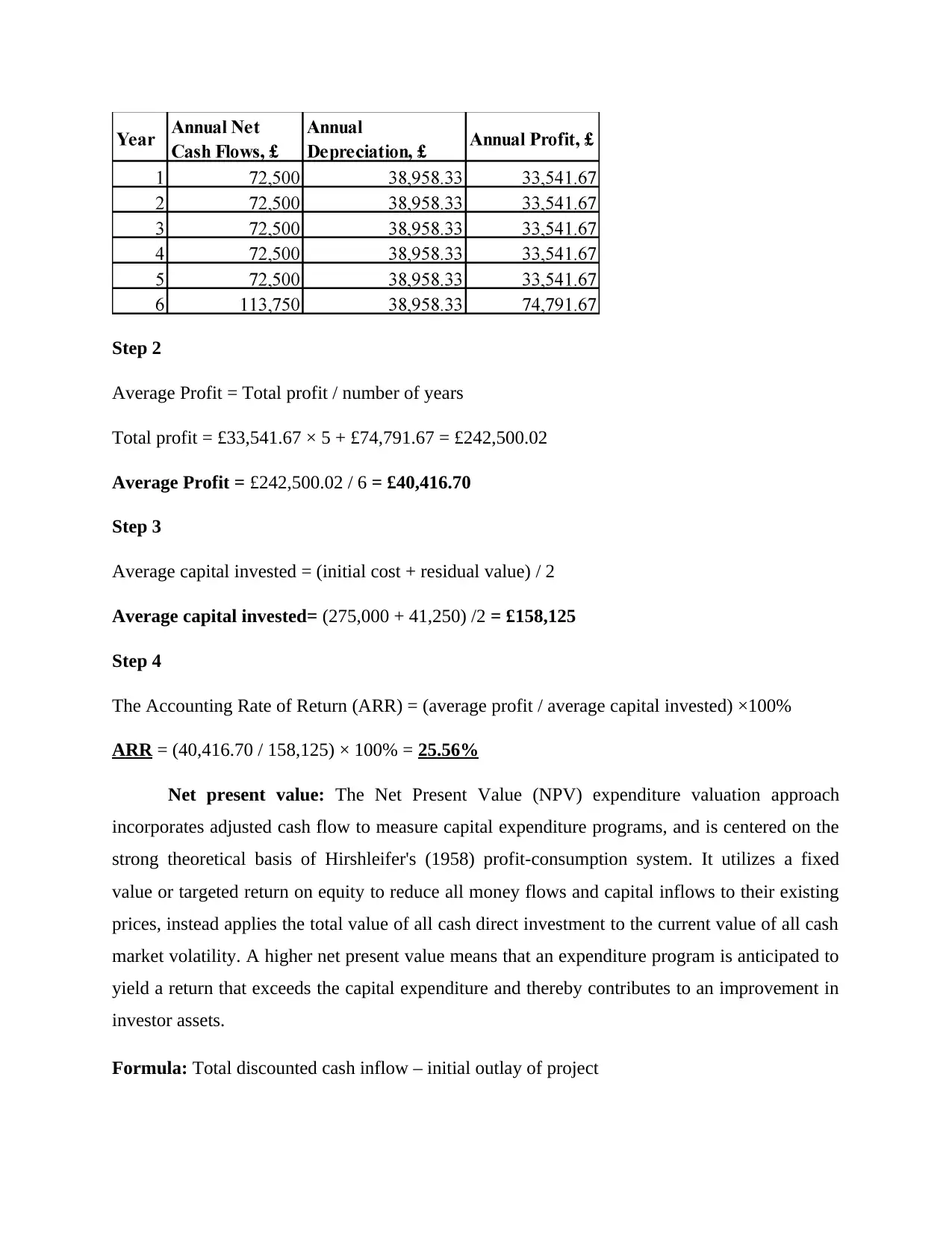

Annual Profit = Annual Net Cash flow – Annual Depreciation

Residual value £41,250 added to year 6

approve a proposal if the repayment duration is comparable to or above a defined minimum

value. An estimation of the repayment period to many integers can be obtained if dividend

payments are expected to take place equally during every period, but a greater level of precision

is not ideal in measuring the time horizon because it does not provide knowledge that is

particularly effective. Formula of it is follows:

Pay back period = I / C

I = Initial investment

C = Cash Inflow

Calculation of it is as follows:

Payback period= 275000/ 72500

= 3.79 years

Accounting rate of return: There are alternate meanings of the return on equity worked

(ROCE), which is often named the return on the investment (ROI) and the rate of interest on

accounting (ARR). All meanings apply to accounting income of a certain proportion of the

resources engaged in a construction project. One broadly-used concept is: The rate of return to

contract is the estimated rate of return on the investment. The estimate is the plan's financial

benefit, separated by both the original project expenditure (Martin, 2016). Someone will approve

a venture if the calculation produces an amount that reaches the same level of challenge that the

business considers as its guaranteed return on investment. The calculation for the rate of return to

payment is:

Annual Profit = Annual Net Cash flow – Annual Depreciation

Residual value £41,250 added to year 6

Step 2

Average Profit = Total profit / number of years

Total profit = £33,541.67 × 5 + £74,791.67 = £242,500.02

Average Profit = £242,500.02 / 6 = £40,416.70

Step 3

Average capital invested = (initial cost + residual value) / 2

Average capital invested= (275,000 + 41,250) /2 = £158,125

Step 4

The Accounting Rate of Return (ARR) = (average profit / average capital invested) ×100%

ARR = (40,416.70 / 158,125) × 100% = 25.56%

Net present value: The Net Present Value (NPV) expenditure valuation approach

incorporates adjusted cash flow to measure capital expenditure programs, and is centered on the

strong theoretical basis of Hirshleifer's (1958) profit-consumption system. It utilizes a fixed

value or targeted return on equity to reduce all money flows and capital inflows to their existing

prices, instead applies the total value of all cash direct investment to the current value of all cash

market volatility. A higher net present value means that an expenditure program is anticipated to

yield a return that exceeds the capital expenditure and thereby contributes to an improvement in

investor assets.

Formula: Total discounted cash inflow – initial outlay of project

Average Profit = Total profit / number of years

Total profit = £33,541.67 × 5 + £74,791.67 = £242,500.02

Average Profit = £242,500.02 / 6 = £40,416.70

Step 3

Average capital invested = (initial cost + residual value) / 2

Average capital invested= (275,000 + 41,250) /2 = £158,125

Step 4

The Accounting Rate of Return (ARR) = (average profit / average capital invested) ×100%

ARR = (40,416.70 / 158,125) × 100% = 25.56%

Net present value: The Net Present Value (NPV) expenditure valuation approach

incorporates adjusted cash flow to measure capital expenditure programs, and is centered on the

strong theoretical basis of Hirshleifer's (1958) profit-consumption system. It utilizes a fixed

value or targeted return on equity to reduce all money flows and capital inflows to their existing

prices, instead applies the total value of all cash direct investment to the current value of all cash

market volatility. A higher net present value means that an expenditure program is anticipated to

yield a return that exceeds the capital expenditure and thereby contributes to an improvement in

investor assets.

Formula: Total discounted cash inflow – initial outlay of project

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.