APC308 Financial Management Assignment: Investment and Valuation

VerifiedAdded on 2022/12/15

|14

|3859

|239

Homework Assignment

AI Summary

This document presents a detailed solution to a financial management assignment, addressing key concepts in investment appraisal and valuation. The assignment begins by calculating and interpreting various investment appraisal techniques, including the payback period, accounting rate of ret...

Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Q2. Investment Appraisal technique................................................................................................3

Question 3 – Mergers and Takeovers..............................................................................................9

REFERENCES..............................................................................................................................14

2

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Q2. Investment Appraisal technique................................................................................................3

Question 3 – Mergers and Takeovers..............................................................................................9

REFERENCES..............................................................................................................................14

2

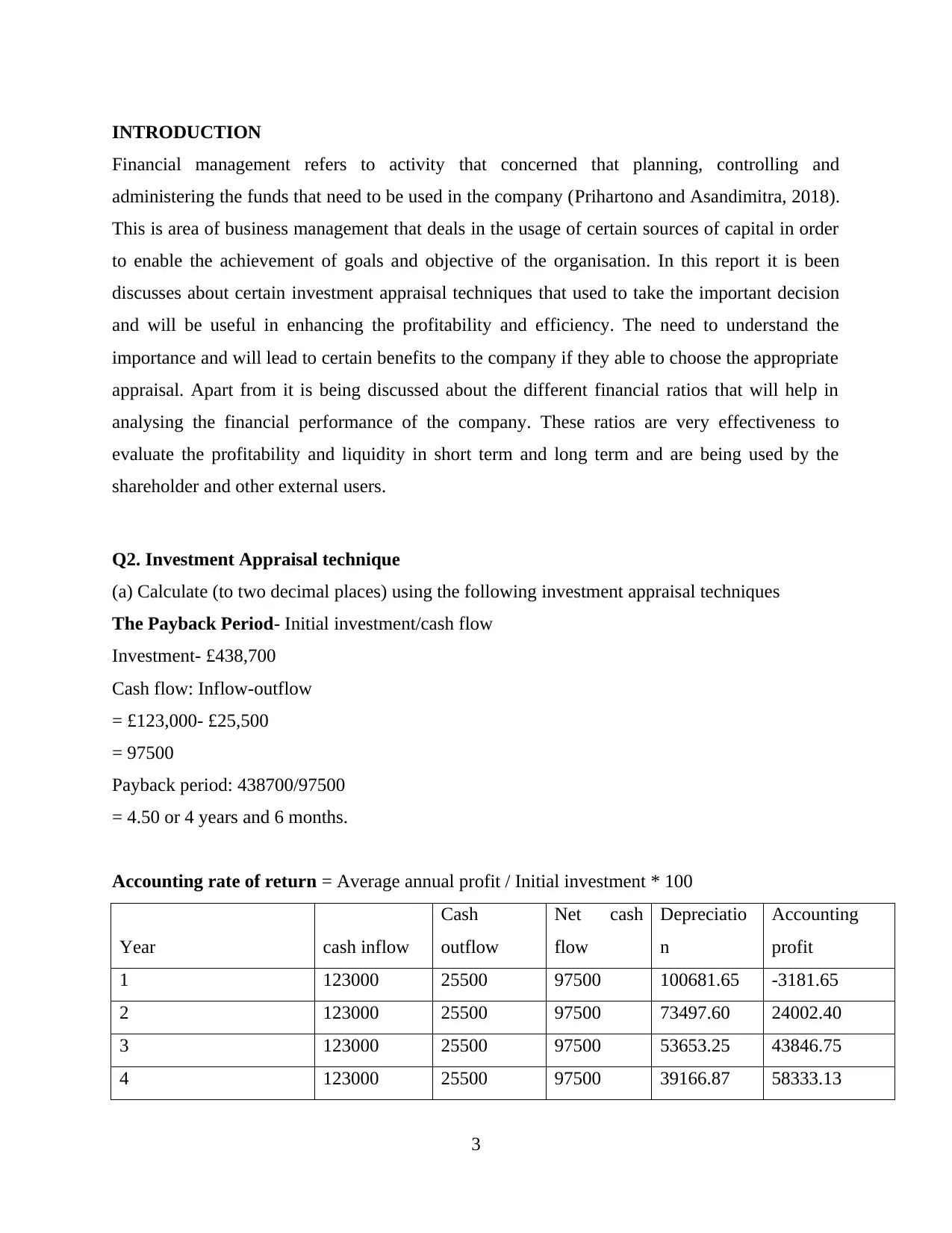

INTRODUCTION

Financial management refers to activity that concerned that planning, controlling and

administering the funds that need to be used in the company (Prihartono and Asandimitra, 2018).

This is area of business management that deals in the usage of certain sources of capital in order

to enable the achievement of goals and objective of the organisation. In this report it is been

discusses about certain investment appraisal techniques that used to take the important decision

and will be useful in enhancing the profitability and efficiency. The need to understand the

importance and will lead to certain benefits to the company if they able to choose the appropriate

appraisal. Apart from it is being discussed about the different financial ratios that will help in

analysing the financial performance of the company. These ratios are very effectiveness to

evaluate the profitability and liquidity in short term and long term and are being used by the

shareholder and other external users.

Q2. Investment Appraisal technique

(a) Calculate (to two decimal places) using the following investment appraisal techniques

The Payback Period- Initial investment/cash flow

Investment- £438,700

Cash flow: Inflow-outflow

= £123,000- £25,500

= 97500

Payback period: 438700/97500

= 4.50 or 4 years and 6 months.

Accounting rate of return = Average annual profit / Initial investment * 100

Year cash inflow

Cash

outflow

Net cash

flow

Depreciatio

n

Accounting

profit

1 123000 25500 97500 100681.65 -3181.65

2 123000 25500 97500 73497.60 24002.40

3 123000 25500 97500 53653.25 43846.75

4 123000 25500 97500 39166.87 58333.13

3

Financial management refers to activity that concerned that planning, controlling and

administering the funds that need to be used in the company (Prihartono and Asandimitra, 2018).

This is area of business management that deals in the usage of certain sources of capital in order

to enable the achievement of goals and objective of the organisation. In this report it is been

discusses about certain investment appraisal techniques that used to take the important decision

and will be useful in enhancing the profitability and efficiency. The need to understand the

importance and will lead to certain benefits to the company if they able to choose the appropriate

appraisal. Apart from it is being discussed about the different financial ratios that will help in

analysing the financial performance of the company. These ratios are very effectiveness to

evaluate the profitability and liquidity in short term and long term and are being used by the

shareholder and other external users.

Q2. Investment Appraisal technique

(a) Calculate (to two decimal places) using the following investment appraisal techniques

The Payback Period- Initial investment/cash flow

Investment- £438,700

Cash flow: Inflow-outflow

= £123,000- £25,500

= 97500

Payback period: 438700/97500

= 4.50 or 4 years and 6 months.

Accounting rate of return = Average annual profit / Initial investment * 100

Year cash inflow

Cash

outflow

Net cash

flow

Depreciatio

n

Accounting

profit

1 123000 25500 97500 100681.65 -3181.65

2 123000 25500 97500 73497.60 24002.40

3 123000 25500 97500 53653.25 43846.75

4 123000 25500 97500 39166.87 58333.13

3

You're viewing a preview

Unlock full access by subscribing today!

5 123000 25500 97500 28591.82 68908.18

6 123000 25500 97500 20872.03 76627.97

268536.78

Average accounting profit: 268536.78/6

= 44756.13

ARR: 44756.13/438700*100

= 10.20%

Working Note:

Calculation of depreciation

Depreciation Expenses = (Net Book Value –

Residual value) X Depreciation Rate

Net book value: 438700

Residual value: 15% of cost 65805

Depreciation rate 27%

Year

Net book

value

Residu

al value Rate

Depreciati

on

1

438700.0

0 65805 27 100681.65

2

338018.3

5 65805 27 73497.60

3

264520.7

5 65805 27 53653.25

4

210867.4

9 65805 27 39166.87

5

171700.6

2 65805 27 28591.82

6

143108.8

0 65805 27 20872.03

4

6 123000 25500 97500 20872.03 76627.97

268536.78

Average accounting profit: 268536.78/6

= 44756.13

ARR: 44756.13/438700*100

= 10.20%

Working Note:

Calculation of depreciation

Depreciation Expenses = (Net Book Value –

Residual value) X Depreciation Rate

Net book value: 438700

Residual value: 15% of cost 65805

Depreciation rate 27%

Year

Net book

value

Residu

al value Rate

Depreciati

on

1

438700.0

0 65805 27 100681.65

2

338018.3

5 65805 27 73497.60

3

264520.7

5 65805 27 53653.25

4

210867.4

9 65805 27 39166.87

5

171700.6

2 65805 27 28591.82

6

143108.8

0 65805 27 20872.03

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

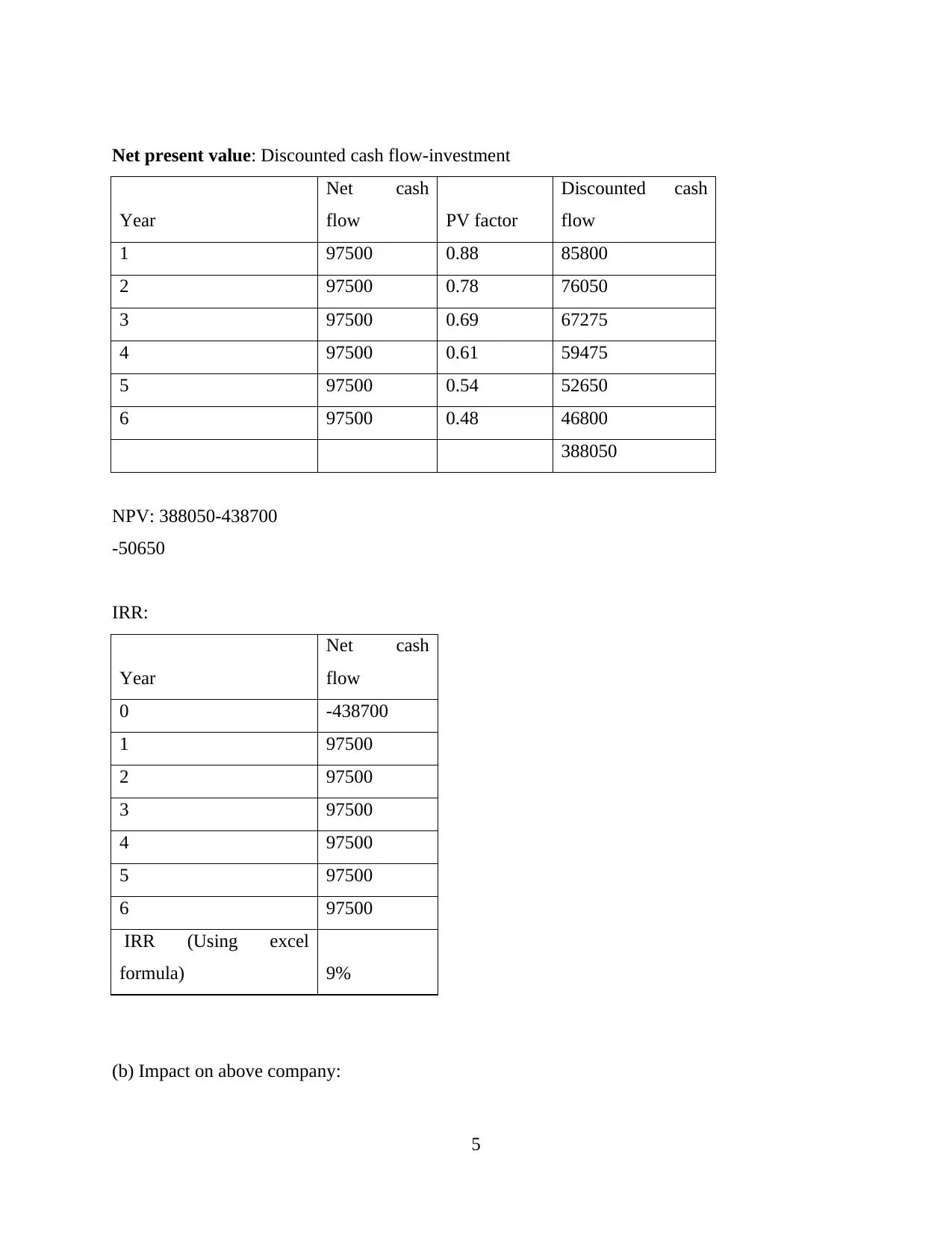

Net present value: Discounted cash flow-investment

Year

Net cash

flow PV factor

Discounted cash

flow

1 97500 0.88 85800

2 97500 0.78 76050

3 97500 0.69 67275

4 97500 0.61 59475

5 97500 0.54 52650

6 97500 0.48 46800

388050

NPV: 388050-438700

-50650

IRR:

Year

Net cash

flow

0 -438700

1 97500

2 97500

3 97500

4 97500

5 97500

6 97500

IRR (Using excel

formula) 9%

(b) Impact on above company:

5

Year

Net cash

flow PV factor

Discounted cash

flow

1 97500 0.88 85800

2 97500 0.78 76050

3 97500 0.69 67275

4 97500 0.61 59475

5 97500 0.54 52650

6 97500 0.48 46800

388050

NPV: 388050-438700

-50650

IRR:

Year

Net cash

flow

0 -438700

1 97500

2 97500

3 97500

4 97500

5 97500

6 97500

IRR (Using excel

formula) 9%

(b) Impact on above company:

5

Payback period: The payback period is of 4 years and 6 months. This shows that cost of above

investment will be covered in 4.5 years. Though life of project is of 6 years which shows that this

project is useful. If above company will acquire this than it will be useful for them to gain higher

financial advantage.

Accounting rate of return- The ARR of above project is of 10.20% that shows that above project

will generate return or profit with this rate which is higher. If above company will acquire this

project than it will lead to positive impact on company’s financial performance during particular

accounting period.

Net present value- The net present value of this project is negative due to less number of cash

flow. In such case above company needs to rethink before making invest in such project.

IRR- the IRR of above project is positive and higher which is of 9%. It shows that above

company needs to make invest in order to generate higher return from this venture. If above

company will make invest than it will be beneficial for them.

c. Evaluating benefits and limitations of investment appraisal technique

Investment appraisal technique concern with method that business will able to assess the

attractiveness of possible investment or projects that is based on the finding of several different

capital budgeting and financing technique (Jones, Kovner and Mose, 2018). Some are as follows-

Payback period- This refers to the length of time making an investment and the time at which

that investment is broken. This helps in revealing the payback period is the time it takes for the

cash flows of incomes from particular projects to cover the initial investment.

Some of its benefits are as follows-

Simple and easy to use- This is one of the significant advantages of payback period as it

need very few inputs in the calculation and relatively easier to calculate than other capital

budgeting. This helps the analyst to evaluate the best investment appraisal.

Quick solution- As, it is easy to use and calculate and hence help the analyst to make the

informed decision quickly and does not waste much time to determine the investment

6

investment will be covered in 4.5 years. Though life of project is of 6 years which shows that this

project is useful. If above company will acquire this than it will be useful for them to gain higher

financial advantage.

Accounting rate of return- The ARR of above project is of 10.20% that shows that above project

will generate return or profit with this rate which is higher. If above company will acquire this

project than it will lead to positive impact on company’s financial performance during particular

accounting period.

Net present value- The net present value of this project is negative due to less number of cash

flow. In such case above company needs to rethink before making invest in such project.

IRR- the IRR of above project is positive and higher which is of 9%. It shows that above

company needs to make invest in order to generate higher return from this venture. If above

company will make invest than it will be beneficial for them.

c. Evaluating benefits and limitations of investment appraisal technique

Investment appraisal technique concern with method that business will able to assess the

attractiveness of possible investment or projects that is based on the finding of several different

capital budgeting and financing technique (Jones, Kovner and Mose, 2018). Some are as follows-

Payback period- This refers to the length of time making an investment and the time at which

that investment is broken. This helps in revealing the payback period is the time it takes for the

cash flows of incomes from particular projects to cover the initial investment.

Some of its benefits are as follows-

Simple and easy to use- This is one of the significant advantages of payback period as it

need very few inputs in the calculation and relatively easier to calculate than other capital

budgeting. This helps the analyst to evaluate the best investment appraisal.

Quick solution- As, it is easy to use and calculate and hence help the analyst to make the

informed decision quickly and does not waste much time to determine the investment

6

You're viewing a preview

Unlock full access by subscribing today!

proposal. This is effective for the companies who has limited resources and wants better

decision-making technique.

Beneficial in uncertainty of case- This method is very effective to use when Company is

facing the uncertainties in their business and were not sure about the future circumstances

(Zietlo, Seidner and O'Brien, 2018). Hence, this method is useful in undertaking the

project with short PBP and reduce the chances of loss through obsolescence.

Some of the disadvantages are as follows-

Ignores time value of money- This is main disadvantages of company that it ignores the

time value of money which is very important for the purpose of business. This method

does not consider the real value and that reduces its efficiency in long period of time.

Not realistic- This method is as simple in use as it does not consider the normal business

scenarios. Capital investments are not just one-time investments and will need further

investment in following years as well and will leads to project usually have irregular cash

inflows in the company.

Accounting rate of return- The average accounting return formula for the evaluation of

commercial assets is dependent upon an expected yield for that time using the accounting rate for

a given period of years. Usually, the average return approach is used to compare two or more

financial performance with future profitability (Loke, 2017). As other analytical instruments, this

approach is used with its share of advantages and disadvantages.

Advantages- The overall return rate is simple to calculate. Managers will easily see how an

investment potential can be sufficiently profitable to merit further assessment. Go back to the

example of modern machines being purchased to improve production. If, however, investment in

camions to supply goods to consumers would cut the shipping costs by 10% if the initial estimate

indicates that buying only results in a 2% rise in earnings, then the management will have to

consider if decreased shipping costs are a safer investment.

Disadvantage- The time worth for resources is ignored by ARR. The principal flaw of the mean

cash return system is that the time value of the funds is overlooked.

Contrary to other investment assessment approaches, the RRA is focused not on cash flow but on

earnings. The ARR procedure lacks the investment cash balance (Nowicki, 2018). The

corporation will invest in other lucrative investments if an investment provides cash input

7

decision-making technique.

Beneficial in uncertainty of case- This method is very effective to use when Company is

facing the uncertainties in their business and were not sure about the future circumstances

(Zietlo, Seidner and O'Brien, 2018). Hence, this method is useful in undertaking the

project with short PBP and reduce the chances of loss through obsolescence.

Some of the disadvantages are as follows-

Ignores time value of money- This is main disadvantages of company that it ignores the

time value of money which is very important for the purpose of business. This method

does not consider the real value and that reduces its efficiency in long period of time.

Not realistic- This method is as simple in use as it does not consider the normal business

scenarios. Capital investments are not just one-time investments and will need further

investment in following years as well and will leads to project usually have irregular cash

inflows in the company.

Accounting rate of return- The average accounting return formula for the evaluation of

commercial assets is dependent upon an expected yield for that time using the accounting rate for

a given period of years. Usually, the average return approach is used to compare two or more

financial performance with future profitability (Loke, 2017). As other analytical instruments, this

approach is used with its share of advantages and disadvantages.

Advantages- The overall return rate is simple to calculate. Managers will easily see how an

investment potential can be sufficiently profitable to merit further assessment. Go back to the

example of modern machines being purchased to improve production. If, however, investment in

camions to supply goods to consumers would cut the shipping costs by 10% if the initial estimate

indicates that buying only results in a 2% rise in earnings, then the management will have to

consider if decreased shipping costs are a safer investment.

Disadvantage- The time worth for resources is ignored by ARR. The principal flaw of the mean

cash return system is that the time value of the funds is overlooked.

Contrary to other investment assessment approaches, the RRA is focused not on cash flow but on

earnings. The ARR procedure lacks the investment cash balance (Nowicki, 2018). The

corporation will invest in other lucrative investments if an investment provides cash input

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rapidly. But the approach of accounting return relies instead on cash balance on total net

accounting revenue. It is influenced by arbitrary, non-cash items such as the depreciation rate

that you use for benefit calculation.

There are various methods for an ARR calculation that can also be used. The ARR approach

does not take into account the project's final value. You have to make confident that you are

measuring the ARR on a regular basis by using the ARR to compare various investments.

The ARR should not take the pacing of profits into consideration. A return of £100,000 five

years is equal to £100,000 next year after estimating the ARR. Cash inflows that are greater than

accounting earnings are not taken into account. In reality, relatively soon you would like benefit.

Net present value- The Net Present Value (NPV) is a way of deciding whether an investment in

a project or company should be carried out solely for financial analysis. Compared to initial

investments, the current value of potential cash flights (Ward and Forker, 2017). Net present

value is an instrument for the working capital of a project or expenditure to assess the feasibility

of it. The difference between actual cash inflow value and the current cash outflow valuation is

measured over the duration.

Advantages- The main advantage of using NPV is that it takes the idea of the time of money into

account: the stronger dollar, due to its income power, is more than one dollar future. In the NPV

calculation, the reduced net cash flow from a project is taken into account to calculate its

feasibility. Understanding how current values are crucial to the budgeting of resources (Mitchell,

2017).

Disadvantages- The complete calculation of NPV relies on the reduction of potential cash flows

by the necessary rates. There are no criteria for this rate to be established, however. This

proportion is left to the discretion of businesses and instances in which the NPV is unreliable due

to an incorrect rate of return could occur.

IRR- The internal rate of return for estimating the feasibility of future expenditure is a measure

used for fundamental reporting. The intrinsic rates of return are a rate of return that within a

financial analysis equals the net present value (NPV) of all free cash flow to null. Computations

of IRR depend on a formula identical to that of NPV. Notice that the IRR is not the program's

8

accounting revenue. It is influenced by arbitrary, non-cash items such as the depreciation rate

that you use for benefit calculation.

There are various methods for an ARR calculation that can also be used. The ARR approach

does not take into account the project's final value. You have to make confident that you are

measuring the ARR on a regular basis by using the ARR to compare various investments.

The ARR should not take the pacing of profits into consideration. A return of £100,000 five

years is equal to £100,000 next year after estimating the ARR. Cash inflows that are greater than

accounting earnings are not taken into account. In reality, relatively soon you would like benefit.

Net present value- The Net Present Value (NPV) is a way of deciding whether an investment in

a project or company should be carried out solely for financial analysis. Compared to initial

investments, the current value of potential cash flights (Ward and Forker, 2017). Net present

value is an instrument for the working capital of a project or expenditure to assess the feasibility

of it. The difference between actual cash inflow value and the current cash outflow valuation is

measured over the duration.

Advantages- The main advantage of using NPV is that it takes the idea of the time of money into

account: the stronger dollar, due to its income power, is more than one dollar future. In the NPV

calculation, the reduced net cash flow from a project is taken into account to calculate its

feasibility. Understanding how current values are crucial to the budgeting of resources (Mitchell,

2017).

Disadvantages- The complete calculation of NPV relies on the reduction of potential cash flows

by the necessary rates. There are no criteria for this rate to be established, however. This

proportion is left to the discretion of businesses and instances in which the NPV is unreliable due

to an incorrect rate of return could occur.

IRR- The internal rate of return for estimating the feasibility of future expenditure is a measure

used for fundamental reporting. The intrinsic rates of return are a rate of return that within a

financial analysis equals the net present value (NPV) of all free cash flow to null. Computations

of IRR depend on a formula identical to that of NPV. Notice that the IRR is not the program's

8

real dollar value (Nkundabanyanga, Nalukenge and Tusiime, 2017). The present value is

equivalent to zero for the yearly return.

Advantages- the IRR is an easy metric to quantify and offers an easy way of comparing the value

of different programmes. The IRR gives a brief overview of what capital ventures will have the

highest possible cash flow for all small business owners. It may also be used for tax purpose,

including such providing a brief glimpse of the possible benefit or savings of new machinery,

rather than old equipment repair.

Disadvantages- the IRR approach only covers the expected cash flow from capital injections and

excludes future possible expense impacts. For example, potential costs of fuel and repairs, as you

contemplate investment in trucks, may reduce profits because fuel rates fluctuate and repair

demands change. The need to buy unused properties where a fleet of vehicles can park is a

contingent project and these costs are not a consideration in the IRR estimate of cash flows

created by fleet operations.

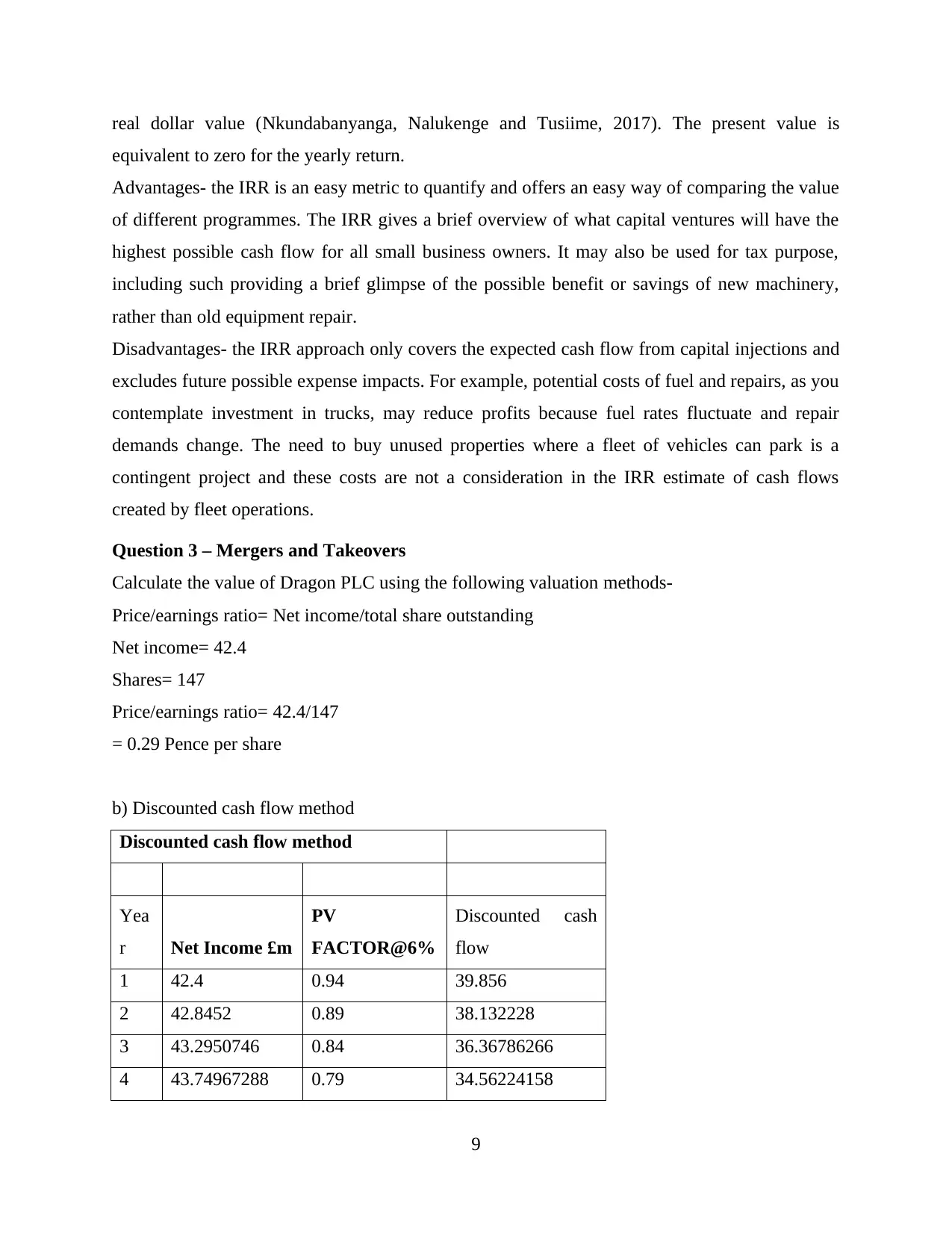

Question 3 – Mergers and Takeovers

Calculate the value of Dragon PLC using the following valuation methods-

Price/earnings ratio= Net income/total share outstanding

Net income= 42.4

Shares= 147

Price/earnings ratio= 42.4/147

= 0.29 Pence per share

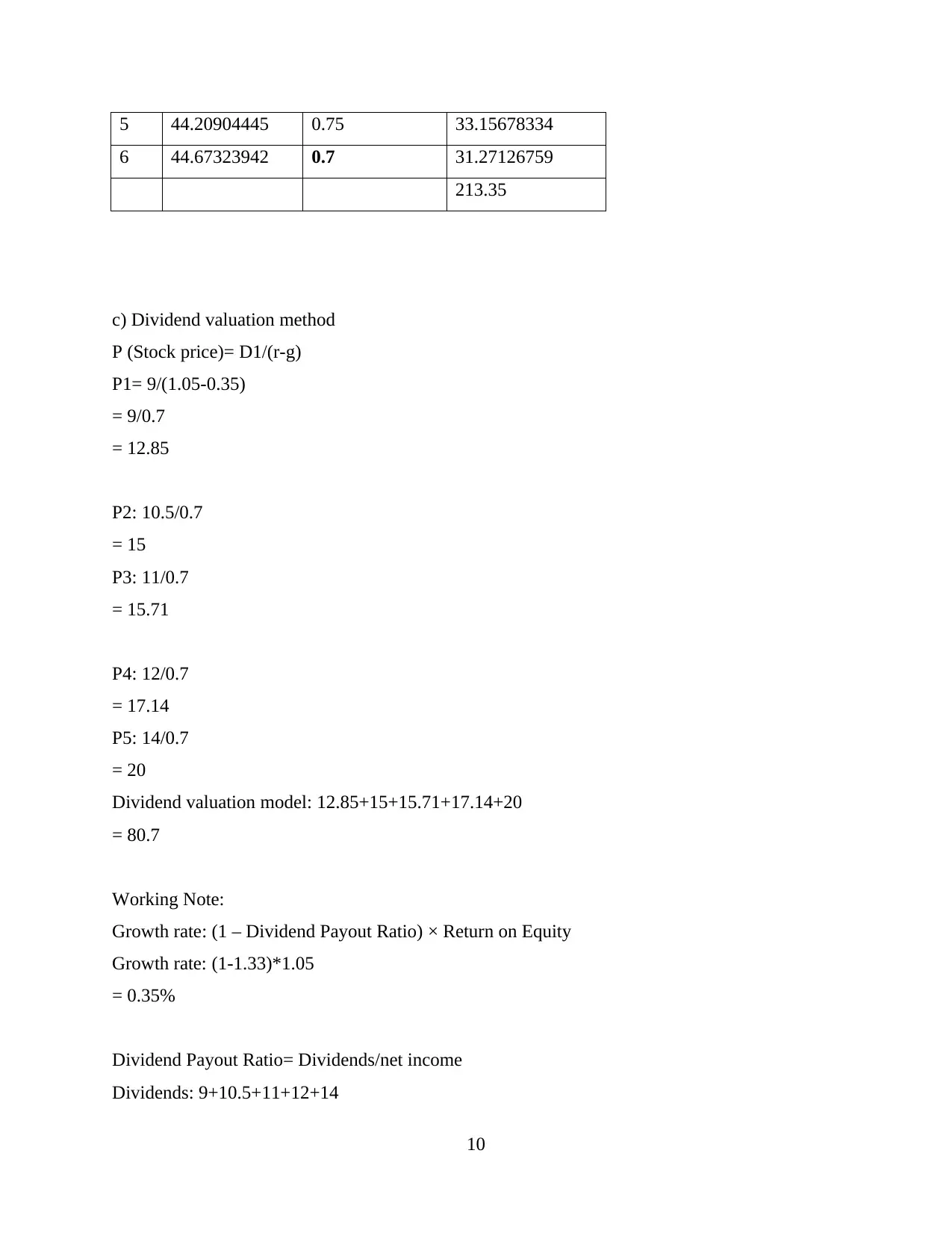

b) Discounted cash flow method

Discounted cash flow method

Yea

r Net Income £m

PV

FACTOR@6%

Discounted cash

flow

1 42.4 0.94 39.856

2 42.8452 0.89 38.132228

3 43.2950746 0.84 36.36786266

4 43.74967288 0.79 34.56224158

9

equivalent to zero for the yearly return.

Advantages- the IRR is an easy metric to quantify and offers an easy way of comparing the value

of different programmes. The IRR gives a brief overview of what capital ventures will have the

highest possible cash flow for all small business owners. It may also be used for tax purpose,

including such providing a brief glimpse of the possible benefit or savings of new machinery,

rather than old equipment repair.

Disadvantages- the IRR approach only covers the expected cash flow from capital injections and

excludes future possible expense impacts. For example, potential costs of fuel and repairs, as you

contemplate investment in trucks, may reduce profits because fuel rates fluctuate and repair

demands change. The need to buy unused properties where a fleet of vehicles can park is a

contingent project and these costs are not a consideration in the IRR estimate of cash flows

created by fleet operations.

Question 3 – Mergers and Takeovers

Calculate the value of Dragon PLC using the following valuation methods-

Price/earnings ratio= Net income/total share outstanding

Net income= 42.4

Shares= 147

Price/earnings ratio= 42.4/147

= 0.29 Pence per share

b) Discounted cash flow method

Discounted cash flow method

Yea

r Net Income £m

PV

FACTOR@6%

Discounted cash

flow

1 42.4 0.94 39.856

2 42.8452 0.89 38.132228

3 43.2950746 0.84 36.36786266

4 43.74967288 0.79 34.56224158

9

You're viewing a preview

Unlock full access by subscribing today!

5 44.20904445 0.75 33.15678334

6 44.67323942 0.7 31.27126759

213.35

c) Dividend valuation method

P (Stock price)= D1/(r-g)

P1= 9/(1.05-0.35)

= 9/0.7

= 12.85

P2: 10.5/0.7

= 15

P3: 11/0.7

= 15.71

P4: 12/0.7

= 17.14

P5: 14/0.7

= 20

Dividend valuation model: 12.85+15+15.71+17.14+20

= 80.7

Working Note:

Growth rate: (1 – Dividend Payout Ratio) × Return on Equity

Growth rate: (1-1.33)*1.05

= 0.35%

Dividend Payout Ratio= Dividends/net income

Dividends: 9+10.5+11+12+14

10

6 44.67323942 0.7 31.27126759

213.35

c) Dividend valuation method

P (Stock price)= D1/(r-g)

P1= 9/(1.05-0.35)

= 9/0.7

= 12.85

P2: 10.5/0.7

= 15

P3: 11/0.7

= 15.71

P4: 12/0.7

= 17.14

P5: 14/0.7

= 20

Dividend valuation model: 12.85+15+15.71+17.14+20

= 80.7

Working Note:

Growth rate: (1 – Dividend Payout Ratio) × Return on Equity

Growth rate: (1-1.33)*1.05

= 0.35%

Dividend Payout Ratio= Dividends/net income

Dividends: 9+10.5+11+12+14

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 56.5 Pence

= 56.5/42.4

= 1.33

(d) Critically discuss the problems associated with using the above valuation techniques.

Price earnings method- In large part, the P/E ratio is formed in respect to a single market share or

market average by the perceived optimism or negativity of the shareholders (Dwiastanti, 2017).

The explanation for this is that the value of the commodity is a crucial factor in the number (the

top part) and directly influences the ratio results. Since it is common sense, stock markets don't

just rationally adjust. Of course, the typical P/Es historically ranged between 10 and 25. (See

P/on E's the left for history Standard & Poor). Even so, the new web, also called dotcoms and

tech firms in the press and everyone in IT in particular.

Advantages-

It is easy to use and understand the greatest benefit of a P / E ratio. And those who do not receive

a financial background are able to recognise it even while it is just an extremely essential

instrument, it can be used to measure the value of an enterprise's securities. For the actual

valuation of the share, P/E is a far more meaningful way than the price alone. I will prove this

with an instance, to see this easier. A stock of 100 dollars with 10 dollars is so far more "cheap"

than an inventory of 10 dollars with 100 dollars. (Because the two shares belong to the same

industry). P/E is an outstanding instrument to measure both the overall industry and the rivals of

the given firm. The P/E therefore determines the real goals of the customer as another way to

compare. The company's share price tends to be higher if it is anticipated to remain good, thus

increasing P/E (Morozko and Didenko, 2018). The actual P/E of the business stocks can be

contrasted with the company's previous results. For instance, if the corporation's EPS has a

continuous growth (which implies each share produces an increasing amount of profit), yet the

Company's P / E appears to be stagnant and equivalent, which implies that the increase in the

stock market does not suit the increase in productivity of such shares.

Disadvantages-

The first concern is that the main reason for P/E is the subjective essence and "we don't know

how much we can sell in price. The irrational essence of stock markets can partly be certified.

The competitive shares are possibly best represented in the survey done in the Standard & Poor's

11

= 56.5/42.4

= 1.33

(d) Critically discuss the problems associated with using the above valuation techniques.

Price earnings method- In large part, the P/E ratio is formed in respect to a single market share or

market average by the perceived optimism or negativity of the shareholders (Dwiastanti, 2017).

The explanation for this is that the value of the commodity is a crucial factor in the number (the

top part) and directly influences the ratio results. Since it is common sense, stock markets don't

just rationally adjust. Of course, the typical P/Es historically ranged between 10 and 25. (See

P/on E's the left for history Standard & Poor). Even so, the new web, also called dotcoms and

tech firms in the press and everyone in IT in particular.

Advantages-

It is easy to use and understand the greatest benefit of a P / E ratio. And those who do not receive

a financial background are able to recognise it even while it is just an extremely essential

instrument, it can be used to measure the value of an enterprise's securities. For the actual

valuation of the share, P/E is a far more meaningful way than the price alone. I will prove this

with an instance, to see this easier. A stock of 100 dollars with 10 dollars is so far more "cheap"

than an inventory of 10 dollars with 100 dollars. (Because the two shares belong to the same

industry). P/E is an outstanding instrument to measure both the overall industry and the rivals of

the given firm. The P/E therefore determines the real goals of the customer as another way to

compare. The company's share price tends to be higher if it is anticipated to remain good, thus

increasing P/E (Morozko and Didenko, 2018). The actual P/E of the business stocks can be

contrasted with the company's previous results. For instance, if the corporation's EPS has a

continuous growth (which implies each share produces an increasing amount of profit), yet the

Company's P / E appears to be stagnant and equivalent, which implies that the increase in the

stock market does not suit the increase in productivity of such shares.

Disadvantages-

The first concern is that the main reason for P/E is the subjective essence and "we don't know

how much we can sell in price. The irrational essence of stock markets can partly be certified.

The competitive shares are possibly best represented in the survey done in the Standard & Poor's

11

500 or S&P500 index by Kevin P. Coyne and Jonathan W. Witter that now the 40 to 100 most

actively involved investors in a certain corporate account for over 50% of the total trading

volume.

Where market and economic conditions are favourable, investors appear to over-price equity,

raising P/E to a degree which, financially speaking, does not explain the business information.

This might spark a boom, which is considered a bubble, because rates and P/Es are so strong it

will burst or plunge sharply at any moment. This happened with the IT sector in the early and

mid 1990s, particularly internet, securities. It is also possible for the economy and the world of

industry to be looked at inferior to the fact that the P/Es, such as in global recessions, are

underestimated by securities and equity stocks. Regions are still overvalued in terms of P/E,

according to real financial results of the region's greatest firms. Such a sub-P/E-region is Central

and Eastern Europe.

Discounted cash flow method- The quality of an investment potential is calculated with a

discounted cash flow (DCF). DCF analyses use projected free flow estimates and discounts them

to achieve a current valuation that assesses the opportunity for profit often during proper

research, (most often using weighted average capital cost). The incentive could be nice if the

benefit achieved by DCF analysis is greater than the actual investment costs. Discounted cash

flow Assessment is dependent on the company's estimated potential cash flow, which is the

calculation of the company's overall risk and its corresponding discount rate (Bai, Liu and Tang,

2017). This strategy is easier to implement for money, companies, etc. whose free cash flow are

actually positive and are projected to be with some stability and where a risk substitute to receive

discounts is possible because of these required conditions for DCF assessment. The further we

move from this idealised setting, the more challenging and less accurate DCF assessment is.

Advantages-

DCF Assessment captures the main factors behind a company (cost of equity, weighted average

cost of capital, growth rate, re-investment rate, etc.). Therefore, the worth of the asset/business is

estimated as near as possible. DCF depends on Free Cash Flows, contrary to most valuations.

Free Cash Flows (FCFs) are to a greater degree a valid means of eliminating the arbitrary

accounts policy and window dressing of recorded earnings. If an outlay of cash is classified in

12

actively involved investors in a certain corporate account for over 50% of the total trading

volume.

Where market and economic conditions are favourable, investors appear to over-price equity,

raising P/E to a degree which, financially speaking, does not explain the business information.

This might spark a boom, which is considered a bubble, because rates and P/Es are so strong it

will burst or plunge sharply at any moment. This happened with the IT sector in the early and

mid 1990s, particularly internet, securities. It is also possible for the economy and the world of

industry to be looked at inferior to the fact that the P/Es, such as in global recessions, are

underestimated by securities and equity stocks. Regions are still overvalued in terms of P/E,

according to real financial results of the region's greatest firms. Such a sub-P/E-region is Central

and Eastern Europe.

Discounted cash flow method- The quality of an investment potential is calculated with a

discounted cash flow (DCF). DCF analyses use projected free flow estimates and discounts them

to achieve a current valuation that assesses the opportunity for profit often during proper

research, (most often using weighted average capital cost). The incentive could be nice if the

benefit achieved by DCF analysis is greater than the actual investment costs. Discounted cash

flow Assessment is dependent on the company's estimated potential cash flow, which is the

calculation of the company's overall risk and its corresponding discount rate (Bai, Liu and Tang,

2017). This strategy is easier to implement for money, companies, etc. whose free cash flow are

actually positive and are projected to be with some stability and where a risk substitute to receive

discounts is possible because of these required conditions for DCF assessment. The further we

move from this idealised setting, the more challenging and less accurate DCF assessment is.

Advantages-

DCF Assessment captures the main factors behind a company (cost of equity, weighted average

cost of capital, growth rate, re-investment rate, etc.). Therefore, the worth of the asset/business is

estimated as near as possible. DCF depends on Free Cash Flows, contrary to most valuations.

Free Cash Flows (FCFs) are to a greater degree a valid means of eliminating the arbitrary

accounts policy and window dressing of recorded earnings. If an outlay of cash is classified in

12

You're viewing a preview

Unlock full access by subscribing today!

P&L as a cost of operation or capitalised into a balance sheet asset, FCF is a real reflection of

investment money.

Disadvantages-

DCF Valuation is very vulnerable to constant growth and sales price assumptions. Every little

tweak every now and then and DCF evaluation will wildly vary wildly and the fair value will not

be right (Yang, Ishtiaq and Anwar, 2018). It just works well if the potential cash flows rely

heavily on it. Although if the activities of the firm are not visible, revenue, operating and capital

spending cannot be predicted for sure. While it is difficult to predict cash flow in the next few

years, it becomes almost impossible to drive them away permanently (required for DCF

assessment). As a result, if not adequately accounted for, DCF is vulnerable to errors.

Dividend valuation method- The first category of discounted cash flow model we are studying is

the Dividend valuation method. Like every other DCF model, the model essentially reduces cash

flows at a regular price. The distinction is that the formulas of the dividend reduction still regard

"dividends" as valid cash flows.

Advantages- The main benefit of the discount model for dividends is the principle that it is

based. The reasoning is straightforward. A company is an ongoing body. When an investor buys

the share of the company, he or she pays a price today that gives him or her the right to profit

from all the dividends that the company pays over its lifespan. The valuation of the company is

essentially that of a continuous supply of returns, which the purchaser expects to obtain later

over time. Many observers therefore conclude that this model has no subjectivity and the

reasoning is crystalline.

Disadvantages- The model applies only to mature and profitable firms that have an established

record of regularly paying dividends. While it might seem like a positive idea, prima facie, there

is a big deal. Investors who invest only in mature, profitable firms appear to lack fast growth.

13

investment money.

Disadvantages-

DCF Valuation is very vulnerable to constant growth and sales price assumptions. Every little

tweak every now and then and DCF evaluation will wildly vary wildly and the fair value will not

be right (Yang, Ishtiaq and Anwar, 2018). It just works well if the potential cash flows rely

heavily on it. Although if the activities of the firm are not visible, revenue, operating and capital

spending cannot be predicted for sure. While it is difficult to predict cash flow in the next few

years, it becomes almost impossible to drive them away permanently (required for DCF

assessment). As a result, if not adequately accounted for, DCF is vulnerable to errors.

Dividend valuation method- The first category of discounted cash flow model we are studying is

the Dividend valuation method. Like every other DCF model, the model essentially reduces cash

flows at a regular price. The distinction is that the formulas of the dividend reduction still regard

"dividends" as valid cash flows.

Advantages- The main benefit of the discount model for dividends is the principle that it is

based. The reasoning is straightforward. A company is an ongoing body. When an investor buys

the share of the company, he or she pays a price today that gives him or her the right to profit

from all the dividends that the company pays over its lifespan. The valuation of the company is

essentially that of a continuous supply of returns, which the purchaser expects to obtain later

over time. Many observers therefore conclude that this model has no subjectivity and the

reasoning is crystalline.

Disadvantages- The model applies only to mature and profitable firms that have an established

record of regularly paying dividends. While it might seem like a positive idea, prima facie, there

is a big deal. Investors who invest only in mature, profitable firms appear to lack fast growth.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Prihartono, M.R.D. and Asandimitra, N., 2018. Analysis factors influencing financial

management behaviour. International Journal of Academic Research in Business and

Social Sciences, 8(8), pp.308-326.

Jones, C., Finkler, S.A., Kovner, C.T. and Mose, J., 2018. Financial Management for Nurse

Managers and Executives-E-Book. Elsevier Health Sciences.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: policies and practices. John Wiley & Sons.

Loke, Y.J., 2017. The influence of socio-demographic and financial knowledge factors on

financial management practices of Malaysians. International Journal of Business and

Society, 18(1).

Nowicki, M., 2018. Introduction to the financial management of healthcare organizations.

Health Administration Press, Chicago, Illinois.

Ward, A.M. and Forker, J., 2017. Financial management effectiveness and board gender

diversity in member-governed, community financial institutions. Journal of business

ethics, 141(2), pp.351-366.

Mitchell, G.E., 2017. Fiscal leanness and fiscal responsiveness: Exploring the normative limits

of strategic nonprofit financial management. Administration & Society, 49(9), pp.1272-

1296.

Nkundabanyanga, S.K., Akankunda, B., Nalukenge, I. and Tusiime, I., 2017. The impact of

financial management practices and competitive advantage on the loan performance of

MFIs. International Journal of Social Economics.

Dwiastanti, A., 2017. Analysis of financial knowledge and financial attitude on locus of control

and financial management behavior. MBR (Management and Business Review), 1(1),

pp.1-8.

Morozko, N. and Didenko, V., 2018. Financial management of small organizations based on a

cognitive approach.

Bai, Y., Gu, C., Chen, Q., Xiao, J., Liu, D. and Tang, S., 2017. The challenges that head nurses

confront on financial management today: A qualitative study. International journal of

nursing sciences, 4(2), pp.122-127.

Yang, S., Ishtiaq, M. and Anwar, M., 2018. Enterprise risk management practices and firm

performance, the mediating role of competitive advantage and the moderating role of

financial literacy. Journal of Risk and Financial Management, 11(3), p.35.

14

Prihartono, M.R.D. and Asandimitra, N., 2018. Analysis factors influencing financial

management behaviour. International Journal of Academic Research in Business and

Social Sciences, 8(8), pp.308-326.

Jones, C., Finkler, S.A., Kovner, C.T. and Mose, J., 2018. Financial Management for Nurse

Managers and Executives-E-Book. Elsevier Health Sciences.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: policies and practices. John Wiley & Sons.

Loke, Y.J., 2017. The influence of socio-demographic and financial knowledge factors on

financial management practices of Malaysians. International Journal of Business and

Society, 18(1).

Nowicki, M., 2018. Introduction to the financial management of healthcare organizations.

Health Administration Press, Chicago, Illinois.

Ward, A.M. and Forker, J., 2017. Financial management effectiveness and board gender

diversity in member-governed, community financial institutions. Journal of business

ethics, 141(2), pp.351-366.

Mitchell, G.E., 2017. Fiscal leanness and fiscal responsiveness: Exploring the normative limits

of strategic nonprofit financial management. Administration & Society, 49(9), pp.1272-

1296.

Nkundabanyanga, S.K., Akankunda, B., Nalukenge, I. and Tusiime, I., 2017. The impact of

financial management practices and competitive advantage on the loan performance of

MFIs. International Journal of Social Economics.

Dwiastanti, A., 2017. Analysis of financial knowledge and financial attitude on locus of control

and financial management behavior. MBR (Management and Business Review), 1(1),

pp.1-8.

Morozko, N. and Didenko, V., 2018. Financial management of small organizations based on a

cognitive approach.

Bai, Y., Gu, C., Chen, Q., Xiao, J., Liu, D. and Tang, S., 2017. The challenges that head nurses

confront on financial management today: A qualitative study. International journal of

nursing sciences, 4(2), pp.122-127.

Yang, S., Ishtiaq, M. and Anwar, M., 2018. Enterprise risk management practices and firm

performance, the mediating role of competitive advantage and the moderating role of

financial literacy. Journal of Risk and Financial Management, 11(3), p.35.

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.