Financial Management Analysis of Jurys Inn Hotel Performance

VerifiedAdded on 2023/06/13

|11

|2735

|141

Report

AI Summary

This report provides a comprehensive financial management analysis of Jurys Inn, a hospitality firm operating in Great Britain and Northern England, focusing on its fiscal efficiency through ratio analysis. It evaluates profitability, sustainability (liquidity), and gearing ratios for the years 2019 and 2020, identifying unfavorable trends in revenue and financial condition, alongside increasing leverage. The report discusses the importance of understanding financial ratios for hospitality administration, including their role in planning, decision-making, assessing long-term solvency, profitability, operational effectiveness, and cost control. It also addresses the advantages and drawbacks of accounting ratios as a decision-making tool, highlighting their limitations due to descriptive approaches, accounting standards variations, and reliance on historical data. The analysis concludes that Jurys Inn's financial performance is deteriorating, necessitating improvements in daily operations and financial management strategies; students can find similar solved assignments and study resources on Desklib.

Financial Management

for the Hotel Industry

for the Hotel Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Evaluation of fiscal efficiency.....................................................................................................1

The importance of comprehending ratios and their variations for hospitality administration is

discussed......................................................................................................................................4

Addressing the advantages and drawbacks of accounting ratios as a decision-making tool.......5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Evaluation of fiscal efficiency.....................................................................................................1

The importance of comprehending ratios and their variations for hospitality administration is

discussed......................................................................................................................................4

Addressing the advantages and drawbacks of accounting ratios as a decision-making tool.......5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Stakeholders are far more convinced by monetary statements. The statements will be

analysed in a range of methods, including accounting ratios, peer-to-peer assessment, year-over-

year evaluation, and inter-departmental interpretation, among others (Firouzjah, 2018).

Proportion assessment is the most common methodological approach. As a Jurys Inn auditor, I

have received charged with providing information for the administration in order to conduct

these accounting ratios. Jurys Inn is a hospitality firm operating in the Great Britain and Northern

England. The firm's current operations have actually taken a sour turn. As a result, the analysis

includes the fiscal success of it and that too in an effective and efficient manner.

MAIN BODY

Evaluation of fiscal efficiency

Monetary effectiveness assessment can be performed in a variety of methods. Proportion

assessment is a fiscal account analytical technique that takes into account various comparisons

for various monetary data. The metrics are the proportional connections between diverse

accounting elements, in which every proportion is calculated as a fraction of the others. Liquidity

position, viability position, engagement proportions, gearing metrics, and leverage percentage

are the five categories of these metrics. Accessibility metrics are a measure of a company's

capacity to repay relatively brief liabilities. Solvency metrics are a measure of a company's

capacity to discharge protracted liabilities (Higgins and Cornwell, 2016). Productivity

percentages are a measure of how efficiently a business uses its operational resources. Gearing

metrics are financial leveraging statistics that reveal the proportion of leveraged in a statement of

financial position as well as its capacity to service debt. Productivity metrics are revenue

representation percentages for various monetary elements like selling, assets, and capital, among

others.

Computing appropriate ratios, debating observed patterns, and deriving conclusions from

analytics of the Jurys Inn

Profitability Ratios 2019 2020 Trend

Gross profit margin 93% 86% -7%

Net profit margin 70% 60% -10%

Return on capital employed 59% 57% -2%

Stakeholders are far more convinced by monetary statements. The statements will be

analysed in a range of methods, including accounting ratios, peer-to-peer assessment, year-over-

year evaluation, and inter-departmental interpretation, among others (Firouzjah, 2018).

Proportion assessment is the most common methodological approach. As a Jurys Inn auditor, I

have received charged with providing information for the administration in order to conduct

these accounting ratios. Jurys Inn is a hospitality firm operating in the Great Britain and Northern

England. The firm's current operations have actually taken a sour turn. As a result, the analysis

includes the fiscal success of it and that too in an effective and efficient manner.

MAIN BODY

Evaluation of fiscal efficiency

Monetary effectiveness assessment can be performed in a variety of methods. Proportion

assessment is a fiscal account analytical technique that takes into account various comparisons

for various monetary data. The metrics are the proportional connections between diverse

accounting elements, in which every proportion is calculated as a fraction of the others. Liquidity

position, viability position, engagement proportions, gearing metrics, and leverage percentage

are the five categories of these metrics. Accessibility metrics are a measure of a company's

capacity to repay relatively brief liabilities. Solvency metrics are a measure of a company's

capacity to discharge protracted liabilities (Higgins and Cornwell, 2016). Productivity

percentages are a measure of how efficiently a business uses its operational resources. Gearing

metrics are financial leveraging statistics that reveal the proportion of leveraged in a statement of

financial position as well as its capacity to service debt. Productivity metrics are revenue

representation percentages for various monetary elements like selling, assets, and capital, among

others.

Computing appropriate ratios, debating observed patterns, and deriving conclusions from

analytics of the Jurys Inn

Profitability Ratios 2019 2020 Trend

Gross profit margin 93% 86% -7%

Net profit margin 70% 60% -10%

Return on capital employed 59% 57% -2%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

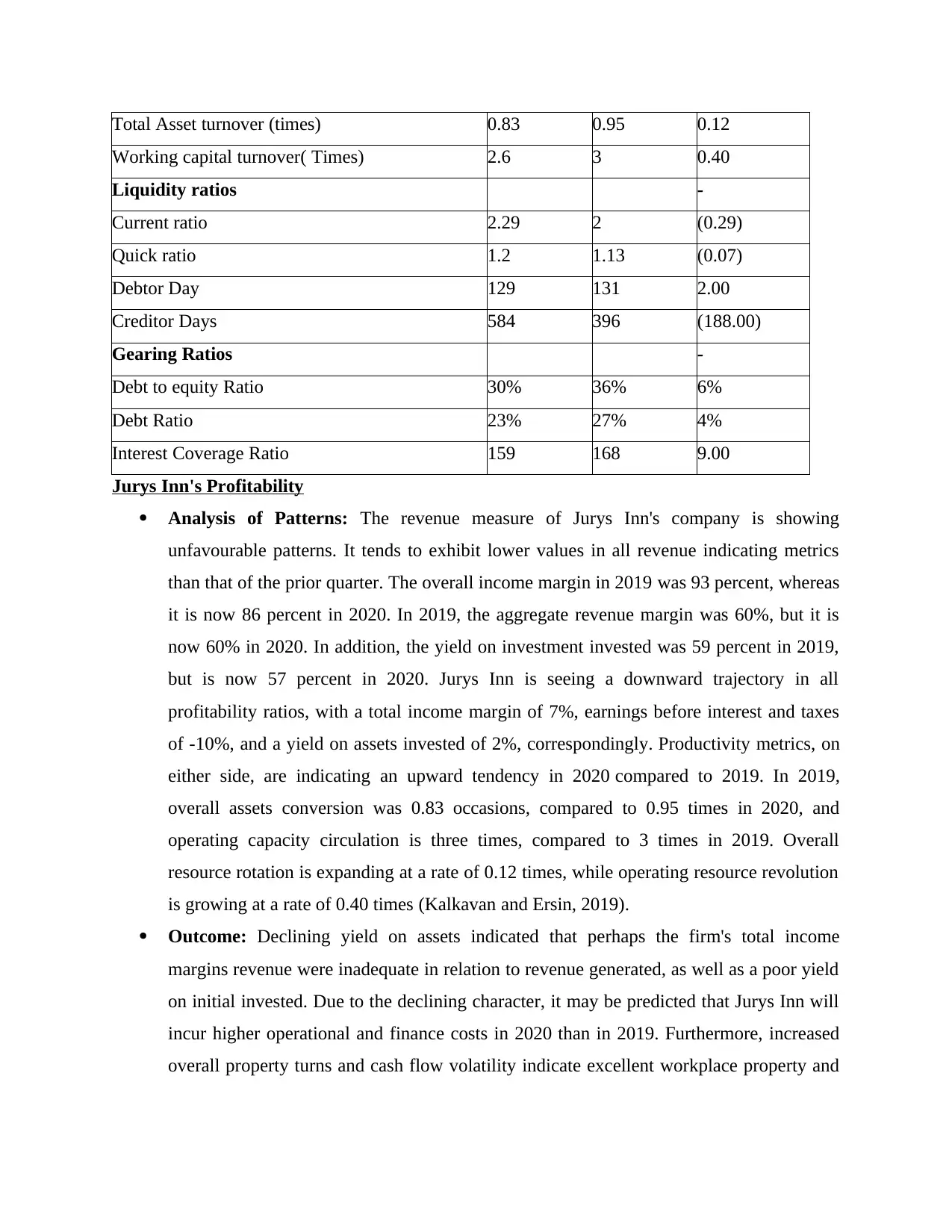

Total Asset turnover (times) 0.83 0.95 0.12

Working capital turnover( Times) 2.6 3 0.40

Liquidity ratios -

Current ratio 2.29 2 (0.29)

Quick ratio 1.2 1.13 (0.07)

Debtor Day 129 131 2.00

Creditor Days 584 396 (188.00)

Gearing Ratios -

Debt to equity Ratio 30% 36% 6%

Debt Ratio 23% 27% 4%

Interest Coverage Ratio 159 168 9.00

Jurys Inn's Profitability

Analysis of Patterns: The revenue measure of Jurys Inn's company is showing

unfavourable patterns. It tends to exhibit lower values in all revenue indicating metrics

than that of the prior quarter. The overall income margin in 2019 was 93 percent, whereas

it is now 86 percent in 2020. In 2019, the aggregate revenue margin was 60%, but it is

now 60% in 2020. In addition, the yield on investment invested was 59 percent in 2019,

but is now 57 percent in 2020. Jurys Inn is seeing a downward trajectory in all

profitability ratios, with a total income margin of 7%, earnings before interest and taxes

of -10%, and a yield on assets invested of 2%, correspondingly. Productivity metrics, on

either side, are indicating an upward tendency in 2020 compared to 2019. In 2019,

overall assets conversion was 0.83 occasions, compared to 0.95 times in 2020, and

operating capacity circulation is three times, compared to 3 times in 2019. Overall

resource rotation is expanding at a rate of 0.12 times, while operating resource revolution

is growing at a rate of 0.40 times (Kalkavan and Ersin, 2019).

Outcome: Declining yield on assets indicated that perhaps the firm's total income

margins revenue were inadequate in relation to revenue generated, as well as a poor yield

on initial invested. Due to the declining character, it may be predicted that Jurys Inn will

incur higher operational and finance costs in 2020 than in 2019. Furthermore, increased

overall property turns and cash flow volatility indicate excellent workplace property and

Working capital turnover( Times) 2.6 3 0.40

Liquidity ratios -

Current ratio 2.29 2 (0.29)

Quick ratio 1.2 1.13 (0.07)

Debtor Day 129 131 2.00

Creditor Days 584 396 (188.00)

Gearing Ratios -

Debt to equity Ratio 30% 36% 6%

Debt Ratio 23% 27% 4%

Interest Coverage Ratio 159 168 9.00

Jurys Inn's Profitability

Analysis of Patterns: The revenue measure of Jurys Inn's company is showing

unfavourable patterns. It tends to exhibit lower values in all revenue indicating metrics

than that of the prior quarter. The overall income margin in 2019 was 93 percent, whereas

it is now 86 percent in 2020. In 2019, the aggregate revenue margin was 60%, but it is

now 60% in 2020. In addition, the yield on investment invested was 59 percent in 2019,

but is now 57 percent in 2020. Jurys Inn is seeing a downward trajectory in all

profitability ratios, with a total income margin of 7%, earnings before interest and taxes

of -10%, and a yield on assets invested of 2%, correspondingly. Productivity metrics, on

either side, are indicating an upward tendency in 2020 compared to 2019. In 2019,

overall assets conversion was 0.83 occasions, compared to 0.95 times in 2020, and

operating capacity circulation is three times, compared to 3 times in 2019. Overall

resource rotation is expanding at a rate of 0.12 times, while operating resource revolution

is growing at a rate of 0.40 times (Kalkavan and Ersin, 2019).

Outcome: Declining yield on assets indicated that perhaps the firm's total income

margins revenue were inadequate in relation to revenue generated, as well as a poor yield

on initial invested. Due to the declining character, it may be predicted that Jurys Inn will

incur higher operational and finance costs in 2020 than in 2019. Furthermore, increased

overall property turns and cash flow volatility indicate excellent workplace property and

operating resource administration. As a result, revenue usually increases, although not

much. The rise in operational costs is to blame for the drop in revenue.

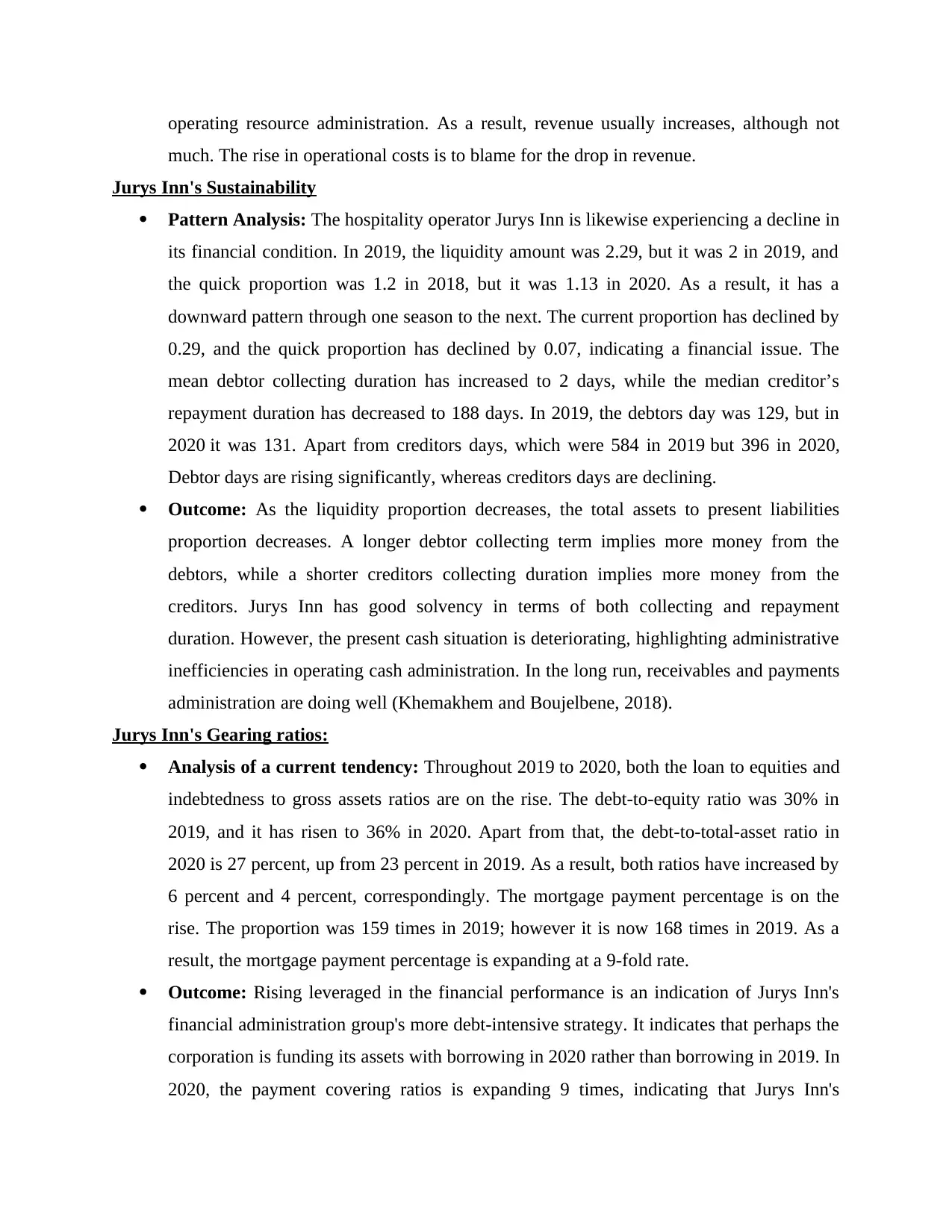

Jurys Inn's Sustainability

Pattern Analysis: The hospitality operator Jurys Inn is likewise experiencing a decline in

its financial condition. In 2019, the liquidity amount was 2.29, but it was 2 in 2019, and

the quick proportion was 1.2 in 2018, but it was 1.13 in 2020. As a result, it has a

downward pattern through one season to the next. The current proportion has declined by

0.29, and the quick proportion has declined by 0.07, indicating a financial issue. The

mean debtor collecting duration has increased to 2 days, while the median creditor’s

repayment duration has decreased to 188 days. In 2019, the debtors day was 129, but in

2020 it was 131. Apart from creditors days, which were 584 in 2019 but 396 in 2020,

Debtor days are rising significantly, whereas creditors days are declining.

Outcome: As the liquidity proportion decreases, the total assets to present liabilities

proportion decreases. A longer debtor collecting term implies more money from the

debtors, while a shorter creditors collecting duration implies more money from the

creditors. Jurys Inn has good solvency in terms of both collecting and repayment

duration. However, the present cash situation is deteriorating, highlighting administrative

inefficiencies in operating cash administration. In the long run, receivables and payments

administration are doing well (Khemakhem and Boujelbene, 2018).

Jurys Inn's Gearing ratios:

Analysis of a current tendency: Throughout 2019 to 2020, both the loan to equities and

indebtedness to gross assets ratios are on the rise. The debt-to-equity ratio was 30% in

2019, and it has risen to 36% in 2020. Apart from that, the debt-to-total-asset ratio in

2020 is 27 percent, up from 23 percent in 2019. As a result, both ratios have increased by

6 percent and 4 percent, correspondingly. The mortgage payment percentage is on the

rise. The proportion was 159 times in 2019; however it is now 168 times in 2019. As a

result, the mortgage payment percentage is expanding at a 9-fold rate.

Outcome: Rising leveraged in the financial performance is an indication of Jurys Inn's

financial administration group's more debt-intensive strategy. It indicates that perhaps the

corporation is funding its assets with borrowing in 2020 rather than borrowing in 2019. In

2020, the payment covering ratios is expanding 9 times, indicating that Jurys Inn's

much. The rise in operational costs is to blame for the drop in revenue.

Jurys Inn's Sustainability

Pattern Analysis: The hospitality operator Jurys Inn is likewise experiencing a decline in

its financial condition. In 2019, the liquidity amount was 2.29, but it was 2 in 2019, and

the quick proportion was 1.2 in 2018, but it was 1.13 in 2020. As a result, it has a

downward pattern through one season to the next. The current proportion has declined by

0.29, and the quick proportion has declined by 0.07, indicating a financial issue. The

mean debtor collecting duration has increased to 2 days, while the median creditor’s

repayment duration has decreased to 188 days. In 2019, the debtors day was 129, but in

2020 it was 131. Apart from creditors days, which were 584 in 2019 but 396 in 2020,

Debtor days are rising significantly, whereas creditors days are declining.

Outcome: As the liquidity proportion decreases, the total assets to present liabilities

proportion decreases. A longer debtor collecting term implies more money from the

debtors, while a shorter creditors collecting duration implies more money from the

creditors. Jurys Inn has good solvency in terms of both collecting and repayment

duration. However, the present cash situation is deteriorating, highlighting administrative

inefficiencies in operating cash administration. In the long run, receivables and payments

administration are doing well (Khemakhem and Boujelbene, 2018).

Jurys Inn's Gearing ratios:

Analysis of a current tendency: Throughout 2019 to 2020, both the loan to equities and

indebtedness to gross assets ratios are on the rise. The debt-to-equity ratio was 30% in

2019, and it has risen to 36% in 2020. Apart from that, the debt-to-total-asset ratio in

2020 is 27 percent, up from 23 percent in 2019. As a result, both ratios have increased by

6 percent and 4 percent, correspondingly. The mortgage payment percentage is on the

rise. The proportion was 159 times in 2019; however it is now 168 times in 2019. As a

result, the mortgage payment percentage is expanding at a 9-fold rate.

Outcome: Rising leveraged in the financial performance is an indication of Jurys Inn's

financial administration group's more debt-intensive strategy. It indicates that perhaps the

corporation is funding its assets with borrowing in 2020 rather than borrowing in 2019. In

2020, the payment covering ratios is expanding 9 times, indicating that Jurys Inn's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

indebtedness managing is strong and that revenue generation for loan payment is also

acceptable.

Upon examining the statistics, it could be concluded that Jurys Inn's financial condition is

deteriorating, and its revenue is deteriorating as well, yet its leveraging is growing. As a result,

Jurys Inn administration must be more concerned with daily operations.

The importance of comprehending ratios and their variations for hospitality administration is

discussed

Understanding the profitability statements and their variation is critical when examining the

data found in the fiscal statements of Hospitality operations. These sorts of monetary data, as

well as the significance of profitability metrics in comprehending them, could be explained in

this section:

Upcoming planning and scheduling: Hospitality administration's fiscal outcomes'

increasing tendency Jurys Inn, for example, assists businesses in developing operating

and economic plans for their operational plans. The current fiscal outcomes' mindset lays

the path for statistical prediction of prospective price accounting, cash requirements, and

bankruptcy position. For a business such as Jurys Inn, a liquidity ratios for all those

monetary data is critical.

Taking a Decision: Borrowing decisions, sources of finance, capital markets, and a

plethora of other management decisions would be simple if the quantitative statements

underlying such decisions is analysed by cross-departmental and cross-business peers. As

a result, proportion assessment is useful in this situation (Liu, Liu and Chen, 2017).

Long term solvency: The capacity to afford protracted obligations and the consequence

of long-term liabilities is an income report enhancing knowledge. The hospitality

administration firm's lending capability and solvency position project a favourable

reputation if the hospitality administration firm, such as Jurys Inn, pays long-term

obligations on time. The accountants and shareholder would be capable of assessing the

hospitality firm's long-term viability situation by comprehending the ratios and doing a

quantitative statements.

Profitability: The viability of a hospitality administration firm, such as Jurys Inn, is

measured in the fiscal account. The competence of a corporation to generate revenue is

determined through a comparative review of multiple revenue indicating metrics. The

acceptable.

Upon examining the statistics, it could be concluded that Jurys Inn's financial condition is

deteriorating, and its revenue is deteriorating as well, yet its leveraging is growing. As a result,

Jurys Inn administration must be more concerned with daily operations.

The importance of comprehending ratios and their variations for hospitality administration is

discussed

Understanding the profitability statements and their variation is critical when examining the

data found in the fiscal statements of Hospitality operations. These sorts of monetary data, as

well as the significance of profitability metrics in comprehending them, could be explained in

this section:

Upcoming planning and scheduling: Hospitality administration's fiscal outcomes'

increasing tendency Jurys Inn, for example, assists businesses in developing operating

and economic plans for their operational plans. The current fiscal outcomes' mindset lays

the path for statistical prediction of prospective price accounting, cash requirements, and

bankruptcy position. For a business such as Jurys Inn, a liquidity ratios for all those

monetary data is critical.

Taking a Decision: Borrowing decisions, sources of finance, capital markets, and a

plethora of other management decisions would be simple if the quantitative statements

underlying such decisions is analysed by cross-departmental and cross-business peers. As

a result, proportion assessment is useful in this situation (Liu, Liu and Chen, 2017).

Long term solvency: The capacity to afford protracted obligations and the consequence

of long-term liabilities is an income report enhancing knowledge. The hospitality

administration firm's lending capability and solvency position project a favourable

reputation if the hospitality administration firm, such as Jurys Inn, pays long-term

obligations on time. The accountants and shareholder would be capable of assessing the

hospitality firm's long-term viability situation by comprehending the ratios and doing a

quantitative statements.

Profitability: The viability of a hospitality administration firm, such as Jurys Inn, is

measured in the fiscal account. The competence of a corporation to generate revenue is

determined through a comparative review of multiple revenue indicating metrics. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fiscal assessment of the earnings per shares of the company and the debt covering

proportion would also reveal payout and debt repayment capability. As a result, the

proportion evaluation is crucial.

Effectiveness of operation: It is necessary to assess the annual accounts, particularly via

proportion assessment, in order to determine the company's operational performance and

the use of various commodities. Various operational percentages indicate various levels

of capacity utilization in the use of working capital. As a result, comparative evaluation is

critical.

Controlling costs and expenses: Various price structures and spending types would be

clarified by comparing ratios from various periods and companies in the hospitality

sector. The concealed arrangement price is defined from the comparison and proportional

evaluation of the finance report. So, if the profitability ratios data is brought into account

in the decision-making procedure, controlling and managing similar costs and

expenditures will be simple (Nindito, 2018).

Liquidity position: An inn's financial condition is critical for meeting relatively brief

obligations. If company are more liquid assets than accessible liabilities, the financial

condition would be good. Aside from that, a much less common source of finance would

leave a weaker posture in fulfilling relatively brief obligations. The extent of this stake

held by any hospitality administration firm could be determined by calculating and

assessing the business's solvency metrics.

Addressing the advantages and drawbacks of accounting ratios as a decision-making tool

The below are some of the advantages of accounting ratios:

If the proportion of monetary statistics provides a clear picture of fiscal activities,

productivity evaluation and compensation system reform may be possible.

Various budgets for company operations are created based on prospective requirements if

Jurys Inn's proportion assessment provides ready-to-use data for budgeting.

Finance proportion assessment would simplify the entire strategic and non-financial

status and outcomes.

A finance data recipient could streamline the connection between multiple bookkeeping

data and outcomes by employing various proportions (Shelton, Smith and Panisch, 2019).

proportion would also reveal payout and debt repayment capability. As a result, the

proportion evaluation is crucial.

Effectiveness of operation: It is necessary to assess the annual accounts, particularly via

proportion assessment, in order to determine the company's operational performance and

the use of various commodities. Various operational percentages indicate various levels

of capacity utilization in the use of working capital. As a result, comparative evaluation is

critical.

Controlling costs and expenses: Various price structures and spending types would be

clarified by comparing ratios from various periods and companies in the hospitality

sector. The concealed arrangement price is defined from the comparison and proportional

evaluation of the finance report. So, if the profitability ratios data is brought into account

in the decision-making procedure, controlling and managing similar costs and

expenditures will be simple (Nindito, 2018).

Liquidity position: An inn's financial condition is critical for meeting relatively brief

obligations. If company are more liquid assets than accessible liabilities, the financial

condition would be good. Aside from that, a much less common source of finance would

leave a weaker posture in fulfilling relatively brief obligations. The extent of this stake

held by any hospitality administration firm could be determined by calculating and

assessing the business's solvency metrics.

Addressing the advantages and drawbacks of accounting ratios as a decision-making tool

The below are some of the advantages of accounting ratios:

If the proportion of monetary statistics provides a clear picture of fiscal activities,

productivity evaluation and compensation system reform may be possible.

Various budgets for company operations are created based on prospective requirements if

Jurys Inn's proportion assessment provides ready-to-use data for budgeting.

Finance proportion assessment would simplify the entire strategic and non-financial

status and outcomes.

A finance data recipient could streamline the connection between multiple bookkeeping

data and outcomes by employing various proportions (Shelton, Smith and Panisch, 2019).

Understanding diverse accounting metrics and fiscal statistics allows the business

authorities of a hospitality administration firm like Jurys Inn to undertake necessary

action to address the firm's unhealthy conduct.

Ratio assessment constraints:

Accounting ratios is restricted in scope of statistical research due to its descriptive

approach. However, the proportion result could be influenced by a number of crucial

quantitative aspects. If the total asset consists primarily of outmoded goods, a high

present proportion might not even indicate a healthy company.

Additional limits of accounting ratios include a variety of elements like item and property

market prices, seasonality challenges in the firm, company's front attired conduct, and so

forth. Furthermore, the income report has restrictions that influence accounting ratios.

Monetary knowledge has intrinsic limitations because it is created by violating various

accountancy standards and ethical elements. As a result, the generating reports have

certain obvious limitations. As a result, such limitations of the accountancy restriction

directly affect bookkeeping ratios (Tumataroa and O'Hare, 2019).

Separate fiscal principles, like amortization strategy, stock measurement strategy, and so

forth, are 3 distinct accountancy rules and standards. The disparity between practices in

various organisations makes comparison assessment extremely difficult, if not

unattainable.

Monetary insight is primarily based on previous facts and understanding. As a result, the

proportion determines generally followed historical patterns. Proportion evaluation does

not allow for prospective reliability.

CONCLUSION

It can be concluded from the above that the fiscal result of Jurys Inn has revealed certain

areas that need to be improved and maintained. The suggestions for such concerns are that

operating costs and expenditures must be tracked and managed while non-operational/financial

expenses must not be prioritised because they are backed up by a lot greater revenue. The

administration of payables and receivables is excellent. By providing adequate intensive service

to such customers, capitalised advantage from kindness can be obtained. Revenue must be

enhanced by implementing a well-thought-out item marketing strategy in tandem with cost-

cutting measures. The loan servicing and leveraging processes must be paid greater emphasis as

authorities of a hospitality administration firm like Jurys Inn to undertake necessary

action to address the firm's unhealthy conduct.

Ratio assessment constraints:

Accounting ratios is restricted in scope of statistical research due to its descriptive

approach. However, the proportion result could be influenced by a number of crucial

quantitative aspects. If the total asset consists primarily of outmoded goods, a high

present proportion might not even indicate a healthy company.

Additional limits of accounting ratios include a variety of elements like item and property

market prices, seasonality challenges in the firm, company's front attired conduct, and so

forth. Furthermore, the income report has restrictions that influence accounting ratios.

Monetary knowledge has intrinsic limitations because it is created by violating various

accountancy standards and ethical elements. As a result, the generating reports have

certain obvious limitations. As a result, such limitations of the accountancy restriction

directly affect bookkeeping ratios (Tumataroa and O'Hare, 2019).

Separate fiscal principles, like amortization strategy, stock measurement strategy, and so

forth, are 3 distinct accountancy rules and standards. The disparity between practices in

various organisations makes comparison assessment extremely difficult, if not

unattainable.

Monetary insight is primarily based on previous facts and understanding. As a result, the

proportion determines generally followed historical patterns. Proportion evaluation does

not allow for prospective reliability.

CONCLUSION

It can be concluded from the above that the fiscal result of Jurys Inn has revealed certain

areas that need to be improved and maintained. The suggestions for such concerns are that

operating costs and expenditures must be tracked and managed while non-operational/financial

expenses must not be prioritised because they are backed up by a lot greater revenue. The

administration of payables and receivables is excellent. By providing adequate intensive service

to such customers, capitalised advantage from kindness can be obtained. Revenue must be

enhanced by implementing a well-thought-out item marketing strategy in tandem with cost-

cutting measures. The loan servicing and leveraging processes must be paid greater emphasis as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

availability declines, the accessible resource must be restored by matching the accessible

obligation. However, efficiency must be taken into account when maintaining a sufficient cash

flow.

obligation. However, efficiency must be taken into account when maintaining a sufficient cash

flow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Firouzjah, K.G., 2018. Assessment of small-scale solar PV systems in Iran: Regions priority,

potentials and financial feasibility. Renewable and Sustainable Energy Reviews, 94,

pp.267-274.

Higgins, E.T. and Cornwell, J.F., 2016. Securing foundations and advancing frontiers:

Prevention and promotion effects on judgment & decision making. Organizational

Behavior and Human Decision Processes, 136, pp.56-67.

Kalkavan, H. and Ersin, I., 2019. Determination of factors affecting the South East Asian crisis

of 1997 probit-logit panel regression: The South East Asian crisis. In Handbook of

research on global issues in financial communication and investment decision making

(pp. 148-167). IGI Global.

Khemakhem, S. and Boujelbene, Y., 2018. Predicting credit risk on the basis of financial and

non-financial variables and data mining. Review of Accounting and Finance.

Liu, P., Liu, J. and Chen, S.M., 2017. Some intuitionistic fuzzy Dombi Bonferroni mean

operators and their application to multi-attribute group decision making. Journal of the

Operational Research Society, pp.1-26.

Nindito, M., 2018. Financial statement fraud: Perspective of the Pentagon Fraud model in

Indonesia. Academy of Accounting and Financial Studies Journal, 22(3), pp.1-9.

Shelton, V.M., Smith, T.E. and Panisch, L.S., 2019. Financial therapy with groups: A case of the

five-step model. Journal of Financial Counseling and Planning, 30(1), pp.18-26.

Tumataroa, S. and O'Hare, D., 2019. Improving self-control through financial counseling: A

randomized controlled trial. Journal of Financial Counseling and Planning, 30(2),

pp.304-312.

Books and journals

Firouzjah, K.G., 2018. Assessment of small-scale solar PV systems in Iran: Regions priority,

potentials and financial feasibility. Renewable and Sustainable Energy Reviews, 94,

pp.267-274.

Higgins, E.T. and Cornwell, J.F., 2016. Securing foundations and advancing frontiers:

Prevention and promotion effects on judgment & decision making. Organizational

Behavior and Human Decision Processes, 136, pp.56-67.

Kalkavan, H. and Ersin, I., 2019. Determination of factors affecting the South East Asian crisis

of 1997 probit-logit panel regression: The South East Asian crisis. In Handbook of

research on global issues in financial communication and investment decision making

(pp. 148-167). IGI Global.

Khemakhem, S. and Boujelbene, Y., 2018. Predicting credit risk on the basis of financial and

non-financial variables and data mining. Review of Accounting and Finance.

Liu, P., Liu, J. and Chen, S.M., 2017. Some intuitionistic fuzzy Dombi Bonferroni mean

operators and their application to multi-attribute group decision making. Journal of the

Operational Research Society, pp.1-26.

Nindito, M., 2018. Financial statement fraud: Perspective of the Pentagon Fraud model in

Indonesia. Academy of Accounting and Financial Studies Journal, 22(3), pp.1-9.

Shelton, V.M., Smith, T.E. and Panisch, L.S., 2019. Financial therapy with groups: A case of the

five-step model. Journal of Financial Counseling and Planning, 30(1), pp.18-26.

Tumataroa, S. and O'Hare, D., 2019. Improving self-control through financial counseling: A

randomized controlled trial. Journal of Financial Counseling and Planning, 30(2),

pp.304-312.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.