Financial Markets: Comparative Analysis of Commonwealth and ANZ Banks

VerifiedAdded on 2020/04/01

|16

|3891

|42

Report

AI Summary

This report provides a comparative financial analysis of the Commonwealth Bank (CWB) and the ANZ Banking Group, two major players in the Australian financial market. The analysis begins with an overview of macroeconomic factors such as GDP growth, interest rates, currency values, and inflation, providing context for the companies' performance. A bottom-up approach then delves into a detailed ratio analysis, including profitability ratios (operating income, operating margin, net income), efficiency ratios (fixed assets turnover, assets turnover), capital structure ratios, and market performance ratios. The report highlights key differences in performance, concluding with a comparative analysis and recommendations, suggesting that CWB may be a more suitable investment based on the provided data. The report leverages financial data from 2017 to evaluate the financial health and market position of both banks.

Financial Management 1

Principles of Financial Markets

Principles of Financial Markets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 2

Executive Summary

This report analyses the financial situation of the Company Common wealth Bank and ANZ

Group. Researcher has given brief introduction of the economic factors like GDP and interest

rate. Its purpose is to analyze the ratios of both the Companies. The current GDP annual growth

rate has been analyzed of Australia that is 1.80% in second (June) quarter of 2017 and projected

2.1% for third quarter in 2017. The financial situation of the Companies is analyzed on the basis

of liquidity, profitability, efficiency, and capital structure and market performance ratio. It has

also been analyzed from the report that the Company Common Wealth Bank is more suitable for

investing by the investors in comparison with the ANZ Company of Australia.

Table of Contents

Executive Summary

This report analyses the financial situation of the Company Common wealth Bank and ANZ

Group. Researcher has given brief introduction of the economic factors like GDP and interest

rate. Its purpose is to analyze the ratios of both the Companies. The current GDP annual growth

rate has been analyzed of Australia that is 1.80% in second (June) quarter of 2017 and projected

2.1% for third quarter in 2017. The financial situation of the Companies is analyzed on the basis

of liquidity, profitability, efficiency, and capital structure and market performance ratio. It has

also been analyzed from the report that the Company Common Wealth Bank is more suitable for

investing by the investors in comparison with the ANZ Company of Australia.

Table of Contents

Financial Management 3

Introduction......................................................................................................................................4

Common Wealth Bank.................................................................................................................4

Australia and New Zealand Banking Group................................................................................5

Top down Analysis..........................................................................................................................6

Current GDP................................................................................................................................6

Current Interest rate.....................................................................................................................7

Current Value of the $AUSD.......................................................................................................7

Current Inflation rate....................................................................................................................7

Personal Disposable Income........................................................................................................8

Bottom up Analysis.........................................................................................................................8

Ratio Analysis..................................................................................................................................9

Profitability ratio..........................................................................................................................9

Efficiency Ratio.........................................................................................................................10

Capital Structure Ratio...............................................................................................................11

Market Performance Ratio.........................................................................................................12

Comparative Analysis....................................................................................................................13

Summary and Recommendations..................................................................................................14

References......................................................................................................................................15

Introduction......................................................................................................................................4

Common Wealth Bank.................................................................................................................4

Australia and New Zealand Banking Group................................................................................5

Top down Analysis..........................................................................................................................6

Current GDP................................................................................................................................6

Current Interest rate.....................................................................................................................7

Current Value of the $AUSD.......................................................................................................7

Current Inflation rate....................................................................................................................7

Personal Disposable Income........................................................................................................8

Bottom up Analysis.........................................................................................................................8

Ratio Analysis..................................................................................................................................9

Profitability ratio..........................................................................................................................9

Efficiency Ratio.........................................................................................................................10

Capital Structure Ratio...............................................................................................................11

Market Performance Ratio.........................................................................................................12

Comparative Analysis....................................................................................................................13

Summary and Recommendations..................................................................................................14

References......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 4

Introduction

Common Wealth Bank

The Common Wealth Bank (CWB) was established in the year 1911 and started its working in

1912. It has the authority and permission for general banking business and savings. CWB is the

biggest Australian company that is listed on ASX. As per recent data of 2016, the CWB has a

staff of 52000 employees and approximately 800,000 shareholders (Commonwealth Bank,

2017). Due to multiple kinds of product offerings, it is quite easy for the CW bank to ensure

sustainable business growth in the market. Different kinds of banking products and services

offered by this bank are premium banking, retail banking, funds management, institutional

banking, and business banking and stock broking products/services. There are various strategies

of CWB diversification strategy, branding strategy, and the high scale sales generation strategy.

In Banking and Financial sector of Australia, the brand image of Common Wealth Bank is very

sound. Different products and services of CWB under retail banking include credit cards, home

loans, personal loan, transaction accounts etc. CWB was the first bank of Australia that has

obtained guarantee from Federal Government of country. CWB started its business from the city

of Melbourne with opening of first branch on 15th July 1912.

The mission of CWB is focused to provide customers the superior quality service. It also creates

value for its customers. It also promotes the stability and economic growth in the community. It

also has core values such as it ensures to the public that it is a great place to work. It also

provides opportunities to the Directors and other stakeholders (Commonwealth Bank, 2017). The

outstanding service is provided to the customers and helps them in achieving financial goals.

Introduction

Common Wealth Bank

The Common Wealth Bank (CWB) was established in the year 1911 and started its working in

1912. It has the authority and permission for general banking business and savings. CWB is the

biggest Australian company that is listed on ASX. As per recent data of 2016, the CWB has a

staff of 52000 employees and approximately 800,000 shareholders (Commonwealth Bank,

2017). Due to multiple kinds of product offerings, it is quite easy for the CW bank to ensure

sustainable business growth in the market. Different kinds of banking products and services

offered by this bank are premium banking, retail banking, funds management, institutional

banking, and business banking and stock broking products/services. There are various strategies

of CWB diversification strategy, branding strategy, and the high scale sales generation strategy.

In Banking and Financial sector of Australia, the brand image of Common Wealth Bank is very

sound. Different products and services of CWB under retail banking include credit cards, home

loans, personal loan, transaction accounts etc. CWB was the first bank of Australia that has

obtained guarantee from Federal Government of country. CWB started its business from the city

of Melbourne with opening of first branch on 15th July 1912.

The mission of CWB is focused to provide customers the superior quality service. It also creates

value for its customers. It also promotes the stability and economic growth in the community. It

also has core values such as it ensures to the public that it is a great place to work. It also

provides opportunities to the Directors and other stakeholders (Commonwealth Bank, 2017). The

outstanding service is provided to the customers and helps them in achieving financial goals.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 5

Australia and New Zealand (ANZ) Banking Group

ANZ banking group counted in largest banking firms in Australia and New Zealand. ANZ

Banking Group is one of the major financial services group and international banking in top 100

banks of globe. The head office of ANZ banking group is situated at city of Melbourne. Starting

year of this bank was 1835. ANZ also operates in 30 other nations.

(Source: ANZ, 2017).

In year 1835, ANZ Bank Company started in London and was established according to

provisions and guidelines of Royal charter (ANZ, 2017). In the year 1950-60s the bank of

Australasia in order to frame the ANZ Bank, the merger has took place between Union Bank of

Australia and New Zealand bank. The ANZ bank started its operations at Solomon Islands and

Honiara in 1966. It has a culturally diverse organization with the employees, which are from

different countries with different culture. The employees with different culture are working in

this organization. Different types of flexibility offered by this bank to its employees are job

sharing, flexible hours etc. The 34 markets are operated globally by this bank in the New

Zealand and Australia countries. ANZ bank has recorded its place in topmost four banks in

Australia. At the same time, it has recorded place in the list of top fifty banks across globe.

Australia and New Zealand (ANZ) Banking Group

ANZ banking group counted in largest banking firms in Australia and New Zealand. ANZ

Banking Group is one of the major financial services group and international banking in top 100

banks of globe. The head office of ANZ banking group is situated at city of Melbourne. Starting

year of this bank was 1835. ANZ also operates in 30 other nations.

(Source: ANZ, 2017).

In year 1835, ANZ Bank Company started in London and was established according to

provisions and guidelines of Royal charter (ANZ, 2017). In the year 1950-60s the bank of

Australasia in order to frame the ANZ Bank, the merger has took place between Union Bank of

Australia and New Zealand bank. The ANZ bank started its operations at Solomon Islands and

Honiara in 1966. It has a culturally diverse organization with the employees, which are from

different countries with different culture. The employees with different culture are working in

this organization. Different types of flexibility offered by this bank to its employees are job

sharing, flexible hours etc. The 34 markets are operated globally by this bank in the New

Zealand and Australia countries. ANZ bank has recorded its place in topmost four banks in

Australia. At the same time, it has recorded place in the list of top fifty banks across globe.

Financial Management 6

Its core values include ‘doing the things right’. It helps the business to achieve better outcomes.

Their values include integrity, Collaboration, Accountability, Respect and Intelligence.

Top down Analysis

In the top down analysis the overall picture of the economy and it analyses different industrial

sectors such as its macroeconomic trend. Here, the investors go through the economic factors and

narrow down the individual stocks (Calligaris, Villard, and Lafitte, 2011). There is an analysis of

economic factors such as, interest rates, GDP growth rates, exchange rates, energy prices and

productivity. This analysis would help the investors to pick a right stock that creates value. These

are described below:

Current GDP

The current Gross domestic product (GDP) of Australia expanded 0.8% in the second quarter in

the year 2017 from 1.8% of GDP in the year 2016. The high growth rate is recorded in

comparison with the expansion of 0.3% in first quarter of 2017. The expansion in the growth rate

is mainly because of increase in net export and domestic demand. The increase in GDP of

Australia is beneficial for the Companies as there is an increase in the economic activity of the

country (Natoli, and Zuhair, 2011).

Current Interest rate

Interest rate is the amount of interest that can be called as amount loaned, which a lender charges

to the borrower as an interest. Australia current interest rate of 2017 is 1.5% which is unchanged

by Reserve Bank of Australia as its interest rate in 2016 was 1.5% and its interest rate in 2015

was 2.0%. It can be seen that the constant interest rate adopted for 2017 which is low in

comparison to the interest rate of 2015 (Arrow, et al., 2013). So, it is expected that there will be

growth in the economy of Australia. Financial industry such as Australia and New Zealand and

Its core values include ‘doing the things right’. It helps the business to achieve better outcomes.

Their values include integrity, Collaboration, Accountability, Respect and Intelligence.

Top down Analysis

In the top down analysis the overall picture of the economy and it analyses different industrial

sectors such as its macroeconomic trend. Here, the investors go through the economic factors and

narrow down the individual stocks (Calligaris, Villard, and Lafitte, 2011). There is an analysis of

economic factors such as, interest rates, GDP growth rates, exchange rates, energy prices and

productivity. This analysis would help the investors to pick a right stock that creates value. These

are described below:

Current GDP

The current Gross domestic product (GDP) of Australia expanded 0.8% in the second quarter in

the year 2017 from 1.8% of GDP in the year 2016. The high growth rate is recorded in

comparison with the expansion of 0.3% in first quarter of 2017. The expansion in the growth rate

is mainly because of increase in net export and domestic demand. The increase in GDP of

Australia is beneficial for the Companies as there is an increase in the economic activity of the

country (Natoli, and Zuhair, 2011).

Current Interest rate

Interest rate is the amount of interest that can be called as amount loaned, which a lender charges

to the borrower as an interest. Australia current interest rate of 2017 is 1.5% which is unchanged

by Reserve Bank of Australia as its interest rate in 2016 was 1.5% and its interest rate in 2015

was 2.0%. It can be seen that the constant interest rate adopted for 2017 which is low in

comparison to the interest rate of 2015 (Arrow, et al., 2013). So, it is expected that there will be

growth in the economy of Australia. Financial industry such as Australia and New Zealand and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 7

Common Wealth bank can adopt the benefit from the constant interest rate. The companies are

highly benefited because of the constant interest rate. There is fluctuation in the interest rate

according to the economic standing and the Reserve Bank.

Current Value of the $AUSD

The current value of 1 AUD is equal to 0.8035 US Dollar. It can be analyzed that value of

Australian dollar is lower than that of US Dollar. It has a negative and positive impact on the

fluctuation of the currency on the overall financial industry of Australia (Hull, et al., 2013). It

can be seen that the rate of AUD is increased in comparison to the value of 1 AUD was equal to

0.7693 on 30th June 2017. It can be said that it is good for the finance industry of Australian

economy.

Current Inflation rate

The inflation rate can be defined as hike price of different products and depreciation in the value

of currency. The inflation rate is increased by 0.2% from the previous year that is 1.5% in 2017

from 1.3 % in last quarter of the year 2016. The inflation rate has increased as compare to 2016

that was 1.3%. So, it can be disadvantage for the financial companies (Aizenman, et al., 2011).

The increase in inflation rate had chances of decrease in the interest rate, which is constant in

2017 that is 1.5%. It will be beneficial for the Companies such as Commonwealth Bank group

limited and ANZ bank. The changes in the interest rate directly affect the inflation and there is

increase or decrease in the inflation rate of banks such as CWB limited and ANZ Group. If there

is increase in interest rate the companies cannot afford to get the finance. It also affects the

demand and supply of inflation.

Common Wealth bank can adopt the benefit from the constant interest rate. The companies are

highly benefited because of the constant interest rate. There is fluctuation in the interest rate

according to the economic standing and the Reserve Bank.

Current Value of the $AUSD

The current value of 1 AUD is equal to 0.8035 US Dollar. It can be analyzed that value of

Australian dollar is lower than that of US Dollar. It has a negative and positive impact on the

fluctuation of the currency on the overall financial industry of Australia (Hull, et al., 2013). It

can be seen that the rate of AUD is increased in comparison to the value of 1 AUD was equal to

0.7693 on 30th June 2017. It can be said that it is good for the finance industry of Australian

economy.

Current Inflation rate

The inflation rate can be defined as hike price of different products and depreciation in the value

of currency. The inflation rate is increased by 0.2% from the previous year that is 1.5% in 2017

from 1.3 % in last quarter of the year 2016. The inflation rate has increased as compare to 2016

that was 1.3%. So, it can be disadvantage for the financial companies (Aizenman, et al., 2011).

The increase in inflation rate had chances of decrease in the interest rate, which is constant in

2017 that is 1.5%. It will be beneficial for the Companies such as Commonwealth Bank group

limited and ANZ bank. The changes in the interest rate directly affect the inflation and there is

increase or decrease in the inflation rate of banks such as CWB limited and ANZ Group. If there

is increase in interest rate the companies cannot afford to get the finance. It also affects the

demand and supply of inflation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 8

Personal Disposable Income

Personal disposable income can be called as the amount of money, which is available for

population or an individual and it can also be called as an income, which is saved after paying of

taxes. The current personal disposable income of Australia is increased to $292336 million in

2017 from $289307 million in 2017. There is a change in the income that is $3029 million

increased from the last quarter and expected to increase more in the end of third quarter of 2017.

Personal disposable income growth reflects an increase in terms of trade (Mertens, and Ravn,

2013). It is important for the business to be considered. It can be analyzed that the Australian

people income is increased in 2017. The increase in income helps to encourage business to

increase in the employment. The increase in income makes a positive impact on the financial

industries such as CWB and ANZ. The increase in disposable income helps in increase in the

well-educated workforce. It would help in expanding the business.

Personal Disposable Income

Personal disposable income can be called as the amount of money, which is available for

population or an individual and it can also be called as an income, which is saved after paying of

taxes. The current personal disposable income of Australia is increased to $292336 million in

2017 from $289307 million in 2017. There is a change in the income that is $3029 million

increased from the last quarter and expected to increase more in the end of third quarter of 2017.

Personal disposable income growth reflects an increase in terms of trade (Mertens, and Ravn,

2013). It is important for the business to be considered. It can be analyzed that the Australian

people income is increased in 2017. The increase in income helps to encourage business to

increase in the employment. The increase in income makes a positive impact on the financial

industries such as CWB and ANZ. The increase in disposable income helps in increase in the

well-educated workforce. It would help in expanding the business.

Financial Management 9

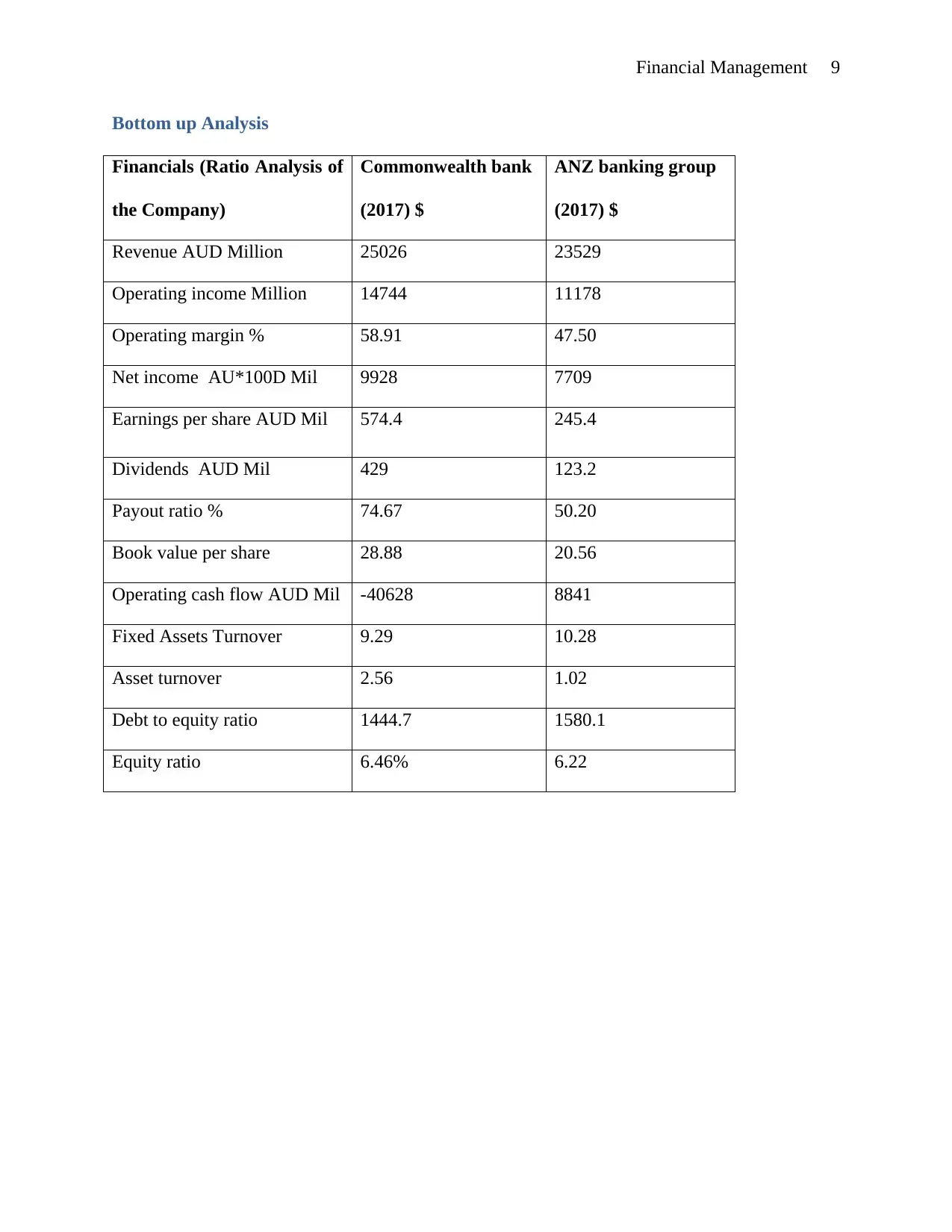

Bottom up Analysis

Financials (Ratio Analysis of

the Company)

Commonwealth bank

(2017) $

ANZ banking group

(2017) $

Revenue AUD Million 25026 23529

Operating income Million 14744 11178

Operating margin % 58.91 47.50

Net income AU*100D Mil 9928 7709

Earnings per share AUD Mil 574.4 245.4

Dividends AUD Mil 429 123.2

Payout ratio % 74.67 50.20

Book value per share 28.88 20.56

Operating cash flow AUD Mil -40628 8841

Fixed Assets Turnover 9.29 10.28

Asset turnover 2.56 1.02

Debt to equity ratio 1444.7 1580.1

Equity ratio 6.46% 6.22

Bottom up Analysis

Financials (Ratio Analysis of

the Company)

Commonwealth bank

(2017) $

ANZ banking group

(2017) $

Revenue AUD Million 25026 23529

Operating income Million 14744 11178

Operating margin % 58.91 47.50

Net income AU*100D Mil 9928 7709

Earnings per share AUD Mil 574.4 245.4

Dividends AUD Mil 429 123.2

Payout ratio % 74.67 50.20

Book value per share 28.88 20.56

Operating cash flow AUD Mil -40628 8841

Fixed Assets Turnover 9.29 10.28

Asset turnover 2.56 1.02

Debt to equity ratio 1444.7 1580.1

Equity ratio 6.46% 6.22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 10

Ratio Analysis

Profitability ratio

Operating income, Operating margin and Net income

This ratio is used in the company so as to measure the overall efficiency. The profitability ratio

includes operating income, operating margin and net income of both the companies. These

margin ratios enable the companies at various measuring stages. The operating margin is also

known as operating profit margin. This margin helps the companies to determine that how well

the businesses are supporting their operations. It is a key indicator for investors and creditors

(Saleem, and Rehman, 2011). The operating margin of Commonwealth Bank Company of 2017

is 58.91% and Australia and New Zealand Banking Group Limited has 47.50% in June, 2017.

The operating income is helpful in analyzing the company’s profit. Operating income of

Commonwealth Bank and Australia and New Zealand is 14744 AUD Million and 11178 AUD

Million in June, 2017. It is taken into account for analyzing the overall profitability of the

banking firm. Moreover, when the operating income of the Company is higher then, it will be

able to pay its debt. The net income can also be called as net profit and these are measured

basically in accounting and finance. The Companies Commonwealth and Australia and New

Zealand net income of 2017 is 9928 AUD and 7709 AUD Mill. It can be analyzed from above

that Common Wealth Bank has high profitability as comparison with ANZ. Higher profit ratio is

more beneficial than the lower profit ratio. It helps the company in gaining profit from its

ongoing operations.

Efficiency Ratio

Fixed Assets Turnover and Assets Turnover Ratios

Ratio Analysis

Profitability ratio

Operating income, Operating margin and Net income

This ratio is used in the company so as to measure the overall efficiency. The profitability ratio

includes operating income, operating margin and net income of both the companies. These

margin ratios enable the companies at various measuring stages. The operating margin is also

known as operating profit margin. This margin helps the companies to determine that how well

the businesses are supporting their operations. It is a key indicator for investors and creditors

(Saleem, and Rehman, 2011). The operating margin of Commonwealth Bank Company of 2017

is 58.91% and Australia and New Zealand Banking Group Limited has 47.50% in June, 2017.

The operating income is helpful in analyzing the company’s profit. Operating income of

Commonwealth Bank and Australia and New Zealand is 14744 AUD Million and 11178 AUD

Million in June, 2017. It is taken into account for analyzing the overall profitability of the

banking firm. Moreover, when the operating income of the Company is higher then, it will be

able to pay its debt. The net income can also be called as net profit and these are measured

basically in accounting and finance. The Companies Commonwealth and Australia and New

Zealand net income of 2017 is 9928 AUD and 7709 AUD Mill. It can be analyzed from above

that Common Wealth Bank has high profitability as comparison with ANZ. Higher profit ratio is

more beneficial than the lower profit ratio. It helps the company in gaining profit from its

ongoing operations.

Efficiency Ratio

Fixed Assets Turnover and Assets Turnover Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 11

Efficiency ratio is used by company for evaluating that efficiency of management of liabilities

and the assets of company. It includes the calculation and analysis of Fixed Assets turnover ratio

as well as the total asset turnover ratio. The ratio of fixed assets turnover is taken into account to

analyze the company’s return on their investment in the property. It also includes that how

efficiently the sales of a company is produced with its machines and equipments. The Companies

Commonwealth Bank and Australia and New Zealand fixed assets turnover ratio is 9.29% and

10.28% in 2017. It can be analyzed that the Company commonwealth is not efficiently using its

assets as its fixed assets as its assets is lower than that of ANZ (Cummins, and Weiss, 2013).

Moreover, Assets turnover ratio is also used by the company that how the Company is

successfully using its assets in order to generate revenue. The Commonwealth and Australia and

New Zealand assets turnover ratio are 2.56% and 1.02% in the year 2017. It can be analyzed that

ANZ bank does not use the assets efficiently as its Assets turnover ratio is low as comparison of

the other Company. It is based on the standard of the industry.

Capital Structure Ratio

Debt to equity ratio and Equity ratio

Capital structure is the ratio, in which the assets of the company are financed. It also helps the

investors to analyze that if the company is not in good condition then, what would happen to

their investments. Capital structure ratio shows the relationship between total debt and net

equity, which helps in making comparison between both the companies. The capital structure

ratio helps in analyzing the capital structure of the company (Eriotis, Frangouli, and Ventoura-

Neokosmides, 2011). It can also be analyzed that the capital structure of the CWB has 1444.7%

of Debt to equity ratio in 2017 and Equity Ratio is 6.46%. The other Company that is ANZ has

1580.1% Debt to equity ratio and 6.22% Equity ratio in 2017 respectively.

Efficiency ratio is used by company for evaluating that efficiency of management of liabilities

and the assets of company. It includes the calculation and analysis of Fixed Assets turnover ratio

as well as the total asset turnover ratio. The ratio of fixed assets turnover is taken into account to

analyze the company’s return on their investment in the property. It also includes that how

efficiently the sales of a company is produced with its machines and equipments. The Companies

Commonwealth Bank and Australia and New Zealand fixed assets turnover ratio is 9.29% and

10.28% in 2017. It can be analyzed that the Company commonwealth is not efficiently using its

assets as its fixed assets as its assets is lower than that of ANZ (Cummins, and Weiss, 2013).

Moreover, Assets turnover ratio is also used by the company that how the Company is

successfully using its assets in order to generate revenue. The Commonwealth and Australia and

New Zealand assets turnover ratio are 2.56% and 1.02% in the year 2017. It can be analyzed that

ANZ bank does not use the assets efficiently as its Assets turnover ratio is low as comparison of

the other Company. It is based on the standard of the industry.

Capital Structure Ratio

Debt to equity ratio and Equity ratio

Capital structure is the ratio, in which the assets of the company are financed. It also helps the

investors to analyze that if the company is not in good condition then, what would happen to

their investments. Capital structure ratio shows the relationship between total debt and net

equity, which helps in making comparison between both the companies. The capital structure

ratio helps in analyzing the capital structure of the company (Eriotis, Frangouli, and Ventoura-

Neokosmides, 2011). It can also be analyzed that the capital structure of the CWB has 1444.7%

of Debt to equity ratio in 2017 and Equity Ratio is 6.46%. The other Company that is ANZ has

1580.1% Debt to equity ratio and 6.22% Equity ratio in 2017 respectively.

Financial Management 12

The higher debt to equity ratio for both the companies helps in providing ratio of stock holder,

which is contributed to the capital to the creditor capital. From the above figure of the equity

ratio it is determined that how much of the total assets by the company are financed by the

investors. It also helps in determining the leverage of the company in respect to the debt of the

company. The equity ratio of CWB is higher as comparison of ANZ (Pratheepkanth, 2011). The

higher equity ratio of Commonwealth Bank Company helps in determining the potential

shareholders, which enables the shareholders to invest in the Company. From the above analysis

of the capital structure of both the companies, it can be determined that ANZ has stability in

comparison of Commonwealth Bank Company.

Market Performance Ratio

EPS, DPS, Dividend Payout and Book per share

It is used to evaluate the current share price of the companies. It includes EPS, DPS, Payout ratio

and Book value per share. EPS that is earning per share is like the profitability ratio as the higher

earnings ratio is better than the lower earnings ratio. If there is higher earnings ratio of the

Company then, the company is more profitable and able to distribute more profit to its

shareholders. The EPS AUD Million of Commonwealth and Australia and New Zealand

Company are 574.4$ and 245.4$ in 2017. It can be analyzed that the Commonwealth has higher

EPS then that of ANZ (Maditinos, et al., 2011). The Dividend per share is studied to measure the

dividend amount. The DPS of Common Wealth and Australia and New Zealand have 429$ and

123.2$. It can be analyzed that DPS of Commonwealth has a good amount of dividend as

comparison with ANZ.

Dividend payout ratio enables to measure the company’s net income, which is distributed among

the shareholders. It is measured in order to maintain the sustainable trends of a company. The

The higher debt to equity ratio for both the companies helps in providing ratio of stock holder,

which is contributed to the capital to the creditor capital. From the above figure of the equity

ratio it is determined that how much of the total assets by the company are financed by the

investors. It also helps in determining the leverage of the company in respect to the debt of the

company. The equity ratio of CWB is higher as comparison of ANZ (Pratheepkanth, 2011). The

higher equity ratio of Commonwealth Bank Company helps in determining the potential

shareholders, which enables the shareholders to invest in the Company. From the above analysis

of the capital structure of both the companies, it can be determined that ANZ has stability in

comparison of Commonwealth Bank Company.

Market Performance Ratio

EPS, DPS, Dividend Payout and Book per share

It is used to evaluate the current share price of the companies. It includes EPS, DPS, Payout ratio

and Book value per share. EPS that is earning per share is like the profitability ratio as the higher

earnings ratio is better than the lower earnings ratio. If there is higher earnings ratio of the

Company then, the company is more profitable and able to distribute more profit to its

shareholders. The EPS AUD Million of Commonwealth and Australia and New Zealand

Company are 574.4$ and 245.4$ in 2017. It can be analyzed that the Commonwealth has higher

EPS then that of ANZ (Maditinos, et al., 2011). The Dividend per share is studied to measure the

dividend amount. The DPS of Common Wealth and Australia and New Zealand have 429$ and

123.2$. It can be analyzed that DPS of Commonwealth has a good amount of dividend as

comparison with ANZ.

Dividend payout ratio enables to measure the company’s net income, which is distributed among

the shareholders. It is measured in order to maintain the sustainable trends of a company. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.