Project TABLE OF CONTENTS INTRODUCTION 1 TASK 11 P1.1 Sources of funds which are available to service and business sector

VerifiedAdded on 2021/01/01

|14

|3880

|451

AI Summary

Project TABLE OF CONTENTS INTRODUCTION 1 TASK 11 P1.1 Sources of funds which are available to service and business industry 1 P1.2 Contribution towards different methods of income generation 2 TASK 22 P2.1 Explaining the elements of cost, gross profit percentage and selling prices for goods and services 2 P2.2 Assessing methods of controlling stock and cash 3 TASK 34 P3.1 3.2 Assessing structure of trial balance and evaluating business accounts 4 P3.3 3.4 Discussing purpose and process of budgetary control in the firm

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Project

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1.1 Sources of funds which are available to service and business industry.........................1

P1.2 Contribution towards different methods of income generation.....................................2

TASK 2............................................................................................................................................2

P2.1 Explaining the elements of cost, gross profit percentage and selling prices for goods and

services...................................................................................................................................2

P2.2 Assessing methods of controlling stock and cash..........................................................3

TASK 3............................................................................................................................................4

P3.1 3.2 Assessing structure of trial balance and evaluating business accounts....................4

P3.3 3.4 Discussing purpose and process of budgetary control in the firm and analysing

budgetary variances................................................................................................................5

TASK 4............................................................................................................................................8

P4.1 Calculation of financial ratios for the organization........................................................8

P4.2 Recommendation for future management strategies to improve performance of

organization............................................................................................................................8

TASK 5............................................................................................................................................8

P5.1 Categorizing cost as variable, fixed and semi-variable of the company........................8

P5.2 Calculating per product contributions and explaining relationship between cost/profit and

volume....................................................................................................................................9

P5.3 Use and significance of Break-Even analysis for taking short-term decision..............10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1.1 Sources of funds which are available to service and business industry.........................1

P1.2 Contribution towards different methods of income generation.....................................2

TASK 2............................................................................................................................................2

P2.1 Explaining the elements of cost, gross profit percentage and selling prices for goods and

services...................................................................................................................................2

P2.2 Assessing methods of controlling stock and cash..........................................................3

TASK 3............................................................................................................................................4

P3.1 3.2 Assessing structure of trial balance and evaluating business accounts....................4

P3.3 3.4 Discussing purpose and process of budgetary control in the firm and analysing

budgetary variances................................................................................................................5

TASK 4............................................................................................................................................8

P4.1 Calculation of financial ratios for the organization........................................................8

P4.2 Recommendation for future management strategies to improve performance of

organization............................................................................................................................8

TASK 5............................................................................................................................................8

P5.1 Categorizing cost as variable, fixed and semi-variable of the company........................8

P5.2 Calculating per product contributions and explaining relationship between cost/profit and

volume....................................................................................................................................9

P5.3 Use and significance of Break-Even analysis for taking short-term decision..............10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Finance is very important in every industry especially in service sector and in the

business of hospitality it has a lead role in creating revenue. In the present report there is brief

discussion about Belgravia Hotel and its sources of finance which are available to business and

industries with the major contribution of different methods for generating income. The business

has been understood with the perspective of different elements of cost and methods for

controlling cash and stock in the business. The report is giving discussion about various sources

and structure of trial balance with the proper evaluation of business accounts, notes and its

adjustments. Along with this, objective of budgetary control and its variances are elaborated.

Ratio analysis is the best possible way for analyzing the financial performance of the

organization and even the concept of marginal costing has been applied.

TASK 1

P1.1 Sources of funds which are available to service and business industry

For pertaining the financial requirement of business, there are different sources which are

available and they are classified in two categories that is internal sources of finance and external

sources of finance. Both the sources of funds are giving great advantage for accomplishing the

Belgravia hotel's capital requirement. In the same series internal sources are:

Operating activities : It consists of various operational efforts like manufacturing the

products and services and how they are deal in the market. In the industry of hospitality it

is the most important aspect related to market and they have to work on the services

related to sale among each and every customers. The margin which is generated while

serving consumers it will be giving huge advantage for achieving satisfied amount of

profit (Quintana-García, Marchante-Lara and Benavides-Chicón, 2018).

Owner's equity : It is considered as a very satisfactory and convenient source of

financing as it is not required for drafting return in capital which has been generated. The

partners and business owners of the organization will uplift all the personal savings

related to business operations which are very effective and initial source for collecting

amount of finance in every activity. The Belgravia hotel will be leading great growth in

capital structure if savings of owners and directors will be used in operational practices.

External sources of finance

1

Finance is very important in every industry especially in service sector and in the

business of hospitality it has a lead role in creating revenue. In the present report there is brief

discussion about Belgravia Hotel and its sources of finance which are available to business and

industries with the major contribution of different methods for generating income. The business

has been understood with the perspective of different elements of cost and methods for

controlling cash and stock in the business. The report is giving discussion about various sources

and structure of trial balance with the proper evaluation of business accounts, notes and its

adjustments. Along with this, objective of budgetary control and its variances are elaborated.

Ratio analysis is the best possible way for analyzing the financial performance of the

organization and even the concept of marginal costing has been applied.

TASK 1

P1.1 Sources of funds which are available to service and business industry

For pertaining the financial requirement of business, there are different sources which are

available and they are classified in two categories that is internal sources of finance and external

sources of finance. Both the sources of funds are giving great advantage for accomplishing the

Belgravia hotel's capital requirement. In the same series internal sources are:

Operating activities : It consists of various operational efforts like manufacturing the

products and services and how they are deal in the market. In the industry of hospitality it

is the most important aspect related to market and they have to work on the services

related to sale among each and every customers. The margin which is generated while

serving consumers it will be giving huge advantage for achieving satisfied amount of

profit (Quintana-García, Marchante-Lara and Benavides-Chicón, 2018).

Owner's equity : It is considered as a very satisfactory and convenient source of

financing as it is not required for drafting return in capital which has been generated. The

partners and business owners of the organization will uplift all the personal savings

related to business operations which are very effective and initial source for collecting

amount of finance in every activity. The Belgravia hotel will be leading great growth in

capital structure if savings of owners and directors will be used in operational practices.

External sources of finance

1

Shareholder's equity : There funds helps the business for selling the equity ownership

of business in the present market. It has been recommended that Belgravia hotel should

perform the specific disclosure of the financial data base of their own organization which

will be attracting all the investors for pertaining interest to invest in their equity. They

may draft attractive dividend policies which will satisfy the investors for making trust

and loyalty with the perspective of business.

Bank loan : It is refereed as borrowings which can be granted through several financial

institutions and banks against any assets or property of the organization. In the present

era, Belgravia hotel will gain specific amount of loans from financial institution and how

the interest payment will be paid at which duration.

P1.2 Contribution towards different methods of income generation

For attaining the activities related to business in that manner then sources of income will

be very beneficial to Belgravia hotels. There is need of sources of funds because they help in

earning extra income and it might be generated in the best possible way. The best quality of food

has been given by hotel in very effective manner and along with this, rooms with high end for

enhancing the satisfaction of customer very effectually (Denizci Guillet and Mohammed, 2015).

Their income will be enhanced and even sales will be maximised by giving various offers which

attracts the consumers in the best possible manner and along with this, discounts will be super

advantage to consumer. These both factors are mailed to each and every customer in very

effective manner. The consumers will be given new offers and technology has also helped the

industry for performing business in innovative way. The promotional tool is also implied that is

contests, social media and networking websites are also giving advantage for generating income

with so much ease.

TASK 2

P2.1 Explaining the elements of cost, gross profit percentage and selling prices for goods and

services

The Belgravia hotel incurs different cost like labour, material and overheads for setting

up the selling price of the goods in very effective manner. The main cost of hotel is considered as

material cost that is ingredients which are applied in flour for making bread. On its contrary

wages, salaries and bonus are considered as labour cost. There is presence of indirect expenditure

2

of business in the present market. It has been recommended that Belgravia hotel should

perform the specific disclosure of the financial data base of their own organization which

will be attracting all the investors for pertaining interest to invest in their equity. They

may draft attractive dividend policies which will satisfy the investors for making trust

and loyalty with the perspective of business.

Bank loan : It is refereed as borrowings which can be granted through several financial

institutions and banks against any assets or property of the organization. In the present

era, Belgravia hotel will gain specific amount of loans from financial institution and how

the interest payment will be paid at which duration.

P1.2 Contribution towards different methods of income generation

For attaining the activities related to business in that manner then sources of income will

be very beneficial to Belgravia hotels. There is need of sources of funds because they help in

earning extra income and it might be generated in the best possible way. The best quality of food

has been given by hotel in very effective manner and along with this, rooms with high end for

enhancing the satisfaction of customer very effectually (Denizci Guillet and Mohammed, 2015).

Their income will be enhanced and even sales will be maximised by giving various offers which

attracts the consumers in the best possible manner and along with this, discounts will be super

advantage to consumer. These both factors are mailed to each and every customer in very

effective manner. The consumers will be given new offers and technology has also helped the

industry for performing business in innovative way. The promotional tool is also implied that is

contests, social media and networking websites are also giving advantage for generating income

with so much ease.

TASK 2

P2.1 Explaining the elements of cost, gross profit percentage and selling prices for goods and

services

The Belgravia hotel incurs different cost like labour, material and overheads for setting

up the selling price of the goods in very effective manner. The main cost of hotel is considered as

material cost that is ingredients which are applied in flour for making bread. On its contrary

wages, salaries and bonus are considered as labour cost. There is presence of indirect expenditure

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

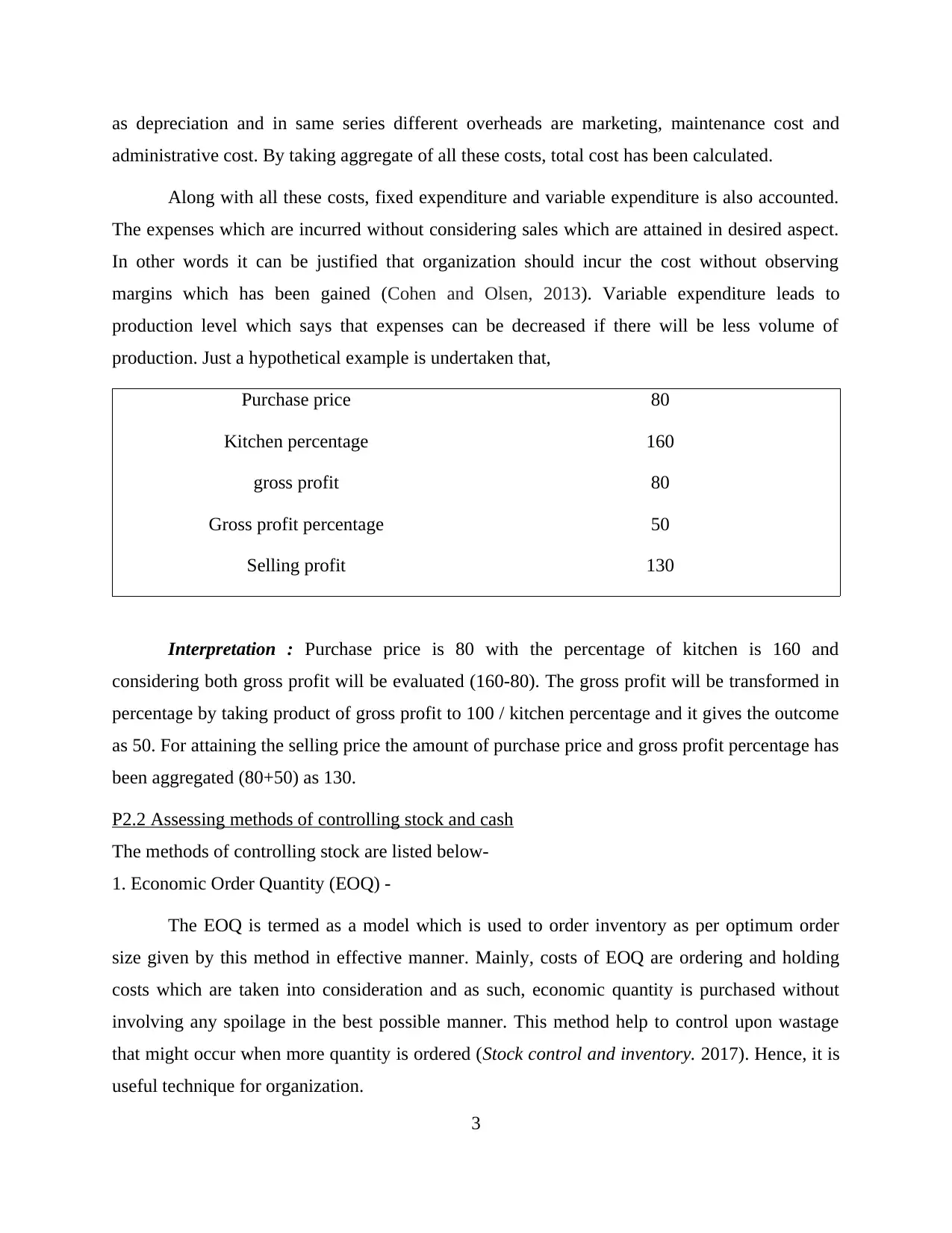

as depreciation and in same series different overheads are marketing, maintenance cost and

administrative cost. By taking aggregate of all these costs, total cost has been calculated.

Along with all these costs, fixed expenditure and variable expenditure is also accounted.

The expenses which are incurred without considering sales which are attained in desired aspect.

In other words it can be justified that organization should incur the cost without observing

margins which has been gained (Cohen and Olsen, 2013). Variable expenditure leads to

production level which says that expenses can be decreased if there will be less volume of

production. Just a hypothetical example is undertaken that,

Purchase price 80

Kitchen percentage 160

gross profit 80

Gross profit percentage 50

Selling profit 130

Interpretation : Purchase price is 80 with the percentage of kitchen is 160 and

considering both gross profit will be evaluated (160-80). The gross profit will be transformed in

percentage by taking product of gross profit to 100 / kitchen percentage and it gives the outcome

as 50. For attaining the selling price the amount of purchase price and gross profit percentage has

been aggregated (80+50) as 130.

P2.2 Assessing methods of controlling stock and cash

The methods of controlling stock are listed below-

1. Economic Order Quantity (EOQ) -

The EOQ is termed as a model which is used to order inventory as per optimum order

size given by this method in effective manner. Mainly, costs of EOQ are ordering and holding

costs which are taken into consideration and as such, economic quantity is purchased without

involving any spoilage in the best possible manner. This method help to control upon wastage

that might occur when more quantity is ordered (Stock control and inventory. 2017). Hence, it is

useful technique for organization.

3

administrative cost. By taking aggregate of all these costs, total cost has been calculated.

Along with all these costs, fixed expenditure and variable expenditure is also accounted.

The expenses which are incurred without considering sales which are attained in desired aspect.

In other words it can be justified that organization should incur the cost without observing

margins which has been gained (Cohen and Olsen, 2013). Variable expenditure leads to

production level which says that expenses can be decreased if there will be less volume of

production. Just a hypothetical example is undertaken that,

Purchase price 80

Kitchen percentage 160

gross profit 80

Gross profit percentage 50

Selling profit 130

Interpretation : Purchase price is 80 with the percentage of kitchen is 160 and

considering both gross profit will be evaluated (160-80). The gross profit will be transformed in

percentage by taking product of gross profit to 100 / kitchen percentage and it gives the outcome

as 50. For attaining the selling price the amount of purchase price and gross profit percentage has

been aggregated (80+50) as 130.

P2.2 Assessing methods of controlling stock and cash

The methods of controlling stock are listed below-

1. Economic Order Quantity (EOQ) -

The EOQ is termed as a model which is used to order inventory as per optimum order

size given by this method in effective manner. Mainly, costs of EOQ are ordering and holding

costs which are taken into consideration and as such, economic quantity is purchased without

involving any spoilage in the best possible manner. This method help to control upon wastage

that might occur when more quantity is ordered (Stock control and inventory. 2017). Hence, it is

useful technique for organization.

3

2. Just in time (JIT) approach-

JIT approach is used to minimise inventory expenses and to maximise efficiency. This

method is quite helpful as waste is decreased by receiving only those items which are needed in

manufacturing process. Hereby, no spoilage or wastage is occurred as goods are needed on time

when actual requirement prevails. Hence, it is adequate method for controlling stock.

Methods of controlling cash are listed below-

1. Balancing-

The transactions that occurs on day-to-day basis in Belgravia Hotels should be accounted

for so that transparency and accuracy may be maintained. It is particularly required as when cash

is withdrawn, then entry should be made in accounting books and when cash receipt is there,

entry should be made accordingly (Liu and Pennington-Gray, 2015). Thus, balancing will help

business to effectively control cash.

2. Reconcile-

The balances occurred in the bank passbook and in accounting records of the entity

should be accounted for on monthly basis. It is required so that differences may be rectified in

both records.

TASK 3

P3.1 3.2 Assessing structure of trial balance and evaluating business accounts

The trial balance is one of the important statement in financial accounting which is done

to examine any arithmetical errors in accounting records of organization. In simpler words, trial

balance judges records entered in journal and entries posted in general ledger and as such,

mathematical errors if any can be easily extracted with the help of preparing such statements.

Hence, accuracy of transactions may be attained in the best possible manner and thus, final

accounts can be prepared quite effectually. Thus, preparation of trial balance help to remove

errors in effective way and organization can produce financial statements quite effectively. The

sources of trial balance are discussed below-

Non-current assets are Equipment at cost, motor vehicles at cost

Current assets are inventory, trade receivables, bank, prepayment (rent)

4

JIT approach is used to minimise inventory expenses and to maximise efficiency. This

method is quite helpful as waste is decreased by receiving only those items which are needed in

manufacturing process. Hereby, no spoilage or wastage is occurred as goods are needed on time

when actual requirement prevails. Hence, it is adequate method for controlling stock.

Methods of controlling cash are listed below-

1. Balancing-

The transactions that occurs on day-to-day basis in Belgravia Hotels should be accounted

for so that transparency and accuracy may be maintained. It is particularly required as when cash

is withdrawn, then entry should be made in accounting books and when cash receipt is there,

entry should be made accordingly (Liu and Pennington-Gray, 2015). Thus, balancing will help

business to effectively control cash.

2. Reconcile-

The balances occurred in the bank passbook and in accounting records of the entity

should be accounted for on monthly basis. It is required so that differences may be rectified in

both records.

TASK 3

P3.1 3.2 Assessing structure of trial balance and evaluating business accounts

The trial balance is one of the important statement in financial accounting which is done

to examine any arithmetical errors in accounting records of organization. In simpler words, trial

balance judges records entered in journal and entries posted in general ledger and as such,

mathematical errors if any can be easily extracted with the help of preparing such statements.

Hence, accuracy of transactions may be attained in the best possible manner and thus, final

accounts can be prepared quite effectually. Thus, preparation of trial balance help to remove

errors in effective way and organization can produce financial statements quite effectively. The

sources of trial balance are discussed below-

Non-current assets are Equipment at cost, motor vehicles at cost

Current assets are inventory, trade receivables, bank, prepayment (rent)

4

Non-current liabilities are Long-term loan 7 %

Current liabilities are Trade payables, accrued interest and accrual telephone

P3.3 3.4 Discussing purpose and process of budgetary control in the firm and analysing

budgetary variances

The budget is termed as financial goal which is to be attained by organization so that it

may be able to earn profits by incurring necessary expenditures in the best possible manner

(Singal, 2014). It is clarified from the fact that Belgravia Hotels is required to effectively prepare

budgets as it will help to gain useful insight regarding future expenses that are required to be

incurred and profits will be made by incurring such expenditures in effectual way. This is

essentially required so that business may anticipate income that will be generated from the

expenditures that will be made and as such, performance can be enhanced in a better way by

taking into account future aspects of company's operations quite effectually. In relation to this,

budgetary control is used when for a particular year, budget is already prepared and as such,

comparison can be made with much ease. In addressing this, comparison means that planned

performance is compared with that of actual performance in order to analyse deviations if any

between these two quite effectively. The main purpose of budgetary control is to assess variances

that occurs in planned and actual output. It is done so that firm may be able to take corrective

action to remove such deviations and improvement can be done.

The budgetary control is used to assess deviations and thus, business performance can be

strengthened in the best possible manner. This is essentially required so that results may be

attained in relation to the expected income to be earned and expenditures to be incurred quite

effectually. Thus, Belgravia Hotels will be able to effectively utilised budgetary control by which

it may improve upon performance with much ease. Hence, purpose of this technique is to

effectively analyse variances and as such, improvement can be done with the help of taking

corrective action quite effectively (Kallmuenzer and Peters, 2018). In relation to this, process of

budgetary control is explained below-

Budget Committee- The decisions are assessed and made which are anticipated by company

that need to be made so that stated objectives can be attained quite effectually. In simpler words,

decisions are taken with main aspect of demand and need raised by various departments of firm.

5

Current liabilities are Trade payables, accrued interest and accrual telephone

P3.3 3.4 Discussing purpose and process of budgetary control in the firm and analysing

budgetary variances

The budget is termed as financial goal which is to be attained by organization so that it

may be able to earn profits by incurring necessary expenditures in the best possible manner

(Singal, 2014). It is clarified from the fact that Belgravia Hotels is required to effectively prepare

budgets as it will help to gain useful insight regarding future expenses that are required to be

incurred and profits will be made by incurring such expenditures in effectual way. This is

essentially required so that business may anticipate income that will be generated from the

expenditures that will be made and as such, performance can be enhanced in a better way by

taking into account future aspects of company's operations quite effectually. In relation to this,

budgetary control is used when for a particular year, budget is already prepared and as such,

comparison can be made with much ease. In addressing this, comparison means that planned

performance is compared with that of actual performance in order to analyse deviations if any

between these two quite effectively. The main purpose of budgetary control is to assess variances

that occurs in planned and actual output. It is done so that firm may be able to take corrective

action to remove such deviations and improvement can be done.

The budgetary control is used to assess deviations and thus, business performance can be

strengthened in the best possible manner. This is essentially required so that results may be

attained in relation to the expected income to be earned and expenditures to be incurred quite

effectually. Thus, Belgravia Hotels will be able to effectively utilised budgetary control by which

it may improve upon performance with much ease. Hence, purpose of this technique is to

effectively analyse variances and as such, improvement can be done with the help of taking

corrective action quite effectively (Kallmuenzer and Peters, 2018). In relation to this, process of

budgetary control is explained below-

Budget Committee- The decisions are assessed and made which are anticipated by company

that need to be made so that stated objectives can be attained quite effectually. In simpler words,

decisions are taken with main aspect of demand and need raised by various departments of firm.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is essentially required so that departments may perform well. Thus, in order to attain this,

budget committee is formed in effective way.

Budget Centres- In this process of budgetary control, costs are allocated to various departments

or units so that they may be able to achieve tasks with much ease. The centre is termed as a unit

and as such, costs are controlled in a better way. Thus, allocation of funds are made to units by

which operational activities can be accomplished by them.

Budget manuals- In respect to this, roles and responsibilities are provided with the help of

budget manual and as such, business is able to impart duties to the personnels. Moreover,

relationship between various personnels are also clarified in budget manual and thus, control can

be initiated to further stage.

Budget Officer appointed- At this stage, budget officer is appointed by Chief Executive Officer

(CEO) so that budget may be scrutinized in a better way (Kasemsap and et.al, 2018). The officer

scrutinizes budget prepared by executives for initiating improvement in the best possible manner.

Thus, business is able to clarify modifications to be made in budget so that variances can be

eradicated and improvement may be done quite effectually.

Budget Period- It is one of the important element as usually budget is prepared for specific time

of one year. This is done so that operational tasks can be performed in a better way by assessing

requirements of firm. On the other hand, period is also dependent upon numerous aspects

prevailing in particular industry.

Analysing key factor- This is the last process of budgetary control which is used to analyse any

key element that might affect Belgravia Hotels in the future course of action. The key factor need

to be analysed by which firm may be able to take corrective action for improvement quite

effectually.

Budget variances for Belgravia Hotels

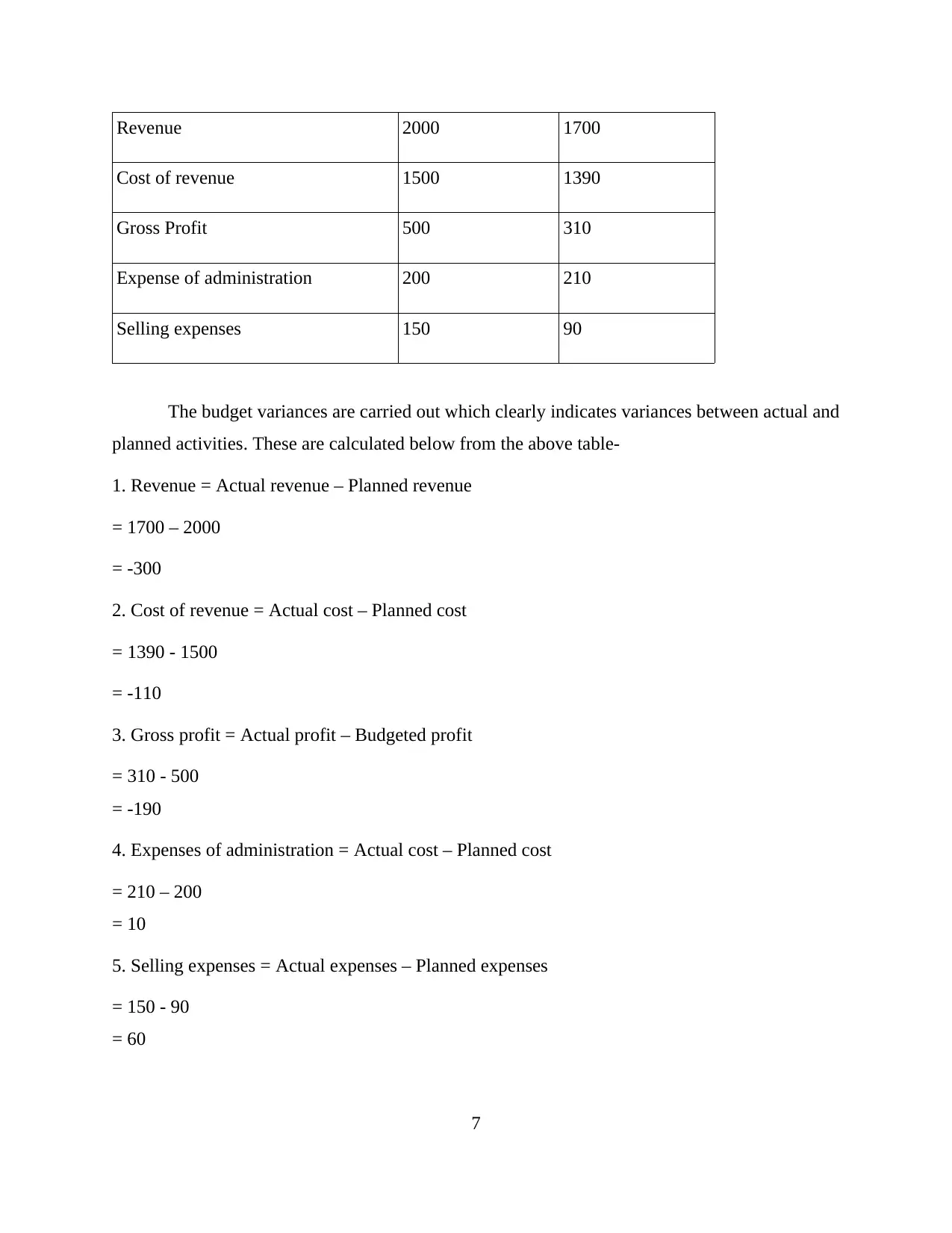

Particulars Budgeted Actual

Hotel customers 20000 15000

£0.00 £0.00

6

budget committee is formed in effective way.

Budget Centres- In this process of budgetary control, costs are allocated to various departments

or units so that they may be able to achieve tasks with much ease. The centre is termed as a unit

and as such, costs are controlled in a better way. Thus, allocation of funds are made to units by

which operational activities can be accomplished by them.

Budget manuals- In respect to this, roles and responsibilities are provided with the help of

budget manual and as such, business is able to impart duties to the personnels. Moreover,

relationship between various personnels are also clarified in budget manual and thus, control can

be initiated to further stage.

Budget Officer appointed- At this stage, budget officer is appointed by Chief Executive Officer

(CEO) so that budget may be scrutinized in a better way (Kasemsap and et.al, 2018). The officer

scrutinizes budget prepared by executives for initiating improvement in the best possible manner.

Thus, business is able to clarify modifications to be made in budget so that variances can be

eradicated and improvement may be done quite effectually.

Budget Period- It is one of the important element as usually budget is prepared for specific time

of one year. This is done so that operational tasks can be performed in a better way by assessing

requirements of firm. On the other hand, period is also dependent upon numerous aspects

prevailing in particular industry.

Analysing key factor- This is the last process of budgetary control which is used to analyse any

key element that might affect Belgravia Hotels in the future course of action. The key factor need

to be analysed by which firm may be able to take corrective action for improvement quite

effectually.

Budget variances for Belgravia Hotels

Particulars Budgeted Actual

Hotel customers 20000 15000

£0.00 £0.00

6

Revenue 2000 1700

Cost of revenue 1500 1390

Gross Profit 500 310

Expense of administration 200 210

Selling expenses 150 90

The budget variances are carried out which clearly indicates variances between actual and

planned activities. These are calculated below from the above table-

1. Revenue = Actual revenue – Planned revenue

= 1700 – 2000

= -300

2. Cost of revenue = Actual cost – Planned cost

= 1390 - 1500

= -110

3. Gross profit = Actual profit – Budgeted profit

= 310 - 500

= -190

4. Expenses of administration = Actual cost – Planned cost

= 210 – 200

= 10

5. Selling expenses = Actual expenses – Planned expenses

= 150 - 90

= 60

7

Cost of revenue 1500 1390

Gross Profit 500 310

Expense of administration 200 210

Selling expenses 150 90

The budget variances are carried out which clearly indicates variances between actual and

planned activities. These are calculated below from the above table-

1. Revenue = Actual revenue – Planned revenue

= 1700 – 2000

= -300

2. Cost of revenue = Actual cost – Planned cost

= 1390 - 1500

= -110

3. Gross profit = Actual profit – Budgeted profit

= 310 - 500

= -190

4. Expenses of administration = Actual cost – Planned cost

= 210 – 200

= 10

5. Selling expenses = Actual expenses – Planned expenses

= 150 - 90

= 60

7

The above calculated variances shows that firm needs to improve upon earnings capacity

so that it may be able to attain sales in a better way. This is essentially required as more profits

can be attained. It is evident from the revenue figure that the same is unfavourable because actual

revenue is less than planned one (Lado-Sestayo and et.al, 2016). Moreover, expenditures of

selling and administration are quite more. Thus, it is required that firm should initiate control

upon expenses so that profits may be maximised up to a high extent.

TASK 4

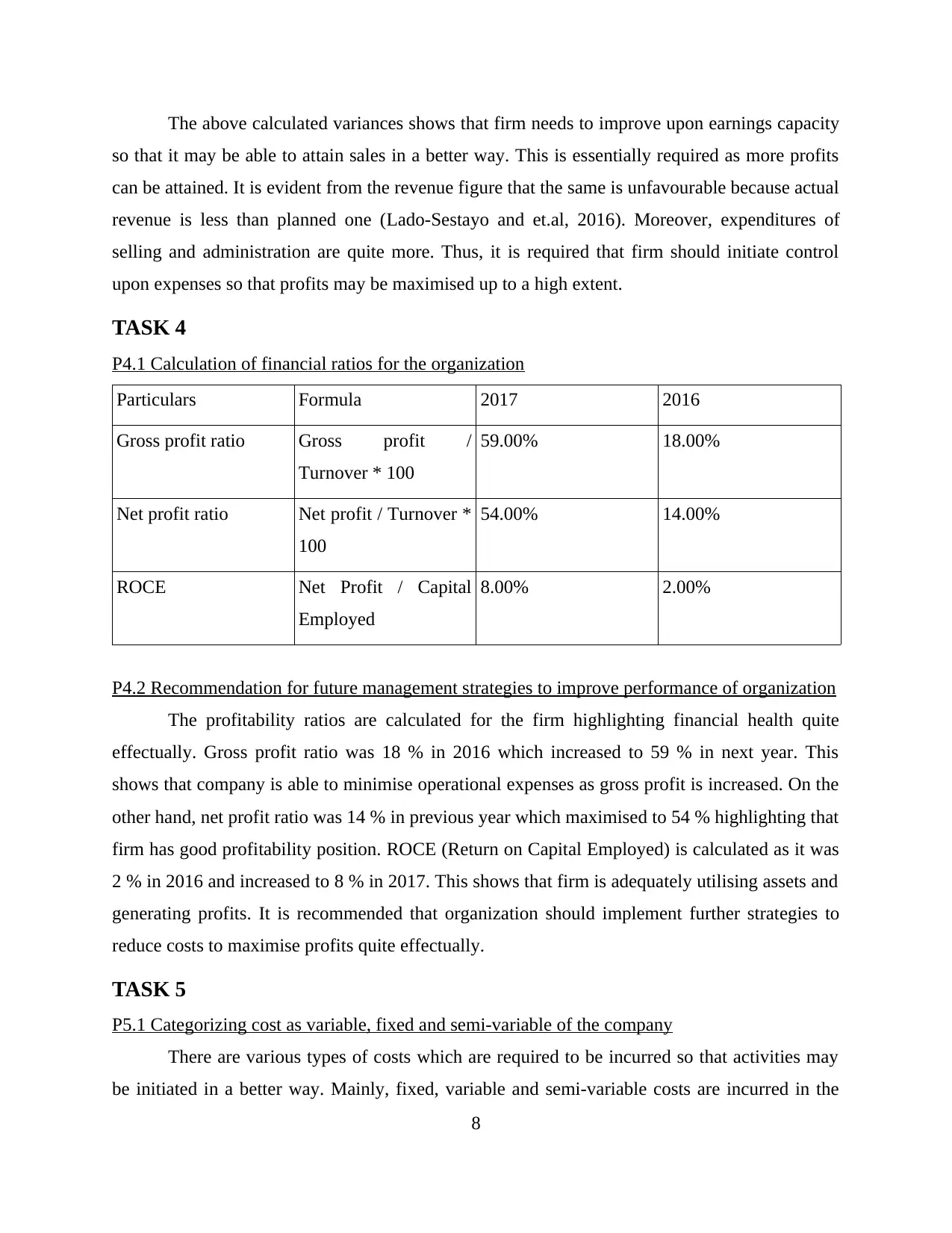

P4.1 Calculation of financial ratios for the organization

Particulars Formula 2017 2016

Gross profit ratio Gross profit /

Turnover * 100

59.00% 18.00%

Net profit ratio Net profit / Turnover *

100

54.00% 14.00%

ROCE Net Profit / Capital

Employed

8.00% 2.00%

P4.2 Recommendation for future management strategies to improve performance of organization

The profitability ratios are calculated for the firm highlighting financial health quite

effectually. Gross profit ratio was 18 % in 2016 which increased to 59 % in next year. This

shows that company is able to minimise operational expenses as gross profit is increased. On the

other hand, net profit ratio was 14 % in previous year which maximised to 54 % highlighting that

firm has good profitability position. ROCE (Return on Capital Employed) is calculated as it was

2 % in 2016 and increased to 8 % in 2017. This shows that firm is adequately utilising assets and

generating profits. It is recommended that organization should implement further strategies to

reduce costs to maximise profits quite effectually.

TASK 5

P5.1 Categorizing cost as variable, fixed and semi-variable of the company

There are various types of costs which are required to be incurred so that activities may

be initiated in a better way. Mainly, fixed, variable and semi-variable costs are incurred in the

8

so that it may be able to attain sales in a better way. This is essentially required as more profits

can be attained. It is evident from the revenue figure that the same is unfavourable because actual

revenue is less than planned one (Lado-Sestayo and et.al, 2016). Moreover, expenditures of

selling and administration are quite more. Thus, it is required that firm should initiate control

upon expenses so that profits may be maximised up to a high extent.

TASK 4

P4.1 Calculation of financial ratios for the organization

Particulars Formula 2017 2016

Gross profit ratio Gross profit /

Turnover * 100

59.00% 18.00%

Net profit ratio Net profit / Turnover *

100

54.00% 14.00%

ROCE Net Profit / Capital

Employed

8.00% 2.00%

P4.2 Recommendation for future management strategies to improve performance of organization

The profitability ratios are calculated for the firm highlighting financial health quite

effectually. Gross profit ratio was 18 % in 2016 which increased to 59 % in next year. This

shows that company is able to minimise operational expenses as gross profit is increased. On the

other hand, net profit ratio was 14 % in previous year which maximised to 54 % highlighting that

firm has good profitability position. ROCE (Return on Capital Employed) is calculated as it was

2 % in 2016 and increased to 8 % in 2017. This shows that firm is adequately utilising assets and

generating profits. It is recommended that organization should implement further strategies to

reduce costs to maximise profits quite effectually.

TASK 5

P5.1 Categorizing cost as variable, fixed and semi-variable of the company

There are various types of costs which are required to be incurred so that activities may

be initiated in a better way. Mainly, fixed, variable and semi-variable costs are incurred in the

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

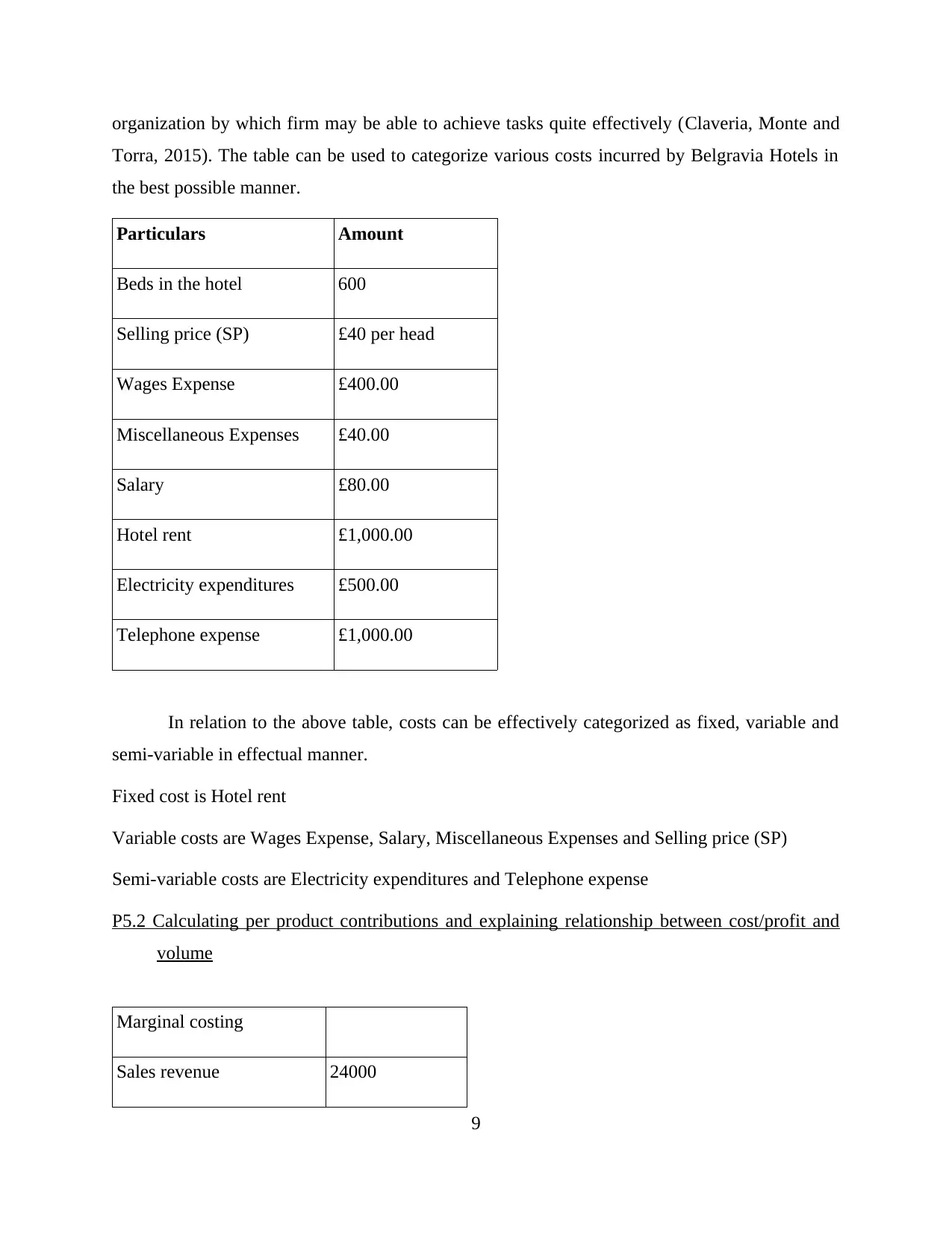

organization by which firm may be able to achieve tasks quite effectively (Claveria, Monte and

Torra, 2015). The table can be used to categorize various costs incurred by Belgravia Hotels in

the best possible manner.

Particulars Amount

Beds in the hotel 600

Selling price (SP) £40 per head

Wages Expense £400.00

Miscellaneous Expenses £40.00

Salary £80.00

Hotel rent £1,000.00

Electricity expenditures £500.00

Telephone expense £1,000.00

In relation to the above table, costs can be effectively categorized as fixed, variable and

semi-variable in effectual manner.

Fixed cost is Hotel rent

Variable costs are Wages Expense, Salary, Miscellaneous Expenses and Selling price (SP)

Semi-variable costs are Electricity expenditures and Telephone expense

P5.2 Calculating per product contributions and explaining relationship between cost/profit and

volume

Marginal costing

Sales revenue 24000

9

Torra, 2015). The table can be used to categorize various costs incurred by Belgravia Hotels in

the best possible manner.

Particulars Amount

Beds in the hotel 600

Selling price (SP) £40 per head

Wages Expense £400.00

Miscellaneous Expenses £40.00

Salary £80.00

Hotel rent £1,000.00

Electricity expenditures £500.00

Telephone expense £1,000.00

In relation to the above table, costs can be effectively categorized as fixed, variable and

semi-variable in effectual manner.

Fixed cost is Hotel rent

Variable costs are Wages Expense, Salary, Miscellaneous Expenses and Selling price (SP)

Semi-variable costs are Electricity expenditures and Telephone expense

P5.2 Calculating per product contributions and explaining relationship between cost/profit and

volume

Marginal costing

Sales revenue 24000

9

Less: Variable costs

Wages Expense 400

Miscellaneous Expenses 40

Salary 80

520

Less: Semi variable costs

Electricity expenditures 500

Telephone expense 1000

Contribution 1500

Less: Fixed costs

Hotel rent 1000

Net Profit 500

The marginal costing statement is prepared showing expenses made and net profit

generated quite effectively. In relation to this, CVP (Cost Volume and Profit) analysis can be

attained by calculating break-even point with much ease. Thus, per product contribution is

computed below-

P/V (Profit Volume) ratio = Contribution / Sales revenue

= 1500 / 24000

= 0.06 %

P5.3 Use and significance of Break-Even analysis for taking short-term decision

Sales can be found out with the help of break-even point at which firm should attain so

that at least losses may not occur. In simpler words, at this point, no profit no loss is achieved by

company (Avilova, Ermakov and Gozalova, 2014). However, if it reaches beyond break-even,

10

Wages Expense 400

Miscellaneous Expenses 40

Salary 80

520

Less: Semi variable costs

Electricity expenditures 500

Telephone expense 1000

Contribution 1500

Less: Fixed costs

Hotel rent 1000

Net Profit 500

The marginal costing statement is prepared showing expenses made and net profit

generated quite effectively. In relation to this, CVP (Cost Volume and Profit) analysis can be

attained by calculating break-even point with much ease. Thus, per product contribution is

computed below-

P/V (Profit Volume) ratio = Contribution / Sales revenue

= 1500 / 24000

= 0.06 %

P5.3 Use and significance of Break-Even analysis for taking short-term decision

Sales can be found out with the help of break-even point at which firm should attain so

that at least losses may not occur. In simpler words, at this point, no profit no loss is achieved by

company (Avilova, Ermakov and Gozalova, 2014). However, if it reaches beyond break-even,

10

then losses occur. It can be analysed that break-even sales are at 2500 units and cost amounts to

50. Hence, firm need to produce at least 2500 units to achieve desired sales.

The significance of break-even analysis for making short-term decision is that business is

able to determine production level to accomplish sales in the best possible manner. This helps to

devise strategies so that adequate production volume may be attained maximising profits.

CONCLUSION

Hereby it can be concluded that finance plays crucial role in the hospitality sector so that

daily tasks may be attained in a better way. There are various sources of funds which are

required to attain finance. Elements of costs in setting selling prices plays important role.

Computation of ratios provides clarity regarding overall financial performance in effective way.

Budgetary control is vital for the business so that deviations may be analysed and improvement

can be done by taking corrective action quite effectively. Hence, finance is required in the

organization for achieving stated objectives.

REFERENCES

Books and Journals

Avilova, N. L., Ermakov, A. S. and Gozalova, M. R., 2014. An analysis of the international

customer attraction experience in the hospitality industry. World Applied Sciences

Journal,30(MCTT)), pp.84-86.

Claveria, O., Monte, E. and Torra, S., 2015. A new forecasting approach for the hospitality

industry. International Journal of Contemporary Hospitality Management, 27(7), pp.1520-

1538.

Cohen, J. F. and Olsen, K., 2013. The impacts of complementary information technology

resources on the service-profit chain and competitive performance of South African

hospitality firms. International journal of hospitality management. 34. pp.245-254.

Denizci Guillet, B. and Mohammed, I., 2015. Revenue management research in hospitality and

tourism: A critical review of current literature and suggestions for future

11

50. Hence, firm need to produce at least 2500 units to achieve desired sales.

The significance of break-even analysis for making short-term decision is that business is

able to determine production level to accomplish sales in the best possible manner. This helps to

devise strategies so that adequate production volume may be attained maximising profits.

CONCLUSION

Hereby it can be concluded that finance plays crucial role in the hospitality sector so that

daily tasks may be attained in a better way. There are various sources of funds which are

required to attain finance. Elements of costs in setting selling prices plays important role.

Computation of ratios provides clarity regarding overall financial performance in effective way.

Budgetary control is vital for the business so that deviations may be analysed and improvement

can be done by taking corrective action quite effectively. Hence, finance is required in the

organization for achieving stated objectives.

REFERENCES

Books and Journals

Avilova, N. L., Ermakov, A. S. and Gozalova, M. R., 2014. An analysis of the international

customer attraction experience in the hospitality industry. World Applied Sciences

Journal,30(MCTT)), pp.84-86.

Claveria, O., Monte, E. and Torra, S., 2015. A new forecasting approach for the hospitality

industry. International Journal of Contemporary Hospitality Management, 27(7), pp.1520-

1538.

Cohen, J. F. and Olsen, K., 2013. The impacts of complementary information technology

resources on the service-profit chain and competitive performance of South African

hospitality firms. International journal of hospitality management. 34. pp.245-254.

Denizci Guillet, B. and Mohammed, I., 2015. Revenue management research in hospitality and

tourism: A critical review of current literature and suggestions for future

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

research. International Journal of Contemporary Hospitality Management. 27(4). pp.526-

560.

Kallmuenzer, A. and Peters, M., 2018. Innovativeness and control mechanisms in tourism and

hospitality family firms: A comparative study. International Journal of Hospitality

Management, 70, pp.66-74.

Kasemsap, K. and et.al, 2018. Facilitating customer relationship management in modern

business. In Encyclopedia of Information Science and Technology, Fourth Edition (pp.

1594-1604). IGI Global.

Lado-Sestayo, R. and et.al, 2016. Impact of location on profitability in the Spanish hotel

sector. Tourism Management, 52, pp.405-415.

Liu, B. and Pennington-Gray, L., 2015. Bed bugs bite the hospitality industry? A framing

analysis of bed bug news coverage. Tourism Management, 48, pp.33-42.

Quintana-García, C., Marchante-Lara, M. and Benavides-Chicón, C.G., 2018. Social

responsibility and total quality in the hospitality industry: does gender matter?. Journal of

Sustainable Tourism. 26(5). pp.722-739.

Singal, M., 2014. The business case for diversity management in the hospitality

industry. International Journal of Hospitality Management, 40, pp.10-19.

Online

Elements of cost. 2018. [Online] Available Through: <http://smallbusiness.chron.com/element-

cost-management-accounting-67261.html>

Stock control and inventory, 2017. [Online] Available Through:

<https://www.nibusinessinfo.co.uk/content/stock-control-methods>

12

560.

Kallmuenzer, A. and Peters, M., 2018. Innovativeness and control mechanisms in tourism and

hospitality family firms: A comparative study. International Journal of Hospitality

Management, 70, pp.66-74.

Kasemsap, K. and et.al, 2018. Facilitating customer relationship management in modern

business. In Encyclopedia of Information Science and Technology, Fourth Edition (pp.

1594-1604). IGI Global.

Lado-Sestayo, R. and et.al, 2016. Impact of location on profitability in the Spanish hotel

sector. Tourism Management, 52, pp.405-415.

Liu, B. and Pennington-Gray, L., 2015. Bed bugs bite the hospitality industry? A framing

analysis of bed bug news coverage. Tourism Management, 48, pp.33-42.

Quintana-García, C., Marchante-Lara, M. and Benavides-Chicón, C.G., 2018. Social

responsibility and total quality in the hospitality industry: does gender matter?. Journal of

Sustainable Tourism. 26(5). pp.722-739.

Singal, M., 2014. The business case for diversity management in the hospitality

industry. International Journal of Hospitality Management, 40, pp.10-19.

Online

Elements of cost. 2018. [Online] Available Through: <http://smallbusiness.chron.com/element-

cost-management-accounting-67261.html>

Stock control and inventory, 2017. [Online] Available Through:

<https://www.nibusinessinfo.co.uk/content/stock-control-methods>

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.