Financial Management Report: Dividend & Investment Appraisal

VerifiedAdded on 2023/01/19

|16

|3270

|51

Report

AI Summary

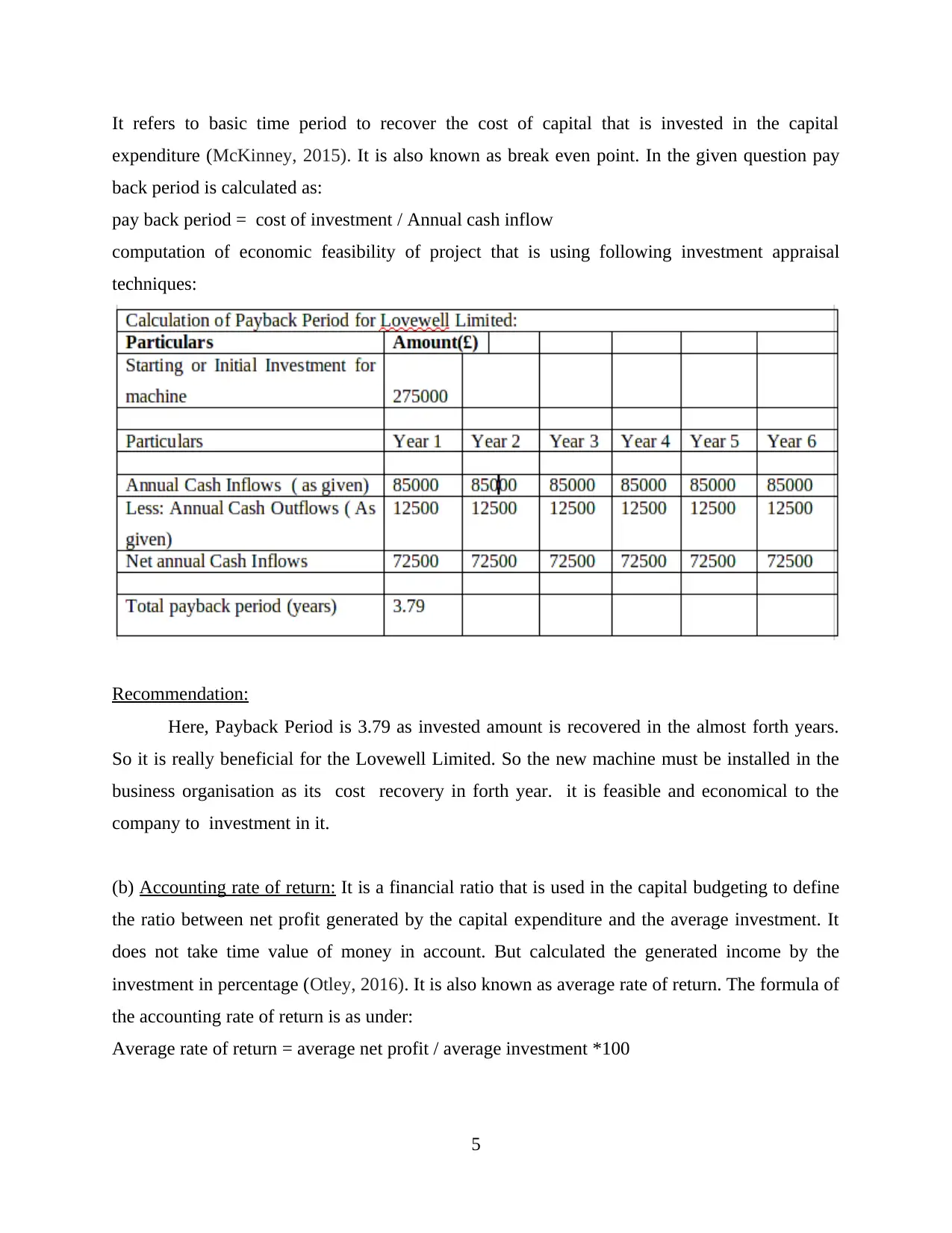

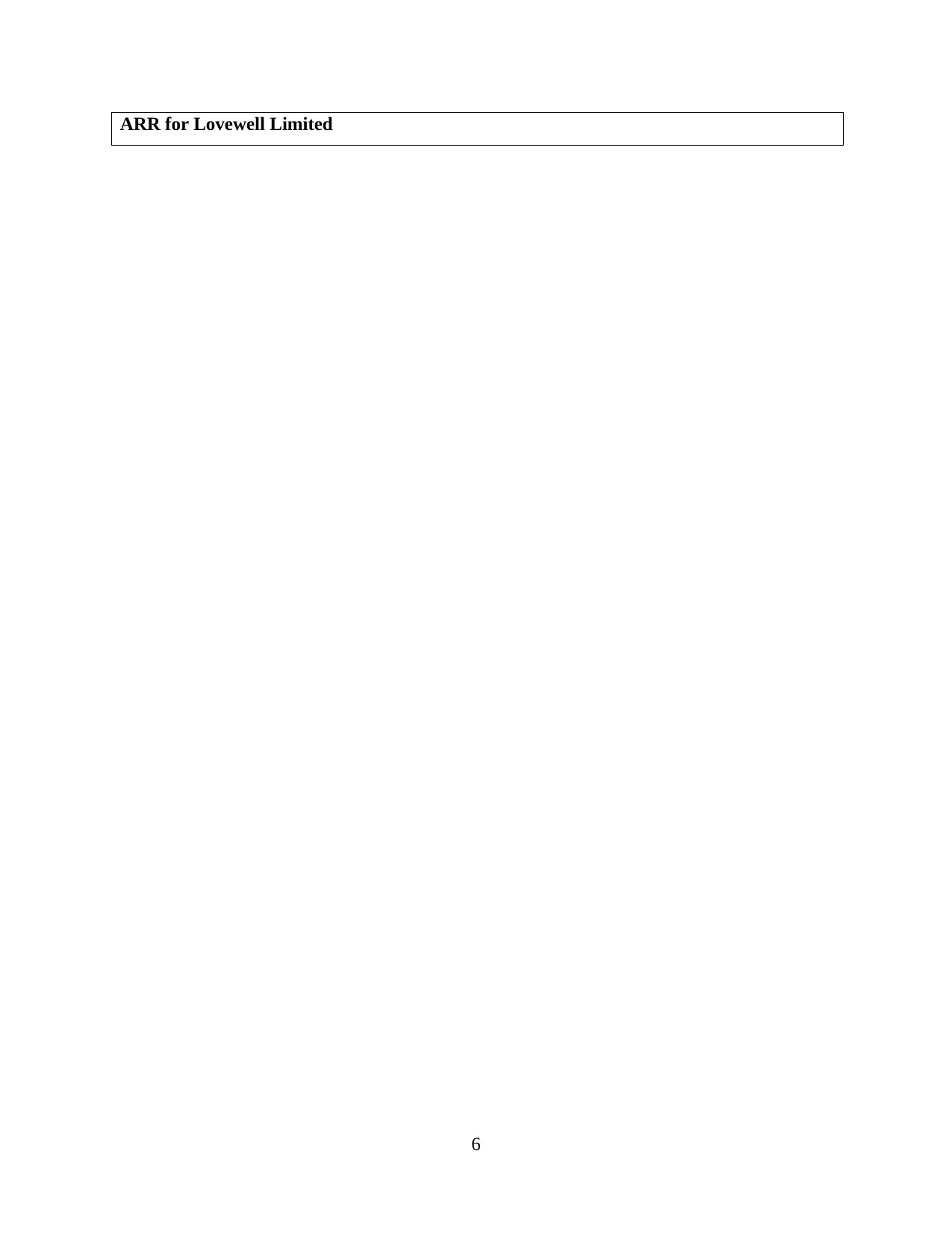

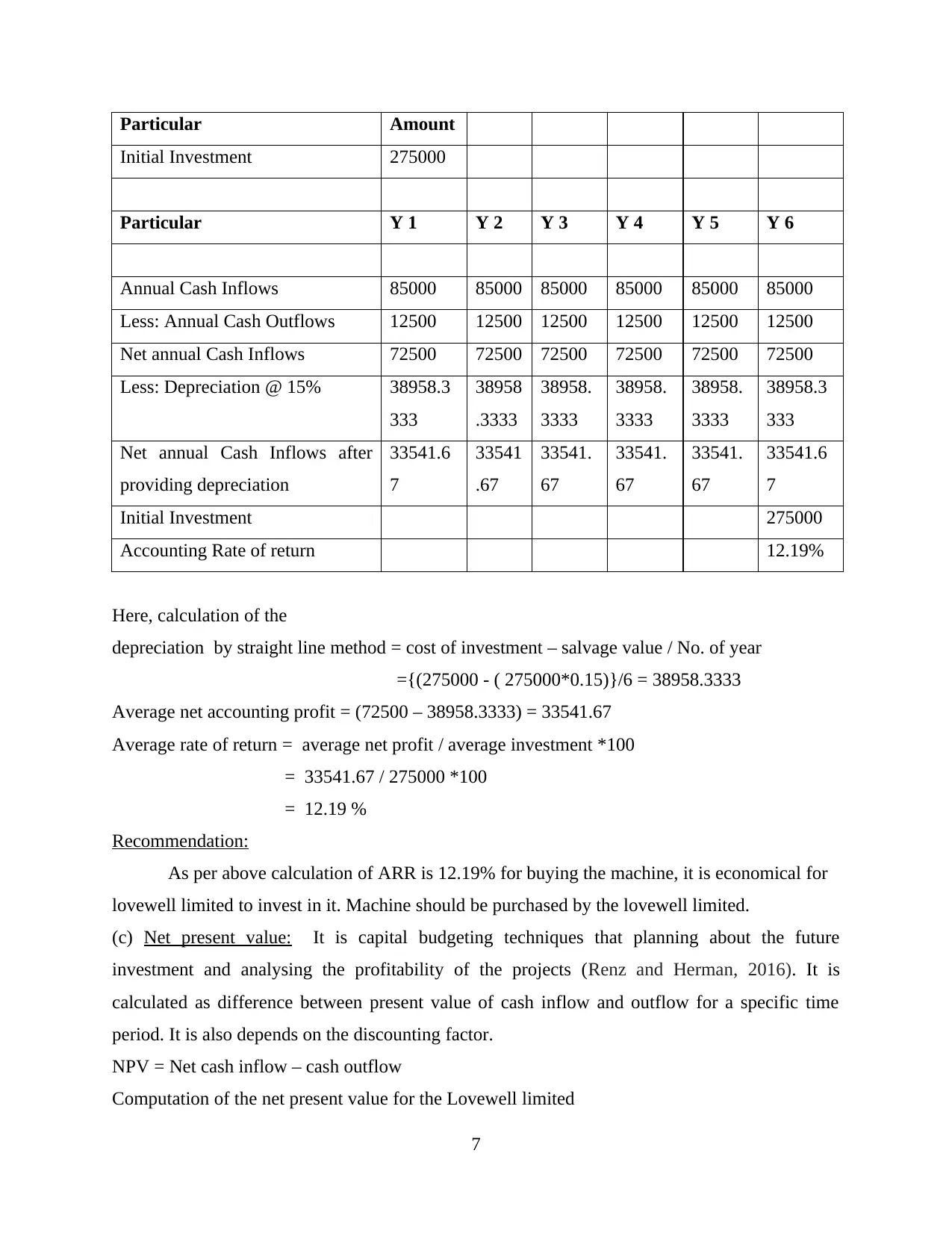

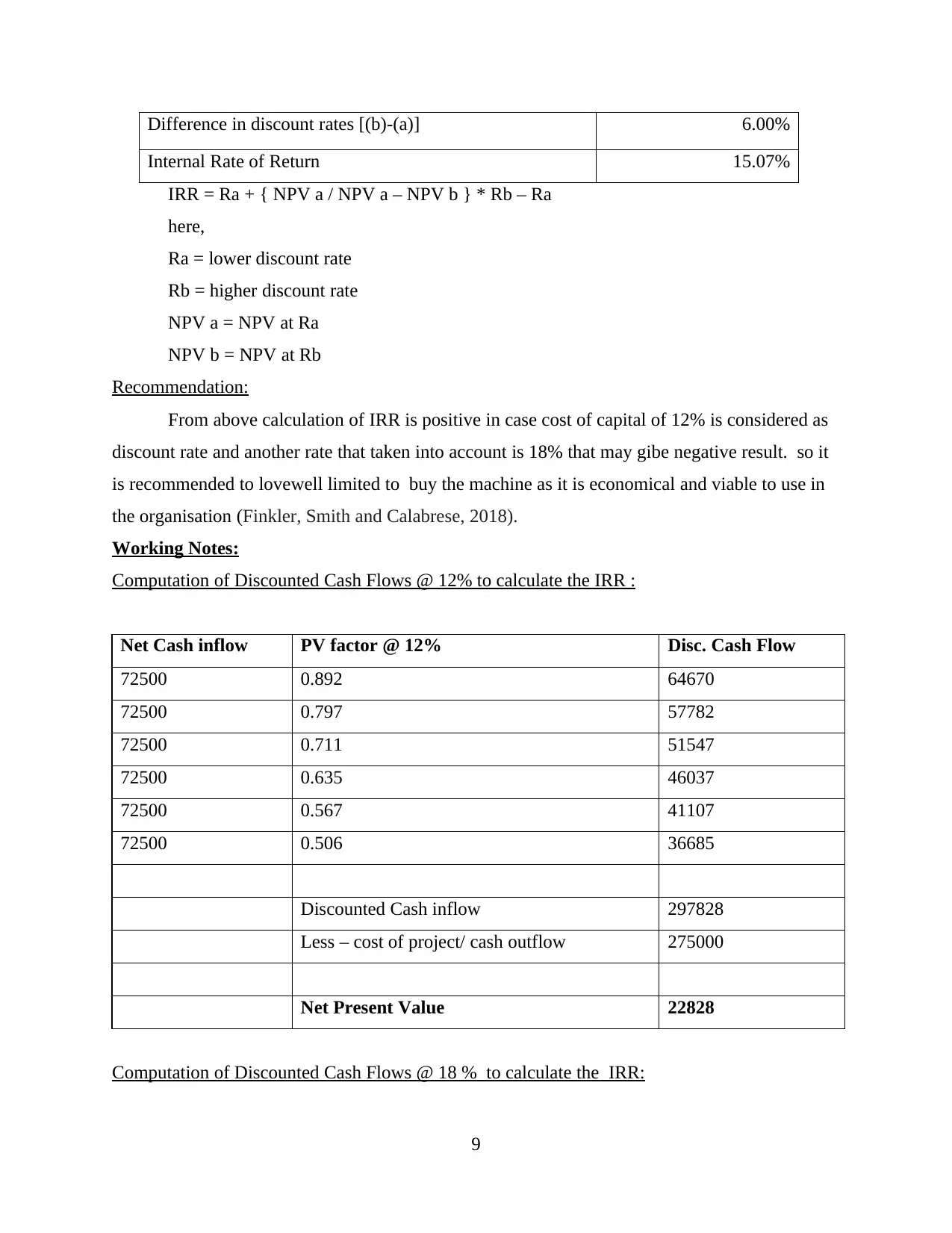

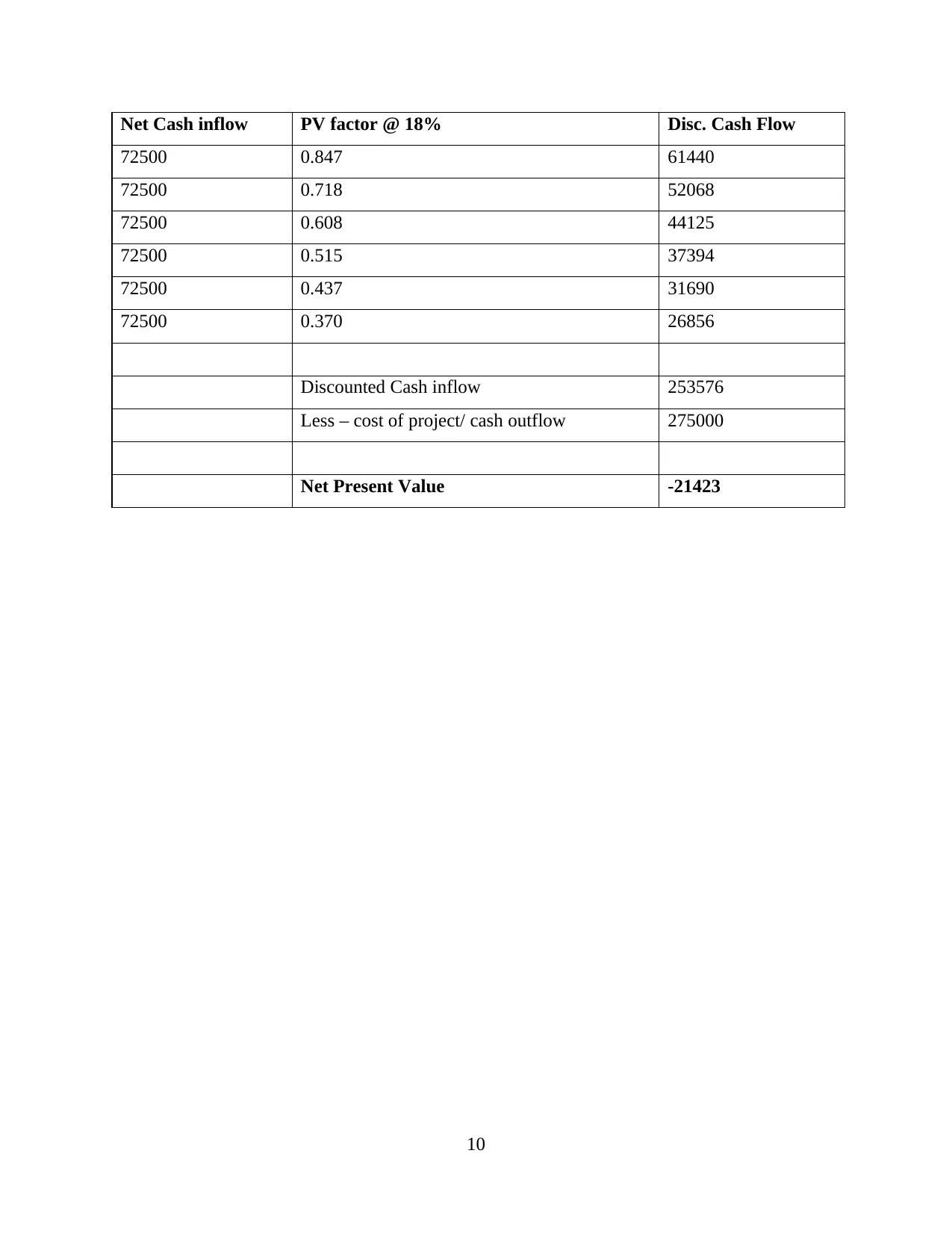

This report delves into the core concepts of financial management, focusing on dividend policy and investment appraisal techniques. It analyzes the dividend policy of Planet Company, utilizing Gordon's model to assess share valuation, and discusses the model's limitations. Furthermore, the report examines investment appraisal techniques, including payback period, accounting rate of return, net present value, and internal rate of return, applying them to a case study of Lovewell Limited. The analysis provides recommendations on investment decisions based on these financial tools, offering insights into financial risk, growth rate considerations, and the importance of accurate forecasting in financial planning. The report emphasizes the application of these concepts in business decision-making, highlighting their practical implications for financial managers. This report, contributed by a student, is available on Desklib, a platform providing AI-powered study tools for students, including past papers and solved assignments.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.