Financial Report: Alpen Choc Project - Break-Even & Cash Flow Analysis

VerifiedAdded on 2023/01/12

|24

|7207

|1

Report

AI Summary

This report presents a comprehensive financial analysis of the Alpen Choc project, evaluating two potential business ventures for Isaac, a Canadian entrepreneur. The analysis includes break-even analysis for both projects, detailing the point at which each becomes profitable, and comparing the potential financial returns of selling chocolates online versus selling to a friend. The report also provides a detailed profit and loss statement and balance sheet for Project 1, offering insights into the project's financial performance and position. Furthermore, the report examines monthly and annual cash flow projections, crucial for understanding the project's liquidity and long-term financial viability. Risk factors are assessed, and a final recommendation is made, considering both financial projections and the entrepreneur's risk appetite. The report uses assumptions to address incomplete information and considers currency exchange rates, cost structures, and sales strategies to provide a well-rounded financial assessment. The report concludes with a recommendation for Isaac, considering both the financial projections and risk factors associated with each project.

B09888

FINANCIAL

MANAGEMENT

FINANCIAL

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

BREAK EVEN ANALYSIS:..........................................................................................................4

Profit and Loss Statement and Balance Sheet Analyses:.................................................................7

Monthly cash flow for the first year of operation..........................................................................12

Projected annual cash inflows for 5 years.....................................................................................13

Cash required by Isaac to start new venture:.................................................................................16

Sensitivity analyses of both projects:............................................................................................19

Upfront fee for the exclusive rights to Alpen Choc:......................................................................21

RISK FACTOR ANALYSIS:........................................................................................................22

CONCLUSION AND RECOMMENDATION............................................................................23

REFERENCES..............................................................................................................................24

EXECUTIVE SUMMARY.............................................................................................................3

BREAK EVEN ANALYSIS:..........................................................................................................4

Profit and Loss Statement and Balance Sheet Analyses:.................................................................7

Monthly cash flow for the first year of operation..........................................................................12

Projected annual cash inflows for 5 years.....................................................................................13

Cash required by Isaac to start new venture:.................................................................................16

Sensitivity analyses of both projects:............................................................................................19

Upfront fee for the exclusive rights to Alpen Choc:......................................................................21

RISK FACTOR ANALYSIS:........................................................................................................22

CONCLUSION AND RECOMMENDATION............................................................................23

REFERENCES..............................................................................................................................24

EXECUTIVE SUMMARY

This report is based on various financial elements such as break even analysis, profit and

loss statement, balance sheet, monthly cash flow and annual cash flows. The case

presented shows that Issac has provided not complete information’s; thus for calculation

purpose data is assumed. The transaction is carried out between two countries; Canada

and Germany. Due to different currencies; foreign currency exchange rate for one

Canadian dollar (CAD) is taken as 0.64 € Euro, all the transactions will be carried out in

Canadian dollar; because Issac is the citizen of Canada and balance sheet and cost of

operations has to be calculated for him. Alpen Choc. is chocolate manufacturer company

situated in Germany. It is also assumed that foreign exchange rate will be constant

throughout the year and no discount is allowed on currency exchange even on bulk

purchase. Average selling price is assumed as CAD 160 per kg and there’s no sales tax

for any transactions. It is believed that all interests on borrowing are paid on time or

there’s no outstanding interest. Cash flow is discounted at rate of 7% per annum

(assumption) because inflation rate is between 5.19% to 8.15%, therefore interest paid on

borrowings are taken as discounted rate for cash flows; all other factors such as

environment change, increase in demand, competitors entry and fluctuation in inflation

rate are remain constant. Total average monthly sales are taken as 400 kg per year; it is

the average of average of starting month sale 50 kg and ending month 750 kg. Company

will order monthly stock at a time. Issac has two alternatives; either sale through internet

or his friend Jade. For calculating equity capital at Liability side; it is assumed that Isaac

would invest whole retirement amount into the business.

This report is based on various financial elements such as break even analysis, profit and

loss statement, balance sheet, monthly cash flow and annual cash flows. The case

presented shows that Issac has provided not complete information’s; thus for calculation

purpose data is assumed. The transaction is carried out between two countries; Canada

and Germany. Due to different currencies; foreign currency exchange rate for one

Canadian dollar (CAD) is taken as 0.64 € Euro, all the transactions will be carried out in

Canadian dollar; because Issac is the citizen of Canada and balance sheet and cost of

operations has to be calculated for him. Alpen Choc. is chocolate manufacturer company

situated in Germany. It is also assumed that foreign exchange rate will be constant

throughout the year and no discount is allowed on currency exchange even on bulk

purchase. Average selling price is assumed as CAD 160 per kg and there’s no sales tax

for any transactions. It is believed that all interests on borrowing are paid on time or

there’s no outstanding interest. Cash flow is discounted at rate of 7% per annum

(assumption) because inflation rate is between 5.19% to 8.15%, therefore interest paid on

borrowings are taken as discounted rate for cash flows; all other factors such as

environment change, increase in demand, competitors entry and fluctuation in inflation

rate are remain constant. Total average monthly sales are taken as 400 kg per year; it is

the average of average of starting month sale 50 kg and ending month 750 kg. Company

will order monthly stock at a time. Issac has two alternatives; either sale through internet

or his friend Jade. For calculating equity capital at Liability side; it is assumed that Isaac

would invest whole retirement amount into the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BREAK EVEN ANALYSIS:

Break-even Analysis (BEP): Break-even analysis shows a point of sale where company

attain the situation of no loss no gain; means it is a point where if company increases

sales, it will gain profit and moving below the point result in loss. In straightforward

words, the make back the initial investment point can be characterized as a point where

complete (costs) and all out deals (income) are equivalent (Brigham and Ehrhardt, 2013).

Break-even analysis shows the original investment point can be portrayed as a point

where there is no net benefit or deficit. The firm just earns back the original investment.

Issac has two alternatives which is either he can sale 4800 kg annual chocolates through

internet or 1200 boxes annually chocolate to his friend Jade.

Project 1

4800 kg Annually CAD CAD

Selling price per kg 160 768000

Less: Variable cost per

kg:

Packaging and Shipping 6

Purchases 113

Handling fee @ 1.2%

per sale 1.920 121 580416

Contribution per Kg 39 187584

Period cost (Fixed

Cost):

Total cost to sales

(annual) @ CAD

2,500/month

-

30000

Rent @ CAD

3,500/month

-

42000 72000 72000

Net Profit 115584

Working Note:

Handling fee per order (400 kg at a

time) =

400 kg × 160 × 1.2%

= 768

Per Kg Handling fee CAD 768/400 Kg = CAD

Break-even Analysis (BEP): Break-even analysis shows a point of sale where company

attain the situation of no loss no gain; means it is a point where if company increases

sales, it will gain profit and moving below the point result in loss. In straightforward

words, the make back the initial investment point can be characterized as a point where

complete (costs) and all out deals (income) are equivalent (Brigham and Ehrhardt, 2013).

Break-even analysis shows the original investment point can be portrayed as a point

where there is no net benefit or deficit. The firm just earns back the original investment.

Issac has two alternatives which is either he can sale 4800 kg annual chocolates through

internet or 1200 boxes annually chocolate to his friend Jade.

Project 1

4800 kg Annually CAD CAD

Selling price per kg 160 768000

Less: Variable cost per

kg:

Packaging and Shipping 6

Purchases 113

Handling fee @ 1.2%

per sale 1.920 121 580416

Contribution per Kg 39 187584

Period cost (Fixed

Cost):

Total cost to sales

(annual) @ CAD

2,500/month

-

30000

Rent @ CAD

3,500/month

-

42000 72000 72000

Net Profit 115584

Working Note:

Handling fee per order (400 kg at a

time) =

400 kg × 160 × 1.2%

= 768

Per Kg Handling fee CAD 768/400 Kg = CAD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

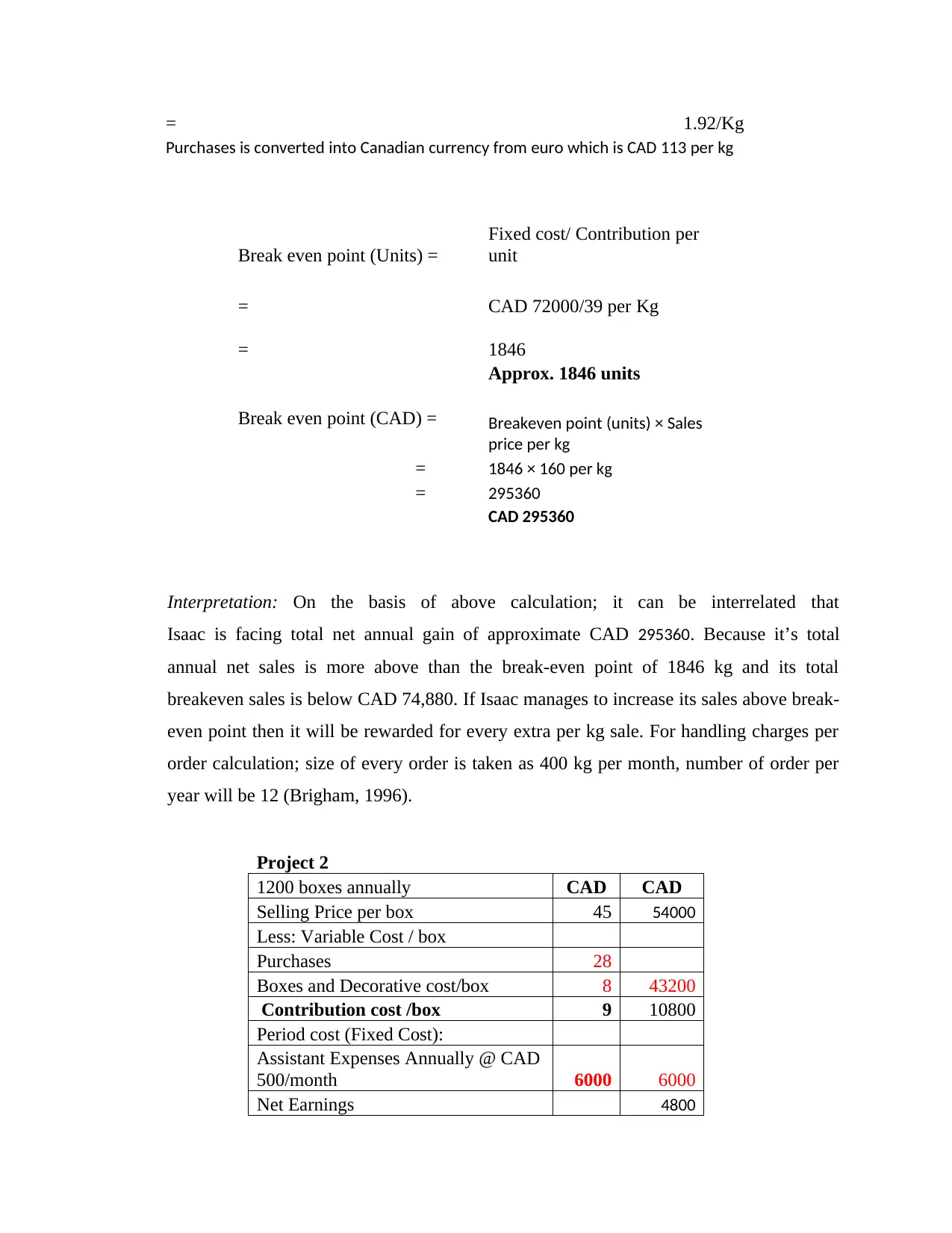

= 1.92/Kg

Purchases is converted into Canadian currency from euro which is CAD 113 per kg

Break even point (Units) =

Fixed cost/ Contribution per

unit

= CAD 72000/39 per Kg

= 1846

Approx. 1846 units

Break even point (CAD) = Breakeven point (units) × Sales

price per kg

= 1846 × 160 per kg

= 295360

CAD 295360

Interpretation: On the basis of above calculation; it can be interrelated that

Isaac is facing total net annual gain of approximate CAD 295360. Because it’s total

annual net sales is more above than the break-even point of 1846 kg and its total

breakeven sales is below CAD 74,880. If Isaac manages to increase its sales above break-

even point then it will be rewarded for every extra per kg sale. For handling charges per

order calculation; size of every order is taken as 400 kg per month, number of order per

year will be 12 (Brigham, 1996).

Project 2

1200 boxes annually CAD CAD

Selling Price per box 45 54000

Less: Variable Cost / box

Purchases 28

Boxes and Decorative cost/box 8 43200

Contribution cost /box 9 10800

Period cost (Fixed Cost):

Assistant Expenses Annually @ CAD

500/month 6000 6000

Net Earnings 4800

Purchases is converted into Canadian currency from euro which is CAD 113 per kg

Break even point (Units) =

Fixed cost/ Contribution per

unit

= CAD 72000/39 per Kg

= 1846

Approx. 1846 units

Break even point (CAD) = Breakeven point (units) × Sales

price per kg

= 1846 × 160 per kg

= 295360

CAD 295360

Interpretation: On the basis of above calculation; it can be interrelated that

Isaac is facing total net annual gain of approximate CAD 295360. Because it’s total

annual net sales is more above than the break-even point of 1846 kg and its total

breakeven sales is below CAD 74,880. If Isaac manages to increase its sales above break-

even point then it will be rewarded for every extra per kg sale. For handling charges per

order calculation; size of every order is taken as 400 kg per month, number of order per

year will be 12 (Brigham, 1996).

Project 2

1200 boxes annually CAD CAD

Selling Price per box 45 54000

Less: Variable Cost / box

Purchases 28

Boxes and Decorative cost/box 8 43200

Contribution cost /box 9 10800

Period cost (Fixed Cost):

Assistant Expenses Annually @ CAD

500/month 6000 6000

Net Earnings 4800

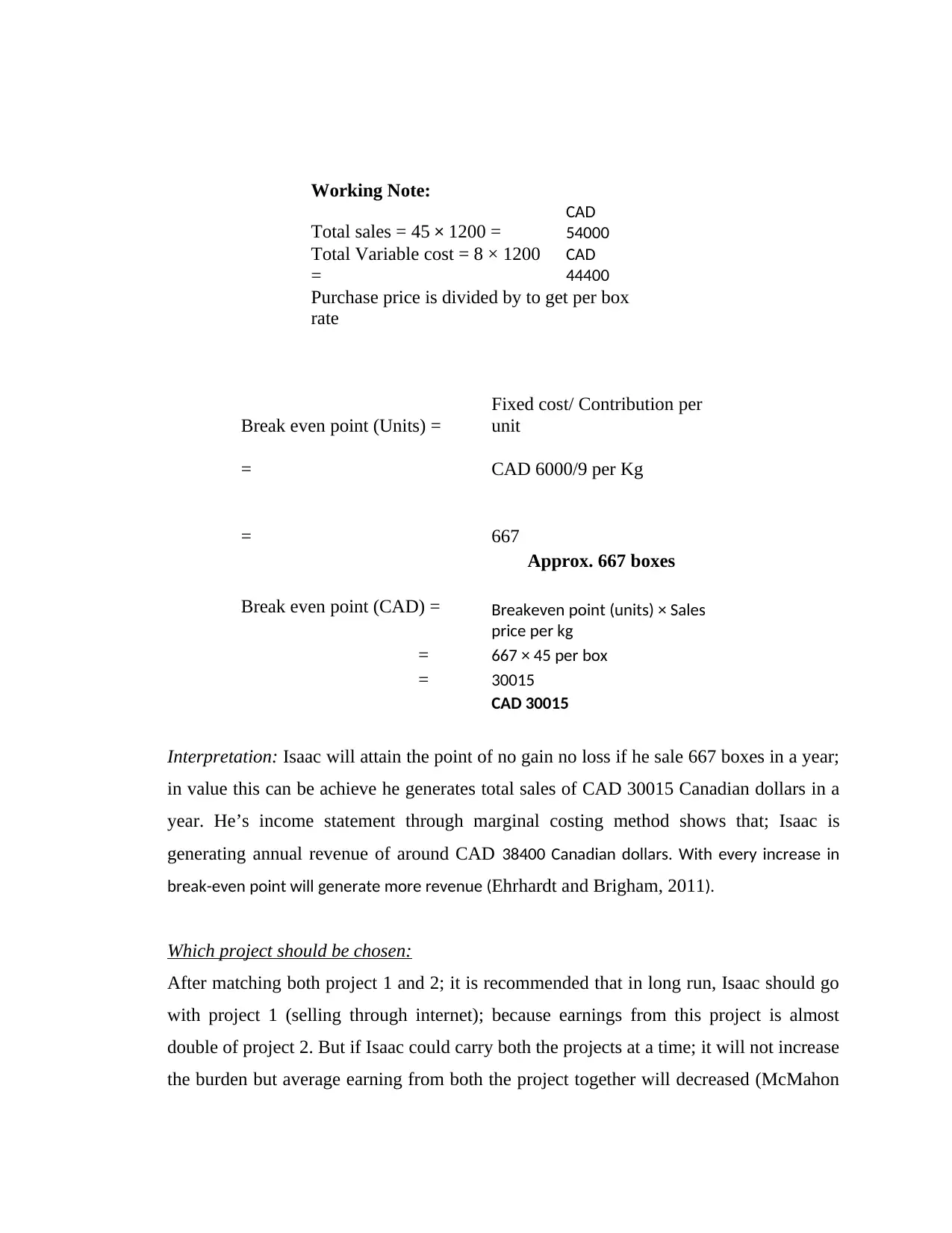

Working Note:

Total sales = 45 × 1200 =

CAD

54000

Total Variable cost = 8 × 1200

=

CAD

44400

Purchase price is divided by to get per box

rate

Break even point (Units) =

Fixed cost/ Contribution per

unit

= CAD 6000/9 per Kg

= 667

Approx. 667 boxes

Break even point (CAD) = Breakeven point (units) × Sales

price per kg

= 667 × 45 per box

= 30015

CAD 30015

Interpretation: Isaac will attain the point of no gain no loss if he sale 667 boxes in a year;

in value this can be achieve he generates total sales of CAD 30015 Canadian dollars in a

year. He’s income statement through marginal costing method shows that; Isaac is

generating annual revenue of around CAD 38400 Canadian dollars. With every increase in

break-even point will generate more revenue (Ehrhardt and Brigham, 2011).

Which project should be chosen:

After matching both project 1 and 2; it is recommended that in long run, Isaac should go

with project 1 (selling through internet); because earnings from this project is almost

double of project 2. But if Isaac could carry both the projects at a time; it will not increase

the burden but average earning from both the project together will decreased (McMahon

Total sales = 45 × 1200 =

CAD

54000

Total Variable cost = 8 × 1200

=

CAD

44400

Purchase price is divided by to get per box

rate

Break even point (Units) =

Fixed cost/ Contribution per

unit

= CAD 6000/9 per Kg

= 667

Approx. 667 boxes

Break even point (CAD) = Breakeven point (units) × Sales

price per kg

= 667 × 45 per box

= 30015

CAD 30015

Interpretation: Isaac will attain the point of no gain no loss if he sale 667 boxes in a year;

in value this can be achieve he generates total sales of CAD 30015 Canadian dollars in a

year. He’s income statement through marginal costing method shows that; Isaac is

generating annual revenue of around CAD 38400 Canadian dollars. With every increase in

break-even point will generate more revenue (Ehrhardt and Brigham, 2011).

Which project should be chosen:

After matching both project 1 and 2; it is recommended that in long run, Isaac should go

with project 1 (selling through internet); because earnings from this project is almost

double of project 2. But if Isaac could carry both the projects at a time; it will not increase

the burden but average earning from both the project together will decreased (McMahon

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and et.al. 1993). But taking into consideration about cost of starting the business; it was

found that in project 1, Isaac has to spend CAD 8,500 with website designer and he

already spent CAD 5,000 for market study; hence total cost of establishment is CAD

13,500. On the other hand, to acquire project 2 he just only require CAD 2,200 onetime

cost for purchase wrapping machine (Chandra, 2011). After analyzing risk factor it was

found that project 1 has only estimated sale of approximate 4800 kg for first year but

project 2 is giving guaranteed sale of 1200 boxes annually on immediate base. It cannot

be ignored that more risk results in more profit; but looking at return on investment

factor, project 1 obviously has less return than project 2. Assuming that Issac is 60 year

old and have less risk apatite; it is recommended that he should go with project 2.

Profit and Loss Statement and Balance Sheet Analyses:

Profit and Loss statement: Also known as Income statement; calculated by every

organization to know about its annual earnings from the business. The profit and loss

(P&L) statement is a budget report that outlines the incomes, expenses, and costs

acquired during a predefined period, normally a financial quarter or year. The P&L

articulation is synonymous with the salary explanation. These records give data about an

organization's capacity or powerlessness to produce benefit by expanding income,

diminishing expenses, or both. Some allude to the P&L articulation as an announcement

of benefit and misfortune, salary proclamation, explanation of tasks, explanation of

money related outcomes or pay, profit proclamation or cost proclamation (Schall and

Haley, 1979).

Balance sheet: It shows financial position of the company at the end of year. It works on

going on concept, means all the elements in balance sheet have their closing balance and

carried forwarded to next year until fully settled by firm. A balance sheet is an

announcement of the budgetary situation of a business that rundowns the benefits,

liabilities, and proprietor's value at a specific point in time. As it were, the accounting

report delineates your business' total assets (Brealey, 2001).

found that in project 1, Isaac has to spend CAD 8,500 with website designer and he

already spent CAD 5,000 for market study; hence total cost of establishment is CAD

13,500. On the other hand, to acquire project 2 he just only require CAD 2,200 onetime

cost for purchase wrapping machine (Chandra, 2011). After analyzing risk factor it was

found that project 1 has only estimated sale of approximate 4800 kg for first year but

project 2 is giving guaranteed sale of 1200 boxes annually on immediate base. It cannot

be ignored that more risk results in more profit; but looking at return on investment

factor, project 1 obviously has less return than project 2. Assuming that Issac is 60 year

old and have less risk apatite; it is recommended that he should go with project 2.

Profit and Loss Statement and Balance Sheet Analyses:

Profit and Loss statement: Also known as Income statement; calculated by every

organization to know about its annual earnings from the business. The profit and loss

(P&L) statement is a budget report that outlines the incomes, expenses, and costs

acquired during a predefined period, normally a financial quarter or year. The P&L

articulation is synonymous with the salary explanation. These records give data about an

organization's capacity or powerlessness to produce benefit by expanding income,

diminishing expenses, or both. Some allude to the P&L articulation as an announcement

of benefit and misfortune, salary proclamation, explanation of tasks, explanation of

money related outcomes or pay, profit proclamation or cost proclamation (Schall and

Haley, 1979).

Balance sheet: It shows financial position of the company at the end of year. It works on

going on concept, means all the elements in balance sheet have their closing balance and

carried forwarded to next year until fully settled by firm. A balance sheet is an

announcement of the budgetary situation of a business that rundowns the benefits,

liabilities, and proprietor's value at a specific point in time. As it were, the accounting

report delineates your business' total assets (Brealey, 2001).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

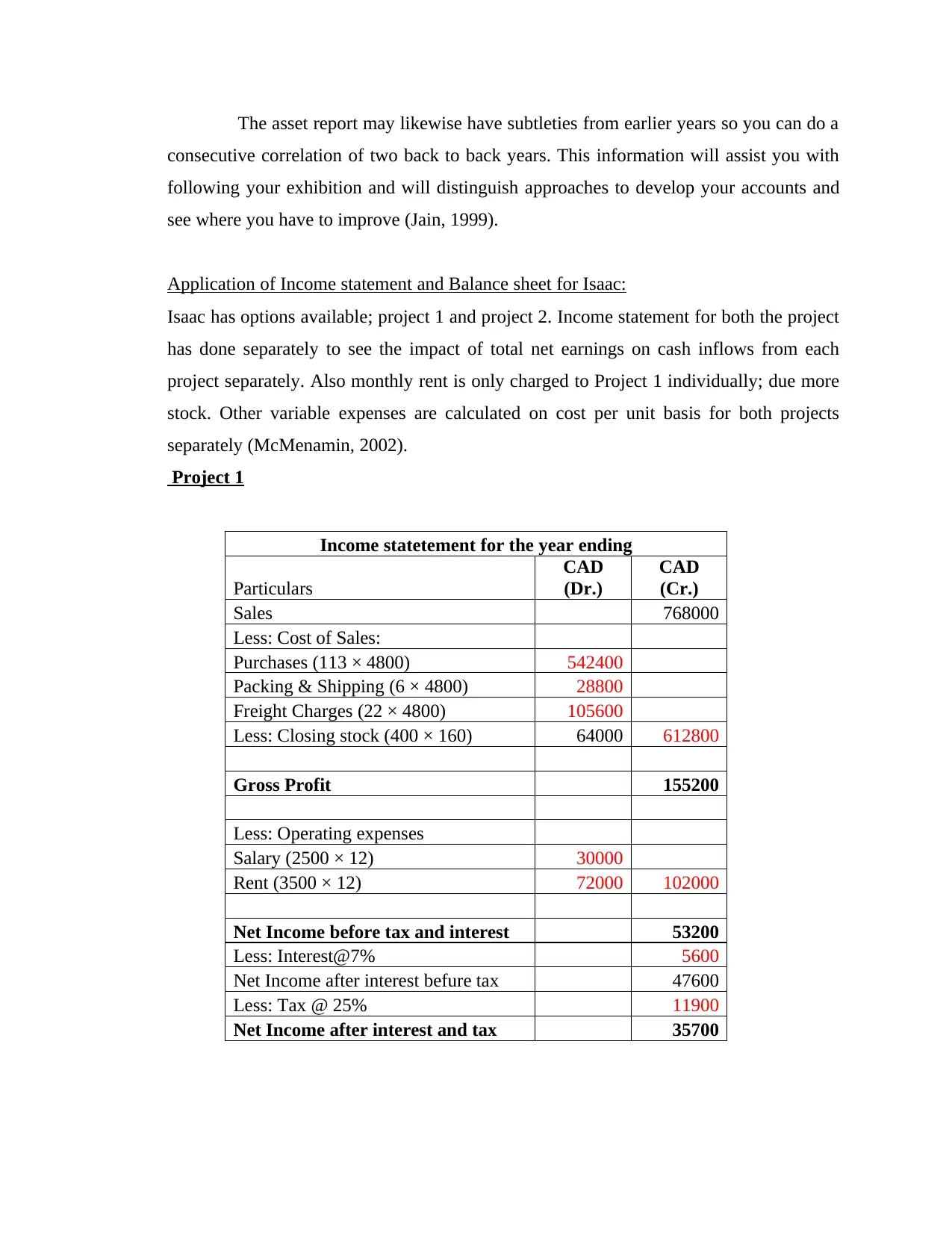

The asset report may likewise have subtleties from earlier years so you can do a

consecutive correlation of two back to back years. This information will assist you with

following your exhibition and will distinguish approaches to develop your accounts and

see where you have to improve (Jain, 1999).

Application of Income statement and Balance sheet for Isaac:

Isaac has options available; project 1 and project 2. Income statement for both the project

has done separately to see the impact of total net earnings on cash inflows from each

project separately. Also monthly rent is only charged to Project 1 individually; due more

stock. Other variable expenses are calculated on cost per unit basis for both projects

separately (McMenamin, 2002).

Project 1

Income statetement for the year ending

Particulars

CAD

(Dr.)

CAD

(Cr.)

Sales 768000

Less: Cost of Sales:

Purchases (113 × 4800) 542400

Packing & Shipping (6 × 4800) 28800

Freight Charges (22 × 4800) 105600

Less: Closing stock (400 × 160) 64000 612800

Gross Profit 155200

Less: Operating expenses

Salary (2500 × 12) 30000

Rent (3500 × 12) 72000 102000

Net Income before tax and interest 53200

Less: Interest@7% 5600

Net Income after interest befure tax 47600

Less: Tax @ 25% 11900

Net Income after interest and tax 35700

consecutive correlation of two back to back years. This information will assist you with

following your exhibition and will distinguish approaches to develop your accounts and

see where you have to improve (Jain, 1999).

Application of Income statement and Balance sheet for Isaac:

Isaac has options available; project 1 and project 2. Income statement for both the project

has done separately to see the impact of total net earnings on cash inflows from each

project separately. Also monthly rent is only charged to Project 1 individually; due more

stock. Other variable expenses are calculated on cost per unit basis for both projects

separately (McMenamin, 2002).

Project 1

Income statetement for the year ending

Particulars

CAD

(Dr.)

CAD

(Cr.)

Sales 768000

Less: Cost of Sales:

Purchases (113 × 4800) 542400

Packing & Shipping (6 × 4800) 28800

Freight Charges (22 × 4800) 105600

Less: Closing stock (400 × 160) 64000 612800

Gross Profit 155200

Less: Operating expenses

Salary (2500 × 12) 30000

Rent (3500 × 12) 72000 102000

Net Income before tax and interest 53200

Less: Interest@7% 5600

Net Income after interest befure tax 47600

Less: Tax @ 25% 11900

Net Income after interest and tax 35700

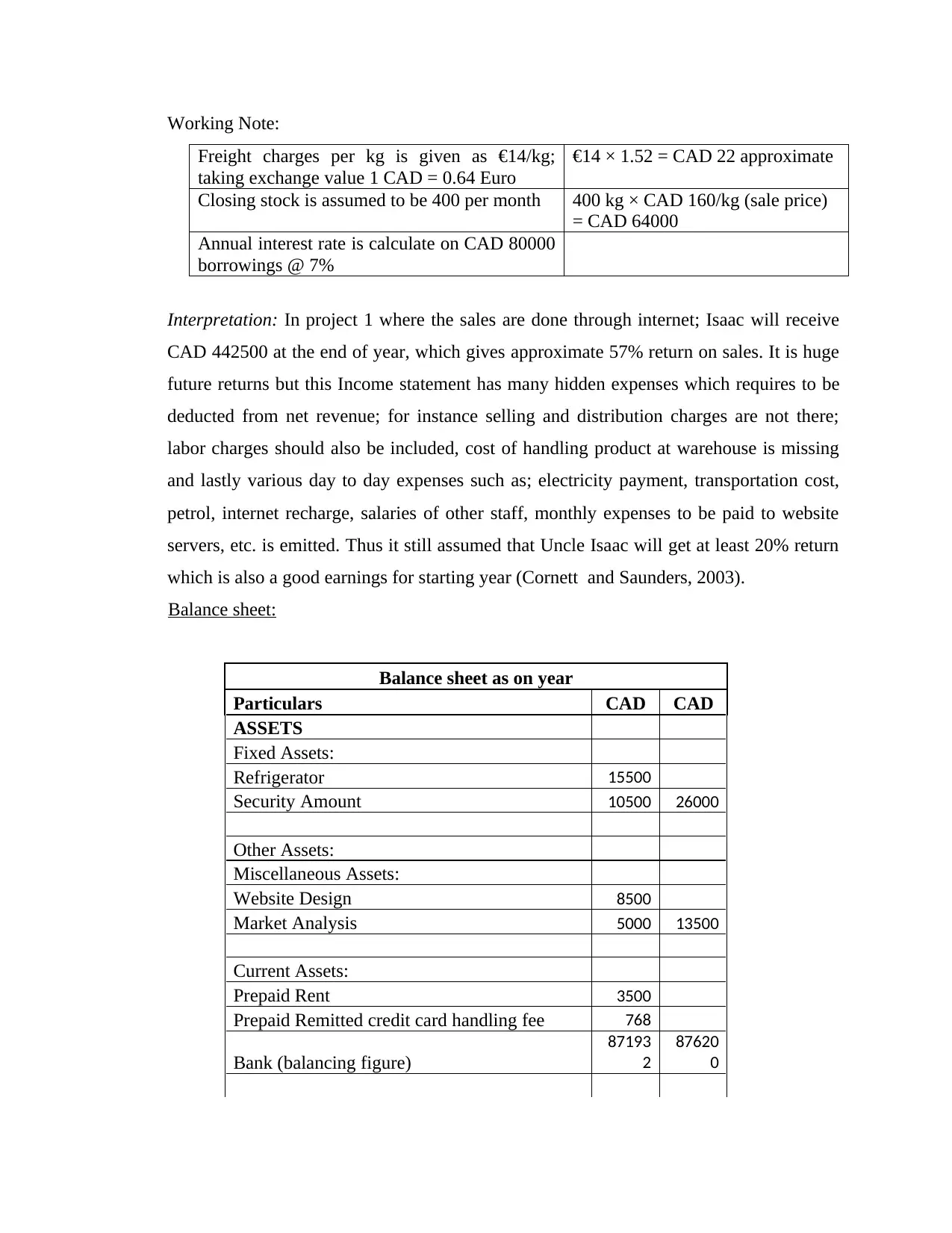

Working Note:

Freight charges per kg is given as €14/kg;

taking exchange value 1 CAD = 0.64 Euro

€14 × 1.52 = CAD 22 approximate

Closing stock is assumed to be 400 per month 400 kg × CAD 160/kg (sale price)

= CAD 64000

Annual interest rate is calculate on CAD 80000

borrowings @ 7%

Interpretation: In project 1 where the sales are done through internet; Isaac will receive

CAD 442500 at the end of year, which gives approximate 57% return on sales. It is huge

future returns but this Income statement has many hidden expenses which requires to be

deducted from net revenue; for instance selling and distribution charges are not there;

labor charges should also be included, cost of handling product at warehouse is missing

and lastly various day to day expenses such as; electricity payment, transportation cost,

petrol, internet recharge, salaries of other staff, monthly expenses to be paid to website

servers, etc. is emitted. Thus it still assumed that Uncle Isaac will get at least 20% return

which is also a good earnings for starting year (Cornett and Saunders, 2003).

Balance sheet:

Balance sheet as on year

Particulars CAD CAD

ASSETS

Fixed Assets:

Refrigerator 15500

Security Amount 10500 26000

Other Assets:

Miscellaneous Assets:

Website Design 8500

Market Analysis 5000 13500

Current Assets:

Prepaid Rent 3500

Prepaid Remitted credit card handling fee 768

Bank (balancing figure)

87193

2

87620

0

Freight charges per kg is given as €14/kg;

taking exchange value 1 CAD = 0.64 Euro

€14 × 1.52 = CAD 22 approximate

Closing stock is assumed to be 400 per month 400 kg × CAD 160/kg (sale price)

= CAD 64000

Annual interest rate is calculate on CAD 80000

borrowings @ 7%

Interpretation: In project 1 where the sales are done through internet; Isaac will receive

CAD 442500 at the end of year, which gives approximate 57% return on sales. It is huge

future returns but this Income statement has many hidden expenses which requires to be

deducted from net revenue; for instance selling and distribution charges are not there;

labor charges should also be included, cost of handling product at warehouse is missing

and lastly various day to day expenses such as; electricity payment, transportation cost,

petrol, internet recharge, salaries of other staff, monthly expenses to be paid to website

servers, etc. is emitted. Thus it still assumed that Uncle Isaac will get at least 20% return

which is also a good earnings for starting year (Cornett and Saunders, 2003).

Balance sheet:

Balance sheet as on year

Particulars CAD CAD

ASSETS

Fixed Assets:

Refrigerator 15500

Security Amount 10500 26000

Other Assets:

Miscellaneous Assets:

Website Design 8500

Market Analysis 5000 13500

Current Assets:

Prepaid Rent 3500

Prepaid Remitted credit card handling fee 768

Bank (balancing figure)

87193

2

87620

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

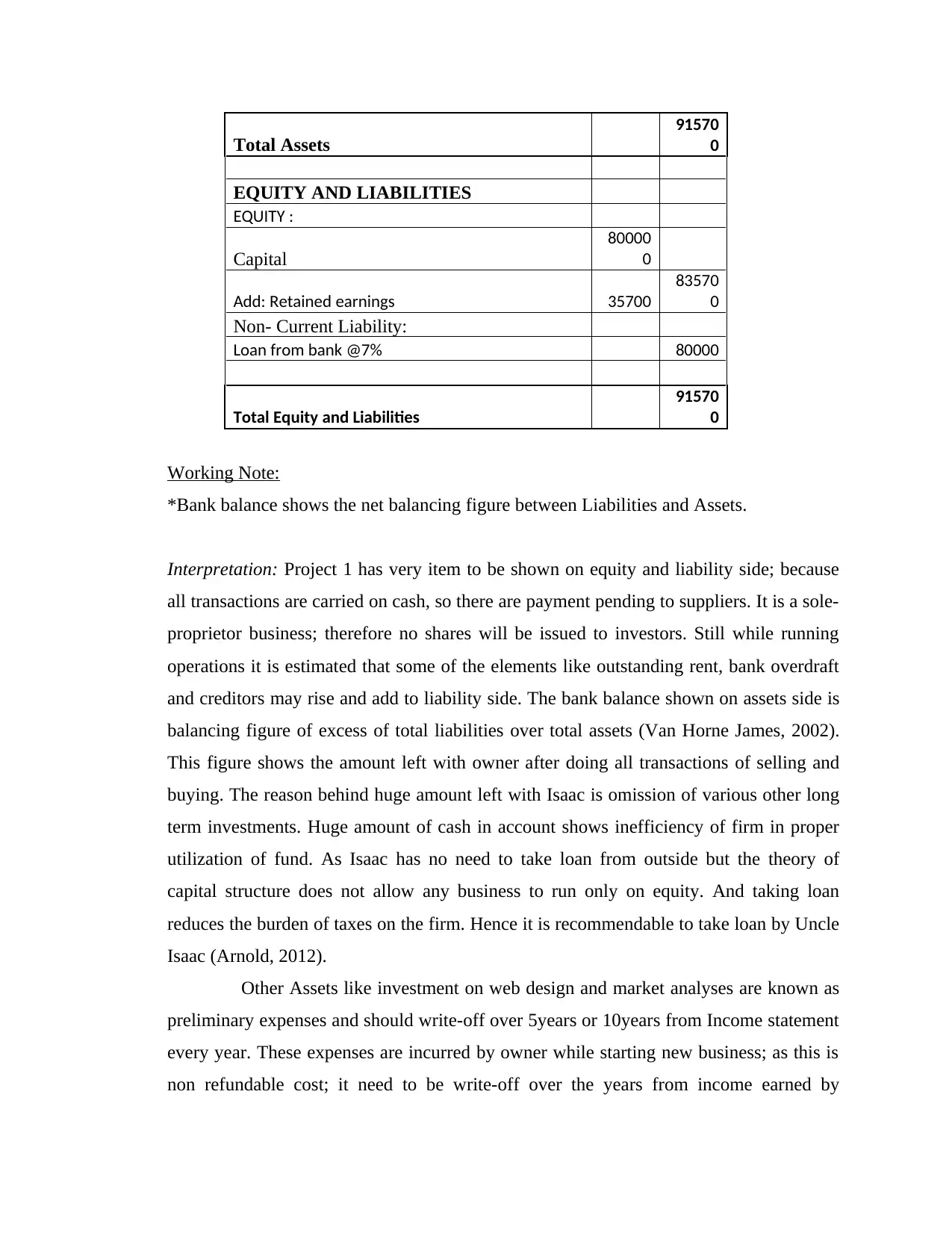

Total Assets

91570

0

EQUITY AND LIABILITIES

EQUITY :

Capital

80000

0

Add: Retained earnings 35700

83570

0

Non- Current Liability:

Loan from bank @7% 80000

Total Equity and Liabilities

91570

0

Working Note:

*Bank balance shows the net balancing figure between Liabilities and Assets.

Interpretation: Project 1 has very item to be shown on equity and liability side; because

all transactions are carried on cash, so there are payment pending to suppliers. It is a sole-

proprietor business; therefore no shares will be issued to investors. Still while running

operations it is estimated that some of the elements like outstanding rent, bank overdraft

and creditors may rise and add to liability side. The bank balance shown on assets side is

balancing figure of excess of total liabilities over total assets (Van Horne James, 2002).

This figure shows the amount left with owner after doing all transactions of selling and

buying. The reason behind huge amount left with Isaac is omission of various other long

term investments. Huge amount of cash in account shows inefficiency of firm in proper

utilization of fund. As Isaac has no need to take loan from outside but the theory of

capital structure does not allow any business to run only on equity. And taking loan

reduces the burden of taxes on the firm. Hence it is recommendable to take loan by Uncle

Isaac (Arnold, 2012).

Other Assets like investment on web design and market analyses are known as

preliminary expenses and should write-off over 5years or 10years from Income statement

every year. These expenses are incurred by owner while starting new business; as this is

non refundable cost; it need to be write-off over the years from income earned by

91570

0

EQUITY AND LIABILITIES

EQUITY :

Capital

80000

0

Add: Retained earnings 35700

83570

0

Non- Current Liability:

Loan from bank @7% 80000

Total Equity and Liabilities

91570

0

Working Note:

*Bank balance shows the net balancing figure between Liabilities and Assets.

Interpretation: Project 1 has very item to be shown on equity and liability side; because

all transactions are carried on cash, so there are payment pending to suppliers. It is a sole-

proprietor business; therefore no shares will be issued to investors. Still while running

operations it is estimated that some of the elements like outstanding rent, bank overdraft

and creditors may rise and add to liability side. The bank balance shown on assets side is

balancing figure of excess of total liabilities over total assets (Van Horne James, 2002).

This figure shows the amount left with owner after doing all transactions of selling and

buying. The reason behind huge amount left with Isaac is omission of various other long

term investments. Huge amount of cash in account shows inefficiency of firm in proper

utilization of fund. As Isaac has no need to take loan from outside but the theory of

capital structure does not allow any business to run only on equity. And taking loan

reduces the burden of taxes on the firm. Hence it is recommendable to take loan by Uncle

Isaac (Arnold, 2012).

Other Assets like investment on web design and market analyses are known as

preliminary expenses and should write-off over 5years or 10years from Income statement

every year. These expenses are incurred by owner while starting new business; as this is

non refundable cost; it need to be write-off over the years from income earned by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company and it is subject to get tax benefit and done before paying taxes by the company

(Besley and Brigham, 2008).

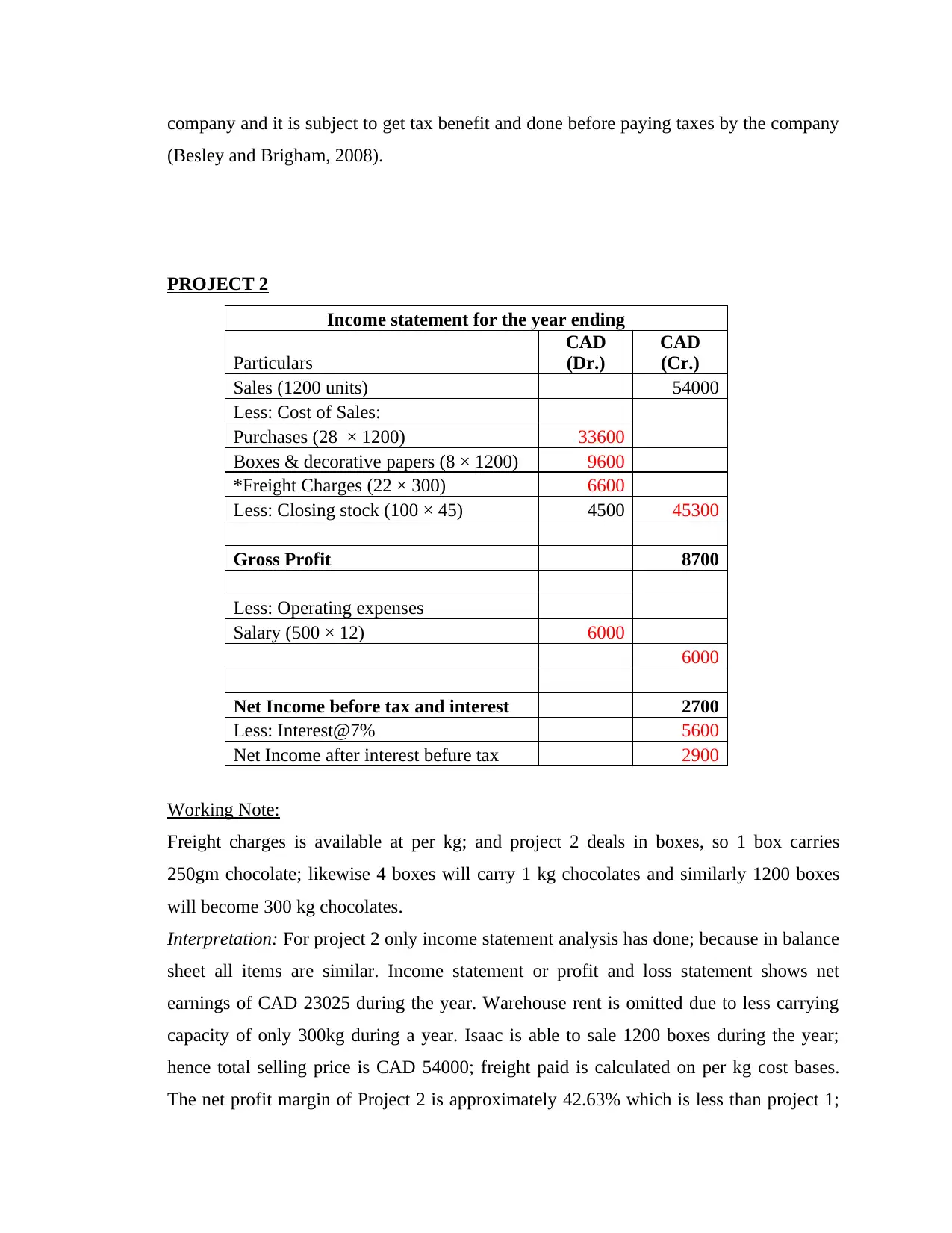

PROJECT 2

Income statement for the year ending

Particulars

CAD

(Dr.)

CAD

(Cr.)

Sales (1200 units) 54000

Less: Cost of Sales:

Purchases (28 × 1200) 33600

Boxes & decorative papers (8 × 1200) 9600

*Freight Charges (22 × 300) 6600

Less: Closing stock (100 × 45) 4500 45300

Gross Profit 8700

Less: Operating expenses

Salary (500 × 12) 6000

6000

Net Income before tax and interest 2700

Less: Interest@7% 5600

Net Income after interest befure tax 2900

Working Note:

Freight charges is available at per kg; and project 2 deals in boxes, so 1 box carries

250gm chocolate; likewise 4 boxes will carry 1 kg chocolates and similarly 1200 boxes

will become 300 kg chocolates.

Interpretation: For project 2 only income statement analysis has done; because in balance

sheet all items are similar. Income statement or profit and loss statement shows net

earnings of CAD 23025 during the year. Warehouse rent is omitted due to less carrying

capacity of only 300kg during a year. Isaac is able to sale 1200 boxes during the year;

hence total selling price is CAD 54000; freight paid is calculated on per kg cost bases.

The net profit margin of Project 2 is approximately 42.63% which is less than project 1;

(Besley and Brigham, 2008).

PROJECT 2

Income statement for the year ending

Particulars

CAD

(Dr.)

CAD

(Cr.)

Sales (1200 units) 54000

Less: Cost of Sales:

Purchases (28 × 1200) 33600

Boxes & decorative papers (8 × 1200) 9600

*Freight Charges (22 × 300) 6600

Less: Closing stock (100 × 45) 4500 45300

Gross Profit 8700

Less: Operating expenses

Salary (500 × 12) 6000

6000

Net Income before tax and interest 2700

Less: Interest@7% 5600

Net Income after interest befure tax 2900

Working Note:

Freight charges is available at per kg; and project 2 deals in boxes, so 1 box carries

250gm chocolate; likewise 4 boxes will carry 1 kg chocolates and similarly 1200 boxes

will become 300 kg chocolates.

Interpretation: For project 2 only income statement analysis has done; because in balance

sheet all items are similar. Income statement or profit and loss statement shows net

earnings of CAD 23025 during the year. Warehouse rent is omitted due to less carrying

capacity of only 300kg during a year. Isaac is able to sale 1200 boxes during the year;

hence total selling price is CAD 54000; freight paid is calculated on per kg cost bases.

The net profit margin of Project 2 is approximately 42.63% which is less than project 1;

the reason is fewer sales as it only able to supply 300 kg to Jade annually (Fabozzi and

Peterson, 2003).

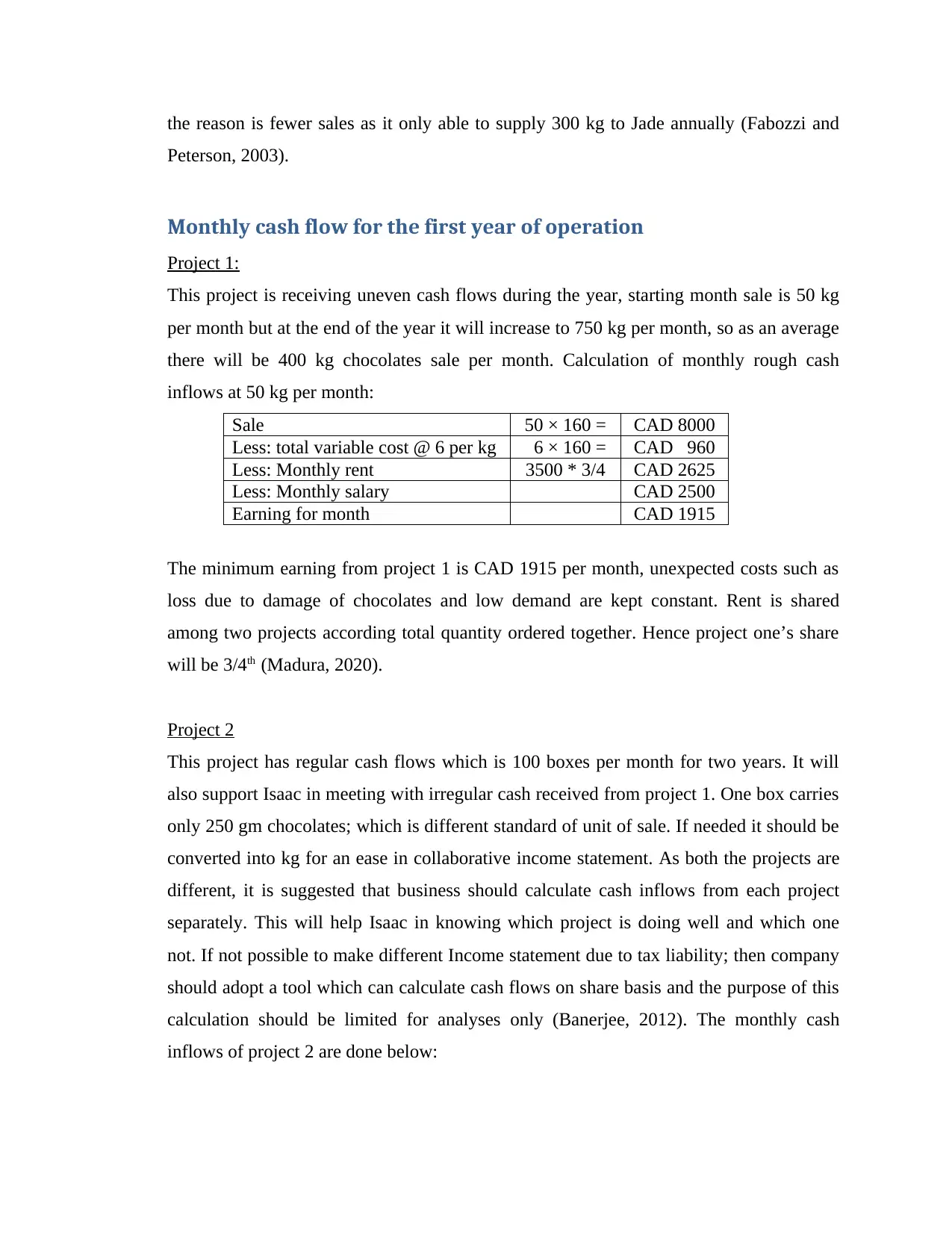

Monthly cash flow for the first year of operation

Project 1:

This project is receiving uneven cash flows during the year, starting month sale is 50 kg

per month but at the end of the year it will increase to 750 kg per month, so as an average

there will be 400 kg chocolates sale per month. Calculation of monthly rough cash

inflows at 50 kg per month:

Sale 50 × 160 = CAD 8000

Less: total variable cost @ 6 per kg 6 × 160 = CAD 960

Less: Monthly rent 3500 * 3/4 CAD 2625

Less: Monthly salary CAD 2500

Earning for month CAD 1915

The minimum earning from project 1 is CAD 1915 per month, unexpected costs such as

loss due to damage of chocolates and low demand are kept constant. Rent is shared

among two projects according total quantity ordered together. Hence project one’s share

will be 3/4th (Madura, 2020).

Project 2

This project has regular cash flows which is 100 boxes per month for two years. It will

also support Isaac in meeting with irregular cash received from project 1. One box carries

only 250 gm chocolates; which is different standard of unit of sale. If needed it should be

converted into kg for an ease in collaborative income statement. As both the projects are

different, it is suggested that business should calculate cash inflows from each project

separately. This will help Isaac in knowing which project is doing well and which one

not. If not possible to make different Income statement due to tax liability; then company

should adopt a tool which can calculate cash flows on share basis and the purpose of this

calculation should be limited for analyses only (Banerjee, 2012). The monthly cash

inflows of project 2 are done below:

Peterson, 2003).

Monthly cash flow for the first year of operation

Project 1:

This project is receiving uneven cash flows during the year, starting month sale is 50 kg

per month but at the end of the year it will increase to 750 kg per month, so as an average

there will be 400 kg chocolates sale per month. Calculation of monthly rough cash

inflows at 50 kg per month:

Sale 50 × 160 = CAD 8000

Less: total variable cost @ 6 per kg 6 × 160 = CAD 960

Less: Monthly rent 3500 * 3/4 CAD 2625

Less: Monthly salary CAD 2500

Earning for month CAD 1915

The minimum earning from project 1 is CAD 1915 per month, unexpected costs such as

loss due to damage of chocolates and low demand are kept constant. Rent is shared

among two projects according total quantity ordered together. Hence project one’s share

will be 3/4th (Madura, 2020).

Project 2

This project has regular cash flows which is 100 boxes per month for two years. It will

also support Isaac in meeting with irregular cash received from project 1. One box carries

only 250 gm chocolates; which is different standard of unit of sale. If needed it should be

converted into kg for an ease in collaborative income statement. As both the projects are

different, it is suggested that business should calculate cash inflows from each project

separately. This will help Isaac in knowing which project is doing well and which one

not. If not possible to make different Income statement due to tax liability; then company

should adopt a tool which can calculate cash flows on share basis and the purpose of this

calculation should be limited for analyses only (Banerjee, 2012). The monthly cash

inflows of project 2 are done below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.