Financial Management: Financial Ratio Analysis of Wizard Industries

VerifiedAdded on 2021/09/16

|8

|1703

|119

Report

AI Summary

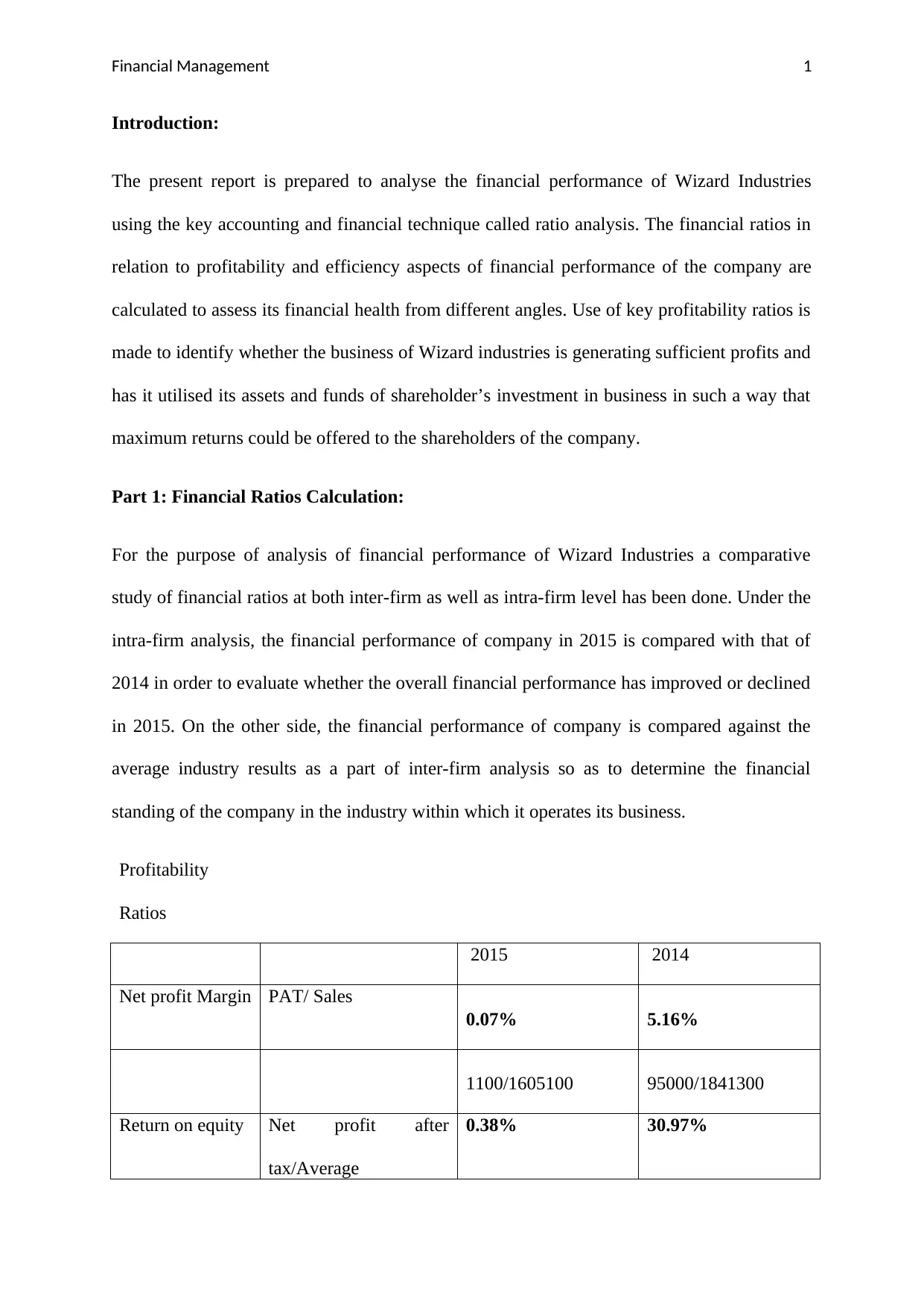

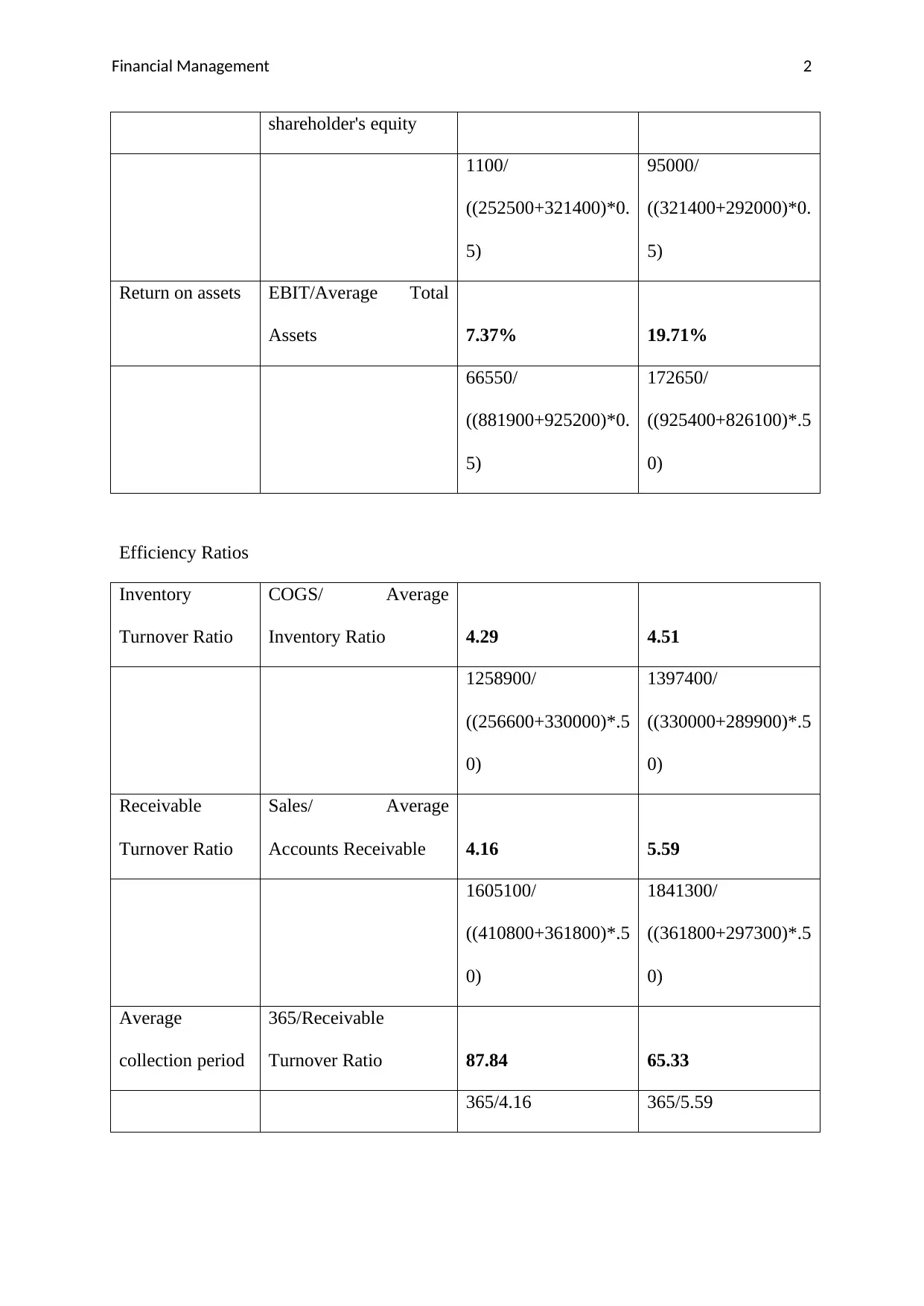

This report presents a financial ratio analysis of Wizard Industries, evaluating its performance in 2015 compared to 2014 and industry averages. The analysis covers profitability ratios (net profit margin, return on equity, return on assets) and efficiency ratios (inventory turnover, receivable turnover, average collection period). The report highlights a decline in financial performance in 2015, with lower profitability and efficiency compared to the previous year and industry benchmarks. The report also discusses the limitations of financial ratio analysis, such as the use of historical data and potential for poor comparability. The conclusion indicates that Wizard Industries' financial standing has weakened, suggesting a need for improved financial management strategies to enhance its market position and competitiveness. The report is well-structured, providing calculations, definitions, and comparisons to support its conclusions and recommendations. The analysis is based on the provided financial data for the company.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.