Financial Management Assignment: Solutions and Calculations

VerifiedAdded on 2021/05/31

|9

|1327

|41

Homework Assignment

AI Summary

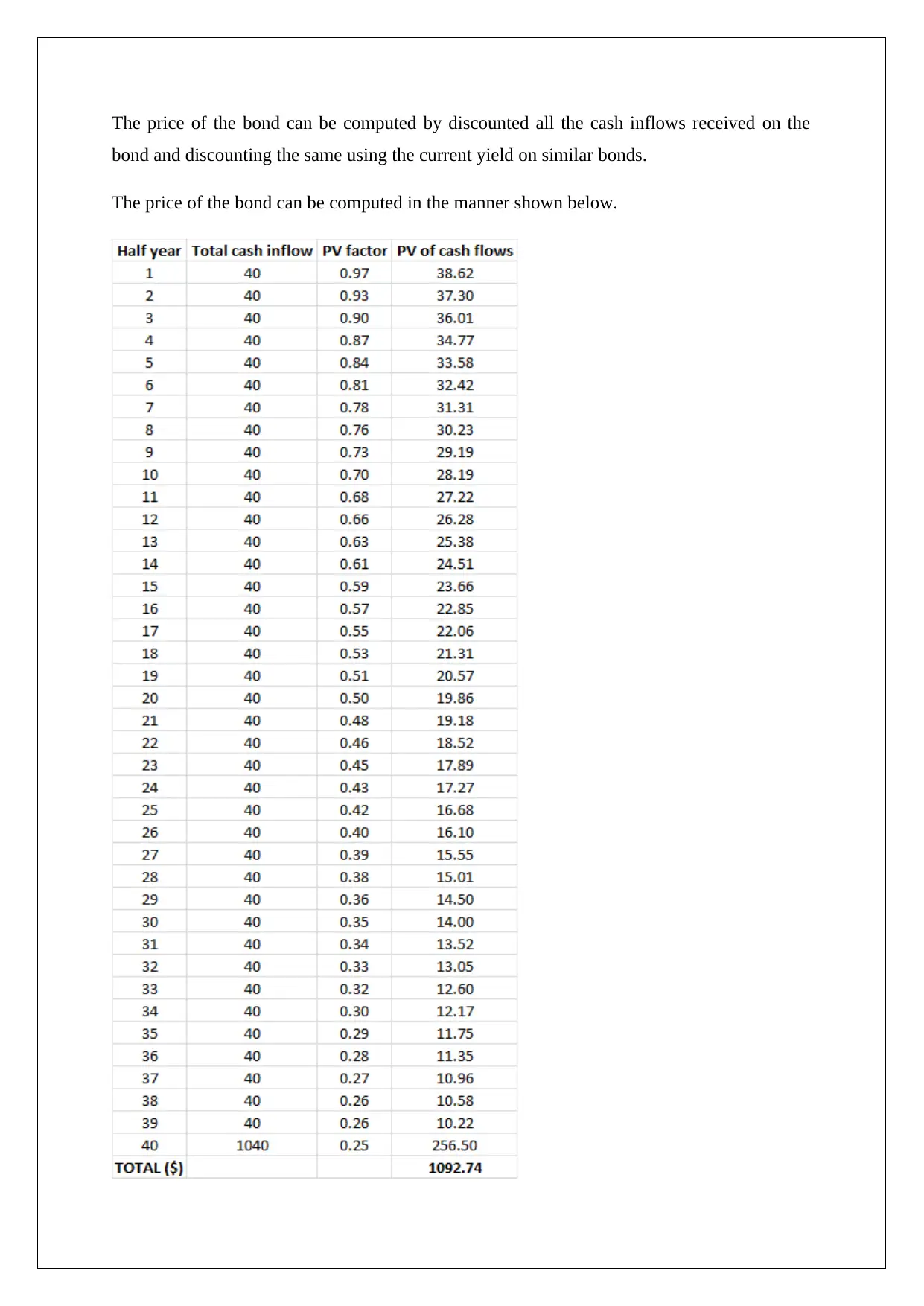

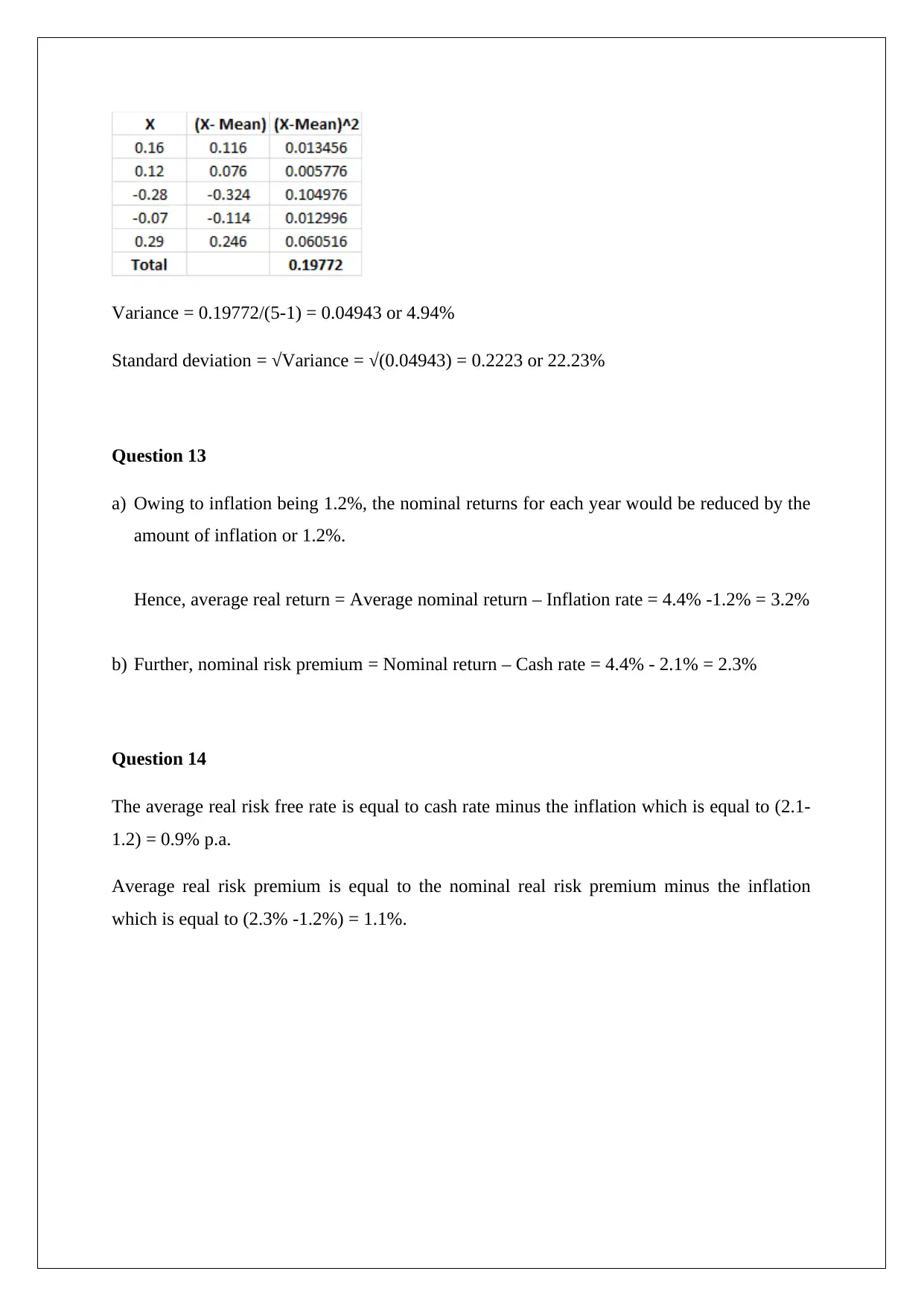

This document provides a comprehensive solution to a financial management assignment, addressing a range of topics including investment analysis, portfolio management, and valuation techniques. The solution begins with calculating the annual percentage yield on an investment, considering the compounding effect. It then proceeds to calculate holding period returns, portfolio beta, and the expected return on a stock using the CAPM model. Further, the solution involves bond valuation, including calculating the price of a bond and the effective annual rate. The assignment also explores stock valuation using the dividend discount model and concludes with an analysis of risk and return, including the calculation of average returns, variance, standard deviation, and real returns. The solutions are detailed, providing step-by-step calculations and explanations for each problem.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.