Financial Management Report: Valuation Techniques and Appraisal

VerifiedAdded on 2023/01/11

|14

|3890

|90

Report

AI Summary

This report delves into the realm of financial management, presenting a comprehensive analysis of various valuation and investment appraisal techniques. The report begins with an examination of valuation methods, including the price/earnings ratio, dividend valuation, and discounted cash flow, providing a detailed explanation of each technique and its practical application in mergers and acquisitions. Furthermore, it offers a critical analysis of these valuation methods, highlighting their strengths and weaknesses. The report then shifts its focus to investment appraisal techniques, such as the payback period, accounting rate of return, net present value, and internal rate of return. The report includes the application of these investment appraisal techniques, with detailed computations, and concludes with a critical evaluation of each method, offering insights into their feasibility and profitability for investment decisions. This report is a valuable resource for students seeking a comprehensive understanding of financial management principles and techniques.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 2........................................................................................................................................3

a) Price/earnings ratio.............................................................................................................3

b) Dividend valuation method................................................................................................3

c) Discounted cash flow method............................................................................................4

d) Critically analysing the various valuation techniques........................................................4

Question 3 .......................................................................................................................................7

1. Application of various investment appraisal techniques....................................................7

2. Critical evaluation of the various investment appraisal techniques.................................10

REFERENCES..............................................................................................................................13

Question 2........................................................................................................................................3

a) Price/earnings ratio.............................................................................................................3

b) Dividend valuation method................................................................................................3

c) Discounted cash flow method............................................................................................4

d) Critically analysing the various valuation techniques........................................................4

Question 3 .......................................................................................................................................7

1. Application of various investment appraisal techniques....................................................7

2. Critical evaluation of the various investment appraisal techniques.................................10

REFERENCES..............................................................................................................................13

Question 2

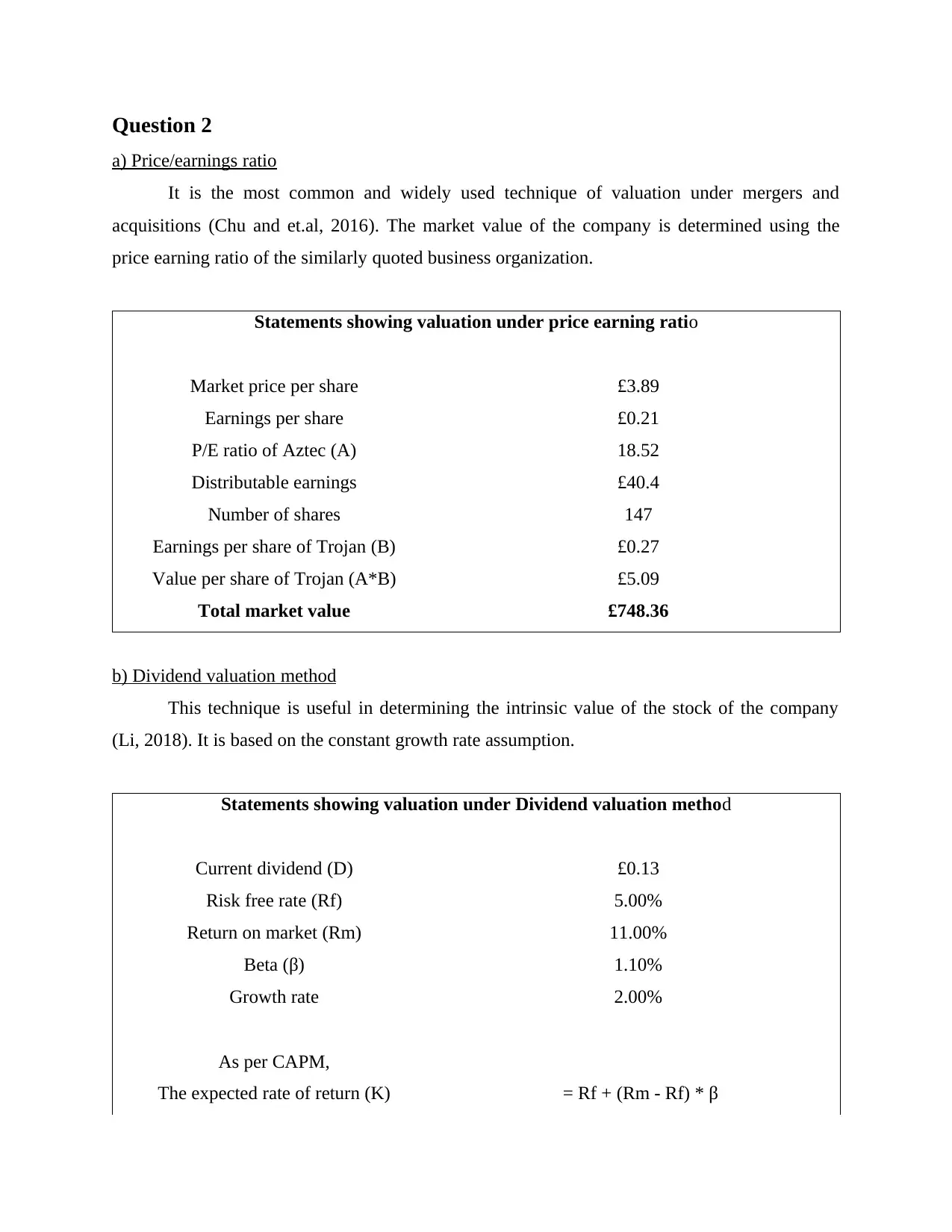

a) Price/earnings ratio

It is the most common and widely used technique of valuation under mergers and

acquisitions (Chu and et.al, 2016). The market value of the company is determined using the

price earning ratio of the similarly quoted business organization.

Statements showing valuation under price earning ratio

Market price per share £3.89

Earnings per share £0.21

P/E ratio of Aztec (A) 18.52

Distributable earnings £40.4

Number of shares 147

Earnings per share of Trojan (B) £0.27

Value per share of Trojan (A*B) £5.09

Total market value £748.36

b) Dividend valuation method

This technique is useful in determining the intrinsic value of the stock of the company

(Li, 2018). It is based on the constant growth rate assumption.

Statements showing valuation under Dividend valuation method

Current dividend (D) £0.13

Risk free rate (Rf) 5.00%

Return on market (Rm) 11.00%

Beta (β) 1.10%

Growth rate 2.00%

As per CAPM,

The expected rate of return (K) = Rf + (Rm - Rf) * β

a) Price/earnings ratio

It is the most common and widely used technique of valuation under mergers and

acquisitions (Chu and et.al, 2016). The market value of the company is determined using the

price earning ratio of the similarly quoted business organization.

Statements showing valuation under price earning ratio

Market price per share £3.89

Earnings per share £0.21

P/E ratio of Aztec (A) 18.52

Distributable earnings £40.4

Number of shares 147

Earnings per share of Trojan (B) £0.27

Value per share of Trojan (A*B) £5.09

Total market value £748.36

b) Dividend valuation method

This technique is useful in determining the intrinsic value of the stock of the company

(Li, 2018). It is based on the constant growth rate assumption.

Statements showing valuation under Dividend valuation method

Current dividend (D) £0.13

Risk free rate (Rf) 5.00%

Return on market (Rm) 11.00%

Beta (β) 1.10%

Growth rate 2.00%

As per CAPM,

The expected rate of return (K) = Rf + (Rm - Rf) * β

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 5% + (11% - 5%) * 1.1%

5.07%

Market price share = D * (1+g)/(K-g)

= 0.13 * (1+2%)/(5.07%-2%)

£4.32

Total market value = 4.32 * 147

£635.04

c) Discounted cash flow method

This is the valuation method under which the market price is determined using the

discounting rate on the free cash flow of the company (Schumacher and Klönne, 2018).

Statements showing valuation under Discounted cash flow method

Computation of free cash flow Amount in £

Net Income 40.4

Add: Non-cash expenses -

Less: Increase in working capital -

Less: Capital expenditure -

Free cash flow 40.4

Discounting rate 9.00%

Market price per share = Free cash flow / Discounting rate

448.89

Total market value = 448.89 * 147

£65986.67

5.07%

Market price share = D * (1+g)/(K-g)

= 0.13 * (1+2%)/(5.07%-2%)

£4.32

Total market value = 4.32 * 147

£635.04

c) Discounted cash flow method

This is the valuation method under which the market price is determined using the

discounting rate on the free cash flow of the company (Schumacher and Klönne, 2018).

Statements showing valuation under Discounted cash flow method

Computation of free cash flow Amount in £

Net Income 40.4

Add: Non-cash expenses -

Less: Increase in working capital -

Less: Capital expenditure -

Free cash flow 40.4

Discounting rate 9.00%

Market price per share = Free cash flow / Discounting rate

448.89

Total market value = 448.89 * 147

£65986.67

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d) Critically analysing the various valuation techniques

Price/earnings ratio

The price earning ratio is used for establishing the relationship between the share price of

the company and its earnings per share. This mainly states about what the willingness of the

market to pay for the profits of the company. It is useful for the purpose of valuing the stock of

the company in which investors are having interest. It helps the investors in knowing the

profitability of the business organization along with the estimation of its future valuation. It is

basically the comparison between the present share price of the company to its per share earnings

(Zhou, 2017). The higher PE ratio indicates the expectation of higher earnings and growth in the

future in comparison to the those companies having low P/E ratio. In mergers and acquisitions.

While valuing the company's price earning ratio, it is most important to compare the ratios of the

company within the same industry It also provides information how much amount the investor is

interested and willing to pay per pound of earnings.

There are certain issues to be considered while using this method of valuation. The first

and foremost important thing is that it can be easily manipulated by the organization's accounting

practices. Also, it is based on the net income which is actually not the cash flow and does not

consider the balance sheet and the capital structure of the organization pertaining to the

investment. It is based on the earnings per share on which it cannot be easily relied as it might

not represent the actual performance of the organization. There are various adjustment that can

be done by the management for ensuring it doesn't fall out of the stock price. The major aspect to

be considered is that it does not take into account the growth aspect of the earnings. It has lack of

visibility about the future performance of the business and it is mainly backward looking. The

large companies provide glimpse on the future performance at least for 1 year for understanding

the stock value. But, there are lot of companies that does not provide any guidance on the future

performance of the organization. Thus, it is important to not depend upon this technique.

Dividend valuation method

The dividend growth model is a stock valuation method which is used in evaluating the

intrinsic value of the stocks of the company. It does not take into consideration the current

market conditions. It is based on certain assumptions such as the business growth model is

stable, that is, there is no major change in the business operation. The company grows at a

constant rate along with stable financial burden and the entire amount of free cash flow is paid as

Price/earnings ratio

The price earning ratio is used for establishing the relationship between the share price of

the company and its earnings per share. This mainly states about what the willingness of the

market to pay for the profits of the company. It is useful for the purpose of valuing the stock of

the company in which investors are having interest. It helps the investors in knowing the

profitability of the business organization along with the estimation of its future valuation. It is

basically the comparison between the present share price of the company to its per share earnings

(Zhou, 2017). The higher PE ratio indicates the expectation of higher earnings and growth in the

future in comparison to the those companies having low P/E ratio. In mergers and acquisitions.

While valuing the company's price earning ratio, it is most important to compare the ratios of the

company within the same industry It also provides information how much amount the investor is

interested and willing to pay per pound of earnings.

There are certain issues to be considered while using this method of valuation. The first

and foremost important thing is that it can be easily manipulated by the organization's accounting

practices. Also, it is based on the net income which is actually not the cash flow and does not

consider the balance sheet and the capital structure of the organization pertaining to the

investment. It is based on the earnings per share on which it cannot be easily relied as it might

not represent the actual performance of the organization. There are various adjustment that can

be done by the management for ensuring it doesn't fall out of the stock price. The major aspect to

be considered is that it does not take into account the growth aspect of the earnings. It has lack of

visibility about the future performance of the business and it is mainly backward looking. The

large companies provide glimpse on the future performance at least for 1 year for understanding

the stock value. But, there are lot of companies that does not provide any guidance on the future

performance of the organization. Thus, it is important to not depend upon this technique.

Dividend valuation method

The dividend growth model is a stock valuation method which is used in evaluating the

intrinsic value of the stocks of the company. It does not take into consideration the current

market conditions. It is based on certain assumptions such as the business growth model is

stable, that is, there is no major change in the business operation. The company grows at a

constant rate along with stable financial burden and the entire amount of free cash flow is paid as

dividend (Poniachek, 2019). This method is mainly suitable for valuing the minority stakes

rather than the entire company. This technique is useful for the companies having large amount

of cash inflow and the company is stable with respect to the financial leverage. The valuation can

be easily done as the inputs required are readily available.

Besides certain advantages, it has some drawbacks as well. The major limitation of this

technique is that it is based on certain assumption with respect to the constant growth in

dividend, reasonable cost of capital and the is based on historical data related to paid dividends.

There are chances that the management may be pursuing the overambitious dividend policy with

the core purpose of high valuation at the expense of not reinvesting in the business for providing

support in its future operations. The future changes in the business operation and performance is

not taken into account. The calculations are done which is completely based on the future

assumption and are also subject to market situations which are dynamic in nature and this

contributes towards the major drawback of this technique. Therefore, of having success with the

companies having higher cash flow, this technique is not suitable for the other companies which

are growing very fast as it is not possible to include the possible fluctuations that are coming

across such as change in the dividend rate. This approach is not apt for the organization's that are

in segregation but it is suitable for the organizations having heavy cash inflow and cash outflow.

This model may result into negative value in case the expected rate of return is lower than the

growth rate. Also, the value per share leads to infinity when the expected rate of return and

growth rate are having the same value which is by concept is wrong or unsound. Also, since this

technique excludes the external factors, there are chances of stocks of the company being

undervalued despite the fact that the company is having a strong brand and steady growth.

Discounted cash flow method

The main principle behind using this valuation technique is that the organization's value

is based upon its ability to generate and grow the cash flow for its investors. In mergers and

acquisitions, this technique is used in determining the enterprise value by forecasting the future

cash flows for a specific period. It also involves calculating the terminal value at the end of the

specific period and then the free cash flow and the terminal value is being discounted to the

present value using the weighted average cost of capital (WACC). If this technique is used

correctly, then it is considered as the most valuable method for the purpose of valuing the

businesses as this method is forward looking and less dependent upon the past results

rather than the entire company. This technique is useful for the companies having large amount

of cash inflow and the company is stable with respect to the financial leverage. The valuation can

be easily done as the inputs required are readily available.

Besides certain advantages, it has some drawbacks as well. The major limitation of this

technique is that it is based on certain assumption with respect to the constant growth in

dividend, reasonable cost of capital and the is based on historical data related to paid dividends.

There are chances that the management may be pursuing the overambitious dividend policy with

the core purpose of high valuation at the expense of not reinvesting in the business for providing

support in its future operations. The future changes in the business operation and performance is

not taken into account. The calculations are done which is completely based on the future

assumption and are also subject to market situations which are dynamic in nature and this

contributes towards the major drawback of this technique. Therefore, of having success with the

companies having higher cash flow, this technique is not suitable for the other companies which

are growing very fast as it is not possible to include the possible fluctuations that are coming

across such as change in the dividend rate. This approach is not apt for the organization's that are

in segregation but it is suitable for the organizations having heavy cash inflow and cash outflow.

This model may result into negative value in case the expected rate of return is lower than the

growth rate. Also, the value per share leads to infinity when the expected rate of return and

growth rate are having the same value which is by concept is wrong or unsound. Also, since this

technique excludes the external factors, there are chances of stocks of the company being

undervalued despite the fact that the company is having a strong brand and steady growth.

Discounted cash flow method

The main principle behind using this valuation technique is that the organization's value

is based upon its ability to generate and grow the cash flow for its investors. In mergers and

acquisitions, this technique is used in determining the enterprise value by forecasting the future

cash flows for a specific period. It also involves calculating the terminal value at the end of the

specific period and then the free cash flow and the terminal value is being discounted to the

present value using the weighted average cost of capital (WACC). If this technique is used

correctly, then it is considered as the most valuable method for the purpose of valuing the

businesses as this method is forward looking and less dependent upon the past results

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(RAHADJENG, 2018). Also, this technique is inward looking and is less affected by the external

factors and the cash flows are also least affected by the accounting practices and various other

components of business is considered in valuation. While using this approach, it is very essential

to understand the impact of assumptions while determining the free cash flow and terminal value

which helps in accurate valuation.

Just like other techniques, this approach is also having few limitations which are required

to be taken into account while using this method for valuation. This method is extremely

sensitive to various assumptions in relation to the perpetual growth rate and discounting rate.

Any minor deviation in the same would lead to inaccurate valuation. This is best suited in the

situation when there is high degree of confidence with respect to the future cash flows. But it is

totally depends upon the company's ability to predict its future which sometimes become

difficult to forecast the sales, expenses and the capital expenditure and investment with some

certainty. Forecasting the cash flows for the coming years is difficult and putting them as

perpetually is near to impossible. There are greater chances of error if the input items are not

properly accounted for. Another criticism of discounted cash flow model is that terminal value

comprises much of the total value which is approximately 65-75%. Thus, a small variation in

assumptions in a terminal year might have a crucial impact over the actual valuation result. It is

not suitable for the short term investing purpose as it focusses towards the long term value

creation.

After conducting the crucial analysis of all these valuation techniques which are mainly

used for the valuation of the company, it can be said that the DCF method is more appropriate

for Aztec to use because it similar to P/E ratio but just the fact that it considers the projected cash

flows which accounts for inflation as well, providing accurate result.

Question 3

1. Application of various investment appraisal techniques

a. The Payback Period

This method is used by the business organization for the purpose of determining the time

frame in which the company would be able to recover the amount it has invested initially in the

project (Abor, 2017).

Computation of payback period

factors and the cash flows are also least affected by the accounting practices and various other

components of business is considered in valuation. While using this approach, it is very essential

to understand the impact of assumptions while determining the free cash flow and terminal value

which helps in accurate valuation.

Just like other techniques, this approach is also having few limitations which are required

to be taken into account while using this method for valuation. This method is extremely

sensitive to various assumptions in relation to the perpetual growth rate and discounting rate.

Any minor deviation in the same would lead to inaccurate valuation. This is best suited in the

situation when there is high degree of confidence with respect to the future cash flows. But it is

totally depends upon the company's ability to predict its future which sometimes become

difficult to forecast the sales, expenses and the capital expenditure and investment with some

certainty. Forecasting the cash flows for the coming years is difficult and putting them as

perpetually is near to impossible. There are greater chances of error if the input items are not

properly accounted for. Another criticism of discounted cash flow model is that terminal value

comprises much of the total value which is approximately 65-75%. Thus, a small variation in

assumptions in a terminal year might have a crucial impact over the actual valuation result. It is

not suitable for the short term investing purpose as it focusses towards the long term value

creation.

After conducting the crucial analysis of all these valuation techniques which are mainly

used for the valuation of the company, it can be said that the DCF method is more appropriate

for Aztec to use because it similar to P/E ratio but just the fact that it considers the projected cash

flows which accounts for inflation as well, providing accurate result.

Question 3

1. Application of various investment appraisal techniques

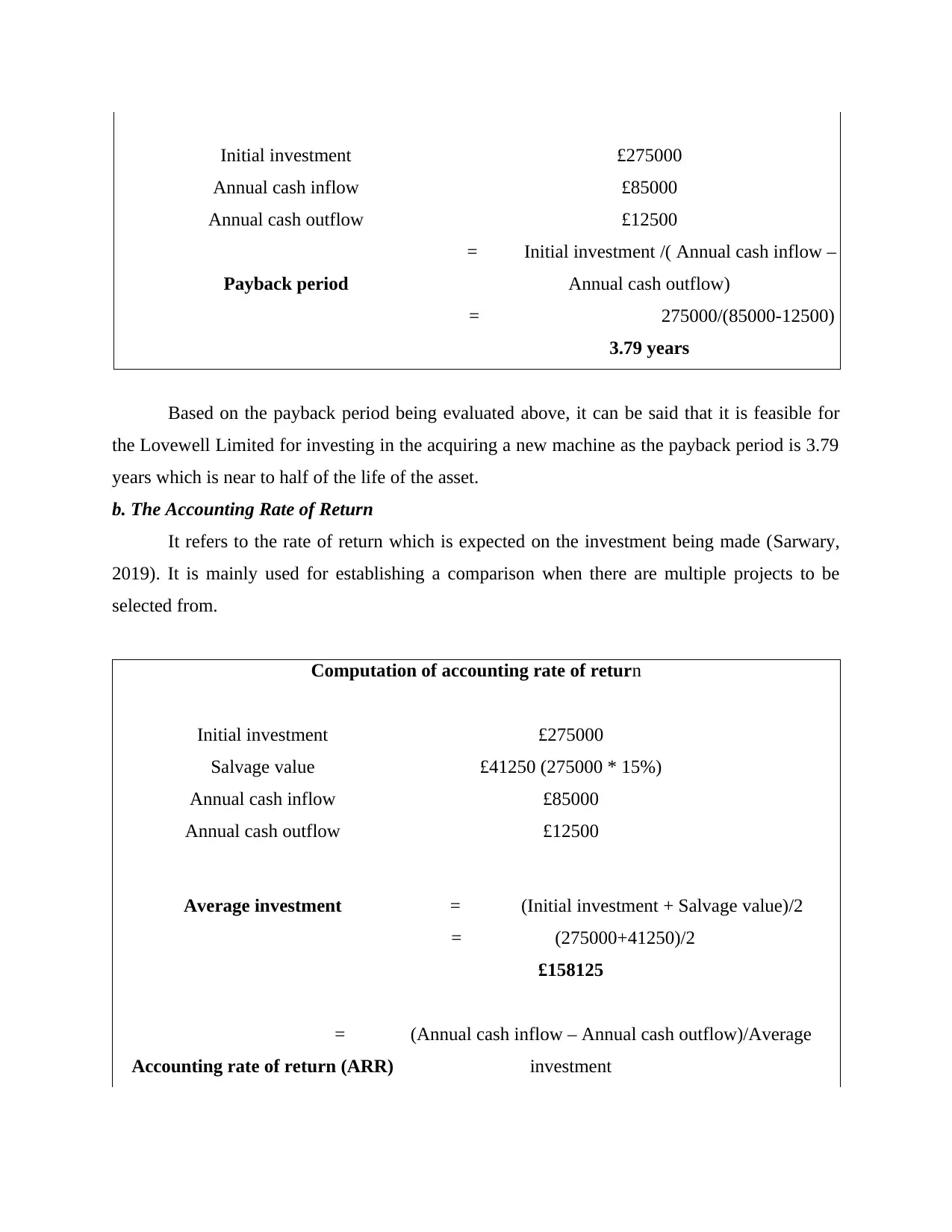

a. The Payback Period

This method is used by the business organization for the purpose of determining the time

frame in which the company would be able to recover the amount it has invested initially in the

project (Abor, 2017).

Computation of payback period

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Initial investment £275000

Annual cash inflow £85000

Annual cash outflow £12500

Payback period

= Initial investment /( Annual cash inflow –

Annual cash outflow)

= 275000/(85000-12500)

3.79 years

Based on the payback period being evaluated above, it can be said that it is feasible for

the Lovewell Limited for investing in the acquiring a new machine as the payback period is 3.79

years which is near to half of the life of the asset.

b. The Accounting Rate of Return

It refers to the rate of return which is expected on the investment being made (Sarwary,

2019). It is mainly used for establishing a comparison when there are multiple projects to be

selected from.

Computation of accounting rate of return

Initial investment £275000

Salvage value £41250 (275000 * 15%)

Annual cash inflow £85000

Annual cash outflow £12500

Average investment = (Initial investment + Salvage value)/2

= (275000+41250)/2

£158125

Accounting rate of return (ARR)

= (Annual cash inflow – Annual cash outflow)/Average

investment

Annual cash inflow £85000

Annual cash outflow £12500

Payback period

= Initial investment /( Annual cash inflow –

Annual cash outflow)

= 275000/(85000-12500)

3.79 years

Based on the payback period being evaluated above, it can be said that it is feasible for

the Lovewell Limited for investing in the acquiring a new machine as the payback period is 3.79

years which is near to half of the life of the asset.

b. The Accounting Rate of Return

It refers to the rate of return which is expected on the investment being made (Sarwary,

2019). It is mainly used for establishing a comparison when there are multiple projects to be

selected from.

Computation of accounting rate of return

Initial investment £275000

Salvage value £41250 (275000 * 15%)

Annual cash inflow £85000

Annual cash outflow £12500

Average investment = (Initial investment + Salvage value)/2

= (275000+41250)/2

£158125

Accounting rate of return (ARR)

= (Annual cash inflow – Annual cash outflow)/Average

investment

= (85000-12500)/158125

ARR 45.85%

From above, it can be interpreted that the company should make an investment in

machinery as the accounting rate of return which is 45.85% is much more than the cost of capital

of 12%. Thus, it is very beneficial for the company Lovewell Limited.

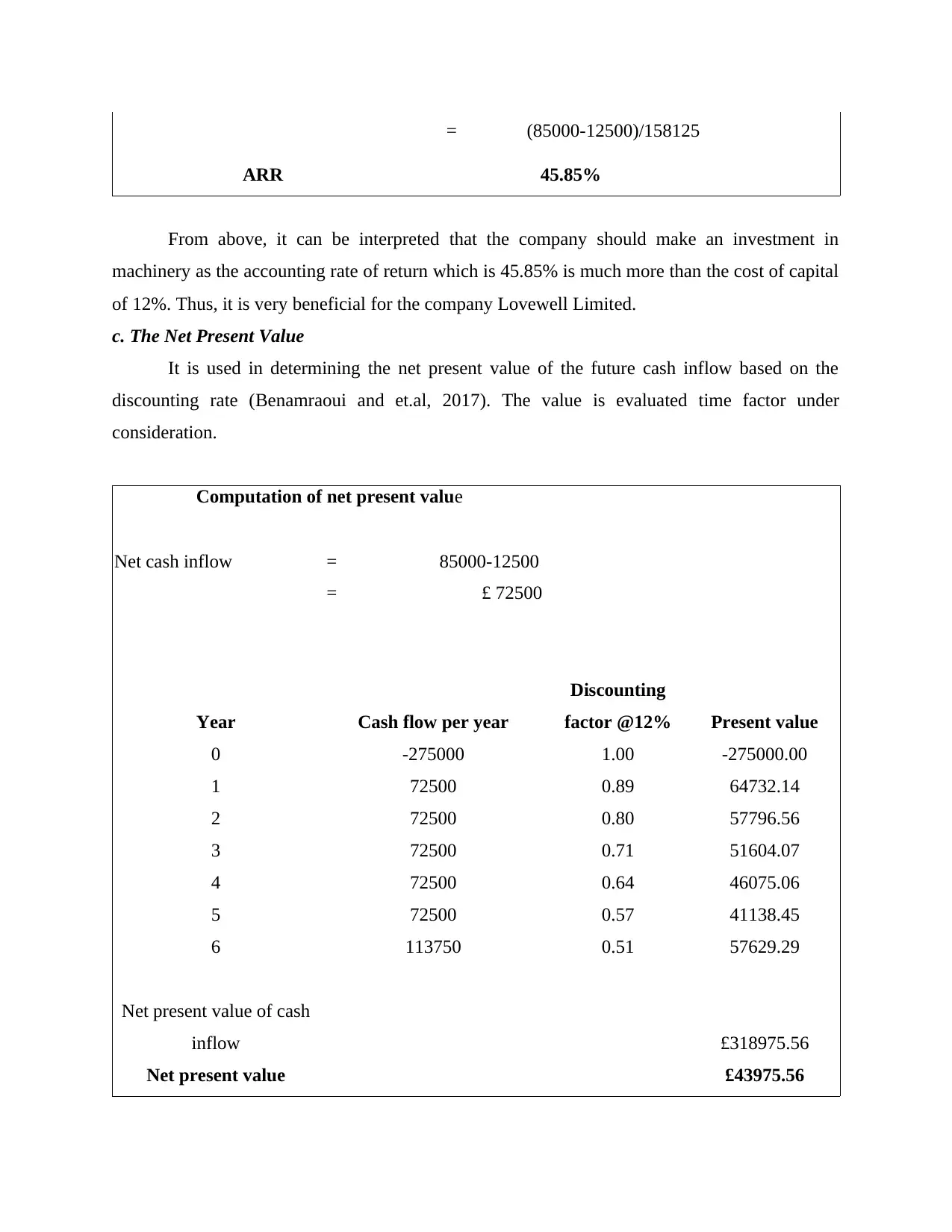

c. The Net Present Value

It is used in determining the net present value of the future cash inflow based on the

discounting rate (Benamraoui and et.al, 2017). The value is evaluated time factor under

consideration.

Computation of net present value

Net cash inflow = 85000-12500

= £ 72500

Year Cash flow per year

Discounting

factor @12% Present value

0 -275000 1.00 -275000.00

1 72500 0.89 64732.14

2 72500 0.80 57796.56

3 72500 0.71 51604.07

4 72500 0.64 46075.06

5 72500 0.57 41138.45

6 113750 0.51 57629.29

Net present value of cash

inflow £318975.56

Net present value £43975.56

ARR 45.85%

From above, it can be interpreted that the company should make an investment in

machinery as the accounting rate of return which is 45.85% is much more than the cost of capital

of 12%. Thus, it is very beneficial for the company Lovewell Limited.

c. The Net Present Value

It is used in determining the net present value of the future cash inflow based on the

discounting rate (Benamraoui and et.al, 2017). The value is evaluated time factor under

consideration.

Computation of net present value

Net cash inflow = 85000-12500

= £ 72500

Year Cash flow per year

Discounting

factor @12% Present value

0 -275000 1.00 -275000.00

1 72500 0.89 64732.14

2 72500 0.80 57796.56

3 72500 0.71 51604.07

4 72500 0.64 46075.06

5 72500 0.57 41138.45

6 113750 0.51 57629.29

Net present value of cash

inflow £318975.56

Net present value £43975.56

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

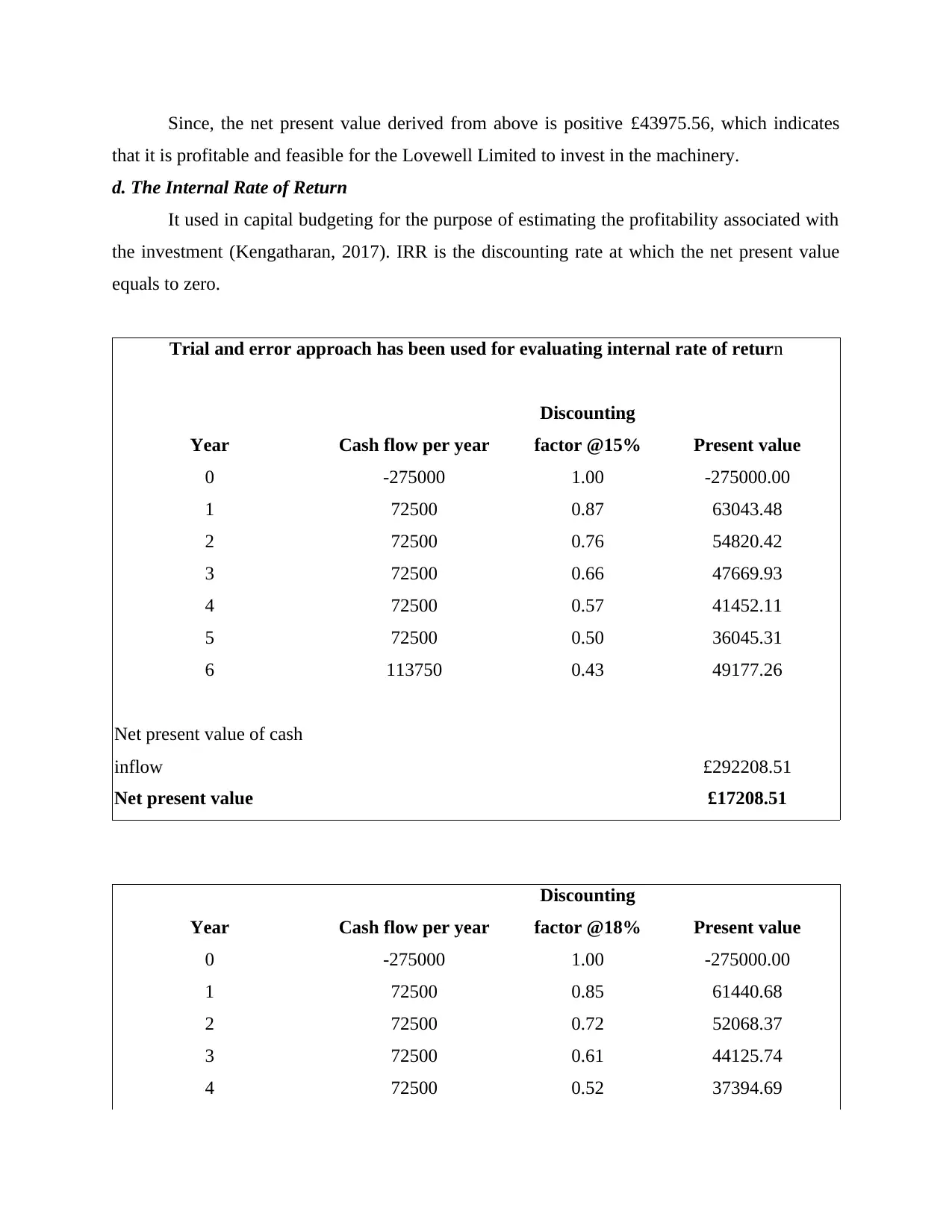

Since, the net present value derived from above is positive £43975.56, which indicates

that it is profitable and feasible for the Lovewell Limited to invest in the machinery.

d. The Internal Rate of Return

It used in capital budgeting for the purpose of estimating the profitability associated with

the investment (Kengatharan, 2017). IRR is the discounting rate at which the net present value

equals to zero.

Trial and error approach has been used for evaluating internal rate of return

Year Cash flow per year

Discounting

factor @15% Present value

0 -275000 1.00 -275000.00

1 72500 0.87 63043.48

2 72500 0.76 54820.42

3 72500 0.66 47669.93

4 72500 0.57 41452.11

5 72500 0.50 36045.31

6 113750 0.43 49177.26

Net present value of cash

inflow £292208.51

Net present value £17208.51

Year Cash flow per year

Discounting

factor @18% Present value

0 -275000 1.00 -275000.00

1 72500 0.85 61440.68

2 72500 0.72 52068.37

3 72500 0.61 44125.74

4 72500 0.52 37394.69

that it is profitable and feasible for the Lovewell Limited to invest in the machinery.

d. The Internal Rate of Return

It used in capital budgeting for the purpose of estimating the profitability associated with

the investment (Kengatharan, 2017). IRR is the discounting rate at which the net present value

equals to zero.

Trial and error approach has been used for evaluating internal rate of return

Year Cash flow per year

Discounting

factor @15% Present value

0 -275000 1.00 -275000.00

1 72500 0.87 63043.48

2 72500 0.76 54820.42

3 72500 0.66 47669.93

4 72500 0.57 41452.11

5 72500 0.50 36045.31

6 113750 0.43 49177.26

Net present value of cash

inflow £292208.51

Net present value £17208.51

Year Cash flow per year

Discounting

factor @18% Present value

0 -275000 1.00 -275000.00

1 72500 0.85 61440.68

2 72500 0.72 52068.37

3 72500 0.61 44125.74

4 72500 0.52 37394.69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

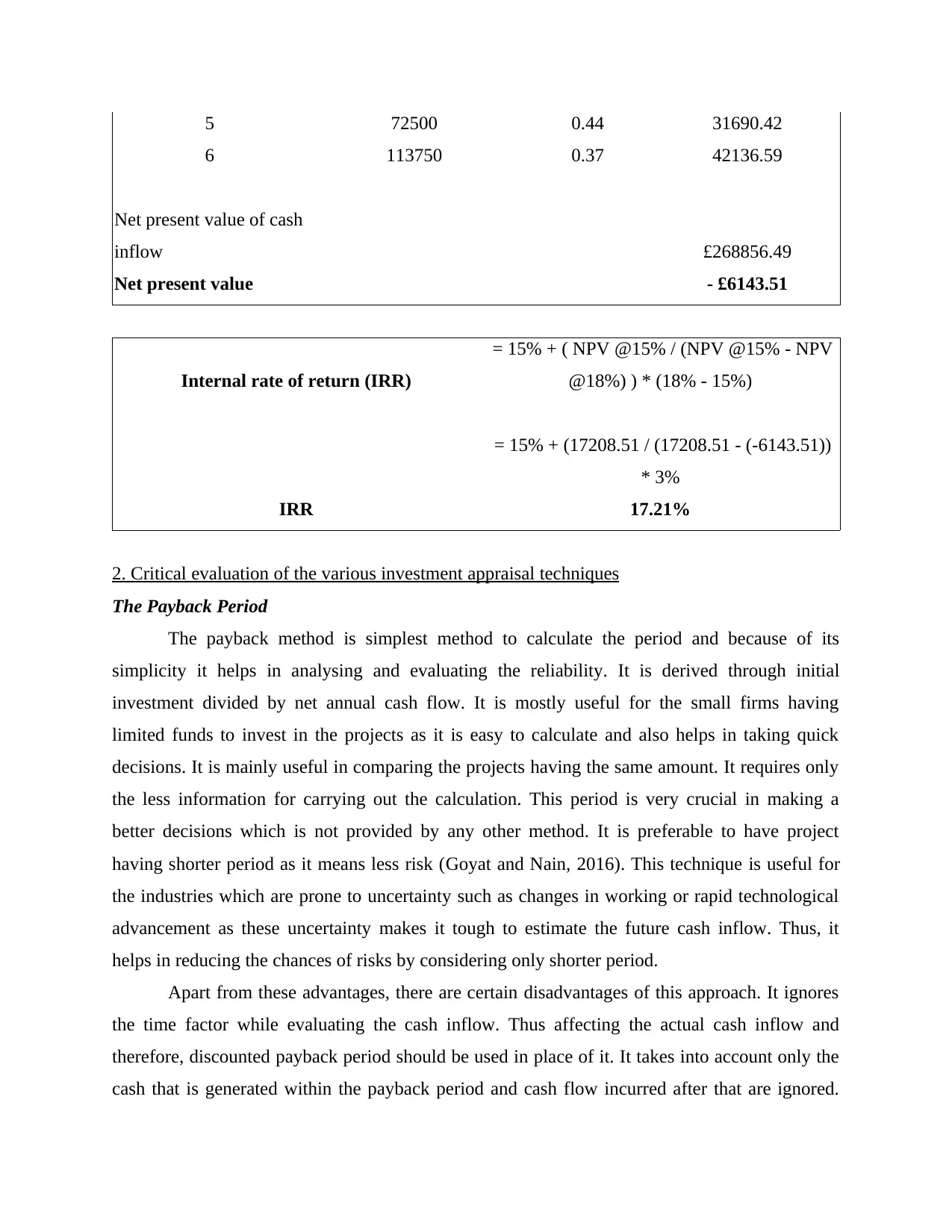

5 72500 0.44 31690.42

6 113750 0.37 42136.59

Net present value of cash

inflow £268856.49

Net present value - £6143.51

Internal rate of return (IRR)

= 15% + ( NPV @15% / (NPV @15% - NPV

@18%) ) * (18% - 15%)

= 15% + (17208.51 / (17208.51 - (-6143.51))

* 3%

IRR 17.21%

2. Critical evaluation of the various investment appraisal techniques

The Payback Period

The payback method is simplest method to calculate the period and because of its

simplicity it helps in analysing and evaluating the reliability. It is derived through initial

investment divided by net annual cash flow. It is mostly useful for the small firms having

limited funds to invest in the projects as it is easy to calculate and also helps in taking quick

decisions. It is mainly useful in comparing the projects having the same amount. It requires only

the less information for carrying out the calculation. This period is very crucial in making a

better decisions which is not provided by any other method. It is preferable to have project

having shorter period as it means less risk (Goyat and Nain, 2016). This technique is useful for

the industries which are prone to uncertainty such as changes in working or rapid technological

advancement as these uncertainty makes it tough to estimate the future cash inflow. Thus, it

helps in reducing the chances of risks by considering only shorter period.

Apart from these advantages, there are certain disadvantages of this approach. It ignores

the time factor while evaluating the cash inflow. Thus affecting the actual cash inflow and

therefore, discounted payback period should be used in place of it. It takes into account only the

cash that is generated within the payback period and cash flow incurred after that are ignored.

6 113750 0.37 42136.59

Net present value of cash

inflow £268856.49

Net present value - £6143.51

Internal rate of return (IRR)

= 15% + ( NPV @15% / (NPV @15% - NPV

@18%) ) * (18% - 15%)

= 15% + (17208.51 / (17208.51 - (-6143.51))

* 3%

IRR 17.21%

2. Critical evaluation of the various investment appraisal techniques

The Payback Period

The payback method is simplest method to calculate the period and because of its

simplicity it helps in analysing and evaluating the reliability. It is derived through initial

investment divided by net annual cash flow. It is mostly useful for the small firms having

limited funds to invest in the projects as it is easy to calculate and also helps in taking quick

decisions. It is mainly useful in comparing the projects having the same amount. It requires only

the less information for carrying out the calculation. This period is very crucial in making a

better decisions which is not provided by any other method. It is preferable to have project

having shorter period as it means less risk (Goyat and Nain, 2016). This technique is useful for

the industries which are prone to uncertainty such as changes in working or rapid technological

advancement as these uncertainty makes it tough to estimate the future cash inflow. Thus, it

helps in reducing the chances of risks by considering only shorter period.

Apart from these advantages, there are certain disadvantages of this approach. It ignores

the time factor while evaluating the cash inflow. Thus affecting the actual cash inflow and

therefore, discounted payback period should be used in place of it. It takes into account only the

cash that is generated within the payback period and cash flow incurred after that are ignored.

This leads to overlooking at the lucrative project that has the potential to generate higher cash

flows in future years. Also, the project with shorter payback period does not guarantee profits.

The Accounting Rate of Return

Like payback period, it is also very easy to calculate. It requires only total profits over the

life of the project and the initial amount invested. It provides a clear picture with respect to the

profitability attached to the project. In comparison to other investment appraisal techniques, only

this technique considers the net operating profits for the purpose of deriving rate of return. The

accounting rate of return (ARR), makes the decision-making much easier on account of each

individual capital project. The project with high accounting rate of return (ARR) is selected and

lower one is rejected (Uwah and Asuquo, 2016). It measures the profitability associated with the

project which is advantageous for the shareholders and the owners.

The major drawback of this method is that it ignores the time value of money. It also does

not consider the external factors which might have a huge impact over the profits of the project.

Along with this, ignores the time period in which the profit is being earned. For instance, 21%

rate of return in 10 years would be considered favourable in comparison to the 18% rate of return

in 7 years. This is not proper as the longer the project more is the risk attached to it. Not

applicable in the projects where the investment is being made in parts and also when the

investment is done in installments at different interval of time. It ignores the terminal value

which is very essential in accounting.

The Net Present Value

The NPV of the project is determined by deducting present value of cash outflow from

the present value of cash inflow. This method is widely used by the business organizations. It

takes under consideration each cash inflow over the life of the project unlike payback period

method. It is very effective in measuring the profitability of the projects and the project is

selected only when it is having a higher NPV. The net present value method uses discounting

rate for determining the NPV and the other risk factors associated with the undertaking such as

business risk, financial risk and operational risk.

Besides these benefits, it is prone to certain limitations as well. It ignores the sunk cost

which is incurred before initiating the project such as R&D expenses (Chadha and Sharma,

2019). These costs are sometimes very high and ignoring it might be difficult for the finance

team. The discounting rate which is being used by the management for determining the present

flows in future years. Also, the project with shorter payback period does not guarantee profits.

The Accounting Rate of Return

Like payback period, it is also very easy to calculate. It requires only total profits over the

life of the project and the initial amount invested. It provides a clear picture with respect to the

profitability attached to the project. In comparison to other investment appraisal techniques, only

this technique considers the net operating profits for the purpose of deriving rate of return. The

accounting rate of return (ARR), makes the decision-making much easier on account of each

individual capital project. The project with high accounting rate of return (ARR) is selected and

lower one is rejected (Uwah and Asuquo, 2016). It measures the profitability associated with the

project which is advantageous for the shareholders and the owners.

The major drawback of this method is that it ignores the time value of money. It also does

not consider the external factors which might have a huge impact over the profits of the project.

Along with this, ignores the time period in which the profit is being earned. For instance, 21%

rate of return in 10 years would be considered favourable in comparison to the 18% rate of return

in 7 years. This is not proper as the longer the project more is the risk attached to it. Not

applicable in the projects where the investment is being made in parts and also when the

investment is done in installments at different interval of time. It ignores the terminal value

which is very essential in accounting.

The Net Present Value

The NPV of the project is determined by deducting present value of cash outflow from

the present value of cash inflow. This method is widely used by the business organizations. It

takes under consideration each cash inflow over the life of the project unlike payback period

method. It is very effective in measuring the profitability of the projects and the project is

selected only when it is having a higher NPV. The net present value method uses discounting

rate for determining the NPV and the other risk factors associated with the undertaking such as

business risk, financial risk and operational risk.

Besides these benefits, it is prone to certain limitations as well. It ignores the sunk cost

which is incurred before initiating the project such as R&D expenses (Chadha and Sharma,

2019). These costs are sometimes very high and ignoring it might be difficult for the finance

team. The discounting rate which is being used by the management for determining the present

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.