APC308 Financial Management Assignment: Investment and Mergers

VerifiedAdded on 2022/12/01

|14

|3780

|235

Homework Assignment

AI Summary

This financial management assignment addresses investment appraisal techniques and mergers and acquisitions. The solution begins with calculations related to investment appraisal, including payback period, accounting rate of return, net present value, and internal rate of return, providing a comprehensive analysis of a machine acquisition scenario for Super Tasty Limited. It then discusses the effect of a proposal on Super Tasty Limited, focusing on equity repurchase and dividend payments. The assignment further evaluates the benefits and limitations of each investment appraisal technique. The second part of the solution delves into mergers and takeovers, examining the price/earnings ratio, discounted cash flow method, and dividend valuation method. The assignment concludes with a critical analysis of these valuation methods, offering a complete overview of financial management principles.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 2 - Investment Appraisal Techniques.........................................................................3

(a) Calculations regarding investment appraisal...............................................................3

(b) Discussing the effect of proposal on Super Tasty Limited..........................................5

(c) Evaluating the benefits and limitations of each investment appraisal technique........6

Question 3 – Mergers and Takeovers.........................................................................................9

a) Price/earnings ratio............................................................................................................9

b) Discounted cash flow method (DCF)..............................................................................10

c) Dividend valuation method..............................................................................................11

d) Critical analysis................................................................................................................12

REFERENCES.........................................................................................................................14

Question 2 - Investment Appraisal Techniques.........................................................................3

(a) Calculations regarding investment appraisal...............................................................3

(b) Discussing the effect of proposal on Super Tasty Limited..........................................5

(c) Evaluating the benefits and limitations of each investment appraisal technique........6

Question 3 – Mergers and Takeovers.........................................................................................9

a) Price/earnings ratio............................................................................................................9

b) Discounted cash flow method (DCF)..............................................................................10

c) Dividend valuation method..............................................................................................11

d) Critical analysis................................................................................................................12

REFERENCES.........................................................................................................................14

Question 2 - Investment Appraisal Techniques

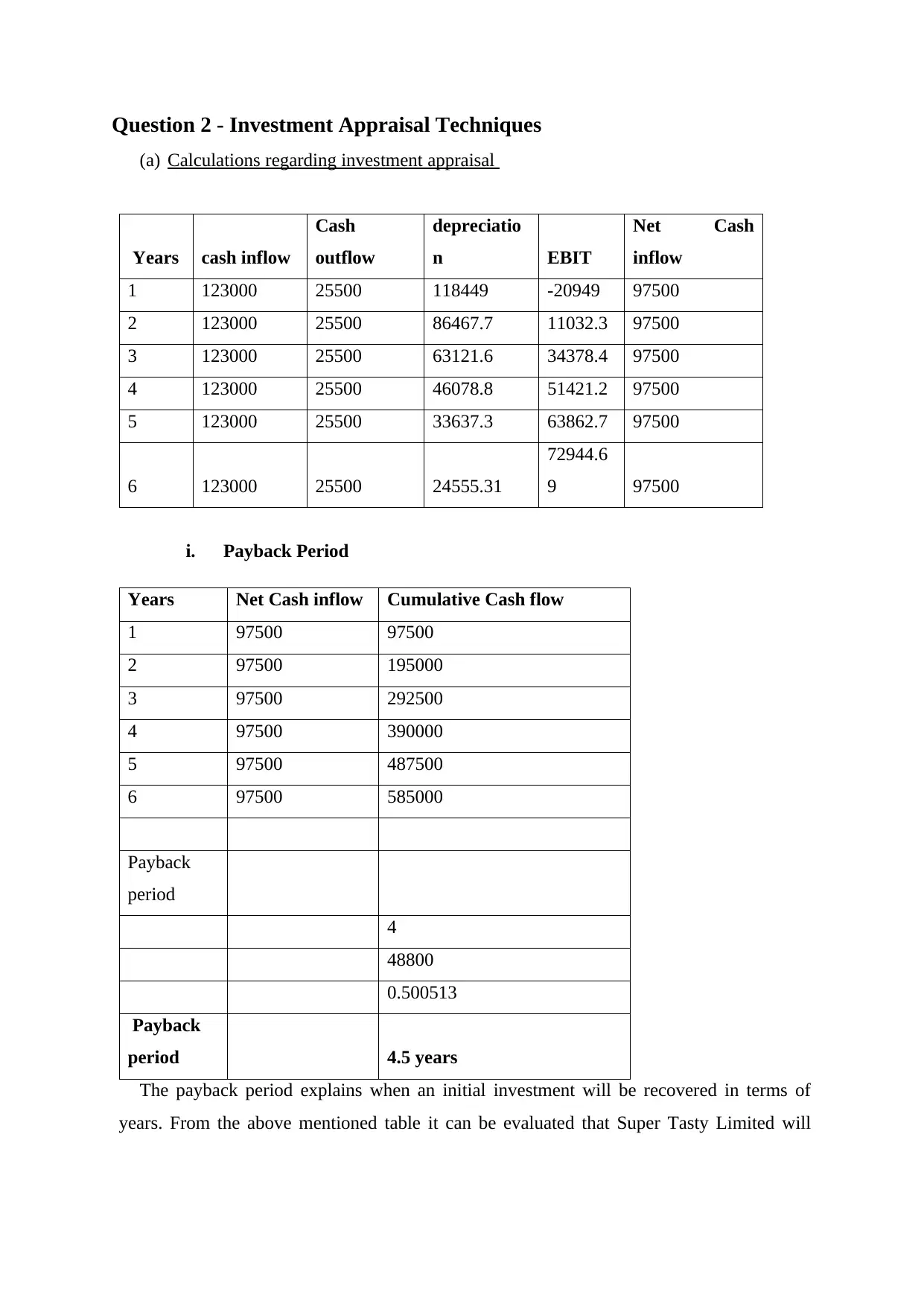

(a) Calculations regarding investment appraisal

Years cash inflow

Cash

outflow

depreciatio

n EBIT

Net Cash

inflow

1 123000 25500 118449 -20949 97500

2 123000 25500 86467.7 11032.3 97500

3 123000 25500 63121.6 34378.4 97500

4 123000 25500 46078.8 51421.2 97500

5 123000 25500 33637.3 63862.7 97500

6 123000 25500 24555.31

72944.6

9 97500

i. Payback Period

Years Net Cash inflow Cumulative Cash flow

1 97500 97500

2 97500 195000

3 97500 292500

4 97500 390000

5 97500 487500

6 97500 585000

Payback

period

4

48800

0.500513

Payback

period 4.5 years

The payback period explains when an initial investment will be recovered in terms of

years. From the above mentioned table it can be evaluated that Super Tasty Limited will

(a) Calculations regarding investment appraisal

Years cash inflow

Cash

outflow

depreciatio

n EBIT

Net Cash

inflow

1 123000 25500 118449 -20949 97500

2 123000 25500 86467.7 11032.3 97500

3 123000 25500 63121.6 34378.4 97500

4 123000 25500 46078.8 51421.2 97500

5 123000 25500 33637.3 63862.7 97500

6 123000 25500 24555.31

72944.6

9 97500

i. Payback Period

Years Net Cash inflow Cumulative Cash flow

1 97500 97500

2 97500 195000

3 97500 292500

4 97500 390000

5 97500 487500

6 97500 585000

Payback

period

4

48800

0.500513

Payback

period 4.5 years

The payback period explains when an initial investment will be recovered in terms of

years. From the above mentioned table it can be evaluated that Super Tasty Limited will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recover its initial investment of 438700 in 4.5 years. The indications are showing positive

outcome according to the Payback period of capital appraisal technique.

ii. Accounting Rate of Return

Initial Investment 438700

Life of machine 6

Depreciated

amount

62149.1

6

Average

investment

250424.

6

Average EAT 97500

ARR 0.39%

This is calculated for the purpose of identifying the expected rate of return n

investment. The above illustrated table shows the 0.39% of ARR.

iii. Net Present Value

Years Net Cash inflow

PV factor

@13%

Discounted cash

flow

1 97500 0.884955752 86283.18

2 97500 0.783146683 76356.80

3 97500 0.693050162 67572.39

4 97500 0.613318728 59798.57

5 97500 0.542759936 52919.09

6 97500 0.480318527 46831.05

Sum of discounted

cash flow 389761.10

Initial investment 438700

outcome according to the Payback period of capital appraisal technique.

ii. Accounting Rate of Return

Initial Investment 438700

Life of machine 6

Depreciated

amount

62149.1

6

Average

investment

250424.

6

Average EAT 97500

ARR 0.39%

This is calculated for the purpose of identifying the expected rate of return n

investment. The above illustrated table shows the 0.39% of ARR.

iii. Net Present Value

Years Net Cash inflow

PV factor

@13%

Discounted cash

flow

1 97500 0.884955752 86283.18

2 97500 0.783146683 76356.80

3 97500 0.693050162 67572.39

4 97500 0.613318728 59798.57

5 97500 0.542759936 52919.09

6 97500 0.480318527 46831.05

Sum of discounted

cash flow 389761.10

Initial investment 438700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

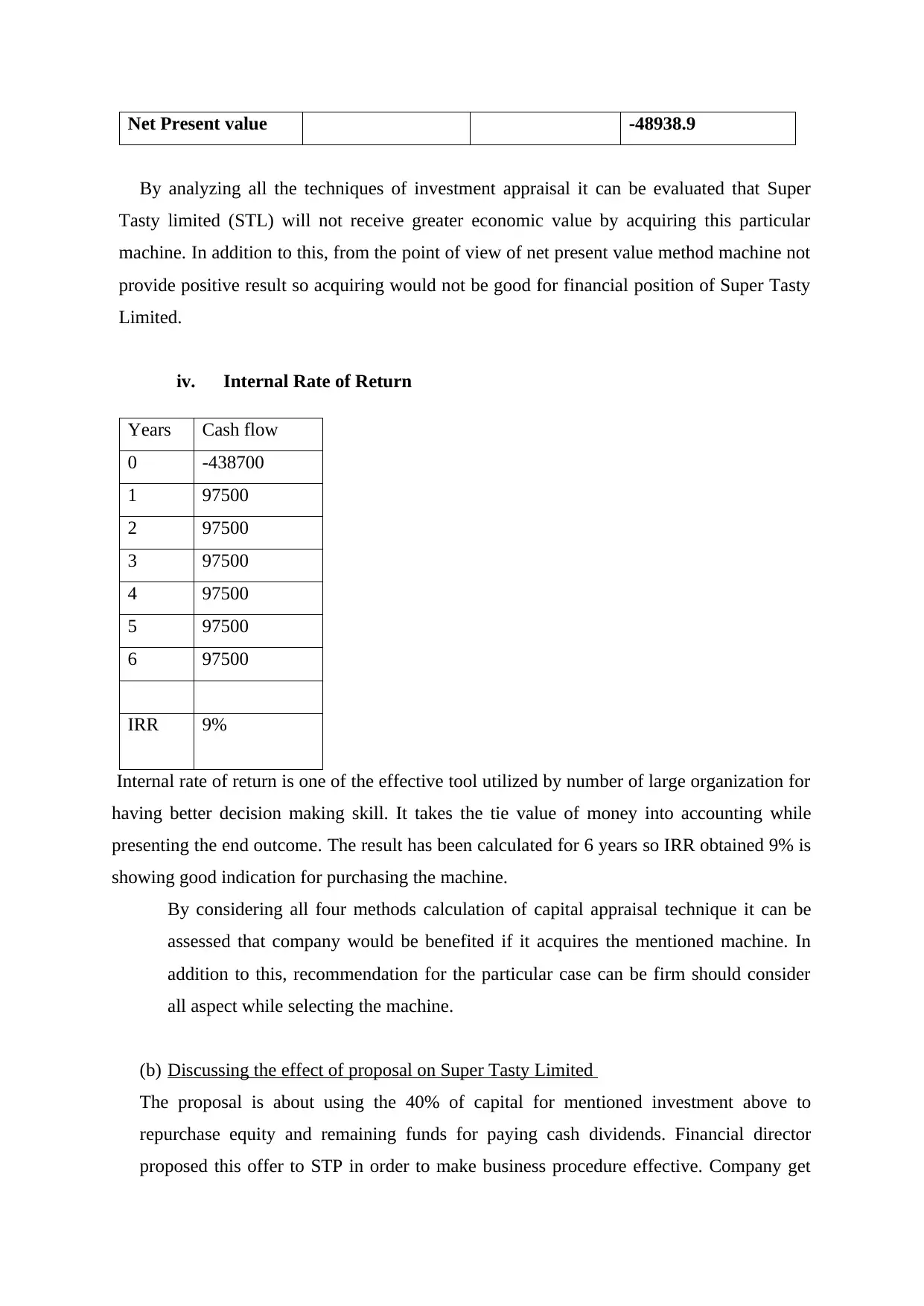

Net Present value -48938.9

By analyzing all the techniques of investment appraisal it can be evaluated that Super

Tasty limited (STL) will not receive greater economic value by acquiring this particular

machine. In addition to this, from the point of view of net present value method machine not

provide positive result so acquiring would not be good for financial position of Super Tasty

Limited.

iv. Internal Rate of Return

Years Cash flow

0 -438700

1 97500

2 97500

3 97500

4 97500

5 97500

6 97500

IRR 9%

Internal rate of return is one of the effective tool utilized by number of large organization for

having better decision making skill. It takes the tie value of money into accounting while

presenting the end outcome. The result has been calculated for 6 years so IRR obtained 9% is

showing good indication for purchasing the machine.

By considering all four methods calculation of capital appraisal technique it can be

assessed that company would be benefited if it acquires the mentioned machine. In

addition to this, recommendation for the particular case can be firm should consider

all aspect while selecting the machine.

(b) Discussing the effect of proposal on Super Tasty Limited

The proposal is about using the 40% of capital for mentioned investment above to

repurchase equity and remaining funds for paying cash dividends. Financial director

proposed this offer to STP in order to make business procedure effective. Company get

By analyzing all the techniques of investment appraisal it can be evaluated that Super

Tasty limited (STL) will not receive greater economic value by acquiring this particular

machine. In addition to this, from the point of view of net present value method machine not

provide positive result so acquiring would not be good for financial position of Super Tasty

Limited.

iv. Internal Rate of Return

Years Cash flow

0 -438700

1 97500

2 97500

3 97500

4 97500

5 97500

6 97500

IRR 9%

Internal rate of return is one of the effective tool utilized by number of large organization for

having better decision making skill. It takes the tie value of money into accounting while

presenting the end outcome. The result has been calculated for 6 years so IRR obtained 9% is

showing good indication for purchasing the machine.

By considering all four methods calculation of capital appraisal technique it can be

assessed that company would be benefited if it acquires the mentioned machine. In

addition to this, recommendation for the particular case can be firm should consider

all aspect while selecting the machine.

(b) Discussing the effect of proposal on Super Tasty Limited

The proposal is about using the 40% of capital for mentioned investment above to

repurchase equity and remaining funds for paying cash dividends. Financial director

proposed this offer to STP in order to make business procedure effective. Company get

consultation from the financial director for achieving the business objectives in effectual

manner by considering all influencing factors. Capitalization structure should be

formulated by company in such a manner that it can fulfill its internal as well external

financial requirements. Utilization of 40% of 438700 in order to repurchase equity and

spending 60% on giving cash dividends to shareholders. The main objective of

organization is to maximize profitability along with shareholders wealth so that better

reputation can be gained in market. The stakeholder’s satisfactions increase the

institutions’ scope of growth in industry and enables it to acquire competitive advantages.

Another objective behind doing this is that it will not require the company to pay

dividend on the equity shares it repurchased which will help it in retaining more from its

profits which can be further utilized in the investment requirements of the business. Also,

it will result into making it easy for the company in paying dividend to its investors in a

better way or at higher percentage which will build up good and positive image in front of

them. This is the most important factor which might make this proposal acceptable as it is

beneficial for the company. Thus, this step results int bringing in various benefits to the

business which cannot be avoided leading to making it can acceptable and viable deal. In

nutshell, this proposal will lead to effectively managing the cash flow of the business as

the company will no longer required to pay dividend on certain percentage of its equity

shares.

The proper segregation of capital in equity and retained earnings for providing

dividends, continuing business operations largely contribute in gaining success. There are

several factors which leads business to accept mentioned proposal it depends on the

financial position of organization that it will be benefited or not. The advantages of

keeping 40% equity capital will be no repayment requirements, lower risk, etc. STP

would be able to attract more investors by offering them trustworthiness that company is

contributing for shareholders growth along with organizational development. Productivity

and profitability of Super Tasty limited will be increased by accepting the mentioned

proposal.

(c) Evaluating the benefits and limitations of each investment appraisal technique

Investment Appraisal Techniques (IAT) play crucial role in making investing decisions

effective. There are various components which influences the decisions making criteria of

organizations (Mohan and Narwal, 2017). While utilizing each of the technique related to

CA company should pay attentions of pros and cons for knowing scope and limitations.

manner by considering all influencing factors. Capitalization structure should be

formulated by company in such a manner that it can fulfill its internal as well external

financial requirements. Utilization of 40% of 438700 in order to repurchase equity and

spending 60% on giving cash dividends to shareholders. The main objective of

organization is to maximize profitability along with shareholders wealth so that better

reputation can be gained in market. The stakeholder’s satisfactions increase the

institutions’ scope of growth in industry and enables it to acquire competitive advantages.

Another objective behind doing this is that it will not require the company to pay

dividend on the equity shares it repurchased which will help it in retaining more from its

profits which can be further utilized in the investment requirements of the business. Also,

it will result into making it easy for the company in paying dividend to its investors in a

better way or at higher percentage which will build up good and positive image in front of

them. This is the most important factor which might make this proposal acceptable as it is

beneficial for the company. Thus, this step results int bringing in various benefits to the

business which cannot be avoided leading to making it can acceptable and viable deal. In

nutshell, this proposal will lead to effectively managing the cash flow of the business as

the company will no longer required to pay dividend on certain percentage of its equity

shares.

The proper segregation of capital in equity and retained earnings for providing

dividends, continuing business operations largely contribute in gaining success. There are

several factors which leads business to accept mentioned proposal it depends on the

financial position of organization that it will be benefited or not. The advantages of

keeping 40% equity capital will be no repayment requirements, lower risk, etc. STP

would be able to attract more investors by offering them trustworthiness that company is

contributing for shareholders growth along with organizational development. Productivity

and profitability of Super Tasty limited will be increased by accepting the mentioned

proposal.

(c) Evaluating the benefits and limitations of each investment appraisal technique

Investment Appraisal Techniques (IAT) play crucial role in making investing decisions

effective. There are various components which influences the decisions making criteria of

organizations (Mohan and Narwal, 2017). While utilizing each of the technique related to

CA company should pay attentions of pros and cons for knowing scope and limitations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition to this, limitation should be provided focus due to its adverse impact on

company’s growth. the following are benefits and limitations:

Payback Period (PP)

It is one of the important tool of CA which requires most focus of business as helps

organization to understand the time period for recovering its invested capital (Lefley,

2018). PP has its own advantages and disadvantages which requires the attentions for the

purpose of reaching accurate decision regarding project selection.

Advantages

The of the biggest benefit of implementing PP method in company is related with

its unique characteristics of being simple to use and understand. It uses the input

for providing the accurate outcome

Useful in cases of uncertainty that face rapid changing circumstances. In addition

to this, uncertainty lead to make difficult for identifying the management of

organization in making evaluation of unequal cash inflows. Thus utilization of it

reduces chances of loss through obsolescence.

Payback period provide preference to liquidity which aid company to know

amount of money it going to recover in specified span of time.

Disadvantages

It ignores the time value of money so not all cash flows are covered under this

technique of capital appraisal.

Reality is neglected which unable firm to estimate the actual profitability.

Return on investment is as well ignored by PP which is biggest limitation of

this tool.

Net Present Value (NPV)

It comprises the worth of cash flows received in future which provides

transparency to organization regarding its accomplishment of business objectives.

Benefits and dreawbacks are mentioned below:

Benefits

Unambiguous measure is provided by NPV helps in comparing marginal

forestry investment for particular project.

Straightforward calculations can be computed with help of this technique.

Time value of money is recognized by NPV which provides assistance in

making choice among multiple alternatives.

company’s growth. the following are benefits and limitations:

Payback Period (PP)

It is one of the important tool of CA which requires most focus of business as helps

organization to understand the time period for recovering its invested capital (Lefley,

2018). PP has its own advantages and disadvantages which requires the attentions for the

purpose of reaching accurate decision regarding project selection.

Advantages

The of the biggest benefit of implementing PP method in company is related with

its unique characteristics of being simple to use and understand. It uses the input

for providing the accurate outcome

Useful in cases of uncertainty that face rapid changing circumstances. In addition

to this, uncertainty lead to make difficult for identifying the management of

organization in making evaluation of unequal cash inflows. Thus utilization of it

reduces chances of loss through obsolescence.

Payback period provide preference to liquidity which aid company to know

amount of money it going to recover in specified span of time.

Disadvantages

It ignores the time value of money so not all cash flows are covered under this

technique of capital appraisal.

Reality is neglected which unable firm to estimate the actual profitability.

Return on investment is as well ignored by PP which is biggest limitation of

this tool.

Net Present Value (NPV)

It comprises the worth of cash flows received in future which provides

transparency to organization regarding its accomplishment of business objectives.

Benefits and dreawbacks are mentioned below:

Benefits

Unambiguous measure is provided by NPV helps in comparing marginal

forestry investment for particular project.

Straightforward calculations can be computed with help of this technique.

Time value of money is recognized by NPV which provides assistance in

making choice among multiple alternatives.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Limitation

It assumes the single discount rate for the whole life of the investment.

Inappropriate assumption related to estimation of accurate future cash flow is

assumed which is adversely impact the company’s progress.

In appropriate decisions are taken on the basis of improper information

provided by net present value.

Accounting Rate of Return (ARR)

ARR is used in capital budgeting is way of comparing the profit investor

expect and amount need to invest. Every procedure has its own pros and cons

that creates its own identity which are as follows:

Pros

It is very easy to calculate and understand so that correct decision can

be identified with help of this procedure

Net earnings concept is given preference in ARR method of capital

appraisal technique.

Comparison between multiple project becomes easy due its simple

presentation nature.

Current performance of firm can be assessed with help of ARR

Cons

Time factor is ignored which is primary weakness that results in

unawareness of time value of money.

Fair rate of return cannot be determined by ARR.

Internal Rate of Return (IRR)

IRR is used as capital budgeting technique to estimate the time

value of money even if cash flow is even or uneven (Magni and

Marchioni, 2020). The following are benefits and limitations:

Benefits

It is simple to interpret by its proper visualization nature

No requirement of finding hurdle is present here

It assumes the single discount rate for the whole life of the investment.

Inappropriate assumption related to estimation of accurate future cash flow is

assumed which is adversely impact the company’s progress.

In appropriate decisions are taken on the basis of improper information

provided by net present value.

Accounting Rate of Return (ARR)

ARR is used in capital budgeting is way of comparing the profit investor

expect and amount need to invest. Every procedure has its own pros and cons

that creates its own identity which are as follows:

Pros

It is very easy to calculate and understand so that correct decision can

be identified with help of this procedure

Net earnings concept is given preference in ARR method of capital

appraisal technique.

Comparison between multiple project becomes easy due its simple

presentation nature.

Current performance of firm can be assessed with help of ARR

Cons

Time factor is ignored which is primary weakness that results in

unawareness of time value of money.

Fair rate of return cannot be determined by ARR.

Internal Rate of Return (IRR)

IRR is used as capital budgeting technique to estimate the time

value of money even if cash flow is even or uneven (Magni and

Marchioni, 2020). The following are benefits and limitations:

Benefits

It is simple to interpret by its proper visualization nature

No requirement of finding hurdle is present here

Limitations

Economies of scale is ignore by IRR

Contingents projects are being neglected by this technique

Question 3 – Mergers and Takeovers

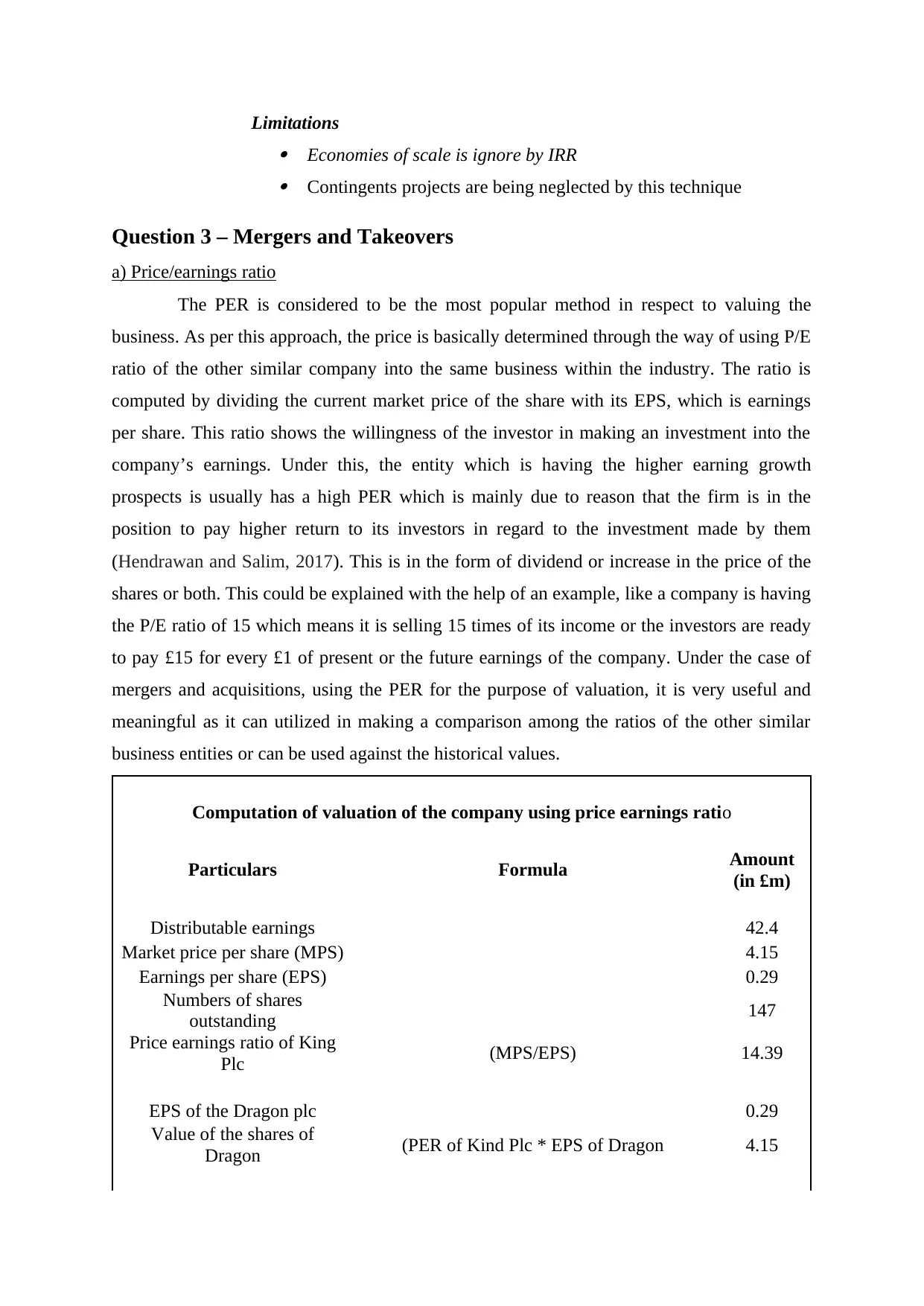

a) Price/earnings ratio

The PER is considered to be the most popular method in respect to valuing the

business. As per this approach, the price is basically determined through the way of using P/E

ratio of the other similar company into the same business within the industry. The ratio is

computed by dividing the current market price of the share with its EPS, which is earnings

per share. This ratio shows the willingness of the investor in making an investment into the

company’s earnings. Under this, the entity which is having the higher earning growth

prospects is usually has a high PER which is mainly due to reason that the firm is in the

position to pay higher return to its investors in regard to the investment made by them

(Hendrawan and Salim, 2017). This is in the form of dividend or increase in the price of the

shares or both. This could be explained with the help of an example, like a company is having

the P/E ratio of 15 which means it is selling 15 times of its income or the investors are ready

to pay £15 for every £1 of present or the future earnings of the company. Under the case of

mergers and acquisitions, using the PER for the purpose of valuation, it is very useful and

meaningful as it can utilized in making a comparison among the ratios of the other similar

business entities or can be used against the historical values.

Computation of valuation of the company using price earnings ratio

Particulars Formula Amount

(in £m)

Distributable earnings 42.4

Market price per share (MPS) 4.15

Earnings per share (EPS) 0.29

Numbers of shares

outstanding 147

Price earnings ratio of King

Plc (MPS/EPS) 14.39

EPS of the Dragon plc 0.29

Value of the shares of

Dragon (PER of Kind Plc * EPS of Dragon 4.15

Economies of scale is ignore by IRR

Contingents projects are being neglected by this technique

Question 3 – Mergers and Takeovers

a) Price/earnings ratio

The PER is considered to be the most popular method in respect to valuing the

business. As per this approach, the price is basically determined through the way of using P/E

ratio of the other similar company into the same business within the industry. The ratio is

computed by dividing the current market price of the share with its EPS, which is earnings

per share. This ratio shows the willingness of the investor in making an investment into the

company’s earnings. Under this, the entity which is having the higher earning growth

prospects is usually has a high PER which is mainly due to reason that the firm is in the

position to pay higher return to its investors in regard to the investment made by them

(Hendrawan and Salim, 2017). This is in the form of dividend or increase in the price of the

shares or both. This could be explained with the help of an example, like a company is having

the P/E ratio of 15 which means it is selling 15 times of its income or the investors are ready

to pay £15 for every £1 of present or the future earnings of the company. Under the case of

mergers and acquisitions, using the PER for the purpose of valuation, it is very useful and

meaningful as it can utilized in making a comparison among the ratios of the other similar

business entities or can be used against the historical values.

Computation of valuation of the company using price earnings ratio

Particulars Formula Amount

(in £m)

Distributable earnings 42.4

Market price per share (MPS) 4.15

Earnings per share (EPS) 0.29

Numbers of shares

outstanding 147

Price earnings ratio of King

Plc (MPS/EPS) 14.39

EPS of the Dragon plc 0.29

Value of the shares of

Dragon (PER of Kind Plc * EPS of Dragon 4.15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Determining the market

value Dragon plc

= Value of the shares of Dragon * Numbers

of shares outstanding

= 4.15 * 147 610.05

It can be inferred from the above that the value of Dragon Plc is £610.05as it can be

seen in the above table. The MV is being determined through the way of multiplying the no.

of shares with the price per share of Trojan plc.

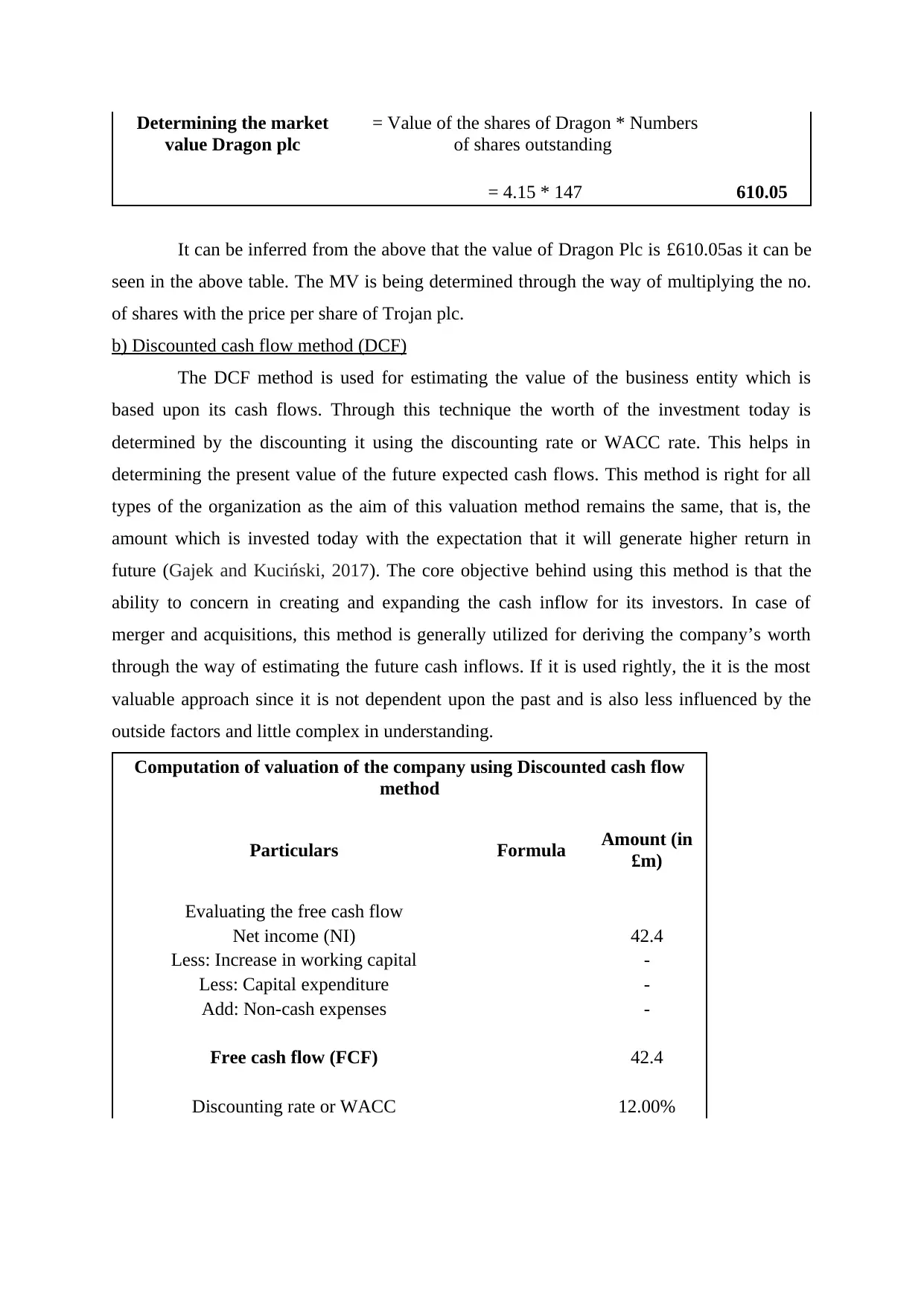

b) Discounted cash flow method (DCF)

The DCF method is used for estimating the value of the business entity which is

based upon its cash flows. Through this technique the worth of the investment today is

determined by the discounting it using the discounting rate or WACC rate. This helps in

determining the present value of the future expected cash flows. This method is right for all

types of the organization as the aim of this valuation method remains the same, that is, the

amount which is invested today with the expectation that it will generate higher return in

future (Gajek and Kuciński, 2017). The core objective behind using this method is that the

ability to concern in creating and expanding the cash inflow for its investors. In case of

merger and acquisitions, this method is generally utilized for deriving the company’s worth

through the way of estimating the future cash inflows. If it is used rightly, the it is the most

valuable approach since it is not dependent upon the past and is also less influenced by the

outside factors and little complex in understanding.

Computation of valuation of the company using Discounted cash flow

method

Particulars Formula Amount (in

£m)

Evaluating the free cash flow

Net income (NI) 42.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 42.4

Discounting rate or WACC 12.00%

value Dragon plc

= Value of the shares of Dragon * Numbers

of shares outstanding

= 4.15 * 147 610.05

It can be inferred from the above that the value of Dragon Plc is £610.05as it can be

seen in the above table. The MV is being determined through the way of multiplying the no.

of shares with the price per share of Trojan plc.

b) Discounted cash flow method (DCF)

The DCF method is used for estimating the value of the business entity which is

based upon its cash flows. Through this technique the worth of the investment today is

determined by the discounting it using the discounting rate or WACC rate. This helps in

determining the present value of the future expected cash flows. This method is right for all

types of the organization as the aim of this valuation method remains the same, that is, the

amount which is invested today with the expectation that it will generate higher return in

future (Gajek and Kuciński, 2017). The core objective behind using this method is that the

ability to concern in creating and expanding the cash inflow for its investors. In case of

merger and acquisitions, this method is generally utilized for deriving the company’s worth

through the way of estimating the future cash inflows. If it is used rightly, the it is the most

valuable approach since it is not dependent upon the past and is also less influenced by the

outside factors and little complex in understanding.

Computation of valuation of the company using Discounted cash flow

method

Particulars Formula Amount (in

£m)

Evaluating the free cash flow

Net income (NI) 42.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 42.4

Discounting rate or WACC 12.00%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MPS

= Free cash

flow /

Discounting

rate

353

Market value of Dragon plc

= MPS *

Number of

shares

= 353 * 147 51940

It can be concluded from the above that the value of Dragon plc is £51940 under the

discounted cash flow approach.

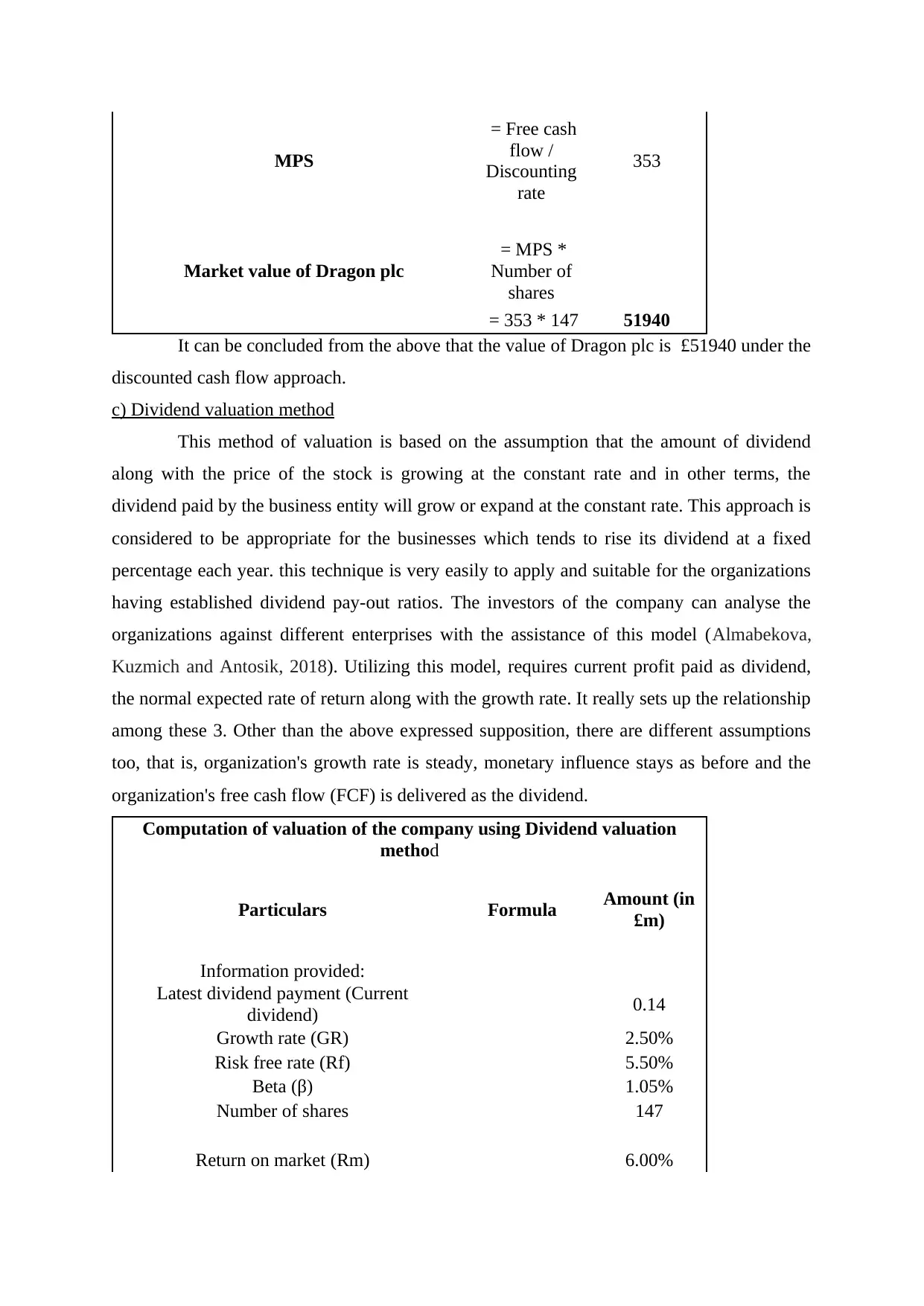

c) Dividend valuation method

This method of valuation is based on the assumption that the amount of dividend

along with the price of the stock is growing at the constant rate and in other terms, the

dividend paid by the business entity will grow or expand at the constant rate. This approach is

considered to be appropriate for the businesses which tends to rise its dividend at a fixed

percentage each year. this technique is very easily to apply and suitable for the organizations

having established dividend pay-out ratios. The investors of the company can analyse the

organizations against different enterprises with the assistance of this model (Almabekova,

Kuzmich and Antosik, 2018). Utilizing this model, requires current profit paid as dividend,

the normal expected rate of return along with the growth rate. It really sets up the relationship

among these 3. Other than the above expressed supposition, there are different assumptions

too, that is, organization's growth rate is steady, monetary influence stays as before and the

organization's free cash flow (FCF) is delivered as the dividend.

Computation of valuation of the company using Dividend valuation

method

Particulars Formula Amount (in

£m)

Information provided:

Latest dividend payment (Current

dividend) 0.14

Growth rate (GR) 2.50%

Risk free rate (Rf) 5.50%

Beta (β) 1.05%

Number of shares 147

Return on market (Rm) 6.00%

= Free cash

flow /

Discounting

rate

353

Market value of Dragon plc

= MPS *

Number of

shares

= 353 * 147 51940

It can be concluded from the above that the value of Dragon plc is £51940 under the

discounted cash flow approach.

c) Dividend valuation method

This method of valuation is based on the assumption that the amount of dividend

along with the price of the stock is growing at the constant rate and in other terms, the

dividend paid by the business entity will grow or expand at the constant rate. This approach is

considered to be appropriate for the businesses which tends to rise its dividend at a fixed

percentage each year. this technique is very easily to apply and suitable for the organizations

having established dividend pay-out ratios. The investors of the company can analyse the

organizations against different enterprises with the assistance of this model (Almabekova,

Kuzmich and Antosik, 2018). Utilizing this model, requires current profit paid as dividend,

the normal expected rate of return along with the growth rate. It really sets up the relationship

among these 3. Other than the above expressed supposition, there are different assumptions

too, that is, organization's growth rate is steady, monetary influence stays as before and the

organization's free cash flow (FCF) is delivered as the dividend.

Computation of valuation of the company using Dividend valuation

method

Particulars Formula Amount (in

£m)

Information provided:

Latest dividend payment (Current

dividend) 0.14

Growth rate (GR) 2.50%

Risk free rate (Rf) 5.50%

Beta (β) 1.05%

Number of shares 147

Return on market (Rm) 6.00%

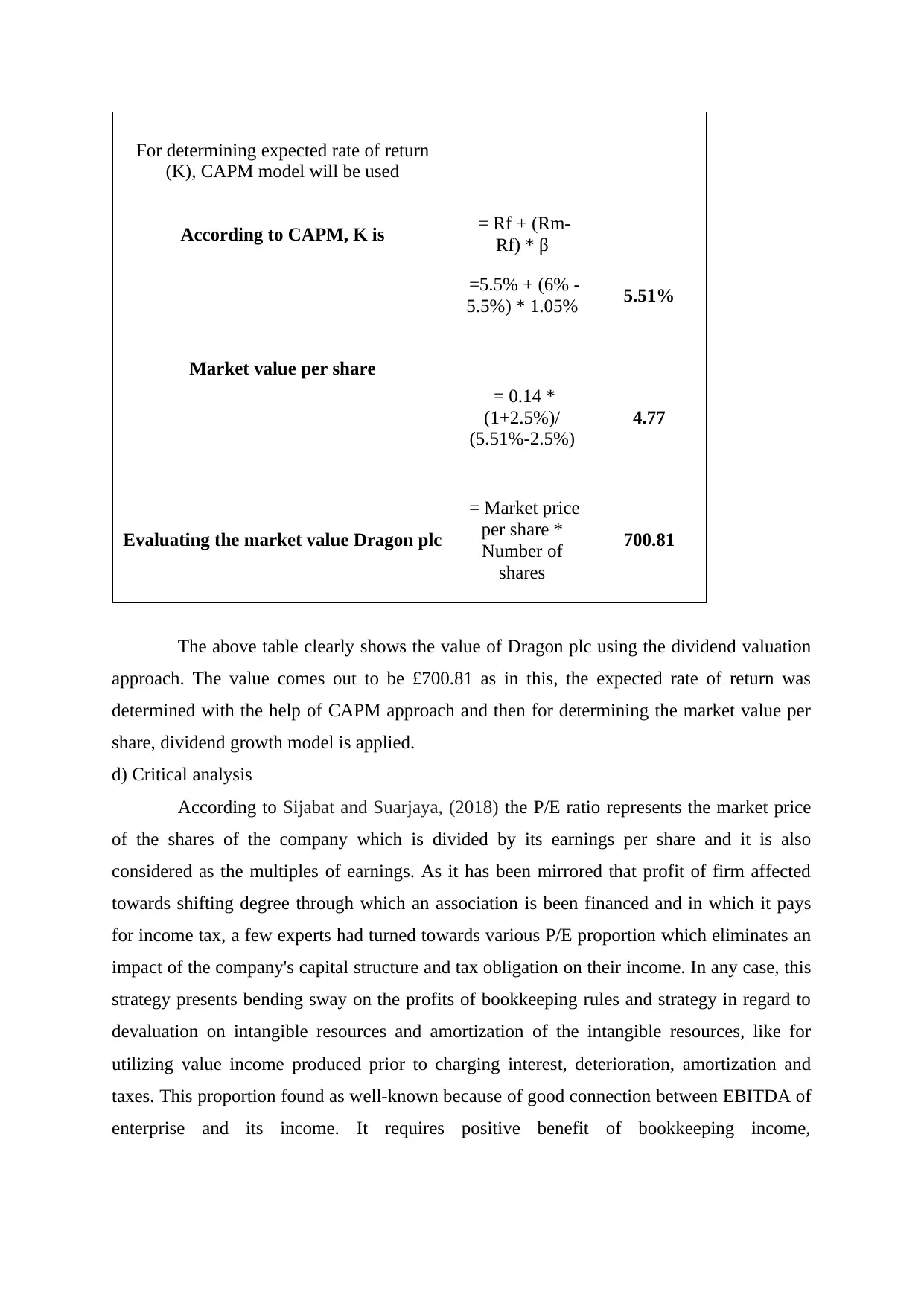

For determining expected rate of return

(K), CAPM model will be used

According to CAPM, K is = Rf + (Rm-

Rf) * β

=5.5% + (6% -

5.5%) * 1.05% 5.51%

Market value per share

= 0.14 *

(1+2.5%)/

(5.51%-2.5%)

4.77

Evaluating the market value Dragon plc

= Market price

per share *

Number of

shares

700.81

The above table clearly shows the value of Dragon plc using the dividend valuation

approach. The value comes out to be £700.81 as in this, the expected rate of return was

determined with the help of CAPM approach and then for determining the market value per

share, dividend growth model is applied.

d) Critical analysis

According to Sijabat and Suarjaya, (2018) the P/E ratio represents the market price

of the shares of the company which is divided by its earnings per share and it is also

considered as the multiples of earnings. As it has been mirrored that profit of firm affected

towards shifting degree through which an association is been financed and in which it pays

for income tax, a few experts had turned towards various P/E proportion which eliminates an

impact of the company's capital structure and tax obligation on their income. In any case, this

strategy presents bending sway on the profits of bookkeeping rules and strategy in regard to

devaluation on intangible resources and amortization of the intangible resources, like for

utilizing value income produced prior to charging interest, deterioration, amortization and

taxes. This proportion found as well-known because of good connection between EBITDA of

enterprise and its income. It requires positive benefit of bookkeeping income,

(K), CAPM model will be used

According to CAPM, K is = Rf + (Rm-

Rf) * β

=5.5% + (6% -

5.5%) * 1.05% 5.51%

Market value per share

= 0.14 *

(1+2.5%)/

(5.51%-2.5%)

4.77

Evaluating the market value Dragon plc

= Market price

per share *

Number of

shares

700.81

The above table clearly shows the value of Dragon plc using the dividend valuation

approach. The value comes out to be £700.81 as in this, the expected rate of return was

determined with the help of CAPM approach and then for determining the market value per

share, dividend growth model is applied.

d) Critical analysis

According to Sijabat and Suarjaya, (2018) the P/E ratio represents the market price

of the shares of the company which is divided by its earnings per share and it is also

considered as the multiples of earnings. As it has been mirrored that profit of firm affected

towards shifting degree through which an association is been financed and in which it pays

for income tax, a few experts had turned towards various P/E proportion which eliminates an

impact of the company's capital structure and tax obligation on their income. In any case, this

strategy presents bending sway on the profits of bookkeeping rules and strategy in regard to

devaluation on intangible resources and amortization of the intangible resources, like for

utilizing value income produced prior to charging interest, deterioration, amortization and

taxes. This proportion found as well-known because of good connection between EBITDA of

enterprise and its income. It requires positive benefit of bookkeeping income,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.