Financial Management Report: Kadlex PLC, Happy Meal Ltd, Cost Analysis

VerifiedAdded on 2021/02/20

|14

|3498

|47

Report

AI Summary

This report delves into key financial management concepts through the analysis of practical problems. It begins with the calculation of the Weighted Average Cost of Capital (WACC) for Kadlex plc, exploring both book value and market value WACC, and the implications of capital structure changes. The report then examines various investment appraisal techniques, including payback period, accounting rate of return, Net Present Value (NPV), and Internal Rate of Return (IRR), using a case study of Happy Meal Ltd. The calculations and recommendations are provided for each technique, offering insights into project viability. The report also discusses the impact of short-termism on bankruptcy and agency problems, providing a well-rounded understanding of financial management principles.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Finance is the life line of any business organisation in long term survival and enhance the

profitability of its business operations. Finance management is about to raising the money,

managing and application of funds in doing its business operations efficiently and effectively.

The management of finance is essential activity in an organisation in order to achieve its finance

related goals and objectives. This report provides the understanding of net present value, pay

back period and accounting rate of return by solving some numerical problems. This also

provides information about how a business firm may find out its internal rate of return for

evaluating its performances. In this report various questions is given related to financial

management for better understanding of this. This report provides information about calculation

of cost of capital and another related aspects (Renz, D.O. and Herman, R.D. eds., 2016Arnold, 2012).

Finance is the life line of any business organisation in long term survival and enhance the

profitability of its business operations. Finance management is about to raising the money,

managing and application of funds in doing its business operations efficiently and effectively.

The management of finance is essential activity in an organisation in order to achieve its finance

related goals and objectives. This report provides the understanding of net present value, pay

back period and accounting rate of return by solving some numerical problems. This also

provides information about how a business firm may find out its internal rate of return for

evaluating its performances. In this report various questions is given related to financial

management for better understanding of this. This report provides information about calculation

of cost of capital and another related aspects (Renz, D.O. and Herman, R.D. eds., 2016Arnold, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

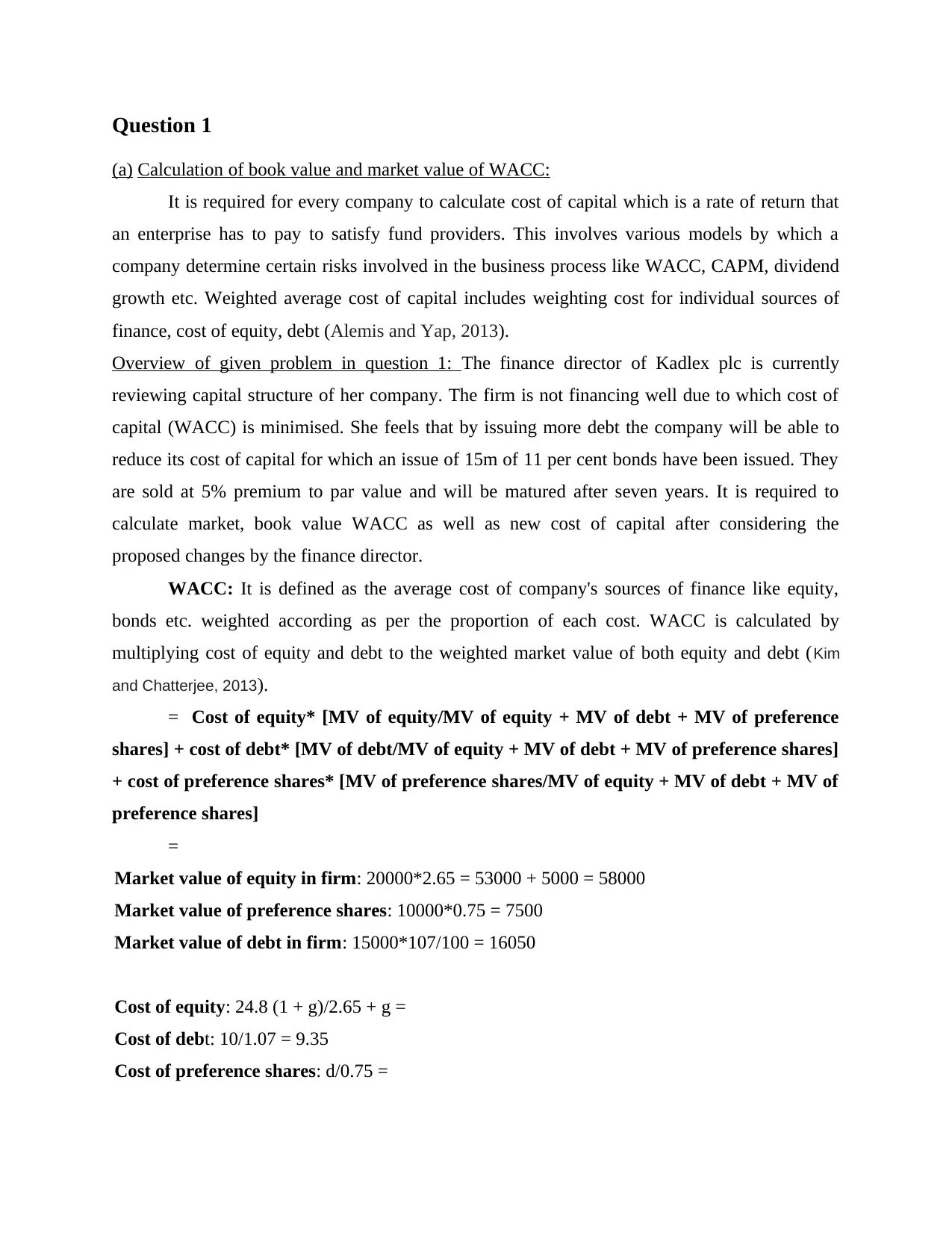

Question 1

(a) Calculation of book value and market value of WACC:

It is required for every company to calculate cost of capital which is a rate of return that

an enterprise has to pay to satisfy fund providers. This involves various models by which a

company determine certain risks involved in the business process like WACC, CAPM, dividend

growth etc. Weighted average cost of capital includes weighting cost for individual sources of

finance, cost of equity, debt (Alemis and Yap, 2013).

Overview of given problem in question 1: The finance director of Kadlex plc is currently

reviewing capital structure of her company. The firm is not financing well due to which cost of

capital (WACC) is minimised. She feels that by issuing more debt the company will be able to

reduce its cost of capital for which an issue of 15m of 11 per cent bonds have been issued. They

are sold at 5% premium to par value and will be matured after seven years. It is required to

calculate market, book value WACC as well as new cost of capital after considering the

proposed changes by the finance director.

WACC: It is defined as the average cost of company's sources of finance like equity,

bonds etc. weighted according as per the proportion of each cost. WACC is calculated by

multiplying cost of equity and debt to the weighted market value of both equity and debt (Kim

and Chatterjee, 2013).

= Cost of equity* [MV of equity/MV of equity + MV of debt + MV of preference

shares] + cost of debt* [MV of debt/MV of equity + MV of debt + MV of preference shares]

+ cost of preference shares* [MV of preference shares/MV of equity + MV of debt + MV of

preference shares]

=

Market value of equity in firm: 20000*2.65 = 53000 + 5000 = 58000

Market value of preference shares: 10000*0.75 = 7500

Market value of debt in firm: 15000*107/100 = 16050

Cost of equity: 24.8 (1 + g)/2.65 + g =

Cost of debt: 10/1.07 = 9.35

Cost of preference shares: d/0.75 =

(a) Calculation of book value and market value of WACC:

It is required for every company to calculate cost of capital which is a rate of return that

an enterprise has to pay to satisfy fund providers. This involves various models by which a

company determine certain risks involved in the business process like WACC, CAPM, dividend

growth etc. Weighted average cost of capital includes weighting cost for individual sources of

finance, cost of equity, debt (Alemis and Yap, 2013).

Overview of given problem in question 1: The finance director of Kadlex plc is currently

reviewing capital structure of her company. The firm is not financing well due to which cost of

capital (WACC) is minimised. She feels that by issuing more debt the company will be able to

reduce its cost of capital for which an issue of 15m of 11 per cent bonds have been issued. They

are sold at 5% premium to par value and will be matured after seven years. It is required to

calculate market, book value WACC as well as new cost of capital after considering the

proposed changes by the finance director.

WACC: It is defined as the average cost of company's sources of finance like equity,

bonds etc. weighted according as per the proportion of each cost. WACC is calculated by

multiplying cost of equity and debt to the weighted market value of both equity and debt (Kim

and Chatterjee, 2013).

= Cost of equity* [MV of equity/MV of equity + MV of debt + MV of preference

shares] + cost of debt* [MV of debt/MV of equity + MV of debt + MV of preference shares]

+ cost of preference shares* [MV of preference shares/MV of equity + MV of debt + MV of

preference shares]

=

Market value of equity in firm: 20000*2.65 = 53000 + 5000 = 58000

Market value of preference shares: 10000*0.75 = 7500

Market value of debt in firm: 15000*107/100 = 16050

Cost of equity: 24.8 (1 + g)/2.65 + g =

Cost of debt: 10/1.07 = 9.35

Cost of preference shares: d/0.75 =

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B) Cost of capital:

Given: 15m of 11% bonds @ 5% premium after 7years

Share price: 2.85

Pref share price:

Tax: 30%

WACC:

Market value of equity in firm: 20000*2.85 = 57000 + 5000 = 62000

Market value of preference shares: 10000*0.68 = 6800

Market value of debt in firm: 15000*

Cost of equity: 24.8*(1 + 0.2)/2.85 + 0.2 = 9.75

Cost of debt: 11(1-0.3)/1.07 = 7.2

Cost of preference shares: d/0.75

(c) Integration of sensible level of gearing into capital structure:

There is a huge impact of the selection of a good structure of capital in overall

profitability and long term survival of company. Therefore, it is necessary to focus on the capital

structure of any business organisation. There is also necessary to have inclusion of debt portion

(gearing) in a capital structure in a sensible manner. By inclusion of gearing proportion may

enhance the volume of production and ultimately profits of the company may be increased

(Parker, 2012).

Therefore, a capital structure should required to have also debt portion to reduce the

weighted average cost of capital (Moutinho, L. and Vargas-Sanchez, 2018).

(d) Effect of short termism on bankruptcy and agency problem:

Short termism refers to focusing on short term results by ignoring the long term interest.

Short-term performance coerces on investors can trigger in an extra emphasis on its parts on

periodic earnings, with giving few attention to strategy, fundamentals and long-term value

establishment. Bankruptcy is a legal process by which business organisations may be declares

as insolvent if any organisation is unable to pay its outstanding debt. The process of bankruptcy

Given: 15m of 11% bonds @ 5% premium after 7years

Share price: 2.85

Pref share price:

Tax: 30%

WACC:

Market value of equity in firm: 20000*2.85 = 57000 + 5000 = 62000

Market value of preference shares: 10000*0.68 = 6800

Market value of debt in firm: 15000*

Cost of equity: 24.8*(1 + 0.2)/2.85 + 0.2 = 9.75

Cost of debt: 11(1-0.3)/1.07 = 7.2

Cost of preference shares: d/0.75

(c) Integration of sensible level of gearing into capital structure:

There is a huge impact of the selection of a good structure of capital in overall

profitability and long term survival of company. Therefore, it is necessary to focus on the capital

structure of any business organisation. There is also necessary to have inclusion of debt portion

(gearing) in a capital structure in a sensible manner. By inclusion of gearing proportion may

enhance the volume of production and ultimately profits of the company may be increased

(Parker, 2012).

Therefore, a capital structure should required to have also debt portion to reduce the

weighted average cost of capital (Moutinho, L. and Vargas-Sanchez, 2018).

(d) Effect of short termism on bankruptcy and agency problem:

Short termism refers to focusing on short term results by ignoring the long term interest.

Short-term performance coerces on investors can trigger in an extra emphasis on its parts on

periodic earnings, with giving few attention to strategy, fundamentals and long-term value

establishment. Bankruptcy is a legal process by which business organisations may be declares

as insolvent if any organisation is unable to pay its outstanding debt. The process of bankruptcy

may be started by by applying any application to an authorised authority which is constituted for

this purpose.

There is huge impact of short termism on the bankruptcy, as in this condition, business

organisation becomes bankrupt due to focusing its funds on the short therm goals. Due to this,

company's fund become zero. A short termism also effect the agency business and creates

problem related to this. Therefore, it is required that business shall understand this term and its

benefits and weaknesses, so that it can effectively and efficiently utilise its funds (Finn,

O’connell and Fitzpatrick, 2013).

Question 3

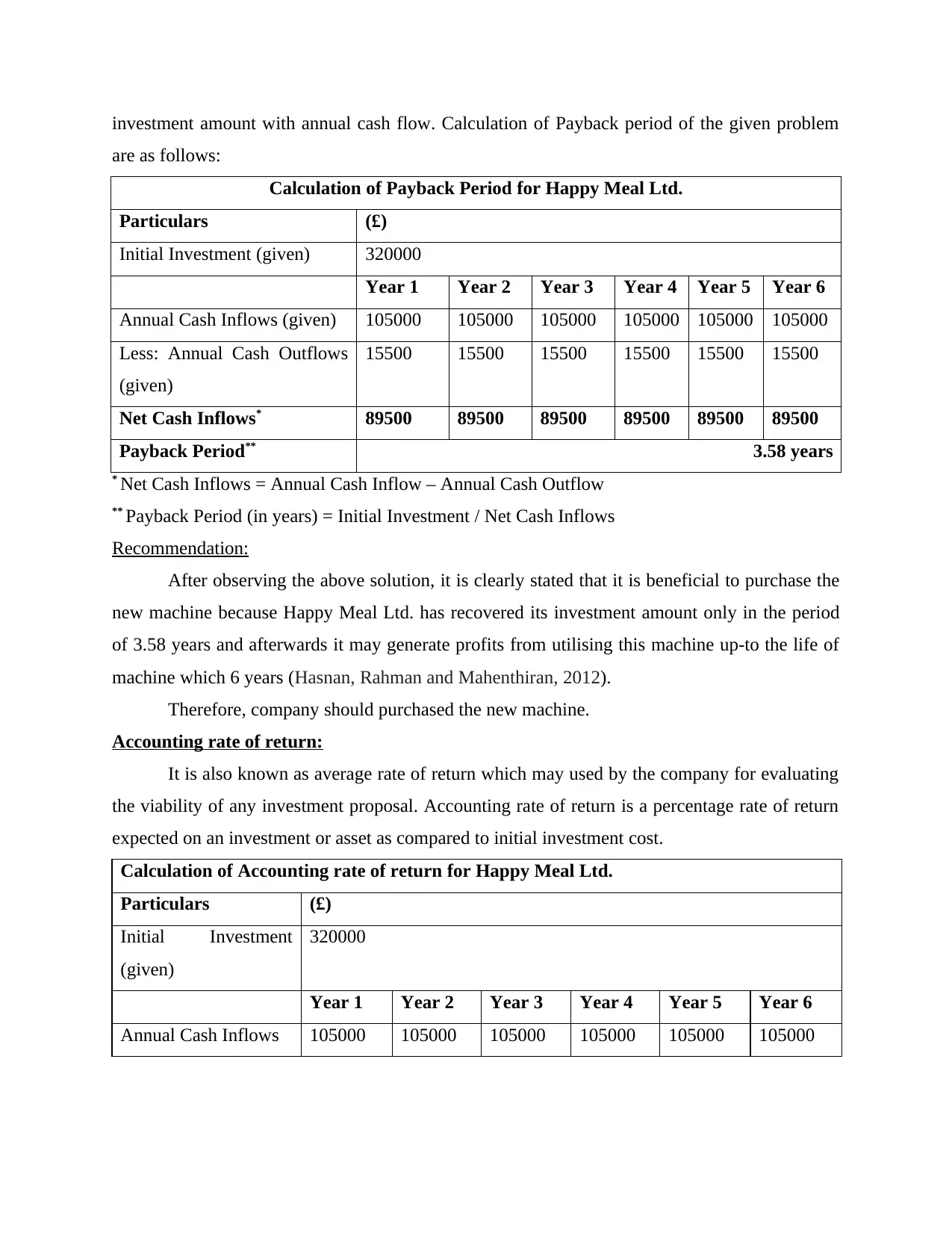

(a) Evaluation of various investment appraisal techniques:

These are the techniques which are useful for the company in evaluation of various

capital projects for assessing the viability of these projects for the benefit of company. Appraisal

techniques help the company in drawing conclusions regarding whether a given project shall be

selected or not. Various investment appraisal techniques includes pay back period, net present

value, internal rate of return and so on (Habib and Islam, 2013).

Overview of given problem in question 3: Happy meal Ltd. Is a food manufacturer which plans

to purchase a new machine having costing of £320,000. This machine will generate annual cash

inflow £105000 as well as cash outflow of £15500 for each of its six years. Depreciation is

charged on the machine on reducing method at rate of 20%. the residual value shall be estimated

at the rate of 10% of the original cost of the machine.

The above sum is evaluated by applying different types of investment appraisal

techniques which are as follows:

Pay back period:

In normal term, pay back period may be defined as a average period of time which shall

be required for recovering its investment amount from the given project (proposal). This is

important method for accepting of an investment proposal if there is shorter payback period

(Brandimarte, 2014). The payback period of any investment proposal is calculated by dividing the

this purpose.

There is huge impact of short termism on the bankruptcy, as in this condition, business

organisation becomes bankrupt due to focusing its funds on the short therm goals. Due to this,

company's fund become zero. A short termism also effect the agency business and creates

problem related to this. Therefore, it is required that business shall understand this term and its

benefits and weaknesses, so that it can effectively and efficiently utilise its funds (Finn,

O’connell and Fitzpatrick, 2013).

Question 3

(a) Evaluation of various investment appraisal techniques:

These are the techniques which are useful for the company in evaluation of various

capital projects for assessing the viability of these projects for the benefit of company. Appraisal

techniques help the company in drawing conclusions regarding whether a given project shall be

selected or not. Various investment appraisal techniques includes pay back period, net present

value, internal rate of return and so on (Habib and Islam, 2013).

Overview of given problem in question 3: Happy meal Ltd. Is a food manufacturer which plans

to purchase a new machine having costing of £320,000. This machine will generate annual cash

inflow £105000 as well as cash outflow of £15500 for each of its six years. Depreciation is

charged on the machine on reducing method at rate of 20%. the residual value shall be estimated

at the rate of 10% of the original cost of the machine.

The above sum is evaluated by applying different types of investment appraisal

techniques which are as follows:

Pay back period:

In normal term, pay back period may be defined as a average period of time which shall

be required for recovering its investment amount from the given project (proposal). This is

important method for accepting of an investment proposal if there is shorter payback period

(Brandimarte, 2014). The payback period of any investment proposal is calculated by dividing the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investment amount with annual cash flow. Calculation of Payback period of the given problem

are as follows:

Calculation of Payback Period for Happy Meal Ltd.

Particulars (£)

Initial Investment (given) 320000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows (given) 105000 105000 105000 105000 105000 105000

Less: Annual Cash Outflows

(given)

15500 15500 15500 15500 15500 15500

Net Cash Inflows* 89500 89500 89500 89500 89500 89500

Payback Period** 3.58 years

* Net Cash Inflows = Annual Cash Inflow – Annual Cash Outflow

** Payback Period (in years) = Initial Investment / Net Cash Inflows

Recommendation:

After observing the above solution, it is clearly stated that it is beneficial to purchase the

new machine because Happy Meal Ltd. has recovered its investment amount only in the period

of 3.58 years and afterwards it may generate profits from utilising this machine up-to the life of

machine which 6 years (Hasnan, Rahman and Mahenthiran, 2012).

Therefore, company should purchased the new machine.

Accounting rate of return:

It is also known as average rate of return which may used by the company for evaluating

the viability of any investment proposal. Accounting rate of return is a percentage rate of return

expected on an investment or asset as compared to initial investment cost.

Calculation of Accounting rate of return for Happy Meal Ltd.

Particulars (£)

Initial Investment

(given)

320000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows 105000 105000 105000 105000 105000 105000

are as follows:

Calculation of Payback Period for Happy Meal Ltd.

Particulars (£)

Initial Investment (given) 320000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows (given) 105000 105000 105000 105000 105000 105000

Less: Annual Cash Outflows

(given)

15500 15500 15500 15500 15500 15500

Net Cash Inflows* 89500 89500 89500 89500 89500 89500

Payback Period** 3.58 years

* Net Cash Inflows = Annual Cash Inflow – Annual Cash Outflow

** Payback Period (in years) = Initial Investment / Net Cash Inflows

Recommendation:

After observing the above solution, it is clearly stated that it is beneficial to purchase the

new machine because Happy Meal Ltd. has recovered its investment amount only in the period

of 3.58 years and afterwards it may generate profits from utilising this machine up-to the life of

machine which 6 years (Hasnan, Rahman and Mahenthiran, 2012).

Therefore, company should purchased the new machine.

Accounting rate of return:

It is also known as average rate of return which may used by the company for evaluating

the viability of any investment proposal. Accounting rate of return is a percentage rate of return

expected on an investment or asset as compared to initial investment cost.

Calculation of Accounting rate of return for Happy Meal Ltd.

Particulars (£)

Initial Investment

(given)

320000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflows 105000 105000 105000 105000 105000 105000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Annual Cash

Outflows

15500 15500 15500 15500 15500 15500

Net Cash Inflows 89500 89500 89500 89500 89500 89500

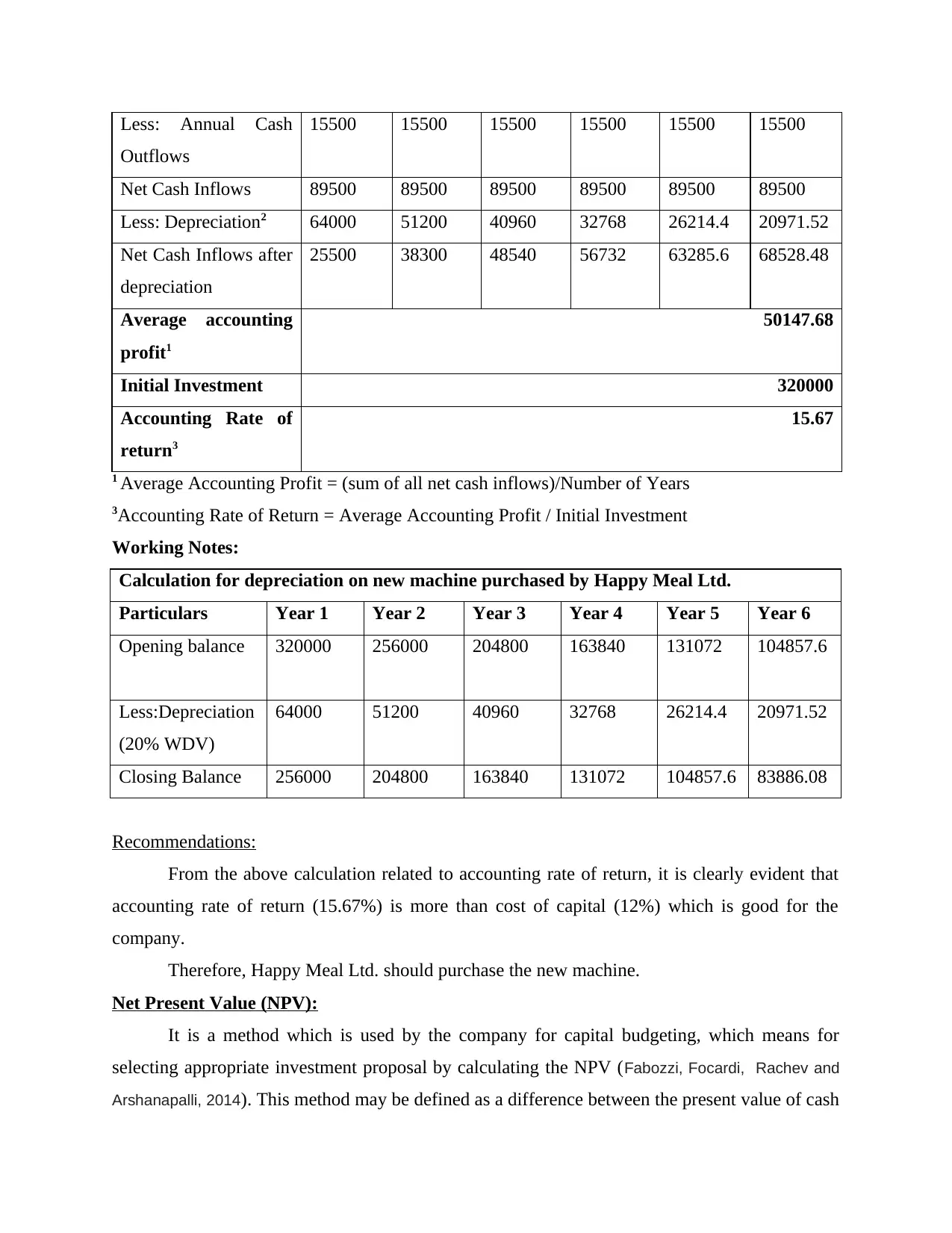

Less: Depreciation2 64000 51200 40960 32768 26214.4 20971.52

Net Cash Inflows after

depreciation

25500 38300 48540 56732 63285.6 68528.48

Average accounting

profit1

50147.68

Initial Investment 320000

Accounting Rate of

return3

15.67

1 Average Accounting Profit = (sum of all net cash inflows)/Number of Years

3Accounting Rate of Return = Average Accounting Profit / Initial Investment

Working Notes:

Calculation for depreciation on new machine purchased by Happy Meal Ltd.

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Opening balance 320000 256000 204800 163840 131072 104857.6

Less:Depreciation

(20% WDV)

64000 51200 40960 32768 26214.4 20971.52

Closing Balance 256000 204800 163840 131072 104857.6 83886.08

Recommendations:

From the above calculation related to accounting rate of return, it is clearly evident that

accounting rate of return (15.67%) is more than cost of capital (12%) which is good for the

company.

Therefore, Happy Meal Ltd. should purchase the new machine.

Net Present Value (NPV):

It is a method which is used by the company for capital budgeting, which means for

selecting appropriate investment proposal by calculating the NPV (Fabozzi, Focardi, Rachev and

Arshanapalli, 2014). This method may be defined as a difference between the present value of cash

Outflows

15500 15500 15500 15500 15500 15500

Net Cash Inflows 89500 89500 89500 89500 89500 89500

Less: Depreciation2 64000 51200 40960 32768 26214.4 20971.52

Net Cash Inflows after

depreciation

25500 38300 48540 56732 63285.6 68528.48

Average accounting

profit1

50147.68

Initial Investment 320000

Accounting Rate of

return3

15.67

1 Average Accounting Profit = (sum of all net cash inflows)/Number of Years

3Accounting Rate of Return = Average Accounting Profit / Initial Investment

Working Notes:

Calculation for depreciation on new machine purchased by Happy Meal Ltd.

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Opening balance 320000 256000 204800 163840 131072 104857.6

Less:Depreciation

(20% WDV)

64000 51200 40960 32768 26214.4 20971.52

Closing Balance 256000 204800 163840 131072 104857.6 83886.08

Recommendations:

From the above calculation related to accounting rate of return, it is clearly evident that

accounting rate of return (15.67%) is more than cost of capital (12%) which is good for the

company.

Therefore, Happy Meal Ltd. should purchase the new machine.

Net Present Value (NPV):

It is a method which is used by the company for capital budgeting, which means for

selecting appropriate investment proposal by calculating the NPV (Fabozzi, Focardi, Rachev and

Arshanapalli, 2014). This method may be defined as a difference between the present value of cash

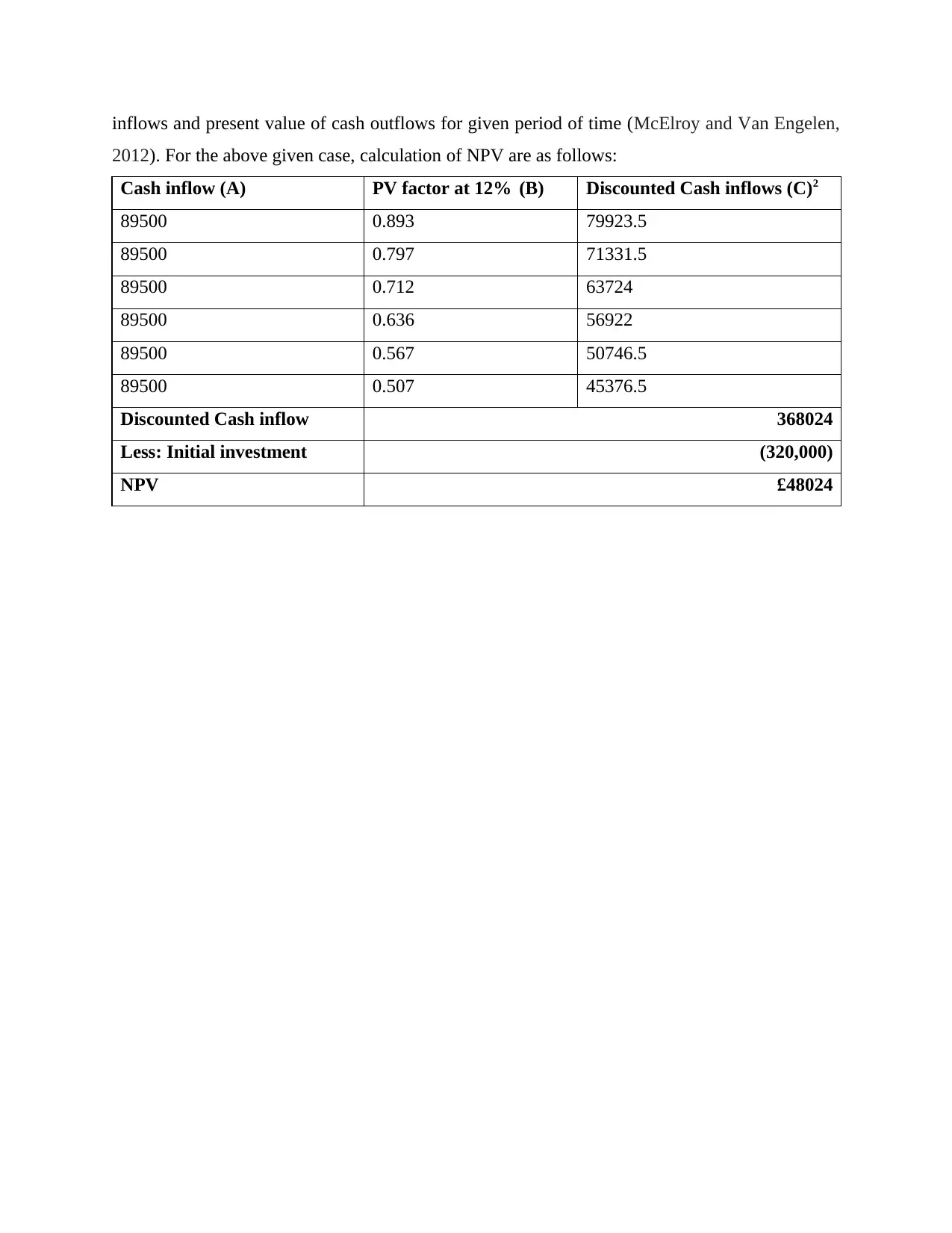

inflows and present value of cash outflows for given period of time (McElroy and Van Engelen,

2012). For the above given case, calculation of NPV are as follows:

Cash inflow (A) PV factor at 12% (B) Discounted Cash inflows (C)2

89500 0.893 79923.5

89500 0.797 71331.5

89500 0.712 63724

89500 0.636 56922

89500 0.567 50746.5

89500 0.507 45376.5

Discounted Cash inflow 368024

Less: Initial investment (320,000)

NPV £48024

2012). For the above given case, calculation of NPV are as follows:

Cash inflow (A) PV factor at 12% (B) Discounted Cash inflows (C)2

89500 0.893 79923.5

89500 0.797 71331.5

89500 0.712 63724

89500 0.636 56922

89500 0.567 50746.5

89500 0.507 45376.5

Discounted Cash inflow 368024

Less: Initial investment (320,000)

NPV £48024

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

NOTE: Cost of capital of 12% furnished in the sum itself which is taken as the discounting rate

for calculating the present value of cash inflows.

Recommendations:

After observing the above solution related to NPV, it is clearly evident that there is a

positive net present value in this scenario which is £48024. Therefore, Happy Meal Ltd. should

purchase this new machine for better results for its future profitability.

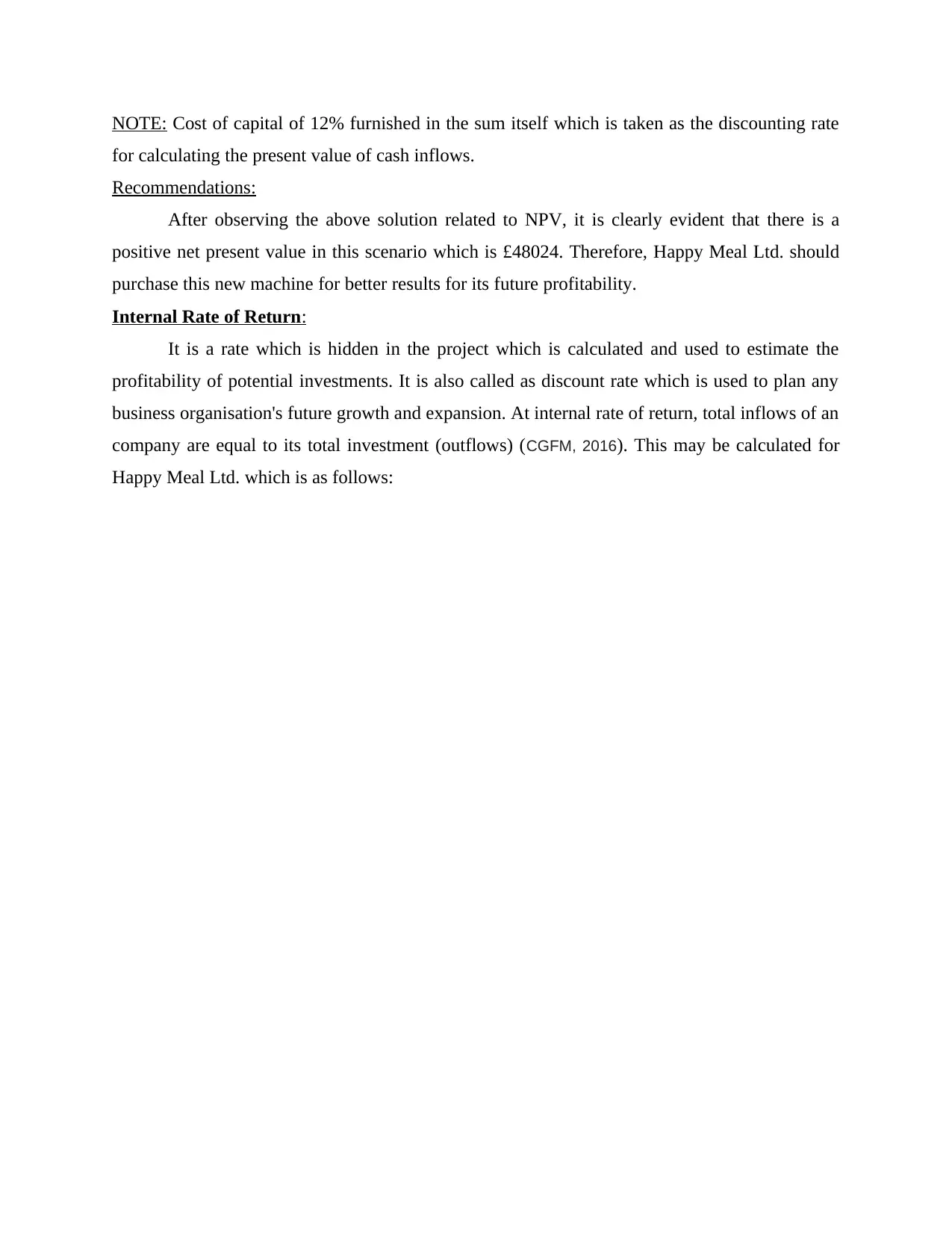

Internal Rate of Return:

It is a rate which is hidden in the project which is calculated and used to estimate the

profitability of potential investments. It is also called as discount rate which is used to plan any

business organisation's future growth and expansion. At internal rate of return, total inflows of an

company are equal to its total investment (outflows) (CGFM, 2016). This may be calculated for

Happy Meal Ltd. which is as follows:

for calculating the present value of cash inflows.

Recommendations:

After observing the above solution related to NPV, it is clearly evident that there is a

positive net present value in this scenario which is £48024. Therefore, Happy Meal Ltd. should

purchase this new machine for better results for its future profitability.

Internal Rate of Return:

It is a rate which is hidden in the project which is calculated and used to estimate the

profitability of potential investments. It is also called as discount rate which is used to plan any

business organisation's future growth and expansion. At internal rate of return, total inflows of an

company are equal to its total investment (outflows) (CGFM, 2016). This may be calculated for

Happy Meal Ltd. which is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working Notes:

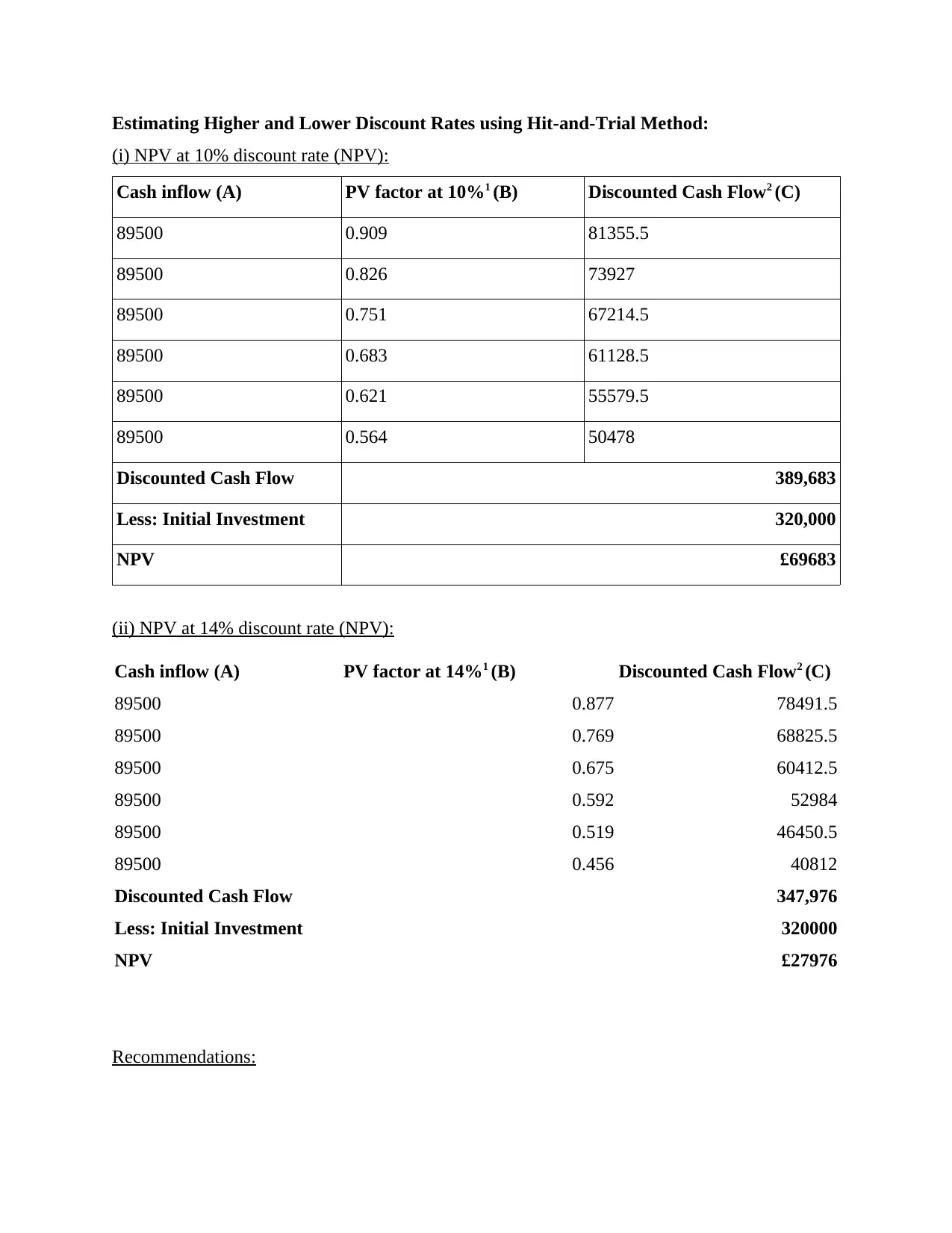

Estimating Higher and Lower Discount Rates using Hit-and-Trial Method:

(i) NPV at 10% discount rate (NPV):

Cash inflow (A) PV factor at 10%1 (B) Discounted Cash Flow2 (C)

89500 0.909 81355.5

89500 0.826 73927

89500 0.751 67214.5

89500 0.683 61128.5

89500 0.621 55579.5

89500 0.564 50478

Discounted Cash Flow 389,683

Less: Initial Investment 320,000

NPV £69683

(ii) NPV at 14% discount rate (NPV):

Cash inflow (A) PV factor at 14%1 (B) Discounted Cash Flow2 (C)

89500 0.877 78491.5

89500 0.769 68825.5

89500 0.675 60412.5

89500 0.592 52984

89500 0.519 46450.5

89500 0.456 40812

Discounted Cash Flow 347,976

Less: Initial Investment 320000

NPV £27976

Recommendations:

(i) NPV at 10% discount rate (NPV):

Cash inflow (A) PV factor at 10%1 (B) Discounted Cash Flow2 (C)

89500 0.909 81355.5

89500 0.826 73927

89500 0.751 67214.5

89500 0.683 61128.5

89500 0.621 55579.5

89500 0.564 50478

Discounted Cash Flow 389,683

Less: Initial Investment 320,000

NPV £69683

(ii) NPV at 14% discount rate (NPV):

Cash inflow (A) PV factor at 14%1 (B) Discounted Cash Flow2 (C)

89500 0.877 78491.5

89500 0.769 68825.5

89500 0.675 60412.5

89500 0.592 52984

89500 0.519 46450.5

89500 0.456 40812

Discounted Cash Flow 347,976

Less: Initial Investment 320000

NPV £27976

Recommendations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.