Financial Management Report: Analyzing Investment Appraisal Methods

VerifiedAdded on 2022/12/14

|14

|3721

|345

Report

AI Summary

This comprehensive report delves into the core concepts of financial management, providing an in-depth analysis of key investment appraisal techniques. It begins with an introduction to financial management and its role in organizing and controlling financial activities within an organization. The report then explores the payback period, discounted cash flow, accounting rate of return, net present value (NPV), and internal rate of return (IRR), detailing their methodologies, advantages, and limitations. The report includes calculations and examples to illustrate these concepts. Furthermore, it examines the advantages and disadvantages of various investment appraisal techniques, including the benefits and drawbacks of the payback period, accounting rate of return, NPV, and IRR. The report also touches upon mergers and acquisitions and price-earnings ratio and their significance in financial analysis.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................2

Payback period.............................................................................................................................3

Merger and acquisition.................................................................................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction......................................................................................................................................2

Payback period.............................................................................................................................3

Merger and acquisition.................................................................................................................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Introduction

Financial management levels to the lining organising and controlling of the financial activities in

the organisation (Bulturbayevich and et.al 2020). This report focuses on IRR, NPV, and payback

period. Besides this, price earning ration and discounted cash flow is also mentioned in this

report.

Payback period

Payback period is widely used in capital budgeting. Payback period shows the required time to

reach at the breakeven point. Payback period includes positive and negative cash flow to

calculate the break even and assist the company how much investment they have to make more

to reach at the breakeven point. As per the Thumb rule it states that shorter payback period give

more return as compared to longer payback period. One of the biggest advantages of using

payback period is that the concept is very simple and easy to adopt. It helps the company and

investor to know the return on the invested amount in how much money they will generate in the

future apart from this it also gives the information about risk which is present in the investment

Discounted cash flow

It is also one of the methods which is used for valuation and it estimate the value of an

investment which is based on its expected and predicted future cash flow (Atmadja and et.al

2018). Discounted cash flow helps in analysing the value of an investment which is present today

the value is based on projections of money which will going to generate in the future.

Accounting rate of return

Accounting rate of return as widely known as average rate of return. It is also one of the financial

ratio which is used and proffered in capital budgeting. This ratio also helps the investor to know

the rate of return on their investment. Apart from this accounting rate of return compares the

future expected price to present value. One of the biggest advantages of accounting rate of return

is that it is being used in multiple projects and provides expected rate of return for each and

individual project. Accounting rate of return to not used for long-term projects as it increases the

uncertainty of long time duration apart from this it does not consider any kind of risk in the

investment. Basically accounting rate of return provides the profitability off the investment by

evaluating the capital invested in the project. One of the biggest advantages of accounting rate of

Financial management levels to the lining organising and controlling of the financial activities in

the organisation (Bulturbayevich and et.al 2020). This report focuses on IRR, NPV, and payback

period. Besides this, price earning ration and discounted cash flow is also mentioned in this

report.

Payback period

Payback period is widely used in capital budgeting. Payback period shows the required time to

reach at the breakeven point. Payback period includes positive and negative cash flow to

calculate the break even and assist the company how much investment they have to make more

to reach at the breakeven point. As per the Thumb rule it states that shorter payback period give

more return as compared to longer payback period. One of the biggest advantages of using

payback period is that the concept is very simple and easy to adopt. It helps the company and

investor to know the return on the invested amount in how much money they will generate in the

future apart from this it also gives the information about risk which is present in the investment

Discounted cash flow

It is also one of the methods which is used for valuation and it estimate the value of an

investment which is based on its expected and predicted future cash flow (Atmadja and et.al

2018). Discounted cash flow helps in analysing the value of an investment which is present today

the value is based on projections of money which will going to generate in the future.

Accounting rate of return

Accounting rate of return as widely known as average rate of return. It is also one of the financial

ratio which is used and proffered in capital budgeting. This ratio also helps the investor to know

the rate of return on their investment. Apart from this accounting rate of return compares the

future expected price to present value. One of the biggest advantages of accounting rate of return

is that it is being used in multiple projects and provides expected rate of return for each and

individual project. Accounting rate of return to not used for long-term projects as it increases the

uncertainty of long time duration apart from this it does not consider any kind of risk in the

investment. Basically accounting rate of return provides the profitability off the investment by

evaluating the capital invested in the project. One of the biggest advantages of accounting rate of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

return is that it is easy to calculate and provide accurate results to the investor and Company.

Besides this the main feature of accounting rate of return is that it measures the overall

performance and current performance of the project and gives the rate of profitability to the

investor so that they can make their decision according to the return (Brigham and et.al 2021).

This method provides a comparison of different projects to the investor so that they can select

best option which is available for them and create profit in the long run.

Net present value

Net present value provides the present value of the cash flow on the required rate of return for the

project which is compared to the initial investment. Basically net present value is the difference

between cash inflow and the cash outflow for a period of time. This is also a tool of capital

budgeting which is used to analyse and recognise the profitability of the project. Net present

value is used to compare different investment alternatives. Net present value is fully dependent

on discount rate which can be calculated from the cost of capital required. The main motive of

using net present value is to calculate the total value which is present today and it assist the

company or the investor about the future payment and expenses. Positive net present value shows

that the project is in profit and investment will provide better return to the investor and the

company (Loke, 2017). On the flip side and negative net present value shows that investor or the

company will face loss in the future. Net present value shows that whatever value of the money

is present today will not remain the same in the future it may fall down or will raise so as per the

money net present value provides better education and information to the investor so that by

seeing all the projected net present value they can make their investment decisions.

Internal rate of return

Internal rate of return is it tool and matrix which is used and financial analysis to recognise the

profitability of the investment. The internal rate of return is popularly known as discount rate

which makes the net present value and cash flow equal to zero in the analysis of discounted cash

flow. The formula of internal rate of return is similar to net present value. It shows the annual

rate of return which makes the entire net present value equal to zero (Wijesuriya and et.al 2017).

Higher rate of return shows that project is going to have high profitability and will generate more

return as compared to low internal rate of return. It is also used in selecting best project and

investment option from the available options. It helps the investor to compare different projects

and investment options and assist them to select best option for them which will provide them

Besides this the main feature of accounting rate of return is that it measures the overall

performance and current performance of the project and gives the rate of profitability to the

investor so that they can make their decision according to the return (Brigham and et.al 2021).

This method provides a comparison of different projects to the investor so that they can select

best option which is available for them and create profit in the long run.

Net present value

Net present value provides the present value of the cash flow on the required rate of return for the

project which is compared to the initial investment. Basically net present value is the difference

between cash inflow and the cash outflow for a period of time. This is also a tool of capital

budgeting which is used to analyse and recognise the profitability of the project. Net present

value is used to compare different investment alternatives. Net present value is fully dependent

on discount rate which can be calculated from the cost of capital required. The main motive of

using net present value is to calculate the total value which is present today and it assist the

company or the investor about the future payment and expenses. Positive net present value shows

that the project is in profit and investment will provide better return to the investor and the

company (Loke, 2017). On the flip side and negative net present value shows that investor or the

company will face loss in the future. Net present value shows that whatever value of the money

is present today will not remain the same in the future it may fall down or will raise so as per the

money net present value provides better education and information to the investor so that by

seeing all the projected net present value they can make their investment decisions.

Internal rate of return

Internal rate of return is it tool and matrix which is used and financial analysis to recognise the

profitability of the investment. The internal rate of return is popularly known as discount rate

which makes the net present value and cash flow equal to zero in the analysis of discounted cash

flow. The formula of internal rate of return is similar to net present value. It shows the annual

rate of return which makes the entire net present value equal to zero (Wijesuriya and et.al 2017).

Higher rate of return shows that project is going to have high profitability and will generate more

return as compared to low internal rate of return. It is also used in selecting best project and

investment option from the available options. It helps the investor to compare different projects

and investment options and assist them to select best option for them which will provide them

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

better return and outcome. Internal rate of return widely used to know the potential rate of return

on the project.

Advantage and disadvantage of investment appraisal technique

Advantages of Payback period

One of the biggest advantages of Payback period is that it is easy to calculate and use. Apart from

this payback period used very less inputs and provide better result. With the help of initial cost of

project and annual cash flow payback period can be calculated. Apart from this it provides quick

solution to the company about the investment. As it is useful for shorter time duration therefore

payback period provides more liquidity to the investor.

Limitations of Payback period

As payback period has many advantages but the biggest limitation of this method is that it knows

the time value of money from the project (Crespo and et.al 2019. ). Apart from this while

calculating payback period and do not include all cash flows which sometimes give wrong

information and result to the investor. Those project which are short term in nature so payback

period do not give any guarantee that the short projects will get profit in the future.

Benefits of accounting rate of return

It is also one of the easiest ways to calculate the profit for a project apart from this it includes the

total profit and savings for the entire life of the project. This method is basically used by those

companies who have many projects to invest with the help of accounting rate of return they can

select best project for them. This method provides clear picture of revenue and profit of the

project. This method is very useful for the investors as it satisfy the need of the Investor by

providing them accurate rate of return on the investment.

Disadvantage of accounting rate of return

One of the biggest disadvantages of accounting rate of return is that it sometimes provide

different result for the same project which can provide misleading information to the investor.

Another thing is that accounting rate of return to not include time factor which is one of the

primary weakness of this method (Abdelhady, 2021). Accounting rate of return do not consider

external factors as well which can harm the profitability of the project. Apart from this

accounting rate of return do not use cash inflows which are the most important part of the

prophet. So these are the primary weaknesses of accounting rate of return.

Advantages of net present value

on the project.

Advantage and disadvantage of investment appraisal technique

Advantages of Payback period

One of the biggest advantages of Payback period is that it is easy to calculate and use. Apart from

this payback period used very less inputs and provide better result. With the help of initial cost of

project and annual cash flow payback period can be calculated. Apart from this it provides quick

solution to the company about the investment. As it is useful for shorter time duration therefore

payback period provides more liquidity to the investor.

Limitations of Payback period

As payback period has many advantages but the biggest limitation of this method is that it knows

the time value of money from the project (Crespo and et.al 2019. ). Apart from this while

calculating payback period and do not include all cash flows which sometimes give wrong

information and result to the investor. Those project which are short term in nature so payback

period do not give any guarantee that the short projects will get profit in the future.

Benefits of accounting rate of return

It is also one of the easiest ways to calculate the profit for a project apart from this it includes the

total profit and savings for the entire life of the project. This method is basically used by those

companies who have many projects to invest with the help of accounting rate of return they can

select best project for them. This method provides clear picture of revenue and profit of the

project. This method is very useful for the investors as it satisfy the need of the Investor by

providing them accurate rate of return on the investment.

Disadvantage of accounting rate of return

One of the biggest disadvantages of accounting rate of return is that it sometimes provide

different result for the same project which can provide misleading information to the investor.

Another thing is that accounting rate of return to not include time factor which is one of the

primary weakness of this method (Abdelhady, 2021). Accounting rate of return do not consider

external factors as well which can harm the profitability of the project. Apart from this

accounting rate of return do not use cash inflows which are the most important part of the

prophet. So these are the primary weaknesses of accounting rate of return.

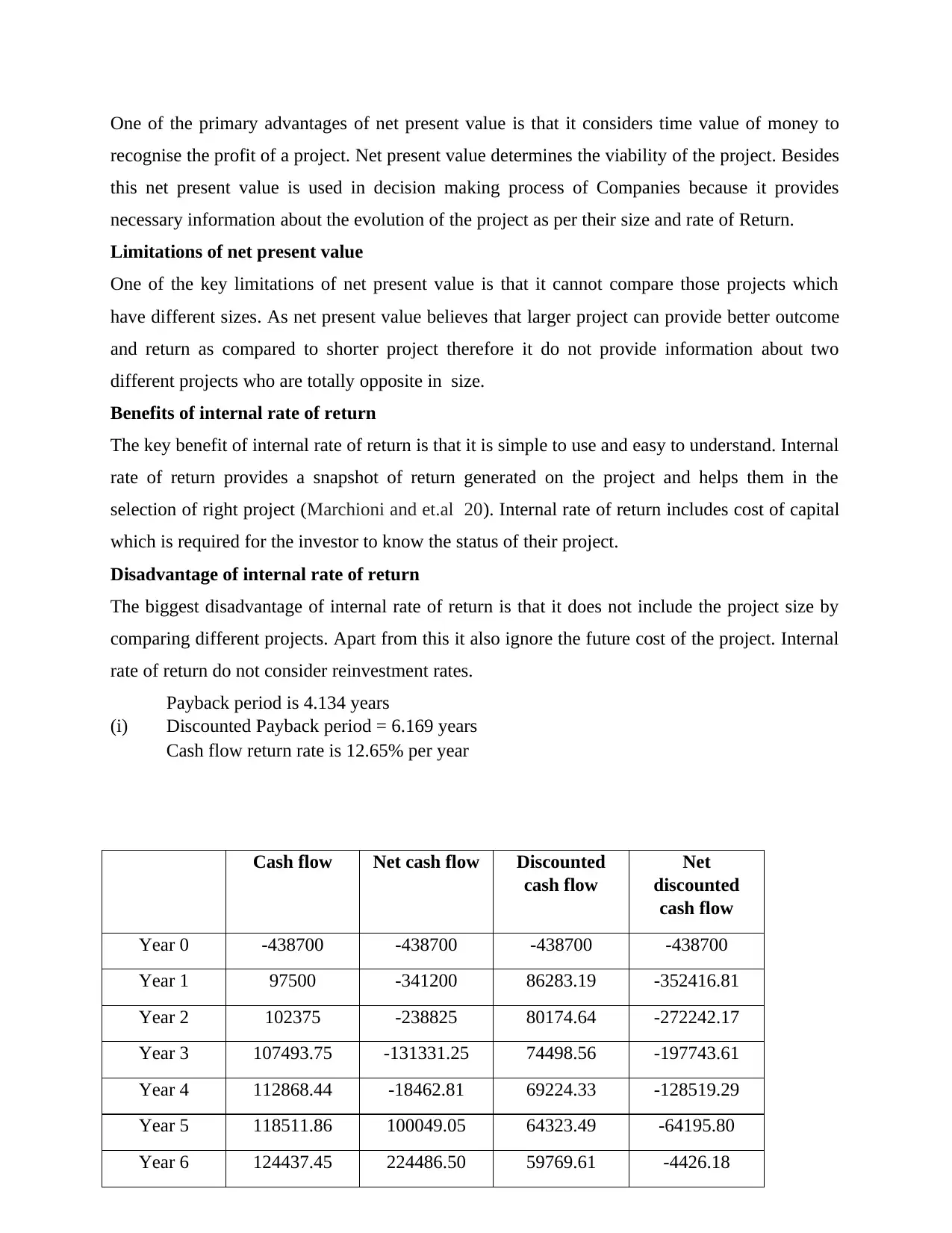

Advantages of net present value

One of the primary advantages of net present value is that it considers time value of money to

recognise the profit of a project. Net present value determines the viability of the project. Besides

this net present value is used in decision making process of Companies because it provides

necessary information about the evolution of the project as per their size and rate of Return.

Limitations of net present value

One of the key limitations of net present value is that it cannot compare those projects which

have different sizes. As net present value believes that larger project can provide better outcome

and return as compared to shorter project therefore it do not provide information about two

different projects who are totally opposite in size.

Benefits of internal rate of return

The key benefit of internal rate of return is that it is simple to use and easy to understand. Internal

rate of return provides a snapshot of return generated on the project and helps them in the

selection of right project (Marchioni and et.al 20). Internal rate of return includes cost of capital

which is required for the investor to know the status of their project.

Disadvantage of internal rate of return

The biggest disadvantage of internal rate of return is that it does not include the project size by

comparing different projects. Apart from this it also ignore the future cost of the project. Internal

rate of return do not consider reinvestment rates.

Payback period is 4.134 years

(i) Discounted Payback period = 6.169 years

Cash flow return rate is 12.65% per year

Cash flow Net cash flow Discounted

cash flow

Net

discounted

cash flow

Year 0 -438700 -438700 -438700 -438700

Year 1 97500 -341200 86283.19 -352416.81

Year 2 102375 -238825 80174.64 -272242.17

Year 3 107493.75 -131331.25 74498.56 -197743.61

Year 4 112868.44 -18462.81 69224.33 -128519.29

Year 5 118511.86 100049.05 64323.49 -64195.80

Year 6 124437.45 224486.50 59769.61 -4426.18

recognise the profit of a project. Net present value determines the viability of the project. Besides

this net present value is used in decision making process of Companies because it provides

necessary information about the evolution of the project as per their size and rate of Return.

Limitations of net present value

One of the key limitations of net present value is that it cannot compare those projects which

have different sizes. As net present value believes that larger project can provide better outcome

and return as compared to shorter project therefore it do not provide information about two

different projects who are totally opposite in size.

Benefits of internal rate of return

The key benefit of internal rate of return is that it is simple to use and easy to understand. Internal

rate of return provides a snapshot of return generated on the project and helps them in the

selection of right project (Marchioni and et.al 20). Internal rate of return includes cost of capital

which is required for the investor to know the status of their project.

Disadvantage of internal rate of return

The biggest disadvantage of internal rate of return is that it does not include the project size by

comparing different projects. Apart from this it also ignore the future cost of the project. Internal

rate of return do not consider reinvestment rates.

Payback period is 4.134 years

(i) Discounted Payback period = 6.169 years

Cash flow return rate is 12.65% per year

Cash flow Net cash flow Discounted

cash flow

Net

discounted

cash flow

Year 0 -438700 -438700 -438700 -438700

Year 1 97500 -341200 86283.19 -352416.81

Year 2 102375 -238825 80174.64 -272242.17

Year 3 107493.75 -131331.25 74498.56 -197743.61

Year 4 112868.44 -18462.81 69224.33 -128519.29

Year 5 118511.86 100049.05 64323.49 -64195.80

Year 6 124437.45 224486.50 59769.61 -4426.18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

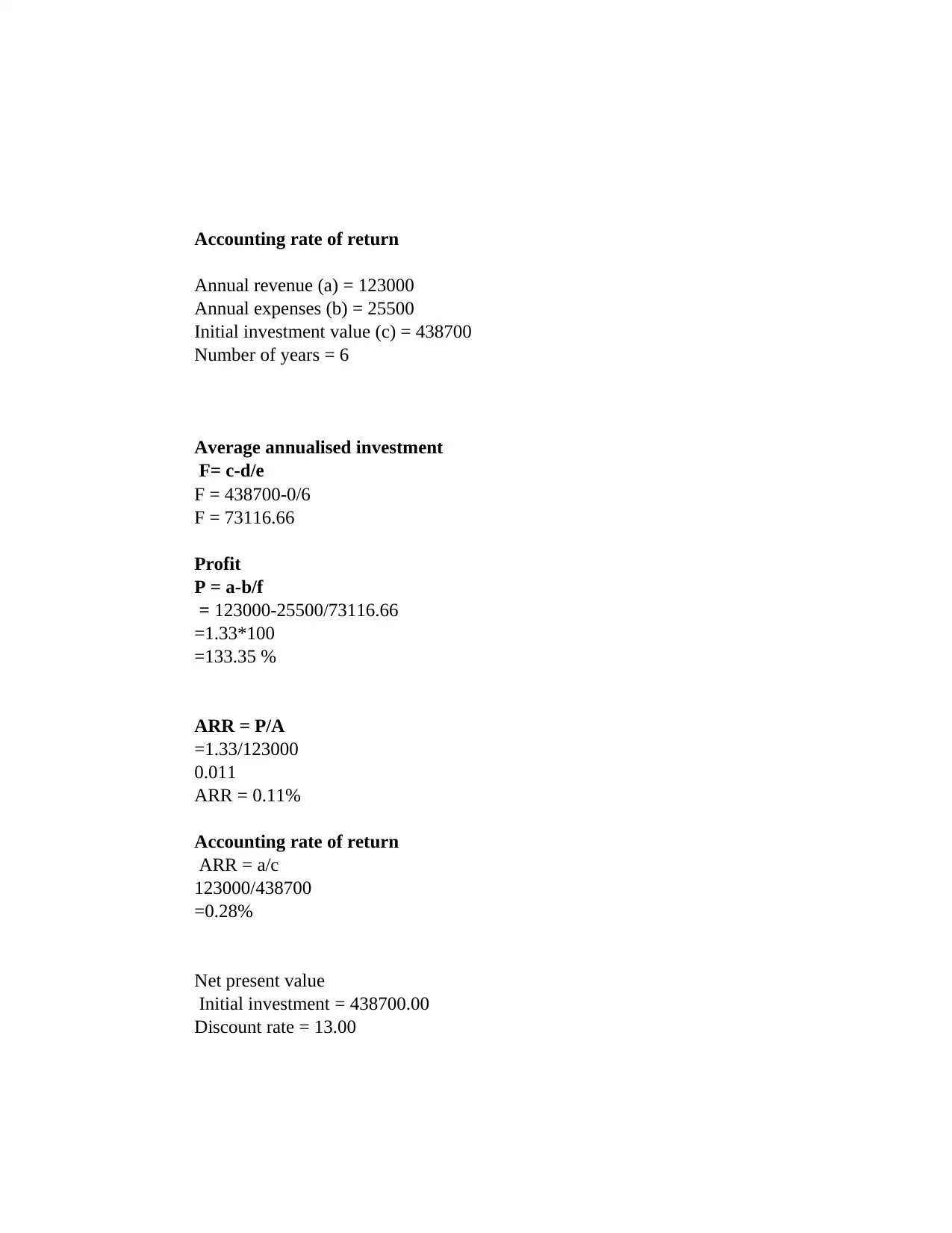

Accounting rate of return

Annual revenue (a) = 123000

Annual expenses (b) = 25500

Initial investment value (c) = 438700

Number of years = 6

Average annualised investment

F= c-d/e

F = 438700-0/6

F = 73116.66

Profit

P = a-b/f

= 123000-25500/73116.66

=1.33*100

=133.35 %

ARR = P/A

=1.33/123000

0.011

ARR = 0.11%

Accounting rate of return

ARR = a/c

123000/438700

=0.28%

Net present value

Initial investment = 438700.00

Discount rate = 13.00

Annual revenue (a) = 123000

Annual expenses (b) = 25500

Initial investment value (c) = 438700

Number of years = 6

Average annualised investment

F= c-d/e

F = 438700-0/6

F = 73116.66

Profit

P = a-b/f

= 123000-25500/73116.66

=1.33*100

=133.35 %

ARR = P/A

=1.33/123000

0.011

ARR = 0.11%

Accounting rate of return

ARR = a/c

123000/438700

=0.28%

Net present value

Initial investment = 438700.00

Discount rate = 13.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

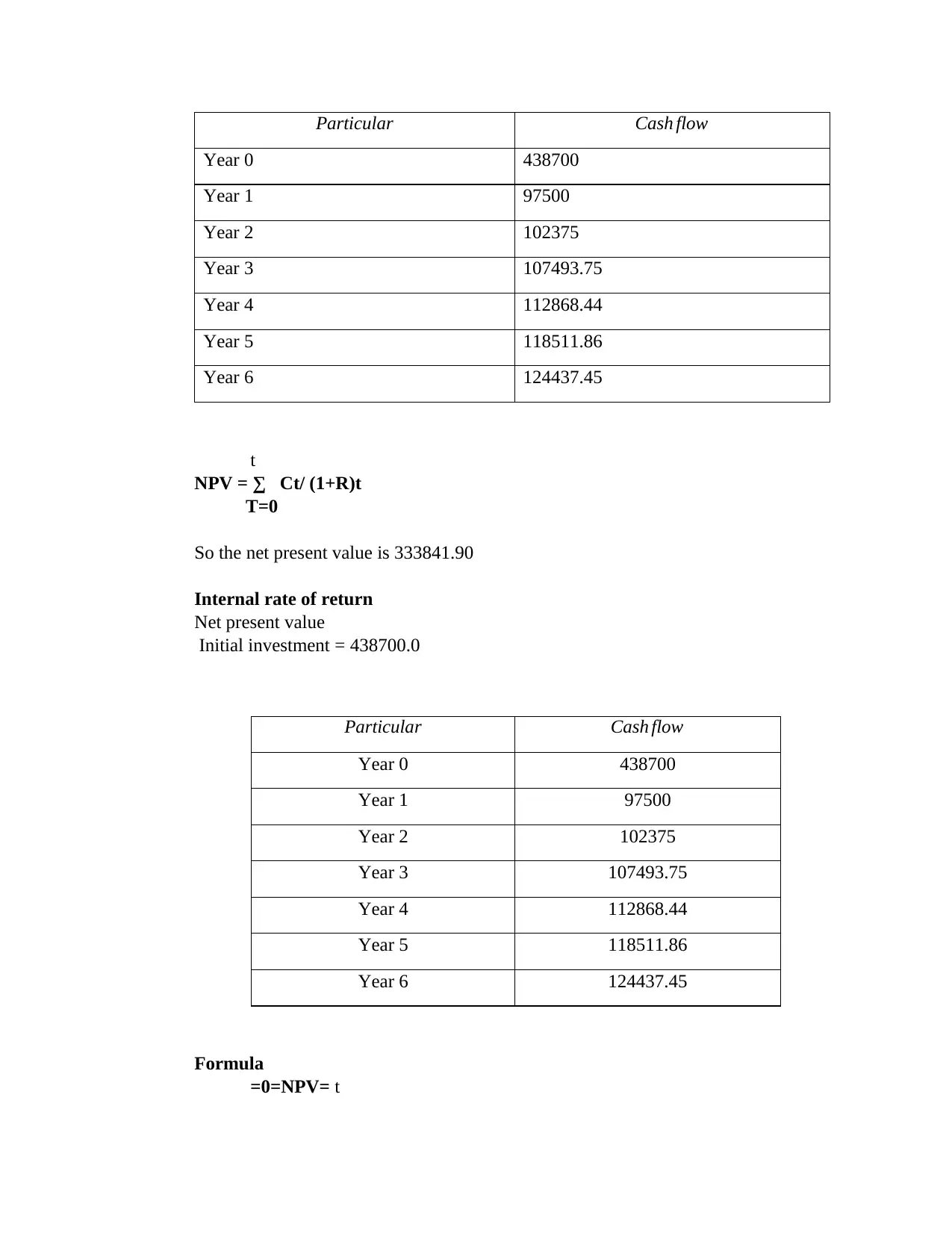

Particular Cash flow

Year 0 438700

Year 1 97500

Year 2 102375

Year 3 107493.75

Year 4 112868.44

Year 5 118511.86

Year 6 124437.45

t

NPV = ∑ Ct/ (1+R)t

T=0

So the net present value is 333841.90

Internal rate of return

Net present value

Initial investment = 438700.0

Particular Cash flow

Year 0 438700

Year 1 97500

Year 2 102375

Year 3 107493.75

Year 4 112868.44

Year 5 118511.86

Year 6 124437.45

Formula

=0=NPV= t

Year 0 438700

Year 1 97500

Year 2 102375

Year 3 107493.75

Year 4 112868.44

Year 5 118511.86

Year 6 124437.45

t

NPV = ∑ Ct/ (1+R)t

T=0

So the net present value is 333841.90

Internal rate of return

Net present value

Initial investment = 438700.0

Particular Cash flow

Year 0 438700

Year 1 97500

Year 2 102375

Year 3 107493.75

Year 4 112868.44

Year 5 118511.86

Year 6 124437.45

Formula

=0=NPV= t

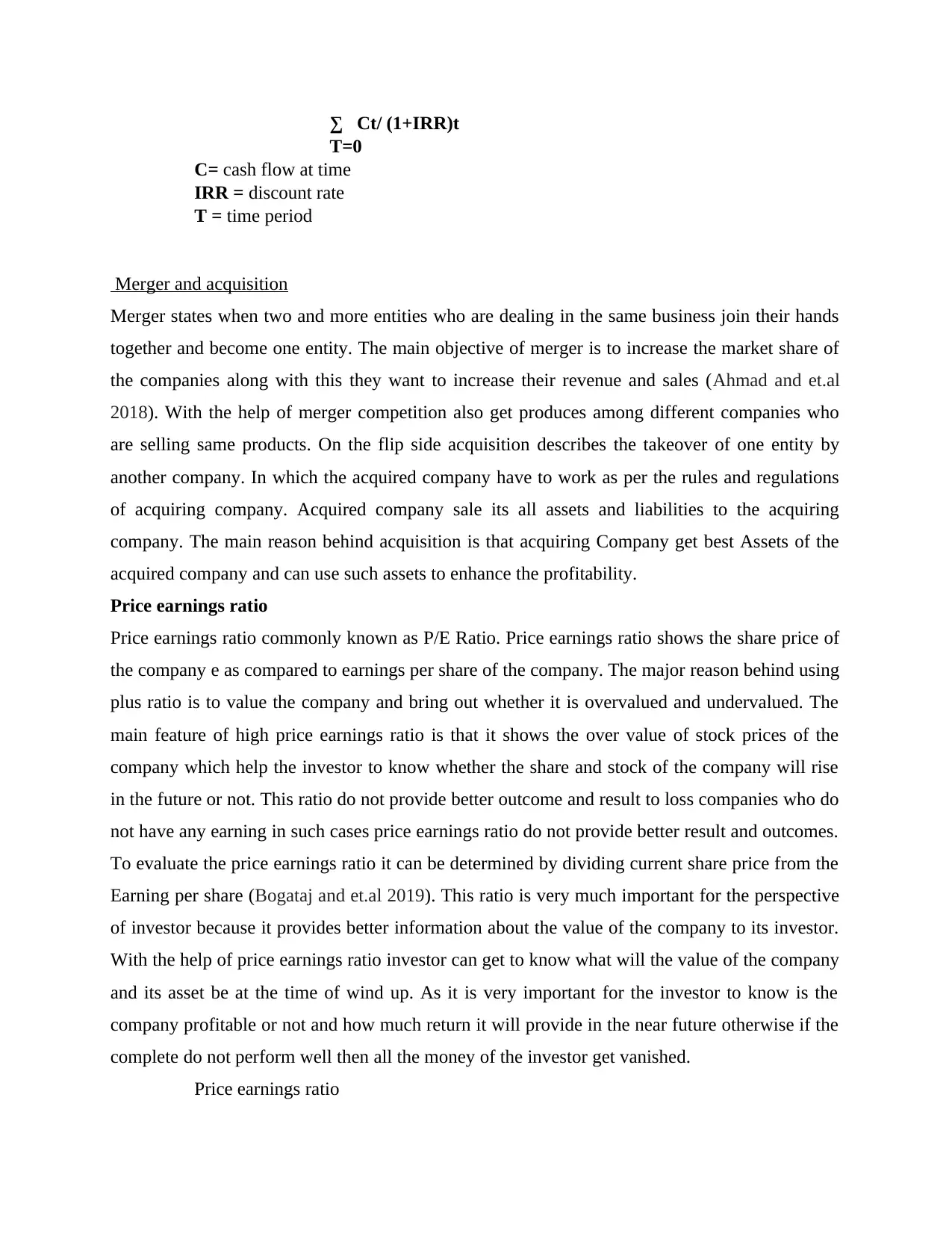

∑ Ct/ (1+IRR)t

T=0

C= cash flow at time

IRR = discount rate

T = time period

Merger and acquisition

Merger states when two and more entities who are dealing in the same business join their hands

together and become one entity. The main objective of merger is to increase the market share of

the companies along with this they want to increase their revenue and sales (Ahmad and et.al

2018). With the help of merger competition also get produces among different companies who

are selling same products. On the flip side acquisition describes the takeover of one entity by

another company. In which the acquired company have to work as per the rules and regulations

of acquiring company. Acquired company sale its all assets and liabilities to the acquiring

company. The main reason behind acquisition is that acquiring Company get best Assets of the

acquired company and can use such assets to enhance the profitability.

Price earnings ratio

Price earnings ratio commonly known as P/E Ratio. Price earnings ratio shows the share price of

the company e as compared to earnings per share of the company. The major reason behind using

plus ratio is to value the company and bring out whether it is overvalued and undervalued. The

main feature of high price earnings ratio is that it shows the over value of stock prices of the

company which help the investor to know whether the share and stock of the company will rise

in the future or not. This ratio do not provide better outcome and result to loss companies who do

not have any earning in such cases price earnings ratio do not provide better result and outcomes.

To evaluate the price earnings ratio it can be determined by dividing current share price from the

Earning per share (Bogataj and et.al 2019). This ratio is very much important for the perspective

of investor because it provides better information about the value of the company to its investor.

With the help of price earnings ratio investor can get to know what will the value of the company

and its asset be at the time of wind up. As it is very important for the investor to know is the

company profitable or not and how much return it will provide in the near future otherwise if the

complete do not perform well then all the money of the investor get vanished.

Price earnings ratio

T=0

C= cash flow at time

IRR = discount rate

T = time period

Merger and acquisition

Merger states when two and more entities who are dealing in the same business join their hands

together and become one entity. The main objective of merger is to increase the market share of

the companies along with this they want to increase their revenue and sales (Ahmad and et.al

2018). With the help of merger competition also get produces among different companies who

are selling same products. On the flip side acquisition describes the takeover of one entity by

another company. In which the acquired company have to work as per the rules and regulations

of acquiring company. Acquired company sale its all assets and liabilities to the acquiring

company. The main reason behind acquisition is that acquiring Company get best Assets of the

acquired company and can use such assets to enhance the profitability.

Price earnings ratio

Price earnings ratio commonly known as P/E Ratio. Price earnings ratio shows the share price of

the company e as compared to earnings per share of the company. The major reason behind using

plus ratio is to value the company and bring out whether it is overvalued and undervalued. The

main feature of high price earnings ratio is that it shows the over value of stock prices of the

company which help the investor to know whether the share and stock of the company will rise

in the future or not. This ratio do not provide better outcome and result to loss companies who do

not have any earning in such cases price earnings ratio do not provide better result and outcomes.

To evaluate the price earnings ratio it can be determined by dividing current share price from the

Earning per share (Bogataj and et.al 2019). This ratio is very much important for the perspective

of investor because it provides better information about the value of the company to its investor.

With the help of price earnings ratio investor can get to know what will the value of the company

and its asset be at the time of wind up. As it is very important for the investor to know is the

company profitable or not and how much return it will provide in the near future otherwise if the

complete do not perform well then all the money of the investor get vanished.

Price earnings ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

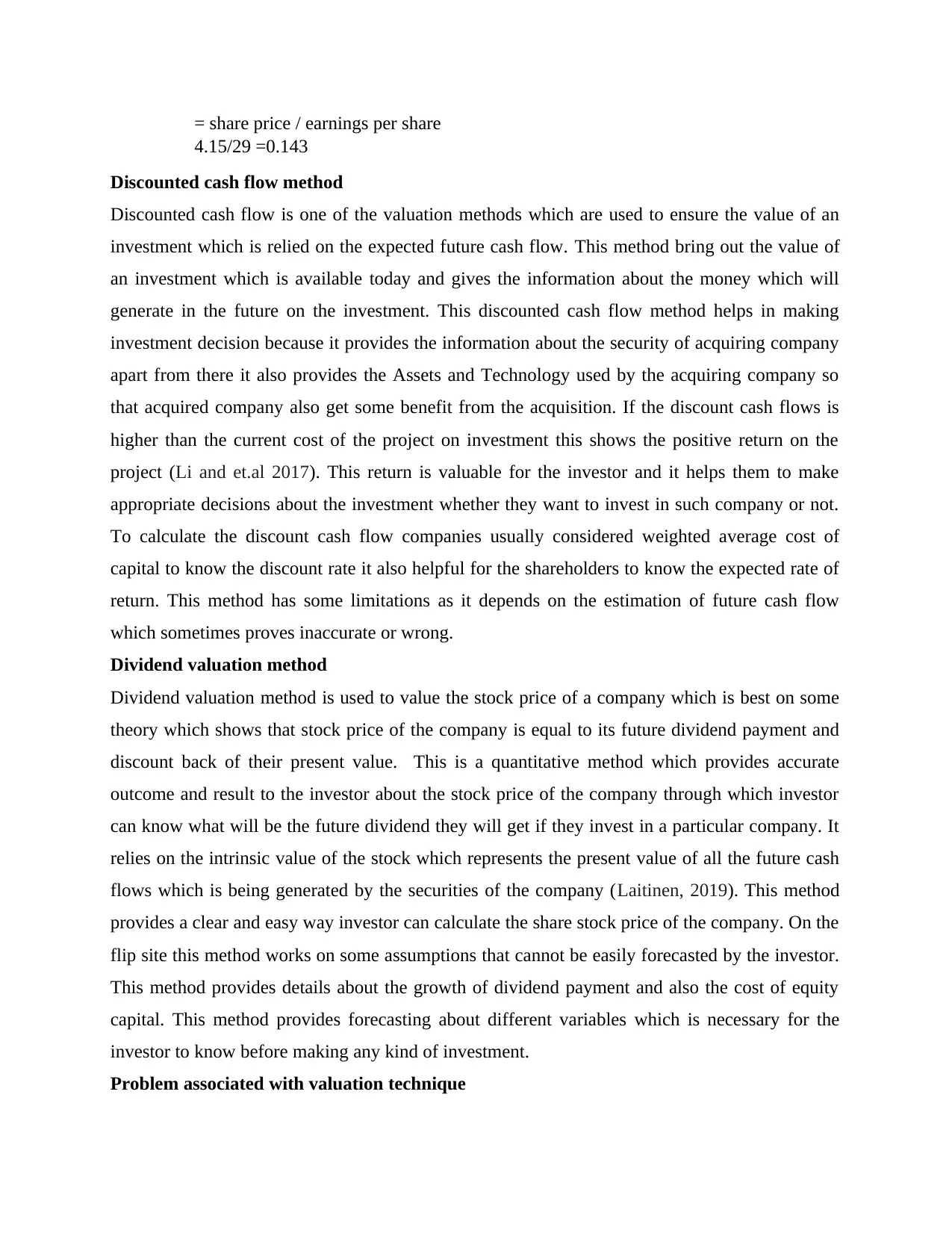

= share price / earnings per share

4.15/29 =0.143

Discounted cash flow method

Discounted cash flow is one of the valuation methods which are used to ensure the value of an

investment which is relied on the expected future cash flow. This method bring out the value of

an investment which is available today and gives the information about the money which will

generate in the future on the investment. This discounted cash flow method helps in making

investment decision because it provides the information about the security of acquiring company

apart from there it also provides the Assets and Technology used by the acquiring company so

that acquired company also get some benefit from the acquisition. If the discount cash flows is

higher than the current cost of the project on investment this shows the positive return on the

project (Li and et.al 2017). This return is valuable for the investor and it helps them to make

appropriate decisions about the investment whether they want to invest in such company or not.

To calculate the discount cash flow companies usually considered weighted average cost of

capital to know the discount rate it also helpful for the shareholders to know the expected rate of

return. This method has some limitations as it depends on the estimation of future cash flow

which sometimes proves inaccurate or wrong.

Dividend valuation method

Dividend valuation method is used to value the stock price of a company which is best on some

theory which shows that stock price of the company is equal to its future dividend payment and

discount back of their present value. This is a quantitative method which provides accurate

outcome and result to the investor about the stock price of the company through which investor

can know what will be the future dividend they will get if they invest in a particular company. It

relies on the intrinsic value of the stock which represents the present value of all the future cash

flows which is being generated by the securities of the company (Laitinen, 2019). This method

provides a clear and easy way investor can calculate the share stock price of the company. On the

flip site this method works on some assumptions that cannot be easily forecasted by the investor.

This method provides details about the growth of dividend payment and also the cost of equity

capital. This method provides forecasting about different variables which is necessary for the

investor to know before making any kind of investment.

Problem associated with valuation technique

4.15/29 =0.143

Discounted cash flow method

Discounted cash flow is one of the valuation methods which are used to ensure the value of an

investment which is relied on the expected future cash flow. This method bring out the value of

an investment which is available today and gives the information about the money which will

generate in the future on the investment. This discounted cash flow method helps in making

investment decision because it provides the information about the security of acquiring company

apart from there it also provides the Assets and Technology used by the acquiring company so

that acquired company also get some benefit from the acquisition. If the discount cash flows is

higher than the current cost of the project on investment this shows the positive return on the

project (Li and et.al 2017). This return is valuable for the investor and it helps them to make

appropriate decisions about the investment whether they want to invest in such company or not.

To calculate the discount cash flow companies usually considered weighted average cost of

capital to know the discount rate it also helpful for the shareholders to know the expected rate of

return. This method has some limitations as it depends on the estimation of future cash flow

which sometimes proves inaccurate or wrong.

Dividend valuation method

Dividend valuation method is used to value the stock price of a company which is best on some

theory which shows that stock price of the company is equal to its future dividend payment and

discount back of their present value. This is a quantitative method which provides accurate

outcome and result to the investor about the stock price of the company through which investor

can know what will be the future dividend they will get if they invest in a particular company. It

relies on the intrinsic value of the stock which represents the present value of all the future cash

flows which is being generated by the securities of the company (Laitinen, 2019). This method

provides a clear and easy way investor can calculate the share stock price of the company. On the

flip site this method works on some assumptions that cannot be easily forecasted by the investor.

This method provides details about the growth of dividend payment and also the cost of equity

capital. This method provides forecasting about different variables which is necessary for the

investor to know before making any kind of investment.

Problem associated with valuation technique

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are few problems which is associated with price to earnings ratio although it is helpful my

drink which gives good relations about the company’s share price. What price do i need a show

sometimes become difficult to use while comparing different companies of the industry. Is

different industries but different companies have different price to earnings ratio. Some

companies have zero P/E ratio and some have very high price to earnings ratio. With the help of

price to earnings ratio it can be known which stocks are cheap and which is blue chip in nature so

as per the prices of stocks investor can made their decisions. P/ E ratio provides a benchmark to

the investor about the company and its stock prices. It can be fluctuate and there is a possibility

that the stock do not fluctuate as per the P/E ratio so these are the limitations of this ratio.

Problems of discounted cash flow method

Discounted cash flow also has some problems as it works on certain assumptions. It may provide

uncertainty in providing terminal value to the company or the investor. Sometimes discounted

cash flow method does not provide projected growth about the project so the investor and

company may face loss and difficulties (Gajek. and et. al 2017). Discounted cash flow method

also uses weighed average cost of capital which makes the process lengthy. Apart from this,

another issue which is being held in discounted cash flow is that it works on large number of

assumptions which can impact the overall return on the investment. Chances of having errors are

also high in case of discounted cash flow. Besides this, it provides high detail about the outcome

and results which will bring issues to the investor. Apart from this discounted cash flow do not

look at the competitors which are a major disadvantage of this method.

Problems of dividend valuation method

The downside of this models us that it does not provide accurate projection about the investment.

The reason behind this is that dividend valuation method do not includes buy back factor. This

method can only used by such companies who dividend growth is high and declares dividend to

its investors on real time (Nie, 2018). Another issue which is present in this model is that it have

very limited use, only blue chip companies can use this model to know the dividend details and

information. Mostly high growth companies uses this model because they have many upcoming

opportunities in the near future however investor also wants to invest in those companies who

provide better dividend. The next key limitation of this method is that sometimes it do not relate

the earning, if the earning of any company is high then it must provide high dividend to its

drink which gives good relations about the company’s share price. What price do i need a show

sometimes become difficult to use while comparing different companies of the industry. Is

different industries but different companies have different price to earnings ratio. Some

companies have zero P/E ratio and some have very high price to earnings ratio. With the help of

price to earnings ratio it can be known which stocks are cheap and which is blue chip in nature so

as per the prices of stocks investor can made their decisions. P/ E ratio provides a benchmark to

the investor about the company and its stock prices. It can be fluctuate and there is a possibility

that the stock do not fluctuate as per the P/E ratio so these are the limitations of this ratio.

Problems of discounted cash flow method

Discounted cash flow also has some problems as it works on certain assumptions. It may provide

uncertainty in providing terminal value to the company or the investor. Sometimes discounted

cash flow method does not provide projected growth about the project so the investor and

company may face loss and difficulties (Gajek. and et. al 2017). Discounted cash flow method

also uses weighed average cost of capital which makes the process lengthy. Apart from this,

another issue which is being held in discounted cash flow is that it works on large number of

assumptions which can impact the overall return on the investment. Chances of having errors are

also high in case of discounted cash flow. Besides this, it provides high detail about the outcome

and results which will bring issues to the investor. Apart from this discounted cash flow do not

look at the competitors which are a major disadvantage of this method.

Problems of dividend valuation method

The downside of this models us that it does not provide accurate projection about the investment.

The reason behind this is that dividend valuation method do not includes buy back factor. This

method can only used by such companies who dividend growth is high and declares dividend to

its investors on real time (Nie, 2018). Another issue which is present in this model is that it have

very limited use, only blue chip companies can use this model to know the dividend details and

information. Mostly high growth companies uses this model because they have many upcoming

opportunities in the near future however investor also wants to invest in those companies who

provide better dividend. The next key limitation of this method is that sometimes it do not relate

the earning, if the earning of any company is high then it must provide high dividend to its

investors but many times it happens where companies do not declare dividend even though they

earn profit.

Conclusion

From the above report it can be concluded that it provides details about financial management.

Apart from this, it gives details about IRR, NPV, Payback period etc. These reports discuss

discounted cash flow method and dividend method to provide correct details to the investor.

References

Books and Journals

Abdelhady, S., 2021. Performance and cost evaluation of solar dish power plant: sensitivity

analysis of levelized cost of electricity (LCOE) and net present value (NPV). Renewable

Energy. 168. pp.332-342.

Ahmad and et.al 2018. Molecular identification and pathological characteristics of NPV isolated

from Spodopteralitura (Fabricius) in Pakistan.

Atmadja and et.al 2018. Determinant factors influencing the accountability of village financial

management. Academy of Strategic Management Journal.17(1).pp.1-9.

Bogataj and et.al 2019. NPV approach to material requirements planning theory–a 50-year

review of these research achievements. International Journal of Production

Research. 57(15-16), pp.5137-5153.

Brigham and et.al 2021. Fundamentals of financial management. Cengage Learning.

earn profit.

Conclusion

From the above report it can be concluded that it provides details about financial management.

Apart from this, it gives details about IRR, NPV, Payback period etc. These reports discuss

discounted cash flow method and dividend method to provide correct details to the investor.

References

Books and Journals

Abdelhady, S., 2021. Performance and cost evaluation of solar dish power plant: sensitivity

analysis of levelized cost of electricity (LCOE) and net present value (NPV). Renewable

Energy. 168. pp.332-342.

Ahmad and et.al 2018. Molecular identification and pathological characteristics of NPV isolated

from Spodopteralitura (Fabricius) in Pakistan.

Atmadja and et.al 2018. Determinant factors influencing the accountability of village financial

management. Academy of Strategic Management Journal.17(1).pp.1-9.

Bogataj and et.al 2019. NPV approach to material requirements planning theory–a 50-year

review of these research achievements. International Journal of Production

Research. 57(15-16), pp.5137-5153.

Brigham and et.al 2021. Fundamentals of financial management. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.