Financial Performance Analysis: Alam PLC and Chiller Ltd

VerifiedAdded on 2021/02/20

|20

|6630

|64

Report

AI Summary

This financial management report provides a detailed analysis of various aspects of financial performance and decision-making. The report is divided into three parts, each focusing on a different company: Alam PLC, Chiller Ltd, and Crosswell. Part A focuses on Alam PLC, calculating and interpreting various financial ratios for 2018 and 2017, including profitability, liquidity, and gearing ratios. Part B examines Chiller Ltd, calculating break-even points and margins of safety, and critically analyzing the assumptions of the break-even model. Part C explores Crosswell, evaluating the benefits and limitations of different investment appraisal techniques and recommending the best techniques, along with an evaluation of main sources of finance for a capital investment project. The report provides a comprehensive overview of financial analysis and management practices, offering valuable insights into company performance and strategic financial decisions.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A - ALAM PLC...................................................................................................................1

Ratios calculations related to Alam Plc for year 2018 and 2017:...............................................1

PART B – CHILLER LTD..............................................................................................................9

Break even point and margin of safety calculations for year 2018 and 2017 related to Chiller

Ltd ..............................................................................................................................................9

Critical Analysis of the key assumptions of Break-even Model in present business scenario. 10

PART C: CROSSWELL................................................................................................................10

Benefits and limitations of various investment appraisal techniques and recommendation of

best techniques:.........................................................................................................................10

Evaluation of main sources of finance for utilisation by a company to finance its capital

investment project:....................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................17

INTRODUCTION...........................................................................................................................1

PART A - ALAM PLC...................................................................................................................1

Ratios calculations related to Alam Plc for year 2018 and 2017:...............................................1

PART B – CHILLER LTD..............................................................................................................9

Break even point and margin of safety calculations for year 2018 and 2017 related to Chiller

Ltd ..............................................................................................................................................9

Critical Analysis of the key assumptions of Break-even Model in present business scenario. 10

PART C: CROSSWELL................................................................................................................10

Benefits and limitations of various investment appraisal techniques and recommendation of

best techniques:.........................................................................................................................10

Evaluation of main sources of finance for utilisation by a company to finance its capital

investment project:....................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

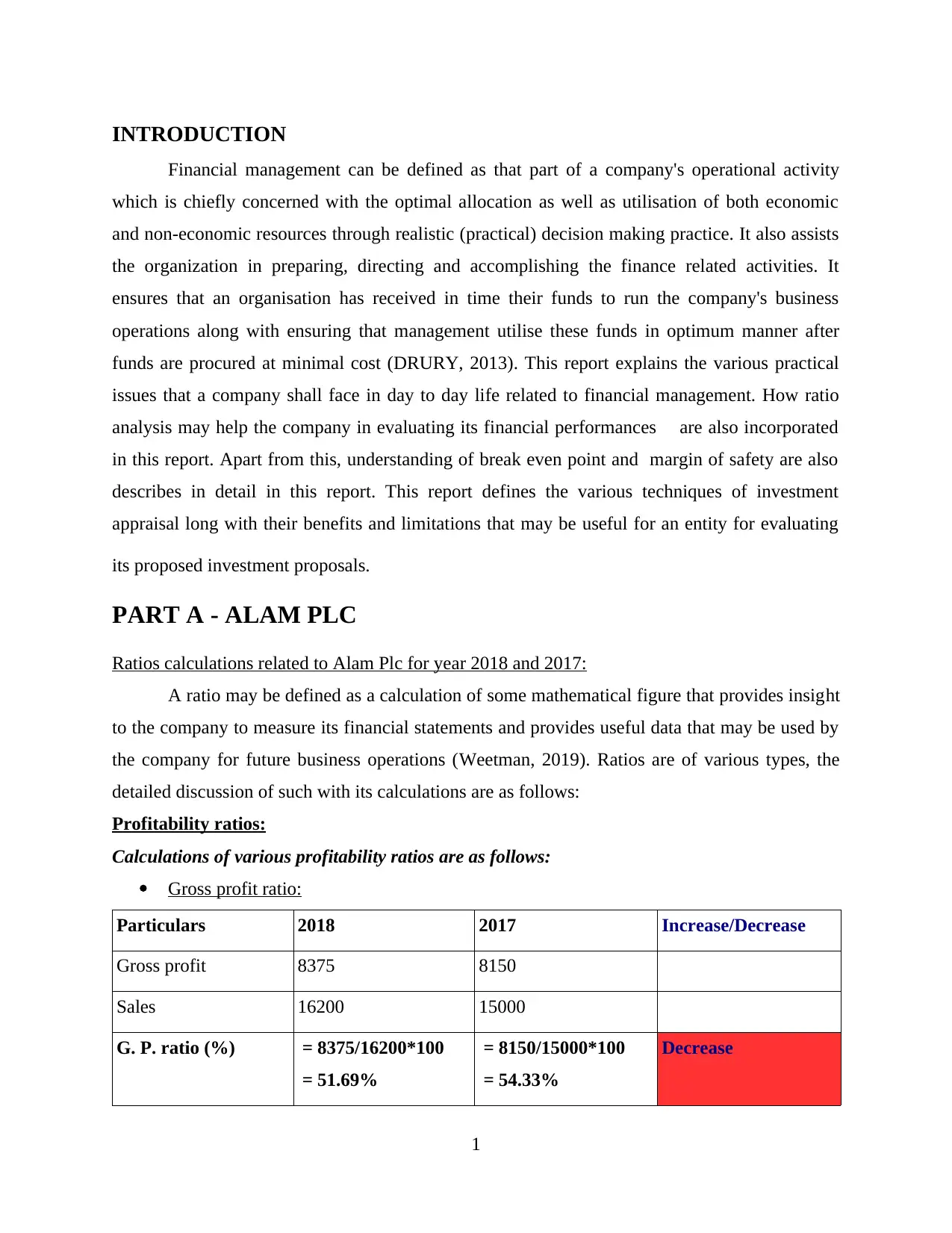

INTRODUCTION

Financial management can be defined as that part of a company's operational activity

which is chiefly concerned with the optimal allocation as well as utilisation of both economic

and non-economic resources through realistic (practical) decision making practice. It also assists

the organization in preparing, directing and accomplishing the finance related activities. It

ensures that an organisation has received in time their funds to run the company's business

operations along with ensuring that management utilise these funds in optimum manner after

funds are procured at minimal cost (DRURY, 2013). This report explains the various practical

issues that a company shall face in day to day life related to financial management. How ratio

analysis may help the company in evaluating its financial performances are also incorporated

in this report. Apart from this, understanding of break even point and margin of safety are also

describes in detail in this report. This report defines the various techniques of investment

appraisal long with their benefits and limitations that may be useful for an entity for evaluating

its proposed investment proposals.

PART A - ALAM PLC

Ratios calculations related to Alam Plc for year 2018 and 2017:

A ratio may be defined as a calculation of some mathematical figure that provides insight

to the company to measure its financial statements and provides useful data that may be used by

the company for future business operations (Weetman, 2019). Ratios are of various types, the

detailed discussion of such with its calculations are as follows:

Profitability ratios:

Calculations of various profitability ratios are as follows:

Gross profit ratio:

Particulars 2018 2017 Increase/Decrease

Gross profit 8375 8150

Sales 16200 15000

G. P. ratio (%) = 8375/16200*100

= 51.69%

= 8150/15000*100

= 54.33%

Decrease

1

Financial management can be defined as that part of a company's operational activity

which is chiefly concerned with the optimal allocation as well as utilisation of both economic

and non-economic resources through realistic (practical) decision making practice. It also assists

the organization in preparing, directing and accomplishing the finance related activities. It

ensures that an organisation has received in time their funds to run the company's business

operations along with ensuring that management utilise these funds in optimum manner after

funds are procured at minimal cost (DRURY, 2013). This report explains the various practical

issues that a company shall face in day to day life related to financial management. How ratio

analysis may help the company in evaluating its financial performances are also incorporated

in this report. Apart from this, understanding of break even point and margin of safety are also

describes in detail in this report. This report defines the various techniques of investment

appraisal long with their benefits and limitations that may be useful for an entity for evaluating

its proposed investment proposals.

PART A - ALAM PLC

Ratios calculations related to Alam Plc for year 2018 and 2017:

A ratio may be defined as a calculation of some mathematical figure that provides insight

to the company to measure its financial statements and provides useful data that may be used by

the company for future business operations (Weetman, 2019). Ratios are of various types, the

detailed discussion of such with its calculations are as follows:

Profitability ratios:

Calculations of various profitability ratios are as follows:

Gross profit ratio:

Particulars 2018 2017 Increase/Decrease

Gross profit 8375 8150

Sales 16200 15000

G. P. ratio (%) = 8375/16200*100

= 51.69%

= 8150/15000*100

= 54.33%

Decrease

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Formula: G.P. Ratio = G.P. / Sales*100

Interpretation:

From the above calculations it may be observed that gross profit ratio of Alam Plc has

decreased in current year (51.7 %) as compared to last year which is 54.33 %. Although, there is

not much difference but company shall look into this matter to find the actual reason ( Taylor,

2013). Some of the reasons of such reduced ratio is that profit is not increased as per sales

proportion from last year. So it can be interpreted to board of Alam plc that their gross profit is

not increasing as they should focus on increasing it.

Net profit ratio:

Particulars 2018 2017 Increase/Decrease

Net profit before tax

and interest

1510 2865

Sales 16200 15000

N. P. ratio (%) = 1510/16200*100

= 9.32%

= 2865/15000*100

= 19.10%

Decrease

Formula: N.P. Ratio = N.P. Before tax and interest / Sales*100

Interpretation: From the above calculations related to net profit, it may be evident that such

company has not performing well and not able to control its operating cost. Due to this, its

current year net profit ratio is 4.04% as compared to its last year N.P. Ratio which is 15.5%. The

reason of this is that its net profit decreases as compared to last year. Same as the above gross

profit ratio, the net profit ratio is also decreasing so it be stated to the board of Alam plc that their

net profits are not in ideal condition.

Return on capital employed ratio: Net profit before tax and interest / share capital+ long

term loan x 100

Particulars 2018 2017 Increase/Decrease

Net profit before tax

and interest

1510 2865

share capital+ long 7215+4450 = 11665 5030+4075 = 9105

2

Interpretation:

From the above calculations it may be observed that gross profit ratio of Alam Plc has

decreased in current year (51.7 %) as compared to last year which is 54.33 %. Although, there is

not much difference but company shall look into this matter to find the actual reason ( Taylor,

2013). Some of the reasons of such reduced ratio is that profit is not increased as per sales

proportion from last year. So it can be interpreted to board of Alam plc that their gross profit is

not increasing as they should focus on increasing it.

Net profit ratio:

Particulars 2018 2017 Increase/Decrease

Net profit before tax

and interest

1510 2865

Sales 16200 15000

N. P. ratio (%) = 1510/16200*100

= 9.32%

= 2865/15000*100

= 19.10%

Decrease

Formula: N.P. Ratio = N.P. Before tax and interest / Sales*100

Interpretation: From the above calculations related to net profit, it may be evident that such

company has not performing well and not able to control its operating cost. Due to this, its

current year net profit ratio is 4.04% as compared to its last year N.P. Ratio which is 15.5%. The

reason of this is that its net profit decreases as compared to last year. Same as the above gross

profit ratio, the net profit ratio is also decreasing so it be stated to the board of Alam plc that their

net profits are not in ideal condition.

Return on capital employed ratio: Net profit before tax and interest / share capital+ long

term loan x 100

Particulars 2018 2017 Increase/Decrease

Net profit before tax

and interest

1510 2865

share capital+ long 7215+4450 = 11665 5030+4075 = 9105

2

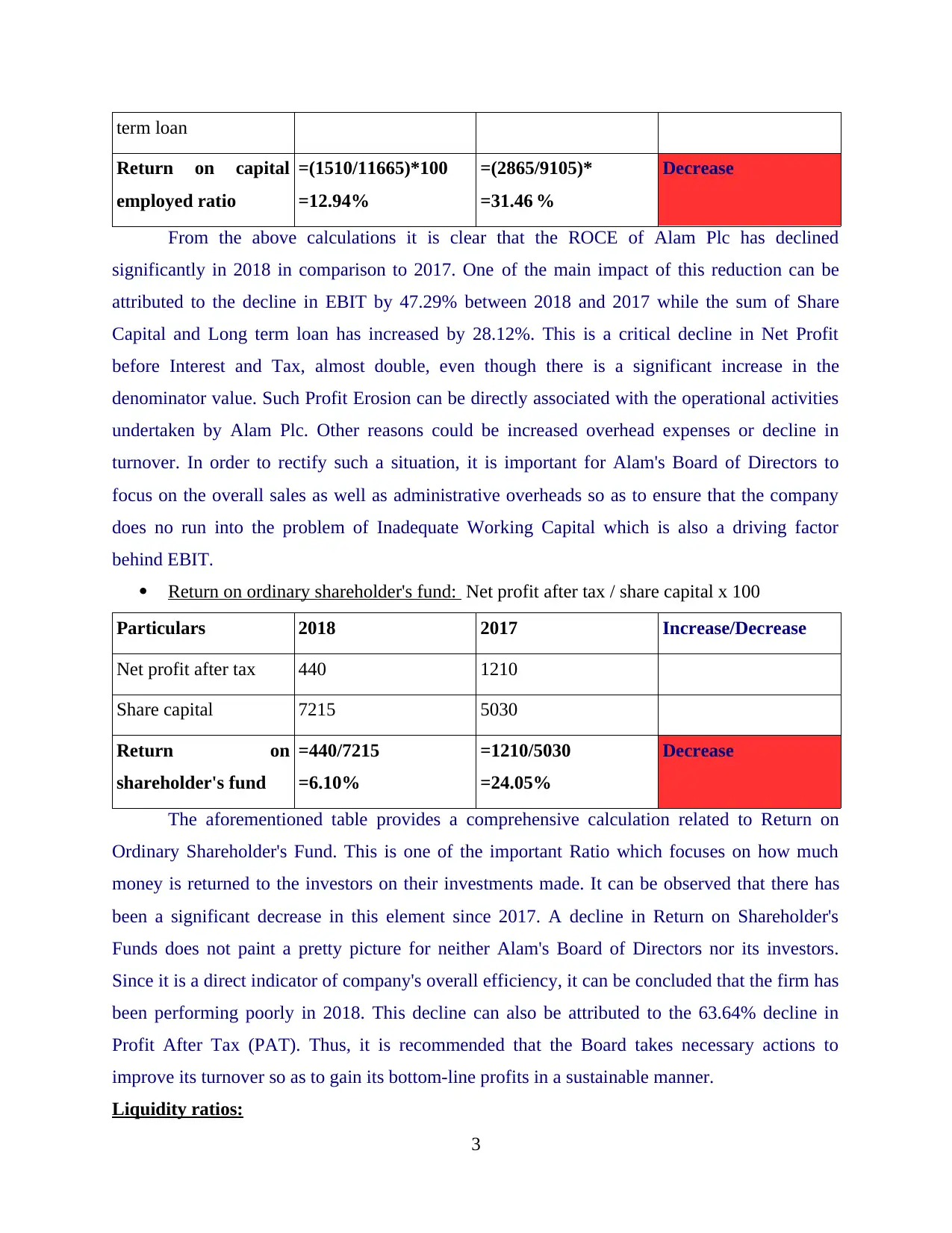

term loan

Return on capital

employed ratio

=(1510/11665)*100

=12.94%

=(2865/9105)*

=31.46 %

Decrease

From the above calculations it is clear that the ROCE of Alam Plc has declined

significantly in 2018 in comparison to 2017. One of the main impact of this reduction can be

attributed to the decline in EBIT by 47.29% between 2018 and 2017 while the sum of Share

Capital and Long term loan has increased by 28.12%. This is a critical decline in Net Profit

before Interest and Tax, almost double, even though there is a significant increase in the

denominator value. Such Profit Erosion can be directly associated with the operational activities

undertaken by Alam Plc. Other reasons could be increased overhead expenses or decline in

turnover. In order to rectify such a situation, it is important for Alam's Board of Directors to

focus on the overall sales as well as administrative overheads so as to ensure that the company

does no run into the problem of Inadequate Working Capital which is also a driving factor

behind EBIT.

Return on ordinary shareholder's fund: Net profit after tax / share capital x 100

Particulars 2018 2017 Increase/Decrease

Net profit after tax 440 1210

Share capital 7215 5030

Return on

shareholder's fund

=440/7215

=6.10%

=1210/5030

=24.05%

Decrease

The aforementioned table provides a comprehensive calculation related to Return on

Ordinary Shareholder's Fund. This is one of the important Ratio which focuses on how much

money is returned to the investors on their investments made. It can be observed that there has

been a significant decrease in this element since 2017. A decline in Return on Shareholder's

Funds does not paint a pretty picture for neither Alam's Board of Directors nor its investors.

Since it is a direct indicator of company's overall efficiency, it can be concluded that the firm has

been performing poorly in 2018. This decline can also be attributed to the 63.64% decline in

Profit After Tax (PAT). Thus, it is recommended that the Board takes necessary actions to

improve its turnover so as to gain its bottom-line profits in a sustainable manner.

Liquidity ratios:

3

Return on capital

employed ratio

=(1510/11665)*100

=12.94%

=(2865/9105)*

=31.46 %

Decrease

From the above calculations it is clear that the ROCE of Alam Plc has declined

significantly in 2018 in comparison to 2017. One of the main impact of this reduction can be

attributed to the decline in EBIT by 47.29% between 2018 and 2017 while the sum of Share

Capital and Long term loan has increased by 28.12%. This is a critical decline in Net Profit

before Interest and Tax, almost double, even though there is a significant increase in the

denominator value. Such Profit Erosion can be directly associated with the operational activities

undertaken by Alam Plc. Other reasons could be increased overhead expenses or decline in

turnover. In order to rectify such a situation, it is important for Alam's Board of Directors to

focus on the overall sales as well as administrative overheads so as to ensure that the company

does no run into the problem of Inadequate Working Capital which is also a driving factor

behind EBIT.

Return on ordinary shareholder's fund: Net profit after tax / share capital x 100

Particulars 2018 2017 Increase/Decrease

Net profit after tax 440 1210

Share capital 7215 5030

Return on

shareholder's fund

=440/7215

=6.10%

=1210/5030

=24.05%

Decrease

The aforementioned table provides a comprehensive calculation related to Return on

Ordinary Shareholder's Fund. This is one of the important Ratio which focuses on how much

money is returned to the investors on their investments made. It can be observed that there has

been a significant decrease in this element since 2017. A decline in Return on Shareholder's

Funds does not paint a pretty picture for neither Alam's Board of Directors nor its investors.

Since it is a direct indicator of company's overall efficiency, it can be concluded that the firm has

been performing poorly in 2018. This decline can also be attributed to the 63.64% decline in

Profit After Tax (PAT). Thus, it is recommended that the Board takes necessary actions to

improve its turnover so as to gain its bottom-line profits in a sustainable manner.

Liquidity ratios:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current ratio:

Particulars 2018 2017 Increase/Decrease

Current assets 4675 3755

Current liabilities 2425 2255

Current ratio = 4675/2425

= 1.92 times

= 3755/2255

= 1.66 times

Increase

Formula: Current ratio = Current assets / Current liabilities

Interpretation:

Current ratio of year 2018 is 1.93 whereas such ratio in year 2017 is 1.67, this shows that

Alam Plc has taken positive steps in increasing its current ratio, this has happened because the

company has utilises its current assets in efficient manner to pay off its current liabilities.

Reasons for such increased ratio is that current assets increases as compared to last year and its

current year liabilities is not increased in that proportion. This can be informed to the board of

Alam plc is that their current ratio is increasing as compared to previous year though it is not in

an ideal condition that is of 2:1.

Quick ratio:

Particulars 2018 2017 Increase/Decrease

Quick assets 3750 2955

Current liabilities 2425 2255

Quick ratio = 4675-925/ 2425

=1.54 times

= 3755 – 800/2255

= 1.31 times

Increase

Formula: Quick Ratio = Quick assets / Current liabilities

Interpretation:

In year 2018 quick ratio is 1.55 and in year 2017 it is 1.31, this means that company has

performing well in utilising its quick assets to pay its short term liabilities and such company has

in good condition. But Alam Plc is required to work effectively and efficiently in order to

enhance the company's quick assets more as compared to its current liabilities, so that,

company's liquidity position may be enhanced. The standard quick ratio is equal to 1.5: 1, this

means that company has to performed well in current year, due to this, it quick ratio enhanced

4

Particulars 2018 2017 Increase/Decrease

Current assets 4675 3755

Current liabilities 2425 2255

Current ratio = 4675/2425

= 1.92 times

= 3755/2255

= 1.66 times

Increase

Formula: Current ratio = Current assets / Current liabilities

Interpretation:

Current ratio of year 2018 is 1.93 whereas such ratio in year 2017 is 1.67, this shows that

Alam Plc has taken positive steps in increasing its current ratio, this has happened because the

company has utilises its current assets in efficient manner to pay off its current liabilities.

Reasons for such increased ratio is that current assets increases as compared to last year and its

current year liabilities is not increased in that proportion. This can be informed to the board of

Alam plc is that their current ratio is increasing as compared to previous year though it is not in

an ideal condition that is of 2:1.

Quick ratio:

Particulars 2018 2017 Increase/Decrease

Quick assets 3750 2955

Current liabilities 2425 2255

Quick ratio = 4675-925/ 2425

=1.54 times

= 3755 – 800/2255

= 1.31 times

Increase

Formula: Quick Ratio = Quick assets / Current liabilities

Interpretation:

In year 2018 quick ratio is 1.55 and in year 2017 it is 1.31, this means that company has

performing well in utilising its quick assets to pay its short term liabilities and such company has

in good condition. But Alam Plc is required to work effectively and efficiently in order to

enhance the company's quick assets more as compared to its current liabilities, so that,

company's liquidity position may be enhanced. The standard quick ratio is equal to 1.5: 1, this

means that company has to performed well in current year, due to this, it quick ratio enhanced

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and higher than standard ratio. The board of Alam plc are being informed that company's quick

ratio is in better condition because it is increasing as well as in ideal condition in year 2018.

Working capital cycle: Inventory turnover+ debtors turnover- creditors turnover

Particulars 2018 2017 Increase/Decrease

Inventory Turnover 40.23 38.63

Debtors Turnover 84.49 60.71

Creditors Turnover 98.71 107.93

Working Capital

Cycle

=40.23+84.49-98.71

=26 days

=38.63+60.71- 107.93

=-9 days

Increase

From the above table, it is evident that there has been a considerable increase in the

number of days the working capital cycle takes to complete. In 2017, this value was in negative,

however, in 2018, this has increased to 26 days. A negative working capital cycle which

indicates that the current liabilities exceed the current assets within an organisation. Thus, until

2017, Alam was able to generate cash so quickly that it was able to to sell its products even

before paying off the supplier. However, this changed in 2018, where the cycle ventured into a

positive value. This indicates that, to some extent, Alam Plc has been able to do this by reducing

its creditors turnover while increasing its inventory as well as debtors turnover figures. Thus, it is

crucial for Alam to ensure its maintenance and prevention of any delays in the Working Capital

Cycle due to increase in its numbers.

Gearing ratios:

Debt equity ratio:

Particulars 2018 2017 Increase/Decrease

Debt 4450 4075

Equity 11665 9105

Debt equity ratio =

(4450/7215+4450)*10

0

=

(4075/5030+4075)*10

0

Decrease

5

ratio is in better condition because it is increasing as well as in ideal condition in year 2018.

Working capital cycle: Inventory turnover+ debtors turnover- creditors turnover

Particulars 2018 2017 Increase/Decrease

Inventory Turnover 40.23 38.63

Debtors Turnover 84.49 60.71

Creditors Turnover 98.71 107.93

Working Capital

Cycle

=40.23+84.49-98.71

=26 days

=38.63+60.71- 107.93

=-9 days

Increase

From the above table, it is evident that there has been a considerable increase in the

number of days the working capital cycle takes to complete. In 2017, this value was in negative,

however, in 2018, this has increased to 26 days. A negative working capital cycle which

indicates that the current liabilities exceed the current assets within an organisation. Thus, until

2017, Alam was able to generate cash so quickly that it was able to to sell its products even

before paying off the supplier. However, this changed in 2018, where the cycle ventured into a

positive value. This indicates that, to some extent, Alam Plc has been able to do this by reducing

its creditors turnover while increasing its inventory as well as debtors turnover figures. Thus, it is

crucial for Alam to ensure its maintenance and prevention of any delays in the Working Capital

Cycle due to increase in its numbers.

Gearing ratios:

Debt equity ratio:

Particulars 2018 2017 Increase/Decrease

Debt 4450 4075

Equity 11665 9105

Debt equity ratio =

(4450/7215+4450)*10

0

=

(4075/5030+4075)*10

0

Decrease

5

=38.14% = 44.75%

Formula: Debt equity ratio = Debt / share capital long term loan

Interpretation:

From the above calculations, it is clearly evident that debt portion of Alam as compared

to its equity portion are less in year 2018 (0.62) as compared to year 2017 (0.81). This shows that

company has less finance risk in current year as compared to year 2017. As a result, the decline

in debt-equity ratio indicates that the company has resorted to equity financing in 2018 which is

quite expensive in comparison to raising funds through debt. It has happened due to issue of

additional share capital in 2018 as compared to 2017. Although, there is an increase in its debt in

2018, such increase is not enough to cover the amount of additional share capital along with its

retained earning earnings.

Interest coverage ratio:

Particulars 2018 2017 Increase/Decrease

EBIT 1510 2865

Interest 850 540

Interest coverage

ratio

= 1510/850

= 1.77 times

= 2865/540

= 5.30 times

Decrease

Formula: Interest coverage ratio = EBIT / Interest

Interpretation:

After seen the above calculation, it may be said that company's interest coverage ratio in

year 2018 is 1.78 and in year 2017 it is 4.75. This clearly shows that Alam Plc has not

performing well as it earnings before interest and tax are less in current year as compared to its

last year and also its finance cost in year 2018 is more as compared to last year. Due to which, its

Interest coverage ratio is less. Hence, this can be interpreted to company's board that they have

sufficient fund to pay its interest cost but if in case of any negative circumstances, such company

may not be able to pay its finance cost.

Efficiency / Assets utilisation ratios:

Stock turnover days: Average inventories / cost of sales x 365 days

Particulars 2018 2017 Increase/Decrease

6

Formula: Debt equity ratio = Debt / share capital long term loan

Interpretation:

From the above calculations, it is clearly evident that debt portion of Alam as compared

to its equity portion are less in year 2018 (0.62) as compared to year 2017 (0.81). This shows that

company has less finance risk in current year as compared to year 2017. As a result, the decline

in debt-equity ratio indicates that the company has resorted to equity financing in 2018 which is

quite expensive in comparison to raising funds through debt. It has happened due to issue of

additional share capital in 2018 as compared to 2017. Although, there is an increase in its debt in

2018, such increase is not enough to cover the amount of additional share capital along with its

retained earning earnings.

Interest coverage ratio:

Particulars 2018 2017 Increase/Decrease

EBIT 1510 2865

Interest 850 540

Interest coverage

ratio

= 1510/850

= 1.77 times

= 2865/540

= 5.30 times

Decrease

Formula: Interest coverage ratio = EBIT / Interest

Interpretation:

After seen the above calculation, it may be said that company's interest coverage ratio in

year 2018 is 1.78 and in year 2017 it is 4.75. This clearly shows that Alam Plc has not

performing well as it earnings before interest and tax are less in current year as compared to its

last year and also its finance cost in year 2018 is more as compared to last year. Due to which, its

Interest coverage ratio is less. Hence, this can be interpreted to company's board that they have

sufficient fund to pay its interest cost but if in case of any negative circumstances, such company

may not be able to pay its finance cost.

Efficiency / Assets utilisation ratios:

Stock turnover days: Average inventories / cost of sales x 365 days

Particulars 2018 2017 Increase/Decrease

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average inventory (800+925) / 2 = 862.5 (650+800) / 2 = 725

Cost of sales 7825 6850

Stock turn over days =(862.5/7825)*365

=41 days

=(725/6850)*365

=39 days

Increase

Interpretation:

From the above calculations, it may be concluded that Alam Plc has been performing

well as far as its business operations are concerned. This is indicated through its stock turnover

ratio which is 39 days in year 2017 and 41 days in 2018. Thus, it can be interpreted that above

company should focus on decreasing their turn over days in year 2018. Thus, with the rise in this

ratio it can be concluded that the Alam has been having a good amount of sales in 2018 in

comparison to 2017. Thus, indicating that the efficiency of the overall activities of Alam has

improved considerably. This can be improved more by ensuring that the per dollar increase in the

bottom-line profits for each sale made by Alam.

Account receivable collection period: Trade receivables / credit sales revenue x 365 days

Particulars 2018 2017 Increase/Decrease

Trade receivables 3750 2495

Credit sales revenue 16200 15000

Account receivables

collection period

=(3750/16200)*365

=85 days

=(2495/15000)*365

=61 days

Increase

Interpretation: On the basis of above calculations this can be interpreted that Alam Plc is taking

61 days in making collection in year 2017 that increased in year 2018 and became of 85 days.

Through this increment, it can be said that Alam's customers have been taking delayed payments

in to pay back their dues to the company. This is not a good sign for Alam as it results in a longer

lock-up period of cash flows for the business. Thus, it is recommended that Alam must utilise the

benefits of a Age Receivable Schedule which will enable to determine who its unpaid customers

effectively.

7

Cost of sales 7825 6850

Stock turn over days =(862.5/7825)*365

=41 days

=(725/6850)*365

=39 days

Increase

Interpretation:

From the above calculations, it may be concluded that Alam Plc has been performing

well as far as its business operations are concerned. This is indicated through its stock turnover

ratio which is 39 days in year 2017 and 41 days in 2018. Thus, it can be interpreted that above

company should focus on decreasing their turn over days in year 2018. Thus, with the rise in this

ratio it can be concluded that the Alam has been having a good amount of sales in 2018 in

comparison to 2017. Thus, indicating that the efficiency of the overall activities of Alam has

improved considerably. This can be improved more by ensuring that the per dollar increase in the

bottom-line profits for each sale made by Alam.

Account receivable collection period: Trade receivables / credit sales revenue x 365 days

Particulars 2018 2017 Increase/Decrease

Trade receivables 3750 2495

Credit sales revenue 16200 15000

Account receivables

collection period

=(3750/16200)*365

=85 days

=(2495/15000)*365

=61 days

Increase

Interpretation: On the basis of above calculations this can be interpreted that Alam Plc is taking

61 days in making collection in year 2017 that increased in year 2018 and became of 85 days.

Through this increment, it can be said that Alam's customers have been taking delayed payments

in to pay back their dues to the company. This is not a good sign for Alam as it results in a longer

lock-up period of cash flows for the business. Thus, it is recommended that Alam must utilise the

benefits of a Age Receivable Schedule which will enable to determine who its unpaid customers

effectively.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Account payable payment period: Account payable / credit purchase x 365 days

Particulars 2018 2017 Increase/Decrease

Account payable 2150 2070

Credit purchase 7950 7000

Account payable

payment period

=(2150/7950)*365

=99 days

=(2070/7000)*365

=108 days

Decrease

Interpretation:

On the basis of above project report this can be analysed that Alam Plc's efficiency

towards making payment has increased in year 2018. This is due to the fact that the overall

Account Payable Payment Period has decreased by 8.33% in 2018 as compared to 2017. Thus,

they are able to effectively pay off their creditors which is crucial for the business and helps it to

enhance its overall credibility as well as strengthen relationship with its creditors in a critical

manner.

Investors:

Dividend payout ratio: Dividend amount for year / earning of the year available for

dividend x 100

Particulars 2018 2017 Increase/Decrease

Dividend amount 190 170

Earning of year for

dividend

440 1210

Dividend payout

ratio

=(190/440)*100

=43.18 %

=(170/1210)*100

=14.04%

Increase

Interpretation: As per above table of dividend payout ratio, this can be analysed that Dividend

Payout ratio for Alam Plc is 14.04% in year 2017 which increased in 2018 and became 43.18%.

Hence, this can be interpreted that their ability for making payment to investors has been

increased significantly in year 2018. Thus, indicating that Alam has been providing cash benefits

to its owners. However, it is recommended to keep such payments in check as excessive

8

Particulars 2018 2017 Increase/Decrease

Account payable 2150 2070

Credit purchase 7950 7000

Account payable

payment period

=(2150/7950)*365

=99 days

=(2070/7000)*365

=108 days

Decrease

Interpretation:

On the basis of above project report this can be analysed that Alam Plc's efficiency

towards making payment has increased in year 2018. This is due to the fact that the overall

Account Payable Payment Period has decreased by 8.33% in 2018 as compared to 2017. Thus,

they are able to effectively pay off their creditors which is crucial for the business and helps it to

enhance its overall credibility as well as strengthen relationship with its creditors in a critical

manner.

Investors:

Dividend payout ratio: Dividend amount for year / earning of the year available for

dividend x 100

Particulars 2018 2017 Increase/Decrease

Dividend amount 190 170

Earning of year for

dividend

440 1210

Dividend payout

ratio

=(190/440)*100

=43.18 %

=(170/1210)*100

=14.04%

Increase

Interpretation: As per above table of dividend payout ratio, this can be analysed that Dividend

Payout ratio for Alam Plc is 14.04% in year 2017 which increased in 2018 and became 43.18%.

Hence, this can be interpreted that their ability for making payment to investors has been

increased significantly in year 2018. Thus, indicating that Alam has been providing cash benefits

to its owners. However, it is recommended to keep such payments in check as excessive

8

Dividend Payouts may result in deficiency of profits to plough back in the business which is

crucial for undertaking future opportunities and projects.

Earnings per share: Earnings available to shareholders / number of share to issue x 100

Particulars 2018 2017 Increase/Decrease

Earnings available to

shareholders

440 1210

Number of share to

issue

6165 4230

Earning per share =(440/6165)*100

=7.13 p

=(1210/4230)*100

=28.60 p

Decrease

Interpretation: On the basis of above table this can be analysed that Alam Plc's EPS is of 28.60p

in 2017 which has decreased in 2018 to 7.13p. Thus, indicating that company's profitability has

decreased significantly. This would result in decline in investor confidence within the company.

Therefore, it is important for Alam's management to ensure that the company is cost-effective

and is able to pursue a higher revenue growth in the foreseeable future.

PART B – CHILLER LTD

Break even point and margin of safety calculations for year 2018 and 2017 related to Chiller Ltd

BEP calculations:

Particulars 2018 2019

Variable cost per unit:

Direct material 200 200

Direct labour cost 30 30

Variable manufacturing cost 30 30

9

crucial for undertaking future opportunities and projects.

Earnings per share: Earnings available to shareholders / number of share to issue x 100

Particulars 2018 2017 Increase/Decrease

Earnings available to

shareholders

440 1210

Number of share to

issue

6165 4230

Earning per share =(440/6165)*100

=7.13 p

=(1210/4230)*100

=28.60 p

Decrease

Interpretation: On the basis of above table this can be analysed that Alam Plc's EPS is of 28.60p

in 2017 which has decreased in 2018 to 7.13p. Thus, indicating that company's profitability has

decreased significantly. This would result in decline in investor confidence within the company.

Therefore, it is important for Alam's management to ensure that the company is cost-effective

and is able to pursue a higher revenue growth in the foreseeable future.

PART B – CHILLER LTD

Break even point and margin of safety calculations for year 2018 and 2017 related to Chiller Ltd

BEP calculations:

Particulars 2018 2019

Variable cost per unit:

Direct material 200 200

Direct labour cost 30 30

Variable manufacturing cost 30 30

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.