Financial Management Report: Sanderson, Holycross, and Winners

VerifiedAdded on 2023/02/02

|17

|4762

|50

Report

AI Summary

This report provides a comprehensive analysis of key financial management concepts. It begins by calculating the corporate tax liability for Sanderson, Inc., detailing the tax rates and surtaxes applicable. The report then delves into the importance of taxation and its socio-economic purposes, highlighting its role in revenue generation and public welfare. Next, it evaluates investment feasibility by assessing risk and returns for two common stocks, Stock A and Stock B, using weighted standard deviation. Financial forecasting is then applied to Holycross Enterprises, calculating total financing needs and discretionary financing needed (DFN). The report further examines financial ratios, their calculations, advantages, and limitations. It concludes by recommending a project using investment appraisal techniques and discussing the features of capital budgeting decisions, as well as analyzing the financial statements of Winners Industry and the role of its finance department.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................1

a. Computing Tax Liability of Sanderson, Inc............................................................................1

b. Evidencing the Importance of Taxation and its socio-economic purposes.............................2

QUESTION 2...................................................................................................................................3

a. Evaluating feasibility of investment based on risk and returns...............................................3

b. Concept of Risk and Diversification.......................................................................................5

QUESTION 3...................................................................................................................................5

a. Estimating Holycross' Total Financing and Net Funding Requirements................................5

b. Forecasting to ascertain discretionary financing needed (DFN).............................................6

QUESTION 4...................................................................................................................................7

a. Calculation of Ratios...............................................................................................................7

b. Advantages and limitations of Ratio Analysis........................................................................9

QUESTION 5.................................................................................................................................10

a. Recommending a Project using Investment Appraisal Techniques......................................10

b. Distinctive Features of Capital Budgeting Decisions...........................................................11

QUESTION 6.................................................................................................................................11

a. Financial Statements of Winners Industry............................................................................11

b. Role of Finance Department ................................................................................................13

REFERENCES..............................................................................................................................14

QUESTION 1...................................................................................................................................1

a. Computing Tax Liability of Sanderson, Inc............................................................................1

b. Evidencing the Importance of Taxation and its socio-economic purposes.............................2

QUESTION 2...................................................................................................................................3

a. Evaluating feasibility of investment based on risk and returns...............................................3

b. Concept of Risk and Diversification.......................................................................................5

QUESTION 3...................................................................................................................................5

a. Estimating Holycross' Total Financing and Net Funding Requirements................................5

b. Forecasting to ascertain discretionary financing needed (DFN).............................................6

QUESTION 4...................................................................................................................................7

a. Calculation of Ratios...............................................................................................................7

b. Advantages and limitations of Ratio Analysis........................................................................9

QUESTION 5.................................................................................................................................10

a. Recommending a Project using Investment Appraisal Techniques......................................10

b. Distinctive Features of Capital Budgeting Decisions...........................................................11

QUESTION 6.................................................................................................................................11

a. Financial Statements of Winners Industry............................................................................11

b. Role of Finance Department ................................................................................................13

REFERENCES..............................................................................................................................14

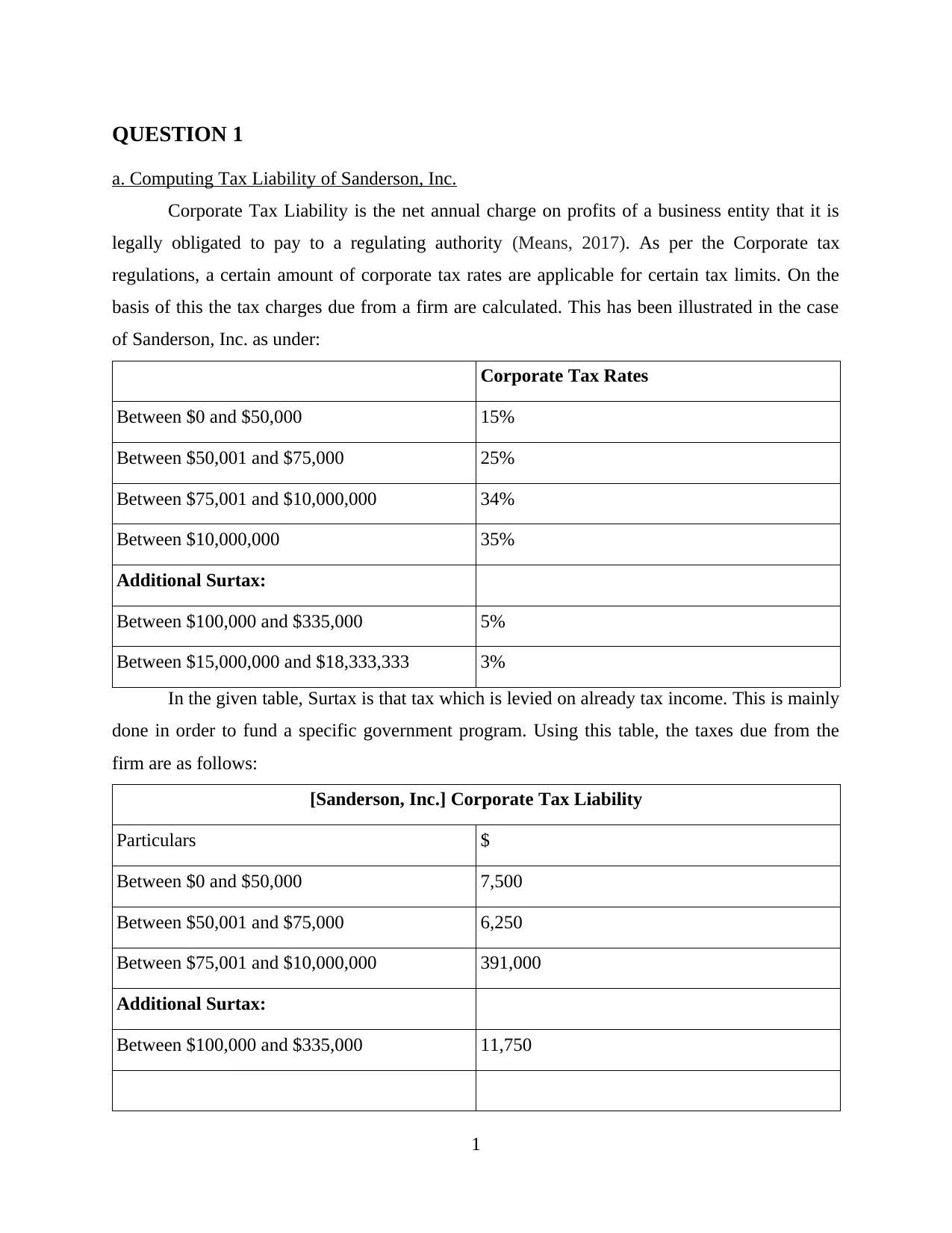

QUESTION 1

a. Computing Tax Liability of Sanderson, Inc.

Corporate Tax Liability is the net annual charge on profits of a business entity that it is

legally obligated to pay to a regulating authority (Means, 2017). As per the Corporate tax

regulations, a certain amount of corporate tax rates are applicable for certain tax limits. On the

basis of this the tax charges due from a firm are calculated. This has been illustrated in the case

of Sanderson, Inc. as under:

Corporate Tax Rates

Between $0 and $50,000 15%

Between $50,001 and $75,000 25%

Between $75,001 and $10,000,000 34%

Between $10,000,000 35%

Additional Surtax:

Between $100,000 and $335,000 5%

Between $15,000,000 and $18,333,333 3%

In the given table, Surtax is that tax which is levied on already tax income. This is mainly

done in order to fund a specific government program. Using this table, the taxes due from the

firm are as follows:

[Sanderson, Inc.] Corporate Tax Liability

Particulars $

Between $0 and $50,000 7,500

Between $50,001 and $75,000 6,250

Between $75,001 and $10,000,000 391,000

Additional Surtax:

Between $100,000 and $335,000 11,750

1

a. Computing Tax Liability of Sanderson, Inc.

Corporate Tax Liability is the net annual charge on profits of a business entity that it is

legally obligated to pay to a regulating authority (Means, 2017). As per the Corporate tax

regulations, a certain amount of corporate tax rates are applicable for certain tax limits. On the

basis of this the tax charges due from a firm are calculated. This has been illustrated in the case

of Sanderson, Inc. as under:

Corporate Tax Rates

Between $0 and $50,000 15%

Between $50,001 and $75,000 25%

Between $75,001 and $10,000,000 34%

Between $10,000,000 35%

Additional Surtax:

Between $100,000 and $335,000 5%

Between $15,000,000 and $18,333,333 3%

In the given table, Surtax is that tax which is levied on already tax income. This is mainly

done in order to fund a specific government program. Using this table, the taxes due from the

firm are as follows:

[Sanderson, Inc.] Corporate Tax Liability

Particulars $

Between $0 and $50,000 7,500

Between $50,001 and $75,000 6,250

Between $75,001 and $10,000,000 391,000

Additional Surtax:

Between $100,000 and $335,000 11,750

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working Notes:

Computation of tax liability

$50000 X 0.15 = 7500

$25000 X 0.25 = 6250

$1150000 X 0.34 = 391000

SUR TAX:

$235000 X 0.05 = 11750

Total Taxes Due = $416500

As per the calculations and working notes provided above, the taxes have been calculated

on corporation's tax liability of $1,225,000. This have been further bifurcated on the basis of tax

limit differences. Hence, firstly a 15% tax rate has been levied on the amount up to $50,000

(=$50,00-$0). The remaining amount is $1,175,000 (=$1,225,000−$50,000). Out of this 25% tax

rate has been levied up to $25,000 (=$75,000-$50,001). It is worthy to note that the firm's annual

taxable income is also eligible for a additional surtax worth $11,750 (=$235,000*0.05).

b. Evidencing the Importance of Taxation and its socio-economic purposes

Taxation is an integral part of any economy that is charged by governments in return of

the public expenditure incurred by them for the welfare of people belonging to that state, region

or economy. Hence, taxes are of paramount importance. The aim of taxation is mainly twofold

viz. Generation of Revenue and Welfare of Public Interest (Schmalbeck, Zelenak and Lawsky,

2015). These are important in order to further development in the economy through improvement

in infrastructures such as buildings, roads, bridges and many more services. This results in not

only infrastructural development but also in socio-economic development of the nation as a

whole. One can say that different tax levy serve different purposes. Thus, they can be classified

in two main categorizes viz. Direct Taxes and Indirect Taxes. It is important to note that these

revenues are unrequited in nature. Originally, federal government's sole purpose was to

generate financing to meet government expenditures. However, as the consumer is assumed to be

knowledgable about the quality and safety and the environment is highly dynamic, this purpose

cannot solely define the government's intentions. Just like a business entity, the government

needs to be socially responsible so as to gain trust and act transparently while concerning

themselves with consumer affairs. For instance, federal government tends to contribute 8 percent

to the elementary as well as secondary education of the children (Federal Government and

2

Computation of tax liability

$50000 X 0.15 = 7500

$25000 X 0.25 = 6250

$1150000 X 0.34 = 391000

SUR TAX:

$235000 X 0.05 = 11750

Total Taxes Due = $416500

As per the calculations and working notes provided above, the taxes have been calculated

on corporation's tax liability of $1,225,000. This have been further bifurcated on the basis of tax

limit differences. Hence, firstly a 15% tax rate has been levied on the amount up to $50,000

(=$50,00-$0). The remaining amount is $1,175,000 (=$1,225,000−$50,000). Out of this 25% tax

rate has been levied up to $25,000 (=$75,000-$50,001). It is worthy to note that the firm's annual

taxable income is also eligible for a additional surtax worth $11,750 (=$235,000*0.05).

b. Evidencing the Importance of Taxation and its socio-economic purposes

Taxation is an integral part of any economy that is charged by governments in return of

the public expenditure incurred by them for the welfare of people belonging to that state, region

or economy. Hence, taxes are of paramount importance. The aim of taxation is mainly twofold

viz. Generation of Revenue and Welfare of Public Interest (Schmalbeck, Zelenak and Lawsky,

2015). These are important in order to further development in the economy through improvement

in infrastructures such as buildings, roads, bridges and many more services. This results in not

only infrastructural development but also in socio-economic development of the nation as a

whole. One can say that different tax levy serve different purposes. Thus, they can be classified

in two main categorizes viz. Direct Taxes and Indirect Taxes. It is important to note that these

revenues are unrequited in nature. Originally, federal government's sole purpose was to

generate financing to meet government expenditures. However, as the consumer is assumed to be

knowledgable about the quality and safety and the environment is highly dynamic, this purpose

cannot solely define the government's intentions. Just like a business entity, the government

needs to be socially responsible so as to gain trust and act transparently while concerning

themselves with consumer affairs. For instance, federal government tends to contribute 8 percent

to the elementary as well as secondary education of the children (Federal Government and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Education, 2019). As the government is responsible for overall development of an economy it is

important for taxes collected to not only fulfil monetary or investment objectives but also ensure

economic security of its people.

This is evidenced in the ILO Report which showed how different governments belonging

to diverse nations aided taxation to accomplish broad social goals. These included job, income,

work , representation, skill reproduction, employment and labour market security. As far as

federal government is concerned one of the socio-economic objective accomplished through

taxation is relieving citizens from poverty by providing basic social services such as wages to

fulfil living expenses through the assignment of social security numbers to the citizens. Another

socio-economic element that is addressed through taxation is that of prevention of concentration

of wealth among to people belonging to a certain class of income. This is achieved through

economic equality and variability in tax levels that lead to a higher tax slab for a higher income

earning bracket (Social Benefits and Costs of Taxation, 2019). Through this, the tax collected

from such taxable classes lead to a better and equitable distribution of wealth among all the tax

brackets.

Hence, one can say that, in recent times, the purpose of federal government to collect

taxes has shifted from generating financing for public expenditure purposes to that of social and

economic centric role.

QUESTION 2

a. Evaluating feasibility of investment based on risk and returns

Risk and Returns are two opposing forces based on which an individual tends to make

important investment decisions (Brigham and Houston, 2012). From a financial perspective, a

risk is considered to be a chance that is taken by the decision-maker, such as investor, with an

expectation that the investment in question will be different from others. Generally, it is observed

that high risk investments give much more fruitful returns. This means that by investing in a high

risk return In order to measure or assess degree of risk related to an investment, measures of

variability and dispersion are taken into consideration. These include variance and standard

deviation respectively.

In the given case scenario, Fair INC. is considering an investment decision in one of two

common stocks viz. Stock A and Stock B. Based on risk and return assessment, it is determined

3

important for taxes collected to not only fulfil monetary or investment objectives but also ensure

economic security of its people.

This is evidenced in the ILO Report which showed how different governments belonging

to diverse nations aided taxation to accomplish broad social goals. These included job, income,

work , representation, skill reproduction, employment and labour market security. As far as

federal government is concerned one of the socio-economic objective accomplished through

taxation is relieving citizens from poverty by providing basic social services such as wages to

fulfil living expenses through the assignment of social security numbers to the citizens. Another

socio-economic element that is addressed through taxation is that of prevention of concentration

of wealth among to people belonging to a certain class of income. This is achieved through

economic equality and variability in tax levels that lead to a higher tax slab for a higher income

earning bracket (Social Benefits and Costs of Taxation, 2019). Through this, the tax collected

from such taxable classes lead to a better and equitable distribution of wealth among all the tax

brackets.

Hence, one can say that, in recent times, the purpose of federal government to collect

taxes has shifted from generating financing for public expenditure purposes to that of social and

economic centric role.

QUESTION 2

a. Evaluating feasibility of investment based on risk and returns

Risk and Returns are two opposing forces based on which an individual tends to make

important investment decisions (Brigham and Houston, 2012). From a financial perspective, a

risk is considered to be a chance that is taken by the decision-maker, such as investor, with an

expectation that the investment in question will be different from others. Generally, it is observed

that high risk investments give much more fruitful returns. This means that by investing in a high

risk return In order to measure or assess degree of risk related to an investment, measures of

variability and dispersion are taken into consideration. These include variance and standard

deviation respectively.

In the given case scenario, Fair INC. is considering an investment decision in one of two

common stocks viz. Stock A and Stock B. Based on risk and return assessment, it is determined

3

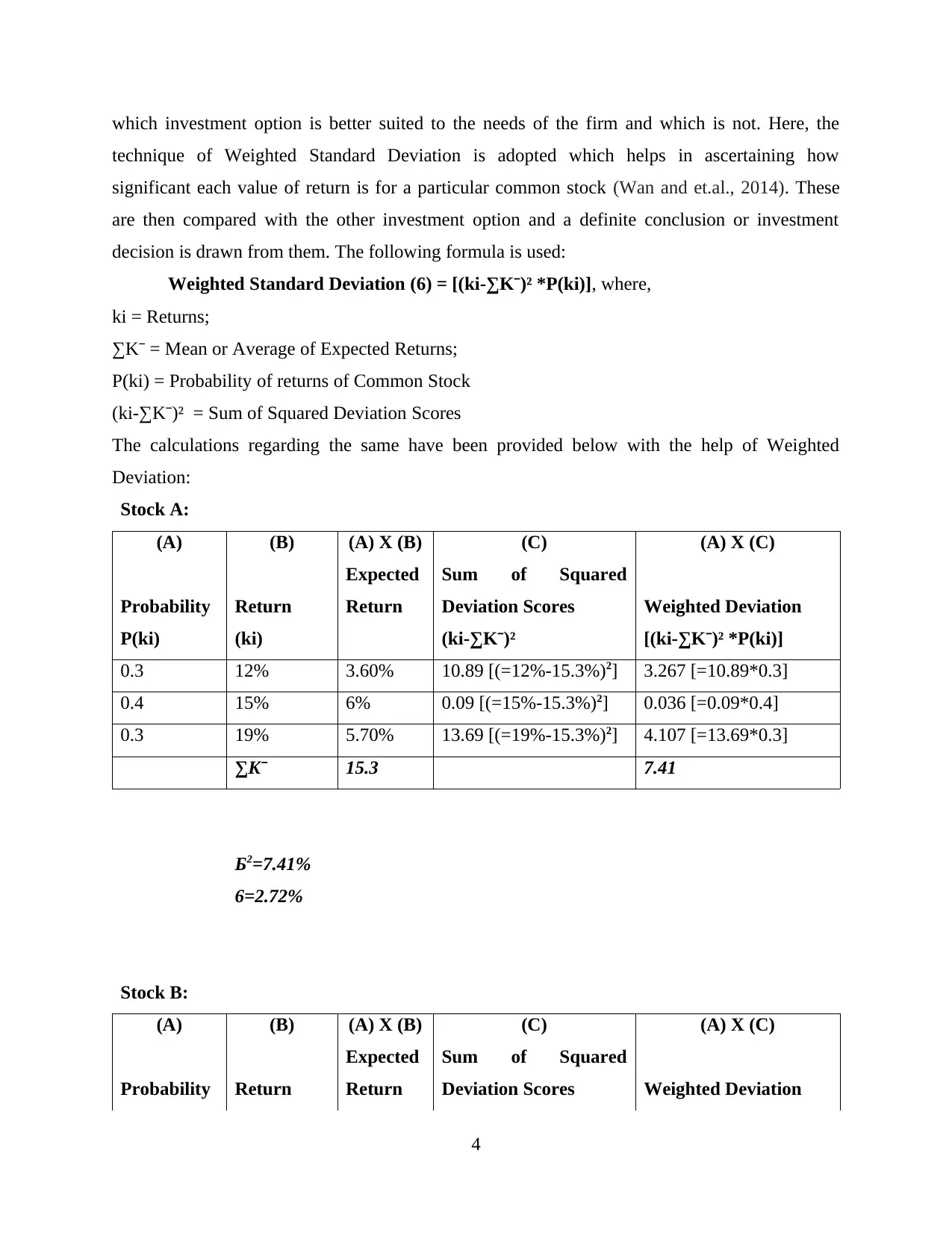

which investment option is better suited to the needs of the firm and which is not. Here, the

technique of Weighted Standard Deviation is adopted which helps in ascertaining how

significant each value of return is for a particular common stock (Wan and et.al., 2014). These

are then compared with the other investment option and a definite conclusion or investment

decision is drawn from them. The following formula is used:

Weighted Standard Deviation (6) = [(ki-∑Kˉ)² *P(ki)], where,

ki = Returns;

∑Kˉ = Mean or Average of Expected Returns;

P(ki) = Probability of returns of Common Stock

(ki-∑Kˉ)² = Sum of Squared Deviation Scores

The calculations regarding the same have been provided below with the help of Weighted

Deviation:

Stock A:

(A) (B) (A) X (B) (C) (A) X (C)

Probability Return

Expected

Return

Sum of Squared

Deviation Scores Weighted Deviation

P(ki) (ki) (ki-∑Kˉ)² [(ki-∑Kˉ)² *P(ki)]

0.3 12% 3.60% 10.89 [(=12%-15.3%)2] 3.267 [=10.89*0.3]

0.4 15% 6% 0.09 [(=15%-15.3%)2] 0.036 [=0.09*0.4]

0.3 19% 5.70% 13.69 [(=19%-15.3%)2] 4.107 [=13.69*0.3]

∑Kˉ 15.3 7.41

Б2=7.41%

6=2.72%

Stock B:

(A) (B) (A) X (B) (C) (A) X (C)

Probability Return

Expected

Return

Sum of Squared

Deviation Scores Weighted Deviation

4

technique of Weighted Standard Deviation is adopted which helps in ascertaining how

significant each value of return is for a particular common stock (Wan and et.al., 2014). These

are then compared with the other investment option and a definite conclusion or investment

decision is drawn from them. The following formula is used:

Weighted Standard Deviation (6) = [(ki-∑Kˉ)² *P(ki)], where,

ki = Returns;

∑Kˉ = Mean or Average of Expected Returns;

P(ki) = Probability of returns of Common Stock

(ki-∑Kˉ)² = Sum of Squared Deviation Scores

The calculations regarding the same have been provided below with the help of Weighted

Deviation:

Stock A:

(A) (B) (A) X (B) (C) (A) X (C)

Probability Return

Expected

Return

Sum of Squared

Deviation Scores Weighted Deviation

P(ki) (ki) (ki-∑Kˉ)² [(ki-∑Kˉ)² *P(ki)]

0.3 12% 3.60% 10.89 [(=12%-15.3%)2] 3.267 [=10.89*0.3]

0.4 15% 6% 0.09 [(=15%-15.3%)2] 0.036 [=0.09*0.4]

0.3 19% 5.70% 13.69 [(=19%-15.3%)2] 4.107 [=13.69*0.3]

∑Kˉ 15.3 7.41

Б2=7.41%

6=2.72%

Stock B:

(A) (B) (A) X (B) (C) (A) X (C)

Probability Return

Expected

Return

Sum of Squared

Deviation Scores Weighted Deviation

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P(ki) (ki) (ki-∑Kˉ)² [(ki-∑Kˉ)²*P(ki)]

0.2 15% 3.00% 2.56 [(=15%-13.4%)2] 0.512 [=2.56*0.2]

0.3 6% 1.80% 54.76 [(=6%-13.4%)2] 16.428 [=54.76*0.3]

0.3 14% 4.20% 0.36 [(=14%-13.4%)2] 0.108 [=0.36*0.3]

0.2 22% 4.40% 73.96 [(=22%-13.4%)2] 14.792 [=73.96*0.2]

∑Kˉ 13.4 31.84

б2=31.84%

6=5.64%

On comparing the two stocks based on the weighted deviation results, investment in

common stock option-A should be accepted as it is less risky compared to stock-B.

b. Concept of Risk and Diversification

From a financial perspective, a risk is considered to be a unplanned opportunity that is

taken by the investor with an expectation that the such an opportunity will be different from

others (Clarke, De Silva and Thorley, 2013). Typically, higher returns are associated with

heavily risky investment options. However, an individual may be conservative and would not

want to invest at all with such high risk attached options. Conversely, an investor may also

choose to diversify their portfolio by adding various investments that have different risks and

returns attached to it. Through this, an investor is able to hedge their risk and gain higher returns,

both at the same time. This phenomenon is known as 'Diversification of Portfolio'. It helps in

reducing the probability of a loss occurrence and increasing the profit derived eventually leading

to wealth maximization for the investor.

QUESTION 3

a. Estimating Holycross' Total Financing and Net Funding Requirements

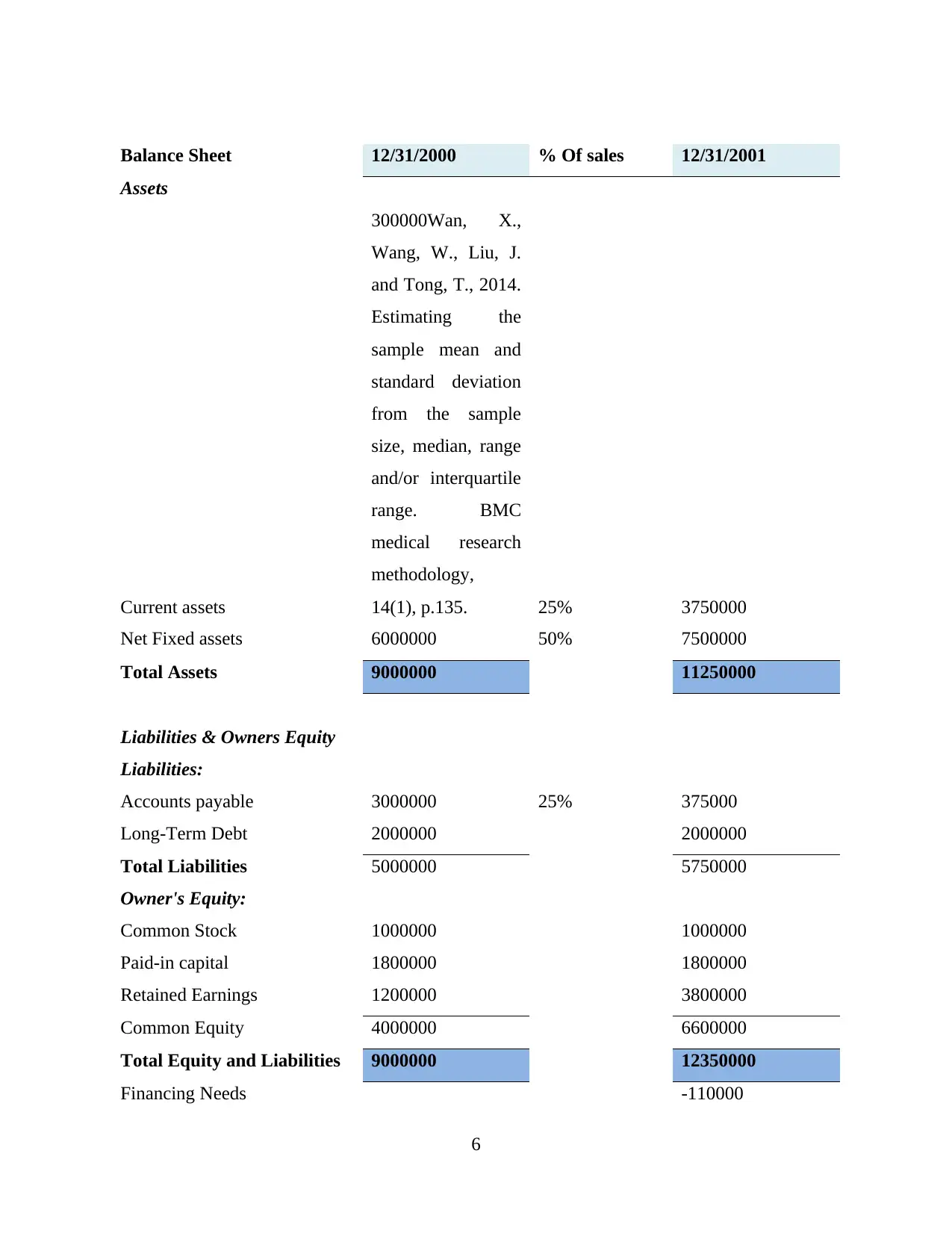

FINANCIAL FORECASTING FOR HOLYCROSS ENTERPRISES

DATE 12/31/2000 12/31/2001

Sales 12000000 15000000

Net Income 1200000 2000000

5

0.2 15% 3.00% 2.56 [(=15%-13.4%)2] 0.512 [=2.56*0.2]

0.3 6% 1.80% 54.76 [(=6%-13.4%)2] 16.428 [=54.76*0.3]

0.3 14% 4.20% 0.36 [(=14%-13.4%)2] 0.108 [=0.36*0.3]

0.2 22% 4.40% 73.96 [(=22%-13.4%)2] 14.792 [=73.96*0.2]

∑Kˉ 13.4 31.84

б2=31.84%

6=5.64%

On comparing the two stocks based on the weighted deviation results, investment in

common stock option-A should be accepted as it is less risky compared to stock-B.

b. Concept of Risk and Diversification

From a financial perspective, a risk is considered to be a unplanned opportunity that is

taken by the investor with an expectation that the such an opportunity will be different from

others (Clarke, De Silva and Thorley, 2013). Typically, higher returns are associated with

heavily risky investment options. However, an individual may be conservative and would not

want to invest at all with such high risk attached options. Conversely, an investor may also

choose to diversify their portfolio by adding various investments that have different risks and

returns attached to it. Through this, an investor is able to hedge their risk and gain higher returns,

both at the same time. This phenomenon is known as 'Diversification of Portfolio'. It helps in

reducing the probability of a loss occurrence and increasing the profit derived eventually leading

to wealth maximization for the investor.

QUESTION 3

a. Estimating Holycross' Total Financing and Net Funding Requirements

FINANCIAL FORECASTING FOR HOLYCROSS ENTERPRISES

DATE 12/31/2000 12/31/2001

Sales 12000000 15000000

Net Income 1200000 2000000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balance Sheet 12/31/2000 % Of sales 12/31/2001

Assets

Current assets

300000Wan, X.,

Wang, W., Liu, J.

and Tong, T., 2014.

Estimating the

sample mean and

standard deviation

from the sample

size, median, range

and/or interquartile

range. BMC

medical research

methodology,

14(1), p.135. 25% 3750000

Net Fixed assets 6000000 50% 7500000

Total Assets 9000000 11250000

Liabilities & Owners Equity

Liabilities:

Accounts payable 3000000 25% 375000

Long-Term Debt 2000000 2000000

Total Liabilities 5000000 5750000

Owner's Equity:

Common Stock 1000000 1000000

Paid-in capital 1800000 1800000

Retained Earnings 1200000 3800000

Common Equity 4000000 6600000

Total Equity and Liabilities 9000000 12350000

Financing Needs -110000

6

Assets

Current assets

300000Wan, X.,

Wang, W., Liu, J.

and Tong, T., 2014.

Estimating the

sample mean and

standard deviation

from the sample

size, median, range

and/or interquartile

range. BMC

medical research

methodology,

14(1), p.135. 25% 3750000

Net Fixed assets 6000000 50% 7500000

Total Assets 9000000 11250000

Liabilities & Owners Equity

Liabilities:

Accounts payable 3000000 25% 375000

Long-Term Debt 2000000 2000000

Total Liabilities 5000000 5750000

Owner's Equity:

Common Stock 1000000 1000000

Paid-in capital 1800000 1800000

Retained Earnings 1200000 3800000

Common Equity 4000000 6600000

Total Equity and Liabilities 9000000 12350000

Financing Needs -110000

6

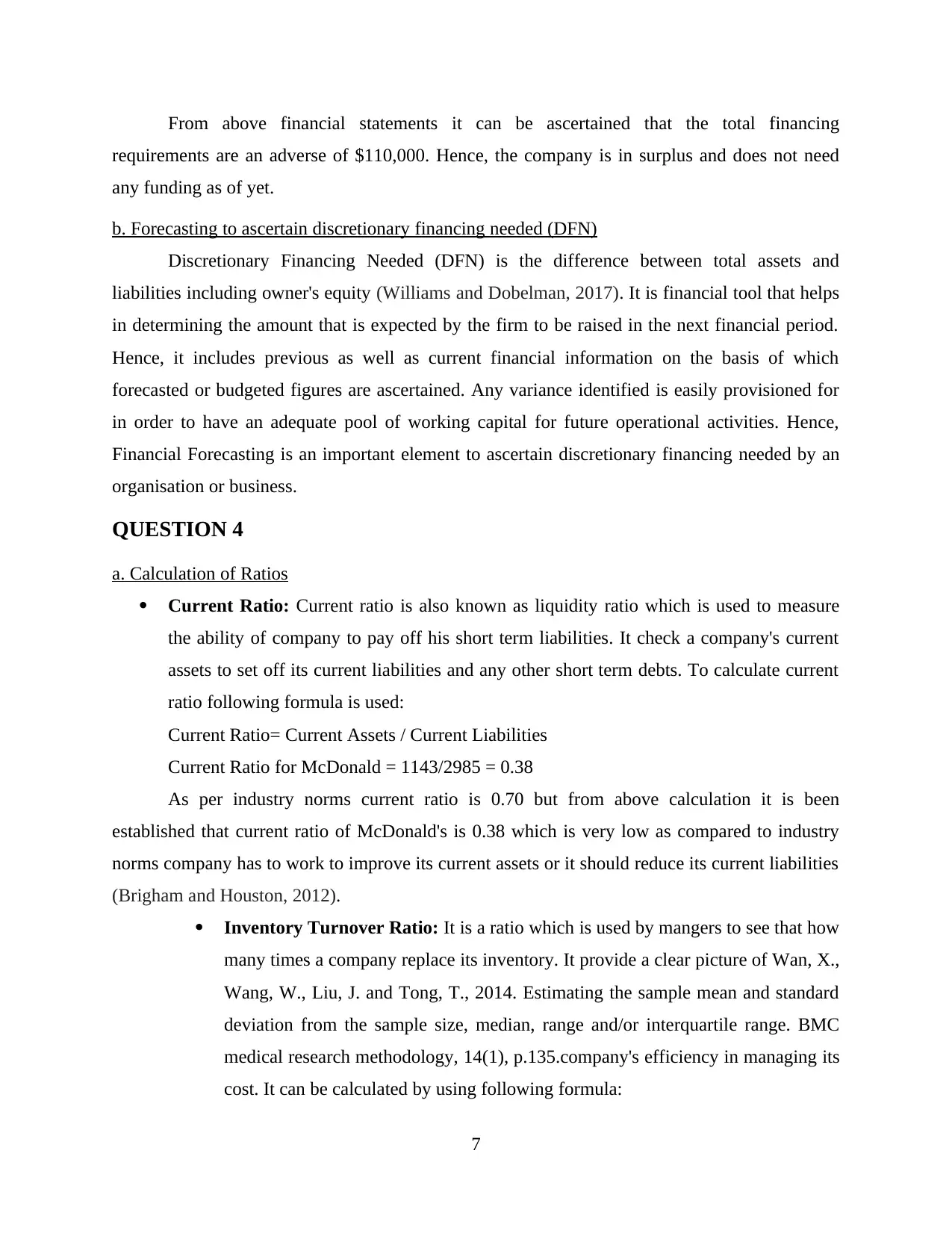

From above financial statements it can be ascertained that the total financing

requirements are an adverse of $110,000. Hence, the company is in surplus and does not need

any funding as of yet.

b. Forecasting to ascertain discretionary financing needed (DFN)

Discretionary Financing Needed (DFN) is the difference between total assets and

liabilities including owner's equity (Williams and Dobelman, 2017). It is financial tool that helps

in determining the amount that is expected by the firm to be raised in the next financial period.

Hence, it includes previous as well as current financial information on the basis of which

forecasted or budgeted figures are ascertained. Any variance identified is easily provisioned for

in order to have an adequate pool of working capital for future operational activities. Hence,

Financial Forecasting is an important element to ascertain discretionary financing needed by an

organisation or business.

QUESTION 4

a. Calculation of Ratios

Current Ratio: Current ratio is also known as liquidity ratio which is used to measure

the ability of company to pay off his short term liabilities. It check a company's current

assets to set off its current liabilities and any other short term debts. To calculate current

ratio following formula is used:

Current Ratio= Current Assets / Current Liabilities

Current Ratio for McDonald = 1143/2985 = 0.38

As per industry norms current ratio is 0.70 but from above calculation it is been

established that current ratio of McDonald's is 0.38 which is very low as compared to industry

norms company has to work to improve its current assets or it should reduce its current liabilities

(Brigham and Houston, 2012).

Inventory Turnover Ratio: It is a ratio which is used by mangers to see that how

many times a company replace its inventory. It provide a clear picture of Wan, X.,

Wang, W., Liu, J. and Tong, T., 2014. Estimating the sample mean and standard

deviation from the sample size, median, range and/or interquartile range. BMC

medical research methodology, 14(1), p.135.company's efficiency in managing its

cost. It can be calculated by using following formula:

7

requirements are an adverse of $110,000. Hence, the company is in surplus and does not need

any funding as of yet.

b. Forecasting to ascertain discretionary financing needed (DFN)

Discretionary Financing Needed (DFN) is the difference between total assets and

liabilities including owner's equity (Williams and Dobelman, 2017). It is financial tool that helps

in determining the amount that is expected by the firm to be raised in the next financial period.

Hence, it includes previous as well as current financial information on the basis of which

forecasted or budgeted figures are ascertained. Any variance identified is easily provisioned for

in order to have an adequate pool of working capital for future operational activities. Hence,

Financial Forecasting is an important element to ascertain discretionary financing needed by an

organisation or business.

QUESTION 4

a. Calculation of Ratios

Current Ratio: Current ratio is also known as liquidity ratio which is used to measure

the ability of company to pay off his short term liabilities. It check a company's current

assets to set off its current liabilities and any other short term debts. To calculate current

ratio following formula is used:

Current Ratio= Current Assets / Current Liabilities

Current Ratio for McDonald = 1143/2985 = 0.38

As per industry norms current ratio is 0.70 but from above calculation it is been

established that current ratio of McDonald's is 0.38 which is very low as compared to industry

norms company has to work to improve its current assets or it should reduce its current liabilities

(Brigham and Houston, 2012).

Inventory Turnover Ratio: It is a ratio which is used by mangers to see that how

many times a company replace its inventory. It provide a clear picture of Wan, X.,

Wang, W., Liu, J. and Tong, T., 2014. Estimating the sample mean and standard

deviation from the sample size, median, range and/or interquartile range. BMC

medical research methodology, 14(1), p.135.company's efficiency in managing its

cost. It can be calculated by using following formula:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

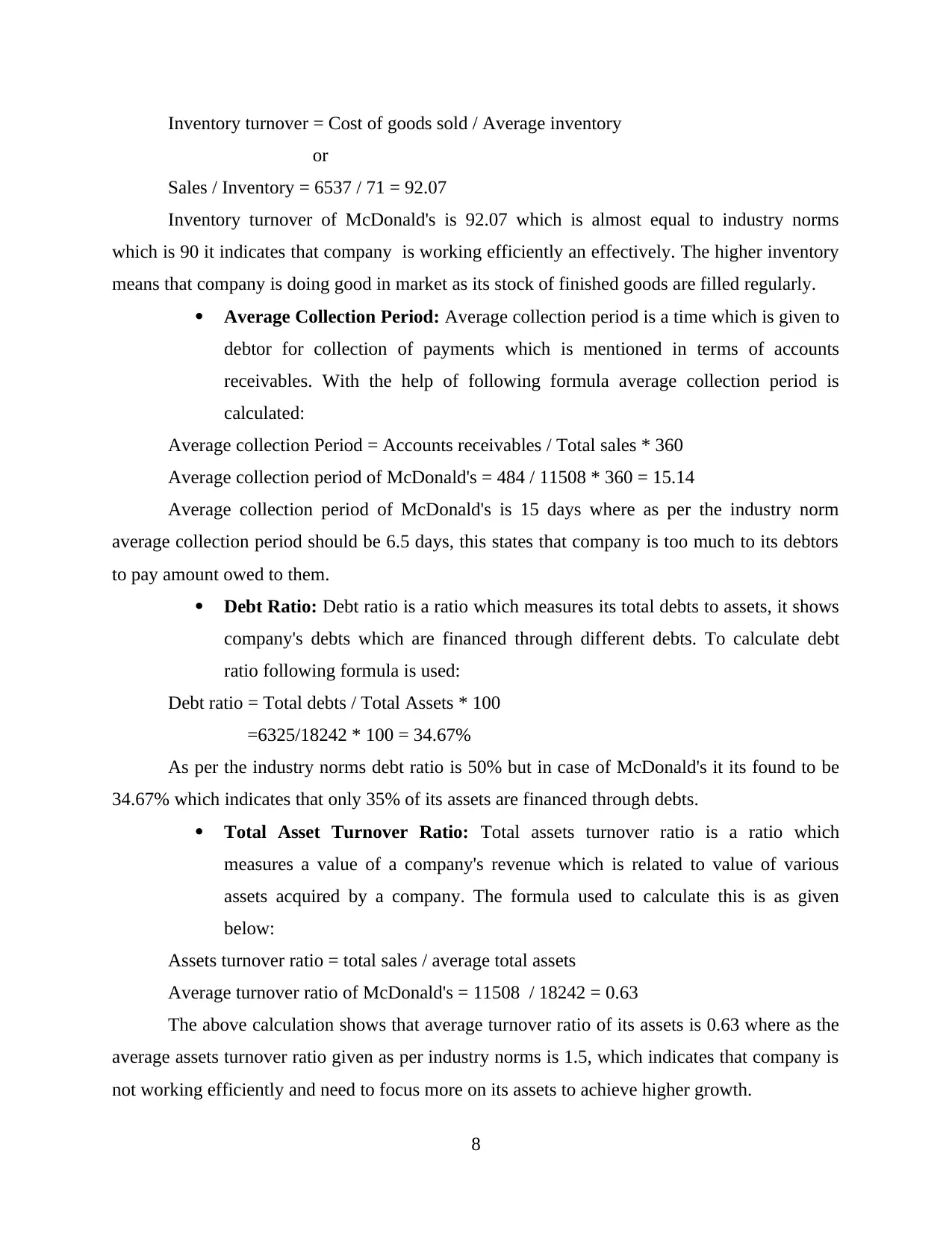

Inventory turnover = Cost of goods sold / Average inventory

or

Sales / Inventory = 6537 / 71 = 92.07

Inventory turnover of McDonald's is 92.07 which is almost equal to industry norms

which is 90 it indicates that company is working efficiently an effectively. The higher inventory

means that company is doing good in market as its stock of finished goods are filled regularly.

Average Collection Period: Average collection period is a time which is given to

debtor for collection of payments which is mentioned in terms of accounts

receivables. With the help of following formula average collection period is

calculated:

Average collection Period = Accounts receivables / Total sales * 360

Average collection period of McDonald's = 484 / 11508 * 360 = 15.14

Average collection period of McDonald's is 15 days where as per the industry norm

average collection period should be 6.5 days, this states that company is too much to its debtors

to pay amount owed to them.

Debt Ratio: Debt ratio is a ratio which measures its total debts to assets, it shows

company's debts which are financed through different debts. To calculate debt

ratio following formula is used:

Debt ratio = Total debts / Total Assets * 100

=6325/18242 * 100 = 34.67%

As per the industry norms debt ratio is 50% but in case of McDonald's it its found to be

34.67% which indicates that only 35% of its assets are financed through debts.

Total Asset Turnover Ratio: Total assets turnover ratio is a ratio which

measures a value of a company's revenue which is related to value of various

assets acquired by a company. The formula used to calculate this is as given

below:

Assets turnover ratio = total sales / average total assets

Average turnover ratio of McDonald's = 11508 / 18242 = 0.63

The above calculation shows that average turnover ratio of its assets is 0.63 where as the

average assets turnover ratio given as per industry norms is 1.5, which indicates that company is

not working efficiently and need to focus more on its assets to achieve higher growth.

8

or

Sales / Inventory = 6537 / 71 = 92.07

Inventory turnover of McDonald's is 92.07 which is almost equal to industry norms

which is 90 it indicates that company is working efficiently an effectively. The higher inventory

means that company is doing good in market as its stock of finished goods are filled regularly.

Average Collection Period: Average collection period is a time which is given to

debtor for collection of payments which is mentioned in terms of accounts

receivables. With the help of following formula average collection period is

calculated:

Average collection Period = Accounts receivables / Total sales * 360

Average collection period of McDonald's = 484 / 11508 * 360 = 15.14

Average collection period of McDonald's is 15 days where as per the industry norm

average collection period should be 6.5 days, this states that company is too much to its debtors

to pay amount owed to them.

Debt Ratio: Debt ratio is a ratio which measures its total debts to assets, it shows

company's debts which are financed through different debts. To calculate debt

ratio following formula is used:

Debt ratio = Total debts / Total Assets * 100

=6325/18242 * 100 = 34.67%

As per the industry norms debt ratio is 50% but in case of McDonald's it its found to be

34.67% which indicates that only 35% of its assets are financed through debts.

Total Asset Turnover Ratio: Total assets turnover ratio is a ratio which

measures a value of a company's revenue which is related to value of various

assets acquired by a company. The formula used to calculate this is as given

below:

Assets turnover ratio = total sales / average total assets

Average turnover ratio of McDonald's = 11508 / 18242 = 0.63

The above calculation shows that average turnover ratio of its assets is 0.63 where as the

average assets turnover ratio given as per industry norms is 1.5, which indicates that company is

not working efficiently and need to focus more on its assets to achieve higher growth.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

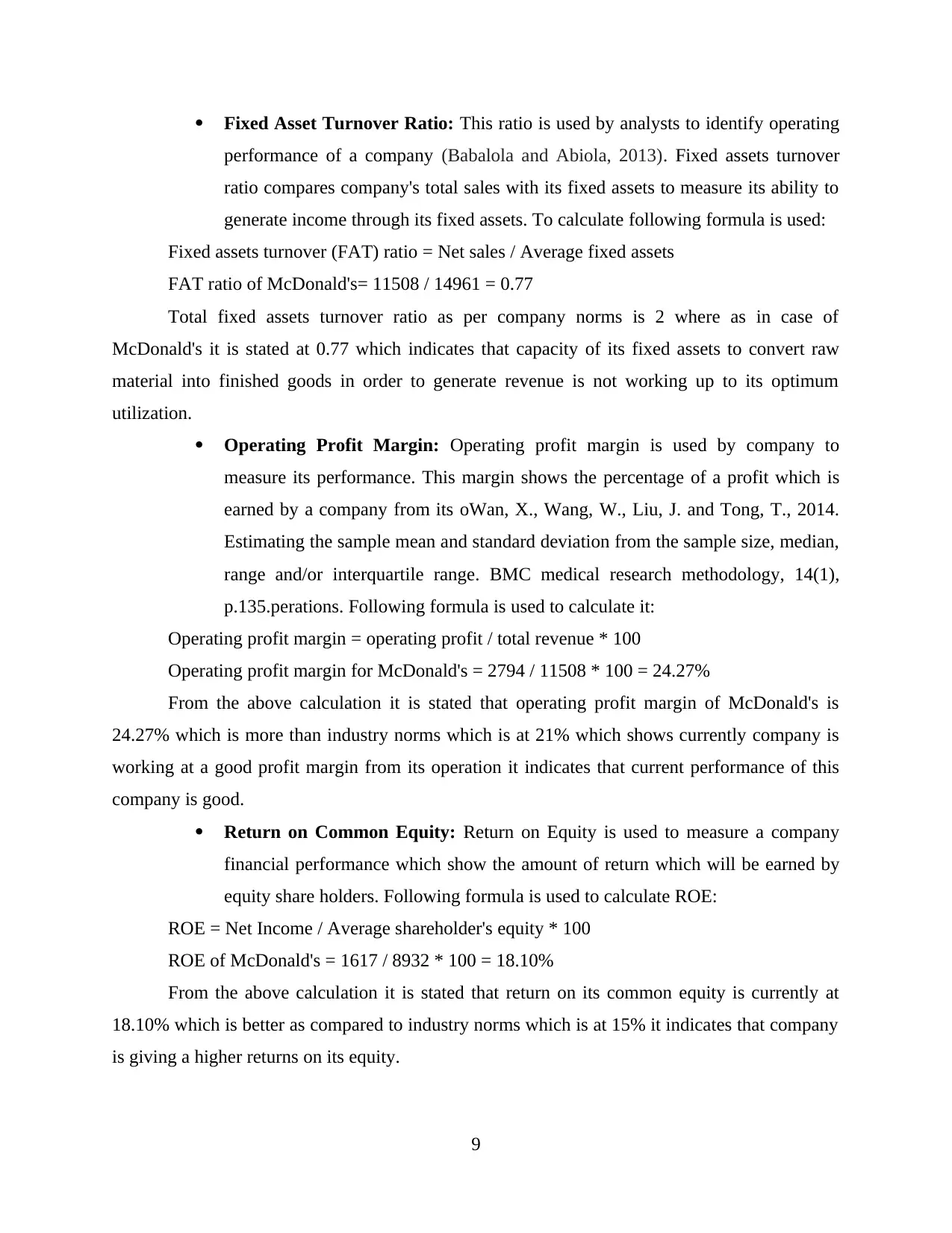

Fixed Asset Turnover Ratio: This ratio is used by analysts to identify operating

performance of a company (Babalola and Abiola, 2013). Fixed assets turnover

ratio compares company's total sales with its fixed assets to measure its ability to

generate income through its fixed assets. To calculate following formula is used:

Fixed assets turnover (FAT) ratio = Net sales / Average fixed assets

FAT ratio of McDonald's= 11508 / 14961 = 0.77

Total fixed assets turnover ratio as per company norms is 2 where as in case of

McDonald's it is stated at 0.77 which indicates that capacity of its fixed assets to convert raw

material into finished goods in order to generate revenue is not working up to its optimum

utilization.

Operating Profit Margin: Operating profit margin is used by company to

measure its performance. This margin shows the percentage of a profit which is

earned by a company from its oWan, X., Wang, W., Liu, J. and Tong, T., 2014.

Estimating the sample mean and standard deviation from the sample size, median,

range and/or interquartile range. BMC medical research methodology, 14(1),

p.135.perations. Following formula is used to calculate it:

Operating profit margin = operating profit / total revenue * 100

Operating profit margin for McDonald's = 2794 / 11508 * 100 = 24.27%

From the above calculation it is stated that operating profit margin of McDonald's is

24.27% which is more than industry norms which is at 21% which shows currently company is

working at a good profit margin from its operation it indicates that current performance of this

company is good.

Return on Common Equity: Return on Equity is used to measure a company

financial performance which show the amount of return which will be earned by

equity share holders. Following formula is used to calculate ROE:

ROE = Net Income / Average shareholder's equity * 100

ROE of McDonald's = 1617 / 8932 * 100 = 18.10%

From the above calculation it is stated that return on its common equity is currently at

18.10% which is better as compared to industry norms which is at 15% it indicates that company

is giving a higher returns on its equity.

9

performance of a company (Babalola and Abiola, 2013). Fixed assets turnover

ratio compares company's total sales with its fixed assets to measure its ability to

generate income through its fixed assets. To calculate following formula is used:

Fixed assets turnover (FAT) ratio = Net sales / Average fixed assets

FAT ratio of McDonald's= 11508 / 14961 = 0.77

Total fixed assets turnover ratio as per company norms is 2 where as in case of

McDonald's it is stated at 0.77 which indicates that capacity of its fixed assets to convert raw

material into finished goods in order to generate revenue is not working up to its optimum

utilization.

Operating Profit Margin: Operating profit margin is used by company to

measure its performance. This margin shows the percentage of a profit which is

earned by a company from its oWan, X., Wang, W., Liu, J. and Tong, T., 2014.

Estimating the sample mean and standard deviation from the sample size, median,

range and/or interquartile range. BMC medical research methodology, 14(1),

p.135.perations. Following formula is used to calculate it:

Operating profit margin = operating profit / total revenue * 100

Operating profit margin for McDonald's = 2794 / 11508 * 100 = 24.27%

From the above calculation it is stated that operating profit margin of McDonald's is

24.27% which is more than industry norms which is at 21% which shows currently company is

working at a good profit margin from its operation it indicates that current performance of this

company is good.

Return on Common Equity: Return on Equity is used to measure a company

financial performance which show the amount of return which will be earned by

equity share holders. Following formula is used to calculate ROE:

ROE = Net Income / Average shareholder's equity * 100

ROE of McDonald's = 1617 / 8932 * 100 = 18.10%

From the above calculation it is stated that return on its common equity is currently at

18.10% which is better as compared to industry norms which is at 15% it indicates that company

is giving a higher returns on its equity.

9

b. Advantages and limitations of Ratio Analysis

Ratio analysis is a financial tool which is used to analyse the financial reports prepared at

the end of an accounting period (Gotze, Northcott and Schuster, 2016) . It gives an advantage to

shareholders to properly interpret this data more accurately following are some advantages and

limitations of it:

Advantages:

It help mangers to check authenticity of validating or disproving financing, operating and

investment decision of a company. It also help investors to take decisions which helps them in

investing as it simplifies a complex accounting systems and financial data in to easy ratio which

are easy to interpret.

Limitations:

Some ratios are calculated on historical cost basis which ignores changes in price due to

inflation and does not reflect correct picture. Firms can make some changes in their financial

statement during year end which does not reflect a correct image of a company and ends up

being Window dressing.

QUESTION 5

a. Recommending a Project using Investment Appraisal Techniques

Payback period:

Average Cash Inflows = Total Cash Inflows / Project Life

Project A = ($10,000+$15,000+$20,000+$25,000+$30,000) / 5 = $20,000

Project B = ($25,000+$25,000+$25,000+$25,000+$25,000) / 5 = $25,000

Payback Period = Initial Outlay / Average Cash flows

Project A = $50,000/$20,000 = 2.5 years

Project B = $100,000/$25,000 = 4 years

Interpretation:

As Project A recovers the cost invested in a shorter time duration as compared to Project

B, it should be selected for investment (Kalyebara and Islam, 2013).

Accounting rate of return (ARR):

Average annual profits= Total net cash flows/ Number of years

Project A = $100,000/5 =$20,000

10

Ratio analysis is a financial tool which is used to analyse the financial reports prepared at

the end of an accounting period (Gotze, Northcott and Schuster, 2016) . It gives an advantage to

shareholders to properly interpret this data more accurately following are some advantages and

limitations of it:

Advantages:

It help mangers to check authenticity of validating or disproving financing, operating and

investment decision of a company. It also help investors to take decisions which helps them in

investing as it simplifies a complex accounting systems and financial data in to easy ratio which

are easy to interpret.

Limitations:

Some ratios are calculated on historical cost basis which ignores changes in price due to

inflation and does not reflect correct picture. Firms can make some changes in their financial

statement during year end which does not reflect a correct image of a company and ends up

being Window dressing.

QUESTION 5

a. Recommending a Project using Investment Appraisal Techniques

Payback period:

Average Cash Inflows = Total Cash Inflows / Project Life

Project A = ($10,000+$15,000+$20,000+$25,000+$30,000) / 5 = $20,000

Project B = ($25,000+$25,000+$25,000+$25,000+$25,000) / 5 = $25,000

Payback Period = Initial Outlay / Average Cash flows

Project A = $50,000/$20,000 = 2.5 years

Project B = $100,000/$25,000 = 4 years

Interpretation:

As Project A recovers the cost invested in a shorter time duration as compared to Project

B, it should be selected for investment (Kalyebara and Islam, 2013).

Accounting rate of return (ARR):

Average annual profits= Total net cash flows/ Number of years

Project A = $100,000/5 =$20,000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.