Comprehensive Financial Analysis: Browns Plc Case Study Report

VerifiedAdded on 2023/06/18

|13

|3500

|445

Case Study

AI Summary

This case study provides a financial analysis of Browns Plc, focusing on ratio analysis, cash flow, and working capital management. The analysis includes calculations and interpretations of key financial ratios such as Gross Profit Margin, Operating Profit Margin, Current Ratio, Quick Ratio, Inventory Holding Period, and Payables Payment Period, comparing the results between 2018 and 2019. The irrelevance of computing the receivables collection period is justified due to the company's cash-based operational practices. Furthermore, the report differentiates between profit and cash flow, explains the components of working capital (receivables, inventory, and payables) along with their advantages and disadvantages, and analyzes the impact of changes in working capital on cash flow. The study concludes with an analysis of the appropriateness of traditional and alternative budgetary systems in the given context. Desklib offers a variety of solved assignments and study resources for students.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

PART 1 FINANCIAL RATIO ANALYSIS................................................................................................3

Ratio Analysis.........................................................................................................................................3

Interpretation of ratios.............................................................................................................................5

Irrelevance of computing the receivables collection period in this case study.........................................7

PART 2 UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF CASH...............7

2.1 Describing profit & cash flow and differentiation among both..........................................................7

2.2 Explaining working capital, receivables, inventory and payables along with advantages and

disadvantages...........................................................................................................................................9

2.3 Explaining the reasons for changes in working capital affecting cash flow.....................................10

2.4 Analyzing appropriate of traditional and alternative budgetary system in the respective format. .11

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................13

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

PART 1 FINANCIAL RATIO ANALYSIS................................................................................................3

Ratio Analysis.........................................................................................................................................3

Interpretation of ratios.............................................................................................................................5

Irrelevance of computing the receivables collection period in this case study.........................................7

PART 2 UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF CASH...............7

2.1 Describing profit & cash flow and differentiation among both..........................................................7

2.2 Explaining working capital, receivables, inventory and payables along with advantages and

disadvantages...........................................................................................................................................9

2.3 Explaining the reasons for changes in working capital affecting cash flow.....................................10

2.4 Analyzing appropriate of traditional and alternative budgetary system in the respective format. .11

CONCLUSION.........................................................................................................................................12

REFERENCES..........................................................................................................................................13

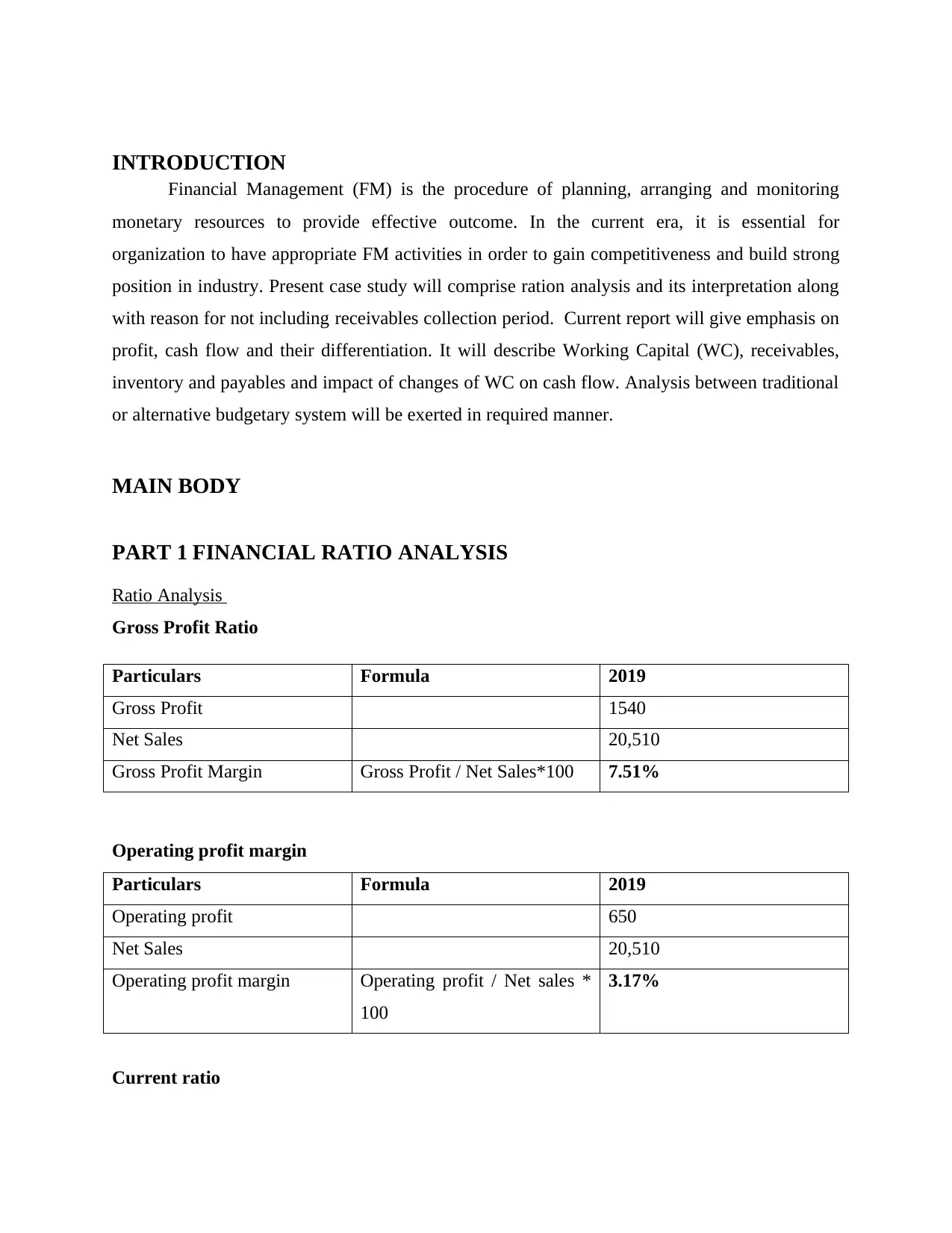

INTRODUCTION

Financial Management (FM) is the procedure of planning, arranging and monitoring

monetary resources to provide effective outcome. In the current era, it is essential for

organization to have appropriate FM activities in order to gain competitiveness and build strong

position in industry. Present case study will comprise ration analysis and its interpretation along

with reason for not including receivables collection period. Current report will give emphasis on

profit, cash flow and their differentiation. It will describe Working Capital (WC), receivables,

inventory and payables and impact of changes of WC on cash flow. Analysis between traditional

or alternative budgetary system will be exerted in required manner.

MAIN BODY

PART 1 FINANCIAL RATIO ANALYSIS

Ratio Analysis

Gross Profit Ratio

Particulars Formula 2019

Gross Profit 1540

Net Sales 20,510

Gross Profit Margin Gross Profit / Net Sales*100 7.51%

Operating profit margin

Particulars Formula 2019

Operating profit 650

Net Sales 20,510

Operating profit margin Operating profit / Net sales *

100

3.17%

Current ratio

Financial Management (FM) is the procedure of planning, arranging and monitoring

monetary resources to provide effective outcome. In the current era, it is essential for

organization to have appropriate FM activities in order to gain competitiveness and build strong

position in industry. Present case study will comprise ration analysis and its interpretation along

with reason for not including receivables collection period. Current report will give emphasis on

profit, cash flow and their differentiation. It will describe Working Capital (WC), receivables,

inventory and payables and impact of changes of WC on cash flow. Analysis between traditional

or alternative budgetary system will be exerted in required manner.

MAIN BODY

PART 1 FINANCIAL RATIO ANALYSIS

Ratio Analysis

Gross Profit Ratio

Particulars Formula 2019

Gross Profit 1540

Net Sales 20,510

Gross Profit Margin Gross Profit / Net Sales*100 7.51%

Operating profit margin

Particulars Formula 2019

Operating profit 650

Net Sales 20,510

Operating profit margin Operating profit / Net sales *

100

3.17%

Current ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

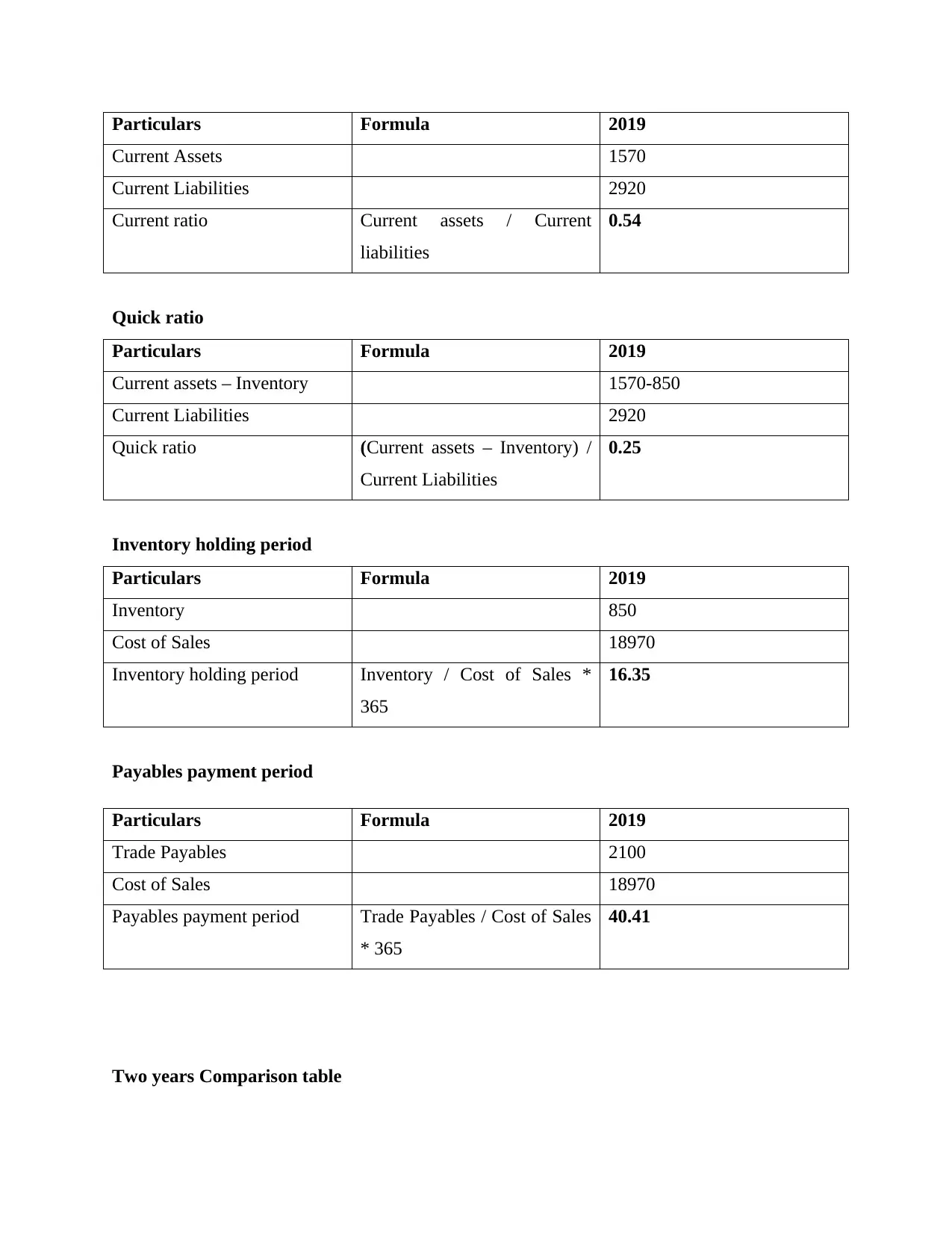

Particulars Formula 2019

Current Assets 1570

Current Liabilities 2920

Current ratio Current assets / Current

liabilities

0.54

Quick ratio

Particulars Formula 2019

Current assets – Inventory 1570-850

Current Liabilities 2920

Quick ratio (Current assets – Inventory) /

Current Liabilities

0.25

Inventory holding period

Particulars Formula 2019

Inventory 850

Cost of Sales 18970

Inventory holding period Inventory / Cost of Sales *

365

16.35

Payables payment period

Particulars Formula 2019

Trade Payables 2100

Cost of Sales 18970

Payables payment period Trade Payables / Cost of Sales

* 365

40.41

Two years Comparison table

Current Assets 1570

Current Liabilities 2920

Current ratio Current assets / Current

liabilities

0.54

Quick ratio

Particulars Formula 2019

Current assets – Inventory 1570-850

Current Liabilities 2920

Quick ratio (Current assets – Inventory) /

Current Liabilities

0.25

Inventory holding period

Particulars Formula 2019

Inventory 850

Cost of Sales 18970

Inventory holding period Inventory / Cost of Sales *

365

16.35

Payables payment period

Particulars Formula 2019

Trade Payables 2100

Cost of Sales 18970

Payables payment period Trade Payables / Cost of Sales

* 365

40.41

Two years Comparison table

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

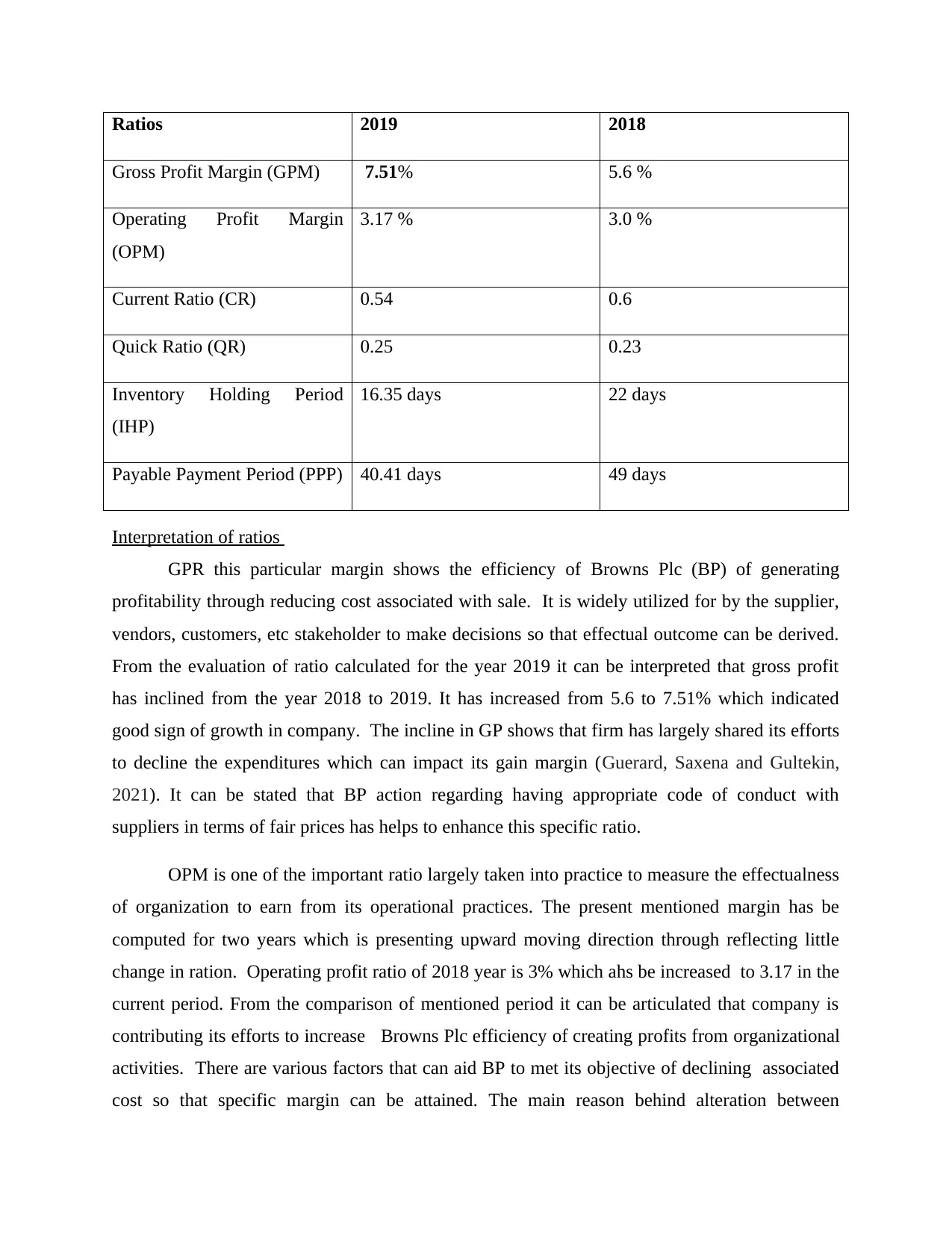

Ratios 2019 2018

Gross Profit Margin (GPM) 7.51% 5.6 %

Operating Profit Margin

(OPM)

3.17 % 3.0 %

Current Ratio (CR) 0.54 0.6

Quick Ratio (QR) 0.25 0.23

Inventory Holding Period

(IHP)

16.35 days 22 days

Payable Payment Period (PPP) 40.41 days 49 days

Interpretation of ratios

GPR this particular margin shows the efficiency of Browns Plc (BP) of generating

profitability through reducing cost associated with sale. It is widely utilized for by the supplier,

vendors, customers, etc stakeholder to make decisions so that effectual outcome can be derived.

From the evaluation of ratio calculated for the year 2019 it can be interpreted that gross profit

has inclined from the year 2018 to 2019. It has increased from 5.6 to 7.51% which indicated

good sign of growth in company. The incline in GP shows that firm has largely shared its efforts

to decline the expenditures which can impact its gain margin (Guerard, Saxena and Gultekin,

2021). It can be stated that BP action regarding having appropriate code of conduct with

suppliers in terms of fair prices has helps to enhance this specific ratio.

OPM is one of the important ratio largely taken into practice to measure the effectualness

of organization to earn from its operational practices. The present mentioned margin has be

computed for two years which is presenting upward moving direction through reflecting little

change in ration. Operating profit ratio of 2018 year is 3% which ahs be increased to 3.17 in the

current period. From the comparison of mentioned period it can be articulated that company is

contributing its efforts to increase Browns Plc efficiency of creating profits from organizational

activities. There are various factors that can aid BP to met its objective of declining associated

cost so that specific margin can be attained. The main reason behind alteration between

Gross Profit Margin (GPM) 7.51% 5.6 %

Operating Profit Margin

(OPM)

3.17 % 3.0 %

Current Ratio (CR) 0.54 0.6

Quick Ratio (QR) 0.25 0.23

Inventory Holding Period

(IHP)

16.35 days 22 days

Payable Payment Period (PPP) 40.41 days 49 days

Interpretation of ratios

GPR this particular margin shows the efficiency of Browns Plc (BP) of generating

profitability through reducing cost associated with sale. It is widely utilized for by the supplier,

vendors, customers, etc stakeholder to make decisions so that effectual outcome can be derived.

From the evaluation of ratio calculated for the year 2019 it can be interpreted that gross profit

has inclined from the year 2018 to 2019. It has increased from 5.6 to 7.51% which indicated

good sign of growth in company. The incline in GP shows that firm has largely shared its efforts

to decline the expenditures which can impact its gain margin (Guerard, Saxena and Gultekin,

2021). It can be stated that BP action regarding having appropriate code of conduct with

suppliers in terms of fair prices has helps to enhance this specific ratio.

OPM is one of the important ratio largely taken into practice to measure the effectualness

of organization to earn from its operational practices. The present mentioned margin has be

computed for two years which is presenting upward moving direction through reflecting little

change in ration. Operating profit ratio of 2018 year is 3% which ahs be increased to 3.17 in the

current period. From the comparison of mentioned period it can be articulated that company is

contributing its efforts to increase Browns Plc efficiency of creating profits from organizational

activities. There are various factors that can aid BP to met its objective of declining associated

cost so that specific margin can be attained. The main reason behind alteration between

mentioned span performance is increase marketing campaign which has enabled BP to get

ability to enhance its scale of operation through spreading larger awareness about offerings.

Current ratio is significant indicator for analyzing company’s financial performance and

stability. It is basically concerned with identifying firm’s efficiency of utilizing its cash and

equivalent resources to meet short term obligations. There are several types of stakeholders who

take decisions on the basis of CR so firm should highly pay attention for giving positive

outcome. The ideal ratio can that give significance in evaluating actual performance is 1.2-2

times (Pattiruhu and PAAIS, 2020). Browns Plc‘s CR has been computed for two period such as

2018 which has given outcome of 0.6 to 0.54 times respectively. It can be identify that BP’s

efficiency of utilizing resources to overcome current liabilities has been declined due to number

of store increased by 10%. This is recognized as main reason as this particular course of action

has affected liquidity position of company s some part of money has been utilized to fulfill

objective.

Quick ratio indicates liquidity position of company through largely emphasis on short

term marketable assets to cover current liabilities. QR of Browns Plc has been determined for

two respective years which represent the actual outcome that can be taken into practice to derive

significant knowledge of liquidity condition of organization. BP’s quick ratio for the year 2018

and 2019 are 0.23 to 0.25 times respectively. It represents positive movement of performance as

compared to previous year by indicating very small change. QR is highly taken in to

consideration by suppliers, Investors, vendors, financial institution, etc. to evaluate company’s

capacity of paying short term obligations. It is important for respective organization to

concentrate on this field to maintain trustworthiness and credibility in industry. It can aid BP to

attain sustainable amount of efficiency for carrying forward its business activities. The reason

behind this modification can be interpreted that change customers purchasing behavior has

positively affected liquidity position. There is 20% enhancement in customers as compared to

previous year.

Inventory holding period shows that how much company’s is keeping its stock which

represents its ability of meeting market forces (Hosaka, 2019). Browns Plc’s IHP has been

ability to enhance its scale of operation through spreading larger awareness about offerings.

Current ratio is significant indicator for analyzing company’s financial performance and

stability. It is basically concerned with identifying firm’s efficiency of utilizing its cash and

equivalent resources to meet short term obligations. There are several types of stakeholders who

take decisions on the basis of CR so firm should highly pay attention for giving positive

outcome. The ideal ratio can that give significance in evaluating actual performance is 1.2-2

times (Pattiruhu and PAAIS, 2020). Browns Plc‘s CR has been computed for two period such as

2018 which has given outcome of 0.6 to 0.54 times respectively. It can be identify that BP’s

efficiency of utilizing resources to overcome current liabilities has been declined due to number

of store increased by 10%. This is recognized as main reason as this particular course of action

has affected liquidity position of company s some part of money has been utilized to fulfill

objective.

Quick ratio indicates liquidity position of company through largely emphasis on short

term marketable assets to cover current liabilities. QR of Browns Plc has been determined for

two respective years which represent the actual outcome that can be taken into practice to derive

significant knowledge of liquidity condition of organization. BP’s quick ratio for the year 2018

and 2019 are 0.23 to 0.25 times respectively. It represents positive movement of performance as

compared to previous year by indicating very small change. QR is highly taken in to

consideration by suppliers, Investors, vendors, financial institution, etc. to evaluate company’s

capacity of paying short term obligations. It is important for respective organization to

concentrate on this field to maintain trustworthiness and credibility in industry. It can aid BP to

attain sustainable amount of efficiency for carrying forward its business activities. The reason

behind this modification can be interpreted that change customers purchasing behavior has

positively affected liquidity position. There is 20% enhancement in customers as compared to

previous year.

Inventory holding period shows that how much company’s is keeping its stock which

represents its ability of meeting market forces (Hosaka, 2019). Browns Plc’s IHP has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

highlighted for mentioned period which helps in comparing current performance with previous.

It can be interpreted that in the year and 2018 & 2019 the respective margin is 22 and

16.35days. The results can be articulated that present year performance has reduced as compared

to earlier period and reason behind this is that company’s online sales has inclined due to higher

marketing campaigns. It has resulted into greater revenue generating capacity as compared to

previous period.

Payable payment period shows company’s ability of paying its debt due to suppliers,

creditors, etc. It is one of the crucial ratios utilized to judge firms’ efficiency of overcoming

liabilities. PPP of 2018 and 2019 are 49 & 40.41 days respectively which is reflecting positive

sign for increasing efficiency of paying debts. The reason behind this action can be long term

borrowing has been utilized to enhance credibility of BP.

Irrelevance of computing the receivables collection period in this case study

There is no scope of credit transaction as Browns Plc’s all operational practices are

conducted in cash manner. The organization’s makes its sales practices in cash manner as there is

involvement of online channels for serving customers. Clients are given option to pay either in

cash or in digital mode of payment so that computation of receivable collection period is

irrelevant. It is calculated when firm conducts sales and offer credit payment option as there is

absence which is main reason for adopted decision.

PART 2 UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Describing profit & cash flow and differentiation among both

Profit is one of the main objective of any organization for which it implements several

course of actions. It is the amount derived from deducting expenses incurred from the revenue

generated. there are three types of profits which helps business to understand efficiency of

organization in each aspect. In addition to this, it includes gross, operating and net profit.

Profitability is an important measure utilized by several stakeholders like creditors, investors,

financial institutions, etc in order to formulate strategic decision. Greater amount of profit

reflects business has good efficiency in utilizing its resources to generated revenues through

reducing Cost associated with it (What is Profitability? 2021). This provides assistance in

It can be interpreted that in the year and 2018 & 2019 the respective margin is 22 and

16.35days. The results can be articulated that present year performance has reduced as compared

to earlier period and reason behind this is that company’s online sales has inclined due to higher

marketing campaigns. It has resulted into greater revenue generating capacity as compared to

previous period.

Payable payment period shows company’s ability of paying its debt due to suppliers,

creditors, etc. It is one of the crucial ratios utilized to judge firms’ efficiency of overcoming

liabilities. PPP of 2018 and 2019 are 49 & 40.41 days respectively which is reflecting positive

sign for increasing efficiency of paying debts. The reason behind this action can be long term

borrowing has been utilized to enhance credibility of BP.

Irrelevance of computing the receivables collection period in this case study

There is no scope of credit transaction as Browns Plc’s all operational practices are

conducted in cash manner. The organization’s makes its sales practices in cash manner as there is

involvement of online channels for serving customers. Clients are given option to pay either in

cash or in digital mode of payment so that computation of receivable collection period is

irrelevant. It is calculated when firm conducts sales and offer credit payment option as there is

absence which is main reason for adopted decision.

PART 2 UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Describing profit & cash flow and differentiation among both

Profit is one of the main objective of any organization for which it implements several

course of actions. It is the amount derived from deducting expenses incurred from the revenue

generated. there are three types of profits which helps business to understand efficiency of

organization in each aspect. In addition to this, it includes gross, operating and net profit.

Profitability is an important measure utilized by several stakeholders like creditors, investors,

financial institutions, etc in order to formulate strategic decision. Greater amount of profit

reflects business has good efficiency in utilizing its resources to generated revenues through

reducing Cost associated with it (What is Profitability? 2021). This provides assistance in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achieving wider range of opportunities prevailing in industry for development. Variety of actions

like increasing marketing, advertising, adoption of advanced technologies, etc are adopted to get

assurance that higher profitability can be achieved.

Cash flow is the actual movement of monetary resources in and out of organization for

conducting business practices. There are two forms of cash such as in and out flow which is

concerned with coming inside as payment received and going outside due to meeting obligations

respectively. Cash Flow (CF) either can be positive or negative which reflects liquidity position

of company (Alvarez, Sensini and Vazquez, 2021). For ascertaining information regarding the

subject matter organization prepares cash flow statement through segregating CF into operating,

financing and investing segment. This gives deeper insights to firm regarding more contribution

factor for increasing liquidity in company. Before making investment decisions stakeholders

highly emphasis on the efficiency of company’s in utilizing its cash & equivalents for increasing

performance. With respect to this, several courses of actions are highlighted by organization for

maintaining and ensuring sufficient amount of cash flows in turn smooth functioning can be

obtained.

Profits Cash flow

The difference between organization’s

ales and expenses incurred is called the

profitability.

This is concerned with real movement

of cash from operational, investing and

financial practices.

Profitability of company is estimated

by taking all expenses amount into

consideration (Nariswari and Nugraha,

2020).

Cash flow is computed by comprising

all essential components that is

representing cash in and outflow to

provide information related to

availability of it within company.

It is determined in form of value

formation which assists in measuring

financial health of entity.

It can be estimated in the terms of

durations such as weeks, months and

year.

Profitability is based on accrual

accounting concepts that made in

unreliable representative of financial

CF is concerned with factual

presentation of incoming and outgoing

of cash.

like increasing marketing, advertising, adoption of advanced technologies, etc are adopted to get

assurance that higher profitability can be achieved.

Cash flow is the actual movement of monetary resources in and out of organization for

conducting business practices. There are two forms of cash such as in and out flow which is

concerned with coming inside as payment received and going outside due to meeting obligations

respectively. Cash Flow (CF) either can be positive or negative which reflects liquidity position

of company (Alvarez, Sensini and Vazquez, 2021). For ascertaining information regarding the

subject matter organization prepares cash flow statement through segregating CF into operating,

financing and investing segment. This gives deeper insights to firm regarding more contribution

factor for increasing liquidity in company. Before making investment decisions stakeholders

highly emphasis on the efficiency of company’s in utilizing its cash & equivalents for increasing

performance. With respect to this, several courses of actions are highlighted by organization for

maintaining and ensuring sufficient amount of cash flows in turn smooth functioning can be

obtained.

Profits Cash flow

The difference between organization’s

ales and expenses incurred is called the

profitability.

This is concerned with real movement

of cash from operational, investing and

financial practices.

Profitability of company is estimated

by taking all expenses amount into

consideration (Nariswari and Nugraha,

2020).

Cash flow is computed by comprising

all essential components that is

representing cash in and outflow to

provide information related to

availability of it within company.

It is determined in form of value

formation which assists in measuring

financial health of entity.

It can be estimated in the terms of

durations such as weeks, months and

year.

Profitability is based on accrual

accounting concepts that made in

unreliable representative of financial

CF is concerned with factual

presentation of incoming and outgoing

of cash.

performance.

This is associated with generating cash

so that fluent organizational process

can be assured.

Cash flow is important source for

generating profitability (Dufour, Luu

and Teller, 2018). This provides

significant ability to attain greater

financial advantages.

Functioning of operational activities in

the absence of profitability can be

obtained.

Without available of CF it is tough to

proceed operational practices in

industry.

It becomes possible to determine the

success extent with help of profitability

through emphasis on directional

growth.

This can be used to reach desirable

level of growth by identifying

appropriate availability.

2.2 Explaining working capital, receivables, inventory and payables along with advantages and

disadvantages

Working capital is the difference between current assets and liability which reflects shirt

term liquidity position to meet day to day operational activities. This operating liquidity

requires effective management system to get appropriate efficiency for smooth

functioning. The benefit that organization can derive from it includes stable liquidity,

enhance profitability, value addition to internal process, improved financial condition

(Afrifa and Tingbani, 2018). The concerned drawbacks are that it only shows monetary

factors, non situational, improper guidance in interpretation largely based on data, etc.

Receivables are debt owed to organization by its customers which is outcome of

providing goods and services on credit basis. It recorded on the assets side of balance

sheet and declines when paymenst are received. The most important benefit that

organization receives through preparing receivable account is that more conversion rates,

good image in industry, loyal customers through building good relationship, etc. on the

This is associated with generating cash

so that fluent organizational process

can be assured.

Cash flow is important source for

generating profitability (Dufour, Luu

and Teller, 2018). This provides

significant ability to attain greater

financial advantages.

Functioning of operational activities in

the absence of profitability can be

obtained.

Without available of CF it is tough to

proceed operational practices in

industry.

It becomes possible to determine the

success extent with help of profitability

through emphasis on directional

growth.

This can be used to reach desirable

level of growth by identifying

appropriate availability.

2.2 Explaining working capital, receivables, inventory and payables along with advantages and

disadvantages

Working capital is the difference between current assets and liability which reflects shirt

term liquidity position to meet day to day operational activities. This operating liquidity

requires effective management system to get appropriate efficiency for smooth

functioning. The benefit that organization can derive from it includes stable liquidity,

enhance profitability, value addition to internal process, improved financial condition

(Afrifa and Tingbani, 2018). The concerned drawbacks are that it only shows monetary

factors, non situational, improper guidance in interpretation largely based on data, etc.

Receivables are debt owed to organization by its customers which is outcome of

providing goods and services on credit basis. It recorded on the assets side of balance

sheet and declines when paymenst are received. The most important benefit that

organization receives through preparing receivable account is that more conversion rates,

good image in industry, loyal customers through building good relationship, etc. on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other side limitation of having receivables are that there is no guarantee of payment

recovery as possibility of bad debt, more time consuming, etc.

Inventory refers to availability of stock regarding finished goods, work in process and

raw material. It helps in obtaining ability to meet market forces which is biggest

advantage. The limitation of it is relatively expensive to have manage due to complex

nature.

Payables are the amount due to pay by company to its suppliers, vendors, etc. which

reflects credibility in industry. Having effective payment payable period helps in raising

funds with lower span of time and gaining trustworthiness among stakeholders. It is

recorded in balance sheet in the head of current liabilities and decreases as payments are

made. Pros of payables are availability of time to manage expenses in order to pay in

organized manner. The cons are that burden is created on suppliers that may harm the

efficiency of organization’s procurement procedure.

2.3 Explaining the reasons for changes in working capital affecting cash flow

These two are most crucial concept of financial analysis so gaining significant knowledge

respect to changes become important. Cash flow statement is widely prepared by organization

irrespective of their scale of operation. Cash is part of current assets that is significant factor for

determining working capital. The changes in any part of current assets or liability impact cash

flow in positive or negative factor. If there is alteration in same proportion then there will no

influence on CF. There are several types of actions taken by firm to reduce negative impact of

WC on cash flow (What is net working capital? 2021). In addition to this, direct and indirect

methods for computing correct balance is utilized in turn depth understanding regarding the same

can be obtained. For instance if the firm is selling fixed assets which means that cash will come

in company that represents growth in current assets. Alteration in working capital will highly

influence the cash flow in positive manner. This reflects that company has good financial health

in terms of liquidity.

Several types of business transaction take place which impacts on working capital as if there is

inclination of current assets then can be interpreted there would be enhance in cash flow of

company in order to maintain sustainable operational practices. If there is increase in liabilities

then it will influence working capital by declining cash flow available with company.

recovery as possibility of bad debt, more time consuming, etc.

Inventory refers to availability of stock regarding finished goods, work in process and

raw material. It helps in obtaining ability to meet market forces which is biggest

advantage. The limitation of it is relatively expensive to have manage due to complex

nature.

Payables are the amount due to pay by company to its suppliers, vendors, etc. which

reflects credibility in industry. Having effective payment payable period helps in raising

funds with lower span of time and gaining trustworthiness among stakeholders. It is

recorded in balance sheet in the head of current liabilities and decreases as payments are

made. Pros of payables are availability of time to manage expenses in order to pay in

organized manner. The cons are that burden is created on suppliers that may harm the

efficiency of organization’s procurement procedure.

2.3 Explaining the reasons for changes in working capital affecting cash flow

These two are most crucial concept of financial analysis so gaining significant knowledge

respect to changes become important. Cash flow statement is widely prepared by organization

irrespective of their scale of operation. Cash is part of current assets that is significant factor for

determining working capital. The changes in any part of current assets or liability impact cash

flow in positive or negative factor. If there is alteration in same proportion then there will no

influence on CF. There are several types of actions taken by firm to reduce negative impact of

WC on cash flow (What is net working capital? 2021). In addition to this, direct and indirect

methods for computing correct balance is utilized in turn depth understanding regarding the same

can be obtained. For instance if the firm is selling fixed assets which means that cash will come

in company that represents growth in current assets. Alteration in working capital will highly

influence the cash flow in positive manner. This reflects that company has good financial health

in terms of liquidity.

Several types of business transaction take place which impacts on working capital as if there is

inclination of current assets then can be interpreted there would be enhance in cash flow of

company in order to maintain sustainable operational practices. If there is increase in liabilities

then it will influence working capital by declining cash flow available with company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.4 Analyzing appropriate of traditional and alternative budgetary system in the respective

format

Traditional Budgetary system revolves around revenues, expenditure, profitability and

loses through adjusting changes in business. This is prepared by taking the base of historical

information by giving emphasis on inflation rate, customers demand. It is not that flexible so

that adopting changing circumstances can become possible for company. It is suitable to some

parts of organization only which has fixed nature and does not require much consideration.

Taking decisions on the basis of traditional budgetary can enable firm to reduce some sort of

competitive in order to manage its financial resources (Chugunov and Makohon, 2020). Two

types of approaches such as bottom up and top down are utilized by firm which comprises some

planning gap. There is inaccurate presentation of goals of company due to largely focus on

decided nature of functioning via avoiding prevailing circumstances.

Alternative budgetary system is largely taken into practice through giving emphasis on

flexible, incremental, zero and activity based budgeting, etc. in the present scenario competition

in sector has inclined that require firm to be prompt and effective decision making. It can be

possible by adopting any of the mentioned method to have effectualness in implementing

flexible nature to cope up with present scenarios (Hartle, 2019). Zero based budgeting is

prepared from the scratch that provides higher convince and feasibility in formulating policies

and actions via taking all essential information of year into consideration. Operational cost can

be declined in all parts through discipline execution of resources. It gives assistance in

accomplishing objectives of organization by executing improvement actions through focusing on

accuracy, efficiency, coordination, communication, etc in all functional areas. Priority based

budgeting is associated with listing all activities of company in order manner to identify higher

prioritize activities. It is ranked from high to low so that allocating, organizing, managing and

controlling resources can be exerted in effectual manner. Activity based budgeting is another

type of alternative system which is concentrate on predicting cost that planning for meeting

unforeseen circumstances can become possible. From the evaluation it can be stated that

alternative budgetary system is more efficient as compared to traditional for planning purpose.

format

Traditional Budgetary system revolves around revenues, expenditure, profitability and

loses through adjusting changes in business. This is prepared by taking the base of historical

information by giving emphasis on inflation rate, customers demand. It is not that flexible so

that adopting changing circumstances can become possible for company. It is suitable to some

parts of organization only which has fixed nature and does not require much consideration.

Taking decisions on the basis of traditional budgetary can enable firm to reduce some sort of

competitive in order to manage its financial resources (Chugunov and Makohon, 2020). Two

types of approaches such as bottom up and top down are utilized by firm which comprises some

planning gap. There is inaccurate presentation of goals of company due to largely focus on

decided nature of functioning via avoiding prevailing circumstances.

Alternative budgetary system is largely taken into practice through giving emphasis on

flexible, incremental, zero and activity based budgeting, etc. in the present scenario competition

in sector has inclined that require firm to be prompt and effective decision making. It can be

possible by adopting any of the mentioned method to have effectualness in implementing

flexible nature to cope up with present scenarios (Hartle, 2019). Zero based budgeting is

prepared from the scratch that provides higher convince and feasibility in formulating policies

and actions via taking all essential information of year into consideration. Operational cost can

be declined in all parts through discipline execution of resources. It gives assistance in

accomplishing objectives of organization by executing improvement actions through focusing on

accuracy, efficiency, coordination, communication, etc in all functional areas. Priority based

budgeting is associated with listing all activities of company in order manner to identify higher

prioritize activities. It is ranked from high to low so that allocating, organizing, managing and

controlling resources can be exerted in effectual manner. Activity based budgeting is another

type of alternative system which is concentrate on predicting cost that planning for meeting

unforeseen circumstances can become possible. From the evaluation it can be stated that

alternative budgetary system is more efficient as compared to traditional for planning purpose.

CONCLUSION

From the above report it can be concluded that report ahs included ratio analysis and its

interpretation in required format. Case study has comprised descriptions of profitability, CF and

differentiation among them. In addition to this, working capital, receivables, inventory, payables

and impact of WC on CF has been explained. The present report has stated the appropriateness

of traditional and alternative budgetary system in required manner.

From the above report it can be concluded that report ahs included ratio analysis and its

interpretation in required format. Case study has comprised descriptions of profitability, CF and

differentiation among them. In addition to this, working capital, receivables, inventory, payables

and impact of WC on CF has been explained. The present report has stated the appropriateness

of traditional and alternative budgetary system in required manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.