Financial Management and Ratio Analysis for Improved Business Performance

VerifiedAdded on 2023/06/18

|13

|2682

|405

AI Summary

This article discusses financial management, including planning, organizing, directing, and controlling. It also covers financial statements, ratio analysis, and ways to improve business performance. The article includes a case study and appendix with balance sheets and calculations. The subject is applied business finance, and the course code and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

BUSINESS FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Section 1...........................................................................................................................................3

MAIN BODY...................................................................................................................................4

Section 2...........................................................................................................................................4

Section 3...........................................................................................................................................6

iv) Analysis of company's profitability, liquidity and efficiency with the help of ratio analysis

.....................................................................................................................................................8

Section 4...........................................................................................................................................9

Process through which the company can improve its financial performance.............................9

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION...........................................................................................................................3

Section 1...........................................................................................................................................3

MAIN BODY...................................................................................................................................4

Section 2...........................................................................................................................................4

Section 3...........................................................................................................................................6

iv) Analysis of company's profitability, liquidity and efficiency with the help of ratio analysis

.....................................................................................................................................................8

Section 4...........................................................................................................................................9

Process through which the company can improve its financial performance.............................9

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................12

INTRODUCTION

Section 1

Definition of financial management: According to Guthman and Dougal, Financial

management is concerned with the activities such as planning, acquiring, controlling and

administering the financial resources of the business.

Financial management is a practice adopted to manage the financial resources associated with

the organisation. Financial management is a concept comprises with various features that involve

planning, implementing, controllability such like factors.

Planning

Planning is a initial stage belong to the financial management as a concept. This is an

initial stage of the financial management practice adopted by the organisation. Planning involve

analysing the need of the business entity in context to financial resources and on the basis of the

needs analysed this is about to plan the use of financial resources at the organisation. Planning

play a significant role in the entire financial management related practices adopted by the

organisation (Yang, 2021). This stage of the financial management practice support both the

aspects or elements such as analysing the financial requirements of the business entity along with

identifying or planning about the right sources to mitigate the respective financial requirements.

Organizing

Organising is among the core financial management practice adopted by the organisation.

This is about to organise all different funds available with the organisation. The role of

organising is very crucial in respect to the business venture when it comes conducting the

financial management practice at the company. This involve identifying the sources and on the

basis of the identification done this is about to organise all different funding requirements of the

company. All different sources of funds are also analysed in this which comprises with long term

sources along with short term sources of funds identified by the business entity.

Directing

Directing is among the core area of practice related to the financial management practice

adopted by the organisation. Directing is about to guide the financial professional to make a best

possible use of the financial resources adopted by the organisation. The role of directing is to

ensure the most optimum level of utilisation related to the financial resource obtain by the entity

Section 1

Definition of financial management: According to Guthman and Dougal, Financial

management is concerned with the activities such as planning, acquiring, controlling and

administering the financial resources of the business.

Financial management is a practice adopted to manage the financial resources associated with

the organisation. Financial management is a concept comprises with various features that involve

planning, implementing, controllability such like factors.

Planning

Planning is a initial stage belong to the financial management as a concept. This is an

initial stage of the financial management practice adopted by the organisation. Planning involve

analysing the need of the business entity in context to financial resources and on the basis of the

needs analysed this is about to plan the use of financial resources at the organisation. Planning

play a significant role in the entire financial management related practices adopted by the

organisation (Yang, 2021). This stage of the financial management practice support both the

aspects or elements such as analysing the financial requirements of the business entity along with

identifying or planning about the right sources to mitigate the respective financial requirements.

Organizing

Organising is among the core financial management practice adopted by the organisation.

This is about to organise all different funds available with the organisation. The role of

organising is very crucial in respect to the business venture when it comes conducting the

financial management practice at the company. This involve identifying the sources and on the

basis of the identification done this is about to organise all different funding requirements of the

company. All different sources of funds are also analysed in this which comprises with long term

sources along with short term sources of funds identified by the business entity.

Directing

Directing is among the core area of practice related to the financial management practice

adopted by the organisation. Directing is about to guide the financial professional to make a best

possible use of the financial resources adopted by the organisation. The role of directing is to

ensure the most optimum level of utilisation related to the financial resource obtain by the entity

(Ferdiana and Sulistyo, 2019). Directing is the use of different techniques like budgeting and

such like practices to make a best possible use of the financial resources adopted by the firm.

Role of directing is very significant in respect to the business venture to support the organisation

in consuming financial resources in the best way possible. This is done byt the head of finance

team and professional contain experience and good knowledge about the financial resources and

its utilisation.

Controlling

Controlling is among the core area or practice that support the business entity to improve

the utility of the financial resource adopted by the organisation. This is a process that involve

taking suitable decisions to manage and control the financial resources entertain by the venture.

The above stated factors are a part of the different concepts related to the financial

management adopted by the organisation.

Importance of financial management

It improve the financial stability at the organisation.

Financial resources are get to utilise in the best way possible through the use of best level

of financial management practices adopted by the company.

Financial management support the financial stability at the organisation.

This also play role in improving the liquidity situation at the organisation.

MAIN BODY

Section 2

Financial statements are all about the documents that demonstrate about the different

areas related to the financial management practices adopted by the organisation. All these

statement demonstrate about the all different areas and tactics related to the financial stability

uphold by the organisation.

Income statement

Income statement is among the core record associate with the financial management

practice adopted by the organisation. This is a statement demonstrate about the income and

expense record belong to the venture (Chmutova, Vovk and Bezrodna, 2017). The role of the

income statement is to project about the income business venture entertain against delivering

business operations and the expense that could be incurred against delivering the business

such like practices to make a best possible use of the financial resources adopted by the firm.

Role of directing is very significant in respect to the business venture to support the organisation

in consuming financial resources in the best way possible. This is done byt the head of finance

team and professional contain experience and good knowledge about the financial resources and

its utilisation.

Controlling

Controlling is among the core area or practice that support the business entity to improve

the utility of the financial resource adopted by the organisation. This is a process that involve

taking suitable decisions to manage and control the financial resources entertain by the venture.

The above stated factors are a part of the different concepts related to the financial

management adopted by the organisation.

Importance of financial management

It improve the financial stability at the organisation.

Financial resources are get to utilise in the best way possible through the use of best level

of financial management practices adopted by the company.

Financial management support the financial stability at the organisation.

This also play role in improving the liquidity situation at the organisation.

MAIN BODY

Section 2

Financial statements are all about the documents that demonstrate about the different

areas related to the financial management practices adopted by the organisation. All these

statement demonstrate about the all different areas and tactics related to the financial stability

uphold by the organisation.

Income statement

Income statement is among the core record associate with the financial management

practice adopted by the organisation. This is a statement demonstrate about the income and

expense record belong to the venture (Chmutova, Vovk and Bezrodna, 2017). The role of the

income statement is to project about the income business venture entertain against delivering

business operations and the expense that could be incurred against delivering the business

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

practices. This is a basic projection related to all income and expenses incurred by the company

in the respective financial year.

Balance sheet

Balance sheet is a summarise statement related to the assets hold by the organisation and

liability owe by the organisation. This demonstrate about all the assets such as current and long

term assets undertake by the venture (Karadag, 2017). Along with this liabilities such as current

liability and long term liabilities are projected in this record. Equity related details are also given

in this statement.

Cash flow statement

Cash flow statement is a projection related to all cash inflow and outflow associated with

the organisation. This statement demonstrate all cash nature income and all cash form of

expenses incurred by the organisation. The aim of the statement is demonstrated about the

liquidity position of the organisation.

Use of ratio in financial management

Ratio is a technique that is used to analysis the financial performance and stability of the

organisation. This is a technique support the organisation to analysis the overall performance of

the venture in the respective financial year. The technique of ratio is to identify the different

performing areas like profitability, liquidity, efficiency and such like areas associated with the

financial management. The basic characteristic of the ratio analysis is to identify the performance

of the organisation and also to compare the ratios with previous financial years (Cashin and

et.al., 2017). The use of ratio is also undertaking decisions relayed to the financial management

at the organisation. In context to the financial management the basic role ratios play in to make

decisions in context o business operations. Ratios support the management to understand the

overall performance of the venture and based on that this is about to make important decisions on

the basis of the financial needs and requirements of venture. Ratio played a key role in

supporting the overall growth of the business entity by identifying certain opportunities or areas

that seek an improvement or development.

in the respective financial year.

Balance sheet

Balance sheet is a summarise statement related to the assets hold by the organisation and

liability owe by the organisation. This demonstrate about all the assets such as current and long

term assets undertake by the venture (Karadag, 2017). Along with this liabilities such as current

liability and long term liabilities are projected in this record. Equity related details are also given

in this statement.

Cash flow statement

Cash flow statement is a projection related to all cash inflow and outflow associated with

the organisation. This statement demonstrate all cash nature income and all cash form of

expenses incurred by the organisation. The aim of the statement is demonstrated about the

liquidity position of the organisation.

Use of ratio in financial management

Ratio is a technique that is used to analysis the financial performance and stability of the

organisation. This is a technique support the organisation to analysis the overall performance of

the venture in the respective financial year. The technique of ratio is to identify the different

performing areas like profitability, liquidity, efficiency and such like areas associated with the

financial management. The basic characteristic of the ratio analysis is to identify the performance

of the organisation and also to compare the ratios with previous financial years (Cashin and

et.al., 2017). The use of ratio is also undertaking decisions relayed to the financial management

at the organisation. In context to the financial management the basic role ratios play in to make

decisions in context o business operations. Ratios support the management to understand the

overall performance of the venture and based on that this is about to make important decisions on

the basis of the financial needs and requirements of venture. Ratio played a key role in

supporting the overall growth of the business entity by identifying certain opportunities or areas

that seek an improvement or development.

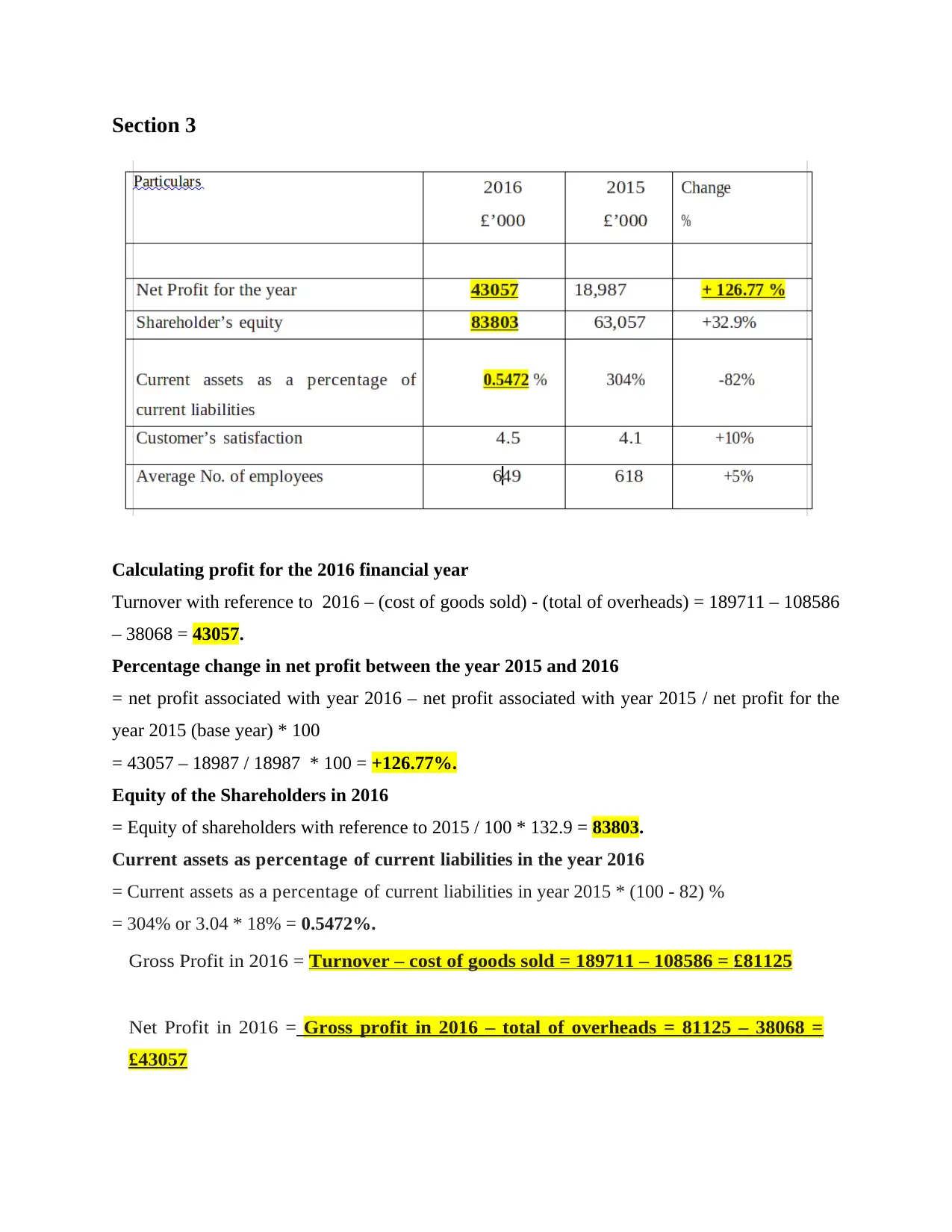

Section 3

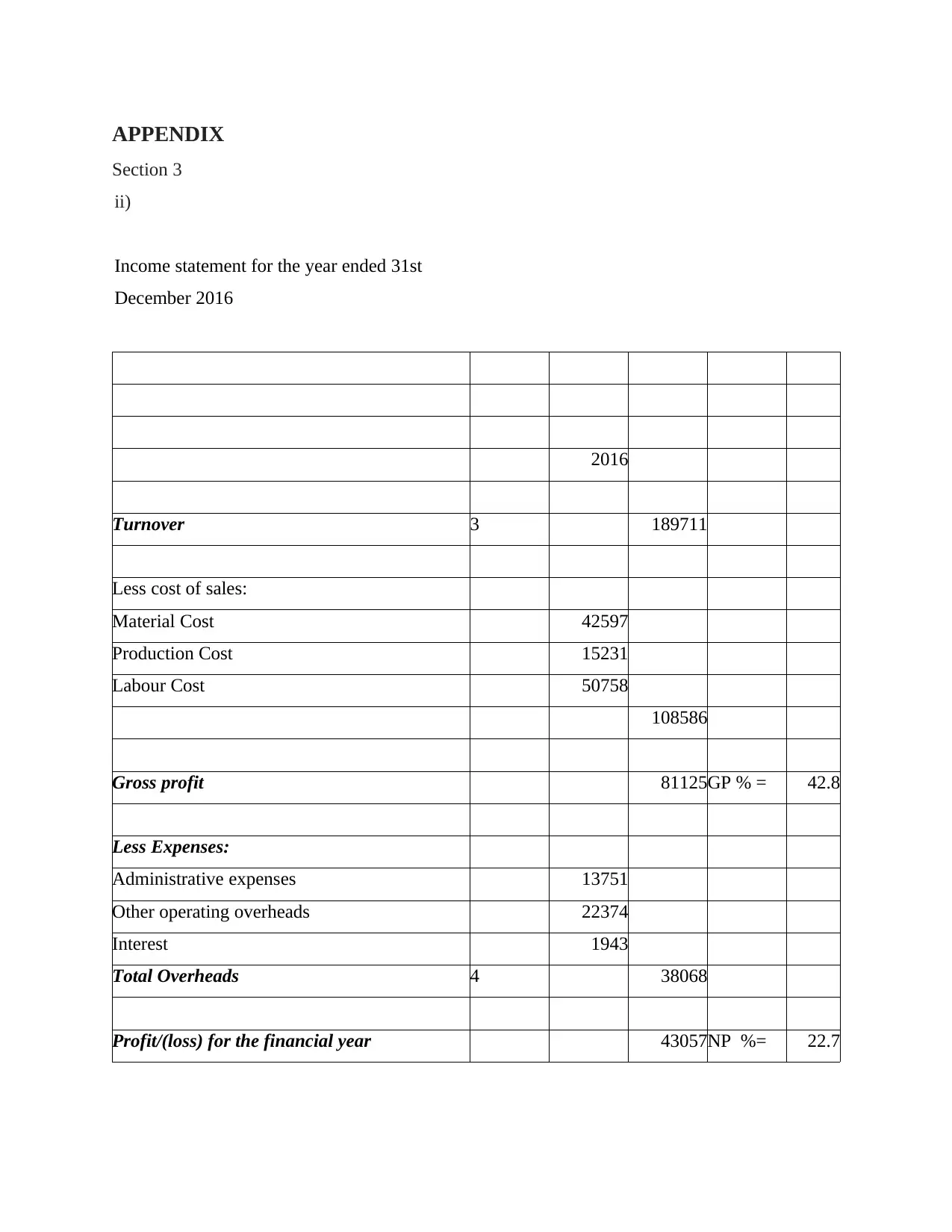

Calculating profit for the 2016 financial year

Turnover with reference to 2016 – (cost of goods sold) - (total of overheads) = 189711 – 108586

– 38068 = 43057.

Percentage change in net profit between the year 2015 and 2016

= net profit associated with year 2016 – net profit associated with year 2015 / net profit for the

year 2015 (base year) * 100

= 43057 – 18987 / 18987 * 100 = +126.77%.

Equity of the Shareholders in 2016

= Equity of shareholders with reference to 2015 / 100 * 132.9 = 83803.

Current assets as percentage of current liabilities in the year 2016

= Current assets as a percentage of current liabilities in year 2015 * (100 - 82) %

= 304% or 3.04 * 18% = 0.5472%.

Gross Profit in 2016 = Turnover – cost of goods sold = 189711 – 108586 = £ 81125

Net Profit in 2016 = Gross profit in 2016 – total of overheads = 81125 – 38068 =

£43057

Calculating profit for the 2016 financial year

Turnover with reference to 2016 – (cost of goods sold) - (total of overheads) = 189711 – 108586

– 38068 = 43057.

Percentage change in net profit between the year 2015 and 2016

= net profit associated with year 2016 – net profit associated with year 2015 / net profit for the

year 2015 (base year) * 100

= 43057 – 18987 / 18987 * 100 = +126.77%.

Equity of the Shareholders in 2016

= Equity of shareholders with reference to 2015 / 100 * 132.9 = 83803.

Current assets as percentage of current liabilities in the year 2016

= Current assets as a percentage of current liabilities in year 2015 * (100 - 82) %

= 304% or 3.04 * 18% = 0.5472%.

Gross Profit in 2016 = Turnover – cost of goods sold = 189711 – 108586 = £ 81125

Net Profit in 2016 = Gross profit in 2016 – total of overheads = 81125 – 38068 =

£43057

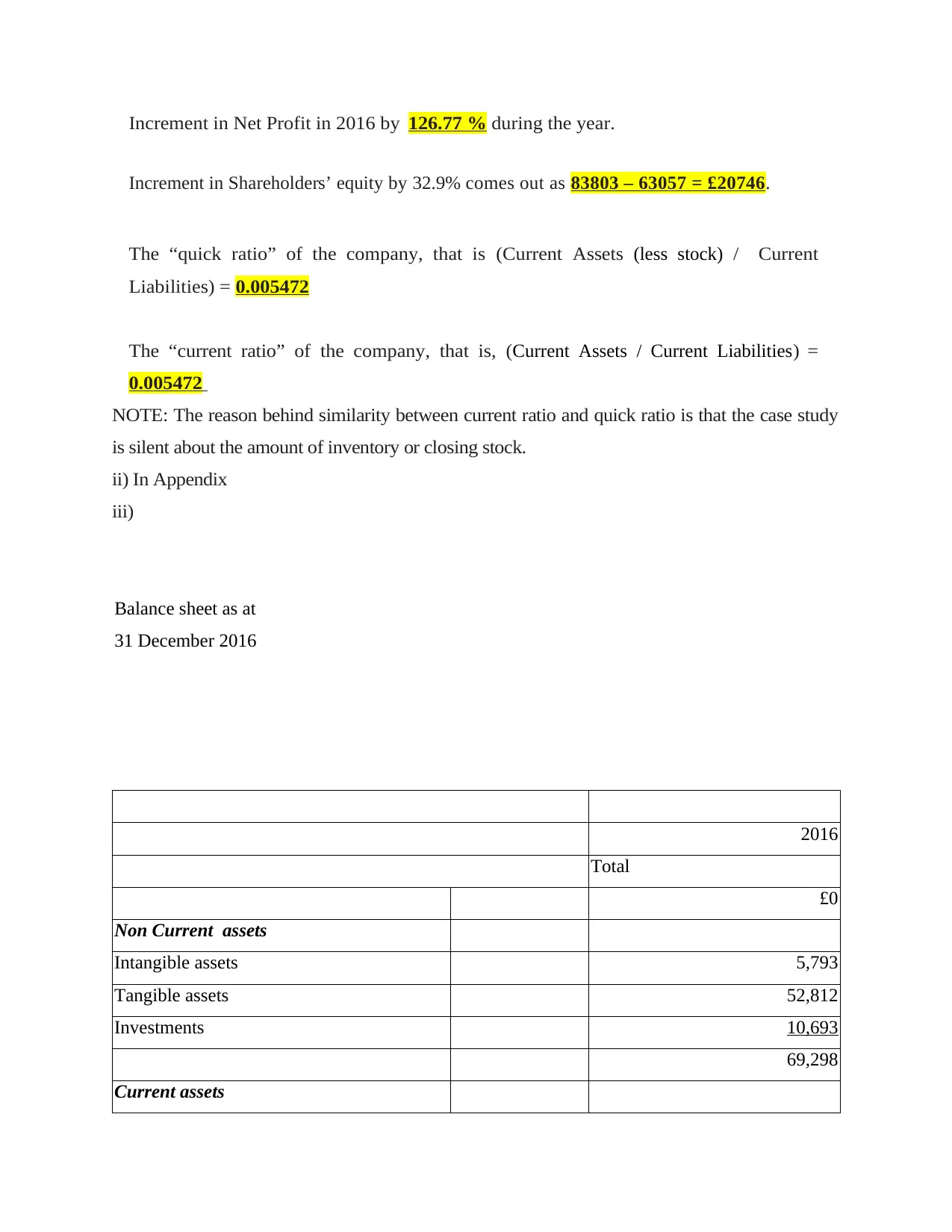

Increment in Net Profit in 2016 by 126.77 % during the year.

Increment in Shareholders’ equity by 32.9% comes out as 83803 – 63057 = £20746.

The “quick ratio” of the company, that is (Current Assets (less stock) / Current

Liabilities) = 0.005472

The “current ratio” of the company, that is, (Current Assets / Current Liabilities ) =

0.005472

NOTE: The reason behind similarity between current ratio and quick ratio is that the case study

is silent about the amount of inventory or closing stock.

ii) In Appendix

iii)

Balance sheet as at

31 December 2016

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Increment in Shareholders’ equity by 32.9% comes out as 83803 – 63057 = £20746.

The “quick ratio” of the company, that is (Current Assets (less stock) / Current

Liabilities) = 0.005472

The “current ratio” of the company, that is, (Current Assets / Current Liabilities ) =

0.005472

NOTE: The reason behind similarity between current ratio and quick ratio is that the case study

is silent about the amount of inventory or closing stock.

ii) In Appendix

iii)

Balance sheet as at

31 December 2016

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

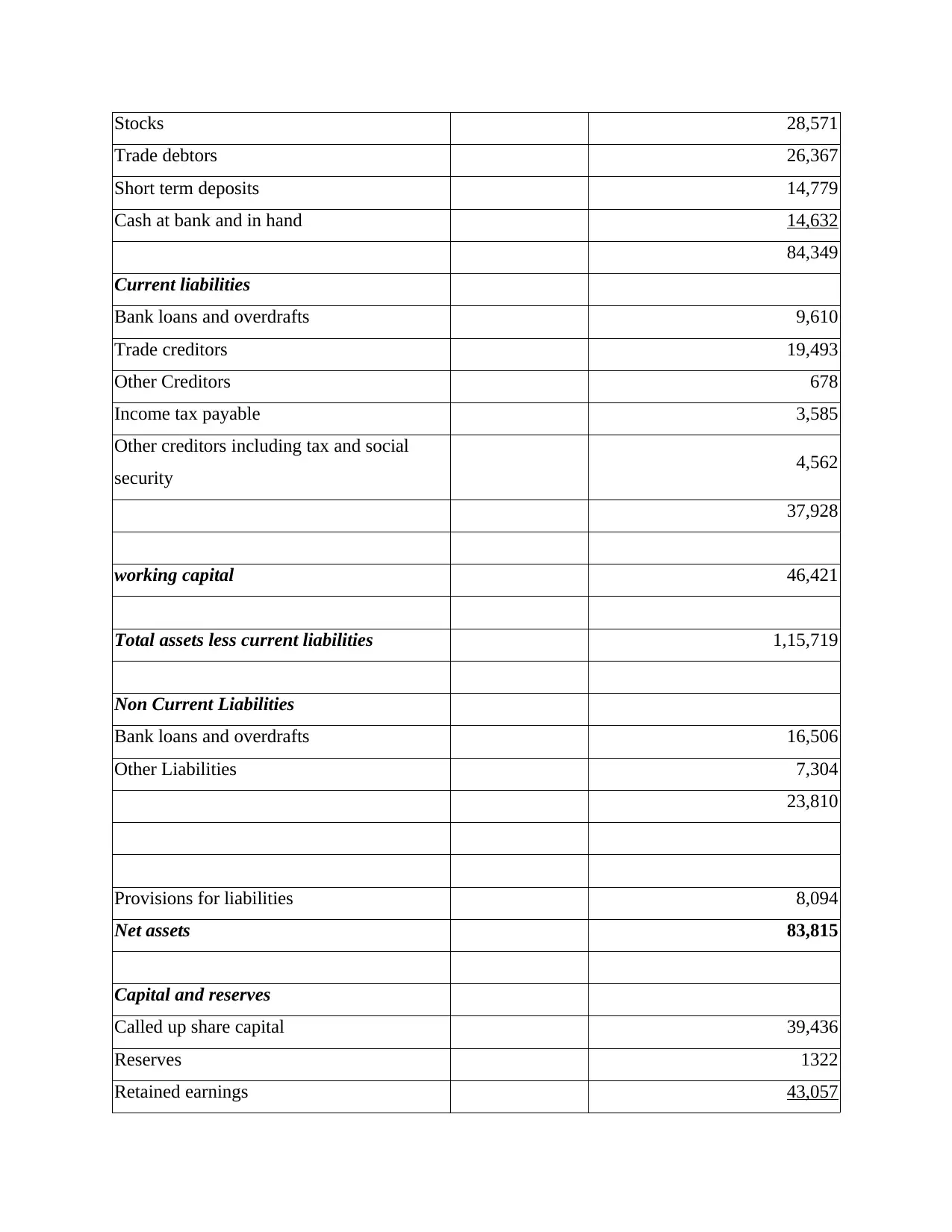

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors including tax and social

security 4,562

37,928

working capital 46,421

Total assets less current liabilities 1,15,719

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors including tax and social

security 4,562

37,928

working capital 46,421

Total assets less current liabilities 1,15,719

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,815

iv) Analysis of company's profitability, liquidity and efficiency with the help of ratio analysis

Profitability analysis of a company: The financial performance of the company as indicated

within the case study is quite stable in terms of gross profit margin. Whatever the fluctuations are

reflected are minor and also a favourable one (Rocchi, Ferrero and Beadle, 2021). As the

company's sales has increased as indicated by turnover of the company, there are increments in

the gross profit margin of the company. Also, there are huge increments in the amount of net

profit generated by the company due to lower overhead costs incurred within the company in the

current year as indicated by lower operating and non-operating costs (interest expenses).

Liquidity analysis of a company: Liquidity of the company can be well seen through its current

and quick ratio. With reference to the company in the case study, there seems a very sharp fall in

the liquidity position of the company. These ratios are indicating company inability to meet their

obligations that are going to arise within a period of one which necessarily required enough

liquid assets against the balance in current liabilities. Both in the previous and current year,

company doesn't have a favourable liquidity position (Salman and Jamil, 2017). As the current

ratio of the company get lowered by 82% in the current year than what it was in previous year

leads to the condition where a company is having a very high current ratio than required to meet

its current liability in the previous year; and in the current year, the current ratio of the company

has lowered down to such low level making it unsuitable for meeting its short term obligations.

Efficiency analysis of a company: The major reduction in the company's non-operating and

operating expenses is the biggest indicator of company's improved efficiency. Lower cost of

operations allows for higher efficiency within the company due to which there are chances of

higher profitability (Maxwell, 2017). In the case study given, it can be seen that the company's

net profit has increased due to higher efficiency in terms of reduced non-operating and operating

costs. Thus, it can be concluded that there are improvements in the overall efficiency of the

company. Also, an increased satisfaction to customer is an indicator of improved efficiency

within the company, as now with reduced costs the company can offer its products in the market

at lower rates which would accordingly results in higher benefits and higher satisfaction to

customers.

iv) Analysis of company's profitability, liquidity and efficiency with the help of ratio analysis

Profitability analysis of a company: The financial performance of the company as indicated

within the case study is quite stable in terms of gross profit margin. Whatever the fluctuations are

reflected are minor and also a favourable one (Rocchi, Ferrero and Beadle, 2021). As the

company's sales has increased as indicated by turnover of the company, there are increments in

the gross profit margin of the company. Also, there are huge increments in the amount of net

profit generated by the company due to lower overhead costs incurred within the company in the

current year as indicated by lower operating and non-operating costs (interest expenses).

Liquidity analysis of a company: Liquidity of the company can be well seen through its current

and quick ratio. With reference to the company in the case study, there seems a very sharp fall in

the liquidity position of the company. These ratios are indicating company inability to meet their

obligations that are going to arise within a period of one which necessarily required enough

liquid assets against the balance in current liabilities. Both in the previous and current year,

company doesn't have a favourable liquidity position (Salman and Jamil, 2017). As the current

ratio of the company get lowered by 82% in the current year than what it was in previous year

leads to the condition where a company is having a very high current ratio than required to meet

its current liability in the previous year; and in the current year, the current ratio of the company

has lowered down to such low level making it unsuitable for meeting its short term obligations.

Efficiency analysis of a company: The major reduction in the company's non-operating and

operating expenses is the biggest indicator of company's improved efficiency. Lower cost of

operations allows for higher efficiency within the company due to which there are chances of

higher profitability (Maxwell, 2017). In the case study given, it can be seen that the company's

net profit has increased due to higher efficiency in terms of reduced non-operating and operating

costs. Thus, it can be concluded that there are improvements in the overall efficiency of the

company. Also, an increased satisfaction to customer is an indicator of improved efficiency

within the company, as now with reduced costs the company can offer its products in the market

at lower rates which would accordingly results in higher benefits and higher satisfaction to

customers.

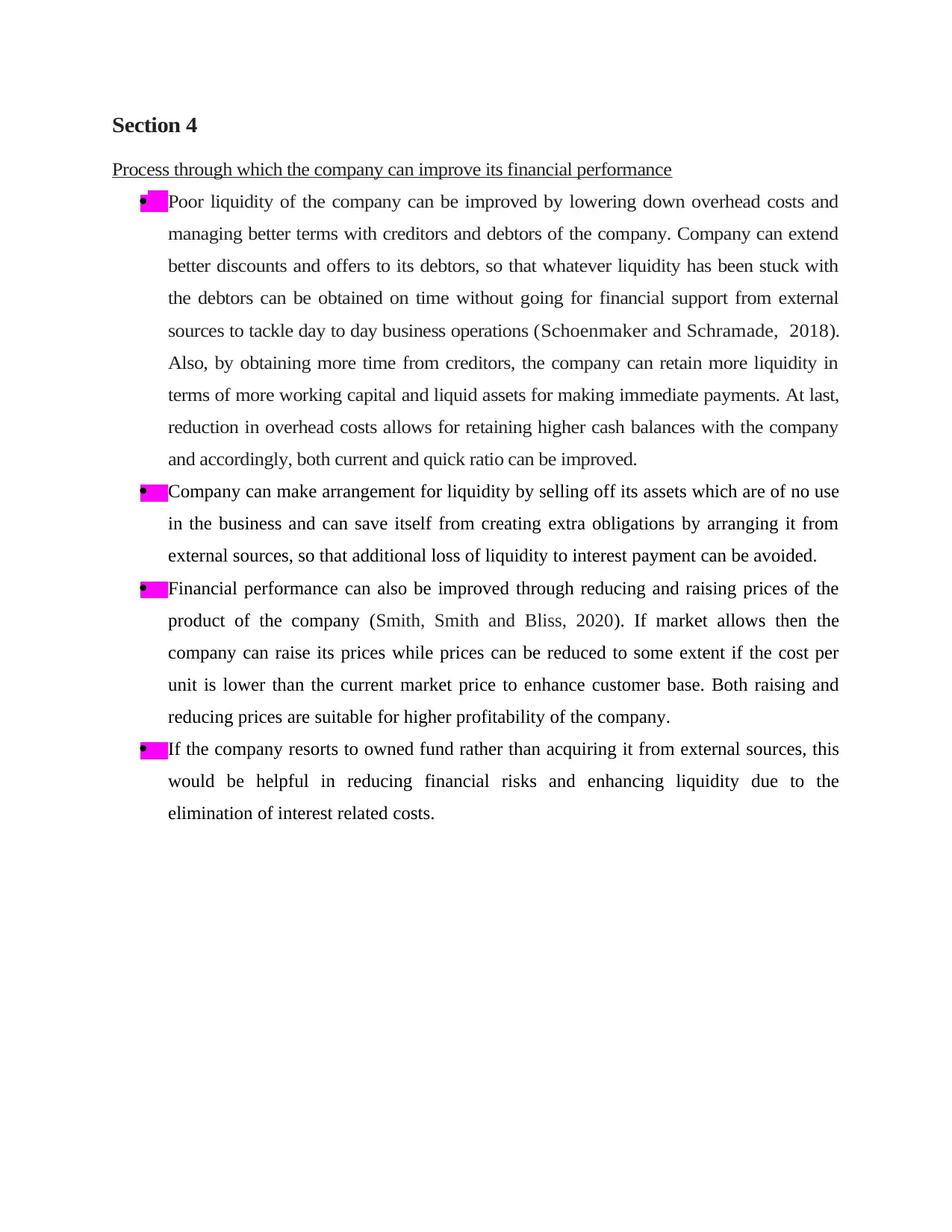

Section 4

Process through which the company can improve its financial performance

Poor liquidity of the company can be improved by lowering down overhead costs and

managing better terms with creditors and debtors of the company. Company can extend

better discounts and offers to its debtors, so that whatever liquidity has been stuck with

the debtors can be obtained on time without going for financial support from external

sources to tackle day to day business operations (Schoenmaker and Schramade, 2018).

Also, by obtaining more time from creditors, the company can retain more liquidity in

terms of more working capital and liquid assets for making immediate payments. At last,

reduction in overhead costs allows for retaining higher cash balances with the company

and accordingly, both current and quick ratio can be improved.

Company can make arrangement for liquidity by selling off its assets which are of no use

in the business and can save itself from creating extra obligations by arranging it from

external sources, so that additional loss of liquidity to interest payment can be avoided.

Financial performance can also be improved through reducing and raising prices of the

product of the company (Smith, Smith and Bliss, 2020). If market allows then the

company can raise its prices while prices can be reduced to some extent if the cost per

unit is lower than the current market price to enhance customer base. Both raising and

reducing prices are suitable for higher profitability of the company.

If the company resorts to owned fund rather than acquiring it from external sources, this

would be helpful in reducing financial risks and enhancing liquidity due to the

elimination of interest related costs.

Process through which the company can improve its financial performance

Poor liquidity of the company can be improved by lowering down overhead costs and

managing better terms with creditors and debtors of the company. Company can extend

better discounts and offers to its debtors, so that whatever liquidity has been stuck with

the debtors can be obtained on time without going for financial support from external

sources to tackle day to day business operations (Schoenmaker and Schramade, 2018).

Also, by obtaining more time from creditors, the company can retain more liquidity in

terms of more working capital and liquid assets for making immediate payments. At last,

reduction in overhead costs allows for retaining higher cash balances with the company

and accordingly, both current and quick ratio can be improved.

Company can make arrangement for liquidity by selling off its assets which are of no use

in the business and can save itself from creating extra obligations by arranging it from

external sources, so that additional loss of liquidity to interest payment can be avoided.

Financial performance can also be improved through reducing and raising prices of the

product of the company (Smith, Smith and Bliss, 2020). If market allows then the

company can raise its prices while prices can be reduced to some extent if the cost per

unit is lower than the current market price to enhance customer base. Both raising and

reducing prices are suitable for higher profitability of the company.

If the company resorts to owned fund rather than acquiring it from external sources, this

would be helpful in reducing financial risks and enhancing liquidity due to the

elimination of interest related costs.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Rocchi, M., Ferrero, I. and Beadle, R., 2021. Can finance be a virtuous practice? A MacIntyrean

account. Business Ethics Quarterly, 31(1), pp.75-105.

Salman, A. and Jamil, S., 2017. Entrepreneurial Finance and its Impact on e-Business. Problems

and perspectives in management, (15, Iss. 3), pp.24-41.

Maxwell, D., 2017. Valuing natural capital: Future proofing business and finance. Routledge.

Schoenmaker, D. and Schramade, W., 2018. Principles of sustainable finance. Oxford

University Press.

Smith, J. K., Smith, R. L. and Bliss, R. T., 2020. Entrepreneurial finance. Stanford University

Press.

Yang, L., 2021. Auditor or Adviser? Auditor (In) Dependence and Its Impact on Financial

Management. Public Administration Review. 81(3). pp.475-487.

Ferdiana, R. and Sulistyo, S., 2019. The role of information technology usage on startup

financial management and taxation. Procedia Computer Science. 161. pp.1308-1315.

Chmutova, I., Vovk, V. and Bezrodna, O., 2017. Analytical tools to implement integrated bank

financial management technologies. Economic annals-XXI. (163). pp.95-99.

Karadag, H., 2017. The impact of industry, firm age and education level on financial

management performance in small and medium-sized enterprises (SMEs): Evidence

from Turkey. Journal of Entrepreneurship in Emerging Economies.

Cashin, C. and et.al., 2017. Aligning public financial management and health financing:

sustaining progress toward universal health coverage (No.

WHO/HIS/HGF/HFWorkingPaper/17.4). World Health Organization.

Books and Journals

Rocchi, M., Ferrero, I. and Beadle, R., 2021. Can finance be a virtuous practice? A MacIntyrean

account. Business Ethics Quarterly, 31(1), pp.75-105.

Salman, A. and Jamil, S., 2017. Entrepreneurial Finance and its Impact on e-Business. Problems

and perspectives in management, (15, Iss. 3), pp.24-41.

Maxwell, D., 2017. Valuing natural capital: Future proofing business and finance. Routledge.

Schoenmaker, D. and Schramade, W., 2018. Principles of sustainable finance. Oxford

University Press.

Smith, J. K., Smith, R. L. and Bliss, R. T., 2020. Entrepreneurial finance. Stanford University

Press.

Yang, L., 2021. Auditor or Adviser? Auditor (In) Dependence and Its Impact on Financial

Management. Public Administration Review. 81(3). pp.475-487.

Ferdiana, R. and Sulistyo, S., 2019. The role of information technology usage on startup

financial management and taxation. Procedia Computer Science. 161. pp.1308-1315.

Chmutova, I., Vovk, V. and Bezrodna, O., 2017. Analytical tools to implement integrated bank

financial management technologies. Economic annals-XXI. (163). pp.95-99.

Karadag, H., 2017. The impact of industry, firm age and education level on financial

management performance in small and medium-sized enterprises (SMEs): Evidence

from Turkey. Journal of Entrepreneurship in Emerging Economies.

Cashin, C. and et.al., 2017. Aligning public financial management and health financing:

sustaining progress toward universal health coverage (No.

WHO/HIS/HGF/HFWorkingPaper/17.4). World Health Organization.

APPENDIX

Section 3

ii)

Income statement for the year ended 31st

December 2016

2016

Turnover 3 189711

Less cost of sales:

Material Cost 42597

Production Cost 15231

Labour Cost 50758

108586

Gross profit 81125GP % = 42.8

Less Expenses:

Administrative expenses 13751

Other operating overheads 22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the financial year 43057NP %= 22.7

Section 3

ii)

Income statement for the year ended 31st

December 2016

2016

Turnover 3 189711

Less cost of sales:

Material Cost 42597

Production Cost 15231

Labour Cost 50758

108586

Gross profit 81125GP % = 42.8

Less Expenses:

Administrative expenses 13751

Other operating overheads 22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the financial year 43057NP %= 22.7

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.