Comprehensive Financial Analysis: Ratios and Business Performance

VerifiedAdded on 2023/06/10

|12

|2900

|66

Report

AI Summary

This report delves into the significance of financial management and its pivotal role in achieving an organization's objectives. It emphasizes the importance of financial statement analysis, specifically focusing on profitability, efficiency, and liquidity through the lens of financial ratios derived from provided income statements. Calculations within the appendix support the analysis, which assesses a company's performance based on sales growth and profit margins. Liquidity is evaluated using current and quick ratios, while business effectiveness is gauged via asset and stock turnover. The report concludes by suggesting strategies to enhance business performance, such as optimizing the gap between accounts receivable and payable, and accelerating stock turnover. Desklib offers a platform to explore similar assignments and study resources.

top17492 3005

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

The Importance of Financial Management:.................................................................................1

The following are some examples of how to use financial statements and ratios:......................1

Performance of the business is assessed:.....................................................................................6

Strategies for boosting business performance.............................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

Appendix:......................................................................................................................................10

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

The Importance of Financial Management:.................................................................................1

The following are some examples of how to use financial statements and ratios:......................1

Performance of the business is assessed:.....................................................................................6

Strategies for boosting business performance.............................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

Appendix:......................................................................................................................................10

INTRODUCTION

The technique of managing financial resources to fulfil an association's cooperative goal is

known as financial management (Bouveret, 2018). This research relies on the idea of financial

management and also the importance of financial management. This research provides financial

ratio for a variety of financial amounts. Furthermore, via an examination of the information

obtained, this study focuses on the profitability, efficacy, and availability of the income

statement provided in the case. In the appendix, you'll find all of the essential calculations.

MAIN BODY

The Importance of Financial Management:

Financial management empowers an enterprise to satisfy the financing needs of regular

business operational activities by ensuring the firm's survivability after having met shareholder

expectations, by ensuring a sufficient supply of financial resources, management of financing for

short and long-term investing activities, and ensuring the firm's effectiveness after achieving

shareholder needs. Financial management establishes a company's optimal investing

structure that comprises the right balance of debt and equity. In terms of financial management, a

company can discover the best financial risk management strategies. The following are important

areas of financial management:

Potential investors of the company may make the best investment decision based on the

financial management's decision (Eka, 2018).

Financial management enables a business to give reliable information to a loan facility or

to taxation administrators.

Through strong finance administration, a corporation can carry on accountancy activities

for the organization's long-term aims.

A corporation's financial manager can employ financial management to find the best

source of cash with the least financing costs.

Financial management enables a corporation to generate aggregate outputs which

appropriately reflect the firm's quantitative success.

The following are some examples of how to use financial statements and ratios:

Balance sheet:

The technique of managing financial resources to fulfil an association's cooperative goal is

known as financial management (Bouveret, 2018). This research relies on the idea of financial

management and also the importance of financial management. This research provides financial

ratio for a variety of financial amounts. Furthermore, via an examination of the information

obtained, this study focuses on the profitability, efficacy, and availability of the income

statement provided in the case. In the appendix, you'll find all of the essential calculations.

MAIN BODY

The Importance of Financial Management:

Financial management empowers an enterprise to satisfy the financing needs of regular

business operational activities by ensuring the firm's survivability after having met shareholder

expectations, by ensuring a sufficient supply of financial resources, management of financing for

short and long-term investing activities, and ensuring the firm's effectiveness after achieving

shareholder needs. Financial management establishes a company's optimal investing

structure that comprises the right balance of debt and equity. In terms of financial management, a

company can discover the best financial risk management strategies. The following are important

areas of financial management:

Potential investors of the company may make the best investment decision based on the

financial management's decision (Eka, 2018).

Financial management enables a business to give reliable information to a loan facility or

to taxation administrators.

Through strong finance administration, a corporation can carry on accountancy activities

for the organization's long-term aims.

A corporation's financial manager can employ financial management to find the best

source of cash with the least financing costs.

Financial management enables a corporation to generate aggregate outputs which

appropriately reflect the firm's quantitative success.

The following are some examples of how to use financial statements and ratios:

Balance sheet:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

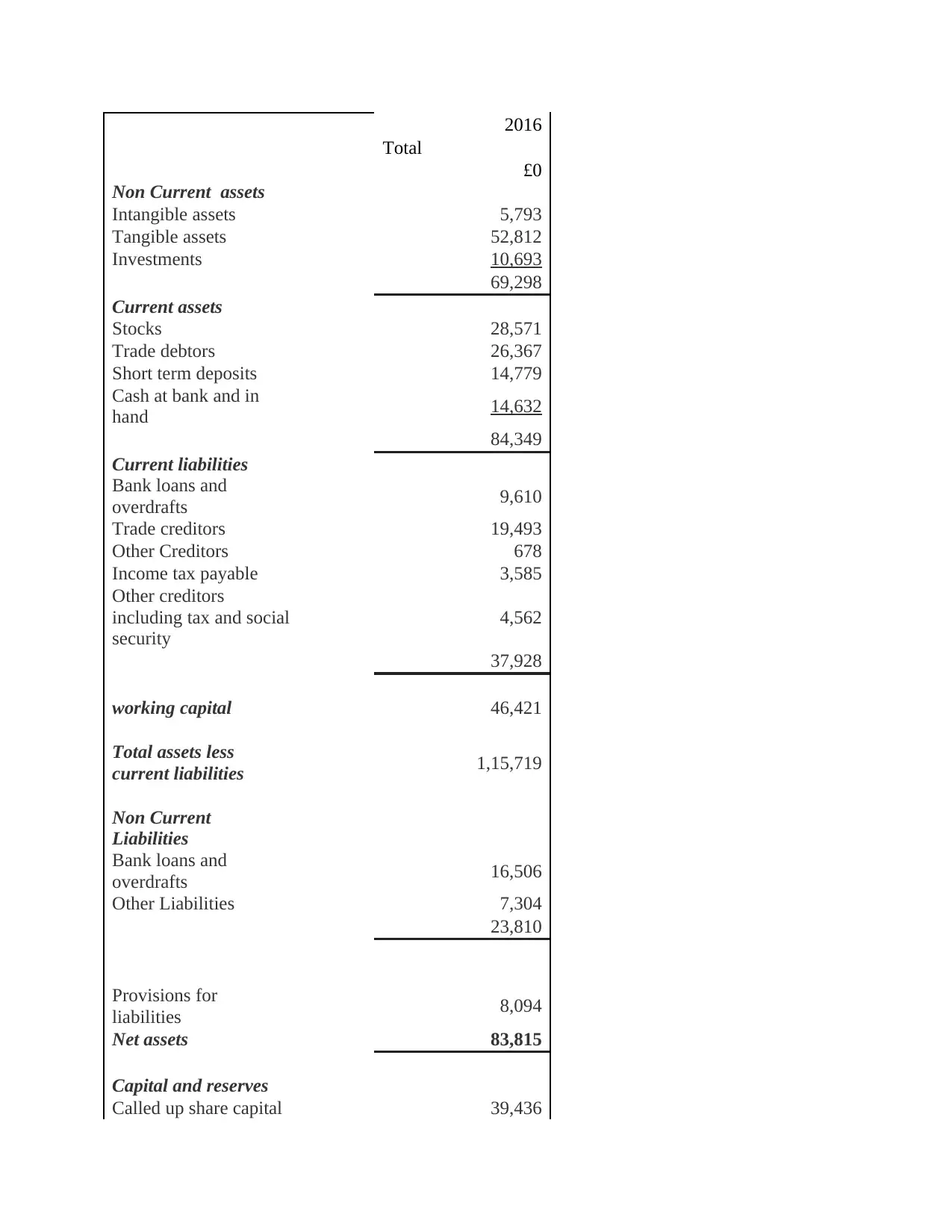

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Current liabilities

Bank loans and

overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors

including tax and social

security

4,562

37,928

working capital 46,421

Total assets less

current liabilities 1,15,719

Non Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for

liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Current liabilities

Bank loans and

overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors

including tax and social

security

4,562

37,928

working capital 46,421

Total assets less

current liabilities 1,15,719

Non Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for

liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

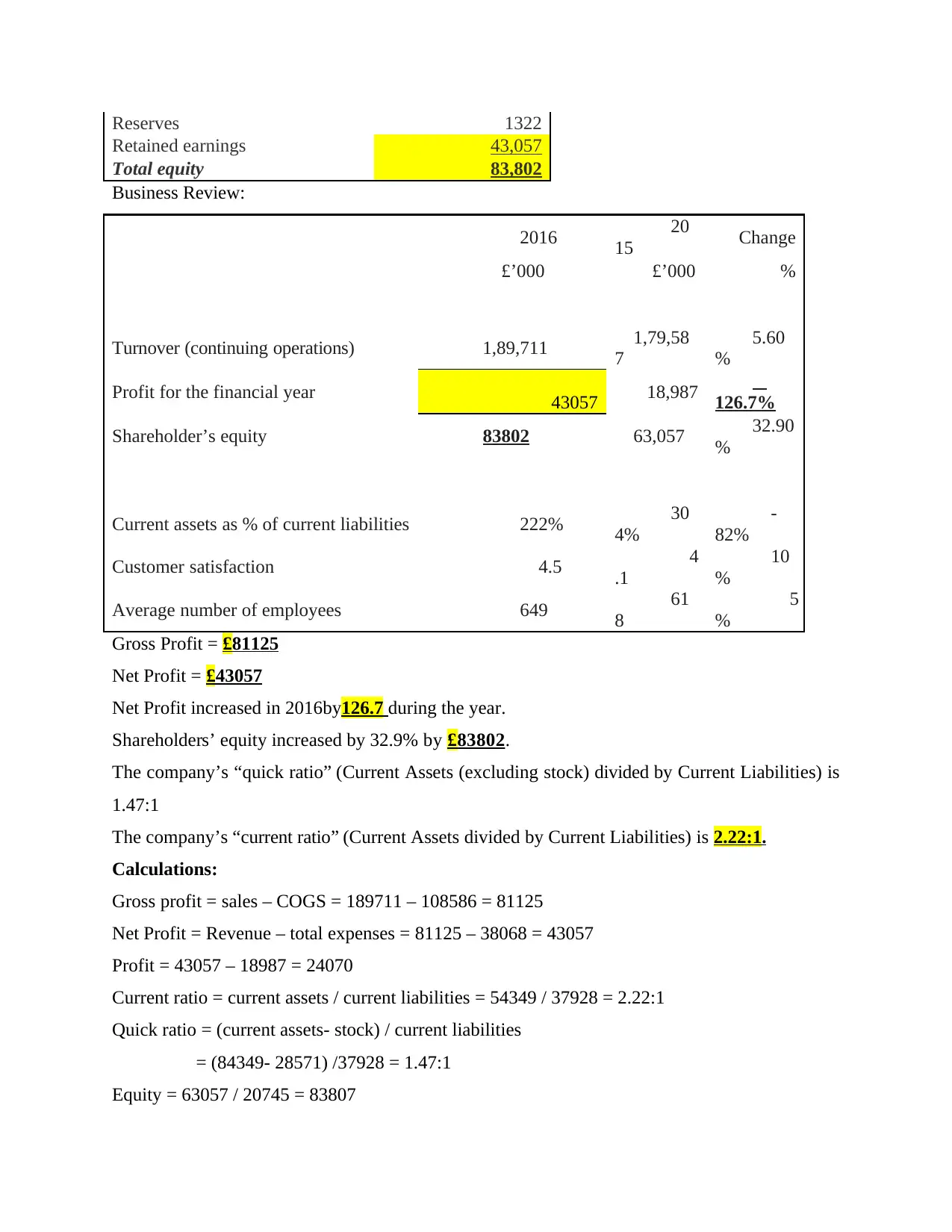

Reserves 1322

Retained earnings 43,057

Total equity 83,802

Business Review:

2016 20

15 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711 1,79,58

7

5.60

%

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802 63,057 32.90

%

Current assets as % of current liabilities 222% 30

4%

-

82%

Customer satisfaction 4.5 4

.1

10

%

Average number of employees 649 61

8

5

%

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016by126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is

1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities) is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Retained earnings 43,057

Total equity 83,802

Business Review:

2016 20

15 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711 1,79,58

7

5.60

%

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802 63,057 32.90

%

Current assets as % of current liabilities 222% 30

4%

-

82%

Customer satisfaction 4.5 4

.1

10

%

Average number of employees 649 61

8

5

%

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016by126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is

1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities) is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

Varied types of financial statements are produced to meet different budgetary

requirements for good finance management (Gomber, Koch and Siering, 2017). The much more

significant financial statements are the income statement, balance sheet, and cash flow assertion.

Ratio analysis from income statements, in especially, can be utilised to assess efficiency,

liquidity, sustainability, and other financial factors for successful financial preparation and thus

below are those financial statements elaborated:

Income Statement: It is a financial account which summarises an organization's earnings

and expenses in order to determine profit and loss. The income statement is also known as profit

and loss statement. There are three main parts to the income statement. The first part is referred

to as revenue, and it entails multiplying aggregate selling by the vendor's worth to get at

advertising revenues. All types of revenue are accumulated, and all expenses are eliminated, to

create a profit or loss over a specified time period, including a year. Such technique can be

employed to determine a profit or loss over a period of duration. After reducing the expenditures

from the gross margin, the operating revenue might be computed (Henager and Cude, 2016).

Balance sheet: It is a financial statement that shows an organisation's assets, liabilities,

and equities in order to assess the corporation's financial position throughout time. For an

appropriate balance sheet, the asset portion of the balance sheet should equal the liabilities side

of the company's balance sheet. The balance sheet can reveal the corporation's fiscal structure by

revealing the amount of shorter and longer run loans, and also the quantity of shareholder

participation.

Cash flow statement: It is a financial report which thus indicates how much funds a

business has with its inflow and outflow whilst an aggregate calculation could be created that

will benefit the business in the long term. The statement of cash flow has three components. The

3 kinds of cash flow that are covered in the statement of cash flows are operational cash flow,

investment cash flow, and finance cash flow. The operational cash flow sector contains cash

inflows and outflows from operational activities, whereas the investment cash flow section

contains the volume of money invested on different projects and capital instruments, and also the

revenue return on spending. To create overall finance in the financial cash flow, it is necessary to

calculate how much income is generated from different sources of investment and cash outflow.

Varied types of financial statements are produced to meet different budgetary

requirements for good finance management (Gomber, Koch and Siering, 2017). The much more

significant financial statements are the income statement, balance sheet, and cash flow assertion.

Ratio analysis from income statements, in especially, can be utilised to assess efficiency,

liquidity, sustainability, and other financial factors for successful financial preparation and thus

below are those financial statements elaborated:

Income Statement: It is a financial account which summarises an organization's earnings

and expenses in order to determine profit and loss. The income statement is also known as profit

and loss statement. There are three main parts to the income statement. The first part is referred

to as revenue, and it entails multiplying aggregate selling by the vendor's worth to get at

advertising revenues. All types of revenue are accumulated, and all expenses are eliminated, to

create a profit or loss over a specified time period, including a year. Such technique can be

employed to determine a profit or loss over a period of duration. After reducing the expenditures

from the gross margin, the operating revenue might be computed (Henager and Cude, 2016).

Balance sheet: It is a financial statement that shows an organisation's assets, liabilities,

and equities in order to assess the corporation's financial position throughout time. For an

appropriate balance sheet, the asset portion of the balance sheet should equal the liabilities side

of the company's balance sheet. The balance sheet can reveal the corporation's fiscal structure by

revealing the amount of shorter and longer run loans, and also the quantity of shareholder

participation.

Cash flow statement: It is a financial report which thus indicates how much funds a

business has with its inflow and outflow whilst an aggregate calculation could be created that

will benefit the business in the long term. The statement of cash flow has three components. The

3 kinds of cash flow that are covered in the statement of cash flows are operational cash flow,

investment cash flow, and finance cash flow. The operational cash flow sector contains cash

inflows and outflows from operational activities, whereas the investment cash flow section

contains the volume of money invested on different projects and capital instruments, and also the

revenue return on spending. To create overall finance in the financial cash flow, it is necessary to

calculate how much income is generated from different sources of investment and cash outflow.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The cash flow report can be employed to assess the company's monetary health (Ivanovich,

2020).

Financial Ratios Assessment: Financial ratios can be used to quickly assess the financial

position and direction of a company. Financial ratios can provide the following fundamental

company objectives:

Financial ratios can be employed to evaluate a company's financial and competitive risk.

Financial ratios can be used to examine the similar monetary position throughout the year

and in comparison to certain other companies in the industry.

Financial ratios can be used to analyse and compare a company's production and

effectiveness to its goal.

Disadvantages:

The evaluation of financial ratios would not reflect operating efficiency.

Financial ratios cannot be used to compare two businesses of different capacities.

The ratios analysis did not factor into consideration the company's price volatility

indicator.

The following are some of the most essential financial ratios:

Solvency ratios: These are indicators which are used to assess a company's capability to

meet long-term obligations and are an important indicator of its commercial feasibility.

From a variety of solvency ratios, the debt ratio, equity ratio, and debt to equity ratio are

the two most essential ones.

Profitability ratios: These can be used to assess a firm's capability to generate revenue.

Sales, founder's stocks, and investment are all aspects that go into determining revenue.

The appropriate ratios are calculated in practise, and they are as follows: The ratios

employed to characterize a corporation's fiscal success include gross income margins,

operational income margin, net profitability margin, return on capital employed, return on

assets, return on selling, and return on investments (Kwilinskyi, Shteingauz and Maslov,

2020).

Efficiency ratio: This metric can be applied to evaluate a company's operating

effectiveness in terms of creating revenue via effective resource utilisation. Receivable

turnover ratio, asset turnover ratio, and inventory turnover ratio are efficiency ratios

2020).

Financial Ratios Assessment: Financial ratios can be used to quickly assess the financial

position and direction of a company. Financial ratios can provide the following fundamental

company objectives:

Financial ratios can be employed to evaluate a company's financial and competitive risk.

Financial ratios can be used to examine the similar monetary position throughout the year

and in comparison to certain other companies in the industry.

Financial ratios can be used to analyse and compare a company's production and

effectiveness to its goal.

Disadvantages:

The evaluation of financial ratios would not reflect operating efficiency.

Financial ratios cannot be used to compare two businesses of different capacities.

The ratios analysis did not factor into consideration the company's price volatility

indicator.

The following are some of the most essential financial ratios:

Solvency ratios: These are indicators which are used to assess a company's capability to

meet long-term obligations and are an important indicator of its commercial feasibility.

From a variety of solvency ratios, the debt ratio, equity ratio, and debt to equity ratio are

the two most essential ones.

Profitability ratios: These can be used to assess a firm's capability to generate revenue.

Sales, founder's stocks, and investment are all aspects that go into determining revenue.

The appropriate ratios are calculated in practise, and they are as follows: The ratios

employed to characterize a corporation's fiscal success include gross income margins,

operational income margin, net profitability margin, return on capital employed, return on

assets, return on selling, and return on investments (Kwilinskyi, Shteingauz and Maslov,

2020).

Efficiency ratio: This metric can be applied to evaluate a company's operating

effectiveness in terms of creating revenue via effective resource utilisation. Receivable

turnover ratio, asset turnover ratio, and inventory turnover ratio are efficiency ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which are widely employed in the marketplace and are thus employed by businesses to

measure and analyse their general effectiveness in the big scheme of things.

Coverage ratio: This metric assesses a firm's financial ability to repay its borrowing and

payment obligations. The higher the coverage ratio, the stronger the group's ability to pay

back the borrowing's interest and other fiscal obligations. The most widely utilised

coverage ratios by businesses are the interest coverage ratio, debt service coverage ratio,

asset coverage ratio.

Liquidity ratios: They are financial measurements which assess a corporation's financial

status, especially its ability to settle short-term debts. The most relevant ratios are the

current and quick ratio.

Performance of the business is assessed:

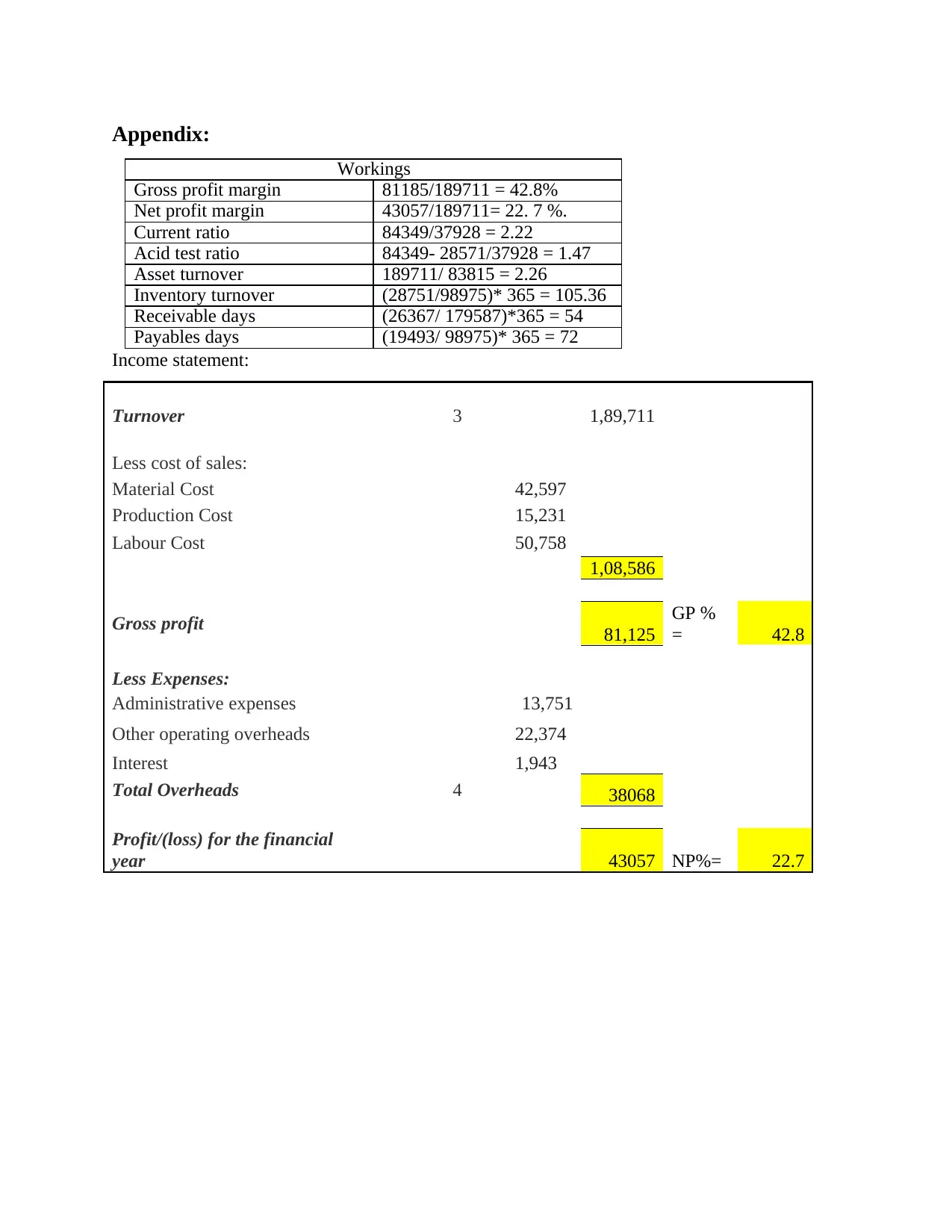

The study sample linked to the excel worksheet in the appendix shows the related firm

performance evaluation:

Performance of the corporation: At the end of 2015, sales were 18,987, and by the end

of 2016, sales had risen to 43057. As a consequence, profit percentages increase by 127%

annually. This indicates that the organisation is performing really well. As per the estimates, the

gross revenue ratio is 42.8 percentage, whereas the net profit ratio is 22.7 percent. It

demonstrates that the company generates a gross profit margin of £ 42.8 for every £ 100

supplied, and a profit margin of £ 22.7 for every £ 100 traded. Whenever it relates to evaluating

effectiveness, the higher the figure, the better it is in the foreseeable future. As a consequence,

the business may be considered successful (Levy, Bouheni and Ammi, 2018).

Liquidity of the corporation: The current ratio and the acid test ratio are being employed

to assess a firm's fiscal viability. The assessment indicates that the company seems to have

enough cash on hand to cover its short-term liabilities. The company does have a £ 2.22 asset for

every £1 in indebtedness, according to this calculation. Moreover, we can infer that the firm

seems to have a £ 1.47 asset for every $ 1 liability if we examine more liquid assets and

eliminate inventories from current assets. This might also be interpreted as the company not

possessing far too much cash in reserve and rather putting it to good use in the foreseeable.

Business’s effectiveness: Asset turnover is a ratio which measures how effectively a

corporation utilises its resources. As per the estimates, the asset turnover ratio in this scenario is

2.26. An asset turnover ratio of 2.5 is considered a good performance. In this scenario, the asset

measure and analyse their general effectiveness in the big scheme of things.

Coverage ratio: This metric assesses a firm's financial ability to repay its borrowing and

payment obligations. The higher the coverage ratio, the stronger the group's ability to pay

back the borrowing's interest and other fiscal obligations. The most widely utilised

coverage ratios by businesses are the interest coverage ratio, debt service coverage ratio,

asset coverage ratio.

Liquidity ratios: They are financial measurements which assess a corporation's financial

status, especially its ability to settle short-term debts. The most relevant ratios are the

current and quick ratio.

Performance of the business is assessed:

The study sample linked to the excel worksheet in the appendix shows the related firm

performance evaluation:

Performance of the corporation: At the end of 2015, sales were 18,987, and by the end

of 2016, sales had risen to 43057. As a consequence, profit percentages increase by 127%

annually. This indicates that the organisation is performing really well. As per the estimates, the

gross revenue ratio is 42.8 percentage, whereas the net profit ratio is 22.7 percent. It

demonstrates that the company generates a gross profit margin of £ 42.8 for every £ 100

supplied, and a profit margin of £ 22.7 for every £ 100 traded. Whenever it relates to evaluating

effectiveness, the higher the figure, the better it is in the foreseeable future. As a consequence,

the business may be considered successful (Levy, Bouheni and Ammi, 2018).

Liquidity of the corporation: The current ratio and the acid test ratio are being employed

to assess a firm's fiscal viability. The assessment indicates that the company seems to have

enough cash on hand to cover its short-term liabilities. The company does have a £ 2.22 asset for

every £1 in indebtedness, according to this calculation. Moreover, we can infer that the firm

seems to have a £ 1.47 asset for every $ 1 liability if we examine more liquid assets and

eliminate inventories from current assets. This might also be interpreted as the company not

possessing far too much cash in reserve and rather putting it to good use in the foreseeable.

Business’s effectiveness: Asset turnover is a ratio which measures how effectively a

corporation utilises its resources. As per the estimates, the asset turnover ratio in this scenario is

2.26. An asset turnover ratio of 2.5 is considered a good performance. In this scenario, the asset

turnover is 2.26, which implies the company employs its resources 2.26 times every year. Stock

turnover refers to the number of things delivered and replaced by a corporation in a given year.

The company's stock turnover is 105.36 days that indicates this would require 106 days to use

and replace the present stock. Days in receivables refers to the number of days a business should

await to collect its accounts receivable. The number 54 depicts the firm's average time to collect

accounts receivable, which is 54 days. Days in payables refers to the number of days a business

will have to settle its accounts payable. In this situation, the days are 72, suggesting that the

corporation needs 72 days to pay back its account payables. The greater the number of accounts

payable days a firm has, the better it is for its firm in the industry wherein it operates. On both

sides, the shorter the account receivable days, the better. In this case, the account receivable time

period is shorter than the accounts payable time period, indicating that the company is in good

shape (Maziriri, Mapuranga and Madinga, 2018).

Strategies for boosting business performance

The following strategy can be applied to boost business performance:

The gap between days of accounts receivable and days of accounts payable has to

broaden further in order to retain more currency in flow for a longer period of time.

Stock turnover ratio can be accelerated, enabling stock to be converted into finished items

in less time, leading to increased sales.

The company does have the capacity to reduce the added expenses it is incurring.

The organization's financial control has to be improved.

In an attempt to produce more revenue, the corporation can boost its standard price.

The corporation's marketing techniques can be improved in way to lure more clients. To

generate income, the company might use an electronic marketing platform and also

different promotional ideas to improve the marketing network (Sari and Fatimah, 2017).

CONCLUSION

Therefore, it may be argued from the foregoing that assessing financial efficiency is an

important part of financial management. Ratio analysis can also be used to evaluate superior

financial performance. The research could well be focused on the understanding of better

financial management as a result of the example survey evaluation, with the description and

calculation in the appendix part.

turnover refers to the number of things delivered and replaced by a corporation in a given year.

The company's stock turnover is 105.36 days that indicates this would require 106 days to use

and replace the present stock. Days in receivables refers to the number of days a business should

await to collect its accounts receivable. The number 54 depicts the firm's average time to collect

accounts receivable, which is 54 days. Days in payables refers to the number of days a business

will have to settle its accounts payable. In this situation, the days are 72, suggesting that the

corporation needs 72 days to pay back its account payables. The greater the number of accounts

payable days a firm has, the better it is for its firm in the industry wherein it operates. On both

sides, the shorter the account receivable days, the better. In this case, the account receivable time

period is shorter than the accounts payable time period, indicating that the company is in good

shape (Maziriri, Mapuranga and Madinga, 2018).

Strategies for boosting business performance

The following strategy can be applied to boost business performance:

The gap between days of accounts receivable and days of accounts payable has to

broaden further in order to retain more currency in flow for a longer period of time.

Stock turnover ratio can be accelerated, enabling stock to be converted into finished items

in less time, leading to increased sales.

The company does have the capacity to reduce the added expenses it is incurring.

The organization's financial control has to be improved.

In an attempt to produce more revenue, the corporation can boost its standard price.

The corporation's marketing techniques can be improved in way to lure more clients. To

generate income, the company might use an electronic marketing platform and also

different promotional ideas to improve the marketing network (Sari and Fatimah, 2017).

CONCLUSION

Therefore, it may be argued from the foregoing that assessing financial efficiency is an

important part of financial management. Ratio analysis can also be used to evaluate superior

financial performance. The research could well be focused on the understanding of better

financial management as a result of the example survey evaluation, with the description and

calculation in the appendix part.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Eka, H., 2018. Corporate finance and firm value in the Indonesian manufacturing

companies. BUSINESS STUDIES. 11(2). pp.113-127.

Gomber, P., Koch, J. A. and Siering, M., 2017. Digital Finance and FinTech: current research

and future research directions. Journal of Business Economics. 87(5). pp.537-580.

Henager, R. and Cude, B.J., 2016. Financial Literacy and Long-and Short-Term Financial

Behavior in Different Age Groups. Journal of Financial Counseling and Planning,

27(1), pp.3-19.

Ivanovich, K.K., 2020. About some questions of classification of institutional conditions

determining the structure of doing business in Uzbekistan. South Asian Journal of

Marketing & Management Research. 10(5). pp.17-28.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for

ensuring effective functioning of the residential real estate market.

Levy, A., Bouheni, F.B. and Ammi, C., 2018. Financial management: USGAAP and IFRS

Standards. John Wiley & Sons.

Maziriri, E. T., Mapuranga, M. and Madinga, N. W., 2018. Self-service banking and financial

literacy as prognosticators of business performance among rural small and medium-sized

enterprises in Zimbabwe. The Southern African Journal of Entrepreneurship and Small

Business Management. 10(1). p.10.

Sari, R.C. and Fatimah, P.R., 2017. Bringing voluntary financial education in emerging

economy: Role of financial socialization during elementary years. The Asia-Pacific

Education Researcher, 26(3), pp.183-192.

Books and journals

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Eka, H., 2018. Corporate finance and firm value in the Indonesian manufacturing

companies. BUSINESS STUDIES. 11(2). pp.113-127.

Gomber, P., Koch, J. A. and Siering, M., 2017. Digital Finance and FinTech: current research

and future research directions. Journal of Business Economics. 87(5). pp.537-580.

Henager, R. and Cude, B.J., 2016. Financial Literacy and Long-and Short-Term Financial

Behavior in Different Age Groups. Journal of Financial Counseling and Planning,

27(1), pp.3-19.

Ivanovich, K.K., 2020. About some questions of classification of institutional conditions

determining the structure of doing business in Uzbekistan. South Asian Journal of

Marketing & Management Research. 10(5). pp.17-28.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for

ensuring effective functioning of the residential real estate market.

Levy, A., Bouheni, F.B. and Ammi, C., 2018. Financial management: USGAAP and IFRS

Standards. John Wiley & Sons.

Maziriri, E. T., Mapuranga, M. and Madinga, N. W., 2018. Self-service banking and financial

literacy as prognosticators of business performance among rural small and medium-sized

enterprises in Zimbabwe. The Southern African Journal of Entrepreneurship and Small

Business Management. 10(1). p.10.

Sari, R.C. and Fatimah, P.R., 2017. Bringing voluntary financial education in emerging

economy: Role of financial socialization during elementary years. The Asia-Pacific

Education Researcher, 26(3), pp.183-192.

Appendix:

Workings

Gross profit margin 81185/189711 = 42.8%

Net profit margin 43057/189711= 22. 7 %.

Current ratio 84349/37928 = 2.22

Acid test ratio 84349- 28571/37928 = 1.47

Asset turnover 189711/ 83815 = 2.26

Inventory turnover (28751/98975)* 365 = 105.36

Receivable days (26367/ 179587)*365 = 54

Payables days (19493/ 98975)* 365 = 72

Income statement:

Turnover 3 1,89,711

Less cost of sales:

Material Cost 42,597

Production Cost 15,231

Labour Cost 50,758

1,08,586

Gross profit 81,125

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751

Other operating overheads 22,374

Interest 1,943

Total Overheads 4 38068

Profit/(loss) for the financial

year 43057 NP%= 22.7

Workings

Gross profit margin 81185/189711 = 42.8%

Net profit margin 43057/189711= 22. 7 %.

Current ratio 84349/37928 = 2.22

Acid test ratio 84349- 28571/37928 = 1.47

Asset turnover 189711/ 83815 = 2.26

Inventory turnover (28751/98975)* 365 = 105.36

Receivable days (26367/ 179587)*365 = 54

Payables days (19493/ 98975)* 365 = 72

Income statement:

Turnover 3 1,89,711

Less cost of sales:

Material Cost 42,597

Production Cost 15,231

Labour Cost 50,758

1,08,586

Gross profit 81,125

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751

Other operating overheads 22,374

Interest 1,943

Total Overheads 4 38068

Profit/(loss) for the financial

year 43057 NP%= 22.7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.