Financial Management Report: WACC, Investment and Bankruptcy Analysis

VerifiedAdded on 2021/02/19

|14

|3724

|29

Report

AI Summary

This report delves into the core principles of financial management, providing a detailed analysis of cost of capital, investment appraisal techniques, and their implications on business decisions. The report begins with the calculation of book and market values for equities and debts, determining growth rates using dividend data. It then proceeds to calculate the Weighted Average Cost of Capital (WACC) using both book and market values, followed by a recalculation based on revised data. A critical discussion on integrating capital structure changes is presented, evaluating the potential cost savings and market value impacts. Furthermore, the report critically evaluates the effects of short-termism on bankruptcy and agency problems, using real-world examples to illustrate the consequences of prioritizing short-term gains. The report also covers various investment appraisal techniques, including the payback period, accounting rate of return (ARR), and net present value (NPV), offering detailed calculations and analysis for each technique. The ARR calculation includes a depreciation analysis to determine the return on investment, while the NPV analysis provides a framework for determining the project's viability. The report concludes by summarizing the key findings and implications of financial management practices on a company's financial health and strategic decision-making process.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

a. Calculation of book value and market value............................................................................1

b. Recalculation of cost of capital of company............................................................................3

c. Critical discussion regarding integration of capital structure of the company........................4

d. Critical evaluation of the effect of short termism on bankruptcy and agency problem..........4

QUESTION 3..................................................................................................................................5

a. Calculation of different investment appraisal techniques........................................................5

b. Merits and demerits of different investment appraisal techniques..........................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

a. Calculation of book value and market value............................................................................1

b. Recalculation of cost of capital of company............................................................................3

c. Critical discussion regarding integration of capital structure of the company........................4

d. Critical evaluation of the effect of short termism on bankruptcy and agency problem..........4

QUESTION 3..................................................................................................................................5

a. Calculation of different investment appraisal techniques........................................................5

b. Merits and demerits of different investment appraisal techniques..........................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial management can be defined as the process which is used by business entities

for the purpose of maintaining monetary resources which are available to the company. For all

the organisations it is very important because it helps to use the funds in appropriate manner so

that long term business goals could be attained (Badolato, Donelson and Ege, 2014). In order to

enhance profitability of the enterprise it is very important to manage financial performance.

There are various techniques which are used for this purpose. One of them is ratio analysis which

helps to assess that the organisation is viable or not. This report covers various topics such as

analysis of cost of capital using WACC and assessment of long term finance of firms. Along

with this, various investment appraisal techniques which are used to form investment decisions

are also covered under this report.

QUESTION 1

a. Calculation of book value and market value

In order to calculate book value and market value for different equities and debts it is very

important to determine the growth rate each year so that the accurate value could be analysed.

For this purpose dividend of all the years is used (Baños-Caballero, García-Teruel and Martínez-

Solano, 2014)

. The calculation of growth rate is as follows:

Year Dividend for the year

First year 21

Second year 23

Third year 25

Fourth year 27

Fifth year 28

The formula for the growth is as follows:

Growth rate = S0*(1+g)n = Sn

:- 21 ( 1+ g ) 4 = 28

:- ( 1+ g ) 4 = 28 / 21

:- ( 1+ g ) = (1.333) 0.25

:- g = ( 1 ) – ( 1.0757 )

1

Financial management can be defined as the process which is used by business entities

for the purpose of maintaining monetary resources which are available to the company. For all

the organisations it is very important because it helps to use the funds in appropriate manner so

that long term business goals could be attained (Badolato, Donelson and Ege, 2014). In order to

enhance profitability of the enterprise it is very important to manage financial performance.

There are various techniques which are used for this purpose. One of them is ratio analysis which

helps to assess that the organisation is viable or not. This report covers various topics such as

analysis of cost of capital using WACC and assessment of long term finance of firms. Along

with this, various investment appraisal techniques which are used to form investment decisions

are also covered under this report.

QUESTION 1

a. Calculation of book value and market value

In order to calculate book value and market value for different equities and debts it is very

important to determine the growth rate each year so that the accurate value could be analysed.

For this purpose dividend of all the years is used (Baños-Caballero, García-Teruel and Martínez-

Solano, 2014)

. The calculation of growth rate is as follows:

Year Dividend for the year

First year 21

Second year 23

Third year 25

Fourth year 27

Fifth year 28

The formula for the growth is as follows:

Growth rate = S0*(1+g)n = Sn

:- 21 ( 1+ g ) 4 = 28

:- ( 1+ g ) 4 = 28 / 21

:- ( 1+ g ) = (1.333) 0.25

:- g = ( 1 ) – ( 1.0757 )

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

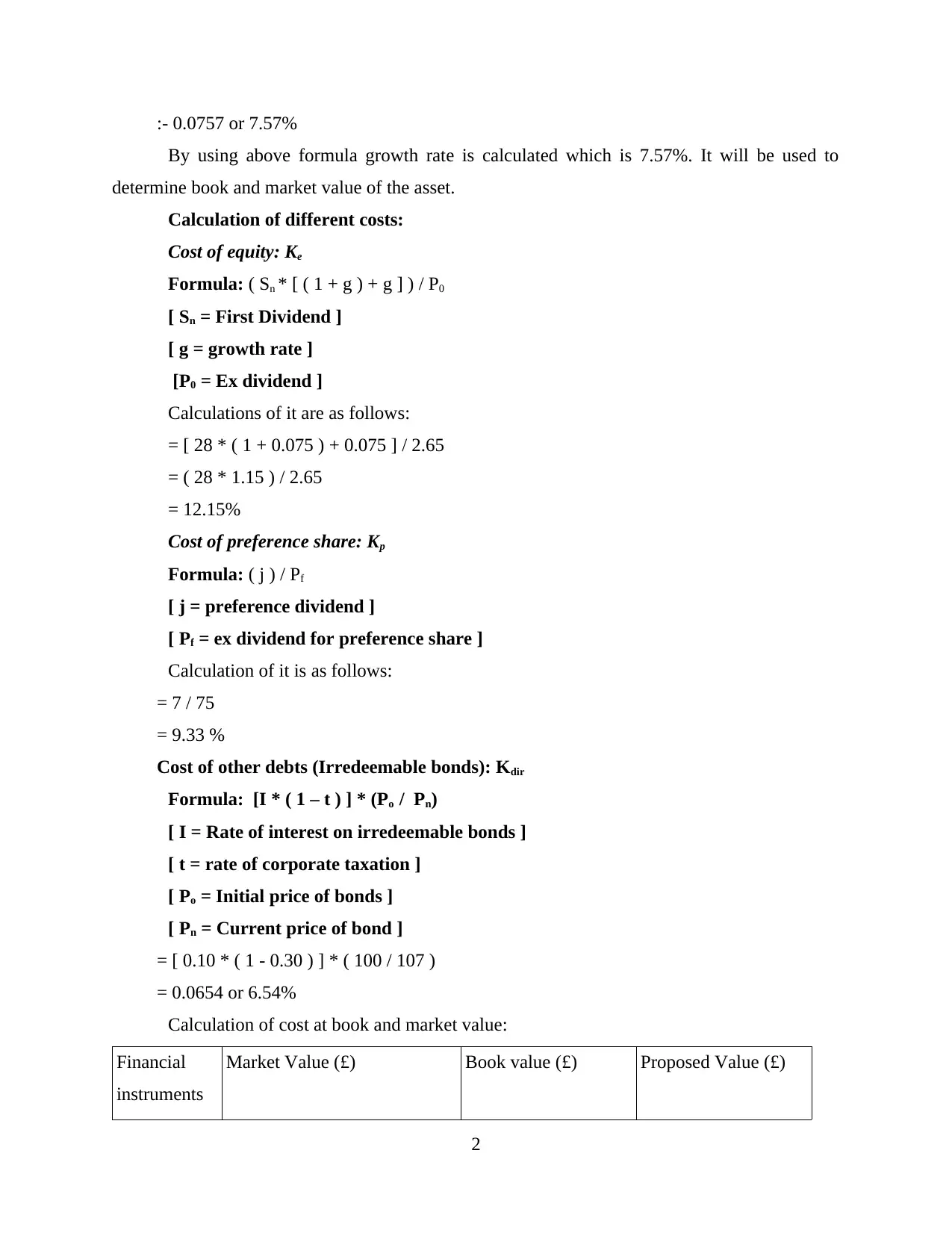

:- 0.0757 or 7.57%

By using above formula growth rate is calculated which is 7.57%. It will be used to

determine book and market value of the asset.

Calculation of different costs:

Cost of equity: Ke

Formula: ( Sn * [ ( 1 + g ) + g ] ) / P0

[ Sn = First Dividend ]

[ g = growth rate ]

[P0 = Ex dividend ]

Calculations of it are as follows:

= [ 28 * ( 1 + 0.075 ) + 0.075 ] / 2.65

= ( 28 * 1.15 ) / 2.65

= 12.15%

Cost of preference share: Kp

Formula: ( j ) / Pf

[ j = preference dividend ]

[ Pf = ex dividend for preference share ]

Calculation of it is as follows:

= 7 / 75

= 9.33 %

Cost of other debts (Irredeemable bonds): Kdir

Formula: [I * ( 1 – t ) ] * (Po / Pn)

[ I = Rate of interest on irredeemable bonds ]

[ t = rate of corporate taxation ]

[ Po = Initial price of bonds ]

[ Pn = Current price of bond ]

= [ 0.10 * ( 1 - 0.30 ) ] * ( 100 / 107 )

= 0.0654 or 6.54%

Calculation of cost at book and market value:

Financial

instruments

Market Value (£) Book value (£) Proposed Value (£)

2

By using above formula growth rate is calculated which is 7.57%. It will be used to

determine book and market value of the asset.

Calculation of different costs:

Cost of equity: Ke

Formula: ( Sn * [ ( 1 + g ) + g ] ) / P0

[ Sn = First Dividend ]

[ g = growth rate ]

[P0 = Ex dividend ]

Calculations of it are as follows:

= [ 28 * ( 1 + 0.075 ) + 0.075 ] / 2.65

= ( 28 * 1.15 ) / 2.65

= 12.15%

Cost of preference share: Kp

Formula: ( j ) / Pf

[ j = preference dividend ]

[ Pf = ex dividend for preference share ]

Calculation of it is as follows:

= 7 / 75

= 9.33 %

Cost of other debts (Irredeemable bonds): Kdir

Formula: [I * ( 1 – t ) ] * (Po / Pn)

[ I = Rate of interest on irredeemable bonds ]

[ t = rate of corporate taxation ]

[ Po = Initial price of bonds ]

[ Pn = Current price of bond ]

= [ 0.10 * ( 1 - 0.30 ) ] * ( 100 / 107 )

= 0.0654 or 6.54%

Calculation of cost at book and market value:

Financial

instruments

Market Value (£) Book value (£) Proposed Value (£)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

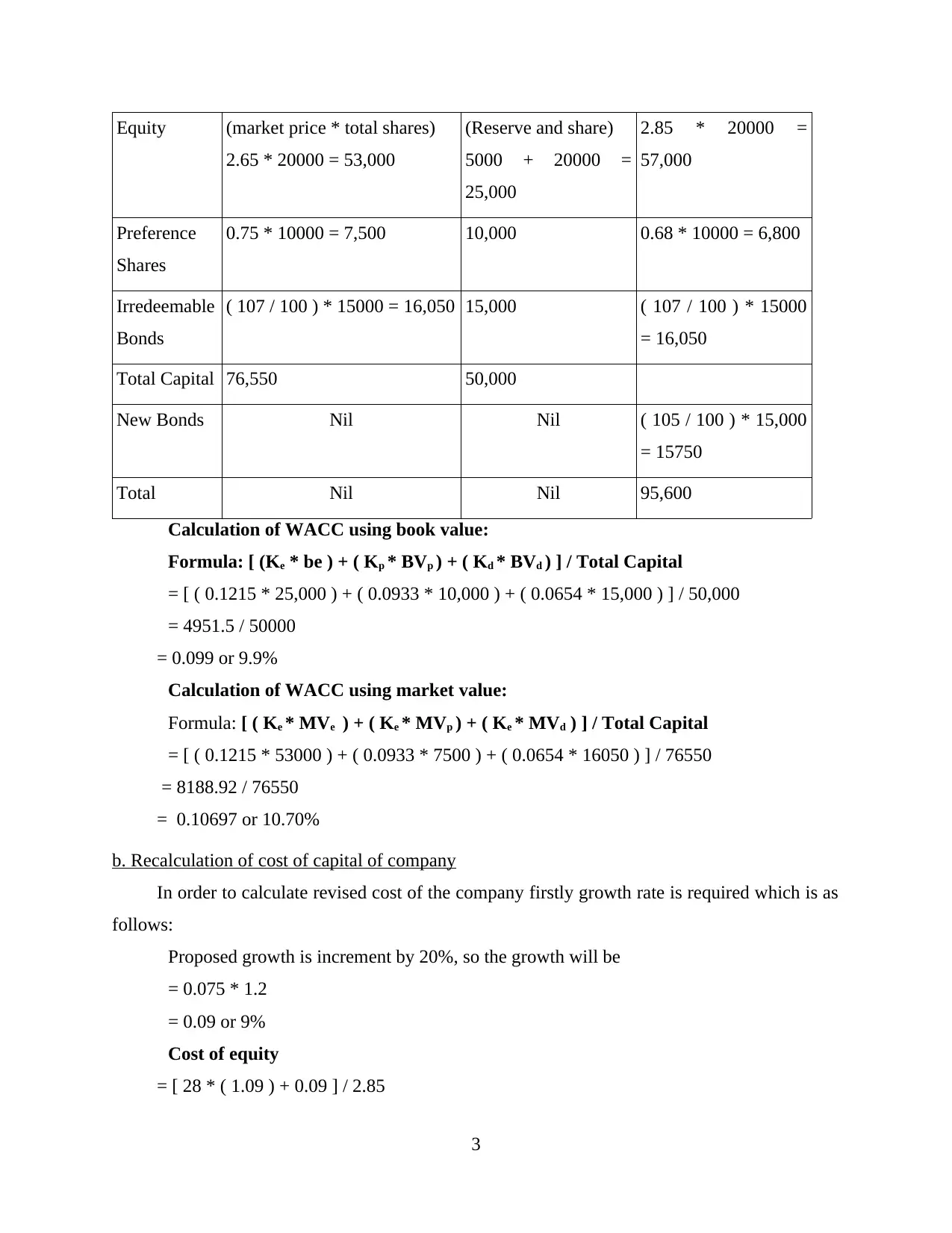

Equity (market price * total shares)

2.65 * 20000 = 53,000

(Reserve and share)

5000 + 20000 =

25,000

2.85 * 20000 =

57,000

Preference

Shares

0.75 * 10000 = 7,500 10,000 0.68 * 10000 = 6,800

Irredeemable

Bonds

( 107 / 100 ) * 15000 = 16,050 15,000 ( 107 / 100 ) * 15000

= 16,050

Total Capital 76,550 50,000

New Bonds Nil Nil ( 105 / 100 ) * 15,000

= 15750

Total Nil Nil 95,600

Calculation of WACC using book value:

Formula: [ (Ke * be ) + ( Kp * BVp ) + ( Kd * BVd ) ] / Total Capital

= [ ( 0.1215 * 25,000 ) + ( 0.0933 * 10,000 ) + ( 0.0654 * 15,000 ) ] / 50,000

= 4951.5 / 50000

= 0.099 or 9.9%

Calculation of WACC using market value:

Formula: [ ( Ke * MVe ) + ( Ke * MVp ) + ( Ke * MVd ) ] / Total Capital

= [ ( 0.1215 * 53000 ) + ( 0.0933 * 7500 ) + ( 0.0654 * 16050 ) ] / 76550

= 8188.92 / 76550

= 0.10697 or 10.70%

b. Recalculation of cost of capital of company

In order to calculate revised cost of the company firstly growth rate is required which is as

follows:

Proposed growth is increment by 20%, so the growth will be

= 0.075 * 1.2

= 0.09 or 9%

Cost of equity

= [ 28 * ( 1.09 ) + 0.09 ] / 2.85

3

2.65 * 20000 = 53,000

(Reserve and share)

5000 + 20000 =

25,000

2.85 * 20000 =

57,000

Preference

Shares

0.75 * 10000 = 7,500 10,000 0.68 * 10000 = 6,800

Irredeemable

Bonds

( 107 / 100 ) * 15000 = 16,050 15,000 ( 107 / 100 ) * 15000

= 16,050

Total Capital 76,550 50,000

New Bonds Nil Nil ( 105 / 100 ) * 15,000

= 15750

Total Nil Nil 95,600

Calculation of WACC using book value:

Formula: [ (Ke * be ) + ( Kp * BVp ) + ( Kd * BVd ) ] / Total Capital

= [ ( 0.1215 * 25,000 ) + ( 0.0933 * 10,000 ) + ( 0.0654 * 15,000 ) ] / 50,000

= 4951.5 / 50000

= 0.099 or 9.9%

Calculation of WACC using market value:

Formula: [ ( Ke * MVe ) + ( Ke * MVp ) + ( Ke * MVd ) ] / Total Capital

= [ ( 0.1215 * 53000 ) + ( 0.0933 * 7500 ) + ( 0.0654 * 16050 ) ] / 76550

= 8188.92 / 76550

= 0.10697 or 10.70%

b. Recalculation of cost of capital of company

In order to calculate revised cost of the company firstly growth rate is required which is as

follows:

Proposed growth is increment by 20%, so the growth will be

= 0.075 * 1.2

= 0.09 or 9%

Cost of equity

= [ 28 * ( 1.09 ) + 0.09 ] / 2.85

3

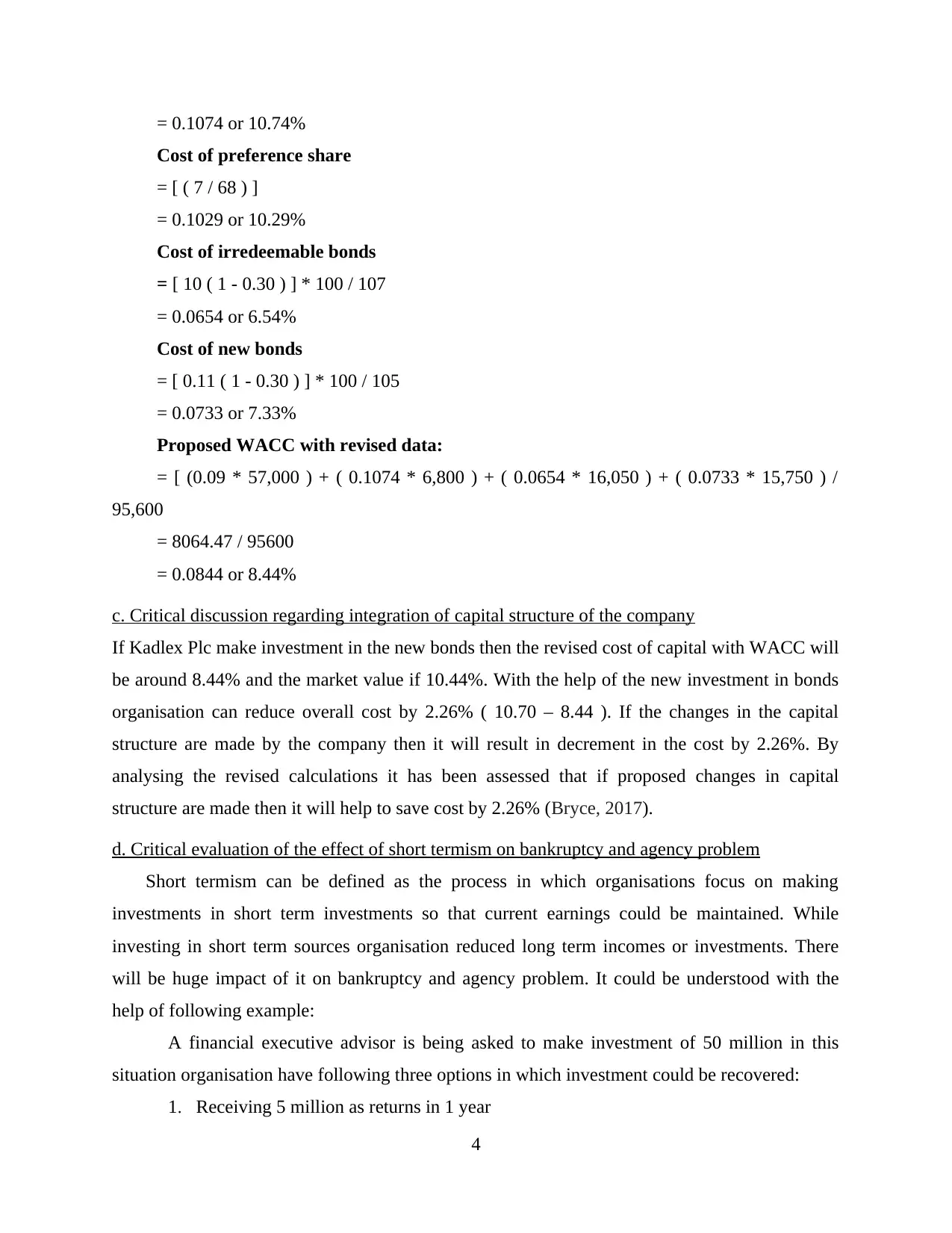

= 0.1074 or 10.74%

Cost of preference share

= [ ( 7 / 68 ) ]

= 0.1029 or 10.29%

Cost of irredeemable bonds

= [ 10 ( 1 - 0.30 ) ] * 100 / 107

= 0.0654 or 6.54%

Cost of new bonds

= [ 0.11 ( 1 - 0.30 ) ] * 100 / 105

= 0.0733 or 7.33%

Proposed WACC with revised data:

= [ (0.09 * 57,000 ) + ( 0.1074 * 6,800 ) + ( 0.0654 * 16,050 ) + ( 0.0733 * 15,750 ) /

95,600

= 8064.47 / 95600

= 0.0844 or 8.44%

c. Critical discussion regarding integration of capital structure of the company

If Kadlex Plc make investment in the new bonds then the revised cost of capital with WACC will

be around 8.44% and the market value if 10.44%. With the help of the new investment in bonds

organisation can reduce overall cost by 2.26% ( 10.70 – 8.44 ). If the changes in the capital

structure are made by the company then it will result in decrement in the cost by 2.26%. By

analysing the revised calculations it has been assessed that if proposed changes in capital

structure are made then it will help to save cost by 2.26% (Bryce, 2017).

d. Critical evaluation of the effect of short termism on bankruptcy and agency problem

Short termism can be defined as the process in which organisations focus on making

investments in short term investments so that current earnings could be maintained. While

investing in short term sources organisation reduced long term incomes or investments. There

will be huge impact of it on bankruptcy and agency problem. It could be understood with the

help of following example:

A financial executive advisor is being asked to make investment of 50 million in this

situation organisation have following three options in which investment could be recovered:

1. Receiving 5 million as returns in 1 year

4

Cost of preference share

= [ ( 7 / 68 ) ]

= 0.1029 or 10.29%

Cost of irredeemable bonds

= [ 10 ( 1 - 0.30 ) ] * 100 / 107

= 0.0654 or 6.54%

Cost of new bonds

= [ 0.11 ( 1 - 0.30 ) ] * 100 / 105

= 0.0733 or 7.33%

Proposed WACC with revised data:

= [ (0.09 * 57,000 ) + ( 0.1074 * 6,800 ) + ( 0.0654 * 16,050 ) + ( 0.0733 * 15,750 ) /

95,600

= 8064.47 / 95600

= 0.0844 or 8.44%

c. Critical discussion regarding integration of capital structure of the company

If Kadlex Plc make investment in the new bonds then the revised cost of capital with WACC will

be around 8.44% and the market value if 10.44%. With the help of the new investment in bonds

organisation can reduce overall cost by 2.26% ( 10.70 – 8.44 ). If the changes in the capital

structure are made by the company then it will result in decrement in the cost by 2.26%. By

analysing the revised calculations it has been assessed that if proposed changes in capital

structure are made then it will help to save cost by 2.26% (Bryce, 2017).

d. Critical evaluation of the effect of short termism on bankruptcy and agency problem

Short termism can be defined as the process in which organisations focus on making

investments in short term investments so that current earnings could be maintained. While

investing in short term sources organisation reduced long term incomes or investments. There

will be huge impact of it on bankruptcy and agency problem. It could be understood with the

help of following example:

A financial executive advisor is being asked to make investment of 50 million in this

situation organisation have following three options in which investment could be recovered:

1. Receiving 5 million as returns in 1 year

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Receiving 20 million as returns in 3 years

3. Receiving 25 million as returns in 5 years

From all the above options the financial advisor will select the option of receiving 5 million in

one year because it will result in money in hand in a small time period. Another viewpoint is that

their occupation and spot in the organisation are not secured so they select the option for self-

interest rather than organisation’s benefits. This type of situation implies to “Agency Problem” in

which interest of shareholders are ignored for making self-growth and development by

corporates. The impacts of this phenomena can be disastrous on a corporation's bankruptcy

(Burtonshaw-Gunn, 2017).

QUESTION 3

a. Calculation of different investment appraisal techniques

The pay back period: It is a technique which is used in capital budgeting for the purpose

of analysing that the amount which is invested in an asset will be recovered in how many years.

With the help of it long term investment decision are formulated by managers as it guides them

to invest monetary resources in that asset which may refund the funds as soon as possible. Main

objective of using this technique is to determine the time period in which investments could be

recovered by the organisation (Cornwall, Vang and Hartman, 2016). Formula of it is follows:

Pay back period = I / C

I = Initial investment

C = Cash Inflow

Calculation of it are as follows:

Information provided: Initial investment = 320000

Life of machine is 6 years

Cash inflow = 105000

Cash out flow = 15500

Net cash in flow = 105000 – 15500

= 89500

Pay back period = 320000 / 89500

= 3.58 years

5

3. Receiving 25 million as returns in 5 years

From all the above options the financial advisor will select the option of receiving 5 million in

one year because it will result in money in hand in a small time period. Another viewpoint is that

their occupation and spot in the organisation are not secured so they select the option for self-

interest rather than organisation’s benefits. This type of situation implies to “Agency Problem” in

which interest of shareholders are ignored for making self-growth and development by

corporates. The impacts of this phenomena can be disastrous on a corporation's bankruptcy

(Burtonshaw-Gunn, 2017).

QUESTION 3

a. Calculation of different investment appraisal techniques

The pay back period: It is a technique which is used in capital budgeting for the purpose

of analysing that the amount which is invested in an asset will be recovered in how many years.

With the help of it long term investment decision are formulated by managers as it guides them

to invest monetary resources in that asset which may refund the funds as soon as possible. Main

objective of using this technique is to determine the time period in which investments could be

recovered by the organisation (Cornwall, Vang and Hartman, 2016). Formula of it is follows:

Pay back period = I / C

I = Initial investment

C = Cash Inflow

Calculation of it are as follows:

Information provided: Initial investment = 320000

Life of machine is 6 years

Cash inflow = 105000

Cash out flow = 15500

Net cash in flow = 105000 – 15500

= 89500

Pay back period = 320000 / 89500

= 3.58 years

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis: From the above calculations it has been analysed that the amount which will be

invested in acquisition of new machine could be redeemed by Happy Meal Limited in 3.58 years.

It will be good for the organisation to buy it as it will repay the amount in half of the life of it.

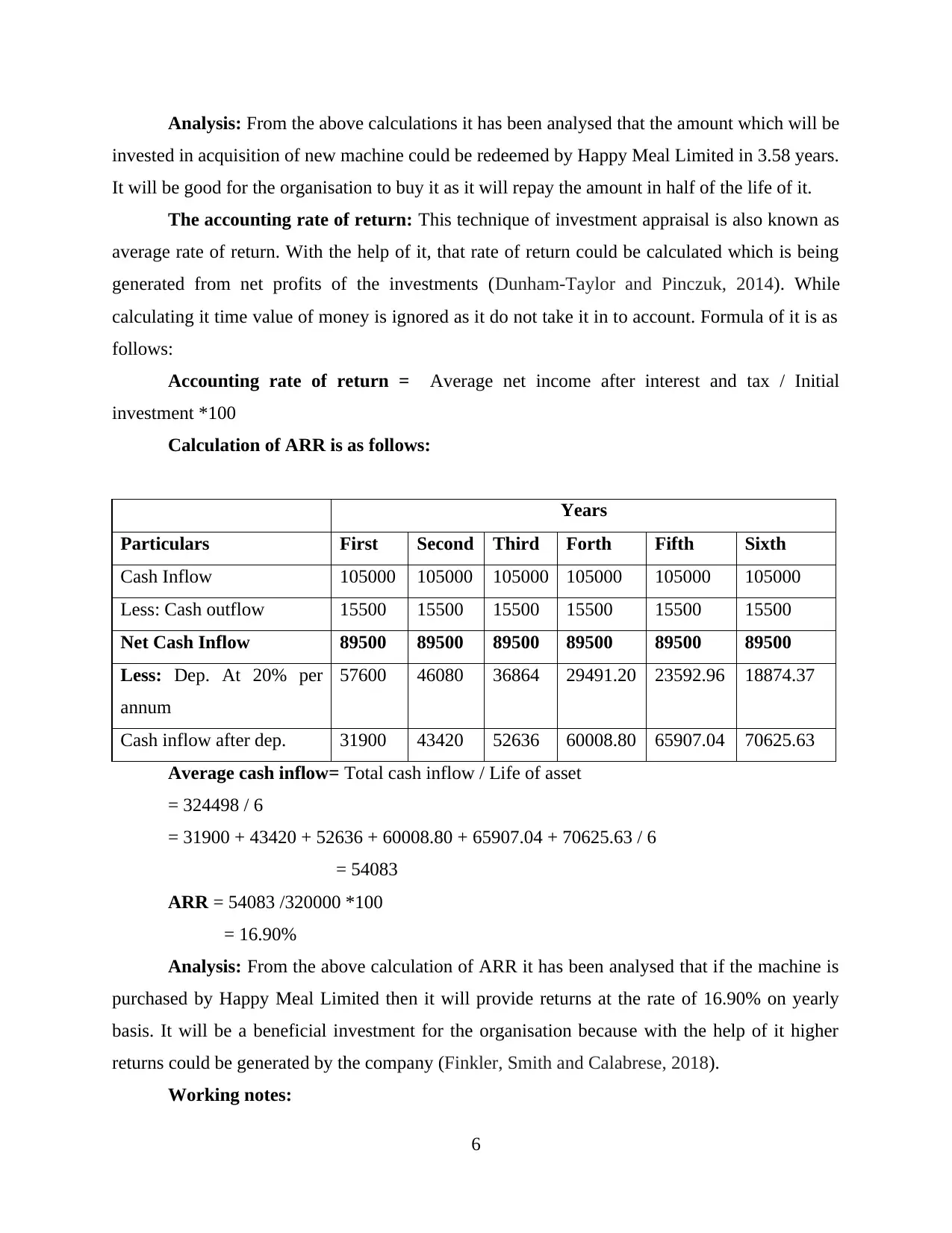

The accounting rate of return: This technique of investment appraisal is also known as

average rate of return. With the help of it, that rate of return could be calculated which is being

generated from net profits of the investments (Dunham-Taylor and Pinczuk, 2014). While

calculating it time value of money is ignored as it do not take it in to account. Formula of it is as

follows:

Accounting rate of return = Average net income after interest and tax / Initial

investment *100

Calculation of ARR is as follows:

Years

Particulars First Second Third Forth Fifth Sixth

Cash Inflow 105000 105000 105000 105000 105000 105000

Less: Cash outflow 15500 15500 15500 15500 15500 15500

Net Cash Inflow 89500 89500 89500 89500 89500 89500

Less: Dep. At 20% per

annum

57600 46080 36864 29491.20 23592.96 18874.37

Cash inflow after dep. 31900 43420 52636 60008.80 65907.04 70625.63

Average cash inflow= Total cash inflow / Life of asset

= 324498 / 6

= 31900 + 43420 + 52636 + 60008.80 + 65907.04 + 70625.63 / 6

= 54083

ARR = 54083 /320000 *100

= 16.90%

Analysis: From the above calculation of ARR it has been analysed that if the machine is

purchased by Happy Meal Limited then it will provide returns at the rate of 16.90% on yearly

basis. It will be a beneficial investment for the organisation because with the help of it higher

returns could be generated by the company (Finkler, Smith and Calabrese, 2018).

Working notes:

6

invested in acquisition of new machine could be redeemed by Happy Meal Limited in 3.58 years.

It will be good for the organisation to buy it as it will repay the amount in half of the life of it.

The accounting rate of return: This technique of investment appraisal is also known as

average rate of return. With the help of it, that rate of return could be calculated which is being

generated from net profits of the investments (Dunham-Taylor and Pinczuk, 2014). While

calculating it time value of money is ignored as it do not take it in to account. Formula of it is as

follows:

Accounting rate of return = Average net income after interest and tax / Initial

investment *100

Calculation of ARR is as follows:

Years

Particulars First Second Third Forth Fifth Sixth

Cash Inflow 105000 105000 105000 105000 105000 105000

Less: Cash outflow 15500 15500 15500 15500 15500 15500

Net Cash Inflow 89500 89500 89500 89500 89500 89500

Less: Dep. At 20% per

annum

57600 46080 36864 29491.20 23592.96 18874.37

Cash inflow after dep. 31900 43420 52636 60008.80 65907.04 70625.63

Average cash inflow= Total cash inflow / Life of asset

= 324498 / 6

= 31900 + 43420 + 52636 + 60008.80 + 65907.04 + 70625.63 / 6

= 54083

ARR = 54083 /320000 *100

= 16.90%

Analysis: From the above calculation of ARR it has been analysed that if the machine is

purchased by Happy Meal Limited then it will provide returns at the rate of 16.90% on yearly

basis. It will be a beneficial investment for the organisation because with the help of it higher

returns could be generated by the company (Finkler, Smith and Calabrese, 2018).

Working notes:

6

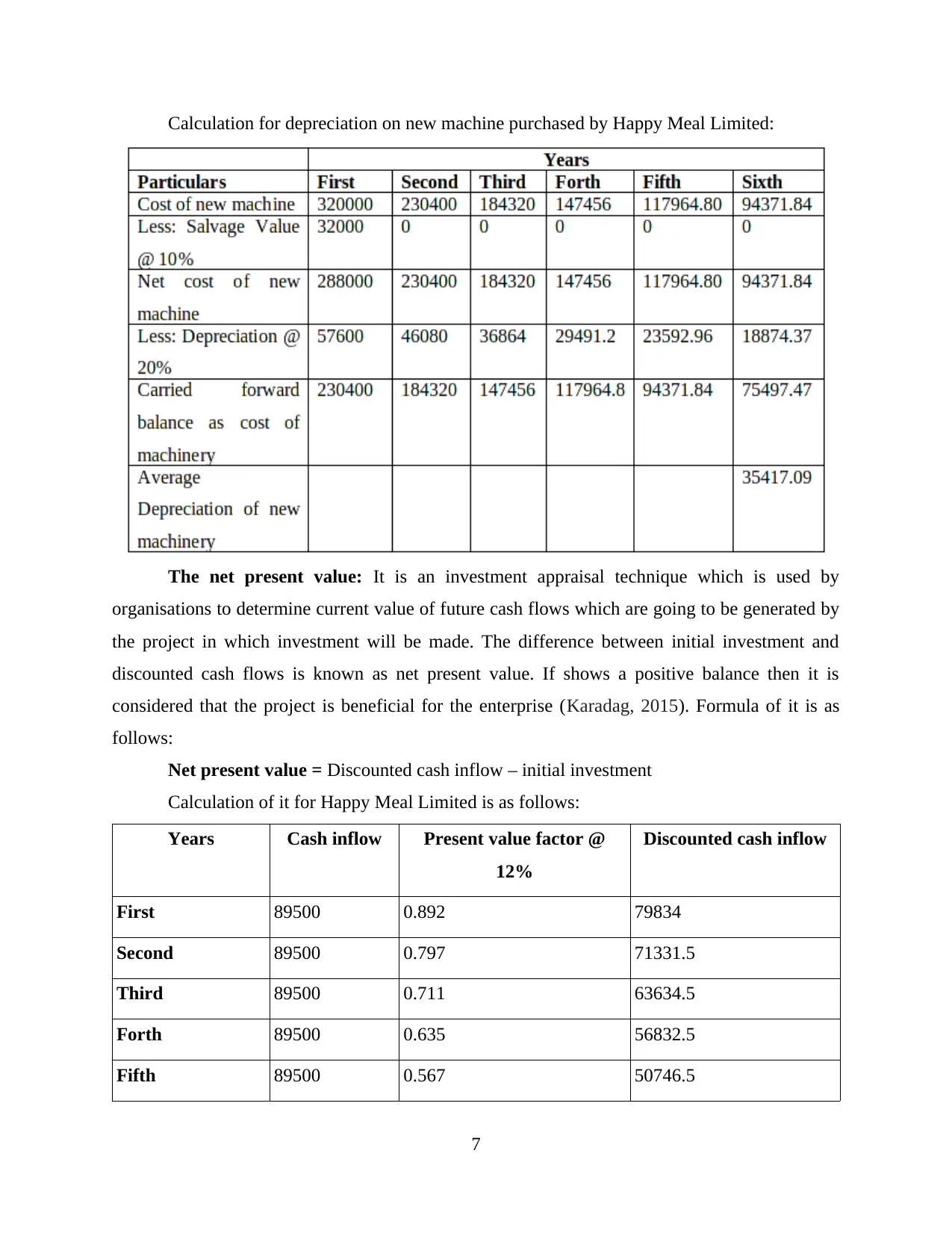

Calculation for depreciation on new machine purchased by Happy Meal Limited:

The net present value: It is an investment appraisal technique which is used by

organisations to determine current value of future cash flows which are going to be generated by

the project in which investment will be made. The difference between initial investment and

discounted cash flows is known as net present value. If shows a positive balance then it is

considered that the project is beneficial for the enterprise (Karadag, 2015). Formula of it is as

follows:

Net present value = Discounted cash inflow – initial investment

Calculation of it for Happy Meal Limited is as follows:

Years Cash inflow Present value factor @

12%

Discounted cash inflow

First 89500 0.892 79834

Second 89500 0.797 71331.5

Third 89500 0.711 63634.5

Forth 89500 0.635 56832.5

Fifth 89500 0.567 50746.5

7

The net present value: It is an investment appraisal technique which is used by

organisations to determine current value of future cash flows which are going to be generated by

the project in which investment will be made. The difference between initial investment and

discounted cash flows is known as net present value. If shows a positive balance then it is

considered that the project is beneficial for the enterprise (Karadag, 2015). Formula of it is as

follows:

Net present value = Discounted cash inflow – initial investment

Calculation of it for Happy Meal Limited is as follows:

Years Cash inflow Present value factor @

12%

Discounted cash inflow

First 89500 0.892 79834

Second 89500 0.797 71331.5

Third 89500 0.711 63634.5

Forth 89500 0.635 56832.5

Fifth 89500 0.567 50746.5

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

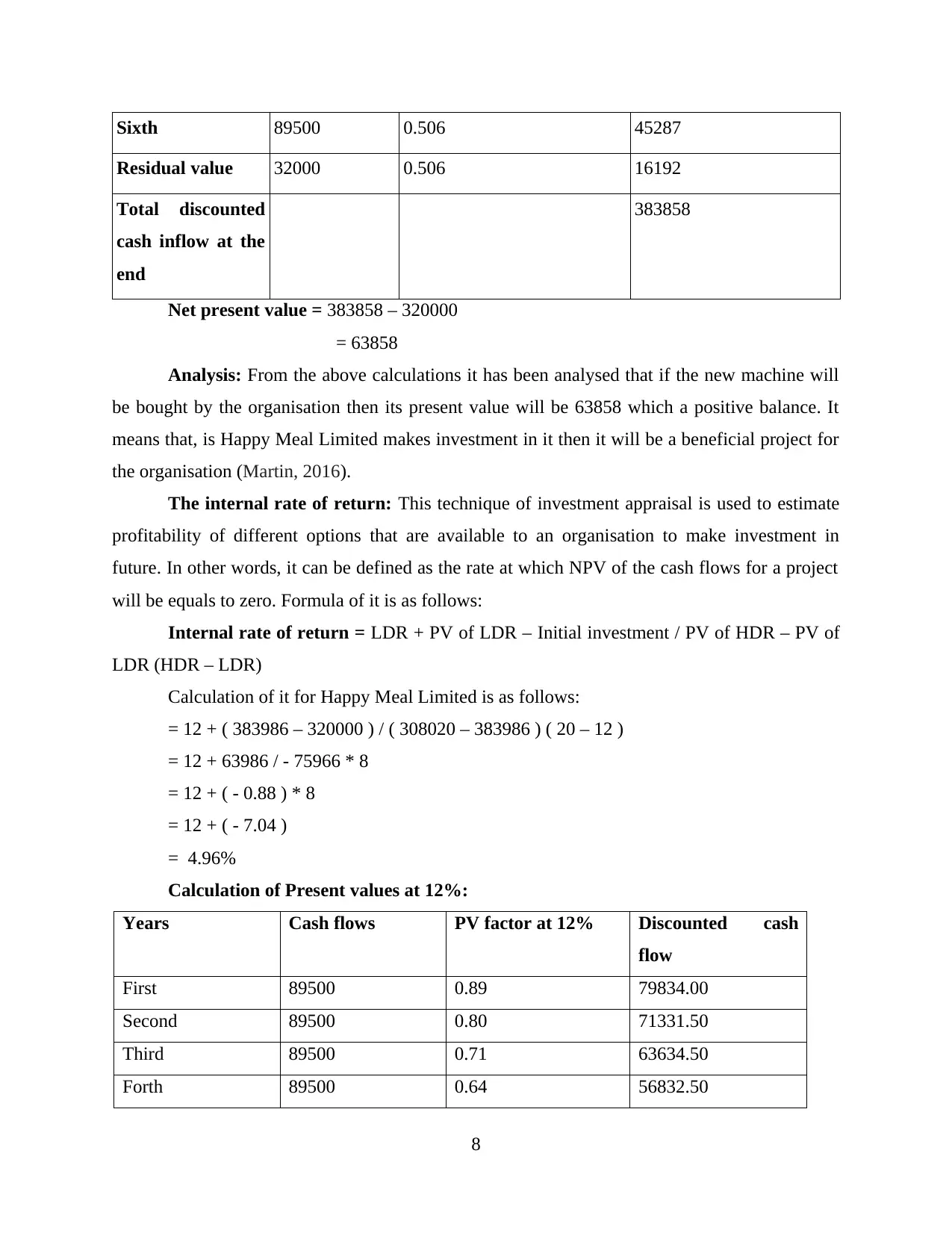

Sixth 89500 0.506 45287

Residual value 32000 0.506 16192

Total discounted

cash inflow at the

end

383858

Net present value = 383858 – 320000

= 63858

Analysis: From the above calculations it has been analysed that if the new machine will

be bought by the organisation then its present value will be 63858 which a positive balance. It

means that, is Happy Meal Limited makes investment in it then it will be a beneficial project for

the organisation (Martin, 2016).

The internal rate of return: This technique of investment appraisal is used to estimate

profitability of different options that are available to an organisation to make investment in

future. In other words, it can be defined as the rate at which NPV of the cash flows for a project

will be equals to zero. Formula of it is as follows:

Internal rate of return = LDR + PV of LDR – Initial investment / PV of HDR – PV of

LDR (HDR – LDR)

Calculation of it for Happy Meal Limited is as follows:

= 12 + ( 383986 – 320000 ) / ( 308020 – 383986 ) ( 20 – 12 )

= 12 + 63986 / - 75966 * 8

= 12 + ( - 0.88 ) * 8

= 12 + ( - 7.04 )

= 4.96%

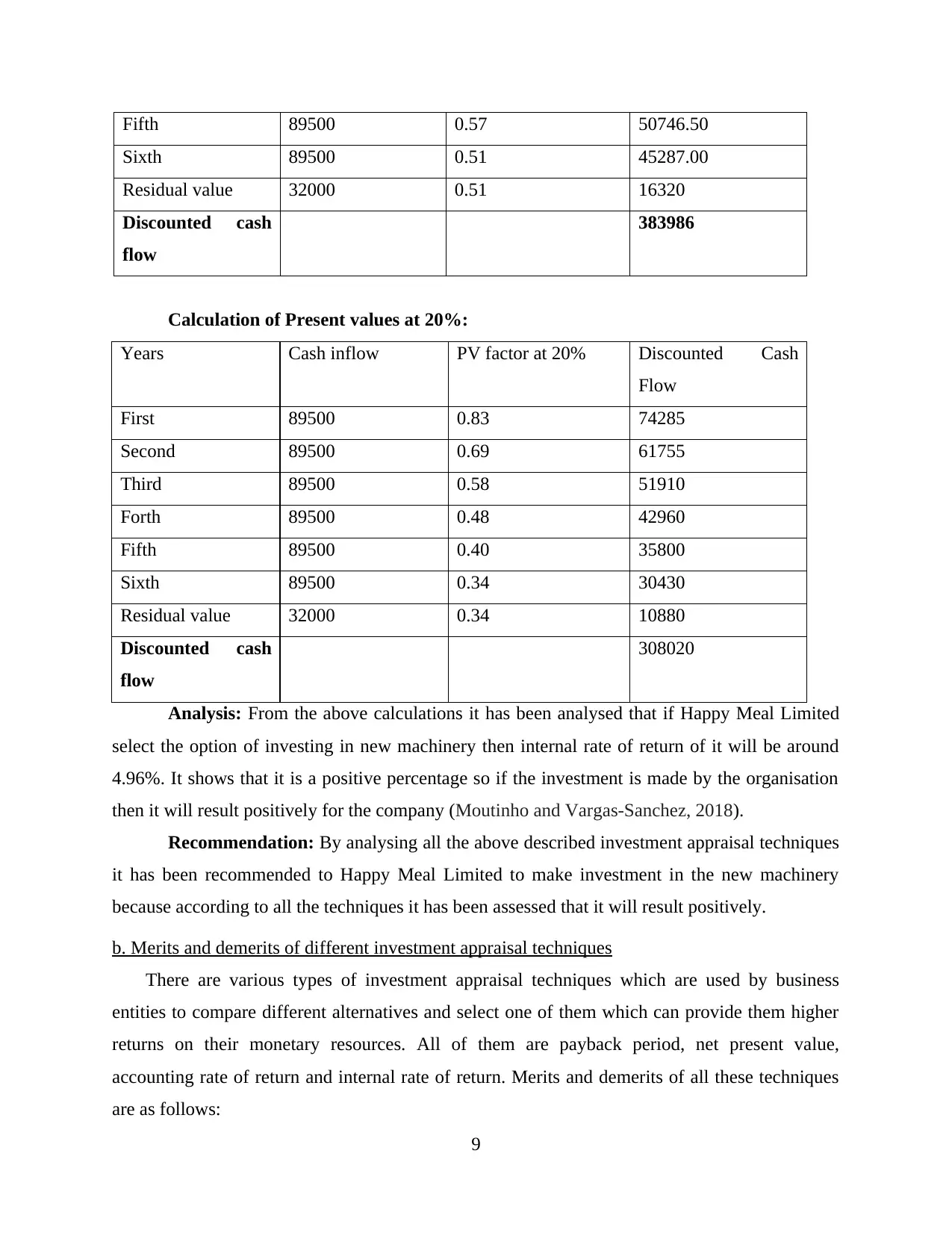

Calculation of Present values at 12%:

Years Cash flows PV factor at 12% Discounted cash

flow

First 89500 0.89 79834.00

Second 89500 0.80 71331.50

Third 89500 0.71 63634.50

Forth 89500 0.64 56832.50

8

Residual value 32000 0.506 16192

Total discounted

cash inflow at the

end

383858

Net present value = 383858 – 320000

= 63858

Analysis: From the above calculations it has been analysed that if the new machine will

be bought by the organisation then its present value will be 63858 which a positive balance. It

means that, is Happy Meal Limited makes investment in it then it will be a beneficial project for

the organisation (Martin, 2016).

The internal rate of return: This technique of investment appraisal is used to estimate

profitability of different options that are available to an organisation to make investment in

future. In other words, it can be defined as the rate at which NPV of the cash flows for a project

will be equals to zero. Formula of it is as follows:

Internal rate of return = LDR + PV of LDR – Initial investment / PV of HDR – PV of

LDR (HDR – LDR)

Calculation of it for Happy Meal Limited is as follows:

= 12 + ( 383986 – 320000 ) / ( 308020 – 383986 ) ( 20 – 12 )

= 12 + 63986 / - 75966 * 8

= 12 + ( - 0.88 ) * 8

= 12 + ( - 7.04 )

= 4.96%

Calculation of Present values at 12%:

Years Cash flows PV factor at 12% Discounted cash

flow

First 89500 0.89 79834.00

Second 89500 0.80 71331.50

Third 89500 0.71 63634.50

Forth 89500 0.64 56832.50

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fifth 89500 0.57 50746.50

Sixth 89500 0.51 45287.00

Residual value 32000 0.51 16320

Discounted cash

flow

383986

Calculation of Present values at 20%:

Years Cash inflow PV factor at 20% Discounted Cash

Flow

First 89500 0.83 74285

Second 89500 0.69 61755

Third 89500 0.58 51910

Forth 89500 0.48 42960

Fifth 89500 0.40 35800

Sixth 89500 0.34 30430

Residual value 32000 0.34 10880

Discounted cash

flow

308020

Analysis: From the above calculations it has been analysed that if Happy Meal Limited

select the option of investing in new machinery then internal rate of return of it will be around

4.96%. It shows that it is a positive percentage so if the investment is made by the organisation

then it will result positively for the company (Moutinho and Vargas-Sanchez, 2018).

Recommendation: By analysing all the above described investment appraisal techniques

it has been recommended to Happy Meal Limited to make investment in the new machinery

because according to all the techniques it has been assessed that it will result positively.

b. Merits and demerits of different investment appraisal techniques

There are various types of investment appraisal techniques which are used by business

entities to compare different alternatives and select one of them which can provide them higher

returns on their monetary resources. All of them are payback period, net present value,

accounting rate of return and internal rate of return. Merits and demerits of all these techniques

are as follows:

9

Sixth 89500 0.51 45287.00

Residual value 32000 0.51 16320

Discounted cash

flow

383986

Calculation of Present values at 20%:

Years Cash inflow PV factor at 20% Discounted Cash

Flow

First 89500 0.83 74285

Second 89500 0.69 61755

Third 89500 0.58 51910

Forth 89500 0.48 42960

Fifth 89500 0.40 35800

Sixth 89500 0.34 30430

Residual value 32000 0.34 10880

Discounted cash

flow

308020

Analysis: From the above calculations it has been analysed that if Happy Meal Limited

select the option of investing in new machinery then internal rate of return of it will be around

4.96%. It shows that it is a positive percentage so if the investment is made by the organisation

then it will result positively for the company (Moutinho and Vargas-Sanchez, 2018).

Recommendation: By analysing all the above described investment appraisal techniques

it has been recommended to Happy Meal Limited to make investment in the new machinery

because according to all the techniques it has been assessed that it will result positively.

b. Merits and demerits of different investment appraisal techniques

There are various types of investment appraisal techniques which are used by business

entities to compare different alternatives and select one of them which can provide them higher

returns on their monetary resources. All of them are payback period, net present value,

accounting rate of return and internal rate of return. Merits and demerits of all these techniques

are as follows:

9

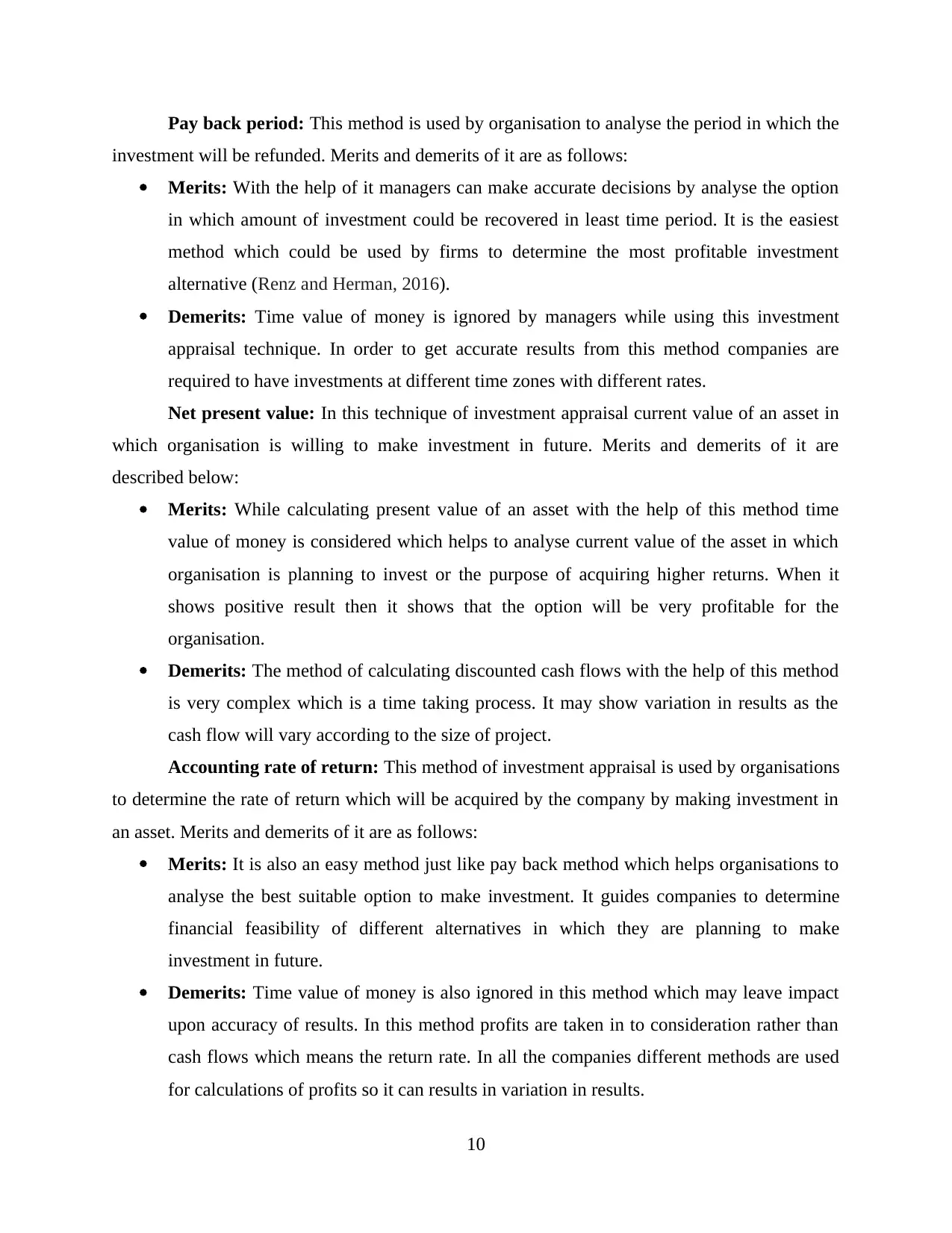

Pay back period: This method is used by organisation to analyse the period in which the

investment will be refunded. Merits and demerits of it are as follows:

Merits: With the help of it managers can make accurate decisions by analyse the option

in which amount of investment could be recovered in least time period. It is the easiest

method which could be used by firms to determine the most profitable investment

alternative (Renz and Herman, 2016).

Demerits: Time value of money is ignored by managers while using this investment

appraisal technique. In order to get accurate results from this method companies are

required to have investments at different time zones with different rates.

Net present value: In this technique of investment appraisal current value of an asset in

which organisation is willing to make investment in future. Merits and demerits of it are

described below:

Merits: While calculating present value of an asset with the help of this method time

value of money is considered which helps to analyse current value of the asset in which

organisation is planning to invest or the purpose of acquiring higher returns. When it

shows positive result then it shows that the option will be very profitable for the

organisation.

Demerits: The method of calculating discounted cash flows with the help of this method

is very complex which is a time taking process. It may show variation in results as the

cash flow will vary according to the size of project.

Accounting rate of return: This method of investment appraisal is used by organisations

to determine the rate of return which will be acquired by the company by making investment in

an asset. Merits and demerits of it are as follows:

Merits: It is also an easy method just like pay back method which helps organisations to

analyse the best suitable option to make investment. It guides companies to determine

financial feasibility of different alternatives in which they are planning to make

investment in future.

Demerits: Time value of money is also ignored in this method which may leave impact

upon accuracy of results. In this method profits are taken in to consideration rather than

cash flows which means the return rate. In all the companies different methods are used

for calculations of profits so it can results in variation in results.

10

investment will be refunded. Merits and demerits of it are as follows:

Merits: With the help of it managers can make accurate decisions by analyse the option

in which amount of investment could be recovered in least time period. It is the easiest

method which could be used by firms to determine the most profitable investment

alternative (Renz and Herman, 2016).

Demerits: Time value of money is ignored by managers while using this investment

appraisal technique. In order to get accurate results from this method companies are

required to have investments at different time zones with different rates.

Net present value: In this technique of investment appraisal current value of an asset in

which organisation is willing to make investment in future. Merits and demerits of it are

described below:

Merits: While calculating present value of an asset with the help of this method time

value of money is considered which helps to analyse current value of the asset in which

organisation is planning to invest or the purpose of acquiring higher returns. When it

shows positive result then it shows that the option will be very profitable for the

organisation.

Demerits: The method of calculating discounted cash flows with the help of this method

is very complex which is a time taking process. It may show variation in results as the

cash flow will vary according to the size of project.

Accounting rate of return: This method of investment appraisal is used by organisations

to determine the rate of return which will be acquired by the company by making investment in

an asset. Merits and demerits of it are as follows:

Merits: It is also an easy method just like pay back method which helps organisations to

analyse the best suitable option to make investment. It guides companies to determine

financial feasibility of different alternatives in which they are planning to make

investment in future.

Demerits: Time value of money is also ignored in this method which may leave impact

upon accuracy of results. In this method profits are taken in to consideration rather than

cash flows which means the return rate. In all the companies different methods are used

for calculations of profits so it can results in variation in results.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.