Financial Management: Investment Appraisal and Finance Report

VerifiedAdded on 2023/01/16

|15

|4074

|29

Report

AI Summary

This report delves into the core aspects of financial management, providing a comprehensive analysis of key concepts and techniques. The introduction establishes the significance of financial management in today's business environment, emphasizing its role in strategic decision-making and the effective allocation of financial resources. The main body of the report addresses specific questions related to long-term finance, focusing on equity finance and the issuance of right shares. It evaluates the benefits of scrip dividends for both shareholders and companies, assessing their advantages and disadvantages. Furthermore, the report explores investment appraisal techniques, including payback period, accounting rate of return, net present value, and internal rate of return, providing detailed calculations and critical evaluations of their respective benefits and drawbacks. The report concludes by summarizing the key findings and reinforcing the importance of sound financial management practices. References are provided to support the information presented.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 2...................................................................................................................................1

(a) Long term finance: Equity finance........................................................................................1

(c) Evaluate the benefits of scrip divided in context of shareholders or companies...................4

QUESTION 3...................................................................................................................................5

a. Investment appraisal technique...............................................................................................5

b. Critical evaluation of investment appraisal techniques with the help of its benefits &

drawbacks....................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION 2...................................................................................................................................1

(a) Long term finance: Equity finance........................................................................................1

(c) Evaluate the benefits of scrip divided in context of shareholders or companies...................4

QUESTION 3...................................................................................................................................5

a. Investment appraisal technique...............................................................................................5

b. Critical evaluation of investment appraisal techniques with the help of its benefits &

drawbacks....................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In present business environment, managing and controlling each and every financial

dealing in a specific time period is known as financial management. In every type of business

there is a need to control and handle financial resources in order to execute the desired activity in

most profitable manner to increase entire profit (Alsemgeest, 2015). This is characterized as a

form of techniques that is best connected to the preparation, organization and management of

monetary practices. This practically focuses on percentages and liabilities as it enables to

maintain the business plan effectively. Therefore, all types of enterprise need this to handle the

funds and resources, if they are small or large.

In this report, key strategic decision are made to take crucial decision, critical

understanding of particular analytical skills to make decision at international level is discussed.

In addition, limitations of current state related to financial theory that make better business

decision are elaborated.

MAIN BODY

QUESTION 2

(a) Long term finance: Equity finance.

(A) Issue of Right share: There are the share which are issued by a respective company in

context of present shareholder. So they have the right to subscribe the share unless the some

specific right are maintain for them to other person (Arianti, 2018). In the case study, Lexbel is

planning to enhance £180000 by issuing right share which support in expansion of present

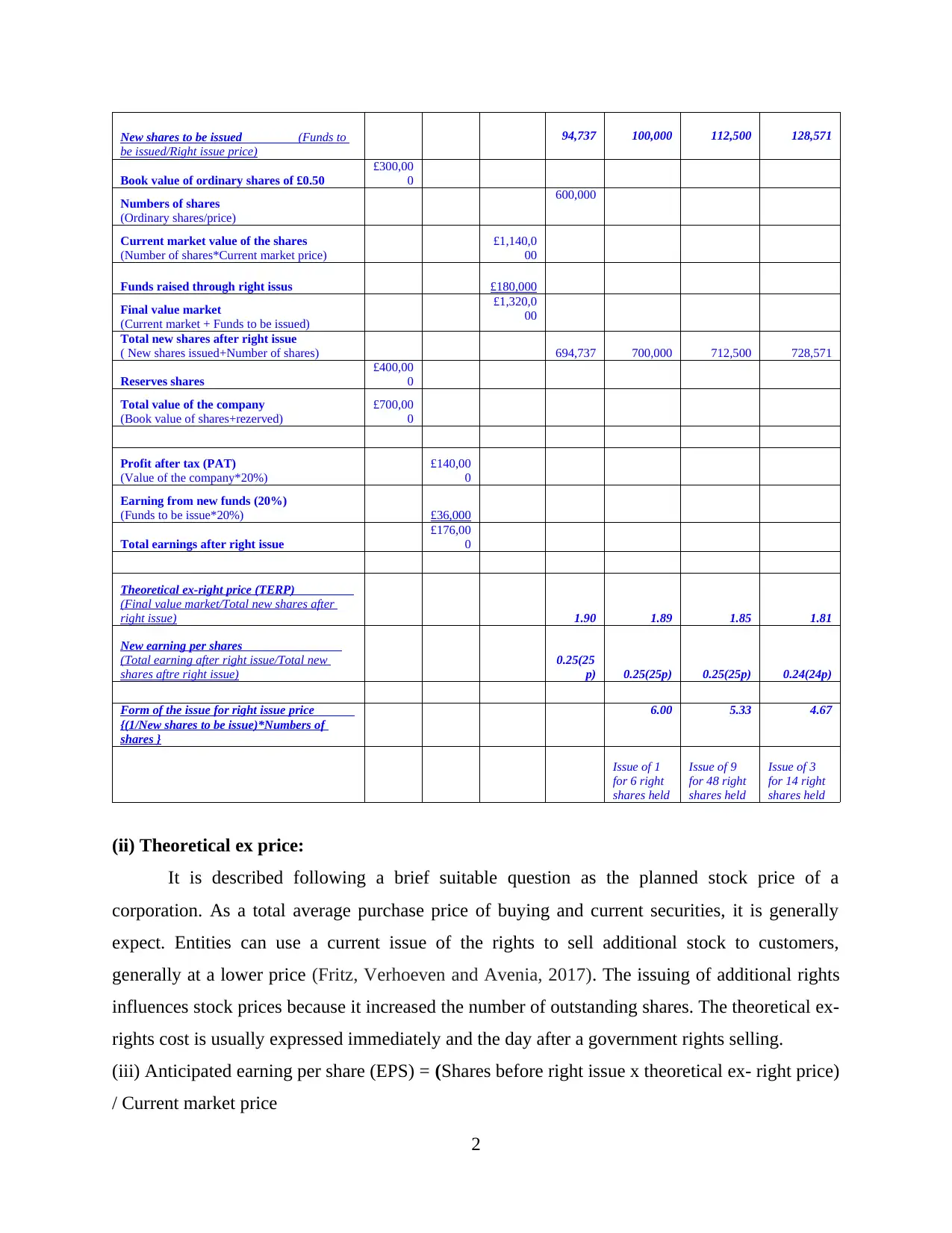

operations. The relevant information is listed below:

Predicted Amount = £180000

Ex dividend market rate= > £1.90

Suggested= > £1.80, £1.60 and £1.40

Curren

t maret

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued

£180,00

0 £180,000 £180,000 £180,000

1

In present business environment, managing and controlling each and every financial

dealing in a specific time period is known as financial management. In every type of business

there is a need to control and handle financial resources in order to execute the desired activity in

most profitable manner to increase entire profit (Alsemgeest, 2015). This is characterized as a

form of techniques that is best connected to the preparation, organization and management of

monetary practices. This practically focuses on percentages and liabilities as it enables to

maintain the business plan effectively. Therefore, all types of enterprise need this to handle the

funds and resources, if they are small or large.

In this report, key strategic decision are made to take crucial decision, critical

understanding of particular analytical skills to make decision at international level is discussed.

In addition, limitations of current state related to financial theory that make better business

decision are elaborated.

MAIN BODY

QUESTION 2

(a) Long term finance: Equity finance.

(A) Issue of Right share: There are the share which are issued by a respective company in

context of present shareholder. So they have the right to subscribe the share unless the some

specific right are maintain for them to other person (Arianti, 2018). In the case study, Lexbel is

planning to enhance £180000 by issuing right share which support in expansion of present

operations. The relevant information is listed below:

Predicted Amount = £180000

Ex dividend market rate= > £1.90

Suggested= > £1.80, £1.60 and £1.40

Curren

t maret

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued

£180,00

0 £180,000 £180,000 £180,000

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

New shares to be issued (Funds to

be issued/Right issue price)

94,737 100,000 112,500 128,571

Book value of ordinary shares of £0.50

£300,00

0

Numbers of shares

(Ordinary shares/price)

600,000

Current market value of the shares

(Number of shares*Current market price)

£1,140,0

00

Funds raised through right issus £180,000

Final value market

(Current market + Funds to be issued)

£1,320,0

00

Total new shares after right issue

( New shares issued+Number of shares) 694,737 700,000 712,500 728,571

Reserves shares

£400,00

0

Total value of the company

(Book value of shares+rezerved)

£700,00

0

Profit after tax (PAT)

(Value of the company*20%)

£140,00

0

Earning from new funds (20%)

(Funds to be issue*20%) £36,000

Total earnings after right issue

£176,00

0

Theoretical ex-right price (TERP)

(Final value market/Total new shares after

right issue) 1.90 1.89 1.85 1.81

New earning per shares

(Total earning after right issue/Total new

shares aftre right issue)

0.25(25

p) 0.25(25p) 0.25(25p) 0.24(24p)

Form of the issue for right issue price

{(1/New shares to be issue)*Numbers of

shares }

6.00 5.33 4.67

Issue of 1

for 6 right

shares held

Issue of 9

for 48 right

shares held

Issue of 3

for 14 right

shares held

(ii) Theoretical ex price:

It is described following a brief suitable question as the planned stock price of a

corporation. As a total average purchase price of buying and current securities, it is generally

expect. Entities can use a current issue of the rights to sell additional stock to customers,

generally at a lower price (Fritz, Verhoeven and Avenia, 2017). The issuing of additional rights

influences stock prices because it increased the number of outstanding shares. The theoretical ex-

rights cost is usually expressed immediately and the day after a government rights selling.

(iii) Anticipated earning per share (EPS) = (Shares before right issue x theoretical ex- right price)

/ Current market price

2

be issued/Right issue price)

94,737 100,000 112,500 128,571

Book value of ordinary shares of £0.50

£300,00

0

Numbers of shares

(Ordinary shares/price)

600,000

Current market value of the shares

(Number of shares*Current market price)

£1,140,0

00

Funds raised through right issus £180,000

Final value market

(Current market + Funds to be issued)

£1,320,0

00

Total new shares after right issue

( New shares issued+Number of shares) 694,737 700,000 712,500 728,571

Reserves shares

£400,00

0

Total value of the company

(Book value of shares+rezerved)

£700,00

0

Profit after tax (PAT)

(Value of the company*20%)

£140,00

0

Earning from new funds (20%)

(Funds to be issue*20%) £36,000

Total earnings after right issue

£176,00

0

Theoretical ex-right price (TERP)

(Final value market/Total new shares after

right issue) 1.90 1.89 1.85 1.81

New earning per shares

(Total earning after right issue/Total new

shares aftre right issue)

0.25(25

p) 0.25(25p) 0.25(25p) 0.24(24p)

Form of the issue for right issue price

{(1/New shares to be issue)*Numbers of

shares }

6.00 5.33 4.67

Issue of 1

for 6 right

shares held

Issue of 9

for 48 right

shares held

Issue of 3

for 14 right

shares held

(ii) Theoretical ex price:

It is described following a brief suitable question as the planned stock price of a

corporation. As a total average purchase price of buying and current securities, it is generally

expect. Entities can use a current issue of the rights to sell additional stock to customers,

generally at a lower price (Fritz, Verhoeven and Avenia, 2017). The issuing of additional rights

influences stock prices because it increased the number of outstanding shares. The theoretical ex-

rights cost is usually expressed immediately and the day after a government rights selling.

(iii) Anticipated earning per share (EPS) = (Shares before right issue x theoretical ex- right price)

/ Current market price

2

Thus,

Market rate= > 1.9

Available share= > 600000

Return on shareholder fund = > 140000

(iv) Form of issue of right issue price:

Critical evaluation:

Issue of every right share rates:

Of every share, the number of organizationally enhanced stocks would be 100,000 shares

in the 1.80 right issue. As a consequence, shareholders must allocate the pro-rata 1 share

to the remaining six shares.

In the context of every share the total share developed by the company in future would be

112500 in the regard of right share of 1.60 (Goel, Chadha and Sharma, 2015). Therefore

the resulted pro-rata 9 right share might be allotted to respective parties in the context of

48 share.

The total sum of share must be improve by the company in upcoming year would be

(v) Evaluate the best option from three right issue:

From the above discussion it has been founded that estimated value which issue @ £ 1.8

that is beneficial for the organization (Throsby, 2016). Because, estimation cost of earning per

share (EPS) is higher than the other two options prices.

(c) Evaluate the benefits of scrip divided in context of shareholders or companies

Scrip dividend: This term refer to the new shares of issuer's stock which issues to the

shareholders rather than providing dividend. Basically it is organization offer the shares to the

shareholders in terms of cash dividend which further automatically maximise the number of

shares as well as dividend. When any firm offer scrip dividend than it means, they provide the

opportunity to the people to maximise their shares without any additional fees or charges. This

method used by the corporation when they have to pay their inventors but they does not have

sufficient money for this (Guess and Ma, 2015). It is basically apply for the newly generated

stocks in comparison to the existing one. In many cases, it will be consider as a form of debt

which has some benefits as well as drawbacks in context of organization as well as shareholders.

Further evaluation discussed below:

3

Market rate= > 1.9

Available share= > 600000

Return on shareholder fund = > 140000

(iv) Form of issue of right issue price:

Critical evaluation:

Issue of every right share rates:

Of every share, the number of organizationally enhanced stocks would be 100,000 shares

in the 1.80 right issue. As a consequence, shareholders must allocate the pro-rata 1 share

to the remaining six shares.

In the context of every share the total share developed by the company in future would be

112500 in the regard of right share of 1.60 (Goel, Chadha and Sharma, 2015). Therefore

the resulted pro-rata 9 right share might be allotted to respective parties in the context of

48 share.

The total sum of share must be improve by the company in upcoming year would be

(v) Evaluate the best option from three right issue:

From the above discussion it has been founded that estimated value which issue @ £ 1.8

that is beneficial for the organization (Throsby, 2016). Because, estimation cost of earning per

share (EPS) is higher than the other two options prices.

(c) Evaluate the benefits of scrip divided in context of shareholders or companies

Scrip dividend: This term refer to the new shares of issuer's stock which issues to the

shareholders rather than providing dividend. Basically it is organization offer the shares to the

shareholders in terms of cash dividend which further automatically maximise the number of

shares as well as dividend. When any firm offer scrip dividend than it means, they provide the

opportunity to the people to maximise their shares without any additional fees or charges. This

method used by the corporation when they have to pay their inventors but they does not have

sufficient money for this (Guess and Ma, 2015). It is basically apply for the newly generated

stocks in comparison to the existing one. In many cases, it will be consider as a form of debt

which has some benefits as well as drawbacks in context of organization as well as shareholders.

Further evaluation discussed below:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

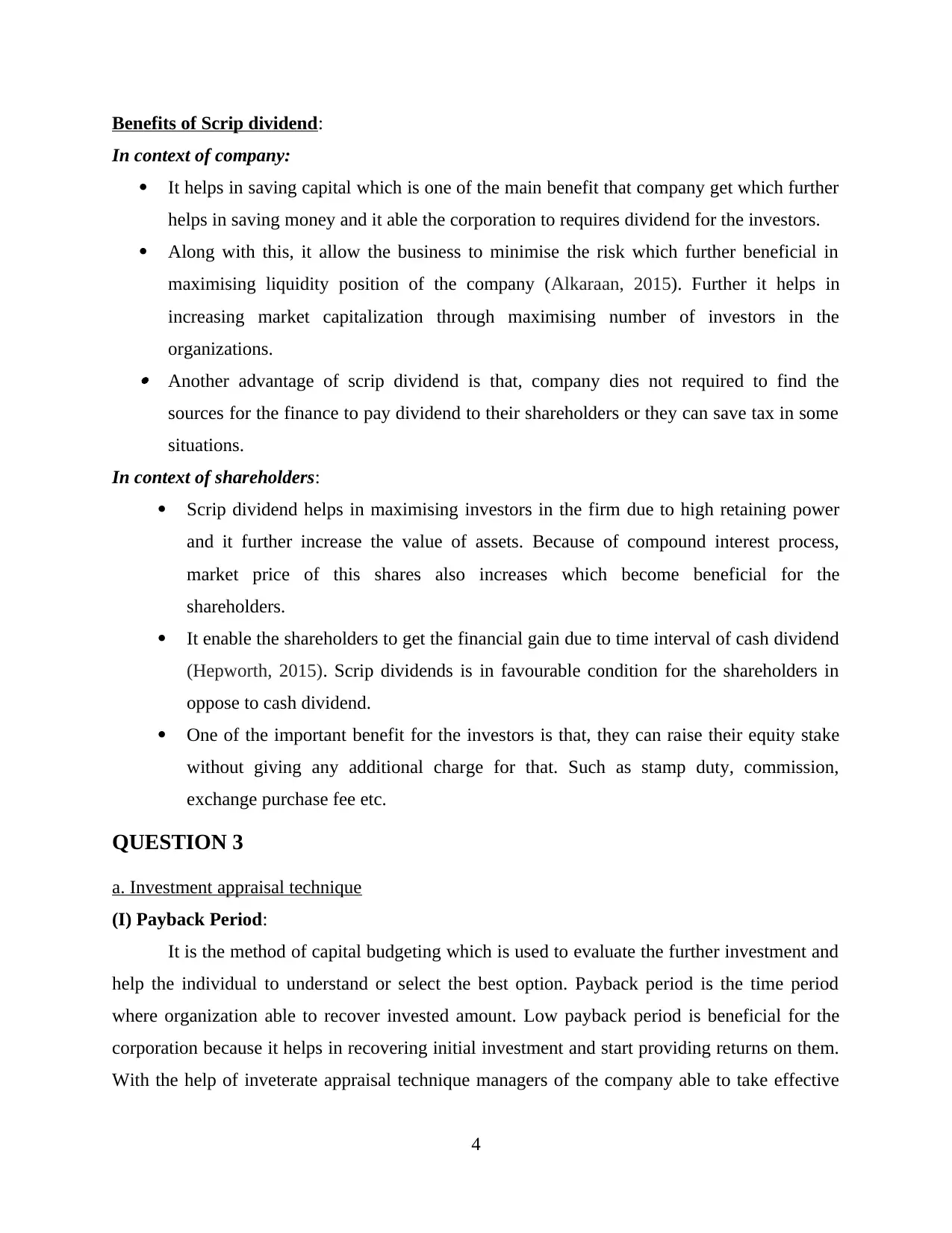

Benefits of Scrip dividend:

In context of company:

It helps in saving capital which is one of the main benefit that company get which further

helps in saving money and it able the corporation to requires dividend for the investors.

Along with this, it allow the business to minimise the risk which further beneficial in

maximising liquidity position of the company (Alkaraan, 2015). Further it helps in

increasing market capitalization through maximising number of investors in the

organizations. Another advantage of scrip dividend is that, company dies not required to find the

sources for the finance to pay dividend to their shareholders or they can save tax in some

situations.

In context of shareholders:

Scrip dividend helps in maximising investors in the firm due to high retaining power

and it further increase the value of assets. Because of compound interest process,

market price of this shares also increases which become beneficial for the

shareholders.

It enable the shareholders to get the financial gain due to time interval of cash dividend

(Hepworth, 2015). Scrip dividends is in favourable condition for the shareholders in

oppose to cash dividend.

One of the important benefit for the investors is that, they can raise their equity stake

without giving any additional charge for that. Such as stamp duty, commission,

exchange purchase fee etc.

QUESTION 3

a. Investment appraisal technique

(I) Payback Period:

It is the method of capital budgeting which is used to evaluate the further investment and

help the individual to understand or select the best option. Payback period is the time period

where organization able to recover invested amount. Low payback period is beneficial for the

corporation because it helps in recovering initial investment and start providing returns on them.

With the help of inveterate appraisal technique managers of the company able to take effective

4

In context of company:

It helps in saving capital which is one of the main benefit that company get which further

helps in saving money and it able the corporation to requires dividend for the investors.

Along with this, it allow the business to minimise the risk which further beneficial in

maximising liquidity position of the company (Alkaraan, 2015). Further it helps in

increasing market capitalization through maximising number of investors in the

organizations. Another advantage of scrip dividend is that, company dies not required to find the

sources for the finance to pay dividend to their shareholders or they can save tax in some

situations.

In context of shareholders:

Scrip dividend helps in maximising investors in the firm due to high retaining power

and it further increase the value of assets. Because of compound interest process,

market price of this shares also increases which become beneficial for the

shareholders.

It enable the shareholders to get the financial gain due to time interval of cash dividend

(Hepworth, 2015). Scrip dividends is in favourable condition for the shareholders in

oppose to cash dividend.

One of the important benefit for the investors is that, they can raise their equity stake

without giving any additional charge for that. Such as stamp duty, commission,

exchange purchase fee etc.

QUESTION 3

a. Investment appraisal technique

(I) Payback Period:

It is the method of capital budgeting which is used to evaluate the further investment and

help the individual to understand or select the best option. Payback period is the time period

where organization able to recover invested amount. Low payback period is beneficial for the

corporation because it helps in recovering initial investment and start providing returns on them.

With the help of inveterate appraisal technique managers of the company able to take effective

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

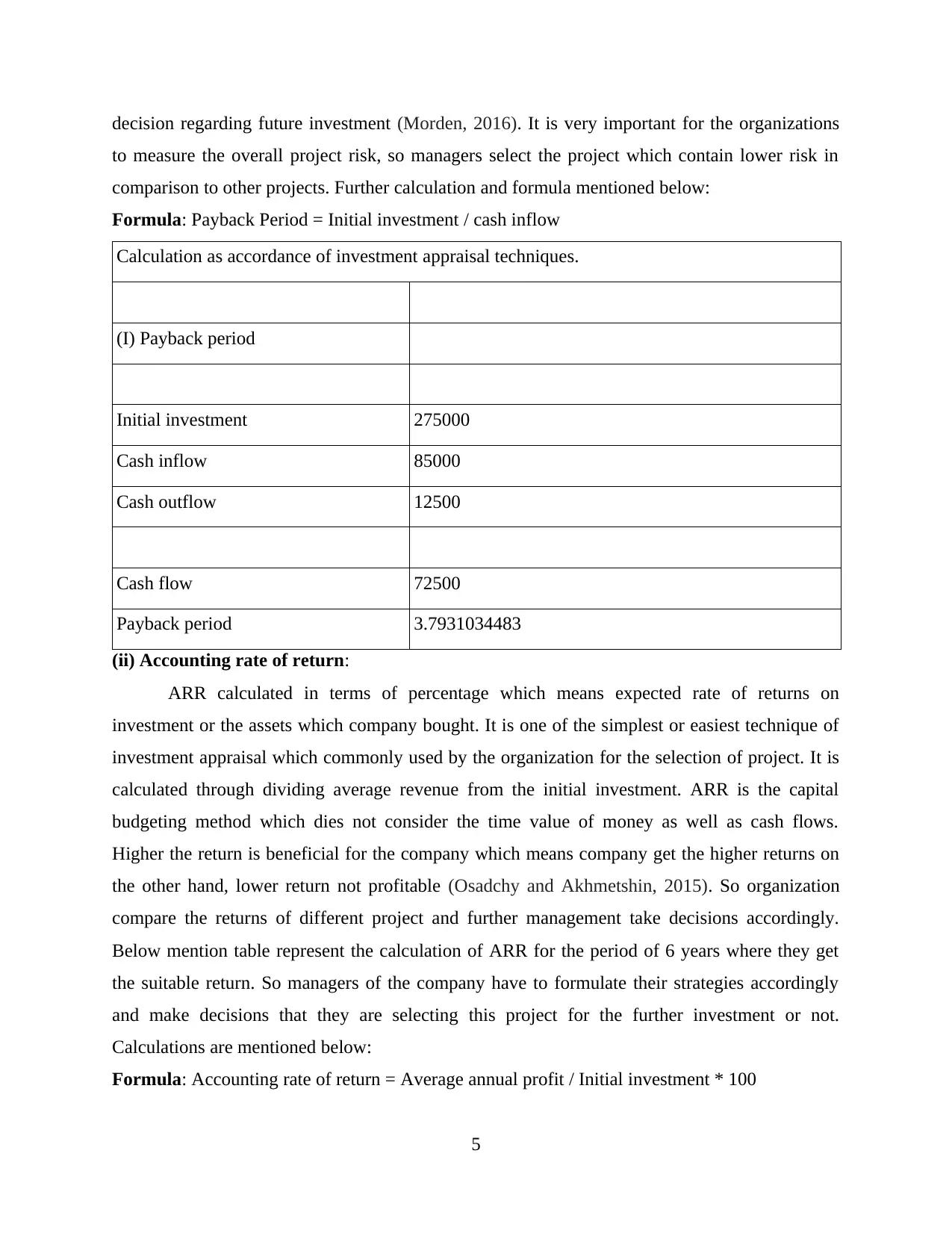

decision regarding future investment (Morden, 2016). It is very important for the organizations

to measure the overall project risk, so managers select the project which contain lower risk in

comparison to other projects. Further calculation and formula mentioned below:

Formula: Payback Period = Initial investment / cash inflow

Calculation as accordance of investment appraisal techniques.

(I) Payback period

Initial investment 275000

Cash inflow 85000

Cash outflow 12500

Cash flow 72500

Payback period 3.7931034483

(ii) Accounting rate of return:

ARR calculated in terms of percentage which means expected rate of returns on

investment or the assets which company bought. It is one of the simplest or easiest technique of

investment appraisal which commonly used by the organization for the selection of project. It is

calculated through dividing average revenue from the initial investment. ARR is the capital

budgeting method which dies not consider the time value of money as well as cash flows.

Higher the return is beneficial for the company which means company get the higher returns on

the other hand, lower return not profitable (Osadchy and Akhmetshin, 2015). So organization

compare the returns of different project and further management take decisions accordingly.

Below mention table represent the calculation of ARR for the period of 6 years where they get

the suitable return. So managers of the company have to formulate their strategies accordingly

and make decisions that they are selecting this project for the further investment or not.

Calculations are mentioned below:

Formula: Accounting rate of return = Average annual profit / Initial investment * 100

5

to measure the overall project risk, so managers select the project which contain lower risk in

comparison to other projects. Further calculation and formula mentioned below:

Formula: Payback Period = Initial investment / cash inflow

Calculation as accordance of investment appraisal techniques.

(I) Payback period

Initial investment 275000

Cash inflow 85000

Cash outflow 12500

Cash flow 72500

Payback period 3.7931034483

(ii) Accounting rate of return:

ARR calculated in terms of percentage which means expected rate of returns on

investment or the assets which company bought. It is one of the simplest or easiest technique of

investment appraisal which commonly used by the organization for the selection of project. It is

calculated through dividing average revenue from the initial investment. ARR is the capital

budgeting method which dies not consider the time value of money as well as cash flows.

Higher the return is beneficial for the company which means company get the higher returns on

the other hand, lower return not profitable (Osadchy and Akhmetshin, 2015). So organization

compare the returns of different project and further management take decisions accordingly.

Below mention table represent the calculation of ARR for the period of 6 years where they get

the suitable return. So managers of the company have to formulate their strategies accordingly

and make decisions that they are selecting this project for the further investment or not.

Calculations are mentioned below:

Formula: Accounting rate of return = Average annual profit / Initial investment * 100

5

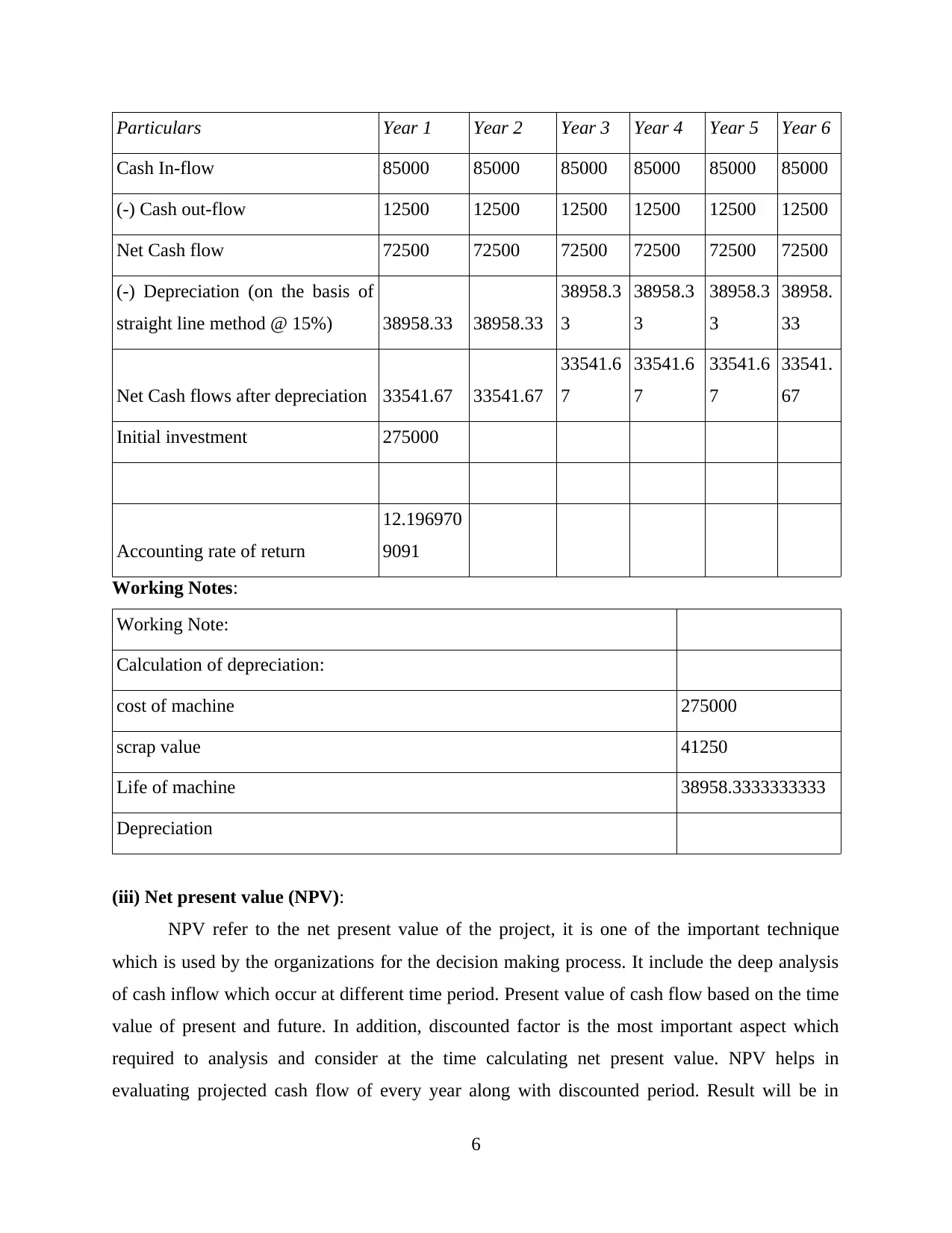

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cash In-flow 85000 85000 85000 85000 85000 85000

(-) Cash out-flow 12500 12500 12500 12500 12500 12500

Net Cash flow 72500 72500 72500 72500 72500 72500

(-) Depreciation (on the basis of

straight line method @ 15%) 38958.33 38958.33

38958.3

3

38958.3

3

38958.3

3

38958.

33

Net Cash flows after depreciation 33541.67 33541.67

33541.6

7

33541.6

7

33541.6

7

33541.

67

Initial investment 275000

Accounting rate of return

12.196970

9091

Working Notes:

Working Note:

Calculation of depreciation:

cost of machine 275000

scrap value 41250

Life of machine 38958.3333333333

Depreciation

(iii) Net present value (NPV):

NPV refer to the net present value of the project, it is one of the important technique

which is used by the organizations for the decision making process. It include the deep analysis

of cash inflow which occur at different time period. Present value of cash flow based on the time

value of present and future. In addition, discounted factor is the most important aspect which

required to analysis and consider at the time calculating net present value. NPV helps in

evaluating projected cash flow of every year along with discounted period. Result will be in

6

Cash In-flow 85000 85000 85000 85000 85000 85000

(-) Cash out-flow 12500 12500 12500 12500 12500 12500

Net Cash flow 72500 72500 72500 72500 72500 72500

(-) Depreciation (on the basis of

straight line method @ 15%) 38958.33 38958.33

38958.3

3

38958.3

3

38958.3

3

38958.

33

Net Cash flows after depreciation 33541.67 33541.67

33541.6

7

33541.6

7

33541.6

7

33541.

67

Initial investment 275000

Accounting rate of return

12.196970

9091

Working Notes:

Working Note:

Calculation of depreciation:

cost of machine 275000

scrap value 41250

Life of machine 38958.3333333333

Depreciation

(iii) Net present value (NPV):

NPV refer to the net present value of the project, it is one of the important technique

which is used by the organizations for the decision making process. It include the deep analysis

of cash inflow which occur at different time period. Present value of cash flow based on the time

value of present and future. In addition, discounted factor is the most important aspect which

required to analysis and consider at the time calculating net present value. NPV helps in

evaluating projected cash flow of every year along with discounted period. Result will be in

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

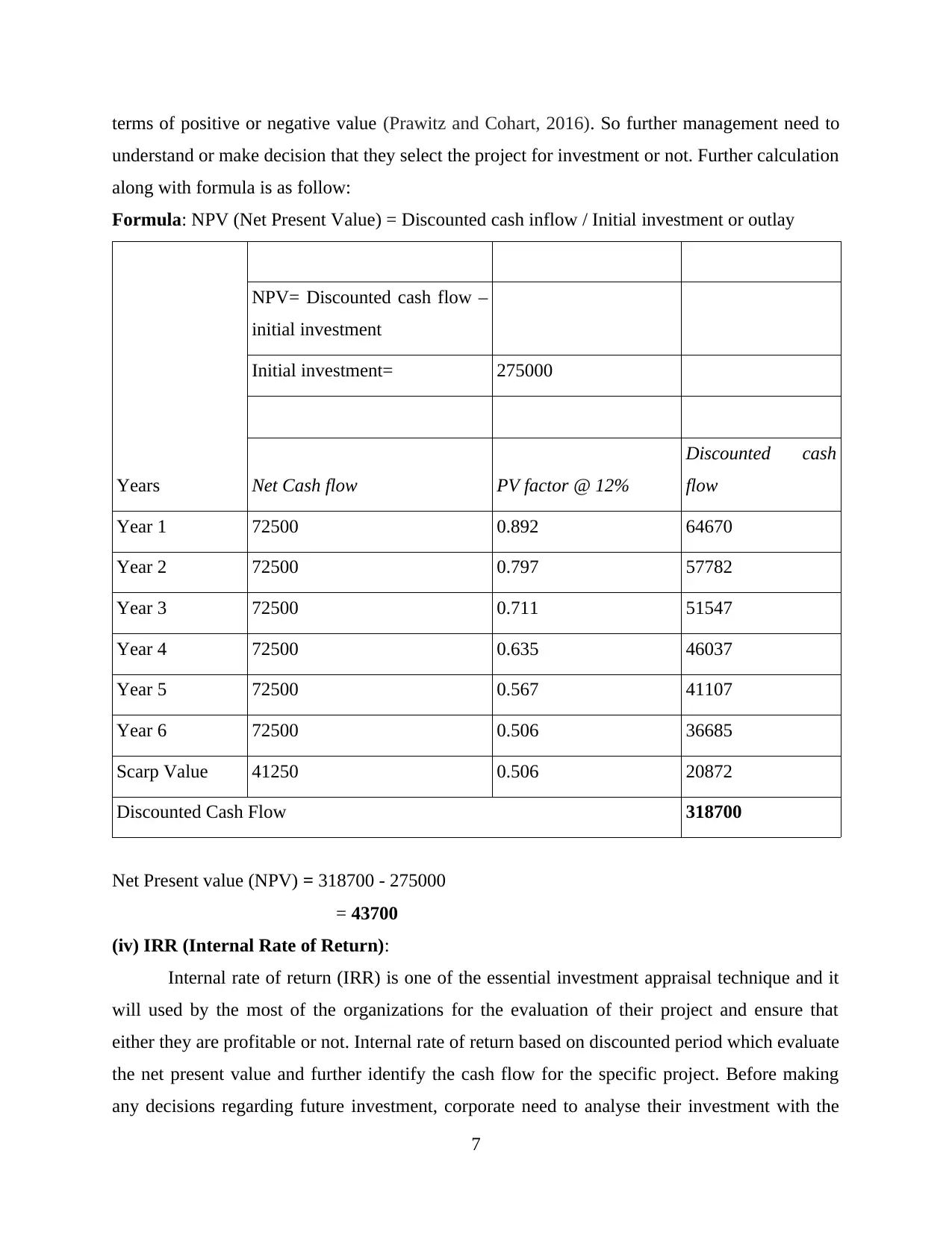

terms of positive or negative value (Prawitz and Cohart, 2016). So further management need to

understand or make decision that they select the project for investment or not. Further calculation

along with formula is as follow:

Formula: NPV (Net Present Value) = Discounted cash inflow / Initial investment or outlay

Years

NPV= Discounted cash flow –

initial investment

Initial investment= 275000

Net Cash flow PV factor @ 12%

Discounted cash

flow

Year 1 72500 0.892 64670

Year 2 72500 0.797 57782

Year 3 72500 0.711 51547

Year 4 72500 0.635 46037

Year 5 72500 0.567 41107

Year 6 72500 0.506 36685

Scarp Value 41250 0.506 20872

Discounted Cash Flow 318700

Net Present value (NPV) = 318700 - 275000

= 43700

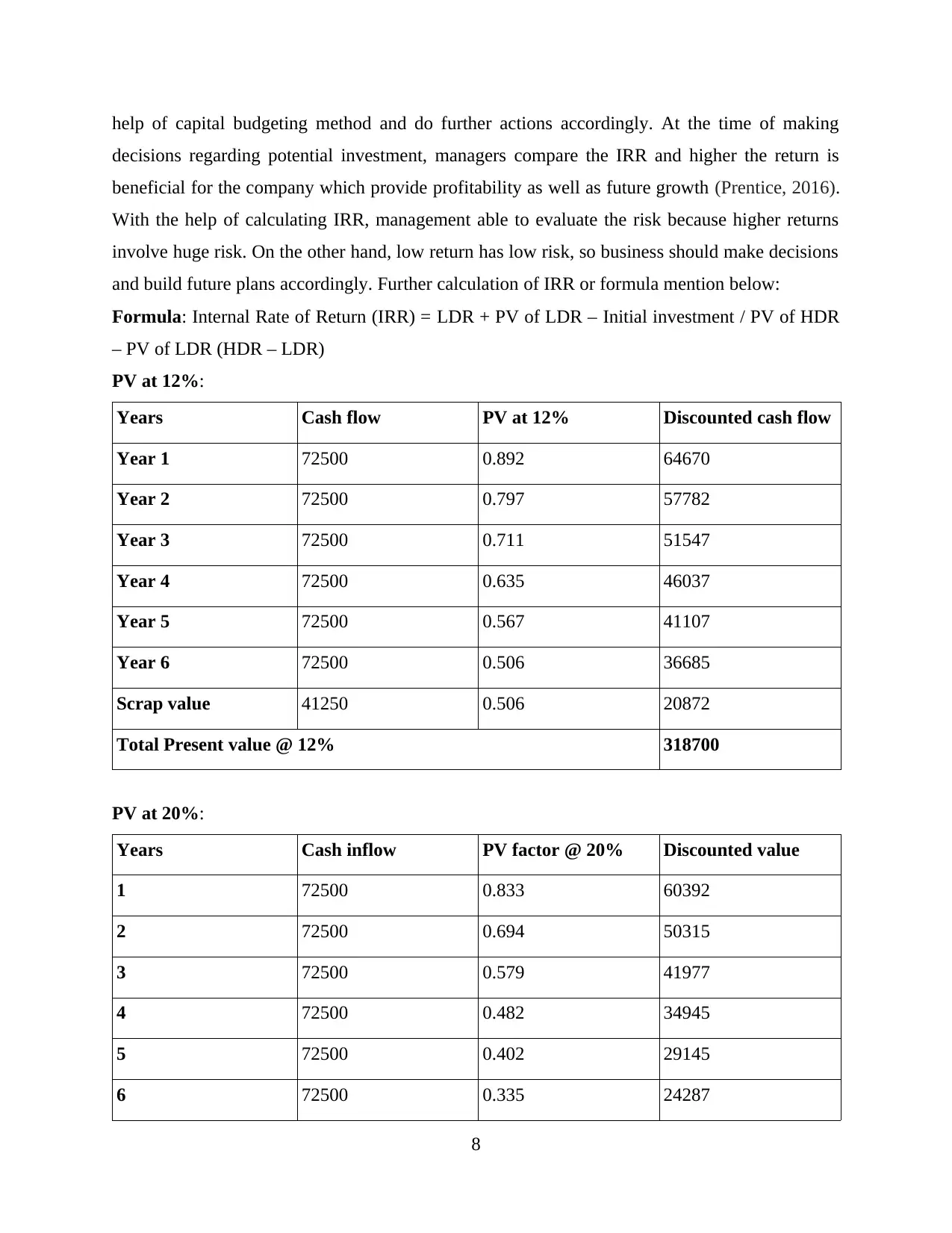

(iv) IRR (Internal Rate of Return):

Internal rate of return (IRR) is one of the essential investment appraisal technique and it

will used by the most of the organizations for the evaluation of their project and ensure that

either they are profitable or not. Internal rate of return based on discounted period which evaluate

the net present value and further identify the cash flow for the specific project. Before making

any decisions regarding future investment, corporate need to analyse their investment with the

7

understand or make decision that they select the project for investment or not. Further calculation

along with formula is as follow:

Formula: NPV (Net Present Value) = Discounted cash inflow / Initial investment or outlay

Years

NPV= Discounted cash flow –

initial investment

Initial investment= 275000

Net Cash flow PV factor @ 12%

Discounted cash

flow

Year 1 72500 0.892 64670

Year 2 72500 0.797 57782

Year 3 72500 0.711 51547

Year 4 72500 0.635 46037

Year 5 72500 0.567 41107

Year 6 72500 0.506 36685

Scarp Value 41250 0.506 20872

Discounted Cash Flow 318700

Net Present value (NPV) = 318700 - 275000

= 43700

(iv) IRR (Internal Rate of Return):

Internal rate of return (IRR) is one of the essential investment appraisal technique and it

will used by the most of the organizations for the evaluation of their project and ensure that

either they are profitable or not. Internal rate of return based on discounted period which evaluate

the net present value and further identify the cash flow for the specific project. Before making

any decisions regarding future investment, corporate need to analyse their investment with the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

help of capital budgeting method and do further actions accordingly. At the time of making

decisions regarding potential investment, managers compare the IRR and higher the return is

beneficial for the company which provide profitability as well as future growth (Prentice, 2016).

With the help of calculating IRR, management able to evaluate the risk because higher returns

involve huge risk. On the other hand, low return has low risk, so business should make decisions

and build future plans accordingly. Further calculation of IRR or formula mention below:

Formula: Internal Rate of Return (IRR) = LDR + PV of LDR – Initial investment / PV of HDR

– PV of LDR (HDR – LDR)

PV at 12%:

Years Cash flow PV at 12% Discounted cash flow

Year 1 72500 0.892 64670

Year 2 72500 0.797 57782

Year 3 72500 0.711 51547

Year 4 72500 0.635 46037

Year 5 72500 0.567 41107

Year 6 72500 0.506 36685

Scrap value 41250 0.506 20872

Total Present value @ 12% 318700

PV at 20%:

Years Cash inflow PV factor @ 20% Discounted value

1 72500 0.833 60392

2 72500 0.694 50315

3 72500 0.579 41977

4 72500 0.482 34945

5 72500 0.402 29145

6 72500 0.335 24287

8

decisions regarding potential investment, managers compare the IRR and higher the return is

beneficial for the company which provide profitability as well as future growth (Prentice, 2016).

With the help of calculating IRR, management able to evaluate the risk because higher returns

involve huge risk. On the other hand, low return has low risk, so business should make decisions

and build future plans accordingly. Further calculation of IRR or formula mention below:

Formula: Internal Rate of Return (IRR) = LDR + PV of LDR – Initial investment / PV of HDR

– PV of LDR (HDR – LDR)

PV at 12%:

Years Cash flow PV at 12% Discounted cash flow

Year 1 72500 0.892 64670

Year 2 72500 0.797 57782

Year 3 72500 0.711 51547

Year 4 72500 0.635 46037

Year 5 72500 0.567 41107

Year 6 72500 0.506 36685

Scrap value 41250 0.506 20872

Total Present value @ 12% 318700

PV at 20%:

Years Cash inflow PV factor @ 20% Discounted value

1 72500 0.833 60392

2 72500 0.694 50315

3 72500 0.579 41977

4 72500 0.482 34945

5 72500 0.402 29145

6 72500 0.335 24287

8

Scrap value 41250 0.335 13818

Total Present value @ 20% 254880

Interval Rate of Return (IRR) = 12 + ( 318703 – 275000 ) / ( 254881 – 318703 ) * ( 20 – 12 )

= 12 + 43703 / -63881 * ( 8 )

= 12 + ( -0.68 ) * 8

= 12 – 5.44

= 6.56 %

Recommendation:

From the above observation it has been recommended that, if Lovewell company bought

new machinery for business operations then it will beneficial for them as well as profitable.

Because it has been analysed that if Lovewell invest in the new machinery then the payback

period of this project is 3.79 years. It means, company recover the amount in the approx 4 years

and the accounting rate of return was 12.19 %. It is observed that, ARR is in favourable

condition which means, if they invest in this project so they get the around 12 % return which is

very good as well as profitable for the business(Rampini, Viswanathan and Vuillemey, 2019).

Net present value of the company is 43700 which is positive that means investment in this

machinery is beneficial for Lovewell company. IRR of this project is 6.56% that is also good

enough to invest in new machinery or maximise the productivity as well as profitability of the

business. With the help of above mention results, managers able to make decision in favour of

this project that is beneficial for the organization to invest in the new machinery for the better

production.

b. Critical evaluation of investment appraisal techniques with the help of its benefits &

drawbacks

Payback period:

Benefits:

simple to use and easy to understand, this method is use to calculate time period of the

project for the management term (Harris, 2017). This required initial cost and annual cash

flows for the getting the period of the project. This methods include few inputs and

easier method to calculate the capital budgeting method.

9

Total Present value @ 20% 254880

Interval Rate of Return (IRR) = 12 + ( 318703 – 275000 ) / ( 254881 – 318703 ) * ( 20 – 12 )

= 12 + 43703 / -63881 * ( 8 )

= 12 + ( -0.68 ) * 8

= 12 – 5.44

= 6.56 %

Recommendation:

From the above observation it has been recommended that, if Lovewell company bought

new machinery for business operations then it will beneficial for them as well as profitable.

Because it has been analysed that if Lovewell invest in the new machinery then the payback

period of this project is 3.79 years. It means, company recover the amount in the approx 4 years

and the accounting rate of return was 12.19 %. It is observed that, ARR is in favourable

condition which means, if they invest in this project so they get the around 12 % return which is

very good as well as profitable for the business(Rampini, Viswanathan and Vuillemey, 2019).

Net present value of the company is 43700 which is positive that means investment in this

machinery is beneficial for Lovewell company. IRR of this project is 6.56% that is also good

enough to invest in new machinery or maximise the productivity as well as profitability of the

business. With the help of above mention results, managers able to make decision in favour of

this project that is beneficial for the organization to invest in the new machinery for the better

production.

b. Critical evaluation of investment appraisal techniques with the help of its benefits &

drawbacks

Payback period:

Benefits:

simple to use and easy to understand, this method is use to calculate time period of the

project for the management term (Harris, 2017). This required initial cost and annual cash

flows for the getting the period of the project. This methods include few inputs and

easier method to calculate the capital budgeting method.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.