Financial Management: Dividend Policy, Mergers and Takeovers Report

VerifiedAdded on 2023/01/12

|17

|3594

|20

Report

AI Summary

This report delves into financial management, focusing on dividend policy and mergers & acquisitions. The first section examines dividend strategies, including factors influencing dividend size, practical implementation issues, and the impact of different dividend options (cash, scrip, and share repurchase) on shareholder wealth. It uses a case study of Squeezeco to illustrate these concepts. The second part explores mergers and takeovers, specifically the valuation of a target company (Trojan plc) by Aztec, utilizing techniques such as price-earnings ratio, dividend valuation, and discounted cash flow methods. The report highlights the problems associated with these valuation techniques. Calculations are included to demonstrate dividend growth rate, fair price determination, and the impact of changes in the required rate of return. The report aims to provide a comprehensive understanding of dividend policy and M&A strategies in financial decision-making.

FINANCIAL MANGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION:..........................................................................................................................3

1. DIVIDEND POLICY...............................................................................................................4

1.1 The size of the annual dividend to return to its shareholders............................................4

1.2 Practical issues that need to be considered when deciding on the size of the dividend

payment........................................................................................................................................5

1.3 Effect of options on the wealth of shareholder.................................................................6

1.4 Critically discuss how company’s decision will be influenced by opportunity to invest

£70m in a project.........................................................................................................................8

2. MERGERS AND TAKEOVERS.............................................................................................9

2.1 Price/earnings ratio:..........................................................................................................9

2.2 Dividend valuation method................................................................................................10

2.2 Discounted cash flow method.........................................................................................11

2.3 Problems associated with using the above valuation techniques....................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION:..........................................................................................................................3

1. DIVIDEND POLICY...............................................................................................................4

1.1 The size of the annual dividend to return to its shareholders............................................4

1.2 Practical issues that need to be considered when deciding on the size of the dividend

payment........................................................................................................................................5

1.3 Effect of options on the wealth of shareholder.................................................................6

1.4 Critically discuss how company’s decision will be influenced by opportunity to invest

£70m in a project.........................................................................................................................8

2. MERGERS AND TAKEOVERS.............................................................................................9

2.1 Price/earnings ratio:..........................................................................................................9

2.2 Dividend valuation method................................................................................................10

2.2 Discounted cash flow method.........................................................................................11

2.3 Problems associated with using the above valuation techniques....................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION:

This project report consists of two question; first question will cover the concept of dividend

policy other question will cover strategies Mergers and acquisition concept. Report shows

various calculations such as calculation of dividend growth rate, identifying average growth

rate for determination of fair price value of the shares; impact of change in required rate of

return by shareholders on fair price of share is also analyzed. Second part calculation includes

number of issued share capital, ordinary to right issues share ratio and earnings per shares.

This report will cover how to calculate fair price through dividend growth model and what

problems faced by company in valuing shares through this model.

Project contains case study of two hypothetical companies; Squeezeco and Aztec; where first

company is looking for distribute dividend among its shareholders with having three

alternatives, report will show which option is best for company. On the other hand; second

company wants to takeover Trojan plc in near future; the main issue facing by Aztec is

deciding the value of takeover. For this various analyses like price earnings ratio, dividend

valuation and discounted cash flow has been done to support decision of the company.

This project report consists of two question; first question will cover the concept of dividend

policy other question will cover strategies Mergers and acquisition concept. Report shows

various calculations such as calculation of dividend growth rate, identifying average growth

rate for determination of fair price value of the shares; impact of change in required rate of

return by shareholders on fair price of share is also analyzed. Second part calculation includes

number of issued share capital, ordinary to right issues share ratio and earnings per shares.

This report will cover how to calculate fair price through dividend growth model and what

problems faced by company in valuing shares through this model.

Project contains case study of two hypothetical companies; Squeezeco and Aztec; where first

company is looking for distribute dividend among its shareholders with having three

alternatives, report will show which option is best for company. On the other hand; second

company wants to takeover Trojan plc in near future; the main issue facing by Aztec is

deciding the value of takeover. For this various analyses like price earnings ratio, dividend

valuation and discounted cash flow has been done to support decision of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. DIVIDEND POLICY

1.1 The size of the annual dividend to return to its shareholders

A company’s dividend policy means mix of strategies for deciding how much

percentage of total earnings after tax has to be shared with outstanding dividend

shareholders. There are two types of shares issued by the company; preference shares

and equity shares, where preference shareholders are liability for the company because

they need to be paid fixed rate of dividend regardless of profit or loss to the company

and they don’t have decision powers in firm. On the other hand; equity holders are

decision makers but not liable to get fixed rate of return (Kadu and Oluoch, 2018).

Company pays off dividend to equity holders to maintain good relation and demand of

firm’s shares in the market. The main issue faces by Squeezeco is deciding the

proportion of annual dividend to be shared among equity holders. Some of the factors

to be considered while deciding annual dividend are discussed below:

1. Working capital required: Squeezeco needs to analyze how much working capital it

requires upcoming year. As working capital is necessary to run business and meet

day to day expenses of the company. So, best thing is to deduct future working

capital requirement from current years earning (Ottoo, 2018).

2. Future expansion plan: If company is looking for merger or takeover or opening

new factory; it requires some fund. Therefore in this case to attract more

shareholders at high market price, it could pay dividend at high payout ratio.

3. Matching with cost of debt: Under this factor; Squeenzeco can match the cost of

equity with cost of debt to decide how much dividend it should pay to shareholders.

For instance; for raising 50 million pound through at the rate of 7%; total cost of

debt for year will be 3.5 million pound. Hence; if company is raising same amount

though equity shares, then it should not pay more than 3.5 million to share holders.

4. Provision for unexpected events: Besides working capital requirement; the another

factor which company should be considered is any unexpected activity during year

such as instant increase in demand, strike, remuneration to government, urgent

1.1 The size of the annual dividend to return to its shareholders

A company’s dividend policy means mix of strategies for deciding how much

percentage of total earnings after tax has to be shared with outstanding dividend

shareholders. There are two types of shares issued by the company; preference shares

and equity shares, where preference shareholders are liability for the company because

they need to be paid fixed rate of dividend regardless of profit or loss to the company

and they don’t have decision powers in firm. On the other hand; equity holders are

decision makers but not liable to get fixed rate of return (Kadu and Oluoch, 2018).

Company pays off dividend to equity holders to maintain good relation and demand of

firm’s shares in the market. The main issue faces by Squeezeco is deciding the

proportion of annual dividend to be shared among equity holders. Some of the factors

to be considered while deciding annual dividend are discussed below:

1. Working capital required: Squeezeco needs to analyze how much working capital it

requires upcoming year. As working capital is necessary to run business and meet

day to day expenses of the company. So, best thing is to deduct future working

capital requirement from current years earning (Ottoo, 2018).

2. Future expansion plan: If company is looking for merger or takeover or opening

new factory; it requires some fund. Therefore in this case to attract more

shareholders at high market price, it could pay dividend at high payout ratio.

3. Matching with cost of debt: Under this factor; Squeenzeco can match the cost of

equity with cost of debt to decide how much dividend it should pay to shareholders.

For instance; for raising 50 million pound through at the rate of 7%; total cost of

debt for year will be 3.5 million pound. Hence; if company is raising same amount

though equity shares, then it should not pay more than 3.5 million to share holders.

4. Provision for unexpected events: Besides working capital requirement; the another

factor which company should be considered is any unexpected activity during year

such as instant increase in demand, strike, remuneration to government, urgent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

repairing of building or plant and machineries, legal issues, etc. Firm’s requires

instant cash; hence after proper analysis of probability of occurring of this risk,

Squeenzeco has to deduct some portion of net earnings.

Above factors are not enough to decide dividend policy and find accurate

proportion to be share with shareholders by Squeenzeco; but analyses of these

points will support company in reach to near size of the annual dividend to return to

its shareholders.

1.2 Practical issues that need to be considered when deciding on the size

of the dividend payment

It’s not only the factors which effects the decision of senior managers for the size of

dividend to be return to shareholders. Practical issues are the problems face by

business while implementing dividend policy. Some of these practical issues have

been discussed below:

1. Choice of shareholders: The first issue is choice or preference of shareholders; as

all shareholders have different tastes and thoughts. Sometimes shareholders don’t

prefer dividend, rather they want company to invest these retained earnings on

acquiring new projects or expansion of existing business. As this step will

improve share price and simultaneously increase market price of share price,

which will benefits shareholders at the time of selling shares.

2. Different options: Business owner could give dividends in two forms; cash

dividend and scrip divided. Main issue face by the company is to decide which

option should be undertaken to satisfy shareholders by meeting their choices

between scrip dividend and cash dividend.

3. Shareholders expectation; It’s hard for company to predict shareholders

expectations for dividend price; as paying more than expected will be thought by

shareholders as company is not focusing on growth and will expect that share

price will down in future.

instant cash; hence after proper analysis of probability of occurring of this risk,

Squeenzeco has to deduct some portion of net earnings.

Above factors are not enough to decide dividend policy and find accurate

proportion to be share with shareholders by Squeenzeco; but analyses of these

points will support company in reach to near size of the annual dividend to return to

its shareholders.

1.2 Practical issues that need to be considered when deciding on the size

of the dividend payment

It’s not only the factors which effects the decision of senior managers for the size of

dividend to be return to shareholders. Practical issues are the problems face by

business while implementing dividend policy. Some of these practical issues have

been discussed below:

1. Choice of shareholders: The first issue is choice or preference of shareholders; as

all shareholders have different tastes and thoughts. Sometimes shareholders don’t

prefer dividend, rather they want company to invest these retained earnings on

acquiring new projects or expansion of existing business. As this step will

improve share price and simultaneously increase market price of share price,

which will benefits shareholders at the time of selling shares.

2. Different options: Business owner could give dividends in two forms; cash

dividend and scrip divided. Main issue face by the company is to decide which

option should be undertaken to satisfy shareholders by meeting their choices

between scrip dividend and cash dividend.

3. Shareholders expectation; It’s hard for company to predict shareholders

expectations for dividend price; as paying more than expected will be thought by

shareholders as company is not focusing on growth and will expect that share

price will down in future.

4. Owner of dividend: After bring shares of the company in open market, it basically

gone through many shareholders; the problem rise is identifying who is the real

owner of shares and whom to pay dividend. Thus to solve this issue firms

considered recorded date; shareholders has to registered himself as the real owner

on particular date given by share issuer firm (Schroeder, Clark and Cathey, 2019).

5. Regulations act: Regulatory authority has abided company with set of rules to be

followed by company without failure such as firm has to maintain a fixed

proportion of reserve according to dividend paid. For instance, if company has

paid 15% dividend then it has to maintain at least 7.5% retained earnings for

reserve.

1.3 Effect of options on the wealth of shareholder

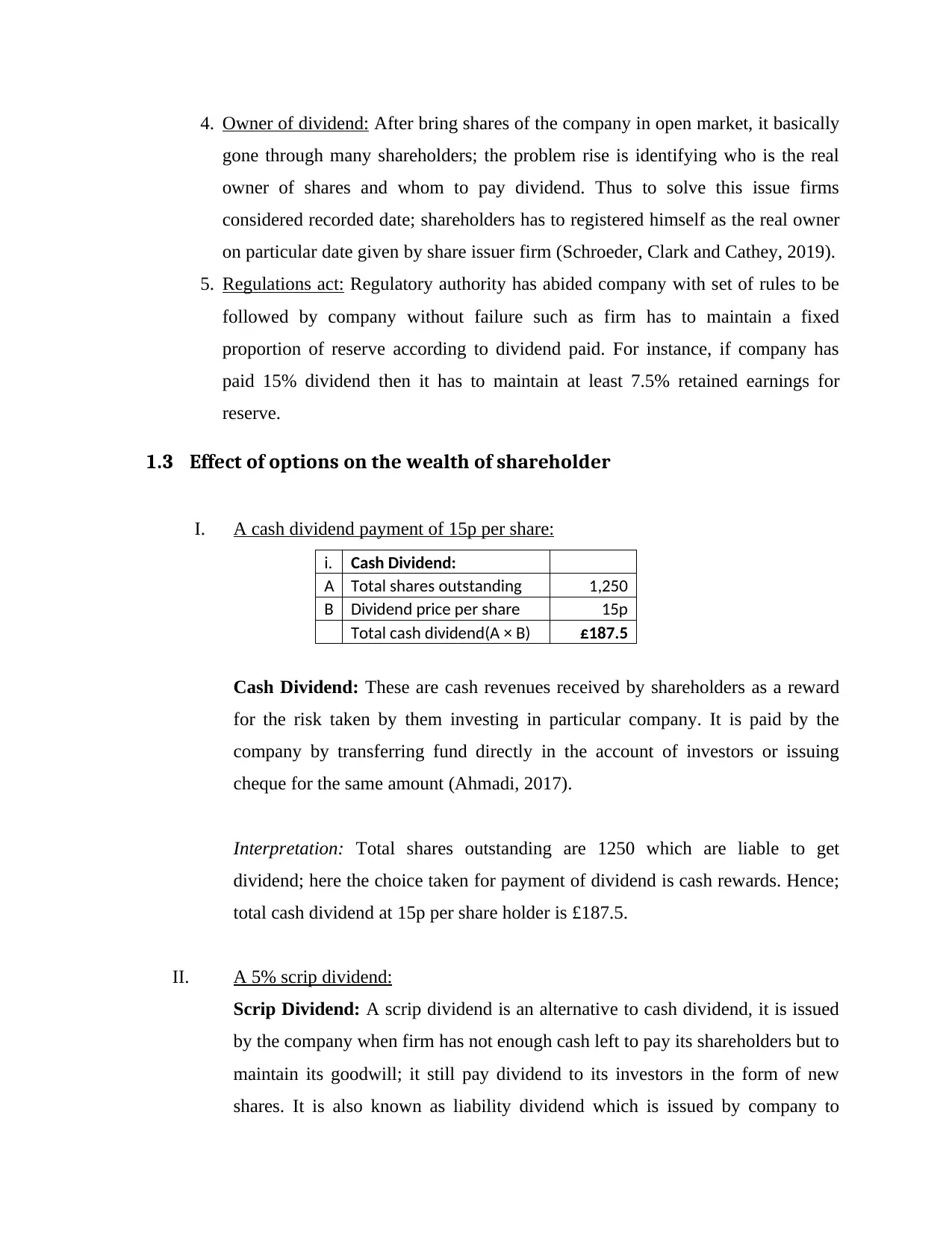

I. A cash dividend payment of 15p per share:

i. Cash Dividend:

A Total shares outstanding 1,250

B Dividend price per share 15p

Total cash dividend(A × B) £187.5

Cash Dividend: These are cash revenues received by shareholders as a reward

for the risk taken by them investing in particular company. It is paid by the

company by transferring fund directly in the account of investors or issuing

cheque for the same amount (Ahmadi, 2017).

Interpretation: Total shares outstanding are 1250 which are liable to get

dividend; here the choice taken for payment of dividend is cash rewards. Hence;

total cash dividend at 15p per share holder is £187.5.

II. A 5% scrip dividend:

Scrip Dividend: A scrip dividend is an alternative to cash dividend, it is issued

by the company when firm has not enough cash left to pay its shareholders but to

maintain its goodwill; it still pay dividend to its investors in the form of new

shares. It is also known as liability dividend which is issued by company to

gone through many shareholders; the problem rise is identifying who is the real

owner of shares and whom to pay dividend. Thus to solve this issue firms

considered recorded date; shareholders has to registered himself as the real owner

on particular date given by share issuer firm (Schroeder, Clark and Cathey, 2019).

5. Regulations act: Regulatory authority has abided company with set of rules to be

followed by company without failure such as firm has to maintain a fixed

proportion of reserve according to dividend paid. For instance, if company has

paid 15% dividend then it has to maintain at least 7.5% retained earnings for

reserve.

1.3 Effect of options on the wealth of shareholder

I. A cash dividend payment of 15p per share:

i. Cash Dividend:

A Total shares outstanding 1,250

B Dividend price per share 15p

Total cash dividend(A × B) £187.5

Cash Dividend: These are cash revenues received by shareholders as a reward

for the risk taken by them investing in particular company. It is paid by the

company by transferring fund directly in the account of investors or issuing

cheque for the same amount (Ahmadi, 2017).

Interpretation: Total shares outstanding are 1250 which are liable to get

dividend; here the choice taken for payment of dividend is cash rewards. Hence;

total cash dividend at 15p per share holder is £187.5.

II. A 5% scrip dividend:

Scrip Dividend: A scrip dividend is an alternative to cash dividend, it is issued

by the company when firm has not enough cash left to pay its shareholders but to

maintain its goodwill; it still pay dividend to its investors in the form of new

shares. It is also known as liability dividend which is issued by company to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shareholders in the form of certificate; issuing scrip dividend is sometimes given

a choice to investors or issued by company when payment of cash dividend is

not possible (Bertsatos, Sakellaris and Tsionas, 2017).

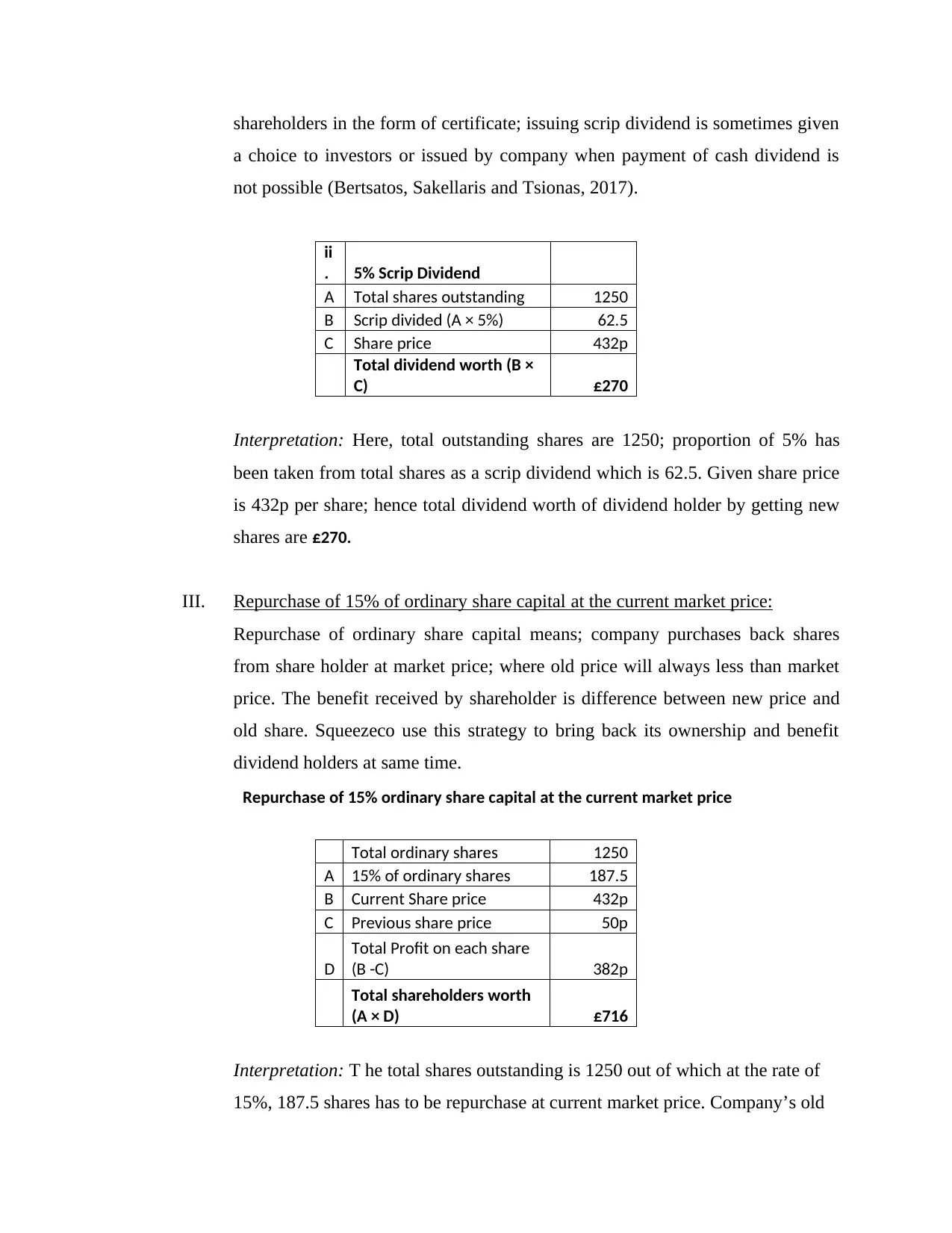

ii

. 5% Scrip Dividend

A Total shares outstanding 1250

B Scrip divided (A × 5%) 62.5

C Share price 432p

Total dividend worth (B ×

C) £270

Interpretation: Here, total outstanding shares are 1250; proportion of 5% has

been taken from total shares as a scrip dividend which is 62.5. Given share price

is 432p per share; hence total dividend worth of dividend holder by getting new

shares are £270.

III. Repurchase of 15% of ordinary share capital at the current market price:

Repurchase of ordinary share capital means; company purchases back shares

from share holder at market price; where old price will always less than market

price. The benefit received by shareholder is difference between new price and

old share. Squeezeco use this strategy to bring back its ownership and benefit

dividend holders at same time.

Repurchase of 15% ordinary share capital at the current market price

Total ordinary shares 1250

A 15% of ordinary shares 187.5

B Current Share price 432p

C Previous share price 50p

D

Total Profit on each share

(B -C) 382p

Total shareholders worth

(A × D) £716

Interpretation: T he total shares outstanding is 1250 out of which at the rate of

15%, 187.5 shares has to be repurchase at current market price. Company’s old

a choice to investors or issued by company when payment of cash dividend is

not possible (Bertsatos, Sakellaris and Tsionas, 2017).

ii

. 5% Scrip Dividend

A Total shares outstanding 1250

B Scrip divided (A × 5%) 62.5

C Share price 432p

Total dividend worth (B ×

C) £270

Interpretation: Here, total outstanding shares are 1250; proportion of 5% has

been taken from total shares as a scrip dividend which is 62.5. Given share price

is 432p per share; hence total dividend worth of dividend holder by getting new

shares are £270.

III. Repurchase of 15% of ordinary share capital at the current market price:

Repurchase of ordinary share capital means; company purchases back shares

from share holder at market price; where old price will always less than market

price. The benefit received by shareholder is difference between new price and

old share. Squeezeco use this strategy to bring back its ownership and benefit

dividend holders at same time.

Repurchase of 15% ordinary share capital at the current market price

Total ordinary shares 1250

A 15% of ordinary shares 187.5

B Current Share price 432p

C Previous share price 50p

D

Total Profit on each share

(B -C) 382p

Total shareholders worth

(A × D) £716

Interpretation: T he total shares outstanding is 1250 out of which at the rate of

15%, 187.5 shares has to be repurchase at current market price. Company’s old

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

price of share was 50p and current market price is 432p; hence the difference of

both which is 382p are the profit received by shareholders. The main advantage

of this strategy is; Squeezeco buy back its share and showing it has paid it in the

form of dividend which is smart step taken by firm.

Comparison:

After comparing all three methods it was found that maximum dividend value

which increases the wealth of shareholder is option iii; where company is

repurchasing its ordinary shares back. And lowest dividend is paid in first option

where company is paying off dividend through cash dividend.

1.4 Critically discuss how company’s decision will be influenced by

opportunity to invest £70m in a project

For investing 70 million pound; the first effect on decision will be selecting alternate

for raising fund for investment. There are three options available with owner of firm;

financing through debt, rising funds through issue of equity shares or utilize reserves

and surplus. These three options have own advantages and disadvantages. The best

strategy could be using mix of all these methods. For instance; firm can breakdown the

requirement of fund into three proportions like 30% through debt, 60% through issuing

equity shares and rest 10% through reserves. In case of issuing shares company has

further three options:

Right issue of shares to existing equity holders.

Issuing preference shares having fixed rate of dividend payment and;

Issuing ordinary shares at reduced market price.

both which is 382p are the profit received by shareholders. The main advantage

of this strategy is; Squeezeco buy back its share and showing it has paid it in the

form of dividend which is smart step taken by firm.

Comparison:

After comparing all three methods it was found that maximum dividend value

which increases the wealth of shareholder is option iii; where company is

repurchasing its ordinary shares back. And lowest dividend is paid in first option

where company is paying off dividend through cash dividend.

1.4 Critically discuss how company’s decision will be influenced by

opportunity to invest £70m in a project

For investing 70 million pound; the first effect on decision will be selecting alternate

for raising fund for investment. There are three options available with owner of firm;

financing through debt, rising funds through issue of equity shares or utilize reserves

and surplus. These three options have own advantages and disadvantages. The best

strategy could be using mix of all these methods. For instance; firm can breakdown the

requirement of fund into three proportions like 30% through debt, 60% through issuing

equity shares and rest 10% through reserves. In case of issuing shares company has

further three options:

Right issue of shares to existing equity holders.

Issuing preference shares having fixed rate of dividend payment and;

Issuing ordinary shares at reduced market price.

2. MERGERS AND TAKEOVERS

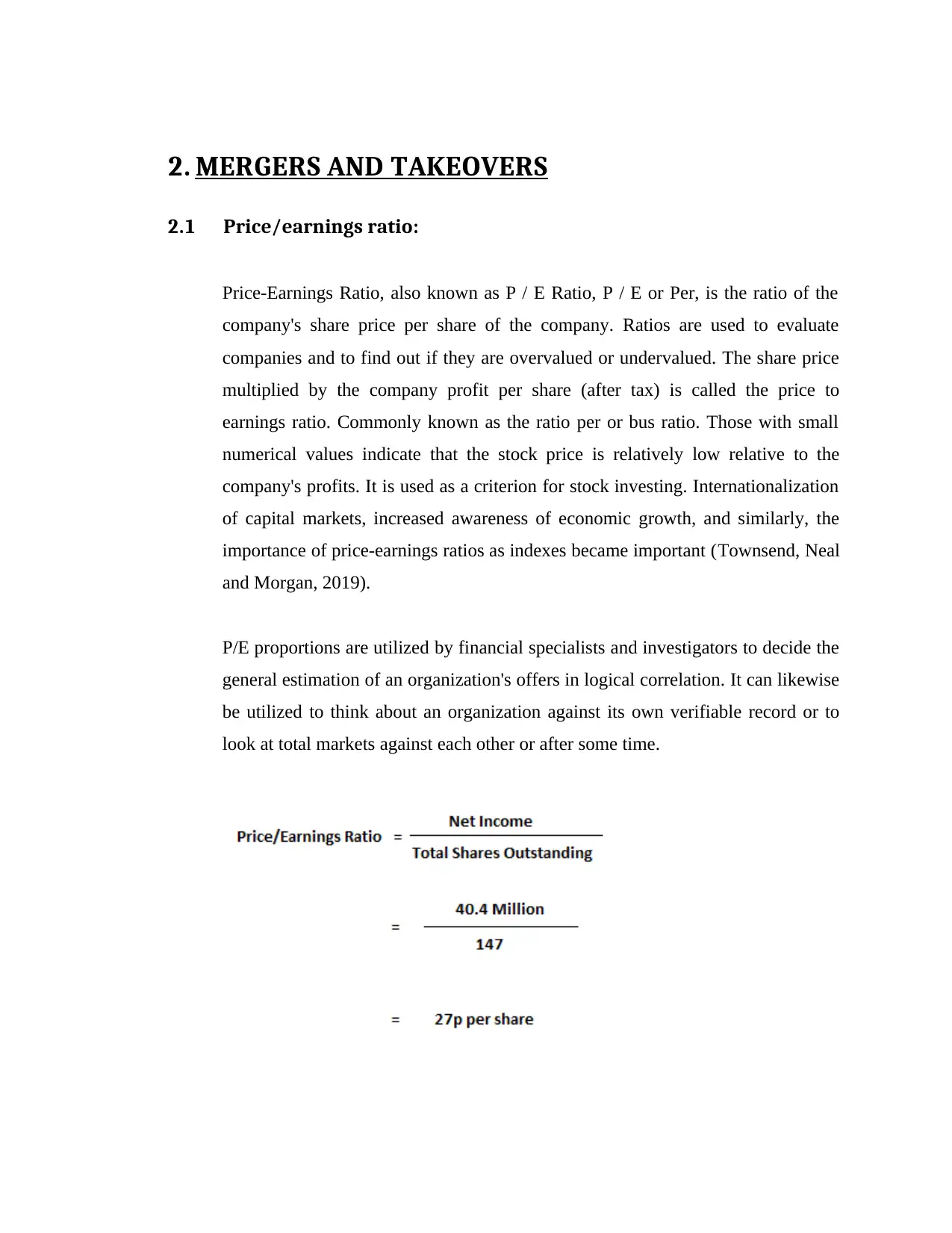

2.1 Price/earnings ratio:

Price-Earnings Ratio, also known as P / E Ratio, P / E or Per, is the ratio of the

company's share price per share of the company. Ratios are used to evaluate

companies and to find out if they are overvalued or undervalued. The share price

multiplied by the company profit per share (after tax) is called the price to

earnings ratio. Commonly known as the ratio per or bus ratio. Those with small

numerical values indicate that the stock price is relatively low relative to the

company's profits. It is used as a criterion for stock investing. Internationalization

of capital markets, increased awareness of economic growth, and similarly, the

importance of price-earnings ratios as indexes became important (Townsend, Neal

and Morgan, 2019).

P/E proportions are utilized by financial specialists and investigators to decide the

general estimation of an organization's offers in logical correlation. It can likewise

be utilized to think about an organization against its own verifiable record or to

look at total markets against each other or after some time.

2.1 Price/earnings ratio:

Price-Earnings Ratio, also known as P / E Ratio, P / E or Per, is the ratio of the

company's share price per share of the company. Ratios are used to evaluate

companies and to find out if they are overvalued or undervalued. The share price

multiplied by the company profit per share (after tax) is called the price to

earnings ratio. Commonly known as the ratio per or bus ratio. Those with small

numerical values indicate that the stock price is relatively low relative to the

company's profits. It is used as a criterion for stock investing. Internationalization

of capital markets, increased awareness of economic growth, and similarly, the

importance of price-earnings ratios as indexes became important (Townsend, Neal

and Morgan, 2019).

P/E proportions are utilized by financial specialists and investigators to decide the

general estimation of an organization's offers in logical correlation. It can likewise

be utilized to think about an organization against its own verifiable record or to

look at total markets against each other or after some time.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: The figure shows that Trojan plc, shareholders have earned 27p

per share. To get price earnings ratio or P/E ratio; total distributable net income

after deducting interest and tax is divided by total shares outstanding or shares

issue by the company. Here total net income of the company during year is 40.4

million pounds, and total outstanding shares are 147 million.

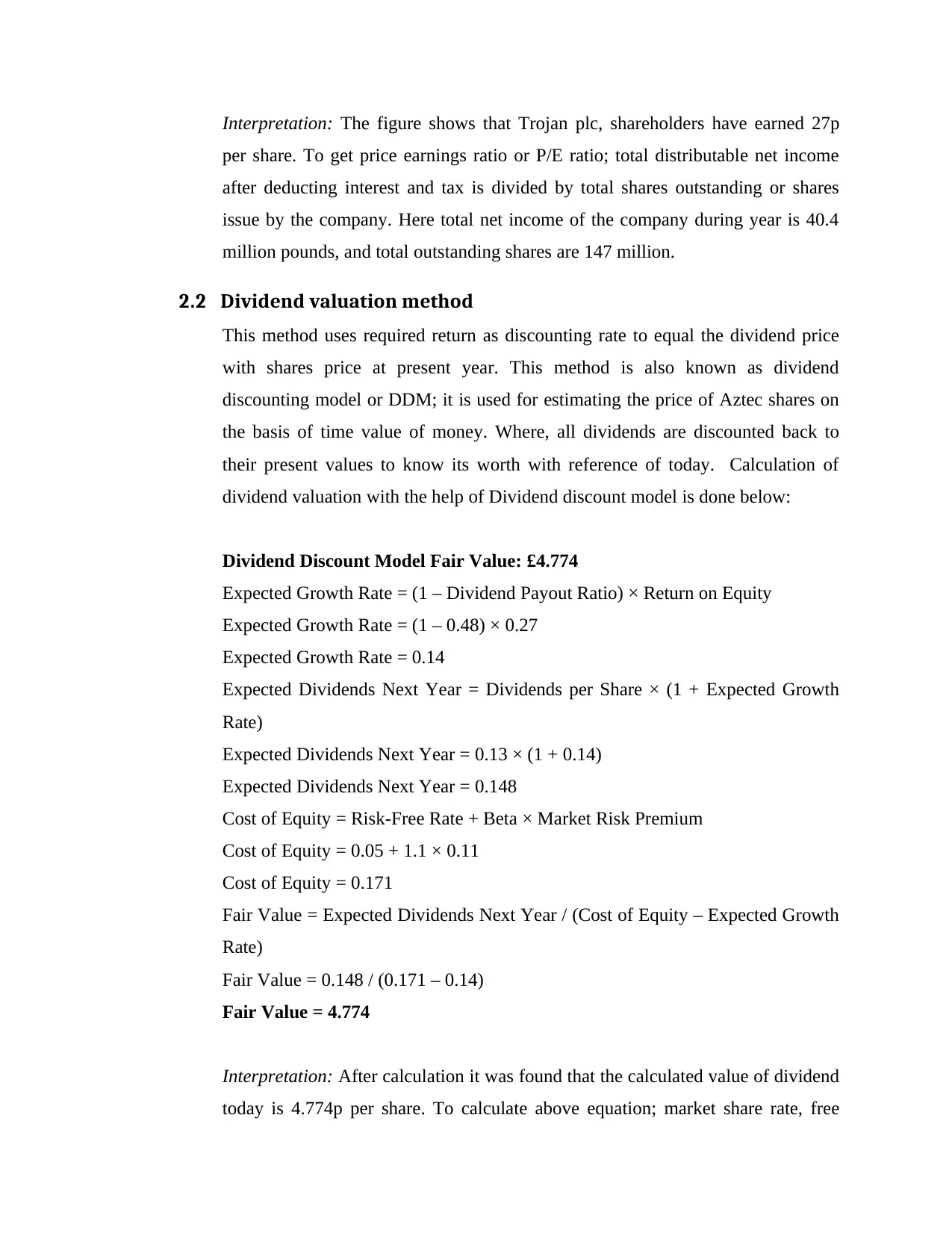

2.2 Dividend valuation method

This method uses required return as discounting rate to equal the dividend price

with shares price at present year. This method is also known as dividend

discounting model or DDM; it is used for estimating the price of Aztec shares on

the basis of time value of money. Where, all dividends are discounted back to

their present values to know its worth with reference of today. Calculation of

dividend valuation with the help of Dividend discount model is done below:

Dividend Discount Model Fair Value: £4.774

Expected Growth Rate = (1 – Dividend Payout Ratio) × Return on Equity

Expected Growth Rate = (1 – 0.48) × 0.27

Expected Growth Rate = 0.14

Expected Dividends Next Year = Dividends per Share × (1 + Expected Growth

Rate)

Expected Dividends Next Year = 0.13 × (1 + 0.14)

Expected Dividends Next Year = 0.148

Cost of Equity = Risk-Free Rate + Beta × Market Risk Premium

Cost of Equity = 0.05 + 1.1 × 0.11

Cost of Equity = 0.171

Fair Value = Expected Dividends Next Year / (Cost of Equity – Expected Growth

Rate)

Fair Value = 0.148 / (0.171 – 0.14)

Fair Value = 4.774

Interpretation: After calculation it was found that the calculated value of dividend

today is 4.774p per share. To calculate above equation; market share rate, free

per share. To get price earnings ratio or P/E ratio; total distributable net income

after deducting interest and tax is divided by total shares outstanding or shares

issue by the company. Here total net income of the company during year is 40.4

million pounds, and total outstanding shares are 147 million.

2.2 Dividend valuation method

This method uses required return as discounting rate to equal the dividend price

with shares price at present year. This method is also known as dividend

discounting model or DDM; it is used for estimating the price of Aztec shares on

the basis of time value of money. Where, all dividends are discounted back to

their present values to know its worth with reference of today. Calculation of

dividend valuation with the help of Dividend discount model is done below:

Dividend Discount Model Fair Value: £4.774

Expected Growth Rate = (1 – Dividend Payout Ratio) × Return on Equity

Expected Growth Rate = (1 – 0.48) × 0.27

Expected Growth Rate = 0.14

Expected Dividends Next Year = Dividends per Share × (1 + Expected Growth

Rate)

Expected Dividends Next Year = 0.13 × (1 + 0.14)

Expected Dividends Next Year = 0.148

Cost of Equity = Risk-Free Rate + Beta × Market Risk Premium

Cost of Equity = 0.05 + 1.1 × 0.11

Cost of Equity = 0.171

Fair Value = Expected Dividends Next Year / (Cost of Equity – Expected Growth

Rate)

Fair Value = 0.148 / (0.171 – 0.14)

Fair Value = 4.774

Interpretation: After calculation it was found that the calculated value of dividend

today is 4.774p per share. To calculate above equation; market share rate, free

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

float rate and equity beta plays major role; market rate also known as premium or

risk rate because this extra premium is taken over taking risk through investment.

While free float rates are not subject to risk because there will be no chance of

losing investment value.

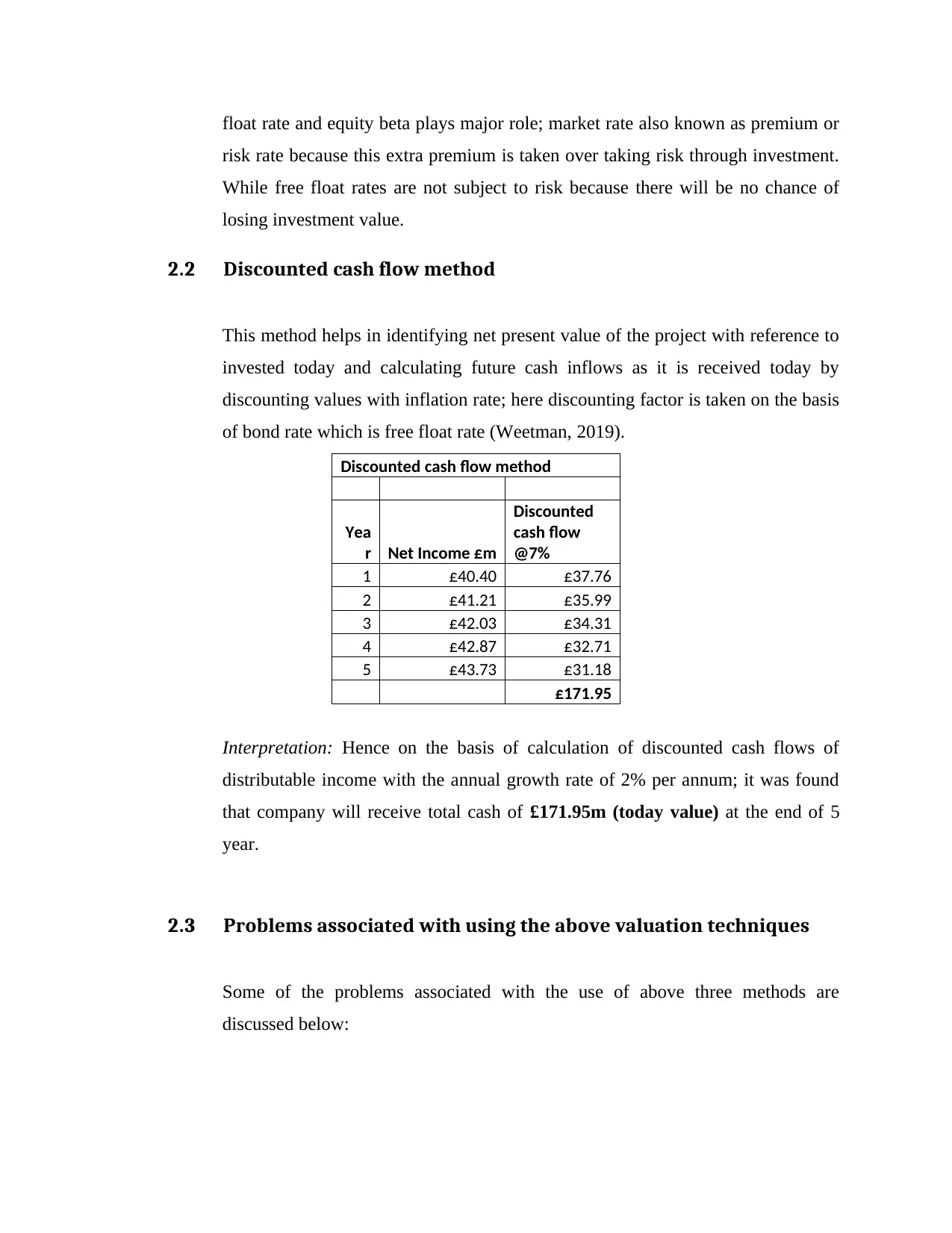

2.2 Discounted cash flow method

This method helps in identifying net present value of the project with reference to

invested today and calculating future cash inflows as it is received today by

discounting values with inflation rate; here discounting factor is taken on the basis

of bond rate which is free float rate (Weetman, 2019).

Discounted cash flow method

Yea

r Net Income £m

Discounted

cash flow

@7%

1 £40.40 £37.76

2 £41.21 £35.99

3 £42.03 £34.31

4 £42.87 £32.71

5 £43.73 £31.18

£171.95

Interpretation: Hence on the basis of calculation of discounted cash flows of

distributable income with the annual growth rate of 2% per annum; it was found

that company will receive total cash of £171.95m (today value) at the end of 5

year.

2.3 Problems associated with using the above valuation techniques

Some of the problems associated with the use of above three methods are

discussed below:

risk rate because this extra premium is taken over taking risk through investment.

While free float rates are not subject to risk because there will be no chance of

losing investment value.

2.2 Discounted cash flow method

This method helps in identifying net present value of the project with reference to

invested today and calculating future cash inflows as it is received today by

discounting values with inflation rate; here discounting factor is taken on the basis

of bond rate which is free float rate (Weetman, 2019).

Discounted cash flow method

Yea

r Net Income £m

Discounted

cash flow

@7%

1 £40.40 £37.76

2 £41.21 £35.99

3 £42.03 £34.31

4 £42.87 £32.71

5 £43.73 £31.18

£171.95

Interpretation: Hence on the basis of calculation of discounted cash flows of

distributable income with the annual growth rate of 2% per annum; it was found

that company will receive total cash of £171.95m (today value) at the end of 5

year.

2.3 Problems associated with using the above valuation techniques

Some of the problems associated with the use of above three methods are

discussed below:

Precision required: It would be more appropriate to say that given the amount

of uncertainty and risk associated with greater dividend-earnings in the distant

future and the greater attachment of shareholders to immediate income from

dividends, Mr. Gordon also His dividend theory had to be changed later, as a

result of which his theory was actually dividend capitalization model (Pratt,

2016).

Accurate forecasting is not possible: Changes are complete. The current style

is subject to change at any time. It is difficult to say when a new fashion will be

adopted by consumers and how long it will be accepted by buyers. If our

product is fashionable and popular, we can get the best results; And if our

products are not in accordance with fashion, sales will be affected. (Maynard,

2017).

The consumer's viewpoint may change at any time. Foreclosure may not be

able to predict consumers' behavior. Some market environments are early in

action. Even rumors can affect market variables. For example, when we use a

particular brand of soap, it can feel itchy on some people and if the news

spreads among the public, sales will be severely affected. (Hoggett and et. al.,

2018).

of uncertainty and risk associated with greater dividend-earnings in the distant

future and the greater attachment of shareholders to immediate income from

dividends, Mr. Gordon also His dividend theory had to be changed later, as a

result of which his theory was actually dividend capitalization model (Pratt,

2016).

Accurate forecasting is not possible: Changes are complete. The current style

is subject to change at any time. It is difficult to say when a new fashion will be

adopted by consumers and how long it will be accepted by buyers. If our

product is fashionable and popular, we can get the best results; And if our

products are not in accordance with fashion, sales will be affected. (Maynard,

2017).

The consumer's viewpoint may change at any time. Foreclosure may not be

able to predict consumers' behavior. Some market environments are early in

action. Even rumors can affect market variables. For example, when we use a

particular brand of soap, it can feel itchy on some people and if the news

spreads among the public, sales will be severely affected. (Hoggett and et. al.,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.