Financial Management: Investment Appraisal and Capital Cost Analysis

VerifiedAdded on 2023/06/12

|14

|3902

|146

Report

AI Summary

This report delves into financial management, focusing on cost of capital and investment appraisal techniques. It calculates book and market value cost of capital for Trust Plc, analyzes the impact of gearing on the overall cost of capital, and evaluates the relationship between WACC and IRR. Various investment appraisal methods, including payback period, accounting rate of return, net present value, and internal rate of return, are computed to assess project viability. The report also discusses the benefits and limitations of these methods, offering suggestions for decision-making. The analysis includes recalculating the cost of capital based on proposed debt increases and examines the effects of agency problems on investment decisions, providing a comprehensive overview of financial management principles applied to Trust Plc's investment strategies. Desklib is a platform where students can find more solved assignments and study tools.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION .............................................................................................................................................3

Main Body..........................................................................................................................................................3

1. a) Calculation Of Book Value and market value cost of capital for Trust Plc.....................................3

b) Recalculation of cost of capital of the capital and making components to projection of the finance

director......................................................................................................................................................5

c) Critical discussion on whether by introduction of gearing the overall cost of capital has been reduced

to an acceptable level:...............................................................................................................................6

d) Evaluation of relationship between WACC and IRR with respect to the investment. Discuss the effects

of agency problem on potential viable investment for Trust Plc:.............................................................6

2. Compute with the help of various investment appraisal techniques and also provide brief suggestions..7

b) Provide comments on decision made by director and examine related effects of proposal on business.

................................................................................................................................................................11

c) State the benefits and limitations of investment appraisal methods...................................................11

REFERENCES.................................................................................................................................................12

INTRODUCTION .............................................................................................................................................3

Main Body..........................................................................................................................................................3

1. a) Calculation Of Book Value and market value cost of capital for Trust Plc.....................................3

b) Recalculation of cost of capital of the capital and making components to projection of the finance

director......................................................................................................................................................5

c) Critical discussion on whether by introduction of gearing the overall cost of capital has been reduced

to an acceptable level:...............................................................................................................................6

d) Evaluation of relationship between WACC and IRR with respect to the investment. Discuss the effects

of agency problem on potential viable investment for Trust Plc:.............................................................6

2. Compute with the help of various investment appraisal techniques and also provide brief suggestions..7

b) Provide comments on decision made by director and examine related effects of proposal on business.

................................................................................................................................................................11

c) State the benefits and limitations of investment appraisal methods...................................................11

REFERENCES.................................................................................................................................................12

INTRODUCTION

The term financial management is the mechanism which is used in financial accounting to assists the

financial activities of the business enterprise during the financial year. It is a well-designed approach that

provides a manner to carry out each and every business transaction effectively and efficiently (Jorge and

et.al., 2019) . It comes up with the regulation, supervision and classification that takes place in the business

environment. In the following report there are different set of questions that recognises the concept of

financial management. In the report first two questions are answered where the evaluation of market value

and book value debts for the current and revised capital structure of an organisation. The second question

comprises of the numerical data in accordance with the different investment appraisal techniques to

calculate the value of the project and the return on investment. The models associated with the capital

budgeting techniques are also in dividend growth model, price earnings ratio method, discounted cash flow

method. Moreover, in the end report also includes the suggestion for the business enterprise that which

measure would be of a great choice among the various measures.

Main Body

1. a) Calculation Of Book Value and market value cost of capital for Trust Plc.

The cost of capital is defined as the amount of money that a company invest on the asset or a project

to get good returns on the investment (Menon., 2019) . Understanding this concept with an example-

Suppose a business owner buys a paint mixing machinery to make colours and get good amount of return

by using that machine. So, here justification of cost is really important because the purpose is to get good

return to achieve the goal.

Weighted average cost of capital is the cost that a company has to pay to its shareholders. In simple terms, if

a company want to invest in the business and funds are required for the same. Then the owner of that

enterprise can issue some stocks and bonds to the public, in order to attract the investment money from

them. This money is then used by the firm for the investment purpose.

Book value of WACC- It shows the value of the assets that is available to the business enterprise. This

balance amount of asset is in the balance sheet of the company.

Market value of WACC- If the firm evaluates the predicted cost of capital then the weighted average cost of

capital process on the ground of numerous components of the market values (Muczyński ., 2020) . Market

value is called as the rate at which the assets are supposed to exported and imported on the basis of high

The term financial management is the mechanism which is used in financial accounting to assists the

financial activities of the business enterprise during the financial year. It is a well-designed approach that

provides a manner to carry out each and every business transaction effectively and efficiently (Jorge and

et.al., 2019) . It comes up with the regulation, supervision and classification that takes place in the business

environment. In the following report there are different set of questions that recognises the concept of

financial management. In the report first two questions are answered where the evaluation of market value

and book value debts for the current and revised capital structure of an organisation. The second question

comprises of the numerical data in accordance with the different investment appraisal techniques to

calculate the value of the project and the return on investment. The models associated with the capital

budgeting techniques are also in dividend growth model, price earnings ratio method, discounted cash flow

method. Moreover, in the end report also includes the suggestion for the business enterprise that which

measure would be of a great choice among the various measures.

Main Body

1. a) Calculation Of Book Value and market value cost of capital for Trust Plc.

The cost of capital is defined as the amount of money that a company invest on the asset or a project

to get good returns on the investment (Menon., 2019) . Understanding this concept with an example-

Suppose a business owner buys a paint mixing machinery to make colours and get good amount of return

by using that machine. So, here justification of cost is really important because the purpose is to get good

return to achieve the goal.

Weighted average cost of capital is the cost that a company has to pay to its shareholders. In simple terms, if

a company want to invest in the business and funds are required for the same. Then the owner of that

enterprise can issue some stocks and bonds to the public, in order to attract the investment money from

them. This money is then used by the firm for the investment purpose.

Book value of WACC- It shows the value of the assets that is available to the business enterprise. This

balance amount of asset is in the balance sheet of the company.

Market value of WACC- If the firm evaluates the predicted cost of capital then the weighted average cost of

capital process on the ground of numerous components of the market values (Muczyński ., 2020) . Market

value is called as the rate at which the assets are supposed to exported and imported on the basis of high

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

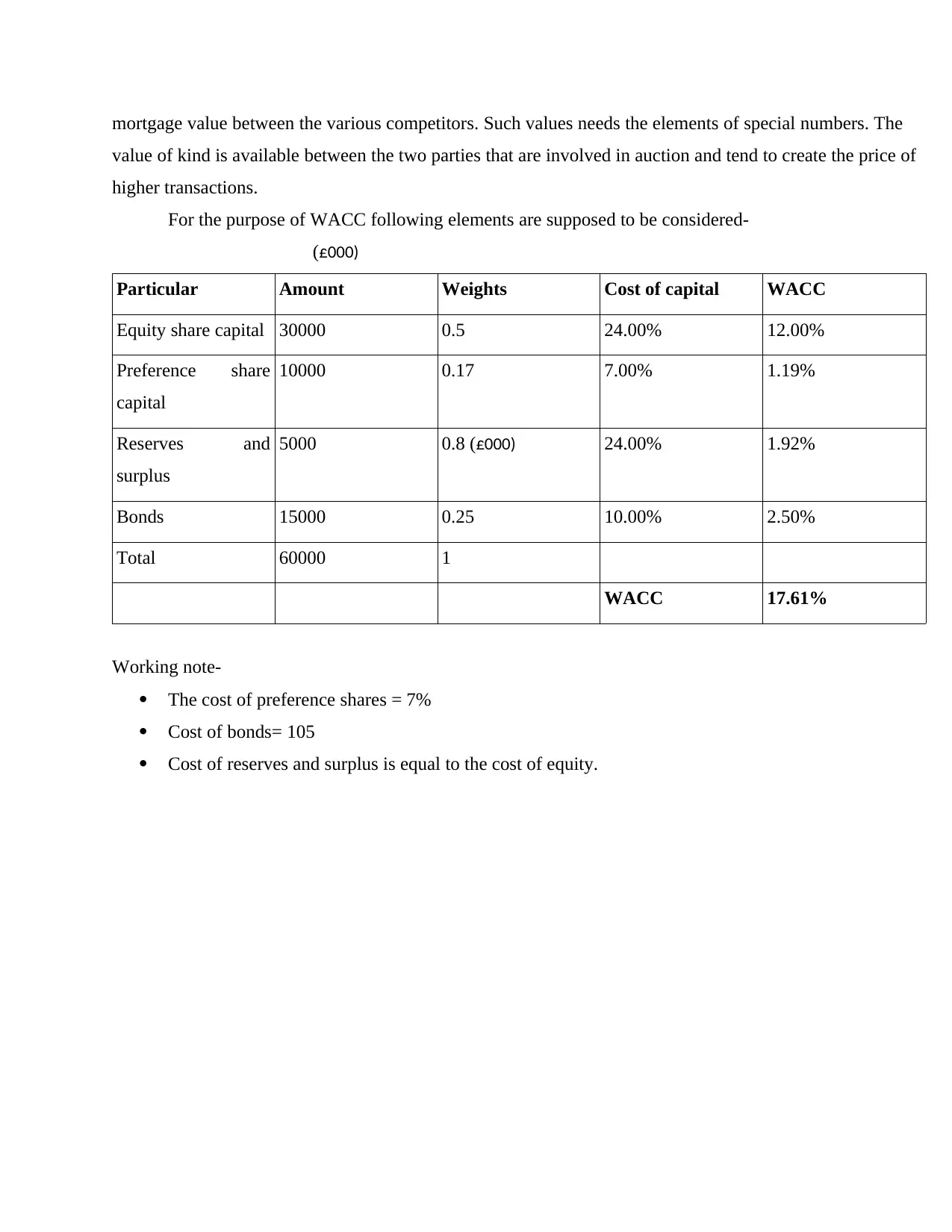

mortgage value between the various competitors. Such values needs the elements of special numbers. The

value of kind is available between the two parties that are involved in auction and tend to create the price of

higher transactions.

For the purpose of WACC following elements are supposed to be considered-

(£000)

Particular Amount Weights Cost of capital WACC

Equity share capital 30000 0.5 24.00% 12.00%

Preference share

capital

10000 0.17 7.00% 1.19%

Reserves and

surplus

5000 0.8 (£000) 24.00% 1.92%

Bonds 15000 0.25 10.00% 2.50%

Total 60000 1

WACC 17.61%

Working note-

The cost of preference shares = 7%

Cost of bonds= 105

Cost of reserves and surplus is equal to the cost of equity.

value of kind is available between the two parties that are involved in auction and tend to create the price of

higher transactions.

For the purpose of WACC following elements are supposed to be considered-

(£000)

Particular Amount Weights Cost of capital WACC

Equity share capital 30000 0.5 24.00% 12.00%

Preference share

capital

10000 0.17 7.00% 1.19%

Reserves and

surplus

5000 0.8 (£000) 24.00% 1.92%

Bonds 15000 0.25 10.00% 2.50%

Total 60000 1

WACC 17.61%

Working note-

The cost of preference shares = 7%

Cost of bonds= 105

Cost of reserves and surplus is equal to the cost of equity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of market value weighted average cost of capital-

Particular Amount Weights Cost of capital WACC

Equity share capital 76800 0.73 24.00% 17.52%

Preference share

capital

7500 0.07 7.00% 0.49%

Reserves and

surplus

5000 0.05 24.00% 1.20%

Bonds 16050 0.15 10.00% 1.50%

Total 105350 1

WACC 20.71%

b) Recalculation of cost of capital of the capital and making components to projection of the finance

director.

Ms. Zara Green the finance director of the organisation wants to bring am increase in the debt of the

business enterprise so that the reduction in cost of capital can be brought. The are giving a proposal to raise

£16m by issuing the 12 % redeemable bonds. The redeemable bonds are issued at the premium of 5% and

are redeemed after the time period of 7 years (Bakke, Mahmudi and Newton, 2020).

Calculation of bonds can be done by the formula listed below-

= {Interest (1- tax rate) + (Redeemable value – Net proceeds) / N } / {Redeemable value + Net Proceeds / 2)

* 100

= {1.92 (1 – 0.30) + (16.80 – 16) / 7} / (16.80 + 16 / 2 ) * 100

= ( 1.34 + .1143) / 16.40 * 100

= 8.87%

Revised Cost of capital

Particulars Amount Weights Cost Of

capital

WACC

Equity share

capital

88500 0.67 23.12% 15.49%

Particular Amount Weights Cost of capital WACC

Equity share capital 76800 0.73 24.00% 17.52%

Preference share

capital

7500 0.07 7.00% 0.49%

Reserves and

surplus

5000 0.05 24.00% 1.20%

Bonds 16050 0.15 10.00% 1.50%

Total 105350 1

WACC 20.71%

b) Recalculation of cost of capital of the capital and making components to projection of the finance

director.

Ms. Zara Green the finance director of the organisation wants to bring am increase in the debt of the

business enterprise so that the reduction in cost of capital can be brought. The are giving a proposal to raise

£16m by issuing the 12 % redeemable bonds. The redeemable bonds are issued at the premium of 5% and

are redeemed after the time period of 7 years (Bakke, Mahmudi and Newton, 2020).

Calculation of bonds can be done by the formula listed below-

= {Interest (1- tax rate) + (Redeemable value – Net proceeds) / N } / {Redeemable value + Net Proceeds / 2)

* 100

= {1.92 (1 – 0.30) + (16.80 – 16) / 7} / (16.80 + 16 / 2 ) * 100

= ( 1.34 + .1143) / 16.40 * 100

= 8.87%

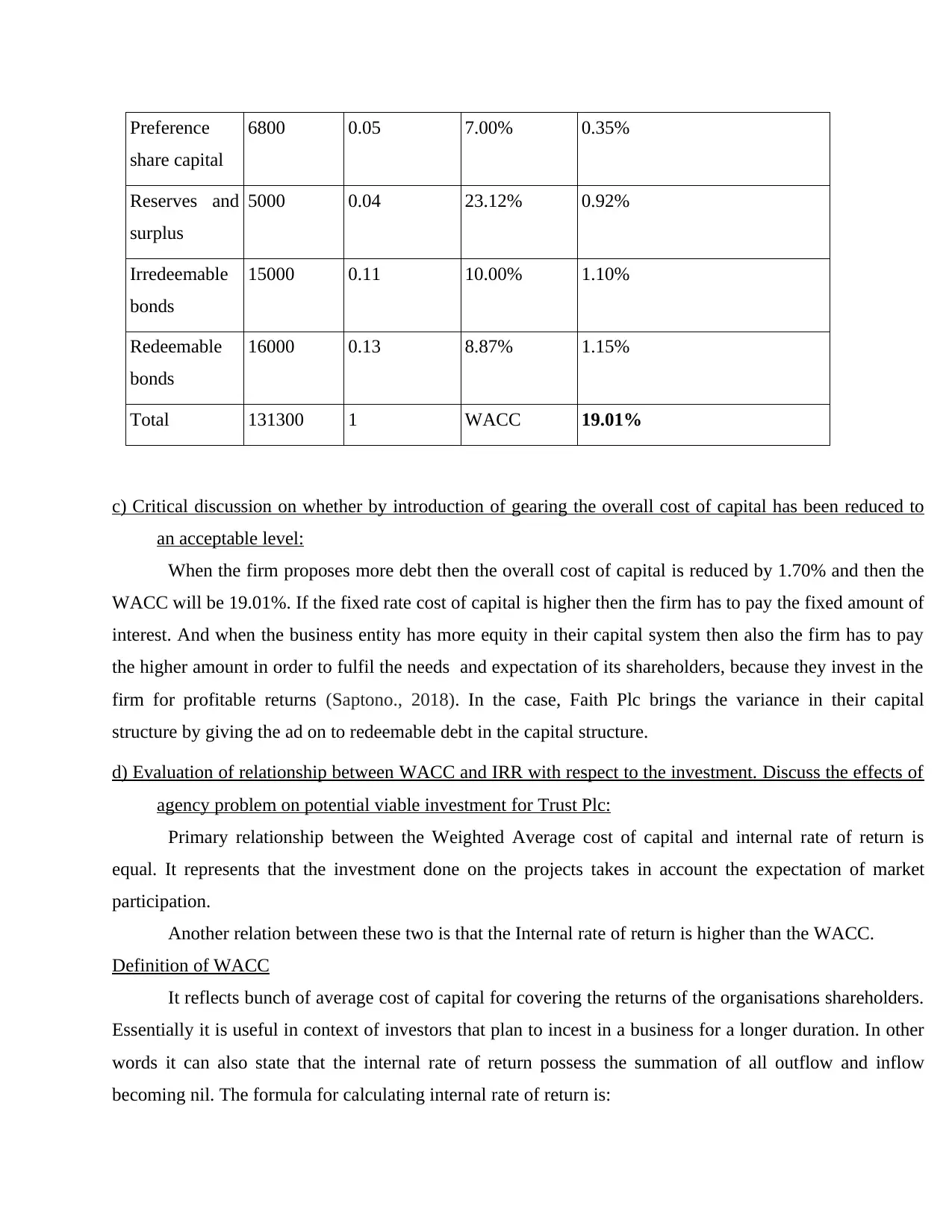

Revised Cost of capital

Particulars Amount Weights Cost Of

capital

WACC

Equity share

capital

88500 0.67 23.12% 15.49%

Preference

share capital

6800 0.05 7.00% 0.35%

Reserves and

surplus

5000 0.04 23.12% 0.92%

Irredeemable

bonds

15000 0.11 10.00% 1.10%

Redeemable

bonds

16000 0.13 8.87% 1.15%

Total 131300 1 WACC 19.01%

c) Critical discussion on whether by introduction of gearing the overall cost of capital has been reduced to

an acceptable level:

When the firm proposes more debt then the overall cost of capital is reduced by 1.70% and then the

WACC will be 19.01%. If the fixed rate cost of capital is higher then the firm has to pay the fixed amount of

interest. And when the business entity has more equity in their capital system then also the firm has to pay

the higher amount in order to fulfil the needs and expectation of its shareholders, because they invest in the

firm for profitable returns (Saptono., 2018). In the case, Faith Plc brings the variance in their capital

structure by giving the ad on to redeemable debt in the capital structure.

d) Evaluation of relationship between WACC and IRR with respect to the investment. Discuss the effects of

agency problem on potential viable investment for Trust Plc:

Primary relationship between the Weighted Average cost of capital and internal rate of return is

equal. It represents that the investment done on the projects takes in account the expectation of market

participation.

Another relation between these two is that the Internal rate of return is higher than the WACC.

Definition of WACC

It reflects bunch of average cost of capital for covering the returns of the organisations shareholders.

Essentially it is useful in context of investors that plan to incest in a business for a longer duration. In other

words it can also state that the internal rate of return possess the summation of all outflow and inflow

becoming nil. The formula for calculating internal rate of return is:

share capital

6800 0.05 7.00% 0.35%

Reserves and

surplus

5000 0.04 23.12% 0.92%

Irredeemable

bonds

15000 0.11 10.00% 1.10%

Redeemable

bonds

16000 0.13 8.87% 1.15%

Total 131300 1 WACC 19.01%

c) Critical discussion on whether by introduction of gearing the overall cost of capital has been reduced to

an acceptable level:

When the firm proposes more debt then the overall cost of capital is reduced by 1.70% and then the

WACC will be 19.01%. If the fixed rate cost of capital is higher then the firm has to pay the fixed amount of

interest. And when the business entity has more equity in their capital system then also the firm has to pay

the higher amount in order to fulfil the needs and expectation of its shareholders, because they invest in the

firm for profitable returns (Saptono., 2018). In the case, Faith Plc brings the variance in their capital

structure by giving the ad on to redeemable debt in the capital structure.

d) Evaluation of relationship between WACC and IRR with respect to the investment. Discuss the effects of

agency problem on potential viable investment for Trust Plc:

Primary relationship between the Weighted Average cost of capital and internal rate of return is

equal. It represents that the investment done on the projects takes in account the expectation of market

participation.

Another relation between these two is that the Internal rate of return is higher than the WACC.

Definition of WACC

It reflects bunch of average cost of capital for covering the returns of the organisations shareholders.

Essentially it is useful in context of investors that plan to incest in a business for a longer duration. In other

words it can also state that the internal rate of return possess the summation of all outflow and inflow

becoming nil. The formula for calculating internal rate of return is:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

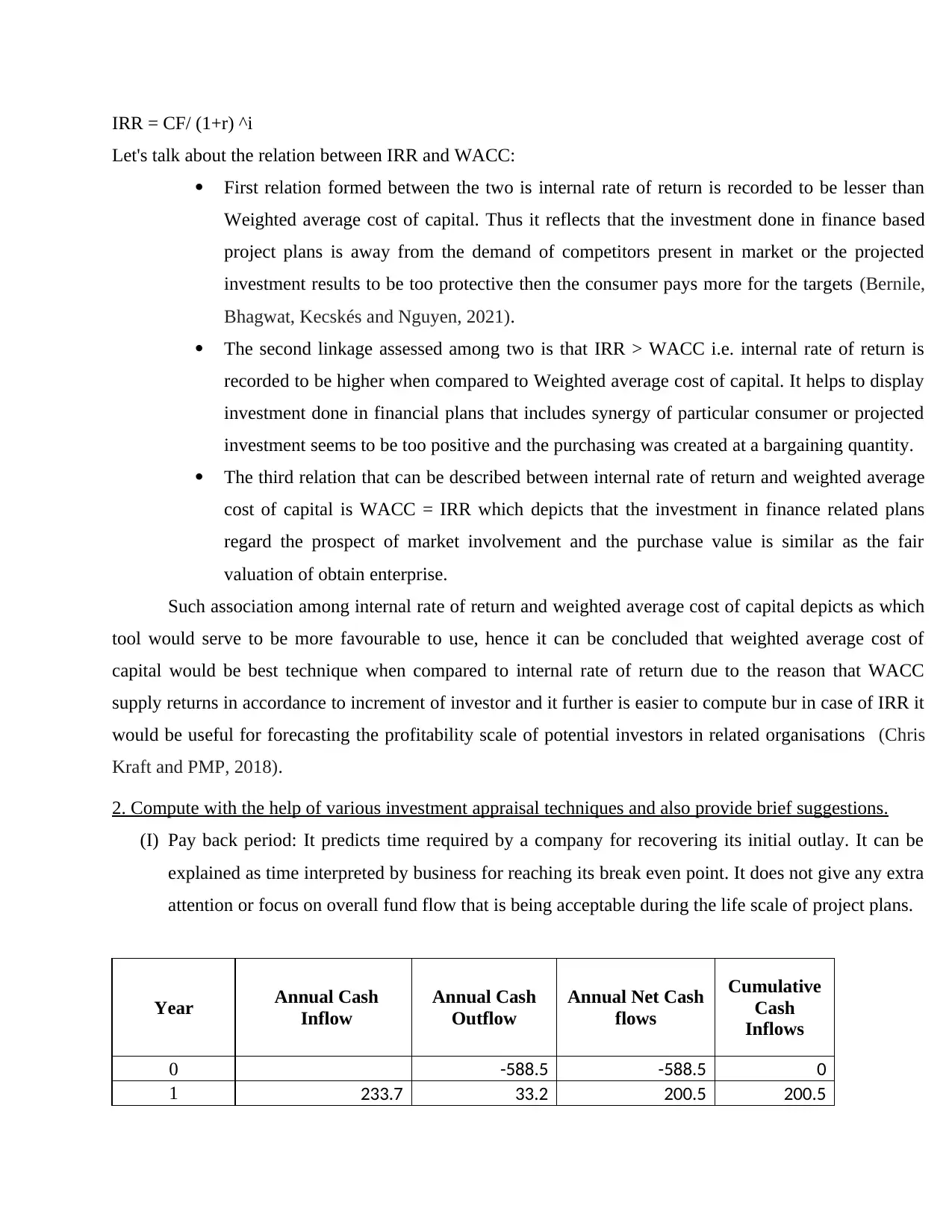

IRR = CF/ (1+r) ^i

Let's talk about the relation between IRR and WACC:

First relation formed between the two is internal rate of return is recorded to be lesser than

Weighted average cost of capital. Thus it reflects that the investment done in finance based

project plans is away from the demand of competitors present in market or the projected

investment results to be too protective then the consumer pays more for the targets (Bernile,

Bhagwat, Kecskés and Nguyen, 2021).

The second linkage assessed among two is that IRR > WACC i.e. internal rate of return is

recorded to be higher when compared to Weighted average cost of capital. It helps to display

investment done in financial plans that includes synergy of particular consumer or projected

investment seems to be too positive and the purchasing was created at a bargaining quantity.

The third relation that can be described between internal rate of return and weighted average

cost of capital is WACC = IRR which depicts that the investment in finance related plans

regard the prospect of market involvement and the purchase value is similar as the fair

valuation of obtain enterprise.

Such association among internal rate of return and weighted average cost of capital depicts as which

tool would serve to be more favourable to use, hence it can be concluded that weighted average cost of

capital would be best technique when compared to internal rate of return due to the reason that WACC

supply returns in accordance to increment of investor and it further is easier to compute bur in case of IRR it

would be useful for forecasting the profitability scale of potential investors in related organisations (Chris

Kraft and PMP, 2018).

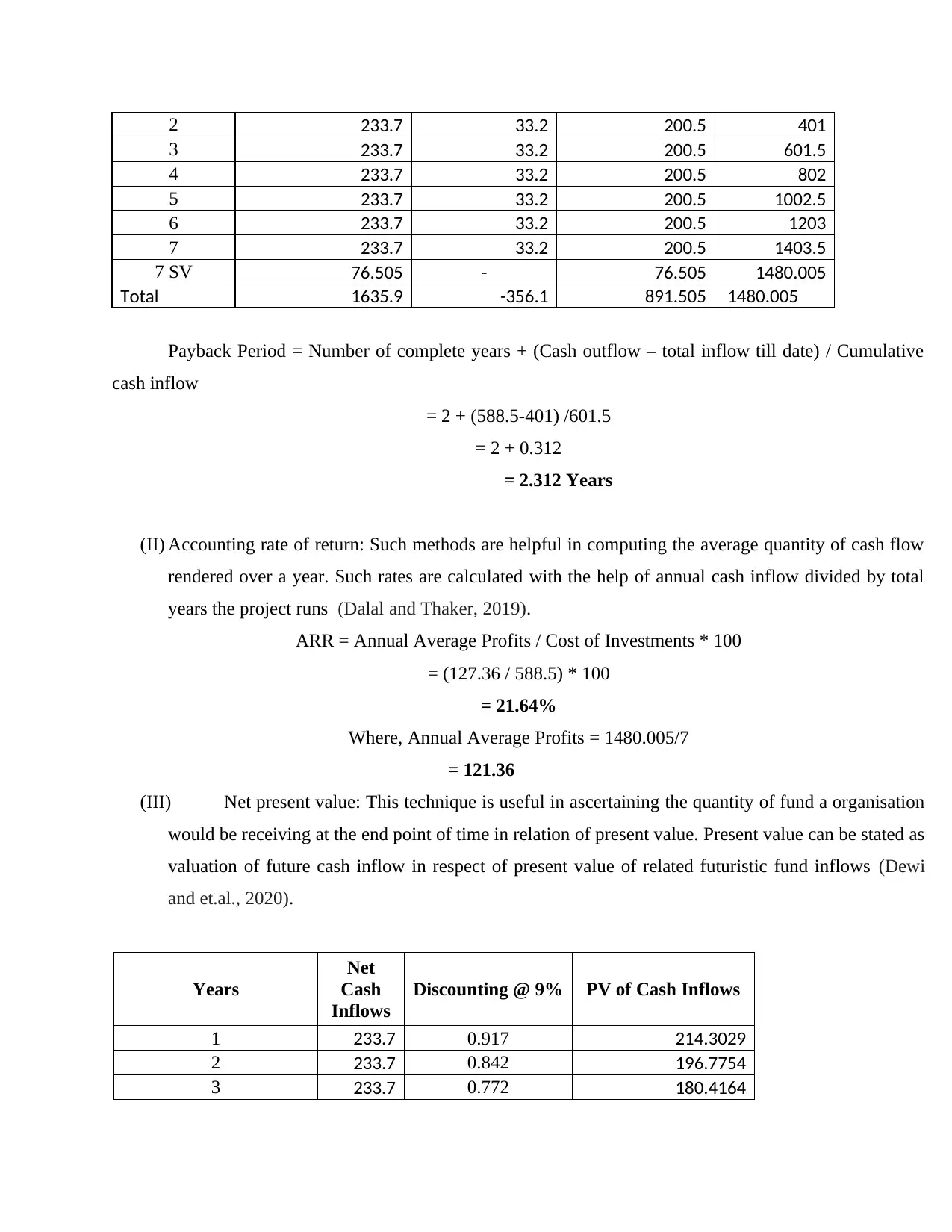

2. Compute with the help of various investment appraisal techniques and also provide brief suggestions.

(I) Pay back period: It predicts time required by a company for recovering its initial outlay. It can be

explained as time interpreted by business for reaching its break even point. It does not give any extra

attention or focus on overall fund flow that is being acceptable during the life scale of project plans.

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 -588.5 -588.5 0

1 233.7 33.2 200.5 200.5

Let's talk about the relation between IRR and WACC:

First relation formed between the two is internal rate of return is recorded to be lesser than

Weighted average cost of capital. Thus it reflects that the investment done in finance based

project plans is away from the demand of competitors present in market or the projected

investment results to be too protective then the consumer pays more for the targets (Bernile,

Bhagwat, Kecskés and Nguyen, 2021).

The second linkage assessed among two is that IRR > WACC i.e. internal rate of return is

recorded to be higher when compared to Weighted average cost of capital. It helps to display

investment done in financial plans that includes synergy of particular consumer or projected

investment seems to be too positive and the purchasing was created at a bargaining quantity.

The third relation that can be described between internal rate of return and weighted average

cost of capital is WACC = IRR which depicts that the investment in finance related plans

regard the prospect of market involvement and the purchase value is similar as the fair

valuation of obtain enterprise.

Such association among internal rate of return and weighted average cost of capital depicts as which

tool would serve to be more favourable to use, hence it can be concluded that weighted average cost of

capital would be best technique when compared to internal rate of return due to the reason that WACC

supply returns in accordance to increment of investor and it further is easier to compute bur in case of IRR it

would be useful for forecasting the profitability scale of potential investors in related organisations (Chris

Kraft and PMP, 2018).

2. Compute with the help of various investment appraisal techniques and also provide brief suggestions.

(I) Pay back period: It predicts time required by a company for recovering its initial outlay. It can be

explained as time interpreted by business for reaching its break even point. It does not give any extra

attention or focus on overall fund flow that is being acceptable during the life scale of project plans.

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 -588.5 -588.5 0

1 233.7 33.2 200.5 200.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 233.7 33.2 200.5 401

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

7 SV 76.505 - 76.505 1480.005

Total 1635.9 -356.1 891.505 1480.005

Payback Period = Number of complete years + (Cash outflow – total inflow till date) / Cumulative

cash inflow

= 2 + (588.5-401) /601.5

= 2 + 0.312

= 2.312 Years

(II) Accounting rate of return: Such methods are helpful in computing the average quantity of cash flow

rendered over a year. Such rates are calculated with the help of annual cash inflow divided by total

years the project runs (Dalal and Thaker, 2019).

ARR = Annual Average Profits / Cost of Investments * 100

= (127.36 / 588.5) * 100

= 21.64%

Where, Annual Average Profits = 1480.005/7

= 121.36

(III) Net present value: This technique is useful in ascertaining the quantity of fund a organisation

would be receiving at the end point of time in relation of present value. Present value can be stated as

valuation of future cash inflow in respect of present value of related futuristic fund inflows (Dewi

and et.al., 2020).

Years

Net

Cash

Inflows

Discounting @ 9% PV of Cash Inflows

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

3 233.7 33.2 200.5 601.5

4 233.7 33.2 200.5 802

5 233.7 33.2 200.5 1002.5

6 233.7 33.2 200.5 1203

7 233.7 33.2 200.5 1403.5

7 SV 76.505 - 76.505 1480.005

Total 1635.9 -356.1 891.505 1480.005

Payback Period = Number of complete years + (Cash outflow – total inflow till date) / Cumulative

cash inflow

= 2 + (588.5-401) /601.5

= 2 + 0.312

= 2.312 Years

(II) Accounting rate of return: Such methods are helpful in computing the average quantity of cash flow

rendered over a year. Such rates are calculated with the help of annual cash inflow divided by total

years the project runs (Dalal and Thaker, 2019).

ARR = Annual Average Profits / Cost of Investments * 100

= (127.36 / 588.5) * 100

= 21.64%

Where, Annual Average Profits = 1480.005/7

= 121.36

(III) Net present value: This technique is useful in ascertaining the quantity of fund a organisation

would be receiving at the end point of time in relation of present value. Present value can be stated as

valuation of future cash inflow in respect of present value of related futuristic fund inflows (Dewi

and et.al., 2020).

Years

Net

Cash

Inflows

Discounting @ 9% PV of Cash Inflows

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

PV of Cash Inflow (A) 1175.9784

PV of Cash Outflow

(B) 588.5

Net Present Value (A-

B) 587.48

(IV) Internal rate of return: This method is helpful to assess the profitability of the investment

amount which is invested in a chosen project. It is refereed as discounting rate that brings the worth

to zero with the help of net present value which is also explained as discounted cash flow (Grossi,

Ho and Joyce, 2020).

Years

Cash

inflows

Discounting Factor

9%

PV value of cash

inflow

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

Total Cash inflow 1175.9784

Total Cash outflow 588.5

NPV (A-B) 587.4784

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

PV of Cash Inflow (A) 1175.9784

PV of Cash Outflow

(B) 588.5

Net Present Value (A-

B) 587.48

(IV) Internal rate of return: This method is helpful to assess the profitability of the investment

amount which is invested in a chosen project. It is refereed as discounting rate that brings the worth

to zero with the help of net present value which is also explained as discounted cash flow (Grossi,

Ho and Joyce, 2020).

Years

Cash

inflows

Discounting Factor

9%

PV value of cash

inflow

1 233.7 0.917 214.3029

2 233.7 0.842 196.7754

3 233.7 0.772 180.4164

4 233.7 0.708 165.4596

5 233.7 0.65 151.905

6 233.7 0.596 139.2852

7 233.7 0.547 127.8339

Total Cash inflow 1175.9784

Total Cash outflow 588.5

NPV (A-B) 587.4784

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

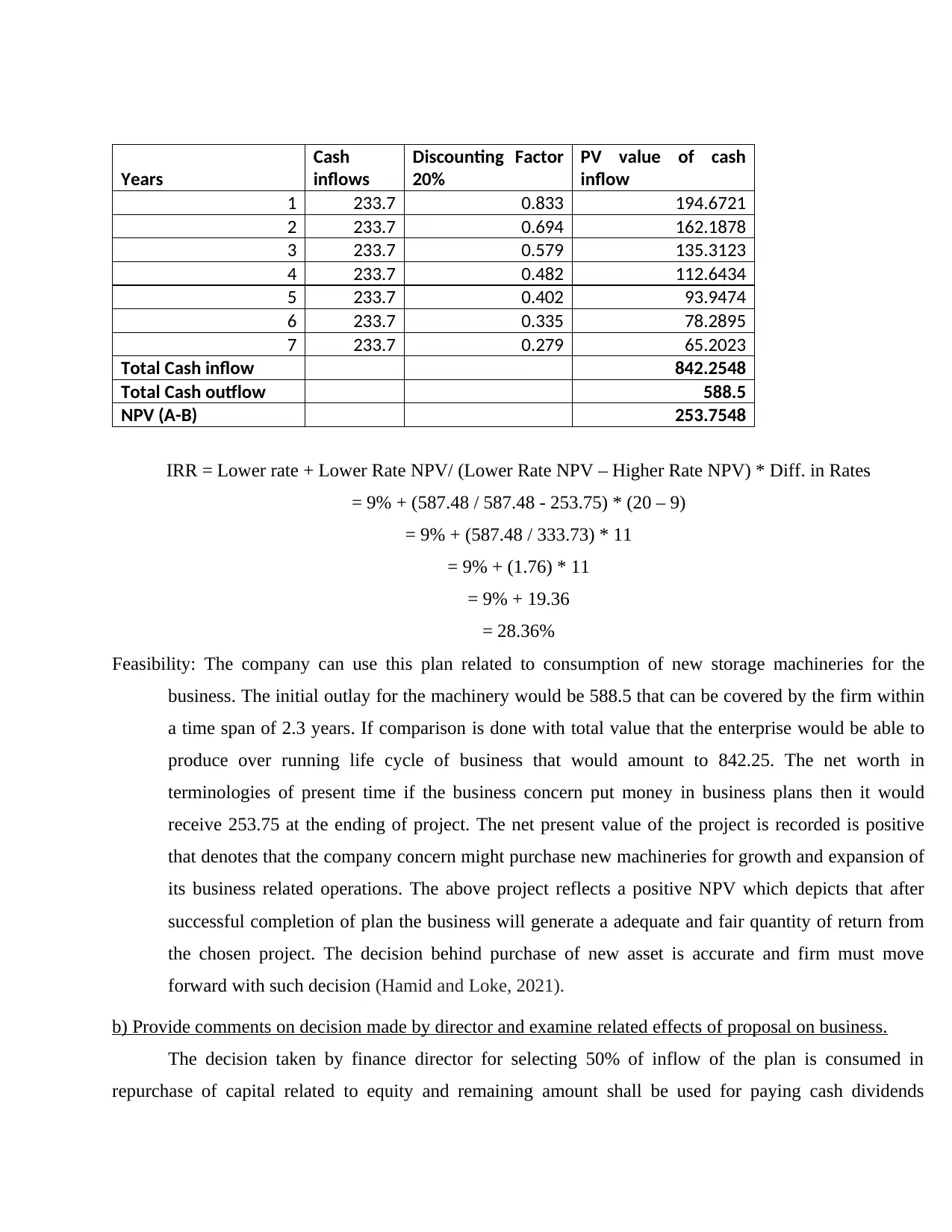

Years

Cash

inflows

Discounting Factor

20%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 9% + (587.48 / 587.48 - 253.75) * (20 – 9)

= 9% + (587.48 / 333.73) * 11

= 9% + (1.76) * 11

= 9% + 19.36

= 28.36%

Feasibility: The company can use this plan related to consumption of new storage machineries for the

business. The initial outlay for the machinery would be 588.5 that can be covered by the firm within

a time span of 2.3 years. If comparison is done with total value that the enterprise would be able to

produce over running life cycle of business that would amount to 842.25. The net worth in

terminologies of present time if the business concern put money in business plans then it would

receive 253.75 at the ending of project. The net present value of the project is recorded is positive

that denotes that the company concern might purchase new machineries for growth and expansion of

its business related operations. The above project reflects a positive NPV which depicts that after

successful completion of plan the business will generate a adequate and fair quantity of return from

the chosen project. The decision behind purchase of new asset is accurate and firm must move

forward with such decision (Hamid and Loke, 2021).

b) Provide comments on decision made by director and examine related effects of proposal on business.

The decision taken by finance director for selecting 50% of inflow of the plan is consumed in

repurchase of capital related to equity and remaining amount shall be used for paying cash dividends

Cash

inflows

Discounting Factor

20%

PV value of cash

inflow

1 233.7 0.833 194.6721

2 233.7 0.694 162.1878

3 233.7 0.579 135.3123

4 233.7 0.482 112.6434

5 233.7 0.402 93.9474

6 233.7 0.335 78.2895

7 233.7 0.279 65.2023

Total Cash inflow 842.2548

Total Cash outflow 588.5

NPV (A-B) 253.7548

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 9% + (587.48 / 587.48 - 253.75) * (20 – 9)

= 9% + (587.48 / 333.73) * 11

= 9% + (1.76) * 11

= 9% + 19.36

= 28.36%

Feasibility: The company can use this plan related to consumption of new storage machineries for the

business. The initial outlay for the machinery would be 588.5 that can be covered by the firm within

a time span of 2.3 years. If comparison is done with total value that the enterprise would be able to

produce over running life cycle of business that would amount to 842.25. The net worth in

terminologies of present time if the business concern put money in business plans then it would

receive 253.75 at the ending of project. The net present value of the project is recorded is positive

that denotes that the company concern might purchase new machineries for growth and expansion of

its business related operations. The above project reflects a positive NPV which depicts that after

successful completion of plan the business will generate a adequate and fair quantity of return from

the chosen project. The decision behind purchase of new asset is accurate and firm must move

forward with such decision (Hamid and Loke, 2021).

b) Provide comments on decision made by director and examine related effects of proposal on business.

The decision taken by finance director for selecting 50% of inflow of the plan is consumed in

repurchase of capital related to equity and remaining amount shall be used for paying cash dividends

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

towards the at present equity shareholders. The company can use funds for raising promoters shareholding

in organisation that would assist in minimizing the existing debt and liabilities in a business. Buy back of

equity shares can be supported by few set of rules and regulations that are described in legal terms (Hashim,

Salleh, Shuhaimi and Ismail, 2020).

Cash dividend are payable towards investors who have made investment in related businesses.

Investors predict dividend to be received in return of their money invested in firm over a period of time.

Innovative ideas and thoughts are supported by large business possibilities, which would help to

attract new customers from environment that would be useful in finding solutions for related problems. The

company is examined through various tools and methods relating tp Investment appraisal techniques. The

firm can adapt net present value that would help to calculate accurate amount in term of present situation.

c) State the benefits and limitations of investment appraisal methods.

Payback period: It is a method which is useful for calculating time needed for covering expense of

investment. If the payback duration is lesser than it states that the investment made is attractive.

The benefits of Payback period is as under:

It is advantageous for such business firms which incline to make investments in smaller quantity.

Payback period doesn't include in excessive complex evaluation thus they do not consider complicated

factors in account. It is also easy in nature because it is simple to calculate and understand as well.

Such tool of investment appraisal concentrate on how early the money can be reverted back from the

investment that a organisation makes. Such interpretation help in computing the standard of risk with respect

to the planned project which business is planning to invest into (Jorge and et.al., 2019).

The metric is beneficial for the project which would return back amount to company in lesser duration.

Hence it can be said that such tool of capital budgeting focuses mainly on liquidity.

This technique is useful for business by providing protection against the risk factor which are linked

with long term spendings.

Limitations of Payback period:

It does not provide any assurance that if the payback period results to be short the company would

generate revenues.

The enterprises cannot depend on such techniques as it does not include discounted rates and other

related factors as well.

Internal rate of return: IT provides help and assistance towards the firm which is useful to understand &

choose better option among available alternatives. This helps in estimation of profit scale that is linked with

in organisation that would assist in minimizing the existing debt and liabilities in a business. Buy back of

equity shares can be supported by few set of rules and regulations that are described in legal terms (Hashim,

Salleh, Shuhaimi and Ismail, 2020).

Cash dividend are payable towards investors who have made investment in related businesses.

Investors predict dividend to be received in return of their money invested in firm over a period of time.

Innovative ideas and thoughts are supported by large business possibilities, which would help to

attract new customers from environment that would be useful in finding solutions for related problems. The

company is examined through various tools and methods relating tp Investment appraisal techniques. The

firm can adapt net present value that would help to calculate accurate amount in term of present situation.

c) State the benefits and limitations of investment appraisal methods.

Payback period: It is a method which is useful for calculating time needed for covering expense of

investment. If the payback duration is lesser than it states that the investment made is attractive.

The benefits of Payback period is as under:

It is advantageous for such business firms which incline to make investments in smaller quantity.

Payback period doesn't include in excessive complex evaluation thus they do not consider complicated

factors in account. It is also easy in nature because it is simple to calculate and understand as well.

Such tool of investment appraisal concentrate on how early the money can be reverted back from the

investment that a organisation makes. Such interpretation help in computing the standard of risk with respect

to the planned project which business is planning to invest into (Jorge and et.al., 2019).

The metric is beneficial for the project which would return back amount to company in lesser duration.

Hence it can be said that such tool of capital budgeting focuses mainly on liquidity.

This technique is useful for business by providing protection against the risk factor which are linked

with long term spendings.

Limitations of Payback period:

It does not provide any assurance that if the payback period results to be short the company would

generate revenues.

The enterprises cannot depend on such techniques as it does not include discounted rates and other

related factors as well.

Internal rate of return: IT provides help and assistance towards the firm which is useful to understand &

choose better option among available alternatives. This helps in estimation of profit scale that is linked with

certain project plan (Meleshenko, Usanova, Kirpikov and Kim, 2019). The IRR can be helpful and prove to

be beneficial because:

It is computed by evaluation of interests rates at which the current value of future based cash flow is

equivalent to the capital investment demanded.

The IRR method does not want the hurdle rate which would make it simple for the business to chose

project that would give the return higher than the cost of capital.

Disadvantage of IRR:

Another limitation for usage of such method is that it won't report the size of plan when comparison

between investment is demanded.

It also takes in consideration upcoming cash flow, but it also makes an supposition that future fund

flow can be invested again.

Net present value: It can be described as an accounting standard which examines the variation between the

present valuation's of present value and future based cash inflow over a certain duration (Menon, 2019).

The advantages of NPV are as under:

It is useful for organisation for providing a idea that the investment made would be helpful for

company or not.

It counts the risk fundamentals and cost of capital in future projects.

Disadvantages of net present value are stated under:

It is very complex to use such methods when the task can be compared and each of them has

variation in their life cycle.

Such tool cannot be implemented towards project that have variation in amount invested.

CONCLUSION

From the above collected data it can be asserted that the company is working for improving the work

performance of organisation. It helps to understand the importance and usefulness of Working capital and

internal rate of return. The report also helps to carry out calculations of net present value and find out ways

that would assess in increasing profitability ratio and revenue scale as well. It also serves as medium to find

ouit various tools and techniques that would contribute in efficient working of business and cutting of costs.

REFERENCES

Books and Journals

be beneficial because:

It is computed by evaluation of interests rates at which the current value of future based cash flow is

equivalent to the capital investment demanded.

The IRR method does not want the hurdle rate which would make it simple for the business to chose

project that would give the return higher than the cost of capital.

Disadvantage of IRR:

Another limitation for usage of such method is that it won't report the size of plan when comparison

between investment is demanded.

It also takes in consideration upcoming cash flow, but it also makes an supposition that future fund

flow can be invested again.

Net present value: It can be described as an accounting standard which examines the variation between the

present valuation's of present value and future based cash inflow over a certain duration (Menon, 2019).

The advantages of NPV are as under:

It is useful for organisation for providing a idea that the investment made would be helpful for

company or not.

It counts the risk fundamentals and cost of capital in future projects.

Disadvantages of net present value are stated under:

It is very complex to use such methods when the task can be compared and each of them has

variation in their life cycle.

Such tool cannot be implemented towards project that have variation in amount invested.

CONCLUSION

From the above collected data it can be asserted that the company is working for improving the work

performance of organisation. It helps to understand the importance and usefulness of Working capital and

internal rate of return. The report also helps to carry out calculations of net present value and find out ways

that would assess in increasing profitability ratio and revenue scale as well. It also serves as medium to find

ouit various tools and techniques that would contribute in efficient working of business and cutting of costs.

REFERENCES

Books and Journals

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.