CRKC7003 Financial Management: Analysis of Aunt Chiara's New Venture

VerifiedAdded on 2023/05/27

|33

|8774

|407

Report

AI Summary

This report assesses the viability of a new retail venture focused on selling nuts in Italy, planned by Aunt Chiara using her retirement funds. It includes a detailed financial plan with assumptions, pro forma financial statements (income statement, cash flow statement, and balance sheet), and a breakeven analysis to determine the minimum sales required for the business to be sustainable. The plan considers importing nuts from the USA, establishing a local business partnership, and managing startup costs. Key assumptions include exchange rates, sales growth, asset depreciation, and tax rates. The analysis aims to provide insights into the potential profitability and long-term success of the business.

0FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Executive Summary...................................................................................................................2

Details of the Plan......................................................................................................................2

Assumptions and Viability Analysis of the Plan........................................................................3

Cash Flow Statement and Financial Viability Analysis.............................................................7

Other Financial Presentation....................................................................................................17

Forecasted Balance Sheet of the Business...............................................................................26

Breakeven Analysis..................................................................................................................27

Recommendation......................................................................................................................28

Reflection.................................................................................................................................29

Reference and Bibliography.....................................................................................................31

Table of Contents

Executive Summary...................................................................................................................2

Details of the Plan......................................................................................................................2

Assumptions and Viability Analysis of the Plan........................................................................3

Cash Flow Statement and Financial Viability Analysis.............................................................7

Other Financial Presentation....................................................................................................17

Forecasted Balance Sheet of the Business...............................................................................26

Breakeven Analysis..................................................................................................................27

Recommendation......................................................................................................................28

Reflection.................................................................................................................................29

Reference and Bibliography.....................................................................................................31

2FINANCIAL MANAGEMENT

Executive Summary

The main purpose of this assessment is to analyze the viability of the business plan which is

being formulated for old aunt Chiara and the same is a new venture plan which would be

undertaken by her. The assessment would be including a detailed financial plan which is

developed for the business which is intended by Chiara. The business which is going to be

established would be in Italy and the main operations of the business is related to retail of

nuts which have a significant market in the country. The assessment considers the financial

aspects of the business plan of a retail business of different variety of nuts. The assessment

would be containing a detailed background of the business venture which is being considered

and the same would be include all the assumptions and factors which needs to be considered

by the owner of the business before taking any decisions. The financial plan would show the

assumptions which are considered while formulating the same and also would show the

preparation of the financial statements of the business. The financial statements would be

formulated on an estimation basis and would be including a profit and loss statement, cash

flow statement and a balance sheet. In addition to this, the attractiveness of the project would

be further assessed with the help of breakeven analysis which would provide an estimate of

minimum sales which the business needs to achieve in order to survive in the market and

continue its operations. This is done in order in order to assess the profit generating capacity

of the business and estimate whether the business would be successful in the market or not.

The financial plan would also be analyzed from the perspective of the market and ensure that

the plan is a viable one.

Details of the Plan

The assessment shows that Aunt Chiara is planning to invest in a business venture

which can bring in some good amount of revenue for the business (Burns and Dewhurst

Executive Summary

The main purpose of this assessment is to analyze the viability of the business plan which is

being formulated for old aunt Chiara and the same is a new venture plan which would be

undertaken by her. The assessment would be including a detailed financial plan which is

developed for the business which is intended by Chiara. The business which is going to be

established would be in Italy and the main operations of the business is related to retail of

nuts which have a significant market in the country. The assessment considers the financial

aspects of the business plan of a retail business of different variety of nuts. The assessment

would be containing a detailed background of the business venture which is being considered

and the same would be include all the assumptions and factors which needs to be considered

by the owner of the business before taking any decisions. The financial plan would show the

assumptions which are considered while formulating the same and also would show the

preparation of the financial statements of the business. The financial statements would be

formulated on an estimation basis and would be including a profit and loss statement, cash

flow statement and a balance sheet. In addition to this, the attractiveness of the project would

be further assessed with the help of breakeven analysis which would provide an estimate of

minimum sales which the business needs to achieve in order to survive in the market and

continue its operations. This is done in order in order to assess the profit generating capacity

of the business and estimate whether the business would be successful in the market or not.

The financial plan would also be analyzed from the perspective of the market and ensure that

the plan is a viable one.

Details of the Plan

The assessment shows that Aunt Chiara is planning to invest in a business venture

which can bring in some good amount of revenue for the business (Burns and Dewhurst

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

2016). The business plan is intended to be a retirement plan and the venture would be

financed from the lump sum retirement amount which Chiara received for early retirement

and the amount which Chiara received is shown to be € 450,000. The business plan which is

formulated aims to open a ratil business which would be supplying nuts to the customers

(Veenhof 2016).

The plan which is device shows that the owner wants to import nuts from USA from a

company named BestNuts Inc. The business plan is to offer a variety of coated nuts to the

consumers and the same would be including different variety such as almonds, brazil,

macadamia, pecan, pistachio. The business of BestNuts Inc. also offers such nuts and

therefore the plan of the management is to import such coated nuts in bulk and engaged in

new venture in Italy. The owner also plans to enter into a tie up agreement with a local

business which would be buying 50 boxes of coated nuts every month. This would ensure

that the business has appropriate amount of revenue and regular income on monthly basis

(Criaco et al. 2016). The market survey also shows that the plan which is formulated by the

owner is viable and can help in generating appropriate profits for the business (André, Cho

and Laine 2018). In addition to this, the owner would also be require some assets and also

needs to incur start-up costs which would be shown in the financial statements which is

prepared for the business (Mason and Harrison 2017).

Assumptions and Viability Analysis of the Plan

The business plan which is being formulated by the management of the company

would be including an appropriate financing plan which can help the business in identifying

the costs and revenue which can be generated by the business on the basis of an estimation.

The viability of the business would be judged from breakeven analysis which is also

incorporated in the assessment which is shown in the assessment. In order to judge the

2016). The business plan is intended to be a retirement plan and the venture would be

financed from the lump sum retirement amount which Chiara received for early retirement

and the amount which Chiara received is shown to be € 450,000. The business plan which is

formulated aims to open a ratil business which would be supplying nuts to the customers

(Veenhof 2016).

The plan which is device shows that the owner wants to import nuts from USA from a

company named BestNuts Inc. The business plan is to offer a variety of coated nuts to the

consumers and the same would be including different variety such as almonds, brazil,

macadamia, pecan, pistachio. The business of BestNuts Inc. also offers such nuts and

therefore the plan of the management is to import such coated nuts in bulk and engaged in

new venture in Italy. The owner also plans to enter into a tie up agreement with a local

business which would be buying 50 boxes of coated nuts every month. This would ensure

that the business has appropriate amount of revenue and regular income on monthly basis

(Criaco et al. 2016). The market survey also shows that the plan which is formulated by the

owner is viable and can help in generating appropriate profits for the business (André, Cho

and Laine 2018). In addition to this, the owner would also be require some assets and also

needs to incur start-up costs which would be shown in the financial statements which is

prepared for the business (Mason and Harrison 2017).

Assumptions and Viability Analysis of the Plan

The business plan which is being formulated by the management of the company

would be including an appropriate financing plan which can help the business in identifying

the costs and revenue which can be generated by the business on the basis of an estimation.

The viability of the business would be judged from breakeven analysis which is also

incorporated in the assessment which is shown in the assessment. In order to judge the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

financial viability, the owner has prepared the income statement on the basis of month and

also an income statement which is yearly in nature (Gonzalez-Uribe and Leatherbee 2017).

The income statement would be showing the revenue which can be generated by the business

and also the costs which the business is most likely to incur as the business continues with its

operations (Xi et al. 2018). The analysis of the income statement is done with an objective to

compute the profitability of the business plan (Yambot et al. 2016). The financial plan also

includes balance sheet and cash flow statement which would give insights on the

performance of the business once the business is successfully established in the market. In

addition to this, the financial plan also includes a breakeven analysis in order to show how

much sales the management needs to achieve in order to ensure that the business is able to

survive in the long run (Gerasymenko, De Clercq and Sapienza 2015). The breakeven

analysis would show how sales the management of the company needs to achieve so that the

management is able to recover the fixed costs of the business so that the business is able to

continue with its operations effectively.

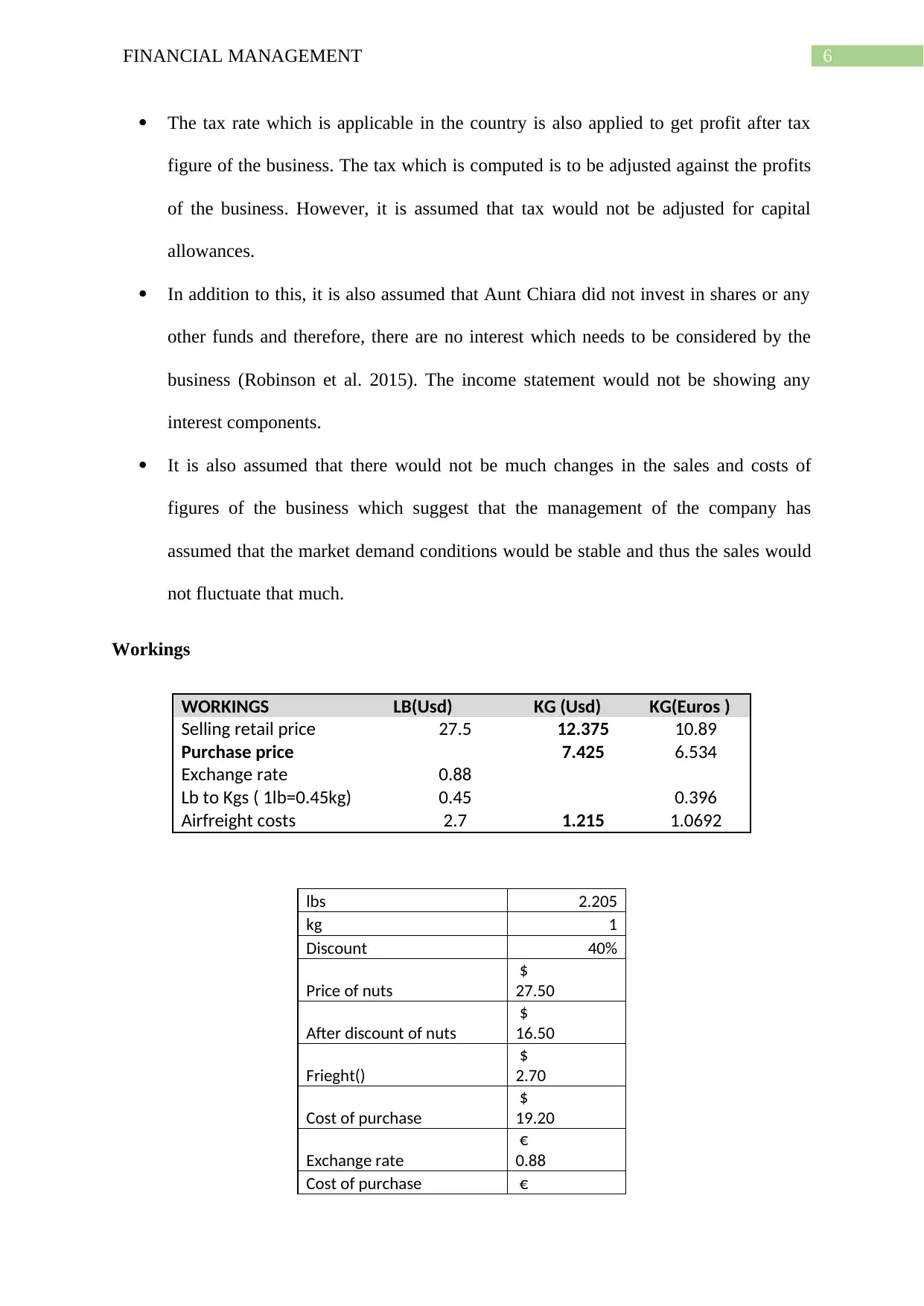

In order to formulate the financial plan, there are certain assumptions which are

considered by the owner so that the financial plans are developed as per the market and

current scenario and also as per the judgment of the owner. The assumptions which are

considered for the financial plan are listed below in point format.

One of the assumption which is considered while preparing the financial statements of

the intended business is that 1 Lb is equal to 0.45 kg and this assumption is used in

the income statement of the business.

The exchange rate of USD to Euro is considered to be 0.88. This is considered as the

business is undertaking imports for the coated nuts from the US and therefore the

foeign currency needs to be converted into home currency (Colombo et al. 2016). In

addition to this, the rate which is taken can change on day to day basis depending on

financial viability, the owner has prepared the income statement on the basis of month and

also an income statement which is yearly in nature (Gonzalez-Uribe and Leatherbee 2017).

The income statement would be showing the revenue which can be generated by the business

and also the costs which the business is most likely to incur as the business continues with its

operations (Xi et al. 2018). The analysis of the income statement is done with an objective to

compute the profitability of the business plan (Yambot et al. 2016). The financial plan also

includes balance sheet and cash flow statement which would give insights on the

performance of the business once the business is successfully established in the market. In

addition to this, the financial plan also includes a breakeven analysis in order to show how

much sales the management needs to achieve in order to ensure that the business is able to

survive in the long run (Gerasymenko, De Clercq and Sapienza 2015). The breakeven

analysis would show how sales the management of the company needs to achieve so that the

management is able to recover the fixed costs of the business so that the business is able to

continue with its operations effectively.

In order to formulate the financial plan, there are certain assumptions which are

considered by the owner so that the financial plans are developed as per the market and

current scenario and also as per the judgment of the owner. The assumptions which are

considered for the financial plan are listed below in point format.

One of the assumption which is considered while preparing the financial statements of

the intended business is that 1 Lb is equal to 0.45 kg and this assumption is used in

the income statement of the business.

The exchange rate of USD to Euro is considered to be 0.88. This is considered as the

business is undertaking imports for the coated nuts from the US and therefore the

foeign currency needs to be converted into home currency (Colombo et al. 2016). In

addition to this, the rate which is taken can change on day to day basis depending on

5FINANCIAL MANAGEMENT

the market situations and therefore a fixed rate of 0.88 is considered for the purpose of

conversion.

The sales figure is anticipated to increase from 40 to 200 over the year and the same is

shown in the profit and loss statement which is formulated by the management of the

business. The sales price is an important consideration which the management of the

company needs to consider while taking any major decisions to proceed for the

business. It is on the basis of the sale price that the profitability of the business as well

as the cost element of the business is determined.

The business also anticipates that they would be requiring certain assets for

effectively carrying out the operations of the business and therefore some assets needs

to be purchased by the management of the business. As per the anticipation of the

owner, the business would be requiring a refrigerator to appropriately store the coated

the nuts of the business. The refrigerator would also be required to be depreciated

over the years and the management anticipates that the asset would have a useful life

of 5 years and the same would be depreciated on straight line basis. The amount of

depreciation would be shown in the profit and loss account of the business.

The business also recognizes that the owner would also be required to appropriately

deal with the initial costs of the business which the owner incurred before the business

was undertaken. The market study costs will be spread over the one year period.

The owner also plans to develop a website in order to enhance the sales of the

business and thereby also increase the profitability of the business. The website is

considered to be an intangible assets of the business and therefore, the intangible

assets of the business are to be amortized over the 5 years period on the basis of

following straight line method.

the market situations and therefore a fixed rate of 0.88 is considered for the purpose of

conversion.

The sales figure is anticipated to increase from 40 to 200 over the year and the same is

shown in the profit and loss statement which is formulated by the management of the

business. The sales price is an important consideration which the management of the

company needs to consider while taking any major decisions to proceed for the

business. It is on the basis of the sale price that the profitability of the business as well

as the cost element of the business is determined.

The business also anticipates that they would be requiring certain assets for

effectively carrying out the operations of the business and therefore some assets needs

to be purchased by the management of the business. As per the anticipation of the

owner, the business would be requiring a refrigerator to appropriately store the coated

the nuts of the business. The refrigerator would also be required to be depreciated

over the years and the management anticipates that the asset would have a useful life

of 5 years and the same would be depreciated on straight line basis. The amount of

depreciation would be shown in the profit and loss account of the business.

The business also recognizes that the owner would also be required to appropriately

deal with the initial costs of the business which the owner incurred before the business

was undertaken. The market study costs will be spread over the one year period.

The owner also plans to develop a website in order to enhance the sales of the

business and thereby also increase the profitability of the business. The website is

considered to be an intangible assets of the business and therefore, the intangible

assets of the business are to be amortized over the 5 years period on the basis of

following straight line method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

The tax rate which is applicable in the country is also applied to get profit after tax

figure of the business. The tax which is computed is to be adjusted against the profits

of the business. However, it is assumed that tax would not be adjusted for capital

allowances.

In addition to this, it is also assumed that Aunt Chiara did not invest in shares or any

other funds and therefore, there are no interest which needs to be considered by the

business (Robinson et al. 2015). The income statement would not be showing any

interest components.

It is also assumed that there would not be much changes in the sales and costs of

figures of the business which suggest that the management of the company has

assumed that the market demand conditions would be stable and thus the sales would

not fluctuate that much.

Workings

WORKINGS LB(Usd) KG (Usd) KG(Euros )

Selling retail price 27.5 12.375 10.89

Purchase price 7.425 6.534

Exchange rate 0.88

Lb to Kgs ( 1lb=0.45kg) 0.45 0.396

Airfreight costs 2.7 1.215 1.0692

lbs 2.205

kg 1

Discount 40%

Price of nuts

$

27.50

After discount of nuts

$

16.50

Frieght()

$

2.70

Cost of purchase

$

19.20

Exchange rate

€

0.88

Cost of purchase €

The tax rate which is applicable in the country is also applied to get profit after tax

figure of the business. The tax which is computed is to be adjusted against the profits

of the business. However, it is assumed that tax would not be adjusted for capital

allowances.

In addition to this, it is also assumed that Aunt Chiara did not invest in shares or any

other funds and therefore, there are no interest which needs to be considered by the

business (Robinson et al. 2015). The income statement would not be showing any

interest components.

It is also assumed that there would not be much changes in the sales and costs of

figures of the business which suggest that the management of the company has

assumed that the market demand conditions would be stable and thus the sales would

not fluctuate that much.

Workings

WORKINGS LB(Usd) KG (Usd) KG(Euros )

Selling retail price 27.5 12.375 10.89

Purchase price 7.425 6.534

Exchange rate 0.88

Lb to Kgs ( 1lb=0.45kg) 0.45 0.396

Airfreight costs 2.7 1.215 1.0692

lbs 2.205

kg 1

Discount 40%

Price of nuts

$

27.50

After discount of nuts

$

16.50

Frieght()

$

2.70

Cost of purchase

$

19.20

Exchange rate

€

0.88

Cost of purchase €

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

16.90

Time to receive the goods 3

Inventory to be maintained 4

Capital

€

4,50,000.00

loan

€

50,000.00

Figure 1: (Table showing other assumptions for the business)

Source: (Created by the Author)

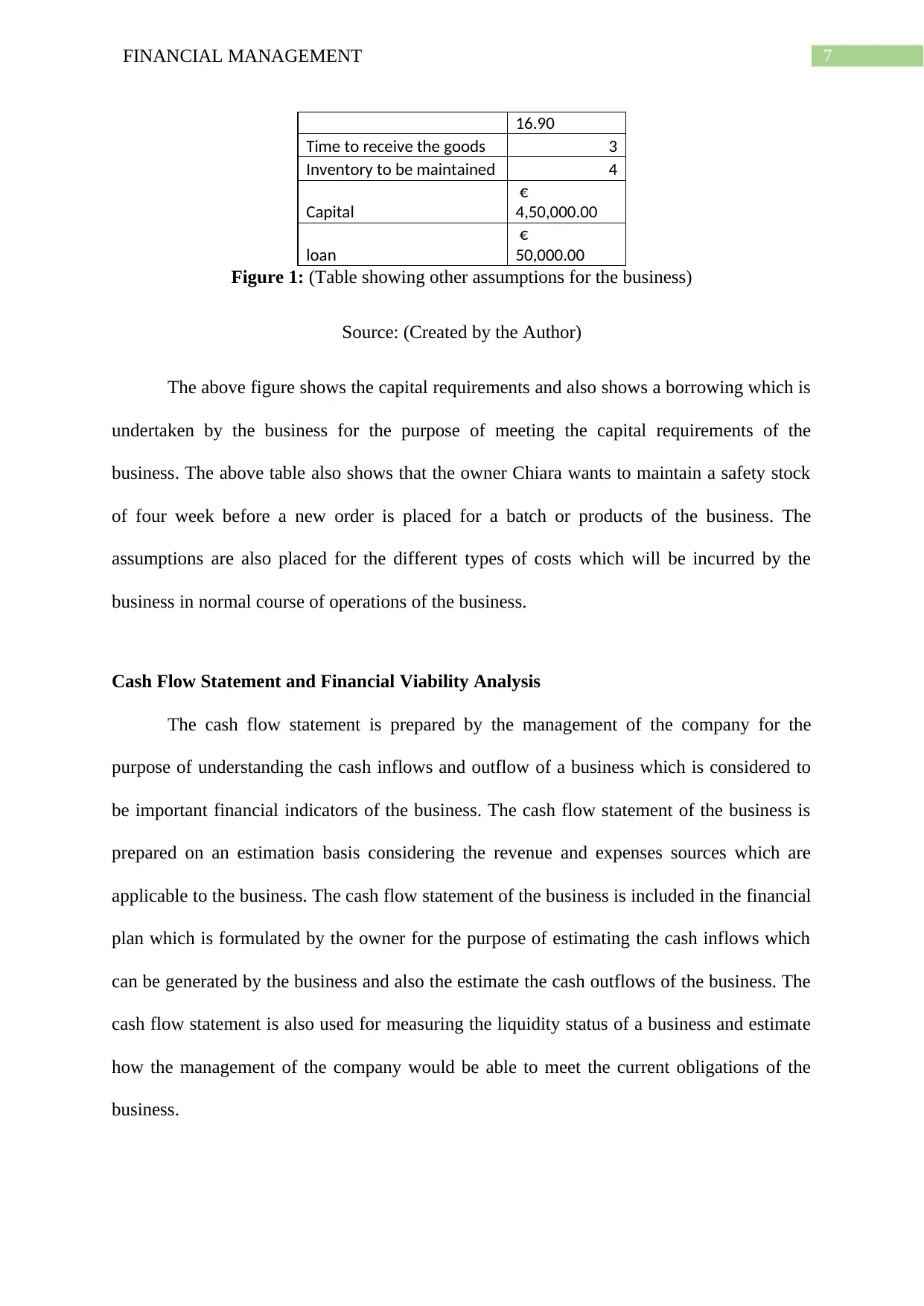

The above figure shows the capital requirements and also shows a borrowing which is

undertaken by the business for the purpose of meeting the capital requirements of the

business. The above table also shows that the owner Chiara wants to maintain a safety stock

of four week before a new order is placed for a batch or products of the business. The

assumptions are also placed for the different types of costs which will be incurred by the

business in normal course of operations of the business.

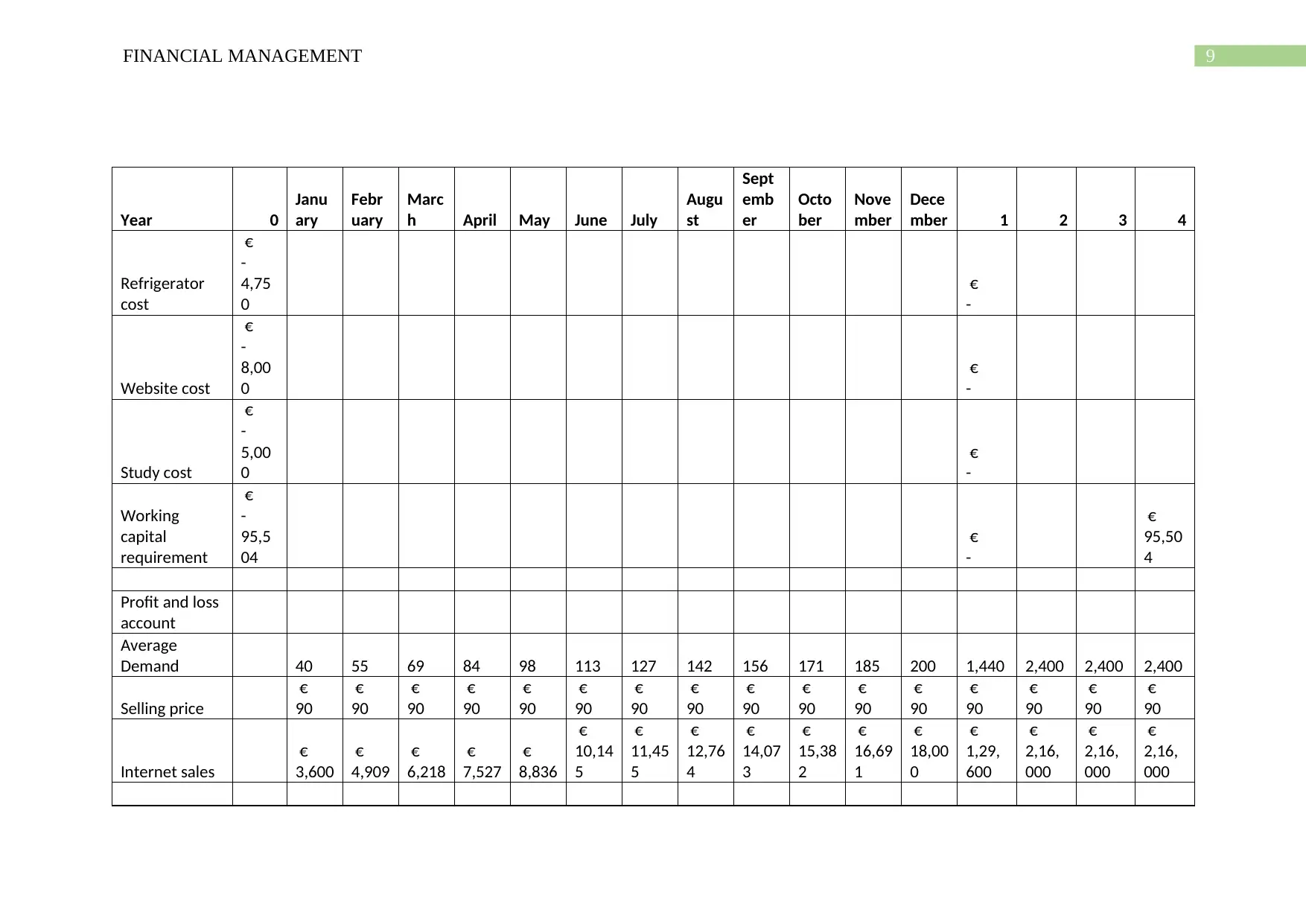

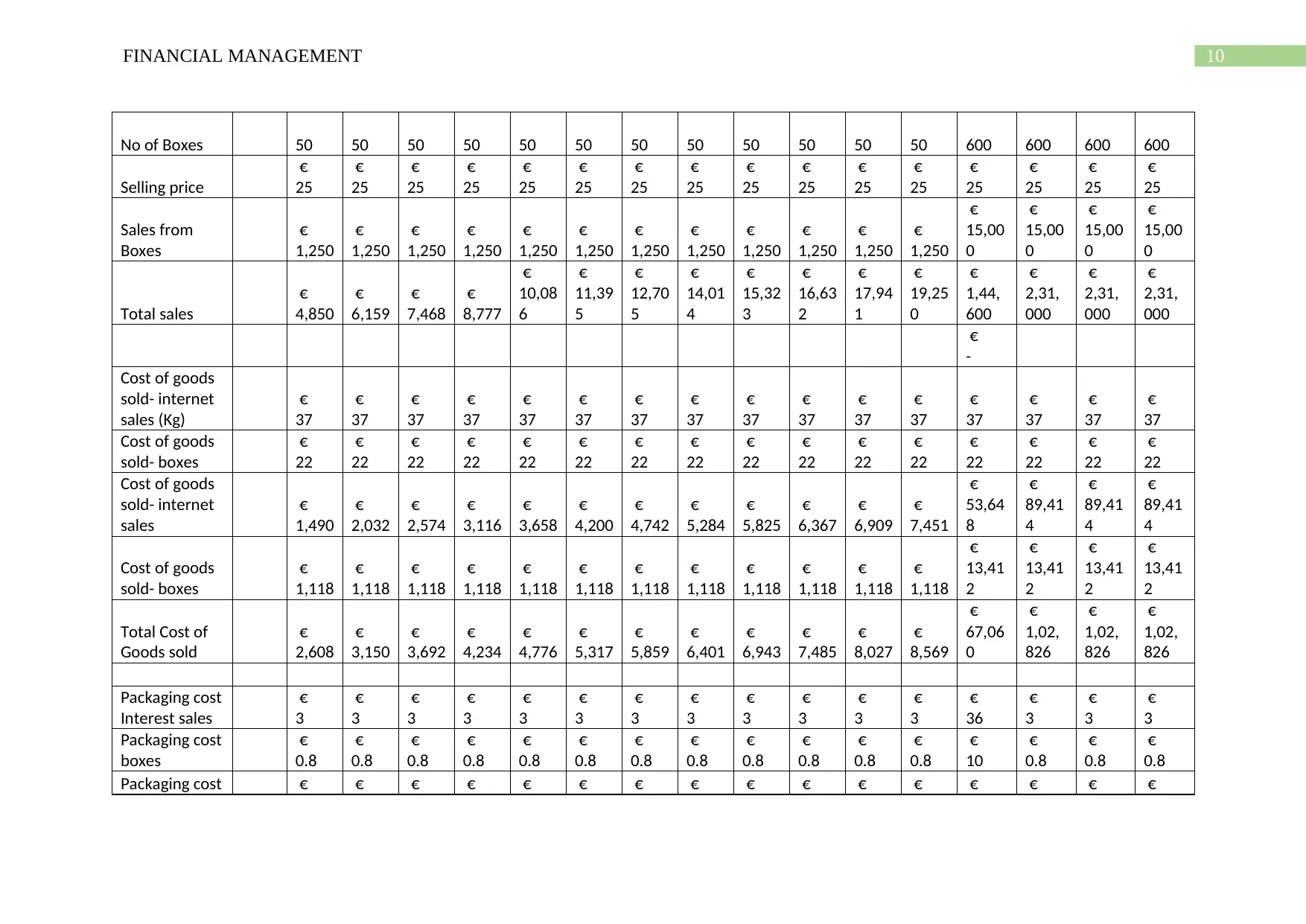

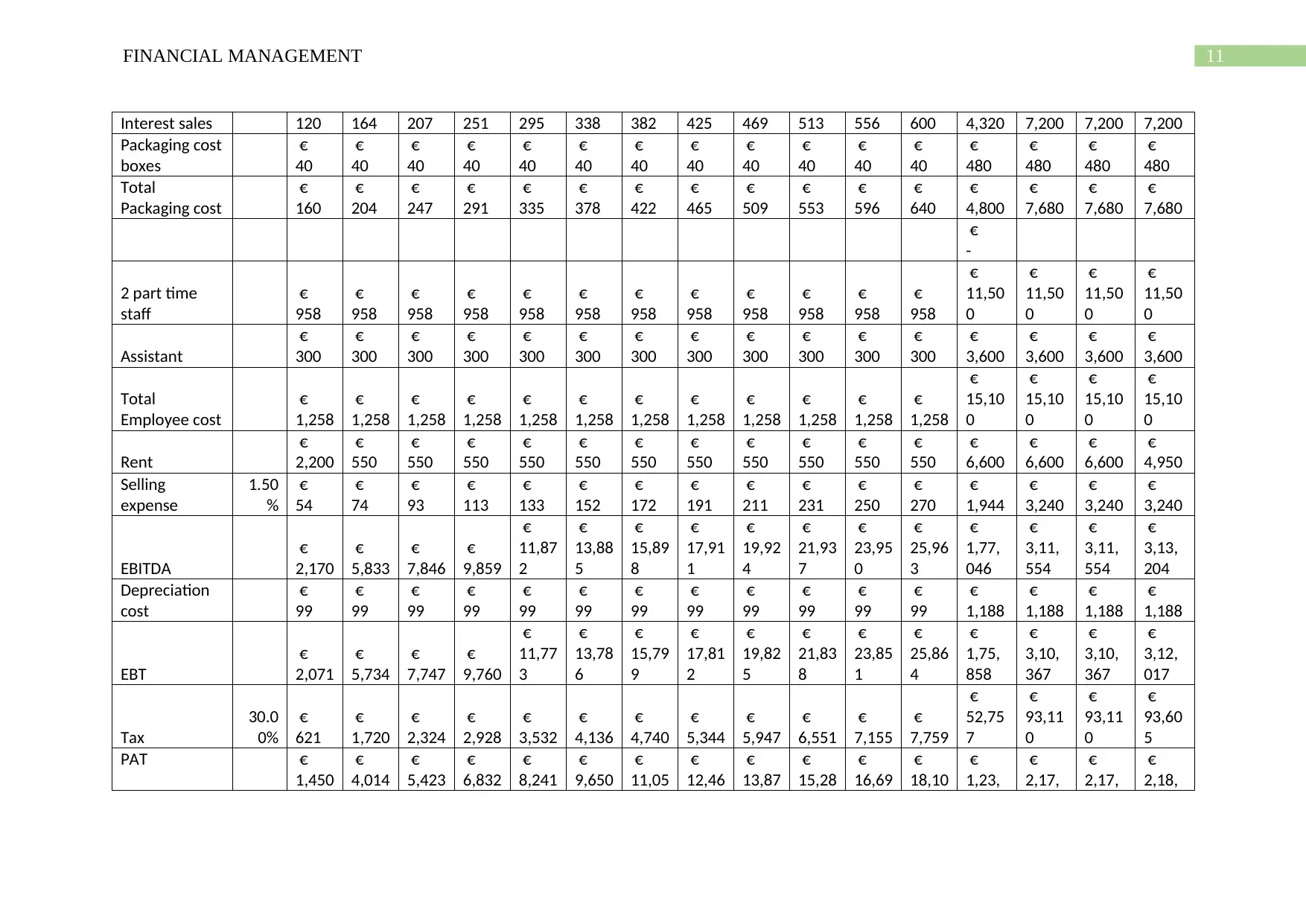

Cash Flow Statement and Financial Viability Analysis

The cash flow statement is prepared by the management of the company for the

purpose of understanding the cash inflows and outflow of a business which is considered to

be important financial indicators of the business. The cash flow statement of the business is

prepared on an estimation basis considering the revenue and expenses sources which are

applicable to the business. The cash flow statement of the business is included in the financial

plan which is formulated by the owner for the purpose of estimating the cash inflows which

can be generated by the business and also the estimate the cash outflows of the business. The

cash flow statement is also used for measuring the liquidity status of a business and estimate

how the management of the company would be able to meet the current obligations of the

business.

16.90

Time to receive the goods 3

Inventory to be maintained 4

Capital

€

4,50,000.00

loan

€

50,000.00

Figure 1: (Table showing other assumptions for the business)

Source: (Created by the Author)

The above figure shows the capital requirements and also shows a borrowing which is

undertaken by the business for the purpose of meeting the capital requirements of the

business. The above table also shows that the owner Chiara wants to maintain a safety stock

of four week before a new order is placed for a batch or products of the business. The

assumptions are also placed for the different types of costs which will be incurred by the

business in normal course of operations of the business.

Cash Flow Statement and Financial Viability Analysis

The cash flow statement is prepared by the management of the company for the

purpose of understanding the cash inflows and outflow of a business which is considered to

be important financial indicators of the business. The cash flow statement of the business is

prepared on an estimation basis considering the revenue and expenses sources which are

applicable to the business. The cash flow statement of the business is included in the financial

plan which is formulated by the owner for the purpose of estimating the cash inflows which

can be generated by the business and also the estimate the cash outflows of the business. The

cash flow statement is also used for measuring the liquidity status of a business and estimate

how the management of the company would be able to meet the current obligations of the

business.

8FINANCIAL MANAGEMENT

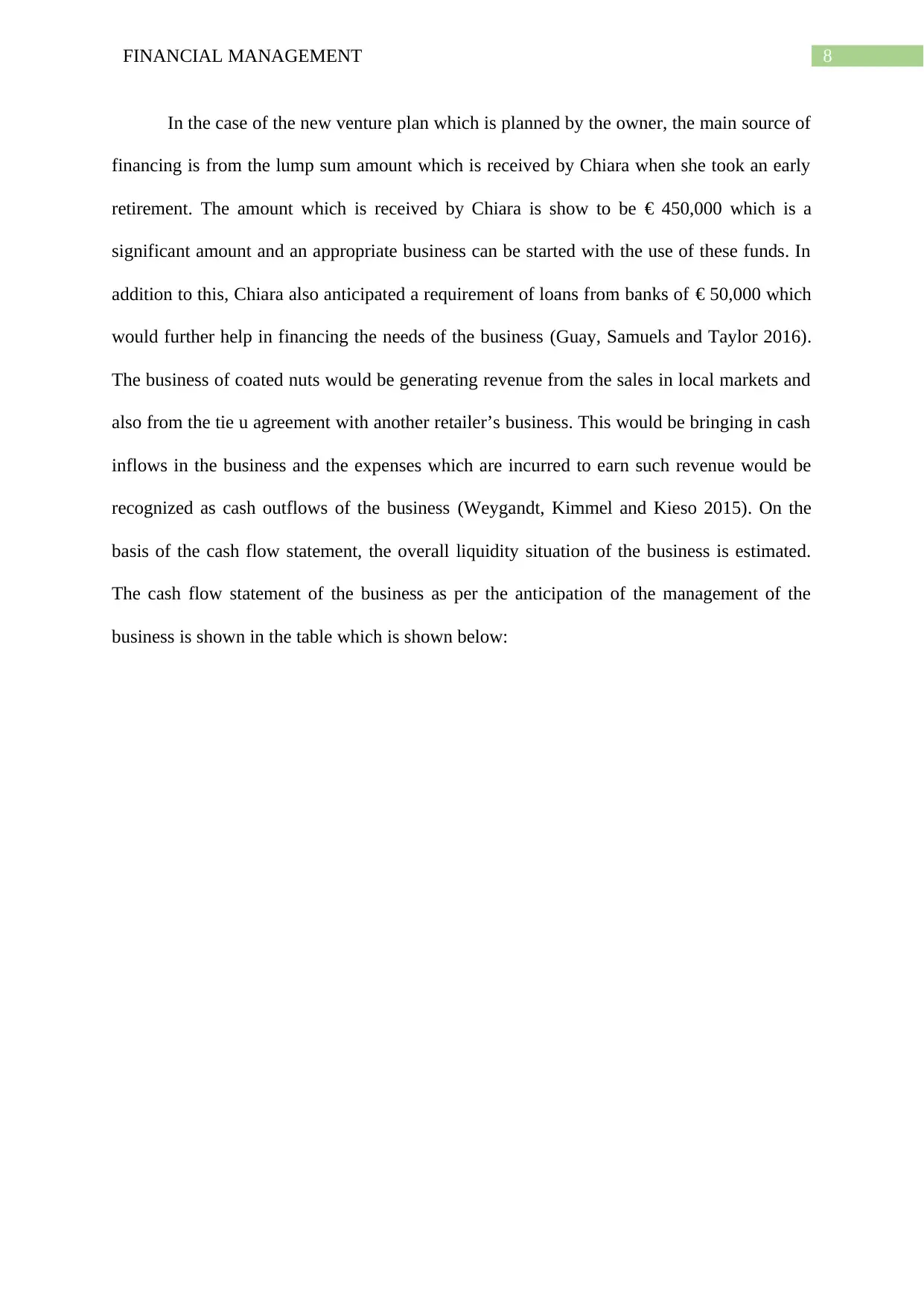

In the case of the new venture plan which is planned by the owner, the main source of

financing is from the lump sum amount which is received by Chiara when she took an early

retirement. The amount which is received by Chiara is show to be € 450,000 which is a

significant amount and an appropriate business can be started with the use of these funds. In

addition to this, Chiara also anticipated a requirement of loans from banks of € 50,000 which

would further help in financing the needs of the business (Guay, Samuels and Taylor 2016).

The business of coated nuts would be generating revenue from the sales in local markets and

also from the tie u agreement with another retailer’s business. This would be bringing in cash

inflows in the business and the expenses which are incurred to earn such revenue would be

recognized as cash outflows of the business (Weygandt, Kimmel and Kieso 2015). On the

basis of the cash flow statement, the overall liquidity situation of the business is estimated.

The cash flow statement of the business as per the anticipation of the management of the

business is shown in the table which is shown below:

In the case of the new venture plan which is planned by the owner, the main source of

financing is from the lump sum amount which is received by Chiara when she took an early

retirement. The amount which is received by Chiara is show to be € 450,000 which is a

significant amount and an appropriate business can be started with the use of these funds. In

addition to this, Chiara also anticipated a requirement of loans from banks of € 50,000 which

would further help in financing the needs of the business (Guay, Samuels and Taylor 2016).

The business of coated nuts would be generating revenue from the sales in local markets and

also from the tie u agreement with another retailer’s business. This would be bringing in cash

inflows in the business and the expenses which are incurred to earn such revenue would be

recognized as cash outflows of the business (Weygandt, Kimmel and Kieso 2015). On the

basis of the cash flow statement, the overall liquidity situation of the business is estimated.

The cash flow statement of the business as per the anticipation of the management of the

business is shown in the table which is shown below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Year 0

Janu

ary

Febr

uary

Marc

h April May June July

Augu

st

Sept

emb

er

Octo

ber

Nove

mber

Dece

mber 1 2 3 4

Refrigerator

cost

€

-

4,75

0

€

-

Website cost

€

-

8,00

0

€

-

Study cost

€

-

5,00

0

€

-

Working

capital

requirement

€

-

95,5

04

€

-

€

95,50

4

Profit and loss

account

Average

Demand 40 55 69 84 98 113 127 142 156 171 185 200 1,440 2,400 2,400 2,400

Selling price

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

Internet sales

€

3,600

€

4,909

€

6,218

€

7,527

€

8,836

€

10,14

5

€

11,45

5

€

12,76

4

€

14,07

3

€

15,38

2

€

16,69

1

€

18,00

0

€

1,29,

600

€

2,16,

000

€

2,16,

000

€

2,16,

000

Year 0

Janu

ary

Febr

uary

Marc

h April May June July

Augu

st

Sept

emb

er

Octo

ber

Nove

mber

Dece

mber 1 2 3 4

Refrigerator

cost

€

-

4,75

0

€

-

Website cost

€

-

8,00

0

€

-

Study cost

€

-

5,00

0

€

-

Working

capital

requirement

€

-

95,5

04

€

-

€

95,50

4

Profit and loss

account

Average

Demand 40 55 69 84 98 113 127 142 156 171 185 200 1,440 2,400 2,400 2,400

Selling price

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

€

90

Internet sales

€

3,600

€

4,909

€

6,218

€

7,527

€

8,836

€

10,14

5

€

11,45

5

€

12,76

4

€

14,07

3

€

15,38

2

€

16,69

1

€

18,00

0

€

1,29,

600

€

2,16,

000

€

2,16,

000

€

2,16,

000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

No of Boxes 50 50 50 50 50 50 50 50 50 50 50 50 600 600 600 600

Selling price

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

Sales from

Boxes

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

15,00

0

€

15,00

0

€

15,00

0

€

15,00

0

Total sales

€

4,850

€

6,159

€

7,468

€

8,777

€

10,08

6

€

11,39

5

€

12,70

5

€

14,01

4

€

15,32

3

€

16,63

2

€

17,94

1

€

19,25

0

€

1,44,

600

€

2,31,

000

€

2,31,

000

€

2,31,

000

€

-

Cost of goods

sold- internet

sales (Kg)

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

Cost of goods

sold- boxes

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

Cost of goods

sold- internet

sales

€

1,490

€

2,032

€

2,574

€

3,116

€

3,658

€

4,200

€

4,742

€

5,284

€

5,825

€

6,367

€

6,909

€

7,451

€

53,64

8

€

89,41

4

€

89,41

4

€

89,41

4

Cost of goods

sold- boxes

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

13,41

2

€

13,41

2

€

13,41

2

€

13,41

2

Total Cost of

Goods sold

€

2,608

€

3,150

€

3,692

€

4,234

€

4,776

€

5,317

€

5,859

€

6,401

€

6,943

€

7,485

€

8,027

€

8,569

€

67,06

0

€

1,02,

826

€

1,02,

826

€

1,02,

826

Packaging cost

Interest sales

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

36

€

3

€

3

€

3

Packaging cost

boxes

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

10

€

0.8

€

0.8

€

0.8

Packaging cost € € € € € € € € € € € € € € € €

No of Boxes 50 50 50 50 50 50 50 50 50 50 50 50 600 600 600 600

Selling price

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

€

25

Sales from

Boxes

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

1,250

€

15,00

0

€

15,00

0

€

15,00

0

€

15,00

0

Total sales

€

4,850

€

6,159

€

7,468

€

8,777

€

10,08

6

€

11,39

5

€

12,70

5

€

14,01

4

€

15,32

3

€

16,63

2

€

17,94

1

€

19,25

0

€

1,44,

600

€

2,31,

000

€

2,31,

000

€

2,31,

000

€

-

Cost of goods

sold- internet

sales (Kg)

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

€

37

Cost of goods

sold- boxes

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

€

22

Cost of goods

sold- internet

sales

€

1,490

€

2,032

€

2,574

€

3,116

€

3,658

€

4,200

€

4,742

€

5,284

€

5,825

€

6,367

€

6,909

€

7,451

€

53,64

8

€

89,41

4

€

89,41

4

€

89,41

4

Cost of goods

sold- boxes

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

1,118

€

13,41

2

€

13,41

2

€

13,41

2

€

13,41

2

Total Cost of

Goods sold

€

2,608

€

3,150

€

3,692

€

4,234

€

4,776

€

5,317

€

5,859

€

6,401

€

6,943

€

7,485

€

8,027

€

8,569

€

67,06

0

€

1,02,

826

€

1,02,

826

€

1,02,

826

Packaging cost

Interest sales

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

3

€

36

€

3

€

3

€

3

Packaging cost

boxes

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

0.8

€

10

€

0.8

€

0.8

€

0.8

Packaging cost € € € € € € € € € € € € € € € €

11FINANCIAL MANAGEMENT

Interest sales 120 164 207 251 295 338 382 425 469 513 556 600 4,320 7,200 7,200 7,200

Packaging cost

boxes

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

480

€

480

€

480

€

480

Total

Packaging cost

€

160

€

204

€

247

€

291

€

335

€

378

€

422

€

465

€

509

€

553

€

596

€

640

€

4,800

€

7,680

€

7,680

€

7,680

€

-

2 part time

staff

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

11,50

0

€

11,50

0

€

11,50

0

€

11,50

0

Assistant

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

3,600

€

3,600

€

3,600

€

3,600

Total

Employee cost

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

15,10

0

€

15,10

0

€

15,10

0

€

15,10

0

Rent

€

2,200

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

6,600

€

6,600

€

6,600

€

4,950

Selling

expense

1.50

%

€

54

€

74

€

93

€

113

€

133

€

152

€

172

€

191

€

211

€

231

€

250

€

270

€

1,944

€

3,240

€

3,240

€

3,240

EBITDA

€

2,170

€

5,833

€

7,846

€

9,859

€

11,87

2

€

13,88

5

€

15,89

8

€

17,91

1

€

19,92

4

€

21,93

7

€

23,95

0

€

25,96

3

€

1,77,

046

€

3,11,

554

€

3,11,

554

€

3,13,

204

Depreciation

cost

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

1,188

€

1,188

€

1,188

€

1,188

EBT

€

2,071

€

5,734

€

7,747

€

9,760

€

11,77

3

€

13,78

6

€

15,79

9

€

17,81

2

€

19,82

5

€

21,83

8

€

23,85

1

€

25,86

4

€

1,75,

858

€

3,10,

367

€

3,10,

367

€

3,12,

017

Tax

30.0

0%

€

621

€

1,720

€

2,324

€

2,928

€

3,532

€

4,136

€

4,740

€

5,344

€

5,947

€

6,551

€

7,155

€

7,759

€

52,75

7

€

93,11

0

€

93,11

0

€

93,60

5

PAT €

1,450

€

4,014

€

5,423

€

6,832

€

8,241

€

9,650

€

11,05

€

12,46

€

13,87

€

15,28

€

16,69

€

18,10

€

1,23,

€

2,17,

€

2,17,

€

2,18,

Interest sales 120 164 207 251 295 338 382 425 469 513 556 600 4,320 7,200 7,200 7,200

Packaging cost

boxes

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

40

€

480

€

480

€

480

€

480

Total

Packaging cost

€

160

€

204

€

247

€

291

€

335

€

378

€

422

€

465

€

509

€

553

€

596

€

640

€

4,800

€

7,680

€

7,680

€

7,680

€

-

2 part time

staff

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

958

€

11,50

0

€

11,50

0

€

11,50

0

€

11,50

0

Assistant

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

300

€

3,600

€

3,600

€

3,600

€

3,600

Total

Employee cost

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

1,258

€

15,10

0

€

15,10

0

€

15,10

0

€

15,10

0

Rent

€

2,200

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

550

€

6,600

€

6,600

€

6,600

€

4,950

Selling

expense

1.50

%

€

54

€

74

€

93

€

113

€

133

€

152

€

172

€

191

€

211

€

231

€

250

€

270

€

1,944

€

3,240

€

3,240

€

3,240

EBITDA

€

2,170

€

5,833

€

7,846

€

9,859

€

11,87

2

€

13,88

5

€

15,89

8

€

17,91

1

€

19,92

4

€

21,93

7

€

23,95

0

€

25,96

3

€

1,77,

046

€

3,11,

554

€

3,11,

554

€

3,13,

204

Depreciation

cost

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

99

€

1,188

€

1,188

€

1,188

€

1,188

EBT

€

2,071

€

5,734

€

7,747

€

9,760

€

11,77

3

€

13,78

6

€

15,79

9

€

17,81

2

€

19,82

5

€

21,83

8

€

23,85

1

€

25,86

4

€

1,75,

858

€

3,10,

367

€

3,10,

367

€

3,12,

017

Tax

30.0

0%

€

621

€

1,720

€

2,324

€

2,928

€

3,532

€

4,136

€

4,740

€

5,344

€

5,947

€

6,551

€

7,155

€

7,759

€

52,75

7

€

93,11

0

€

93,11

0

€

93,60

5

PAT €

1,450

€

4,014

€

5,423

€

6,832

€

8,241

€

9,650

€

11,05

€

12,46

€

13,87

€

15,28

€

16,69

€

18,10

€

1,23,

€

2,17,

€

2,17,

€

2,18,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.