Financial Management: Calculation of WACC and Optimal Investment Decision

VerifiedAdded on 2023/06/12

|10

|2521

|187

AI Summary

This article provides a detailed explanation of the calculation of WACC and optimal investment decision for a business. It includes a statement showing the calculation of cost of equity and NPV and IRR of different investment options. The article is relevant for students studying financial management and related courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL MANAGEMENT

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................2

b)..................................................................................................................................................2

C...................................................................................................................................................7

Reference.........................................................................................................................................9

Table of Contents

Answer to Question 1......................................................................................................................2

a)..................................................................................................................................................2

b)..................................................................................................................................................2

C...................................................................................................................................................7

Reference.........................................................................................................................................9

2FINANCIAL MANAGEMENT

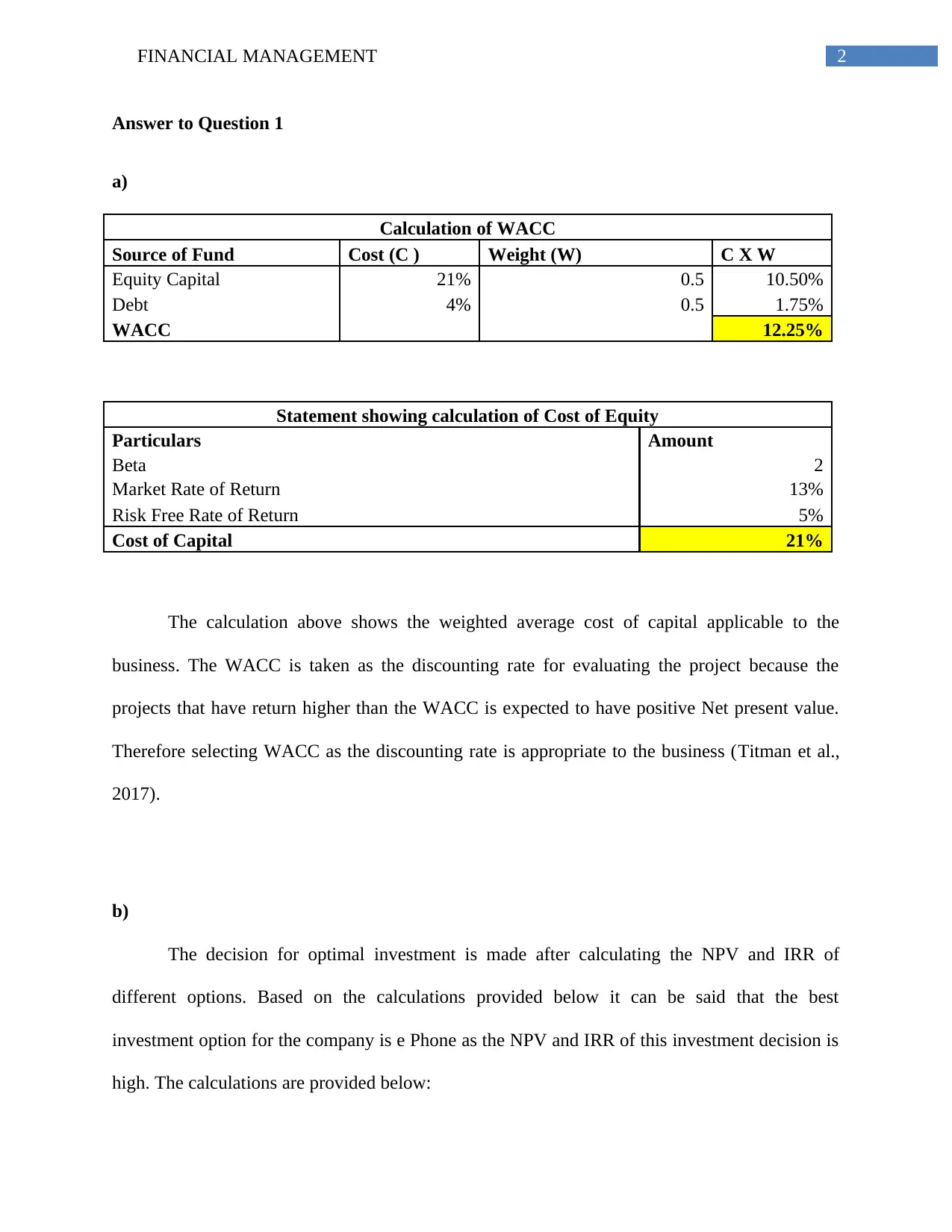

Answer to Question 1

a)

Calculation of WACC

Source of Fund Cost (C ) Weight (W) C X W

Equity Capital 21% 0.5 10.50%

Debt 4% 0.5 1.75%

WACC 12.25%

Statement showing calculation of Cost of Equity

Particulars Amount

Beta 2

Market Rate of Return 13%

Risk Free Rate of Return 5%

Cost of Capital 21%

The calculation above shows the weighted average cost of capital applicable to the

business. The WACC is taken as the discounting rate for evaluating the project because the

projects that have return higher than the WACC is expected to have positive Net present value.

Therefore selecting WACC as the discounting rate is appropriate to the business (Titman et al.,

2017).

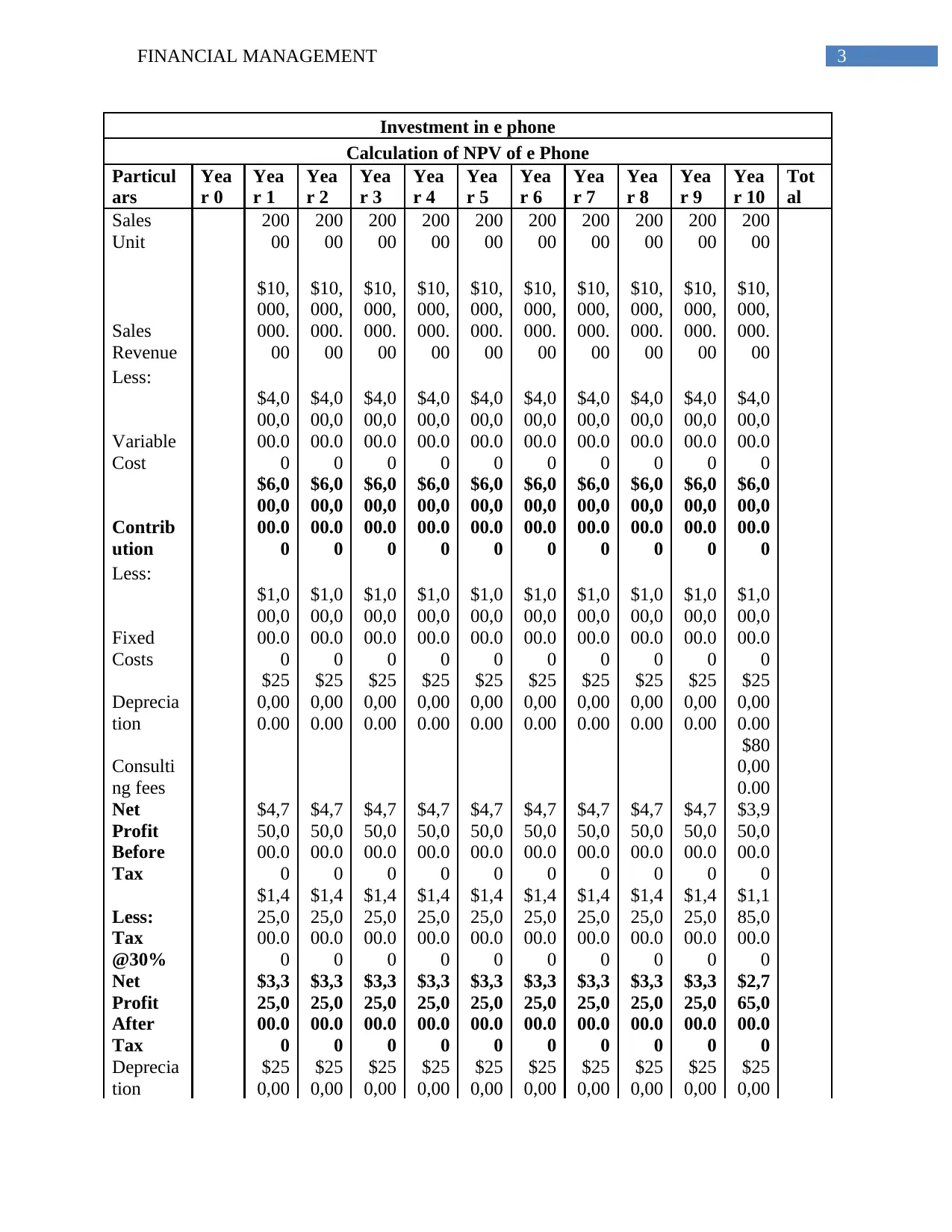

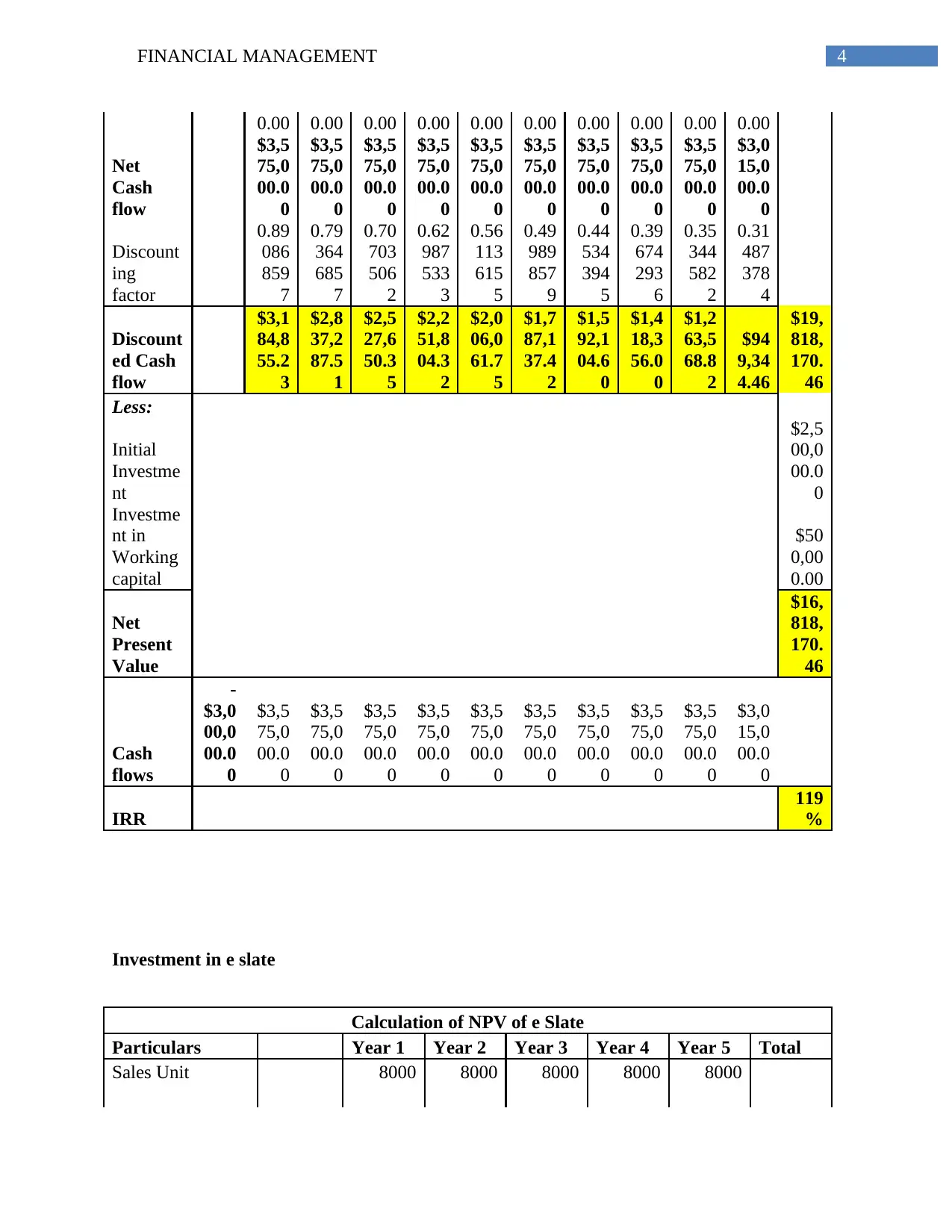

b)

The decision for optimal investment is made after calculating the NPV and IRR of

different options. Based on the calculations provided below it can be said that the best

investment option for the company is e Phone as the NPV and IRR of this investment decision is

high. The calculations are provided below:

Answer to Question 1

a)

Calculation of WACC

Source of Fund Cost (C ) Weight (W) C X W

Equity Capital 21% 0.5 10.50%

Debt 4% 0.5 1.75%

WACC 12.25%

Statement showing calculation of Cost of Equity

Particulars Amount

Beta 2

Market Rate of Return 13%

Risk Free Rate of Return 5%

Cost of Capital 21%

The calculation above shows the weighted average cost of capital applicable to the

business. The WACC is taken as the discounting rate for evaluating the project because the

projects that have return higher than the WACC is expected to have positive Net present value.

Therefore selecting WACC as the discounting rate is appropriate to the business (Titman et al.,

2017).

b)

The decision for optimal investment is made after calculating the NPV and IRR of

different options. Based on the calculations provided below it can be said that the best

investment option for the company is e Phone as the NPV and IRR of this investment decision is

high. The calculations are provided below:

3FINANCIAL MANAGEMENT

Investment in e phone

Calculation of NPV of e Phone

Particul

ars

Yea

r 0

Yea

r 1

Yea

r 2

Yea

r 3

Yea

r 4

Yea

r 5

Yea

r 6

Yea

r 7

Yea

r 8

Yea

r 9

Yea

r 10

Tot

al

Sales

Unit

200

00

200

00

200

00

200

00

200

00

200

00

200

00

200

00

200

00

200

00

Sales

Revenue

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

Less:

Variable

Cost

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

Contrib

ution

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

Less:

Fixed

Costs

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

Deprecia

tion

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

Consulti

ng fees

$80

0,00

0.00

Net

Profit

Before

Tax

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$3,9

50,0

00.0

0

Less:

Tax

@30%

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,1

85,0

00.0

0

Net

Profit

After

Tax

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$2,7

65,0

00.0

0

Deprecia

tion

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

Investment in e phone

Calculation of NPV of e Phone

Particul

ars

Yea

r 0

Yea

r 1

Yea

r 2

Yea

r 3

Yea

r 4

Yea

r 5

Yea

r 6

Yea

r 7

Yea

r 8

Yea

r 9

Yea

r 10

Tot

al

Sales

Unit

200

00

200

00

200

00

200

00

200

00

200

00

200

00

200

00

200

00

200

00

Sales

Revenue

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

$10,

000,

000.

00

Less:

Variable

Cost

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

$4,0

00,0

00.0

0

Contrib

ution

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

$6,0

00,0

00.0

0

Less:

Fixed

Costs

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

$1,0

00,0

00.0

0

Deprecia

tion

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

$25

0,00

0.00

Consulti

ng fees

$80

0,00

0.00

Net

Profit

Before

Tax

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$4,7

50,0

00.0

0

$3,9

50,0

00.0

0

Less:

Tax

@30%

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,4

25,0

00.0

0

$1,1

85,0

00.0

0

Net

Profit

After

Tax

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$3,3

25,0

00.0

0

$2,7

65,0

00.0

0

Deprecia

tion

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

$25

0,00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL MANAGEMENT

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Net

Cash

flow

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,0

15,0

00.0

0

Discount

ing

factor

0.89

086

859

7

0.79

364

685

7

0.70

703

506

2

0.62

987

533

3

0.56

113

615

5

0.49

989

857

9

0.44

534

394

5

0.39

674

293

6

0.35

344

582

2

0.31

487

378

4

Discount

ed Cash

flow

$3,1

84,8

55.2

3

$2,8

37,2

87.5

1

$2,5

27,6

50.3

5

$2,2

51,8

04.3

2

$2,0

06,0

61.7

5

$1,7

87,1

37.4

2

$1,5

92,1

04.6

0

$1,4

18,3

56.0

0

$1,2

63,5

68.8

2

$94

9,34

4.46

$19,

818,

170.

46

Less:

Initial

Investme

nt

$2,5

00,0

00.0

0

Investme

nt in

Working

capital

$50

0,00

0.00

Net

Present

Value

$16,

818,

170.

46

Cash

flows

-

$3,0

00,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,0

15,0

00.0

0

IRR

119

%

Investment in e slate

Calculation of NPV of e Slate

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Total

Sales Unit 8000 8000 8000 8000 8000

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Net

Cash

flow

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,0

15,0

00.0

0

Discount

ing

factor

0.89

086

859

7

0.79

364

685

7

0.70

703

506

2

0.62

987

533

3

0.56

113

615

5

0.49

989

857

9

0.44

534

394

5

0.39

674

293

6

0.35

344

582

2

0.31

487

378

4

Discount

ed Cash

flow

$3,1

84,8

55.2

3

$2,8

37,2

87.5

1

$2,5

27,6

50.3

5

$2,2

51,8

04.3

2

$2,0

06,0

61.7

5

$1,7

87,1

37.4

2

$1,5

92,1

04.6

0

$1,4

18,3

56.0

0

$1,2

63,5

68.8

2

$94

9,34

4.46

$19,

818,

170.

46

Less:

Initial

Investme

nt

$2,5

00,0

00.0

0

Investme

nt in

Working

capital

$50

0,00

0.00

Net

Present

Value

$16,

818,

170.

46

Cash

flows

-

$3,0

00,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,5

75,0

00.0

0

$3,0

15,0

00.0

0

IRR

119

%

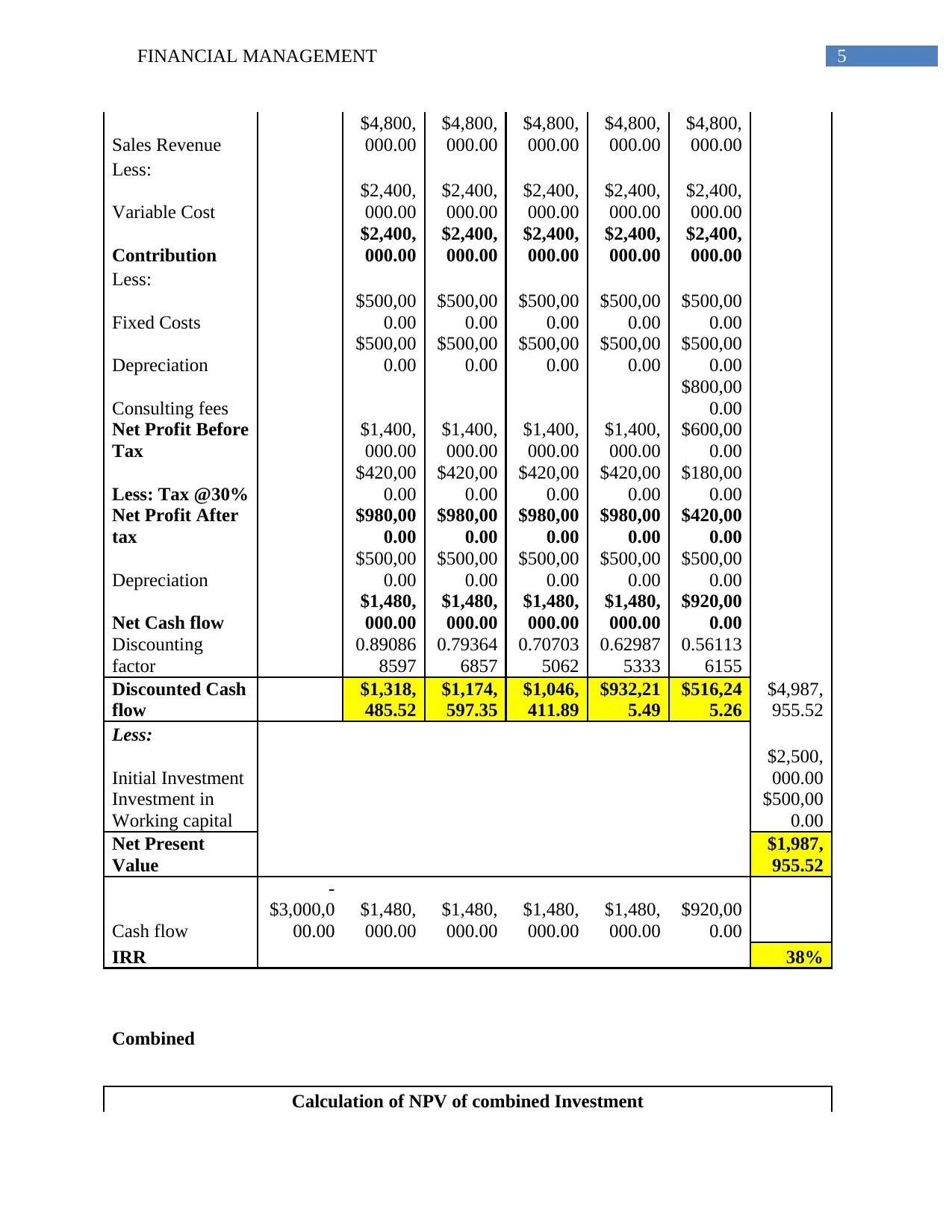

Investment in e slate

Calculation of NPV of e Slate

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Total

Sales Unit 8000 8000 8000 8000 8000

5FINANCIAL MANAGEMENT

Sales Revenue

$4,800,

000.00

$4,800,

000.00

$4,800,

000.00

$4,800,

000.00

$4,800,

000.00

Less:

Variable Cost

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

Contribution

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

Less:

Fixed Costs

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

Depreciation

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

Consulting fees

$800,00

0.00

Net Profit Before

Tax

$1,400,

000.00

$1,400,

000.00

$1,400,

000.00

$1,400,

000.00

$600,00

0.00

Less: Tax @30%

$420,00

0.00

$420,00

0.00

$420,00

0.00

$420,00

0.00

$180,00

0.00

Net Profit After

tax

$980,00

0.00

$980,00

0.00

$980,00

0.00

$980,00

0.00

$420,00

0.00

Depreciation

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

Net Cash flow

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$920,00

0.00

Discounting

factor

0.89086

8597

0.79364

6857

0.70703

5062

0.62987

5333

0.56113

6155

Discounted Cash

flow

$1,318,

485.52

$1,174,

597.35

$1,046,

411.89

$932,21

5.49

$516,24

5.26

$4,987,

955.52

Less:

Initial Investment

$2,500,

000.00

Investment in

Working capital

$500,00

0.00

Net Present

Value

$1,987,

955.52

Cash flow

-

$3,000,0

00.00

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$920,00

0.00

IRR 38%

Combined

Calculation of NPV of combined Investment

Sales Revenue

$4,800,

000.00

$4,800,

000.00

$4,800,

000.00

$4,800,

000.00

$4,800,

000.00

Less:

Variable Cost

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

Contribution

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

$2,400,

000.00

Less:

Fixed Costs

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

Depreciation

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

Consulting fees

$800,00

0.00

Net Profit Before

Tax

$1,400,

000.00

$1,400,

000.00

$1,400,

000.00

$1,400,

000.00

$600,00

0.00

Less: Tax @30%

$420,00

0.00

$420,00

0.00

$420,00

0.00

$420,00

0.00

$180,00

0.00

Net Profit After

tax

$980,00

0.00

$980,00

0.00

$980,00

0.00

$980,00

0.00

$420,00

0.00

Depreciation

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

$500,00

0.00

Net Cash flow

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$920,00

0.00

Discounting

factor

0.89086

8597

0.79364

6857

0.70703

5062

0.62987

5333

0.56113

6155

Discounted Cash

flow

$1,318,

485.52

$1,174,

597.35

$1,046,

411.89

$932,21

5.49

$516,24

5.26

$4,987,

955.52

Less:

Initial Investment

$2,500,

000.00

Investment in

Working capital

$500,00

0.00

Net Present

Value

$1,987,

955.52

Cash flow

-

$3,000,0

00.00

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$1,480,

000.00

$920,00

0.00

IRR 38%

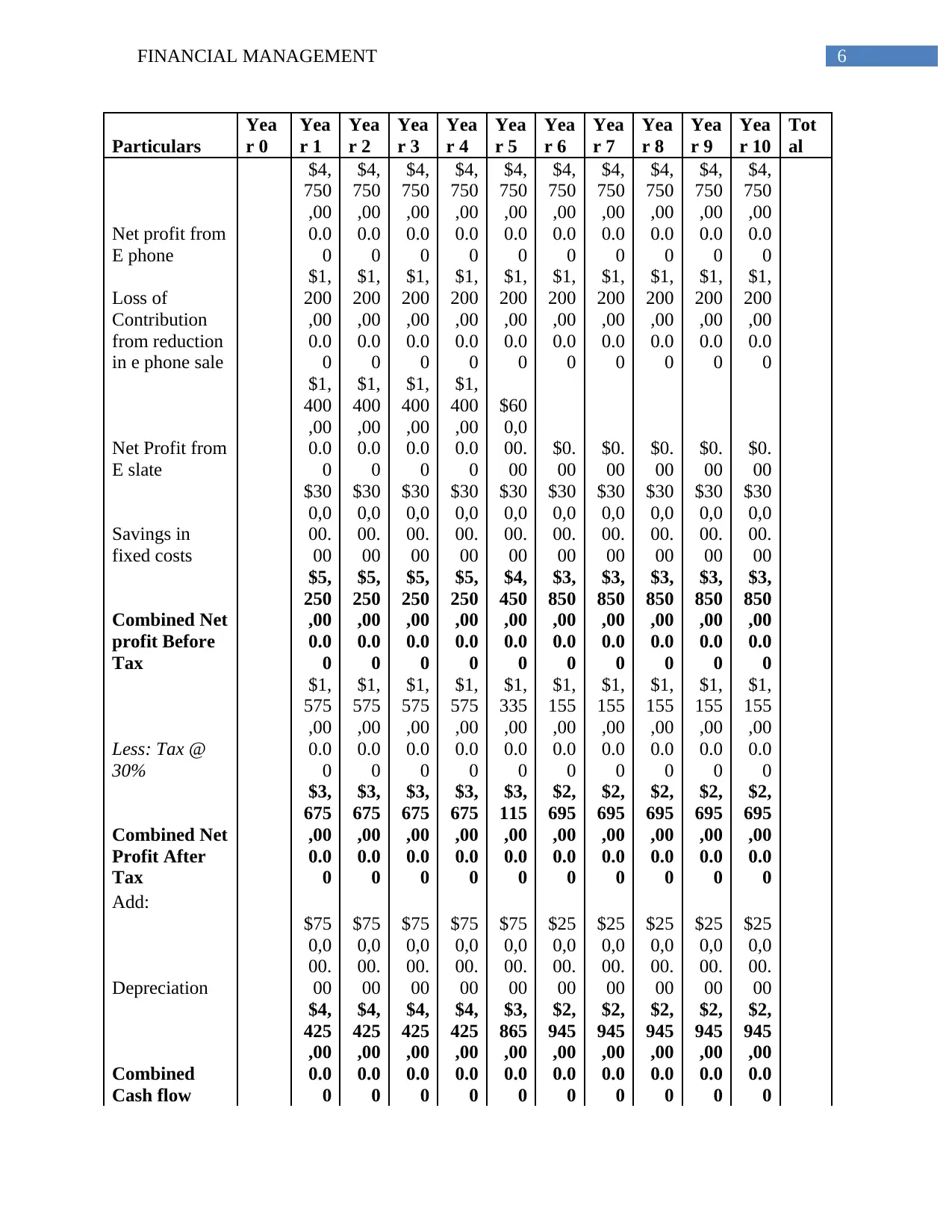

Combined

Calculation of NPV of combined Investment

6FINANCIAL MANAGEMENT

Particulars

Yea

r 0

Yea

r 1

Yea

r 2

Yea

r 3

Yea

r 4

Yea

r 5

Yea

r 6

Yea

r 7

Yea

r 8

Yea

r 9

Yea

r 10

Tot

al

Net profit from

E phone

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

Loss of

Contribution

from reduction

in e phone sale

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

Net Profit from

E slate

$1,

400

,00

0.0

0

$1,

400

,00

0.0

0

$1,

400

,00

0.0

0

$1,

400

,00

0.0

0

$60

0,0

00.

00

$0.

00

$0.

00

$0.

00

$0.

00

$0.

00

Savings in

fixed costs

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

Combined Net

profit Before

Tax

$5,

250

,00

0.0

0

$5,

250

,00

0.0

0

$5,

250

,00

0.0

0

$5,

250

,00

0.0

0

$4,

450

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

Less: Tax @

30%

$1,

575

,00

0.0

0

$1,

575

,00

0.0

0

$1,

575

,00

0.0

0

$1,

575

,00

0.0

0

$1,

335

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

Combined Net

Profit After

Tax

$3,

675

,00

0.0

0

$3,

675

,00

0.0

0

$3,

675

,00

0.0

0

$3,

675

,00

0.0

0

$3,

115

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

Add:

Depreciation

$75

0,0

00.

00

$75

0,0

00.

00

$75

0,0

00.

00

$75

0,0

00.

00

$75

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

Combined

Cash flow

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$3,

865

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

Particulars

Yea

r 0

Yea

r 1

Yea

r 2

Yea

r 3

Yea

r 4

Yea

r 5

Yea

r 6

Yea

r 7

Yea

r 8

Yea

r 9

Yea

r 10

Tot

al

Net profit from

E phone

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

$4,

750

,00

0.0

0

Loss of

Contribution

from reduction

in e phone sale

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

$1,

200

,00

0.0

0

Net Profit from

E slate

$1,

400

,00

0.0

0

$1,

400

,00

0.0

0

$1,

400

,00

0.0

0

$1,

400

,00

0.0

0

$60

0,0

00.

00

$0.

00

$0.

00

$0.

00

$0.

00

$0.

00

Savings in

fixed costs

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

$30

0,0

00.

00

Combined Net

profit Before

Tax

$5,

250

,00

0.0

0

$5,

250

,00

0.0

0

$5,

250

,00

0.0

0

$5,

250

,00

0.0

0

$4,

450

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

$3,

850

,00

0.0

0

Less: Tax @

30%

$1,

575

,00

0.0

0

$1,

575

,00

0.0

0

$1,

575

,00

0.0

0

$1,

575

,00

0.0

0

$1,

335

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

$1,

155

,00

0.0

0

Combined Net

Profit After

Tax

$3,

675

,00

0.0

0

$3,

675

,00

0.0

0

$3,

675

,00

0.0

0

$3,

675

,00

0.0

0

$3,

115

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

$2,

695

,00

0.0

0

Add:

Depreciation

$75

0,0

00.

00

$75

0,0

00.

00

$75

0,0

00.

00

$75

0,0

00.

00

$75

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

$25

0,0

00.

00

Combined

Cash flow

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$3,

865

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

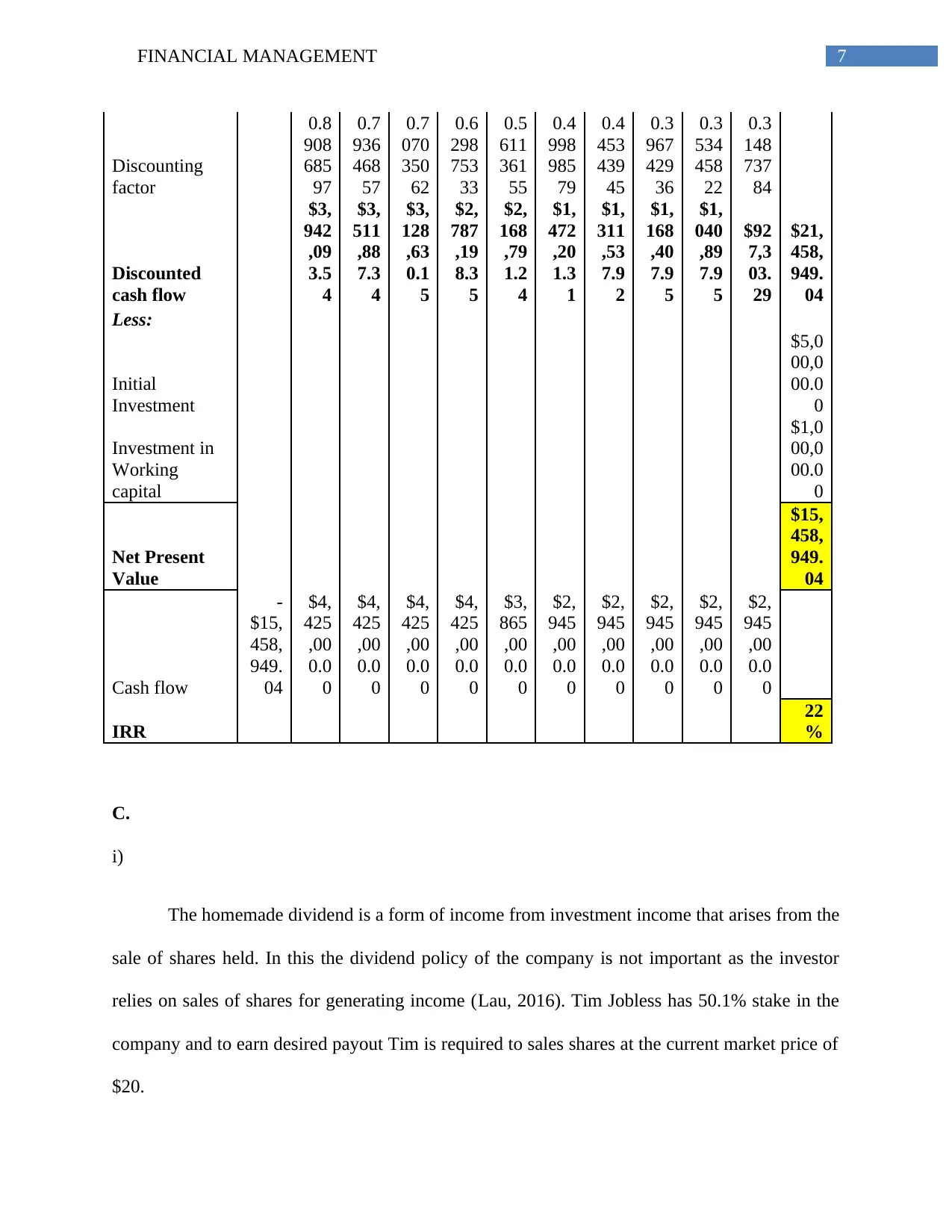

Discounting

factor

0.8

908

685

97

0.7

936

468

57

0.7

070

350

62

0.6

298

753

33

0.5

611

361

55

0.4

998

985

79

0.4

453

439

45

0.3

967

429

36

0.3

534

458

22

0.3

148

737

84

Discounted

cash flow

$3,

942

,09

3.5

4

$3,

511

,88

7.3

4

$3,

128

,63

0.1

5

$2,

787

,19

8.3

5

$2,

168

,79

1.2

4

$1,

472

,20

1.3

1

$1,

311

,53

7.9

2

$1,

168

,40

7.9

5

$1,

040

,89

7.9

5

$92

7,3

03.

29

$21,

458,

949.

04

Less:

Initial

Investment

$5,0

00,0

00.0

0

Investment in

Working

capital

$1,0

00,0

00.0

0

Net Present

Value

$15,

458,

949.

04

Cash flow

-

$15,

458,

949.

04

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$3,

865

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

IRR

22

%

C.

i)

The homemade dividend is a form of income from investment income that arises from the

sale of shares held. In this the dividend policy of the company is not important as the investor

relies on sales of shares for generating income (Lau, 2016). Tim Jobless has 50.1% stake in the

company and to earn desired payout Tim is required to sales shares at the current market price of

$20.

Discounting

factor

0.8

908

685

97

0.7

936

468

57

0.7

070

350

62

0.6

298

753

33

0.5

611

361

55

0.4

998

985

79

0.4

453

439

45

0.3

967

429

36

0.3

534

458

22

0.3

148

737

84

Discounted

cash flow

$3,

942

,09

3.5

4

$3,

511

,88

7.3

4

$3,

128

,63

0.1

5

$2,

787

,19

8.3

5

$2,

168

,79

1.2

4

$1,

472

,20

1.3

1

$1,

311

,53

7.9

2

$1,

168

,40

7.9

5

$1,

040

,89

7.9

5

$92

7,3

03.

29

$21,

458,

949.

04

Less:

Initial

Investment

$5,0

00,0

00.0

0

Investment in

Working

capital

$1,0

00,0

00.0

0

Net Present

Value

$15,

458,

949.

04

Cash flow

-

$15,

458,

949.

04

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$4,

425

,00

0.0

0

$3,

865

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

$2,

945

,00

0.0

0

IRR

22

%

C.

i)

The homemade dividend is a form of income from investment income that arises from the

sale of shares held. In this the dividend policy of the company is not important as the investor

relies on sales of shares for generating income (Lau, 2016). Tim Jobless has 50.1% stake in the

company and to earn desired payout Tim is required to sales shares at the current market price of

$20.

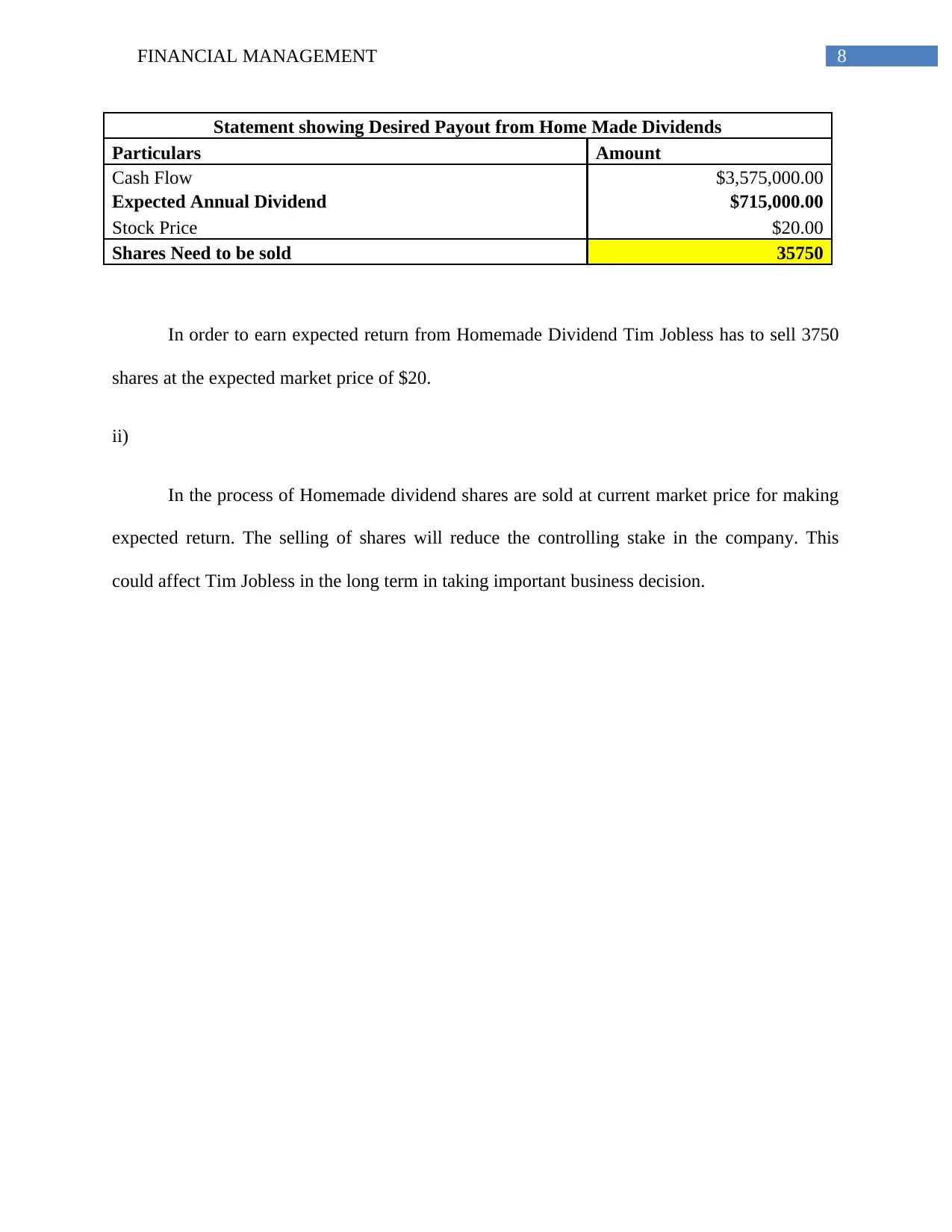

8FINANCIAL MANAGEMENT

Statement showing Desired Payout from Home Made Dividends

Particulars Amount

Cash Flow $3,575,000.00

Expected Annual Dividend $715,000.00

Stock Price $20.00

Shares Need to be sold 35750

In order to earn expected return from Homemade Dividend Tim Jobless has to sell 3750

shares at the expected market price of $20.

ii)

In the process of Homemade dividend shares are sold at current market price for making

expected return. The selling of shares will reduce the controlling stake in the company. This

could affect Tim Jobless in the long term in taking important business decision.

Statement showing Desired Payout from Home Made Dividends

Particulars Amount

Cash Flow $3,575,000.00

Expected Annual Dividend $715,000.00

Stock Price $20.00

Shares Need to be sold 35750

In order to earn expected return from Homemade Dividend Tim Jobless has to sell 3750

shares at the expected market price of $20.

ii)

In the process of Homemade dividend shares are sold at current market price for making

expected return. The selling of shares will reduce the controlling stake in the company. This

could affect Tim Jobless in the long term in taking important business decision.

9FINANCIAL MANAGEMENT

Reference

Lau, C. (2016). Financial Management.

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

Reference

Lau, C. (2016). Financial Management.

Titman, S., Keown, A. J., & Martin, J. D. (2017). Financial management: Principles and

applications. Pearson.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.