Management of the Affairs of the Organizations

VerifiedAdded on 2022/08/19

|6

|1280

|13

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

The investing decisions are key decisions in the management of the affairs of the

organizations and the evaluations of such decisions are conducted in the light of the

quantitative and qualitative factors (Ross, Westerfield, Jaffe & Kakani, 2014). These

decisions are important because of the involvement of the numerous resources such as

manpower, finance, technology, and other expertise; but also by the fact that the decisions

once taken would not be overturned (Goyat and Nain, 2016). Thus, careful evaluation of all

the factors involved is necessitated.

Analysis

There are varied financial techniques that help the financial managers to review the

financial feasibility of a project. The technique that is most used and most relevant is the Net

Present Value technique. Some of the key benefits of the Net Present Value technique over

the other evaluation techniques are time value of money consideration, the presentation of the

results in the complete form so as to assess the amount of the profit or loss, and the

consideration of the cash flows that arise even after the lifetime of the project (Brigham and

Houston, 2012). The NPV is calculated using the formula shown below.

NPV=∑

i=1

n CFi

(1+ d)i

= CF0 + CF1

(1+k )1 + CF 2

(1+k )2 + …. + CF 3

(1+k )3

where:

CFi = net cash flow from year i,

k = cost of capital or the rate for discounting

n = number of periods of the project

CF0 = amount of initial investment

The application of the NPV technique for the evaluation of the equipment for the

manufacturing of the Zithers by the Pristine Urban-Tech Zither, Inc. (PUTZ) has been

presented below.

The investing decisions are key decisions in the management of the affairs of the

organizations and the evaluations of such decisions are conducted in the light of the

quantitative and qualitative factors (Ross, Westerfield, Jaffe & Kakani, 2014). These

decisions are important because of the involvement of the numerous resources such as

manpower, finance, technology, and other expertise; but also by the fact that the decisions

once taken would not be overturned (Goyat and Nain, 2016). Thus, careful evaluation of all

the factors involved is necessitated.

Analysis

There are varied financial techniques that help the financial managers to review the

financial feasibility of a project. The technique that is most used and most relevant is the Net

Present Value technique. Some of the key benefits of the Net Present Value technique over

the other evaluation techniques are time value of money consideration, the presentation of the

results in the complete form so as to assess the amount of the profit or loss, and the

consideration of the cash flows that arise even after the lifetime of the project (Brigham and

Houston, 2012). The NPV is calculated using the formula shown below.

NPV=∑

i=1

n CFi

(1+ d)i

= CF0 + CF1

(1+k )1 + CF 2

(1+k )2 + …. + CF 3

(1+k )3

where:

CFi = net cash flow from year i,

k = cost of capital or the rate for discounting

n = number of periods of the project

CF0 = amount of initial investment

The application of the NPV technique for the evaluation of the equipment for the

manufacturing of the Zithers by the Pristine Urban-Tech Zither, Inc. (PUTZ) has been

presented below.

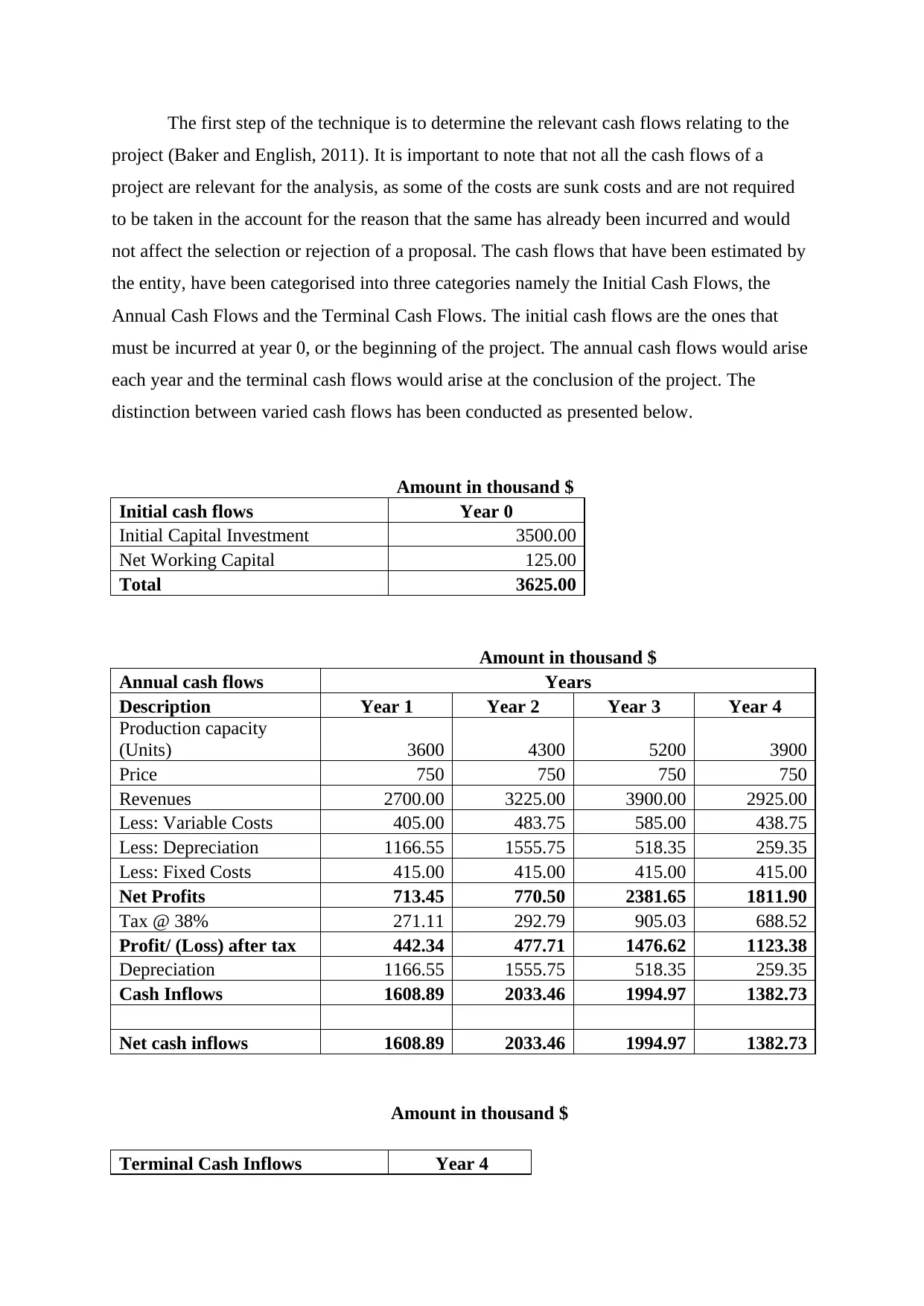

The first step of the technique is to determine the relevant cash flows relating to the

project (Baker and English, 2011). It is important to note that not all the cash flows of a

project are relevant for the analysis, as some of the costs are sunk costs and are not required

to be taken in the account for the reason that the same has already been incurred and would

not affect the selection or rejection of a proposal. The cash flows that have been estimated by

the entity, have been categorised into three categories namely the Initial Cash Flows, the

Annual Cash Flows and the Terminal Cash Flows. The initial cash flows are the ones that

must be incurred at year 0, or the beginning of the project. The annual cash flows would arise

each year and the terminal cash flows would arise at the conclusion of the project. The

distinction between varied cash flows has been conducted as presented below.

Amount in thousand $

Initial cash flows Year 0

Initial Capital Investment 3500.00

Net Working Capital 125.00

Total 3625.00

Amount in thousand $

Annual cash flows Years

Description Year 1 Year 2 Year 3 Year 4

Production capacity

(Units) 3600 4300 5200 3900

Price 750 750 750 750

Revenues 2700.00 3225.00 3900.00 2925.00

Less: Variable Costs 405.00 483.75 585.00 438.75

Less: Depreciation 1166.55 1555.75 518.35 259.35

Less: Fixed Costs 415.00 415.00 415.00 415.00

Net Profits 713.45 770.50 2381.65 1811.90

Tax @ 38% 271.11 292.79 905.03 688.52

Profit/ (Loss) after tax 442.34 477.71 1476.62 1123.38

Depreciation 1166.55 1555.75 518.35 259.35

Cash Inflows 1608.89 2033.46 1994.97 1382.73

Net cash inflows 1608.89 2033.46 1994.97 1382.73

Amount in thousand $

Terminal Cash Inflows Year 4

project (Baker and English, 2011). It is important to note that not all the cash flows of a

project are relevant for the analysis, as some of the costs are sunk costs and are not required

to be taken in the account for the reason that the same has already been incurred and would

not affect the selection or rejection of a proposal. The cash flows that have been estimated by

the entity, have been categorised into three categories namely the Initial Cash Flows, the

Annual Cash Flows and the Terminal Cash Flows. The initial cash flows are the ones that

must be incurred at year 0, or the beginning of the project. The annual cash flows would arise

each year and the terminal cash flows would arise at the conclusion of the project. The

distinction between varied cash flows has been conducted as presented below.

Amount in thousand $

Initial cash flows Year 0

Initial Capital Investment 3500.00

Net Working Capital 125.00

Total 3625.00

Amount in thousand $

Annual cash flows Years

Description Year 1 Year 2 Year 3 Year 4

Production capacity

(Units) 3600 4300 5200 3900

Price 750 750 750 750

Revenues 2700.00 3225.00 3900.00 2925.00

Less: Variable Costs 405.00 483.75 585.00 438.75

Less: Depreciation 1166.55 1555.75 518.35 259.35

Less: Fixed Costs 415.00 415.00 415.00 415.00

Net Profits 713.45 770.50 2381.65 1811.90

Tax @ 38% 271.11 292.79 905.03 688.52

Profit/ (Loss) after tax 442.34 477.71 1476.62 1123.38

Depreciation 1166.55 1555.75 518.35 259.35

Cash Inflows 1608.89 2033.46 1994.97 1382.73

Net cash inflows 1608.89 2033.46 1994.97 1382.73

Amount in thousand $

Terminal Cash Inflows Year 4

Net Working Capital 125.00

Profit on sale of land 350.00

Less: Tax on the profits 133.00

Total 342.00

It is to be noted that the purchase and the sale of the land is out of the perview of the

project proposal for the equipment, as the same has been already purchased and the revenue

realising from the sales from such land would not impact the revenues from the Zithers. In

addition to the above, the analysis cost of the market of the product has also not been

considered because the same is also a sunk cost. The fact that either the proposal is selected

or rejected would not make any difference to the sunk costs like marketing cost, as the same

is already been expensed (Gray, Larson & Desai, 2011). The amount of working capital

would also be introduced in the year 0 and the same is assumed to be recovered in the

terminal year. In addition it is to be noted that in the MACRS depreciation method, there is

no terminal value of the project as the same has been depreciated over the years. However, as

the equipment is stated to be scrapped for $ 350000, the same has been regarded as the profit

on the sale of the equipment.

The present values of the cash flows are calculated as follows at the rate of 13%.

NPV=

Net present value

Year Cash flows PVF@13.00% Present value

Year 0 -3625.00 1.00 -3625.00

Year 1 1608.89 0.88 1423.80

Year 2 2033.46 0.78 1592.50

Year 3 1994.97 0.69 1382.62

Year 4 1382.73 0.61 848.05

Year 4 342.00 0.61 209.76

NPV 1831.72

The selection of the single proposal depends on the fact that the NPV is positive or

negative (Rὂhrich, 2014). If the NPV is computed to be positive, it is beneficial to accept the

proposal subject to the qualitative factors; and vice versa (Pogue, 2010). In the case of project

Profit on sale of land 350.00

Less: Tax on the profits 133.00

Total 342.00

It is to be noted that the purchase and the sale of the land is out of the perview of the

project proposal for the equipment, as the same has been already purchased and the revenue

realising from the sales from such land would not impact the revenues from the Zithers. In

addition to the above, the analysis cost of the market of the product has also not been

considered because the same is also a sunk cost. The fact that either the proposal is selected

or rejected would not make any difference to the sunk costs like marketing cost, as the same

is already been expensed (Gray, Larson & Desai, 2011). The amount of working capital

would also be introduced in the year 0 and the same is assumed to be recovered in the

terminal year. In addition it is to be noted that in the MACRS depreciation method, there is

no terminal value of the project as the same has been depreciated over the years. However, as

the equipment is stated to be scrapped for $ 350000, the same has been regarded as the profit

on the sale of the equipment.

The present values of the cash flows are calculated as follows at the rate of 13%.

NPV=

Net present value

Year Cash flows PVF@13.00% Present value

Year 0 -3625.00 1.00 -3625.00

Year 1 1608.89 0.88 1423.80

Year 2 2033.46 0.78 1592.50

Year 3 1994.97 0.69 1382.62

Year 4 1382.73 0.61 848.05

Year 4 342.00 0.61 209.76

NPV 1831.72

The selection of the single proposal depends on the fact that the NPV is positive or

negative (Rὂhrich, 2014). If the NPV is computed to be positive, it is beneficial to accept the

proposal subject to the qualitative factors; and vice versa (Pogue, 2010). In the case of project

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

proposal as evaluated above, the NPV has been computed to be positive 1831.72. This means

the estimated cash flows would not only cover the initial cost, but also lead to profits to the

tune of 1831.72.

Conclusion

As per the evaluation of the proposal as conducted in the previous parts, it is

recommended to the entity to accept the proposal of the said equipment as the NPV of the

cash flows has been worked out to be positive.

the estimated cash flows would not only cover the initial cost, but also lead to profits to the

tune of 1831.72.

Conclusion

As per the evaluation of the proposal as conducted in the previous parts, it is

recommended to the entity to accept the proposal of the said equipment as the NPV of the

cash flows has been worked out to be positive.

References

Baker, H. K., & English, P. (2011) Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons Inc.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of Financial Management. Boston

MA: Cengage Learning.

Goyat, S., & Nain, A. (2016). Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Gray, C. F., Larson, E. W., & Desai, G. V. (2011). Project Management. The Managerial

Process. 4th ed. New Delhi: Tata McGraw Hill Education Pvt. Ltd./

Pogue, M. (2010). Corporate Investment Decisions: Principles and Practice. New York:

Business Expert Press, p. 53.

Ross, S. A., Westerfield, R. W., Jaffe, J., & Kakani, R. K. (2014) Corporate Finance. 8th ed.

New Delhi: Tata McGraw Hill Education Pvt Ltd.

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a Case

Study. Boston: Walter de Gruyter GmbH & Co.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press.

Baker, H. K., & English, P. (2011) Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons Inc.

Brigham, E. F., & Houston, J. F. (2012). Fundamentals of Financial Management. Boston

MA: Cengage Learning.

Goyat, S., & Nain, A. (2016). Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Gray, C. F., Larson, E. W., & Desai, G. V. (2011). Project Management. The Managerial

Process. 4th ed. New Delhi: Tata McGraw Hill Education Pvt. Ltd./

Pogue, M. (2010). Corporate Investment Decisions: Principles and Practice. New York:

Business Expert Press, p. 53.

Ross, S. A., Westerfield, R. W., Jaffe, J., & Kakani, R. K. (2014) Corporate Finance. 8th ed.

New Delhi: Tata McGraw Hill Education Pvt Ltd.

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a Case

Study. Boston: Walter de Gruyter GmbH & Co.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.