Financial Analysis and Agency Theory in Financial Management

VerifiedAdded on 2021/02/20

|13

|4054

|151

Report

AI Summary

This report provides a detailed financial analysis of Marks and Spencer (M&S), a British global retailer. The study focuses on financial management through ratio analysis, including liquidity, profitability, and gearing ratios, for the years 2018 and 2019. It explains the purpose and relevance of these ratios for stakeholders, analyzes M&S's performance, and highlights areas of concern. Furthermore, the report critically evaluates the use of financial ratios in interpreting and measuring performance. The second part of the report discusses and evaluates agency theory and its application in various business situations where conflicts may arise, specifically in the context of M&S. The analysis includes the interpretation of financial ratios, highlighting strengths, weaknesses, and potential risks for stakeholders. Finally, the report critically evaluates the use of financial ratios in the context of interpreting and measuring performance, discussing both advantages and limitations.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Assessment.......................................................................................................................................1

TASK 1............................................................................................................................................1

a. Explaining purpose and the relevance of the selected ratios in respect of the stakeholders...1

b. Ratio analysis of Marks and Spencer Group Plc for the year 2018 and 2019........................2

c. Highlighting the performance of the company by showing the concern areas for the

stakeholders.................................................................................................................................4

d. Critically evaluating the use of the financial ratios in context of interpreting and

performance measurement .........................................................................................................5

TASK 2............................................................................................................................................6

Critically evaluating the agency theory and its use in various business situation under which

the conflict is been reported........................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Assessment.......................................................................................................................................1

TASK 1............................................................................................................................................1

a. Explaining purpose and the relevance of the selected ratios in respect of the stakeholders...1

b. Ratio analysis of Marks and Spencer Group Plc for the year 2018 and 2019........................2

c. Highlighting the performance of the company by showing the concern areas for the

stakeholders.................................................................................................................................4

d. Critically evaluating the use of the financial ratios in context of interpreting and

performance measurement .........................................................................................................5

TASK 2............................................................................................................................................6

Critically evaluating the agency theory and its use in various business situation under which

the conflict is been reported........................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management referred as significant activity or the practice of planning,

controlling, organising and monitoring the financial resources for achieving the organizational

goals effectively and efficiently. The present study is based on Marks and Spencer, a British

global retailer, deals in clothing, food and the home products. Furthermore, the study throws a

deep insights towards the financial analysis of the Marks and Spencer financial results through

ratio analysis. Moreover, it describes the agency theory and the problems relating to it that has

been faced by the company.

Assessment

TASK 1

a. Explaining purpose and the relevance of the selected ratios in respect of the stakeholders

Ratio analysis refers to the quantitative method that is been used for gaining the insight

towards the towards the liquidity, profitability and the operational efficiency by making the

comparison of the figures that are contained in the financial statements of Marks and Spencer

(Karadag, 2015). This helps the internal and the external stakeholders in assessing the trend of

the company's performance and the position over the time which in turn helps them in making

suitable decisions through comparing the results of M&S with its competitors. Under this study,

liquidity, profitability and the gearing ratios has been selected in order to measure the

performance of an enterprise.

Liquidity ratios- It means the ratios that are used for measuring the capability of the

organization in paying off its current obligations. It includes the current ratio and acid test or

quick ratio. These ratios makes comparison in between various combination of the liquid assets

with that of the current liabilities. It has been stated that greater the ratio, better is the liquidity

position of the company in meeting its short term liabilities effectively. Liquidity ratios helps the

stakeholders like the suppliers and the creditors in knowing the liquidity position of Marks and

Spencer in terms the use of its current assets against its short term liability so as to assess the

ability of the firm in meeting its liability on time (Ward and Forker, 2017). It also helps the

stakeholder in determining the efficient use of the working capital is been made or not within the

organization. It enables the rating agencies for making the analysis of the solvency position so

that it could provide the ratings accordingly.

1

Financial management referred as significant activity or the practice of planning,

controlling, organising and monitoring the financial resources for achieving the organizational

goals effectively and efficiently. The present study is based on Marks and Spencer, a British

global retailer, deals in clothing, food and the home products. Furthermore, the study throws a

deep insights towards the financial analysis of the Marks and Spencer financial results through

ratio analysis. Moreover, it describes the agency theory and the problems relating to it that has

been faced by the company.

Assessment

TASK 1

a. Explaining purpose and the relevance of the selected ratios in respect of the stakeholders

Ratio analysis refers to the quantitative method that is been used for gaining the insight

towards the towards the liquidity, profitability and the operational efficiency by making the

comparison of the figures that are contained in the financial statements of Marks and Spencer

(Karadag, 2015). This helps the internal and the external stakeholders in assessing the trend of

the company's performance and the position over the time which in turn helps them in making

suitable decisions through comparing the results of M&S with its competitors. Under this study,

liquidity, profitability and the gearing ratios has been selected in order to measure the

performance of an enterprise.

Liquidity ratios- It means the ratios that are used for measuring the capability of the

organization in paying off its current obligations. It includes the current ratio and acid test or

quick ratio. These ratios makes comparison in between various combination of the liquid assets

with that of the current liabilities. It has been stated that greater the ratio, better is the liquidity

position of the company in meeting its short term liabilities effectively. Liquidity ratios helps the

stakeholders like the suppliers and the creditors in knowing the liquidity position of Marks and

Spencer in terms the use of its current assets against its short term liability so as to assess the

ability of the firm in meeting its liability on time (Ward and Forker, 2017). It also helps the

stakeholder in determining the efficient use of the working capital is been made or not within the

organization. It enables the rating agencies for making the analysis of the solvency position so

that it could provide the ratings accordingly.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability ratios- It refers to the financial metric that is used for assessing the ability of

the firm in generating the earnings in relation to its revenues, assets, shareholders equity and the

operating cost for a particular accounting period. It includes operating profits, net profit margin,

return on assets and the return on capital employed. The major purpose of profitability ratio is to

provide for the results to the users regarding the earnings and the profits that are gained by the

organization against its sales, assets and the capital (Choi and et.al., 2018). All the stakeholders

are very much concerned about the profitability or the performance of an entity because of the

investments made by them with expectation to gain maximum profit margins. Investors and the

shareholders are the major stakeholders that are has the keen interest in finding out that the

company is performing good or not and in making the decisions regarding further investment,

withdrawal or decreasing the holding.

Gearing ratios- It refers to the financial ratio that is been utilized for measuring

proportion of the borrowed funds towards the equity of the company. This ratio reflects financial

risk through which the business is been affected as the excess of the debts could result to the

financial difficulties. It involves the debt-equity and the interest coverage ratios. Greater gearing

ratio indicates the high proportion of the debt to the equity, whereas the lower gearing ratio states

the lower proportion of the debt against the equity. The purpose of gearing ratio is to assess the

capital structure of the organization and in providing the results to the users regarding the long-

term stability of the Marks and Spencer business (Uechi and et.al., 2015). This information assist

the stakeholders in evaluating failure risk associated with the business and in analysing that the

company is capable in paying off its borrowings on time. It also helps the users in finding out the

interest burden on the firm and in assessing that it has the ability to cover its finance cost or not.

Lenders and the creditors are the main stakeholders that has the interest in the results that are

ascertained from the gearing ratios.

b. Ratio analysis of Marks and Spencer Group Plc for the year 2018 and 2019

Particulars 2018 (in £million) 2019 (in £million )

Liquidity ratio

Current Ratio

Current Assets 1317.9 1490.4

Current Liabilities 1826 2228.4

2

the firm in generating the earnings in relation to its revenues, assets, shareholders equity and the

operating cost for a particular accounting period. It includes operating profits, net profit margin,

return on assets and the return on capital employed. The major purpose of profitability ratio is to

provide for the results to the users regarding the earnings and the profits that are gained by the

organization against its sales, assets and the capital (Choi and et.al., 2018). All the stakeholders

are very much concerned about the profitability or the performance of an entity because of the

investments made by them with expectation to gain maximum profit margins. Investors and the

shareholders are the major stakeholders that are has the keen interest in finding out that the

company is performing good or not and in making the decisions regarding further investment,

withdrawal or decreasing the holding.

Gearing ratios- It refers to the financial ratio that is been utilized for measuring

proportion of the borrowed funds towards the equity of the company. This ratio reflects financial

risk through which the business is been affected as the excess of the debts could result to the

financial difficulties. It involves the debt-equity and the interest coverage ratios. Greater gearing

ratio indicates the high proportion of the debt to the equity, whereas the lower gearing ratio states

the lower proportion of the debt against the equity. The purpose of gearing ratio is to assess the

capital structure of the organization and in providing the results to the users regarding the long-

term stability of the Marks and Spencer business (Uechi and et.al., 2015). This information assist

the stakeholders in evaluating failure risk associated with the business and in analysing that the

company is capable in paying off its borrowings on time. It also helps the users in finding out the

interest burden on the firm and in assessing that it has the ability to cover its finance cost or not.

Lenders and the creditors are the main stakeholders that has the interest in the results that are

ascertained from the gearing ratios.

b. Ratio analysis of Marks and Spencer Group Plc for the year 2018 and 2019

Particulars 2018 (in £million) 2019 (in £million )

Liquidity ratio

Current Ratio

Current Assets 1317.9 1490.4

Current Liabilities 1826 2228.4

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

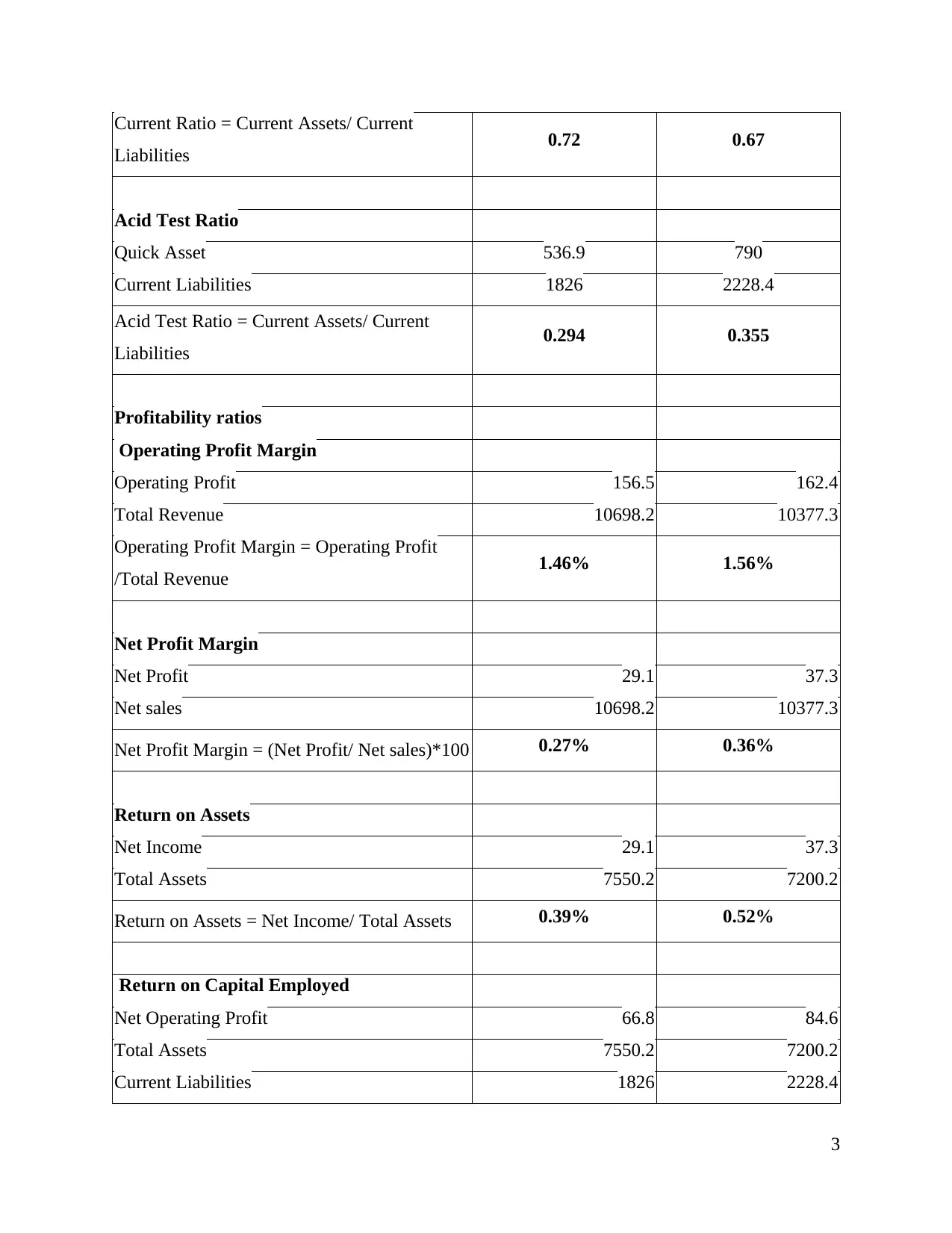

Current Ratio = Current Assets/ Current

Liabilities 0.72 0.67

Acid Test Ratio

Quick Asset 536.9 790

Current Liabilities 1826 2228.4

Acid Test Ratio = Current Assets/ Current

Liabilities 0.294 0.355

Profitability ratios

Operating Profit Margin

Operating Profit 156.5 162.4

Total Revenue 10698.2 10377.3

Operating Profit Margin = Operating Profit

/Total Revenue 1.46% 1.56%

Net Profit Margin

Net Profit 29.1 37.3

Net sales 10698.2 10377.3

Net Profit Margin = (Net Profit/ Net sales)*100 0.27% 0.36%

Return on Assets

Net Income 29.1 37.3

Total Assets 7550.2 7200.2

Return on Assets = Net Income/ Total Assets 0.39% 0.52%

Return on Capital Employed

Net Operating Profit 66.8 84.6

Total Assets 7550.2 7200.2

Current Liabilities 1826 2228.4

3

Liabilities 0.72 0.67

Acid Test Ratio

Quick Asset 536.9 790

Current Liabilities 1826 2228.4

Acid Test Ratio = Current Assets/ Current

Liabilities 0.294 0.355

Profitability ratios

Operating Profit Margin

Operating Profit 156.5 162.4

Total Revenue 10698.2 10377.3

Operating Profit Margin = Operating Profit

/Total Revenue 1.46% 1.56%

Net Profit Margin

Net Profit 29.1 37.3

Net sales 10698.2 10377.3

Net Profit Margin = (Net Profit/ Net sales)*100 0.27% 0.36%

Return on Assets

Net Income 29.1 37.3

Total Assets 7550.2 7200.2

Return on Assets = Net Income/ Total Assets 0.39% 0.52%

Return on Capital Employed

Net Operating Profit 66.8 84.6

Total Assets 7550.2 7200.2

Current Liabilities 1826 2228.4

3

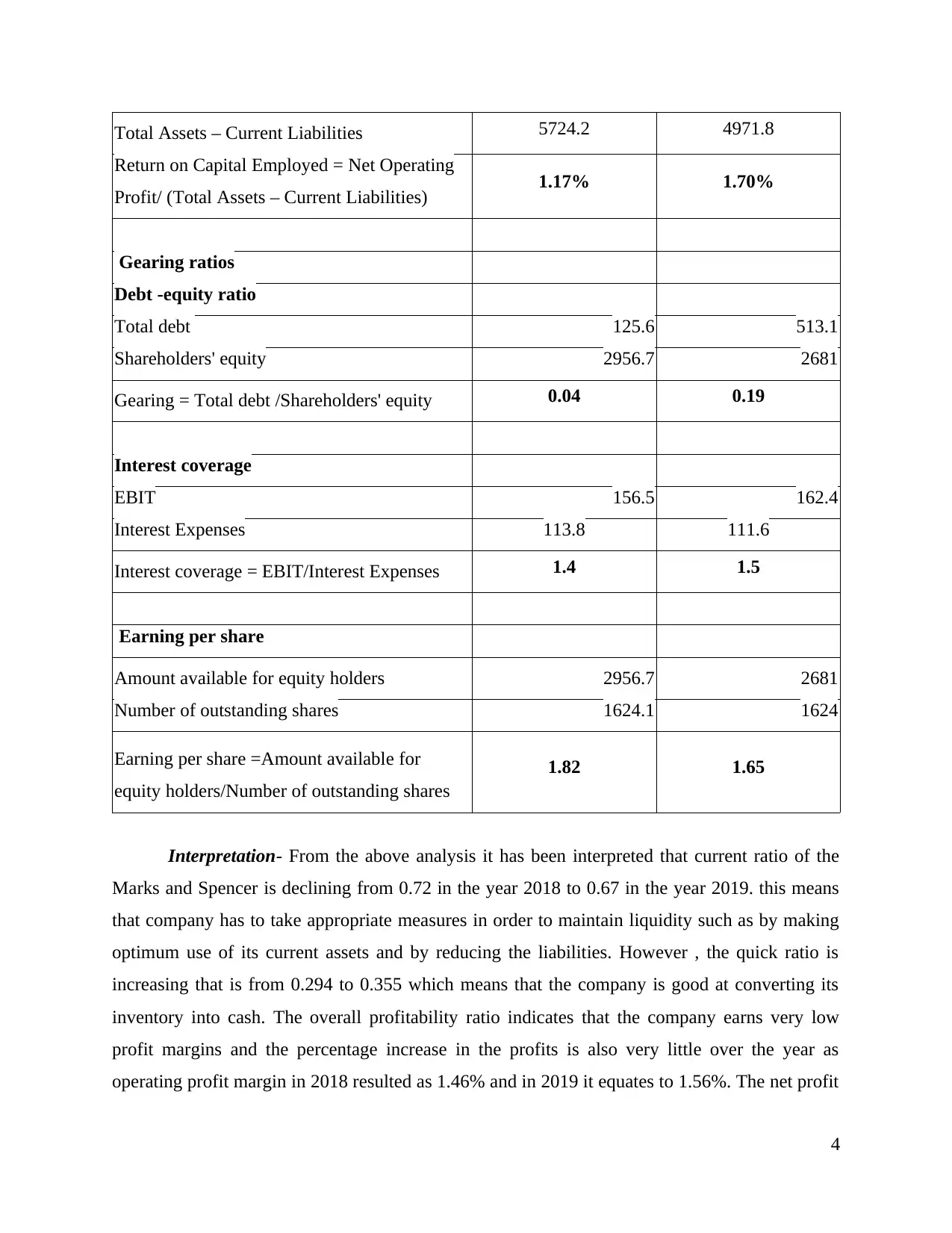

Total Assets – Current Liabilities 5724.2 4971.8

Return on Capital Employed = Net Operating

Profit/ (Total Assets – Current Liabilities) 1.17% 1.70%

Gearing ratios

Debt -equity ratio

Total debt 125.6 513.1

Shareholders' equity 2956.7 2681

Gearing = Total debt /Shareholders' equity 0.04 0.19

Interest coverage

EBIT 156.5 162.4

Interest Expenses 113.8 111.6

Interest coverage = EBIT/Interest Expenses 1.4 1.5

Earning per share

Amount available for equity holders 2956.7 2681

Number of outstanding shares 1624.1 1624

Earning per share =Amount available for

equity holders/Number of outstanding shares

1.82 1.65

Interpretation- From the above analysis it has been interpreted that current ratio of the

Marks and Spencer is declining from 0.72 in the year 2018 to 0.67 in the year 2019. this means

that company has to take appropriate measures in order to maintain liquidity such as by making

optimum use of its current assets and by reducing the liabilities. However , the quick ratio is

increasing that is from 0.294 to 0.355 which means that the company is good at converting its

inventory into cash. The overall profitability ratio indicates that the company earns very low

profit margins and the percentage increase in the profits is also very little over the year as

operating profit margin in 2018 resulted as 1.46% and in 2019 it equates to 1.56%. The net profit

4

Return on Capital Employed = Net Operating

Profit/ (Total Assets – Current Liabilities) 1.17% 1.70%

Gearing ratios

Debt -equity ratio

Total debt 125.6 513.1

Shareholders' equity 2956.7 2681

Gearing = Total debt /Shareholders' equity 0.04 0.19

Interest coverage

EBIT 156.5 162.4

Interest Expenses 113.8 111.6

Interest coverage = EBIT/Interest Expenses 1.4 1.5

Earning per share

Amount available for equity holders 2956.7 2681

Number of outstanding shares 1624.1 1624

Earning per share =Amount available for

equity holders/Number of outstanding shares

1.82 1.65

Interpretation- From the above analysis it has been interpreted that current ratio of the

Marks and Spencer is declining from 0.72 in the year 2018 to 0.67 in the year 2019. this means

that company has to take appropriate measures in order to maintain liquidity such as by making

optimum use of its current assets and by reducing the liabilities. However , the quick ratio is

increasing that is from 0.294 to 0.355 which means that the company is good at converting its

inventory into cash. The overall profitability ratio indicates that the company earns very low

profit margins and the percentage increase in the profits is also very little over the year as

operating profit margin in 2018 resulted as 1.46% and in 2019 it equates to 1.56%. The net profit

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

margin in the year 2018 were 0.27% to 0.36% during the year 2019. Similarly, the return on

assets and capital employed are also increasing. The gearing ratio is also showing an increasing

results which means that the borrowings of the firm has increased over the year and the

shareholders equity has decreased. Increase in the interest coverage ratio reflected a good sign as

it states that the company is capable of meeting its interest obligation.

c. Highlighting the performance of the company by showing the concern areas for the

stakeholders

The overall performance of M&S is not sound and does not reflect better results as its

earning capacity is very low due to lower sales margins which of great concern for the

stakeholders as the performance of the company is been depicted by the profitability and if the

profits are low than the shareholders will get very low amount of dividend. Investors who has

made the investment in the enterprise also gets affected as they could not be able gain higher

returns from as the profits margin is low. The borrowings of the company are also increasing

with a higher amount which and the shareholders equity is decreasing which is considered as the

major concern for the stakeholders as this results in higher debt-to-equity ratio which means that

the financial burden on the enterprise is getting higher and the size of holding within the firm is

declining, this results in higher obligation on the corporate which in turn affects the solvency

position of an entity (Altman and et.al., 2017). The liquidity position is also showing a declining

trend which is also counted as the concern because stakeholders are highly affected by the liquid

position of an enterprise as it is directly linked with meeting the short term obligation which

plays a critical role in smooth functioning of the routine operations within the work environment.

d. Critically evaluating the use of the financial ratios in context of interpreting and performance

measurement

Financial ratios refers to the relationship which is been determined from the financial

information of the company and is used for the purpose of making the comparison.

Advantages Limitations

Ratio analysis helps in validating and

disproving financing, operating and the

investment decisions of an entity. It

helps in summarizing final reports into

the comparative figures and thus

Financial ratios ignores the changes in

the price level because of the inflation.

This leads to the incorrect evaluation of

financial health of an entity.

It also ignores qualitative

5

assets and capital employed are also increasing. The gearing ratio is also showing an increasing

results which means that the borrowings of the firm has increased over the year and the

shareholders equity has decreased. Increase in the interest coverage ratio reflected a good sign as

it states that the company is capable of meeting its interest obligation.

c. Highlighting the performance of the company by showing the concern areas for the

stakeholders

The overall performance of M&S is not sound and does not reflect better results as its

earning capacity is very low due to lower sales margins which of great concern for the

stakeholders as the performance of the company is been depicted by the profitability and if the

profits are low than the shareholders will get very low amount of dividend. Investors who has

made the investment in the enterprise also gets affected as they could not be able gain higher

returns from as the profits margin is low. The borrowings of the company are also increasing

with a higher amount which and the shareholders equity is decreasing which is considered as the

major concern for the stakeholders as this results in higher debt-to-equity ratio which means that

the financial burden on the enterprise is getting higher and the size of holding within the firm is

declining, this results in higher obligation on the corporate which in turn affects the solvency

position of an entity (Altman and et.al., 2017). The liquidity position is also showing a declining

trend which is also counted as the concern because stakeholders are highly affected by the liquid

position of an enterprise as it is directly linked with meeting the short term obligation which

plays a critical role in smooth functioning of the routine operations within the work environment.

d. Critically evaluating the use of the financial ratios in context of interpreting and performance

measurement

Financial ratios refers to the relationship which is been determined from the financial

information of the company and is used for the purpose of making the comparison.

Advantages Limitations

Ratio analysis helps in validating and

disproving financing, operating and the

investment decisions of an entity. It

helps in summarizing final reports into

the comparative figures and thus

Financial ratios ignores the changes in

the price level because of the inflation.

This leads to the incorrect evaluation of

financial health of an entity.

It also ignores qualitative

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enables the management in comparing

and evaluating financial position of the

company.

It is used for simplifying the complex

financial statements and the financial

data into the ratios of the operating and

financial efficiency.

It helps in identifying the problem if

any present in the management and the

financial areas.

It allows the enterprise in conducting

the comparative analysis with its

competitors, industry standards etc.

which in turn helps in developing better

understanding of the fiscal position

throughout the economy.

characteristics that are associated with

the performance of the firm. It only

considers monetary aspects.

Accounting ratios are not the good

measure for resolving the financial

problems faced by the organization

(Gomez-Mejia, Patel and Zellweger,

2018). They only act as the means and

could not be used for getting actual

solution.

TASK 2

Critically evaluating the agency theory and its use in various business situation under which the

conflict is been reported

Agency theory refers to the principle which is been used for resolving the issues that

occurs in the relationship of the business and their agents. For example- it reflects the

relationship in between the shareholders as the principle and the executive of the company as the

agents. Theory of agency addresses the disputes that might arise majorly in two areas that

includes the difference in the goals and the in the risk aversion. This theory makes the

assumption that there is the conflict in relation to the interest of the principal and the agent. In

other words it means there is no any alignment in between the principal and the agent because of

the difference in their interest.

In accordance with the Edwards, Schwab and Shevlin, (2015), it has been reviewed that

under the agency theory helps in developing the good relationship between the principal and its

6

and evaluating financial position of the

company.

It is used for simplifying the complex

financial statements and the financial

data into the ratios of the operating and

financial efficiency.

It helps in identifying the problem if

any present in the management and the

financial areas.

It allows the enterprise in conducting

the comparative analysis with its

competitors, industry standards etc.

which in turn helps in developing better

understanding of the fiscal position

throughout the economy.

characteristics that are associated with

the performance of the firm. It only

considers monetary aspects.

Accounting ratios are not the good

measure for resolving the financial

problems faced by the organization

(Gomez-Mejia, Patel and Zellweger,

2018). They only act as the means and

could not be used for getting actual

solution.

TASK 2

Critically evaluating the agency theory and its use in various business situation under which the

conflict is been reported

Agency theory refers to the principle which is been used for resolving the issues that

occurs in the relationship of the business and their agents. For example- it reflects the

relationship in between the shareholders as the principle and the executive of the company as the

agents. Theory of agency addresses the disputes that might arise majorly in two areas that

includes the difference in the goals and the in the risk aversion. This theory makes the

assumption that there is the conflict in relation to the interest of the principal and the agent. In

other words it means there is no any alignment in between the principal and the agent because of

the difference in their interest.

In accordance with the Edwards, Schwab and Shevlin, (2015), it has been reviewed that

under the agency theory helps in developing the good relationship between the principal and its

6

agent. This reflects that the both of them are been assumed as solely motivated by their self-

interest. However, Shogren, Wehmeyer and Palmer, (2017) analysed that agency theory

anticipate for the complete contracts which includes the catering of all the possible contingencies

like language ambiguity, uncertain events and inadvertence. Such bounded rationality results in

inefficient and incomplete contracts. On the other state, it has also been suggested by the Bosse

and Phillips, (2016) that, at the time when the principal delegates the responsibility regarding

the decision making to its agent, this creates self-motivation within the agents which in turn

could result in better performance. On the other hand, sometimes the agent could use it as the

power in promoting their well-being and will opt for such actions that might not be best to the

interest of the principal.

Pepper and Gore, (2015) also identified that, In the agency relationship, agents and the

principals are assumed as the rational persons who are been capable in forming the unbiased

anticipation relating to the effect of the problem in the agency in consideration with the

associated value of their future wealth. Moreover, agency theory also assumes that the

contracting could eliminate the agency cost and the competence aspect is also not taken into

consideration. Mitnick, (2015) also viewed that the there exist the contractual relationship in

between the principal and the agent which implies for making decisions in such a way that

results in maximizing returns for the shareholders in order to maximize the wealth of the

organization. Banks and et.al., (2018) also stated that, agency theory provides for conflicting

interest of the principals and the agents as the shareholders has the keen interest in the financial

performance while the directors or the executives might has the interest in their duty. This theory

does not recognises for the effect of the third party. These are the party that are been affected by

contract but are not the party that are indulged in the contract.

It has also been determined by the Chari and et.al., (2019) that as per the theory the agent

does not own the resources of the corporation, so they may make misuse of those resources or

might commit for the moral hazards like shirking the duties or enjoying leisure and also hiding

the in efficiencies in order to avoid the reward loss. It is been done by the Prosman Scholten and

Power, (2016) because of the enhancing their personal wealth at cost of its principal. However,

as per the Bendickson and et.al., (2016) it has also been viewed that, for minimizing such

problems mainly two steps has been recognised that includes, firstly the risk-bearing capacity of

the principal-agent is to b monitored by nexus of the contracts and the organization. Secondly,

7

interest. However, Shogren, Wehmeyer and Palmer, (2017) analysed that agency theory

anticipate for the complete contracts which includes the catering of all the possible contingencies

like language ambiguity, uncertain events and inadvertence. Such bounded rationality results in

inefficient and incomplete contracts. On the other state, it has also been suggested by the Bosse

and Phillips, (2016) that, at the time when the principal delegates the responsibility regarding

the decision making to its agent, this creates self-motivation within the agents which in turn

could result in better performance. On the other hand, sometimes the agent could use it as the

power in promoting their well-being and will opt for such actions that might not be best to the

interest of the principal.

Pepper and Gore, (2015) also identified that, In the agency relationship, agents and the

principals are assumed as the rational persons who are been capable in forming the unbiased

anticipation relating to the effect of the problem in the agency in consideration with the

associated value of their future wealth. Moreover, agency theory also assumes that the

contracting could eliminate the agency cost and the competence aspect is also not taken into

consideration. Mitnick, (2015) also viewed that the there exist the contractual relationship in

between the principal and the agent which implies for making decisions in such a way that

results in maximizing returns for the shareholders in order to maximize the wealth of the

organization. Banks and et.al., (2018) also stated that, agency theory provides for conflicting

interest of the principals and the agents as the shareholders has the keen interest in the financial

performance while the directors or the executives might has the interest in their duty. This theory

does not recognises for the effect of the third party. These are the party that are been affected by

contract but are not the party that are indulged in the contract.

It has also been determined by the Chari and et.al., (2019) that as per the theory the agent

does not own the resources of the corporation, so they may make misuse of those resources or

might commit for the moral hazards like shirking the duties or enjoying leisure and also hiding

the in efficiencies in order to avoid the reward loss. It is been done by the Prosman Scholten and

Power, (2016) because of the enhancing their personal wealth at cost of its principal. However,

as per the Bendickson and et.al., (2016) it has also been viewed that, for minimizing such

problems mainly two steps has been recognised that includes, firstly the risk-bearing capacity of

the principal-agent is to b monitored by nexus of the contracts and the organization. Secondly,

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determining it as the positive theory of agency by clarifying the ways in which the enterprise

uses contractual monitoring and the bonding that is been bear on which structure is designed.

On the other side, it is been highlighted that this theory does not considers the

competence aspect and because of this even those managers who are not competent and are

incapable in carrying out the task are appointed. Agency theory does not call for those persons

who are been loyal towards the organization. Moreover, it is the theory that treats the mangers as

they are opportunistic, solely motivated with that of their self-interest. Thus, in accordance with

the agency theory it has been studied that there exist the divergence of the interest and the

purpose of the mangers and the shareholders, one is the person who expects for the separation of

an ownership and the control leads to the damaging effect over the performance of an entity.

This problem could be overcome by direct monitoring on the shareholders through the

concentrated ownership. Such use of the ownership helps in increasing the improvement in the

performance of an enterprise.

The agent under this theory has more of the information as compared to the principal, this

difference of knowledge is been called as the asymmetric information. It is also been studied by

the Bøe, Gulbrandsen and Sørebø, (2015), that the principal could not always ensure for the

performance of the agent to their best interest. This departure of the interest from principal to

agent is called as agency cost. Hence agency theory cause many problems that includes the

difference of interest, personal goals etc. Agency theory assess the cost incurred by reviewing

financial decisions in context of the risk, trade-off and the profitability in between the parties

interest. Principal bears particular costs for reducing possibility of agent in prioritizing the value

of its agent. For the equity holders, such cost are classified as the monitoring cost, residual cost

and the bonding cost.

Examples- Portfolio managers and the financial planners are considered as agents and are

having the responsibility towards their principal assets.

In the real life business situations, this problem occurs in respect of the ways in which the

company is been owned and is operated. The owners elects the BODs, who will be responsible

for monitoring and guiding management team such as supervisors (agents). In the case of the

green-lighting project, more of the authority was in the hand of the agents rather than pursuing

the something that maximizes value of the shareholder.

8

uses contractual monitoring and the bonding that is been bear on which structure is designed.

On the other side, it is been highlighted that this theory does not considers the

competence aspect and because of this even those managers who are not competent and are

incapable in carrying out the task are appointed. Agency theory does not call for those persons

who are been loyal towards the organization. Moreover, it is the theory that treats the mangers as

they are opportunistic, solely motivated with that of their self-interest. Thus, in accordance with

the agency theory it has been studied that there exist the divergence of the interest and the

purpose of the mangers and the shareholders, one is the person who expects for the separation of

an ownership and the control leads to the damaging effect over the performance of an entity.

This problem could be overcome by direct monitoring on the shareholders through the

concentrated ownership. Such use of the ownership helps in increasing the improvement in the

performance of an enterprise.

The agent under this theory has more of the information as compared to the principal, this

difference of knowledge is been called as the asymmetric information. It is also been studied by

the Bøe, Gulbrandsen and Sørebø, (2015), that the principal could not always ensure for the

performance of the agent to their best interest. This departure of the interest from principal to

agent is called as agency cost. Hence agency theory cause many problems that includes the

difference of interest, personal goals etc. Agency theory assess the cost incurred by reviewing

financial decisions in context of the risk, trade-off and the profitability in between the parties

interest. Principal bears particular costs for reducing possibility of agent in prioritizing the value

of its agent. For the equity holders, such cost are classified as the monitoring cost, residual cost

and the bonding cost.

Examples- Portfolio managers and the financial planners are considered as agents and are

having the responsibility towards their principal assets.

In the real life business situations, this problem occurs in respect of the ways in which the

company is been owned and is operated. The owners elects the BODs, who will be responsible

for monitoring and guiding management team such as supervisors (agents). In the case of the

green-lighting project, more of the authority was in the hand of the agents rather than pursuing

the something that maximizes value of the shareholder.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

“ Too Big To Fail” was another example of the agency problem. The idea behinds this business

project was that some organization are so critical and important to economy, that even if they do

anything as per their wish, the government will be helping in bailing out them. It is the situation

that creates the moral hazards, under which the agents will be having no incentive for doing the

right things as they are aware of the not get blamed at end if anything happens.

Market failure is also a critical component for the business and could resulted because of the

conflict of interest in the between principal and the agent. This occurs due to the misallocation in

the resources which leads to the distortion in market (Chang, Kang and Li, 2016). This in turn

creates the inefficiency in overall market. Market failure causes due to four reasons that includes

power abuse, externalities, sole buyer, externalities, information distribution and the public

goods. Mainly the market failures occurs when agent pursues self-interest instead of the

principals interest.

CONCLUSION

By summing up the above report it has been analysed that financial management is an

important aspect for each and every organization because it relates to optimum utilisation of the

resources in order to gain larger profits. It helps the firm in attaining growing success in the long

run and in meeting with the uncertainty occurs if any.

9

project was that some organization are so critical and important to economy, that even if they do

anything as per their wish, the government will be helping in bailing out them. It is the situation

that creates the moral hazards, under which the agents will be having no incentive for doing the

right things as they are aware of the not get blamed at end if anything happens.

Market failure is also a critical component for the business and could resulted because of the

conflict of interest in the between principal and the agent. This occurs due to the misallocation in

the resources which leads to the distortion in market (Chang, Kang and Li, 2016). This in turn

creates the inefficiency in overall market. Market failure causes due to four reasons that includes

power abuse, externalities, sole buyer, externalities, information distribution and the public

goods. Mainly the market failures occurs when agent pursues self-interest instead of the

principals interest.

CONCLUSION

By summing up the above report it has been analysed that financial management is an

important aspect for each and every organization because it relates to optimum utilisation of the

resources in order to gain larger profits. It helps the firm in attaining growing success in the long

run and in meeting with the uncertainty occurs if any.

9

REFERENCES

Books and Journals

Altman, E.I. and et.al., 2017. Financial distress prediction in an international context: A review

and empirical analysis of Altman's Z‐score model. Journal of International Financial

Management & Accounting. 28(2). pp.131-171.

Banks, G. C. and et.al., 2018. A meta‐analytic review of tipping compensation practices: An

agency theory perspective. Personnel Psychology. 71(3). pp.457-478.

Bendickson, J. and et.al., 2016. Agency theory: background and epistemology. Journal of

Management History. 22(4). pp.437-449.

Bøe, T., Gulbrandsen, B. and Sørebø, Ø., 2015. How to stimulate the continued use of ICT in

higher education: Integrating information systems continuance theory and agency

theory. Computers in Human Behavior. 50. pp.375-384.

Bosse, D. A. and Phillips, R. A., 2016. Agency theory and bounded self-interest. Academy of

Management Review. 41(2). pp.276-297.

Chang, K., Kang, E. and Li, Y., 2016. Effect of institutional ownership on dividends: An

agency-theory-based analysis. Journal of Business Research. 69(7). pp.2551-2559.

Chari, M. D. and et.al., 2019. Bowman's risk-return paradox: An agency theory

perspective. Journal of Business Research. 95. pp.357-375.

Choi, K.B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121. pp.355-372.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The

Accounting Review. 91(3). pp.859-881.

Gomez-Mejia, L. R., Patel, P. C. and Zellweger, T. M., 2018. In the horns of the dilemma:

Socioemotional wealth, financial wealth, and acquisitions in family firms. Journal of

Management,. 44(4). pp.1369-1397.

10

Books and Journals

Altman, E.I. and et.al., 2017. Financial distress prediction in an international context: A review

and empirical analysis of Altman's Z‐score model. Journal of International Financial

Management & Accounting. 28(2). pp.131-171.

Banks, G. C. and et.al., 2018. A meta‐analytic review of tipping compensation practices: An

agency theory perspective. Personnel Psychology. 71(3). pp.457-478.

Bendickson, J. and et.al., 2016. Agency theory: background and epistemology. Journal of

Management History. 22(4). pp.437-449.

Bøe, T., Gulbrandsen, B. and Sørebø, Ø., 2015. How to stimulate the continued use of ICT in

higher education: Integrating information systems continuance theory and agency

theory. Computers in Human Behavior. 50. pp.375-384.

Bosse, D. A. and Phillips, R. A., 2016. Agency theory and bounded self-interest. Academy of

Management Review. 41(2). pp.276-297.

Chang, K., Kang, E. and Li, Y., 2016. Effect of institutional ownership on dividends: An

agency-theory-based analysis. Journal of Business Research. 69(7). pp.2551-2559.

Chari, M. D. and et.al., 2019. Bowman's risk-return paradox: An agency theory

perspective. Journal of Business Research. 95. pp.357-375.

Choi, K.B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121. pp.355-372.

Edwards, A., Schwab, C. and Shevlin, T., 2015. Financial constraints and cash tax savings. The

Accounting Review. 91(3). pp.859-881.

Gomez-Mejia, L. R., Patel, P. C. and Zellweger, T. M., 2018. In the horns of the dilemma:

Socioemotional wealth, financial wealth, and acquisitions in family firms. Journal of

Management,. 44(4). pp.1369-1397.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.