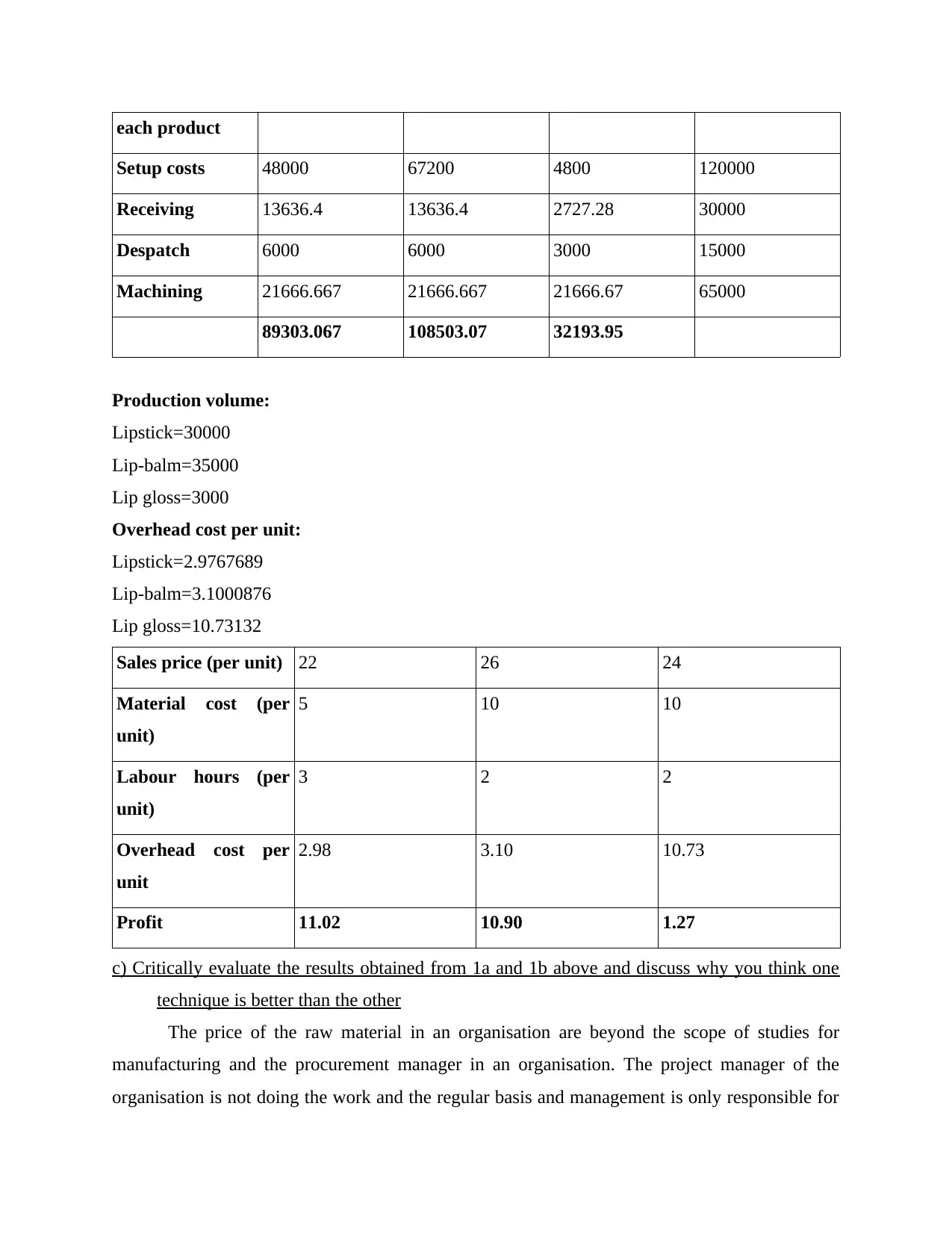

This document discusses various topics in financial management, including cost calculation, sensitivity analysis, and variances. It explores different techniques used in cost absorption and activity-based costing. It also evaluates the results obtained from different techniques and discusses the benefits and limitations of each. Additionally, it discusses how sensitivity analysis helps managers cope with uncertainties. Lastly, it critically examines the problems with the current system of calculating and reporting variances for assessing the performance of the production manager. The document concludes by discussing the limitations of zero-based budgeting and incremental budgeting in planning, coordination, and control.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)