Financial Markets and Institutions: Yield Curve Analysis Report

VerifiedAdded on 2023/04/21

|8

|2008

|450

Report

AI Summary

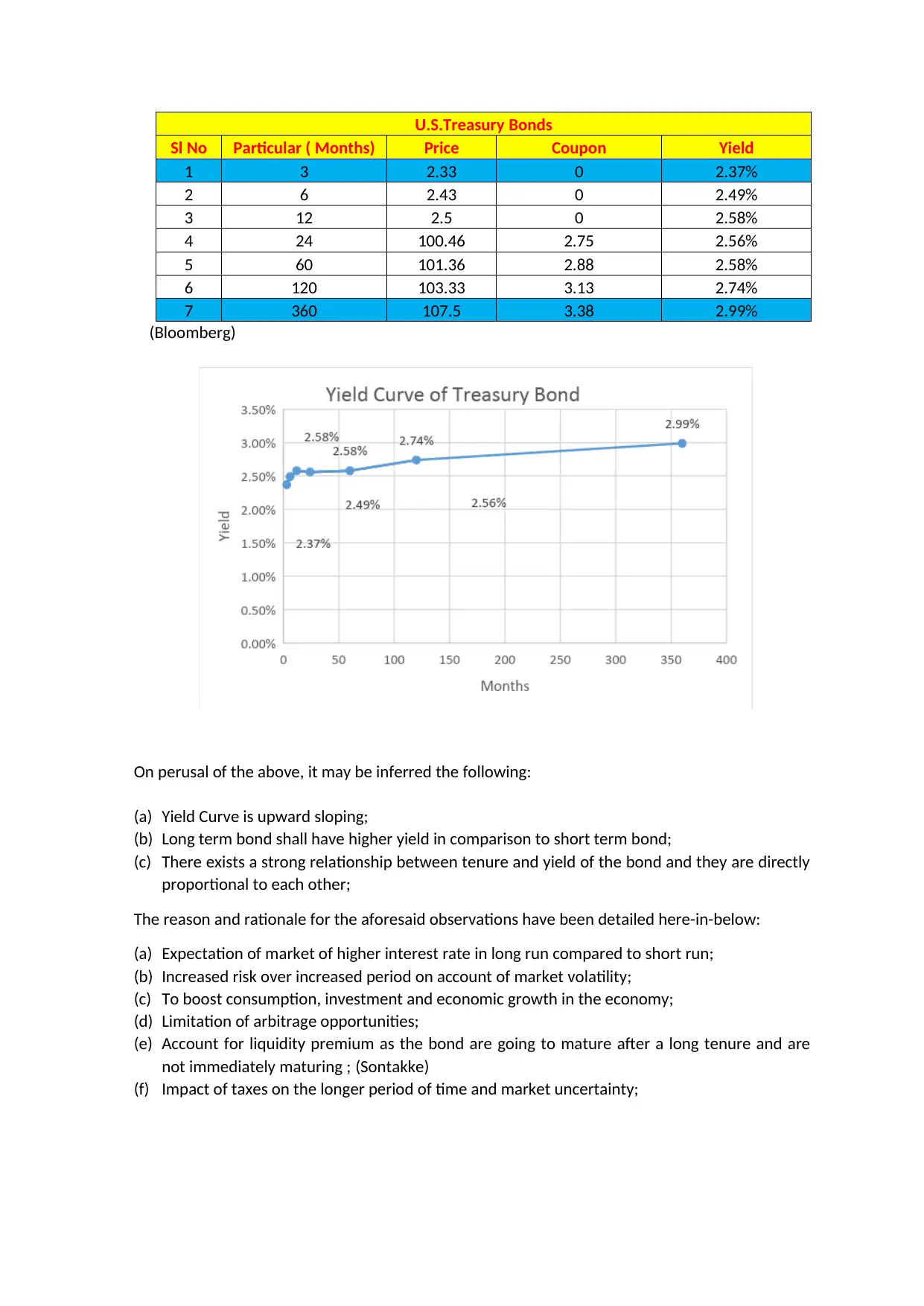

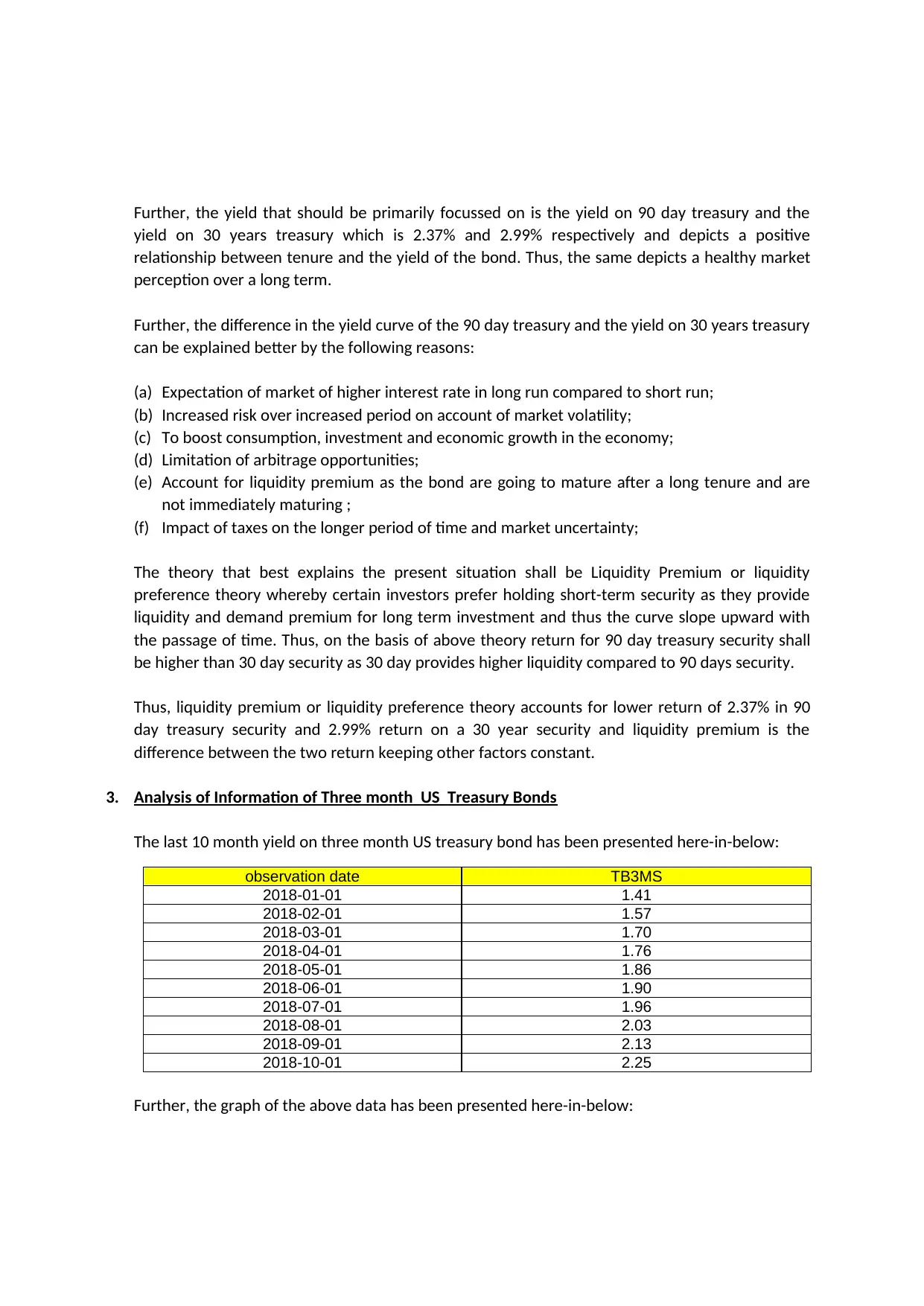

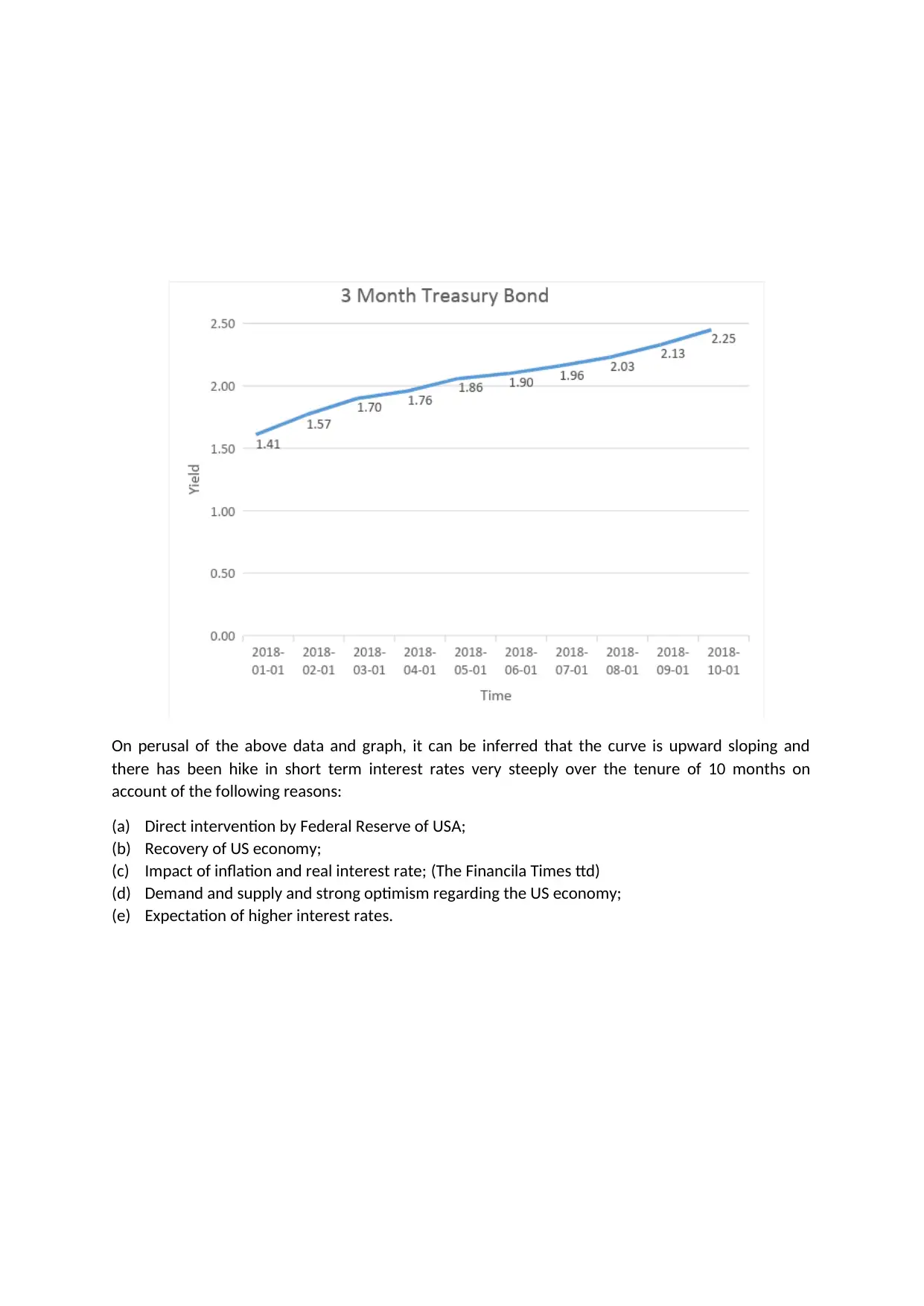

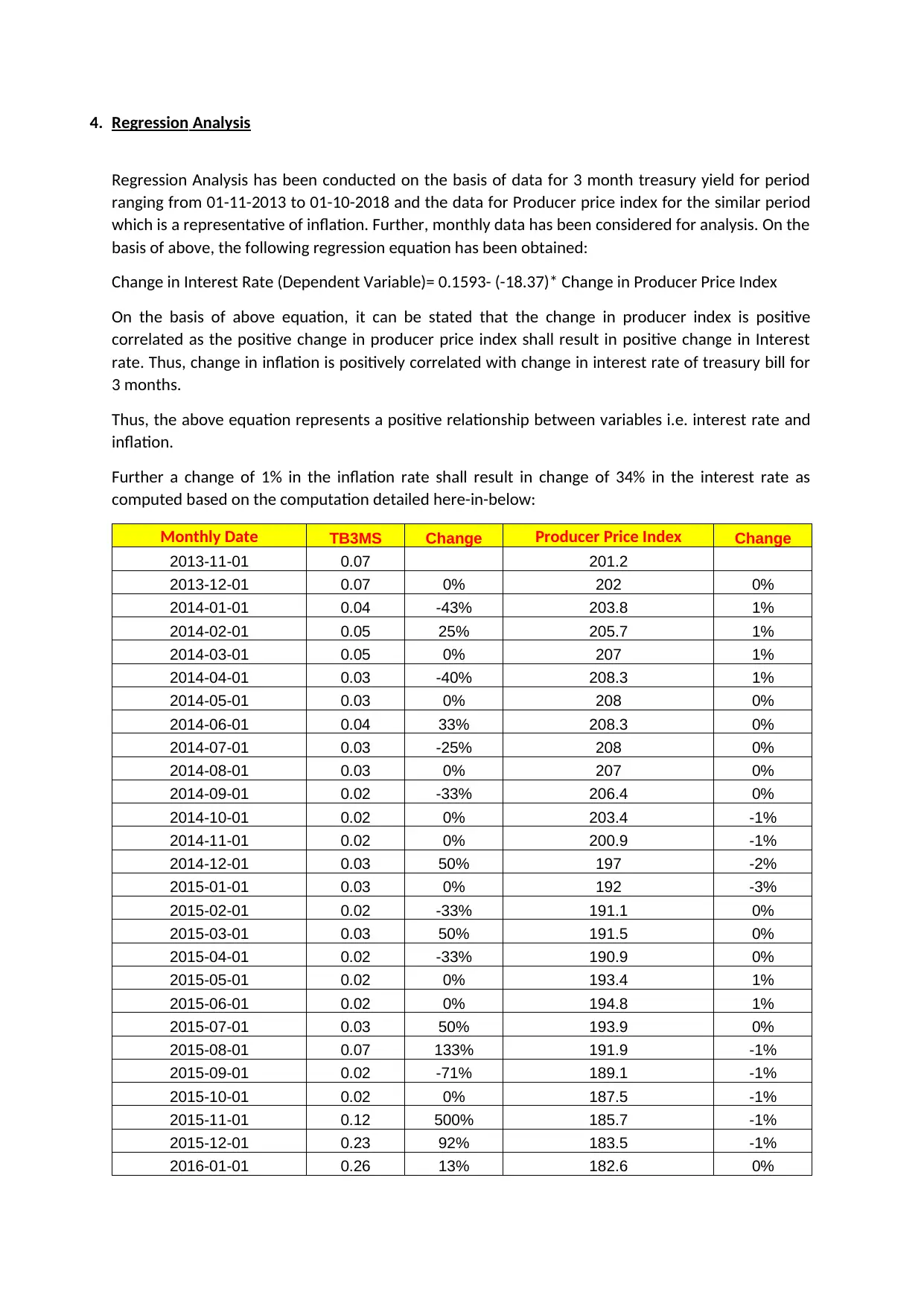

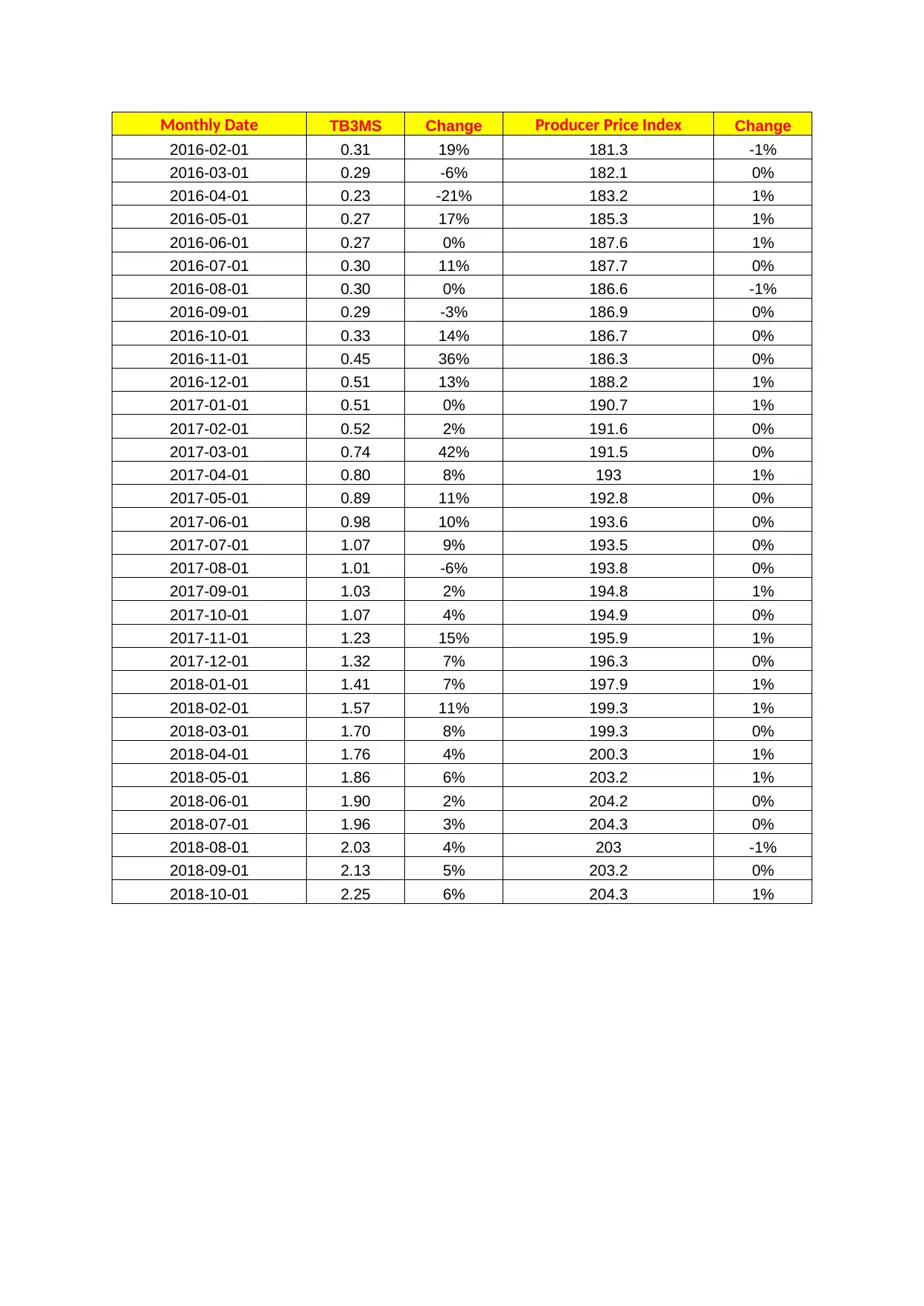

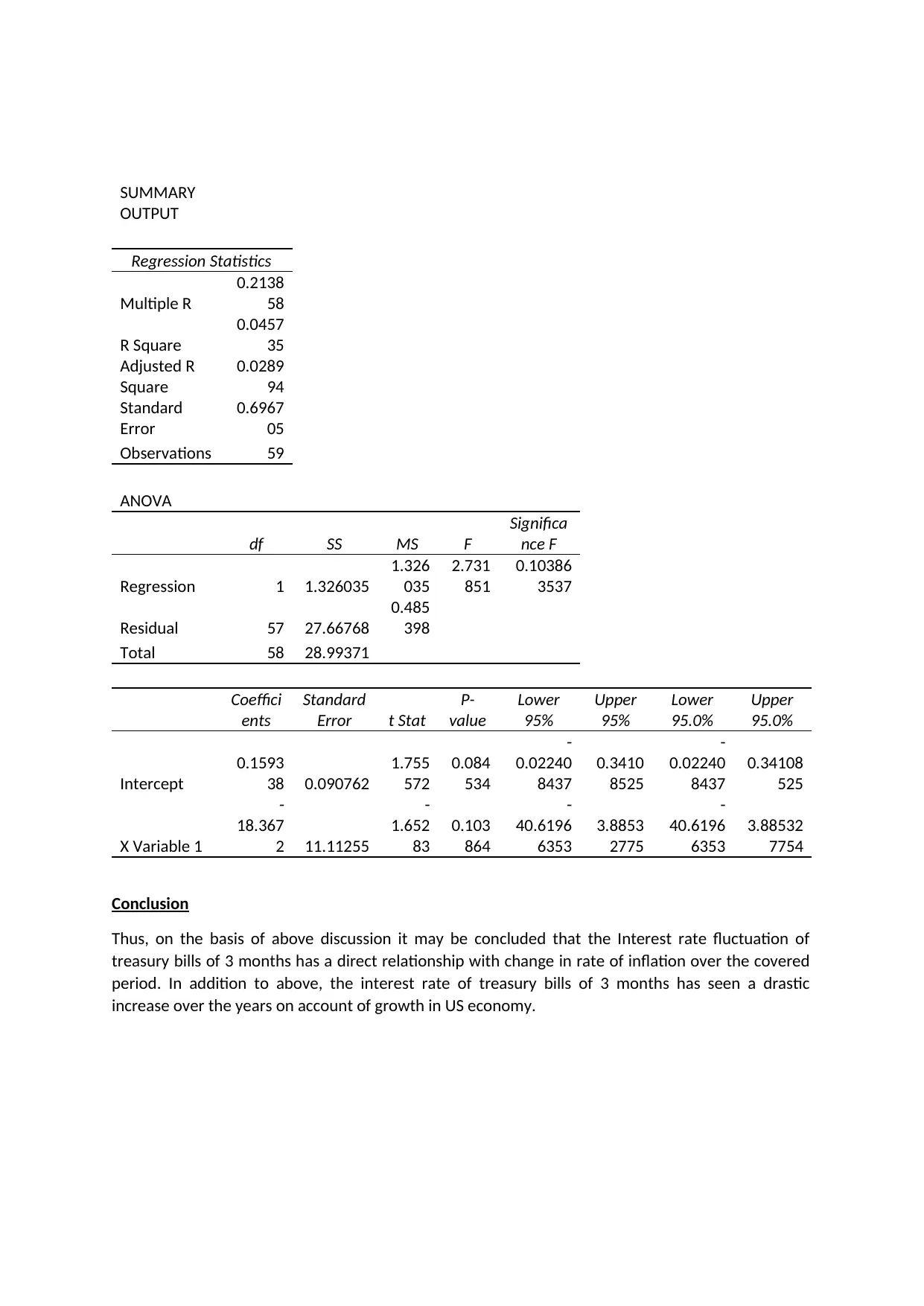

This report provides an in-depth analysis of the US Treasury bond market, focusing on the yield curve and its relationship with interest rates and inflation. The report begins by defining key terms in the bond market, such as face value, coupon, yield, and price. It then analyzes the yield curve of US Treasury bonds, considering bonds with maturities ranging from 3 months to 30 years. The analysis reveals an upward sloping yield curve, indicating that longer-term bonds offer higher yields than shorter-term bonds. The report explains this phenomenon by referencing market expectations of future interest rates, increased risk over longer periods, and the role of liquidity premium. The report also examines the recent trends in 3-month US Treasury bond yields, highlighting the reasons behind the observed changes. Furthermore, a regression analysis is conducted to determine the correlation between changes in interest rates and the producer price index, which serves as a proxy for inflation. The analysis reveals a positive correlation between inflation and interest rates. The report concludes by summarizing the key findings and offering insights into the dynamics of the financial markets. The analysis is supported by data from Bloomberg and other financial sources. It also discusses the liquidity preference theory to explain the difference in yields between short-term and long-term treasury securities.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.