Financial Market and Monitory Policy

VerifiedAdded on 2021/06/18

|16

|3531

|128

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL MARKET AND MONITORY POLICY

Financial market and monitory policy

Name of the student

Name of the university

Author Note

Financial market and monitory policy

Name of the student

Name of the university

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL MARKET AND MONITORY POLICY

Table of Contents

Answer 1:...................................................................................................................................2

Answer 2:...................................................................................................................................8

Answer 3:.................................................................................................................................10

References:...............................................................................................................................14

Table of Contents

Answer 1:...................................................................................................................................2

Answer 2:...................................................................................................................................8

Answer 3:.................................................................................................................................10

References:...............................................................................................................................14

2FINANCIAL MARKET AND MONITORY POLICY

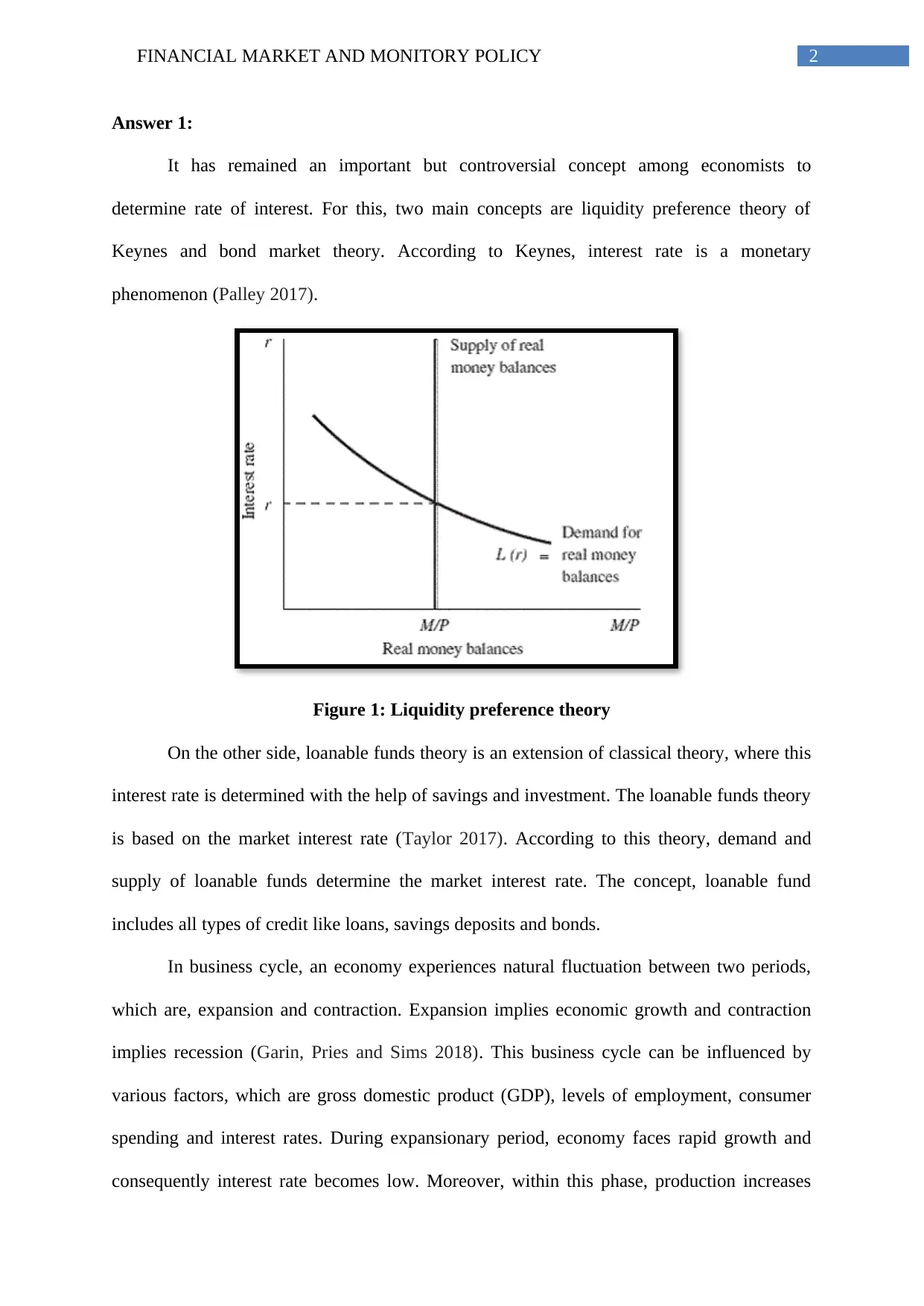

Answer 1:

It has remained an important but controversial concept among economists to

determine rate of interest. For this, two main concepts are liquidity preference theory of

Keynes and bond market theory. According to Keynes, interest rate is a monetary

phenomenon (Palley 2017).

Figure 1: Liquidity preference theory

On the other side, loanable funds theory is an extension of classical theory, where this

interest rate is determined with the help of savings and investment. The loanable funds theory

is based on the market interest rate (Taylor 2017). According to this theory, demand and

supply of loanable funds determine the market interest rate. The concept, loanable fund

includes all types of credit like loans, savings deposits and bonds.

In business cycle, an economy experiences natural fluctuation between two periods,

which are, expansion and contraction. Expansion implies economic growth and contraction

implies recession (Garin, Pries and Sims 2018). This business cycle can be influenced by

various factors, which are gross domestic product (GDP), levels of employment, consumer

spending and interest rates. During expansionary period, economy faces rapid growth and

consequently interest rate becomes low. Moreover, within this phase, production increases

Answer 1:

It has remained an important but controversial concept among economists to

determine rate of interest. For this, two main concepts are liquidity preference theory of

Keynes and bond market theory. According to Keynes, interest rate is a monetary

phenomenon (Palley 2017).

Figure 1: Liquidity preference theory

On the other side, loanable funds theory is an extension of classical theory, where this

interest rate is determined with the help of savings and investment. The loanable funds theory

is based on the market interest rate (Taylor 2017). According to this theory, demand and

supply of loanable funds determine the market interest rate. The concept, loanable fund

includes all types of credit like loans, savings deposits and bonds.

In business cycle, an economy experiences natural fluctuation between two periods,

which are, expansion and contraction. Expansion implies economic growth and contraction

implies recession (Garin, Pries and Sims 2018). This business cycle can be influenced by

various factors, which are gross domestic product (GDP), levels of employment, consumer

spending and interest rates. During expansionary period, economy faces rapid growth and

consequently interest rate becomes low. Moreover, within this phase, production increases

3FINANCIAL MARKET AND MONITORY POLICY

and inflationary pressure occurs within the concerned economy. On the contrary, during

contractionary period, economic growth decreases further.

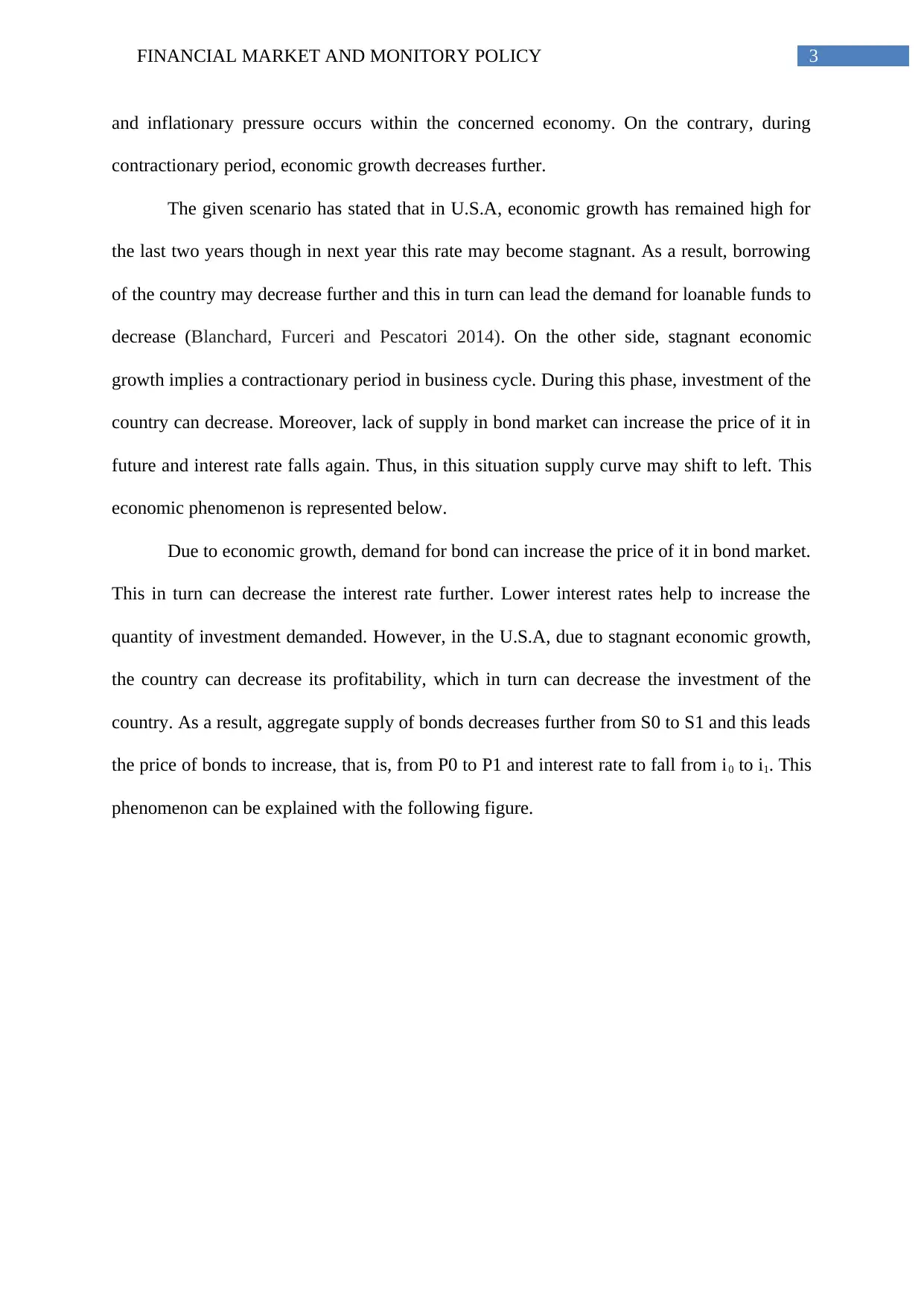

The given scenario has stated that in U.S.A, economic growth has remained high for

the last two years though in next year this rate may become stagnant. As a result, borrowing

of the country may decrease further and this in turn can lead the demand for loanable funds to

decrease (Blanchard, Furceri and Pescatori 2014). On the other side, stagnant economic

growth implies a contractionary period in business cycle. During this phase, investment of the

country can decrease. Moreover, lack of supply in bond market can increase the price of it in

future and interest rate falls again. Thus, in this situation supply curve may shift to left. This

economic phenomenon is represented below.

Due to economic growth, demand for bond can increase the price of it in bond market.

This in turn can decrease the interest rate further. Lower interest rates help to increase the

quantity of investment demanded. However, in the U.S.A, due to stagnant economic growth,

the country can decrease its profitability, which in turn can decrease the investment of the

country. As a result, aggregate supply of bonds decreases further from S0 to S1 and this leads

the price of bonds to increase, that is, from P0 to P1 and interest rate to fall from i0 to i1. This

phenomenon can be explained with the following figure.

and inflationary pressure occurs within the concerned economy. On the contrary, during

contractionary period, economic growth decreases further.

The given scenario has stated that in U.S.A, economic growth has remained high for

the last two years though in next year this rate may become stagnant. As a result, borrowing

of the country may decrease further and this in turn can lead the demand for loanable funds to

decrease (Blanchard, Furceri and Pescatori 2014). On the other side, stagnant economic

growth implies a contractionary period in business cycle. During this phase, investment of the

country can decrease. Moreover, lack of supply in bond market can increase the price of it in

future and interest rate falls again. Thus, in this situation supply curve may shift to left. This

economic phenomenon is represented below.

Due to economic growth, demand for bond can increase the price of it in bond market.

This in turn can decrease the interest rate further. Lower interest rates help to increase the

quantity of investment demanded. However, in the U.S.A, due to stagnant economic growth,

the country can decrease its profitability, which in turn can decrease the investment of the

country. As a result, aggregate supply of bonds decreases further from S0 to S1 and this leads

the price of bonds to increase, that is, from P0 to P1 and interest rate to fall from i0 to i1. This

phenomenon can be explained with the following figure.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL MARKET AND MONITORY POLICY

Price of bonds

Quantity of bonds

Interest rate (i)

Quantity of loanable

funds

S1

S0

DB

D0

D1

SL

P0

P1

i0

i1

Figure 2: Economic growth and impact in bond market

According to Keynesian theory of Liquidity preference, due to stagnant economic

growth, real GDP of the U.S.A can decrease and this in turn can reduce the number of real

transaction. Thus, people may not prefer to hold more cash as liquid for transaction purpose.

Hence, demand for cash decreases and this further can lead the interest rate to decrease.

Price of bonds

Quantity of bonds

Interest rate (i)

Quantity of loanable

funds

S1

S0

DB

D0

D1

SL

P0

P1

i0

i1

Figure 2: Economic growth and impact in bond market

According to Keynesian theory of Liquidity preference, due to stagnant economic

growth, real GDP of the U.S.A can decrease and this in turn can reduce the number of real

transaction. Thus, people may not prefer to hold more cash as liquid for transaction purpose.

Hence, demand for cash decreases and this further can lead the interest rate to decrease.

5FINANCIAL MARKET AND MONITORY POLICY

MD0

MD1

Ms by Fed

Interest rate (i)

Money (M1)

io

i1

Figure 3: Economic growth and impact in Keynesian Market

On the other side, inflation rate has significant influence on the demand for. In the

U.S.A, inflation has remained high more than 3% for the last few years and this rate may

remain same in coming year as well. Inflation rate and interest rate have close relation with

each other (Jelilov 2016). Higher interest rate directly affects lending and borrowing as it

makes servicing loans more costly (Baker, Bloom and Davis 2016). If people expect that

inflation rate of the country can increase further in future, then both savers and borrowers

may prefer to buy more bonds at present and this may lead savers to save less. This in turn

can force demand for bonds to decrease further and consequently supply of loanable funds

can decrease. On the other side, as borrowers need to borrow more money, it may increase

supply of bonds and demand for loanable funds to increase further. However, according to

given scenario, inflation rate has remained unchanged and consequently supply or demand

for loanable funds may remain unaffected and this further cannot influence interest rate of the

country.

MD0

MD1

Ms by Fed

Interest rate (i)

Money (M1)

io

i1

Figure 3: Economic growth and impact in Keynesian Market

On the other side, inflation rate has significant influence on the demand for. In the

U.S.A, inflation has remained high more than 3% for the last few years and this rate may

remain same in coming year as well. Inflation rate and interest rate have close relation with

each other (Jelilov 2016). Higher interest rate directly affects lending and borrowing as it

makes servicing loans more costly (Baker, Bloom and Davis 2016). If people expect that

inflation rate of the country can increase further in future, then both savers and borrowers

may prefer to buy more bonds at present and this may lead savers to save less. This in turn

can force demand for bonds to decrease further and consequently supply of loanable funds

can decrease. On the other side, as borrowers need to borrow more money, it may increase

supply of bonds and demand for loanable funds to increase further. However, according to

given scenario, inflation rate has remained unchanged and consequently supply or demand

for loanable funds may remain unaffected and this further cannot influence interest rate of the

country.

6FINANCIAL MARKET AND MONITORY POLICY

P0

P1

Price of bonds

Quantity of bonds

Interest rate (i)

Quantity of loanable funds

i0

i1

S0

S1

DB D0

SL

D1

On the other side, in Keynesian model, due to unchanged rate of inflation, consumers

and business organizations may remain unaffected regarding holding of money. Hence, at this

situation, demand for money can remain unchanged and this consequently cannot affect

interest rate anymore.

The Federal government, on the other side, is going to cut its spending to decrease

budget deficit. This implies that at present scenario, government expenditure is high compare

to its tax revenue. However, in future, the government can earn budget surplus and as a result,

it can repurchase its bonds from market. This further can reduce the supply of bonds and

consequently, price of it can increase further. Hence, increasing price can lead the interest

rate in market by lowering demand for bonds (Kelikume 2016). Thus, supply curve of

loanable funds in this situation can shift to the left.

Figure 4: Reduce in government expenditure and impact in bond market

P0

P1

Price of bonds

Quantity of bonds

Interest rate (i)

Quantity of loanable funds

i0

i1

S0

S1

DB D0

SL

D1

On the other side, in Keynesian model, due to unchanged rate of inflation, consumers

and business organizations may remain unaffected regarding holding of money. Hence, at this

situation, demand for money can remain unchanged and this consequently cannot affect

interest rate anymore.

The Federal government, on the other side, is going to cut its spending to decrease

budget deficit. This implies that at present scenario, government expenditure is high compare

to its tax revenue. However, in future, the government can earn budget surplus and as a result,

it can repurchase its bonds from market. This further can reduce the supply of bonds and

consequently, price of it can increase further. Hence, increasing price can lead the interest

rate in market by lowering demand for bonds (Kelikume 2016). Thus, supply curve of

loanable funds in this situation can shift to the left.

Figure 4: Reduce in government expenditure and impact in bond market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MARKET AND MONITORY POLICY

Interest rate

Loanable funds

O

DLF0

SLF0

DLF1

I0

I1

SLF1

In addition to this, the Fed is not going to affect its existing money supply of loanable

funds for next year. Thus, this decision cannot influence supply or demand for loanable funds

further (Ogbulu, Uruakpa and Umezinwa 2015). Under liquidity preference theory, increase

in money supply by Fed can lead the interest rate to decrease further while other factors may

remain unchanged. However, in this context, this cannot influence interest rate. Moreover,

savings also play an important role to influence supply of this fund. Biggest source for

demand and supply of bonds in market are savings of households and firms. This theory

considers savings are of two types, which are, ex-ante saving and a difference between

income of past period and consumption of present period. In both cases, savings are

considered as interest elastic (Assenza, Brock and Hommes 2017). However, the neoclassical

economists have stated that at a given level of income, savings can vary with interest rate as

well. If people of the U.S.A start to save more amount of liquid money through selling bonds,

then it can decrease the bond price in market and consequently interest can increase further.

However, in the given context, overall savings may remain stable, which in turn may not

influence the supply of loanable funds.

Figure 5: Demand and supply of loanable funds

Interest rate

Loanable funds

O

DLF0

SLF0

DLF1

I0

I1

SLF1

In addition to this, the Fed is not going to affect its existing money supply of loanable

funds for next year. Thus, this decision cannot influence supply or demand for loanable funds

further (Ogbulu, Uruakpa and Umezinwa 2015). Under liquidity preference theory, increase

in money supply by Fed can lead the interest rate to decrease further while other factors may

remain unchanged. However, in this context, this cannot influence interest rate. Moreover,

savings also play an important role to influence supply of this fund. Biggest source for

demand and supply of bonds in market are savings of households and firms. This theory

considers savings are of two types, which are, ex-ante saving and a difference between

income of past period and consumption of present period. In both cases, savings are

considered as interest elastic (Assenza, Brock and Hommes 2017). However, the neoclassical

economists have stated that at a given level of income, savings can vary with interest rate as

well. If people of the U.S.A start to save more amount of liquid money through selling bonds,

then it can decrease the bond price in market and consequently interest can increase further.

However, in the given context, overall savings may remain stable, which in turn may not

influence the supply of loanable funds.

Figure 5: Demand and supply of loanable funds

8FINANCIAL MARKET AND MONITORY POLICY

Hence, according to above discussion, it can be stated that interest rate is going to

decrease in future in the U.S.A. With the help of bond market and the concept of liquidity

preference theory, it is observed that due to stagnant growth of economy, the interest rate can

be decreased in the U.S.A in coming years. Moreover, reduction in government expenditure

can also influence interest rate to decrease further through considering bond market.

However, unchanged saving and inflation rate cannot influence the interest rate of this

concerned country in future. Thus, the entire interest rate can decrease further.

Answer 2:

If the loan is obtained based on 8% fixed interest rate, then the business organization

needs to repay the whole amount in future based on this rate. However, floating rate of

interest of 8% can be changed in future as the central bank may revise it each month during

the lending period, that is, one year. Hence, it can be difficult for a business entity to predict

that whether this floating interest rate is going to increase in future or not. This is because

floating interest rate depends on economic factors like inflation rate and growth rate of the

country.

As, floating interest rate varies each month, it is important to understand the process

with the help of which a bank can adjust its floating interest rate for loan. Adjustable-rate

mortgages (ARMs) have rates that can be adjusted with the help of present margin along with

a major mortgage index, like London Inter-bank Offered Rate (LIBOR), the monthly treasure

average (MTA) and the cost of funds index (COFI) (Strobl and Kablan 2017). For instance, a

person can take out an ARM based on LIBOR with a 2% margin while LIBOR is at 3% at the

time of rate adjustment of the mortgage, then the rate resets at 5%.

In this context, it can be beneficial to discuss about advantages and disadvantages of

these two types of interest rate.

Advantages regarding fixed interest rate:

Hence, according to above discussion, it can be stated that interest rate is going to

decrease in future in the U.S.A. With the help of bond market and the concept of liquidity

preference theory, it is observed that due to stagnant growth of economy, the interest rate can

be decreased in the U.S.A in coming years. Moreover, reduction in government expenditure

can also influence interest rate to decrease further through considering bond market.

However, unchanged saving and inflation rate cannot influence the interest rate of this

concerned country in future. Thus, the entire interest rate can decrease further.

Answer 2:

If the loan is obtained based on 8% fixed interest rate, then the business organization

needs to repay the whole amount in future based on this rate. However, floating rate of

interest of 8% can be changed in future as the central bank may revise it each month during

the lending period, that is, one year. Hence, it can be difficult for a business entity to predict

that whether this floating interest rate is going to increase in future or not. This is because

floating interest rate depends on economic factors like inflation rate and growth rate of the

country.

As, floating interest rate varies each month, it is important to understand the process

with the help of which a bank can adjust its floating interest rate for loan. Adjustable-rate

mortgages (ARMs) have rates that can be adjusted with the help of present margin along with

a major mortgage index, like London Inter-bank Offered Rate (LIBOR), the monthly treasure

average (MTA) and the cost of funds index (COFI) (Strobl and Kablan 2017). For instance, a

person can take out an ARM based on LIBOR with a 2% margin while LIBOR is at 3% at the

time of rate adjustment of the mortgage, then the rate resets at 5%.

In this context, it can be beneficial to discuss about advantages and disadvantages of

these two types of interest rate.

Advantages regarding fixed interest rate:

9FINANCIAL MARKET AND MONITORY POLICY

The chief benefit that can be obtained through choosing fixed interest rate is

predictability. In this situation, interest rate remains unchanged and consequently, payments

of businessperson may remain same. Hence, during short-term, it can be beneficial for the

business organization to take loan under fixed interest rate (Arrow 2017). Moreover, this

fixed interest rate also allows the company to estimate tax benefits that it can get after

deducting the loan interest for every year. However, for floating interest rate, it can be

difficult to measure tax benefit.

However, this fixed interest rate has some disadvantages, as well. For a small business

firm, a fixed interest rate may cause more costs for on a loan compare to the floating interest

rate during long period.

Figure 6: Fixed exchange rate

Advantages and disadvantages of floating interest rate:

This floating interest rate can be lower compare to fixed interest rate and this in turn

can help a business organization to take more loans and to bear less cost at the time of

repayment. Moreover, with the help of market fluctuation, a business entity can earn

advantage at the time of repayment (Yao 2015). However, on the other side, it is very

difficult for the business organization to predict about the fluctuation of this floating interest

The chief benefit that can be obtained through choosing fixed interest rate is

predictability. In this situation, interest rate remains unchanged and consequently, payments

of businessperson may remain same. Hence, during short-term, it can be beneficial for the

business organization to take loan under fixed interest rate (Arrow 2017). Moreover, this

fixed interest rate also allows the company to estimate tax benefits that it can get after

deducting the loan interest for every year. However, for floating interest rate, it can be

difficult to measure tax benefit.

However, this fixed interest rate has some disadvantages, as well. For a small business

firm, a fixed interest rate may cause more costs for on a loan compare to the floating interest

rate during long period.

Figure 6: Fixed exchange rate

Advantages and disadvantages of floating interest rate:

This floating interest rate can be lower compare to fixed interest rate and this in turn

can help a business organization to take more loans and to bear less cost at the time of

repayment. Moreover, with the help of market fluctuation, a business entity can earn

advantage at the time of repayment (Yao 2015). However, on the other side, it is very

difficult for the business organization to predict about the fluctuation of this floating interest

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL MARKET AND MONITORY POLICY

rate. Hence, due to higher floating rate, the business entity can experience market failure as

well.

However, in the given scenario, the business organization is going to take loan for one

year and from the before discussion it is seen that interest rate of the U.S.A is going to

decrease in future. Hence, with the help of this outcome, it can be said that the business

organization can take loan under floating exchange rate.

Answer 3:

Movement of money from one country’s financial institution to other country is

known as capital flows. The chief reason behind capital inflows or capital outflows consists

with movement of inflation, real interest rate and national income. Through assuming foreign

exchange rate as stable, the mentioned situation can help the U.S individuals to transfer their

savings from financial institutions of their domestic country to financial institutions of the

U.K for earning higher rate of interest.

Figure 7: Interest rate at loanable funds

rate. Hence, due to higher floating rate, the business entity can experience market failure as

well.

However, in the given scenario, the business organization is going to take loan for one

year and from the before discussion it is seen that interest rate of the U.S.A is going to

decrease in future. Hence, with the help of this outcome, it can be said that the business

organization can take loan under floating exchange rate.

Answer 3:

Movement of money from one country’s financial institution to other country is

known as capital flows. The chief reason behind capital inflows or capital outflows consists

with movement of inflation, real interest rate and national income. Through assuming foreign

exchange rate as stable, the mentioned situation can help the U.S individuals to transfer their

savings from financial institutions of their domestic country to financial institutions of the

U.K for earning higher rate of interest.

Figure 7: Interest rate at loanable funds

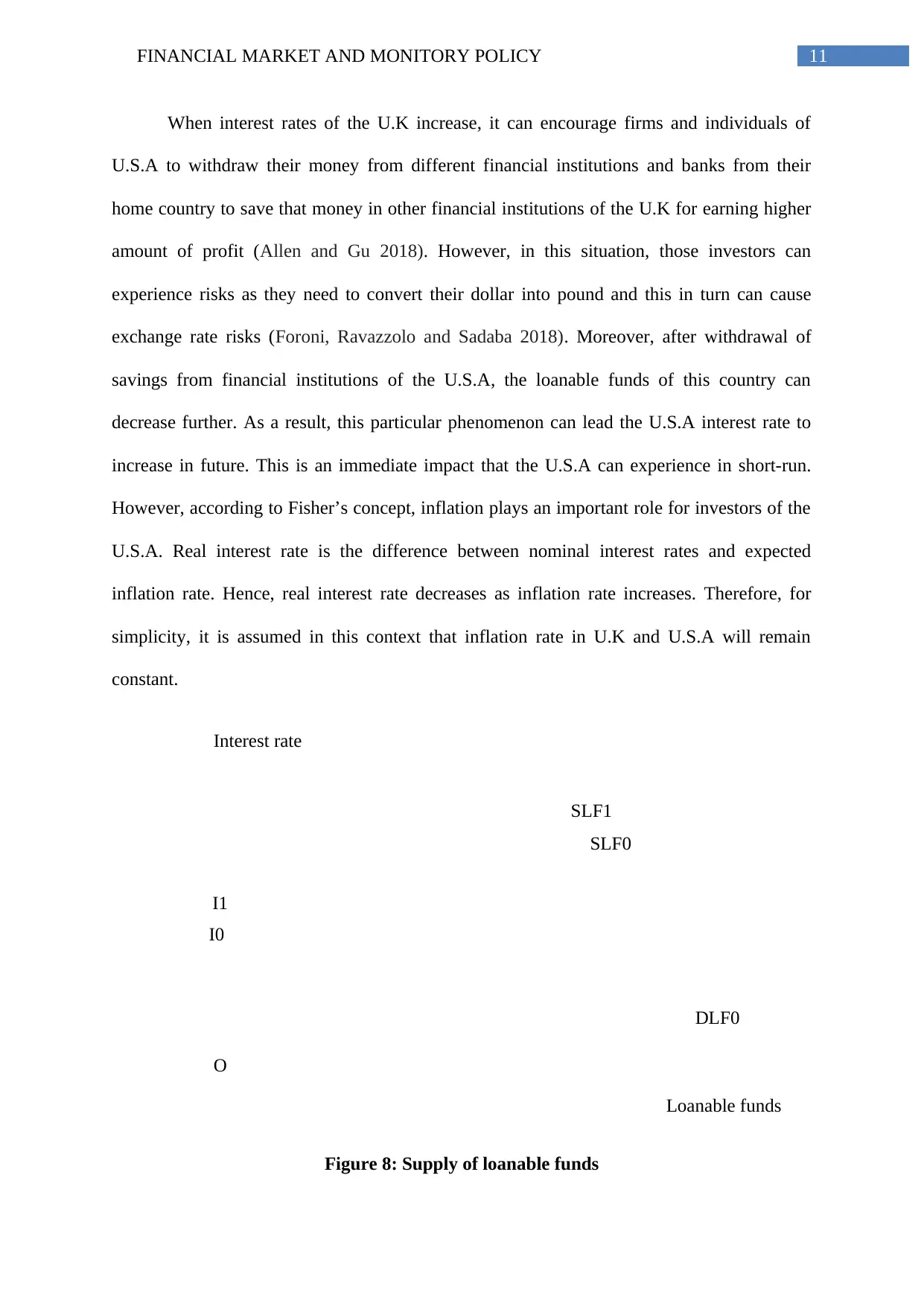

11FINANCIAL MARKET AND MONITORY POLICY

Interest rate

Loanable funds

O

DLF0

SLF0

I0

I1

SLF1

When interest rates of the U.K increase, it can encourage firms and individuals of

U.S.A to withdraw their money from different financial institutions and banks from their

home country to save that money in other financial institutions of the U.K for earning higher

amount of profit (Allen and Gu 2018). However, in this situation, those investors can

experience risks as they need to convert their dollar into pound and this in turn can cause

exchange rate risks (Foroni, Ravazzolo and Sadaba 2018). Moreover, after withdrawal of

savings from financial institutions of the U.S.A, the loanable funds of this country can

decrease further. As a result, this particular phenomenon can lead the U.S.A interest rate to

increase in future. This is an immediate impact that the U.S.A can experience in short-run.

However, according to Fisher’s concept, inflation plays an important role for investors of the

U.S.A. Real interest rate is the difference between nominal interest rates and expected

inflation rate. Hence, real interest rate decreases as inflation rate increases. Therefore, for

simplicity, it is assumed in this context that inflation rate in U.K and U.S.A will remain

constant.

Figure 8: Supply of loanable funds

Interest rate

Loanable funds

O

DLF0

SLF0

I0

I1

SLF1

When interest rates of the U.K increase, it can encourage firms and individuals of

U.S.A to withdraw their money from different financial institutions and banks from their

home country to save that money in other financial institutions of the U.K for earning higher

amount of profit (Allen and Gu 2018). However, in this situation, those investors can

experience risks as they need to convert their dollar into pound and this in turn can cause

exchange rate risks (Foroni, Ravazzolo and Sadaba 2018). Moreover, after withdrawal of

savings from financial institutions of the U.S.A, the loanable funds of this country can

decrease further. As a result, this particular phenomenon can lead the U.S.A interest rate to

increase in future. This is an immediate impact that the U.S.A can experience in short-run.

However, according to Fisher’s concept, inflation plays an important role for investors of the

U.S.A. Real interest rate is the difference between nominal interest rates and expected

inflation rate. Hence, real interest rate decreases as inflation rate increases. Therefore, for

simplicity, it is assumed in this context that inflation rate in U.K and U.S.A will remain

constant.

Figure 8: Supply of loanable funds

12FINANCIAL MARKET AND MONITORY POLICY

In this context, it is required to describe the relationship between a country’s real

interest rates on its exchange rates. Remaining other factors at same level, higher interest rate

of U.K can increase the value of its pound more compare to that for the U.S.A dollar as the

U.S.A offers low rate of interest and consequently exchange rate can increase (Tretvoll

2018). However, only interest rate cannot influence the exchange rate between two countries.

As interest rates of the U.K has increased above 2% points above the U.S interest rates, the

country can attract U.S investors to invest more by increasing the demand for and value of

pound.

This market can be described with the concept of arbitrage, which means buying at

low prices and selling at comparatively higher prices to earn profit (Gloukhovtsev, Schouten

and Mattila 2018). If such opportunity within a market exists, then this market is considered

as out of equilibrium.

Arbitrage and interest rate has a close relation and this can be divided into two parts,

which are, covered interest rate parity condition (CIP) and uncovered interest rate parity

condition (UIP). For each investor, an important question occurs that in which currency they

need to hold their liquid cash balance (Ardoin and Rodriguez 2017). For example, the

concerned person can deposit the cash in U.K bank for comparatively 2% more interest rate

or he can keep this money in the bank if U.S.A with lower interest rate. The chief problem of

this trader is exchange rate risk. In the U.S.A, the banks will return money in the form of

USD to this concerned person. Hence, through depositing dollar the person can get return

money in same currency and in this context, no risks regarding exchange rate exists. on the

other side, if the person deposits his money in the U.K bank, then he will receive money in

the form of U.K pound. However, in future it is impossible to predict that what the £/$ will

be. Hence, at this moment, there are two options for this investor and he can take any one of

In this context, it is required to describe the relationship between a country’s real

interest rates on its exchange rates. Remaining other factors at same level, higher interest rate

of U.K can increase the value of its pound more compare to that for the U.S.A dollar as the

U.S.A offers low rate of interest and consequently exchange rate can increase (Tretvoll

2018). However, only interest rate cannot influence the exchange rate between two countries.

As interest rates of the U.K has increased above 2% points above the U.S interest rates, the

country can attract U.S investors to invest more by increasing the demand for and value of

pound.

This market can be described with the concept of arbitrage, which means buying at

low prices and selling at comparatively higher prices to earn profit (Gloukhovtsev, Schouten

and Mattila 2018). If such opportunity within a market exists, then this market is considered

as out of equilibrium.

Arbitrage and interest rate has a close relation and this can be divided into two parts,

which are, covered interest rate parity condition (CIP) and uncovered interest rate parity

condition (UIP). For each investor, an important question occurs that in which currency they

need to hold their liquid cash balance (Ardoin and Rodriguez 2017). For example, the

concerned person can deposit the cash in U.K bank for comparatively 2% more interest rate

or he can keep this money in the bank if U.S.A with lower interest rate. The chief problem of

this trader is exchange rate risk. In the U.S.A, the banks will return money in the form of

USD to this concerned person. Hence, through depositing dollar the person can get return

money in same currency and in this context, no risks regarding exchange rate exists. on the

other side, if the person deposits his money in the U.K bank, then he will receive money in

the form of U.K pound. However, in future it is impossible to predict that what the £/$ will

be. Hence, at this moment, there are two options for this investor and he can take any one of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL MARKET AND MONITORY POLICY

them. The first option is hedging and the second one is uncovered interest rate parity.

However, it is beneficial for investors to hedge.

In long-run, decreasing money supply leads the loanable funds of the U.S.A to

decrease further and consequently this phenomenon forces the interest rate of this country to

increase further. However, at the same time, stagnant economic growth of next year can force

this rate of interest to decline. Moreover, budget deficit of this country can influence this

outcome further. Hence, after the entire impacts, interest rate of the U.S.A can decrease

further.

them. The first option is hedging and the second one is uncovered interest rate parity.

However, it is beneficial for investors to hedge.

In long-run, decreasing money supply leads the loanable funds of the U.S.A to

decrease further and consequently this phenomenon forces the interest rate of this country to

increase further. However, at the same time, stagnant economic growth of next year can force

this rate of interest to decline. Moreover, budget deficit of this country can influence this

outcome further. Hence, after the entire impacts, interest rate of the U.S.A can decrease

further.

14FINANCIAL MARKET AND MONITORY POLICY

References:

Allen, F. and Gu, X., 2018. The interplay between regulations and financial stability. Journal

of Financial Services Research, pp.1-16.

Ardoin, E. and Rodriguez, A., 2017. NEGATIVE INTEREST RATES AND A POSSIBLE

RIFT IN INTEREST RATE PARITY AND ARBITRAGE. International Journal of

Business, Accounting, & Finance, 11(2).

Arrow, K.J., 2017. Optimal capital policy with irreversible investment. In Value, capital and

growth (pp. 1-20). Routledge.

Assenza, T., Brock, W.A. and Hommes, C.H., 2017. Animal spirits, heterogeneous

expectations, and the amplification and duration of crises. Economic Inquiry, 55(1), pp.542-

564.

Baker, S.R., Bloom, N. and Davis, S.J., 2016. Measuring economic policy uncertainty. The

Quarterly Journal of Economics, 131(4), pp.1593-1636.

Blanchard, O.J., Furceri, D. and Pescatori, A., 2014. A prolonged period of low real interest

rates?. Secular stagnation: facts, causes and cures, p.101.

Foroni, C., Ravazzolo, F. and Sadaba, B., 2018. Assessing the predictive ability of sovereign

default risk on exchange rate returns. Journal of International Money and Finance, 81,

pp.242-264.

Garin, J., Pries, M.J. and Sims, E.R., 2018. The relative importance of aggregate and sectoral

shocks and the changing nature of economic fluctuations. American Economic Journal:

Macroeconomics, 10(1), pp.119-48.

Gloukhovtsev, A., Schouten, J.W. and Mattila, P., 2018. Toward a General Theory of

Regulatory Arbitrage: A Marketing Systems Perspective. Journal of Public Policy &

Marketing, 37(1), pp.142-151.

References:

Allen, F. and Gu, X., 2018. The interplay between regulations and financial stability. Journal

of Financial Services Research, pp.1-16.

Ardoin, E. and Rodriguez, A., 2017. NEGATIVE INTEREST RATES AND A POSSIBLE

RIFT IN INTEREST RATE PARITY AND ARBITRAGE. International Journal of

Business, Accounting, & Finance, 11(2).

Arrow, K.J., 2017. Optimal capital policy with irreversible investment. In Value, capital and

growth (pp. 1-20). Routledge.

Assenza, T., Brock, W.A. and Hommes, C.H., 2017. Animal spirits, heterogeneous

expectations, and the amplification and duration of crises. Economic Inquiry, 55(1), pp.542-

564.

Baker, S.R., Bloom, N. and Davis, S.J., 2016. Measuring economic policy uncertainty. The

Quarterly Journal of Economics, 131(4), pp.1593-1636.

Blanchard, O.J., Furceri, D. and Pescatori, A., 2014. A prolonged period of low real interest

rates?. Secular stagnation: facts, causes and cures, p.101.

Foroni, C., Ravazzolo, F. and Sadaba, B., 2018. Assessing the predictive ability of sovereign

default risk on exchange rate returns. Journal of International Money and Finance, 81,

pp.242-264.

Garin, J., Pries, M.J. and Sims, E.R., 2018. The relative importance of aggregate and sectoral

shocks and the changing nature of economic fluctuations. American Economic Journal:

Macroeconomics, 10(1), pp.119-48.

Gloukhovtsev, A., Schouten, J.W. and Mattila, P., 2018. Toward a General Theory of

Regulatory Arbitrage: A Marketing Systems Perspective. Journal of Public Policy &

Marketing, 37(1), pp.142-151.

15FINANCIAL MARKET AND MONITORY POLICY

Jelilov, G., 2016. The impact of interest rate on economic growth example of

Nigeria. African Journal of Social Sciences, 6(2), pp.51-64.

Kelikume, I., 2016. The effect of budget deficit on interest rates in the countries of sub-

Saharan Africa: A panel VAR approach. The Journal of Developing Areas, 50(6), pp.105-

120.

Matete, J.K., Ndede, F.S. and Ambrose, J., 2014. Factors affecting pricing of loanable funds

by commercial banks in Kenya. International Journal of Business and Social Science, 5(7).

Ogbulu, O.M., Uruakpa, P.C. and Umezinwa, C.L., 2015. Empirical Investigation of the

Impact of Deposit Rates on Fund Mobilization by Deposit Money Banks in Nigeria. Journal

of Finance, 3(1), pp.77-89.

Palley, T., 2017. The General Theory at 80: Reflections on the history and enduring relevance

of Keynes’ economics. Investigación económica, 76(301), pp.87-101.

Taylor, L., 2017. The “Natural” Interest Rate and Secular Stagnation: Loanable Funds Macro

Models Don't Fit Today’s Institutions or Data. Challenge, 60(1), pp.27-39.

Tretvoll, H., 2018. Real exchange rate variability in a two-country business cycle

model. Review of Economic Dynamics, 27, pp.123-145.

Yao, K., 2015. Uncertain contour process and its application in stock model with floating

interest rate. Fuzzy Optimization and Decision Making, 14(4), pp.399-424.

Strobl, E. and Kablan, S., 2017. How do natural disasters impact the exchange rate: an

investigation through small island developing states (SIDS)?. Economics Bulletin, 37(3),

pp.2274-2281.

Jelilov, G., 2016. The impact of interest rate on economic growth example of

Nigeria. African Journal of Social Sciences, 6(2), pp.51-64.

Kelikume, I., 2016. The effect of budget deficit on interest rates in the countries of sub-

Saharan Africa: A panel VAR approach. The Journal of Developing Areas, 50(6), pp.105-

120.

Matete, J.K., Ndede, F.S. and Ambrose, J., 2014. Factors affecting pricing of loanable funds

by commercial banks in Kenya. International Journal of Business and Social Science, 5(7).

Ogbulu, O.M., Uruakpa, P.C. and Umezinwa, C.L., 2015. Empirical Investigation of the

Impact of Deposit Rates on Fund Mobilization by Deposit Money Banks in Nigeria. Journal

of Finance, 3(1), pp.77-89.

Palley, T., 2017. The General Theory at 80: Reflections on the history and enduring relevance

of Keynes’ economics. Investigación económica, 76(301), pp.87-101.

Taylor, L., 2017. The “Natural” Interest Rate and Secular Stagnation: Loanable Funds Macro

Models Don't Fit Today’s Institutions or Data. Challenge, 60(1), pp.27-39.

Tretvoll, H., 2018. Real exchange rate variability in a two-country business cycle

model. Review of Economic Dynamics, 27, pp.123-145.

Yao, K., 2015. Uncertain contour process and its application in stock model with floating

interest rate. Fuzzy Optimization and Decision Making, 14(4), pp.399-424.

Strobl, E. and Kablan, S., 2017. How do natural disasters impact the exchange rate: an

investigation through small island developing states (SIDS)?. Economics Bulletin, 37(3),

pp.2274-2281.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.