Solution to Homework on Fixed Income Securities & Derivatives Pricing

VerifiedAdded on 2024/04/29

|14

|2646

|436

Homework Assignment

AI Summary

This document presents a detailed solution to a homework assignment focused on fixed income securities and derivatives pricing. The solution covers various aspects, including constructing interest rate trees using the BDT model, valuing callable bonds, and applying Monte Carlo simulations for pricing securities. Specific exercises address topics such as calculating zero-coupon bond prices, determining option values in callable bonds, and analyzing mortgage-backed securities. The document also compares results obtained through risk-neutral pricing and Monte Carlo simulation methods, highlighting the accuracy and convergence of these approaches. Additionally, it includes calculations for bond duration and convexity, as well as the derivation of implied interest rates from bond prices and forward rate agreements. This comprehensive solution provides valuable insights into the practical application of fixed income and derivatives pricing models.

Exercise 1

Part 1

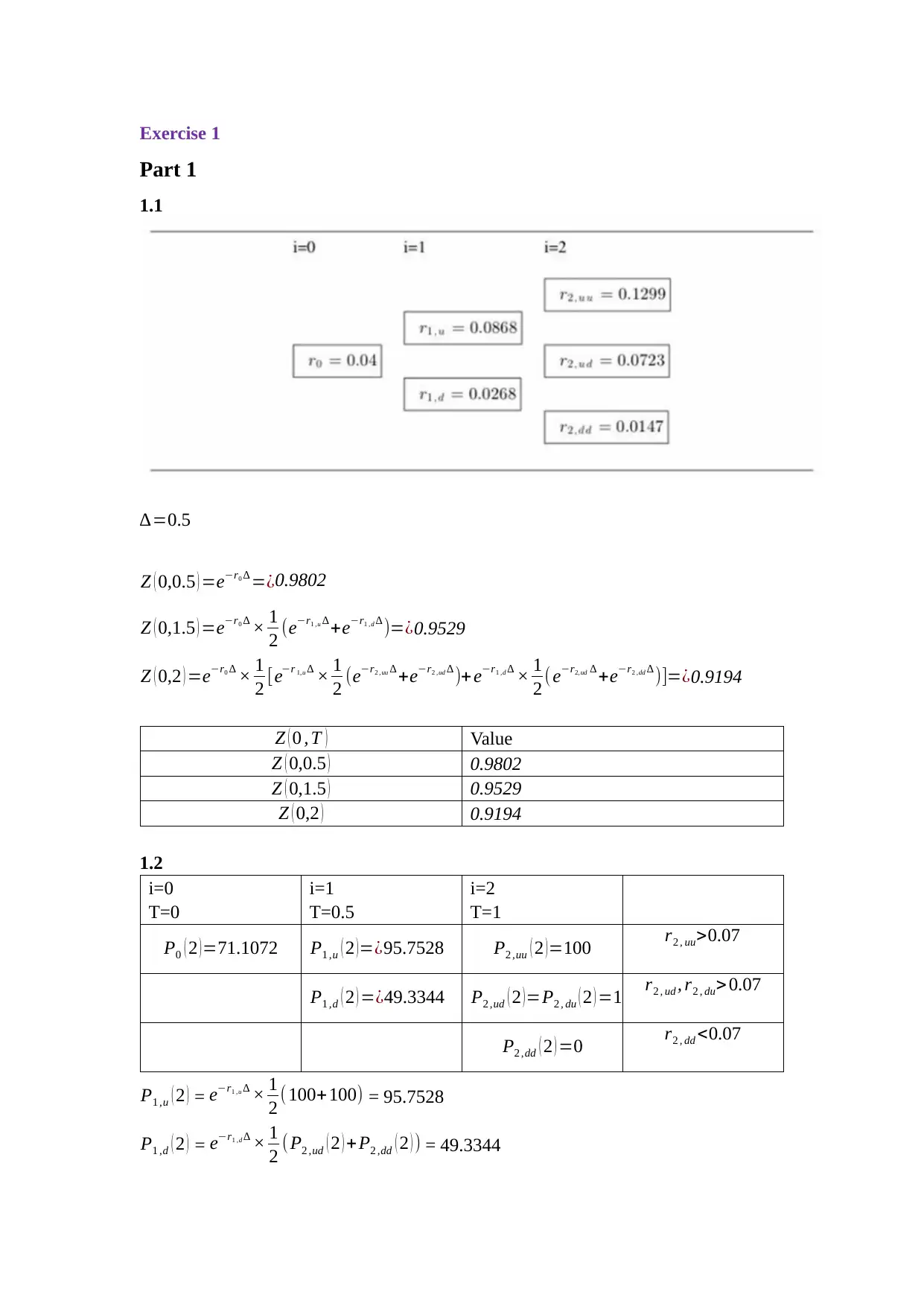

1.1

∆=0.5

Z ( 0,0.5 ) =e−r0 ∆ =¿0.9802

Z ( 0,1.5 ) =e−r0 ∆ × 1

2 (e−r1 ,u ∆ +e−r1 ,d ∆ )=¿0.9529

Z ( 0,2 ) =e−r0 ∆ × 1

2 [e−r 1,u ∆ × 1

2 (e−r2 ,uu ∆ +e−r2 ,ud ∆ )+e−r1 ,d ∆ × 1

2 (e−r2,ud ∆ +e−r2 ,dd ∆ )]=¿0.9194

Z ( 0 , T ) Value

Z ( 0,0.5 ) 0.9802

Z ( 0,1.5 ) 0.9529

Z ( 0,2 ) 0.9194

1.2

i=0 i=1 i=2

T=0 T=0.5 T=1

P0 ( 2 )=71.1072 P1 ,u ( 2 )=¿95.7528 P2 ,uu ( 2 )=100 r2 , uu>0.07

P1 ,d ( 2 ) =¿49.3344 P2 ,ud ( 2 ) =P2 , du ( 2 ) =100 r2 , ud , r2 , du> 0.07

P2 ,dd ( 2 ) =0 r2 , dd <0.07

P1 ,u ( 2 ) = e−r1 ,u ∆ × 1

2 (100+100) = 95.7528

P1 ,d ( 2 ) = e−r1 ,d ∆ × 1

2 (P2 ,ud ( 2 ) + P2 ,dd ( 2 ) ) = 49.3344

Part 1

1.1

∆=0.5

Z ( 0,0.5 ) =e−r0 ∆ =¿0.9802

Z ( 0,1.5 ) =e−r0 ∆ × 1

2 (e−r1 ,u ∆ +e−r1 ,d ∆ )=¿0.9529

Z ( 0,2 ) =e−r0 ∆ × 1

2 [e−r 1,u ∆ × 1

2 (e−r2 ,uu ∆ +e−r2 ,ud ∆ )+e−r1 ,d ∆ × 1

2 (e−r2,ud ∆ +e−r2 ,dd ∆ )]=¿0.9194

Z ( 0 , T ) Value

Z ( 0,0.5 ) 0.9802

Z ( 0,1.5 ) 0.9529

Z ( 0,2 ) 0.9194

1.2

i=0 i=1 i=2

T=0 T=0.5 T=1

P0 ( 2 )=71.1072 P1 ,u ( 2 )=¿95.7528 P2 ,uu ( 2 )=100 r2 , uu>0.07

P1 ,d ( 2 ) =¿49.3344 P2 ,ud ( 2 ) =P2 , du ( 2 ) =100 r2 , ud , r2 , du> 0.07

P2 ,dd ( 2 ) =0 r2 , dd <0.07

P1 ,u ( 2 ) = e−r1 ,u ∆ × 1

2 (100+100) = 95.7528

P1 ,d ( 2 ) = e−r1 ,d ∆ × 1

2 (P2 ,ud ( 2 ) + P2 ,dd ( 2 ) ) = 49.3344

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P0 ( 2 ) = e−r0 ∆ × 1

2 ( P1 ,u ( 2 ) +P1, d ( 2 ) ) =71.1072

1.3

Cash Flow Tree

i=0 i=1 i=2

T=0 T=0.5 T=1

C F0 (1) = 0

r2 (0)= 2(er0 ∆-1) =

0.0404

C F1 ,u (2)=1.9356

r1

(1,u) = 2(

er1 , u ∆-1)

= 0.0887

r2(2,uu) = 0.1342

C F2 ,uu (3)=4.2106

C F1 ,d ( 2)=0

r1

(1,d) = 2(er1 ,d ∆-1)

= 0.0270

C F2 ,ud (3)=1.1811

r2(2,ud) = 0.0736

C F2 ,dd (3)=0

r2(2,dd) = 0.0148

∆=0.5

N = 100

rk = 5%

r2

(2,uu) = 2(

er2 , uu ∆-1) = 0.1342

C F2 ,uu=100 ×0.5 × max ( 0.1342−0.05,0 ) =4.2106

V 2 ,uu=e−r2,uu ∆ ×C F2 , uu

= 3.9458

r2

(2,ud) = 2(er2 ,ud ∆-1) = 0.0736

C F2 ,ud=100 × 0.5 ×max ( 0.0736−0.05,0 ) =1.1811

V 2 ,ud =e−r2 ,ud ∆ ×C F2 ,ud

= 1.1392

r2

(2,dd) = 2(er2 ,dd ∆-1) = 0.0148

C F2 ,dd =100× 0.5 ×max ( 0.0148−0.05,0 ) =0

V 2 , dd=e−r2 ,dd ∆ ×C F2 , dd

= 0

2 ( P1 ,u ( 2 ) +P1, d ( 2 ) ) =71.1072

1.3

Cash Flow Tree

i=0 i=1 i=2

T=0 T=0.5 T=1

C F0 (1) = 0

r2 (0)= 2(er0 ∆-1) =

0.0404

C F1 ,u (2)=1.9356

r1

(1,u) = 2(

er1 , u ∆-1)

= 0.0887

r2(2,uu) = 0.1342

C F2 ,uu (3)=4.2106

C F1 ,d ( 2)=0

r1

(1,d) = 2(er1 ,d ∆-1)

= 0.0270

C F2 ,ud (3)=1.1811

r2(2,ud) = 0.0736

C F2 ,dd (3)=0

r2(2,dd) = 0.0148

∆=0.5

N = 100

rk = 5%

r2

(2,uu) = 2(

er2 , uu ∆-1) = 0.1342

C F2 ,uu=100 ×0.5 × max ( 0.1342−0.05,0 ) =4.2106

V 2 ,uu=e−r2,uu ∆ ×C F2 , uu

= 3.9458

r2

(2,ud) = 2(er2 ,ud ∆-1) = 0.0736

C F2 ,ud=100 × 0.5 ×max ( 0.0736−0.05,0 ) =1.1811

V 2 ,ud =e−r2 ,ud ∆ ×C F2 ,ud

= 1.1392

r2

(2,dd) = 2(er2 ,dd ∆-1) = 0.0148

C F2 ,dd =100× 0.5 ×max ( 0.0148−0.05,0 ) =0

V 2 , dd=e−r2 ,dd ∆ ×C F2 , dd

= 0

r1

(1,u) = 2(

er1 ,u ∆-1) = 0.0887

C F1 ,u=100 × 0.5× max ( 0.0887−0.05,0 ) =1.9356

V 1 ,u =e−r1 ,u ∆ × ¿] = 4.2879

r1

(1,d) = 2(er1 ,d ∆-1) = 0.0270

C F1 ,d =100 ×0.5 ×max ( 0.0270−0.05,0 ) =0

V 1 ,d =e−r 1,d ∆ × ¿] = 0.5620

r2 (0)= 2(

er0 ∆-1) = 0.0404

C F0(1) = 0

V 0=e−r0 ∆ ׿] = 2.3769

1.5 year Cap value tree

i=0 i=1 i=2

T=0 T=0.5 T=1

V 0= 2.3769 V 1 ,u = 4.2879 V 2 ,uu= 3.9458

V 1 ,d = 0.5620 V 2 ,ud = 1.1392

V 2 , dd= 0

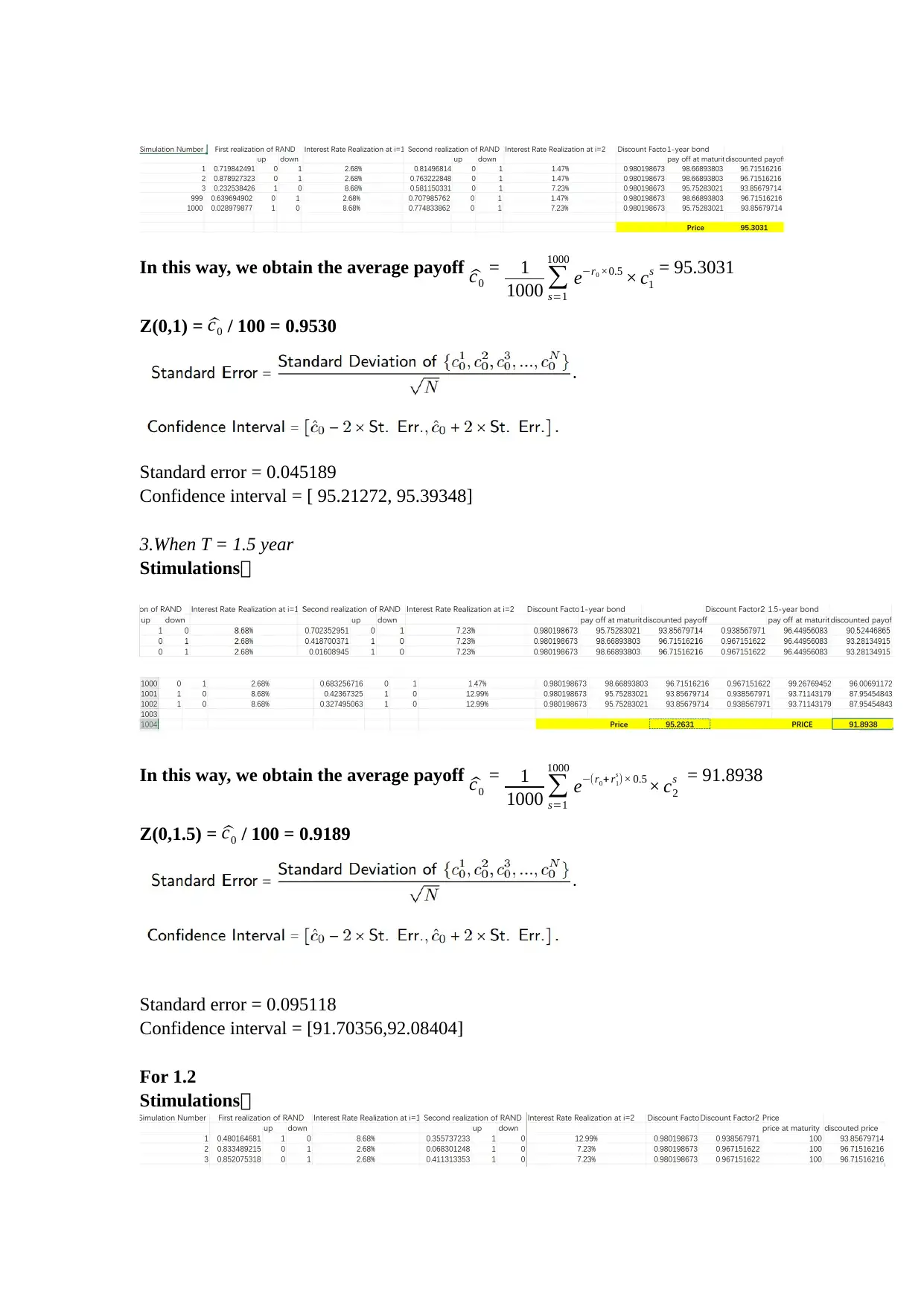

Part 2

we use Monte-Carlo Simulations approach to simulate 1000 times interest rate

scenarios in the future, an then obtain the value of the security by averaging an

appropriate discounted value of the payoff. N = 1,000

For 1.1

1.When T = 0.5 year.

The answers stay the same, Z ( 0,0.5 ) =e−r0 ∆ =¿0.9802.

2.When T = 1 year

Stimulations:

(1,u) = 2(

er1 ,u ∆-1) = 0.0887

C F1 ,u=100 × 0.5× max ( 0.0887−0.05,0 ) =1.9356

V 1 ,u =e−r1 ,u ∆ × ¿] = 4.2879

r1

(1,d) = 2(er1 ,d ∆-1) = 0.0270

C F1 ,d =100 ×0.5 ×max ( 0.0270−0.05,0 ) =0

V 1 ,d =e−r 1,d ∆ × ¿] = 0.5620

r2 (0)= 2(

er0 ∆-1) = 0.0404

C F0(1) = 0

V 0=e−r0 ∆ ׿] = 2.3769

1.5 year Cap value tree

i=0 i=1 i=2

T=0 T=0.5 T=1

V 0= 2.3769 V 1 ,u = 4.2879 V 2 ,uu= 3.9458

V 1 ,d = 0.5620 V 2 ,ud = 1.1392

V 2 , dd= 0

Part 2

we use Monte-Carlo Simulations approach to simulate 1000 times interest rate

scenarios in the future, an then obtain the value of the security by averaging an

appropriate discounted value of the payoff. N = 1,000

For 1.1

1.When T = 0.5 year.

The answers stay the same, Z ( 0,0.5 ) =e−r0 ∆ =¿0.9802.

2.When T = 1 year

Stimulations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

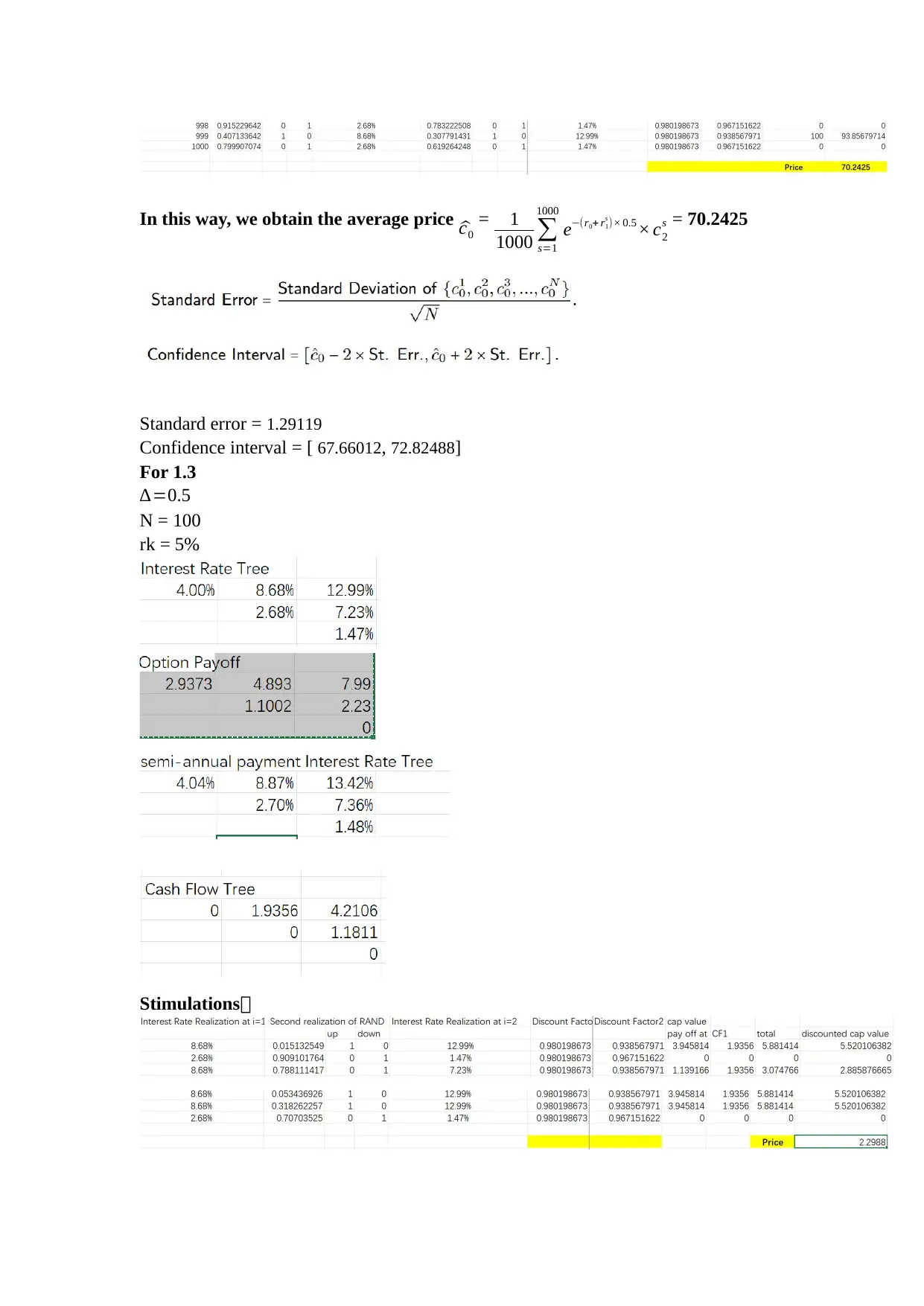

In this way, we obtain the average payoff ^c0

= 1

1000 ∑

s=1

1000

e−r0 ×0.5 × c1

s = 95.3031

Z(0,1) = ^c0 / 100 = 0.9530

Standard error = 0.045189

Confidence interval = [ 95.21272, 95.39348]

3.When T = 1.5 year

Stimulations:

In this way, we obtain the average payoff ^c0

= 1

1000 ∑

s=1

1000

e−(r0+ r1

s )× 0.5× c2

s = 91.8938

Z(0,1.5) = ^c0 / 100 = 0.9189

Standard error = 0.095118

Confidence interval = [91.70356,92.08404]

For 1.2

Stimulations:

= 1

1000 ∑

s=1

1000

e−r0 ×0.5 × c1

s = 95.3031

Z(0,1) = ^c0 / 100 = 0.9530

Standard error = 0.045189

Confidence interval = [ 95.21272, 95.39348]

3.When T = 1.5 year

Stimulations:

In this way, we obtain the average payoff ^c0

= 1

1000 ∑

s=1

1000

e−(r0+ r1

s )× 0.5× c2

s = 91.8938

Z(0,1.5) = ^c0 / 100 = 0.9189

Standard error = 0.095118

Confidence interval = [91.70356,92.08404]

For 1.2

Stimulations:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this way, we obtain the average price ^c0

= 1

1000 ∑

s=1

1000

e−(r0+ r1

s )× 0.5 × c2

s = 70.2425

Standard error = 1.29119

Confidence interval = [ 67.66012, 72.82488]

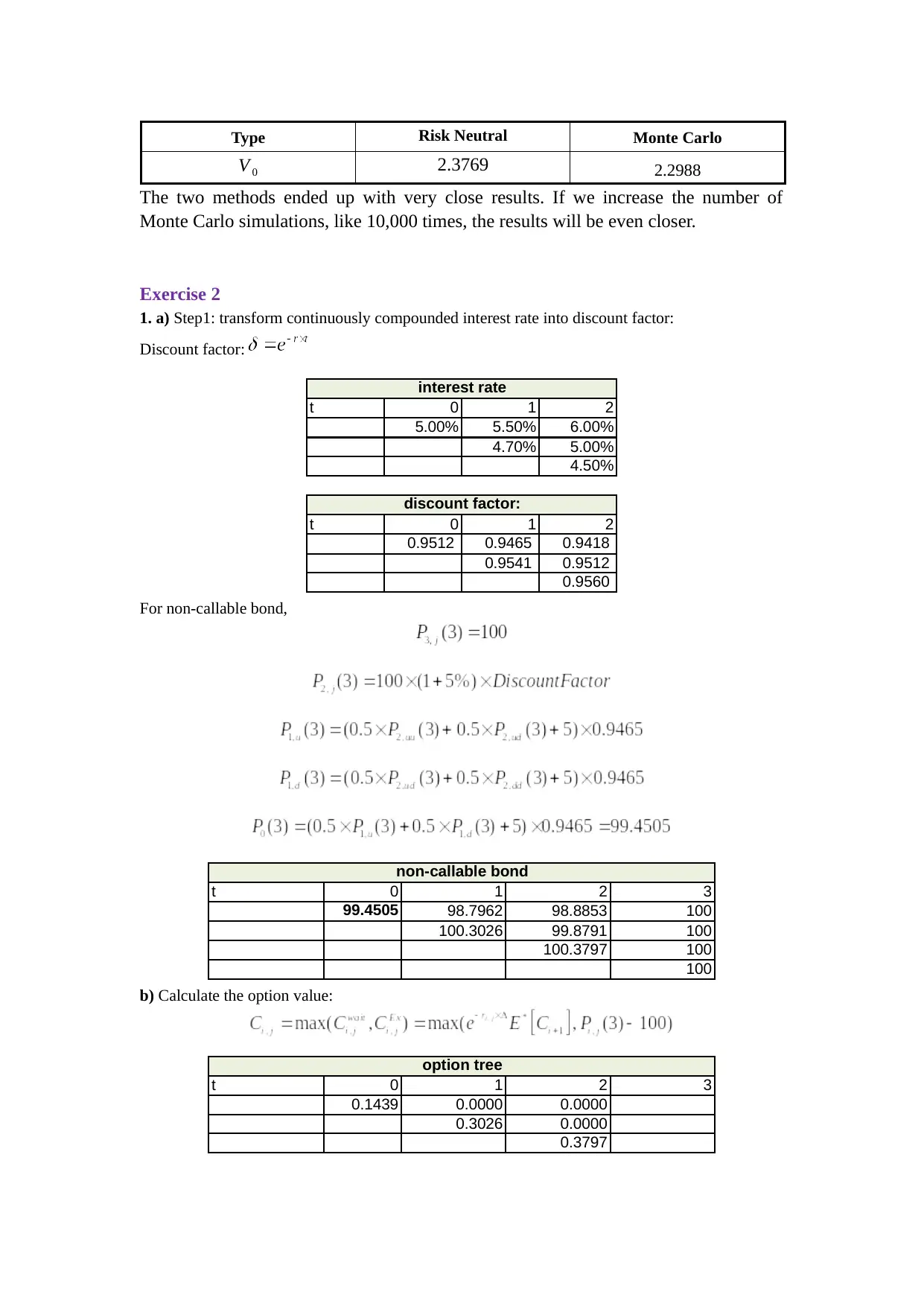

For 1.3

∆=0.5

N = 100

rk = 5%

Stimulations:

= 1

1000 ∑

s=1

1000

e−(r0+ r1

s )× 0.5 × c2

s = 70.2425

Standard error = 1.29119

Confidence interval = [ 67.66012, 72.82488]

For 1.3

∆=0.5

N = 100

rk = 5%

Stimulations:

The payoff at maturity = e−r2

s × 0.5 × CF2

s

the discounted value of payoff at maturity = e−(r 0+r 1

s )×0.5 ¿×

CF2

s+CF1

s)

Obtain the average of the payoff. ^c0

= 1

1000 ∑

s=1

1000

e−(r0+ r1

s )× 0.5(e−r2

s × 0.5× CF2

s +CF1

s ) =

2.2988

Standard error = 0.066223

Confidence interval = [ 2.166354, 2.431246]

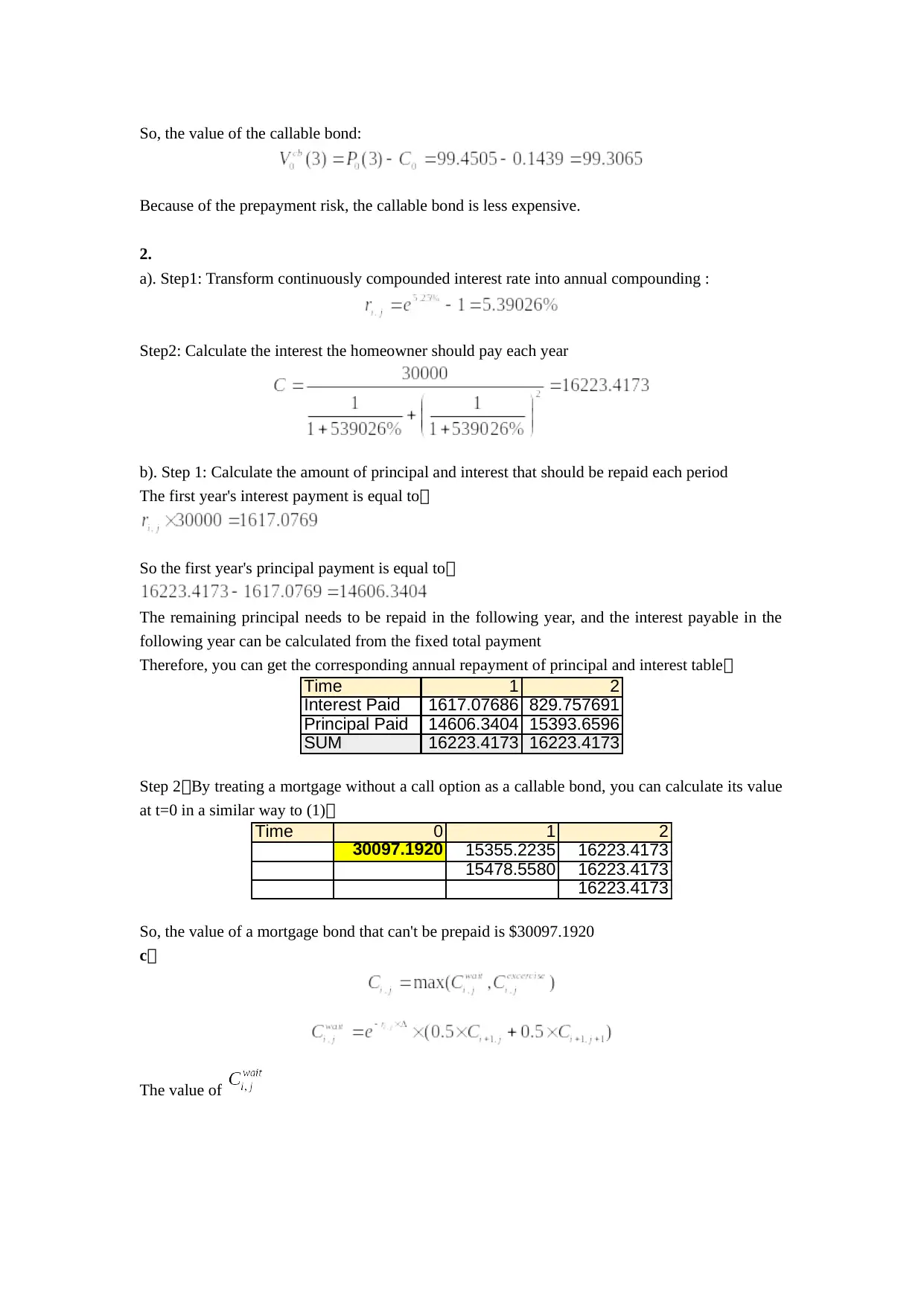

Compare the results obtained in both parts

Type Risk Neutral Monte Carlo

Z ( 0,1.5 ) 0.9529 0.9530

Z ( 0,2 ) 0.9194 0.9189

P0 ( 2 ) 71.1072

70.2425

s × 0.5 × CF2

s

the discounted value of payoff at maturity = e−(r 0+r 1

s )×0.5 ¿×

CF2

s+CF1

s)

Obtain the average of the payoff. ^c0

= 1

1000 ∑

s=1

1000

e−(r0+ r1

s )× 0.5(e−r2

s × 0.5× CF2

s +CF1

s ) =

2.2988

Standard error = 0.066223

Confidence interval = [ 2.166354, 2.431246]

Compare the results obtained in both parts

Type Risk Neutral Monte Carlo

Z ( 0,1.5 ) 0.9529 0.9530

Z ( 0,2 ) 0.9194 0.9189

P0 ( 2 ) 71.1072

70.2425

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Type Risk Neutral Monte Carlo

V 0 2.3769 2.2988

The two methods ended up with very close results. If we increase the number of

Monte Carlo simulations, like 10,000 times, the results will be even closer.

Exercise 2

1. a) Step1: transform continuously compounded interest rate into discount factor:

Discount factor:

interest rate non-c

t 0 1 2

5.00% 5.50% 6.00%

4.70% 5.00%

4.50%

discount factor:

t 0 1 2

0.9512 0.9465 0.9418

0.9541 0.9512

0.9560

For non-callable bond,

non-callable bond

t 0 1 2 3

99.4505 98.7962 98.8853 100

100.3026 99.8791 100

100.3797 100

100

b) Calculate the option value:

option tree

t 0 1 2 3

0.1439 0.0000 0.0000

0.3026 0.0000

0.3797

V 0 2.3769 2.2988

The two methods ended up with very close results. If we increase the number of

Monte Carlo simulations, like 10,000 times, the results will be even closer.

Exercise 2

1. a) Step1: transform continuously compounded interest rate into discount factor:

Discount factor:

interest rate non-c

t 0 1 2

5.00% 5.50% 6.00%

4.70% 5.00%

4.50%

discount factor:

t 0 1 2

0.9512 0.9465 0.9418

0.9541 0.9512

0.9560

For non-callable bond,

non-callable bond

t 0 1 2 3

99.4505 98.7962 98.8853 100

100.3026 99.8791 100

100.3797 100

100

b) Calculate the option value:

option tree

t 0 1 2 3

0.1439 0.0000 0.0000

0.3026 0.0000

0.3797

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

So, the value of the callable bond:

Because of the prepayment risk, the callable bond is less expensive.

2.

a). Step1: Transform continuously compounded interest rate into annual compounding :

Step2: Calculate the interest the homeowner should pay each year

b). Step 1: Calculate the amount of principal and interest that should be repaid each period

The first year's interest payment is equal to:

So the first year's principal payment is equal to:

The remaining principal needs to be repaid in the following year, and the interest payable in the

following year can be calculated from the fixed total payment

Therefore, you can get the corresponding annual repayment of principal and interest table:

Time 1 2

Interest Paid 1617.07686 829.757691

Principal Paid 14606.3404 15393.6596

SUM 16223.4173 16223.4173

Step 2:By treating a mortgage without a call option as a callable bond, you can calculate its value

at t=0 in a similar way to (1):

Time 0 1 2

30097.1920 15355.2235 16223.4173

15478.5580 16223.4173

16223.4173

So, the value of a mortgage bond that can't be prepaid is $30097.1920

c:

The value of

Because of the prepayment risk, the callable bond is less expensive.

2.

a). Step1: Transform continuously compounded interest rate into annual compounding :

Step2: Calculate the interest the homeowner should pay each year

b). Step 1: Calculate the amount of principal and interest that should be repaid each period

The first year's interest payment is equal to:

So the first year's principal payment is equal to:

The remaining principal needs to be repaid in the following year, and the interest payable in the

following year can be calculated from the fixed total payment

Therefore, you can get the corresponding annual repayment of principal and interest table:

Time 1 2

Interest Paid 1617.07686 829.757691

Principal Paid 14606.3404 15393.6596

SUM 16223.4173 16223.4173

Step 2:By treating a mortgage without a call option as a callable bond, you can calculate its value

at t=0 in a similar way to (1):

Time 0 1 2

30097.1920 15355.2235 16223.4173

15478.5580 16223.4173

16223.4173

So, the value of a mortgage bond that can't be prepaid is $30097.1920

c:

The value of

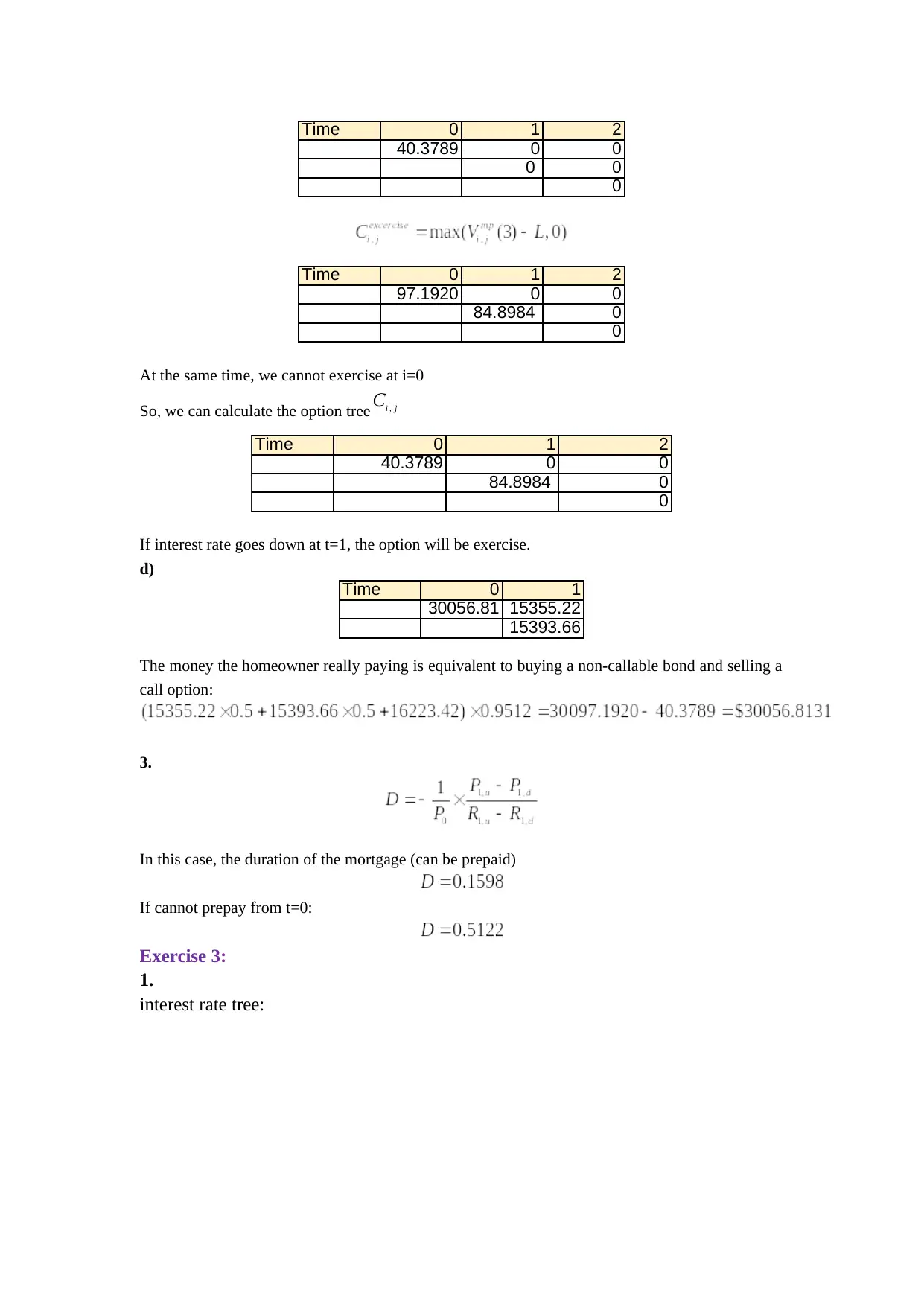

Time 0 1 2

40.3789 0 0

0 0

0

Time 0 1 2

97.1920 0 0

84.8984 0

0

At the same time, we cannot exercise at i=0

So, we can calculate the option tree

Time 0 1 2

40.3789 0 0

84.8984 0

0

If interest rate goes down at t=1, the option will be exercise.

d)

Time 0 1

30056.81 15355.22

15393.66

The money the homeowner really paying is equivalent to buying a non-callable bond and selling a

call option:

3.

In this case, the duration of the mortgage (can be prepaid)

If cannot prepay from t=0:

Exercise 3:

1.

interest rate tree:

40.3789 0 0

0 0

0

Time 0 1 2

97.1920 0 0

84.8984 0

0

At the same time, we cannot exercise at i=0

So, we can calculate the option tree

Time 0 1 2

40.3789 0 0

84.8984 0

0

If interest rate goes down at t=1, the option will be exercise.

d)

Time 0 1

30056.81 15355.22

15393.66

The money the homeowner really paying is equivalent to buying a non-callable bond and selling a

call option:

3.

In this case, the duration of the mortgage (can be prepaid)

If cannot prepay from t=0:

Exercise 3:

1.

interest rate tree:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

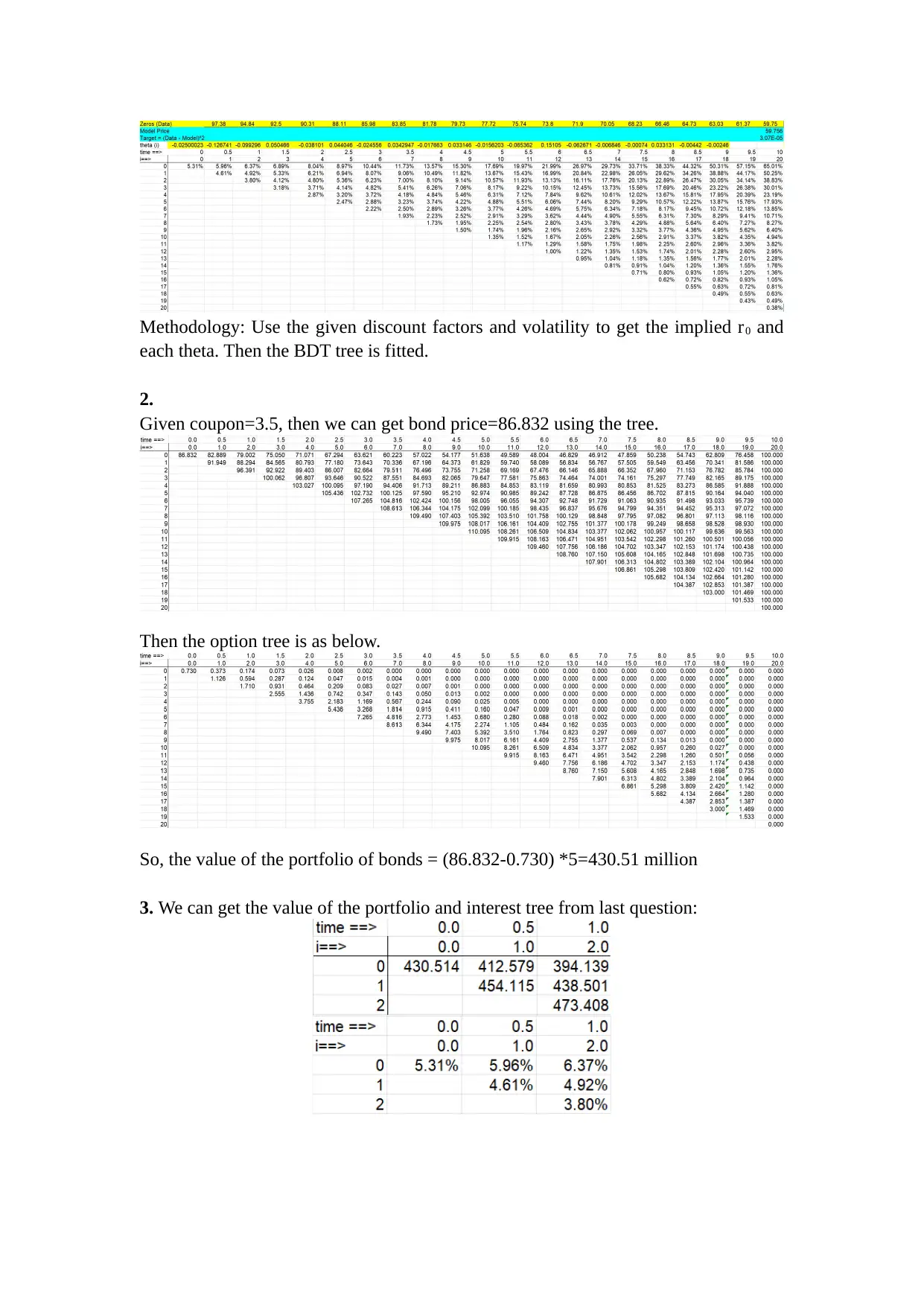

Methodology: Use the given discount factors and volatility to get the implied r0 and

each theta. Then the BDT tree is fitted.

2.

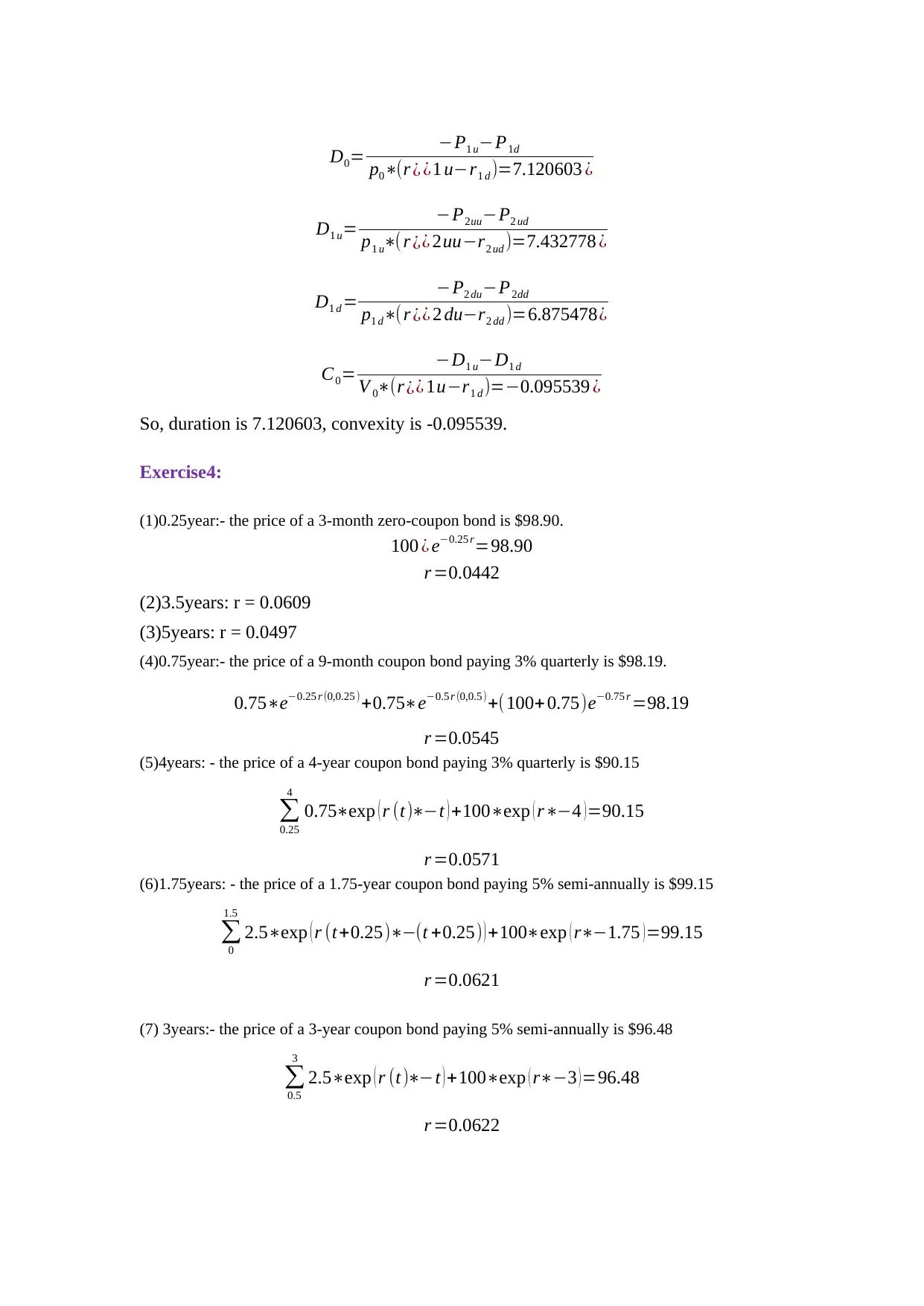

Given coupon=3.5, then we can get bond price=86.832 using the tree.

Then the option tree is as below.

So, the value of the portfolio of bonds = (86.832-0.730) *5=430.51 million

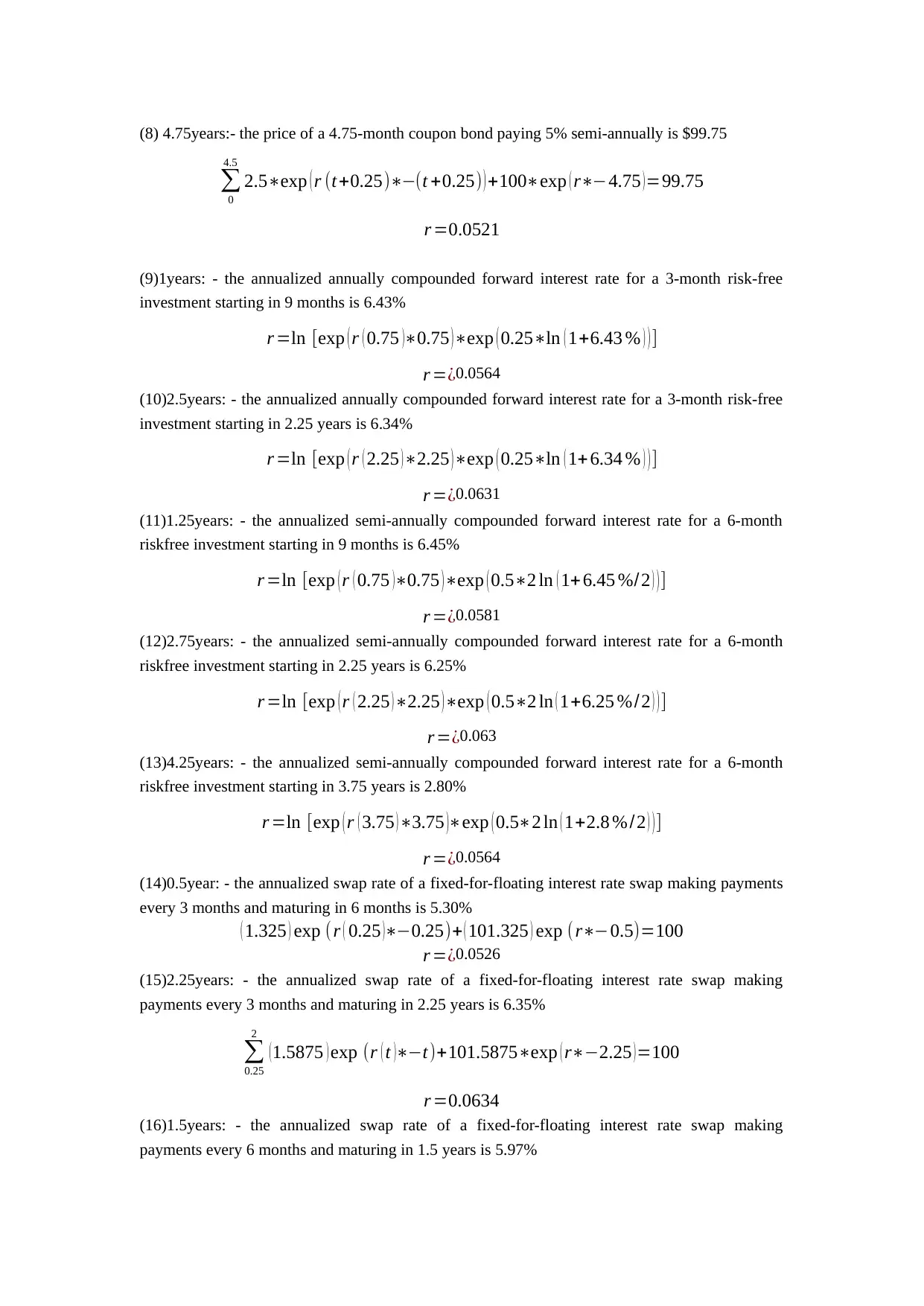

3. We can get the value of the portfolio and interest tree from last question:

each theta. Then the BDT tree is fitted.

2.

Given coupon=3.5, then we can get bond price=86.832 using the tree.

Then the option tree is as below.

So, the value of the portfolio of bonds = (86.832-0.730) *5=430.51 million

3. We can get the value of the portfolio and interest tree from last question:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D0= −P1 u−P1d

p0∗(r ¿ ¿1 u−r1 d )=7.120603 ¿

D1 u= −P2uu−P2 ud

p1 u∗( r ¿¿ 2uu−r2 ud )=7.432778 ¿

D1 d = −P2 du−P2dd

p1 d∗(r ¿¿ 2 du−r2 dd )=6.875478¿

C0= −D1 u−D1 d

V 0∗(r ¿¿ 1u−r1 d )=−0.095539 ¿

So, duration is 7.120603, convexity is -0.095539.

Exercise4:

(1)0.25year:- the price of a 3-month zero-coupon bond is $98.90.

100 ¿ e−0.25 r=98.90

r =0.0442

(2)3.5years: r = 0.0609

(3)5years: r = 0.0497

(4)0.75year:- the price of a 9-month coupon bond paying 3% quarterly is $98.19.

0.75∗e−0.25 r (0,0.25 )+0.75∗e−0.5 r (0,0.5)+(100+0.75)e−0.75 r =98.19

r =0.0545

(5)4years: - the price of a 4-year coupon bond paying 3% quarterly is $90.15

∑

0.25

4

0.75∗exp ( r (t)∗−t ) +100∗exp ( r∗−4 ) =90.15

r =0.0571

(6)1.75years: - the price of a 1.75-year coupon bond paying 5% semi-annually is $99.15

∑

0

1.5

2.5∗exp ( r (t+0.25)∗−(t +0.25) ) +100∗exp ( r∗−1.75 )=99.15

r =0.0621

(7) 3years:- the price of a 3-year coupon bond paying 5% semi-annually is $96.48

∑

0.5

3

2.5∗exp ( r (t)∗−t ) +100∗exp ( r∗−3 ) =96.48

r =0.0622

p0∗(r ¿ ¿1 u−r1 d )=7.120603 ¿

D1 u= −P2uu−P2 ud

p1 u∗( r ¿¿ 2uu−r2 ud )=7.432778 ¿

D1 d = −P2 du−P2dd

p1 d∗(r ¿¿ 2 du−r2 dd )=6.875478¿

C0= −D1 u−D1 d

V 0∗(r ¿¿ 1u−r1 d )=−0.095539 ¿

So, duration is 7.120603, convexity is -0.095539.

Exercise4:

(1)0.25year:- the price of a 3-month zero-coupon bond is $98.90.

100 ¿ e−0.25 r=98.90

r =0.0442

(2)3.5years: r = 0.0609

(3)5years: r = 0.0497

(4)0.75year:- the price of a 9-month coupon bond paying 3% quarterly is $98.19.

0.75∗e−0.25 r (0,0.25 )+0.75∗e−0.5 r (0,0.5)+(100+0.75)e−0.75 r =98.19

r =0.0545

(5)4years: - the price of a 4-year coupon bond paying 3% quarterly is $90.15

∑

0.25

4

0.75∗exp ( r (t)∗−t ) +100∗exp ( r∗−4 ) =90.15

r =0.0571

(6)1.75years: - the price of a 1.75-year coupon bond paying 5% semi-annually is $99.15

∑

0

1.5

2.5∗exp ( r (t+0.25)∗−(t +0.25) ) +100∗exp ( r∗−1.75 )=99.15

r =0.0621

(7) 3years:- the price of a 3-year coupon bond paying 5% semi-annually is $96.48

∑

0.5

3

2.5∗exp ( r (t)∗−t ) +100∗exp ( r∗−3 ) =96.48

r =0.0622

(8) 4.75years:- the price of a 4.75-month coupon bond paying 5% semi-annually is $99.75

∑

0

4.5

2.5∗exp ( r (t+0.25)∗−(t +0.25) ) +100∗exp ( r∗−4.75 )=99.75

r =0.0521

(9)1years: - the annualized annually compounded forward interest rate for a 3-month risk-free

investment starting in 9 months is 6.43%

r =ln [exp ( r ( 0.75 )∗0.75 )∗exp ( 0.25∗ln ( 1+6.43 % ) ) ]

r =¿0.0564

(10)2.5years: - the annualized annually compounded forward interest rate for a 3-month risk-free

investment starting in 2.25 years is 6.34%

r =ln [exp ( r ( 2.25 )∗2.25 )∗exp ( 0.25∗ln ( 1+ 6.34 % ) ) ]

r =¿0.0631

(11)1.25years: - the annualized semi-annually compounded forward interest rate for a 6-month

riskfree investment starting in 9 months is 6.45%

r =ln [exp ( r ( 0.75 )∗0.75 )∗exp ( 0.5∗2 ln ( 1+ 6.45 %/2 ) ) ]

r =¿0.0581

(12)2.75years: - the annualized semi-annually compounded forward interest rate for a 6-month

riskfree investment starting in 2.25 years is 6.25%

r =ln [exp ( r ( 2.25 )∗2.25 )∗exp ( 0.5∗2 ln ( 1+6.25 %/2 ) ) ]

r =¿0.063

(13)4.25years: - the annualized semi-annually compounded forward interest rate for a 6-month

riskfree investment starting in 3.75 years is 2.80%

r =ln [exp ( r ( 3.75 )∗3.75 )∗exp ( 0.5∗2 ln ( 1+2.8 % /2 ) ) ]

r =¿0.0564

(14)0.5year: - the annualized swap rate of a fixed-for-floating interest rate swap making payments

every 3 months and maturing in 6 months is 5.30%

( 1.325 ) exp (r ( 0.25 )∗−0.25)+ ( 101.325 ) exp (r∗−0.5)=100

r =¿0.0526

(15)2.25years: - the annualized swap rate of a fixed-for-floating interest rate swap making

payments every 3 months and maturing in 2.25 years is 6.35%

∑

0.25

2

(1.5875 ) exp (r ( t )∗−t)+101.5875∗exp ( r∗−2.25 )=100

r =0.0634

(16)1.5years: - the annualized swap rate of a fixed-for-floating interest rate swap making

payments every 6 months and maturing in 1.5 years is 5.97%

∑

0

4.5

2.5∗exp ( r (t+0.25)∗−(t +0.25) ) +100∗exp ( r∗−4.75 )=99.75

r =0.0521

(9)1years: - the annualized annually compounded forward interest rate for a 3-month risk-free

investment starting in 9 months is 6.43%

r =ln [exp ( r ( 0.75 )∗0.75 )∗exp ( 0.25∗ln ( 1+6.43 % ) ) ]

r =¿0.0564

(10)2.5years: - the annualized annually compounded forward interest rate for a 3-month risk-free

investment starting in 2.25 years is 6.34%

r =ln [exp ( r ( 2.25 )∗2.25 )∗exp ( 0.25∗ln ( 1+ 6.34 % ) ) ]

r =¿0.0631

(11)1.25years: - the annualized semi-annually compounded forward interest rate for a 6-month

riskfree investment starting in 9 months is 6.45%

r =ln [exp ( r ( 0.75 )∗0.75 )∗exp ( 0.5∗2 ln ( 1+ 6.45 %/2 ) ) ]

r =¿0.0581

(12)2.75years: - the annualized semi-annually compounded forward interest rate for a 6-month

riskfree investment starting in 2.25 years is 6.25%

r =ln [exp ( r ( 2.25 )∗2.25 )∗exp ( 0.5∗2 ln ( 1+6.25 %/2 ) ) ]

r =¿0.063

(13)4.25years: - the annualized semi-annually compounded forward interest rate for a 6-month

riskfree investment starting in 3.75 years is 2.80%

r =ln [exp ( r ( 3.75 )∗3.75 )∗exp ( 0.5∗2 ln ( 1+2.8 % /2 ) ) ]

r =¿0.0564

(14)0.5year: - the annualized swap rate of a fixed-for-floating interest rate swap making payments

every 3 months and maturing in 6 months is 5.30%

( 1.325 ) exp (r ( 0.25 )∗−0.25)+ ( 101.325 ) exp (r∗−0.5)=100

r =¿0.0526

(15)2.25years: - the annualized swap rate of a fixed-for-floating interest rate swap making

payments every 3 months and maturing in 2.25 years is 6.35%

∑

0.25

2

(1.5875 ) exp (r ( t )∗−t)+101.5875∗exp ( r∗−2.25 )=100

r =0.0634

(16)1.5years: - the annualized swap rate of a fixed-for-floating interest rate swap making

payments every 6 months and maturing in 1.5 years is 5.97%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14