Financial Modeling: Spreadsheet Model for NPV and IRR

VerifiedAdded on 2023/04/21

|13

|2375

|497

AI Summary

This document provides a step-by-step guide on creating a spreadsheet model to calculate the Net Present Value (NPV) and Internal Rate of Return (IRR) for an investment. It explains the significance of these financial metrics in project evaluation and decision making. The document also includes a sensitivity analysis and correlation analysis to assess the impact of different variables on the project's outcomes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

MODELING

MODELING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

INTRODUCTION................................................................................................3

Part 1...............................................................................................................3

Spreadsheet model to find the Net Present Value and Internal rate of

Return for the investment............................................................................3

Part B...............................................................................................................7

Simulation on proposed project....................................................................7

Explanation of what the model is doing..............................................10

Model limitations....................................................................................11

CONCLUSION.................................................................................................11

REFRENCES....................................................................................................12

INTRODUCTION................................................................................................3

Part 1...............................................................................................................3

Spreadsheet model to find the Net Present Value and Internal rate of

Return for the investment............................................................................3

Part B...............................................................................................................7

Simulation on proposed project....................................................................7

Explanation of what the model is doing..............................................10

Model limitations....................................................................................11

CONCLUSION.................................................................................................11

REFRENCES....................................................................................................12

INTRODUCTION

In today era it is very difficult to make sound business decision. In

order to reduce this complexity simulation methods are used by the

managers. In this report various methods like sensitive analysis and scenario

analysis are done. Along with this project evaluation is also done in the

report. Hence, it can be said that by using these methods best decisions can

be made by the managers.

PART 1

Spreadsheet model to find the Net Present Value and Internal rate of Return

for the investment

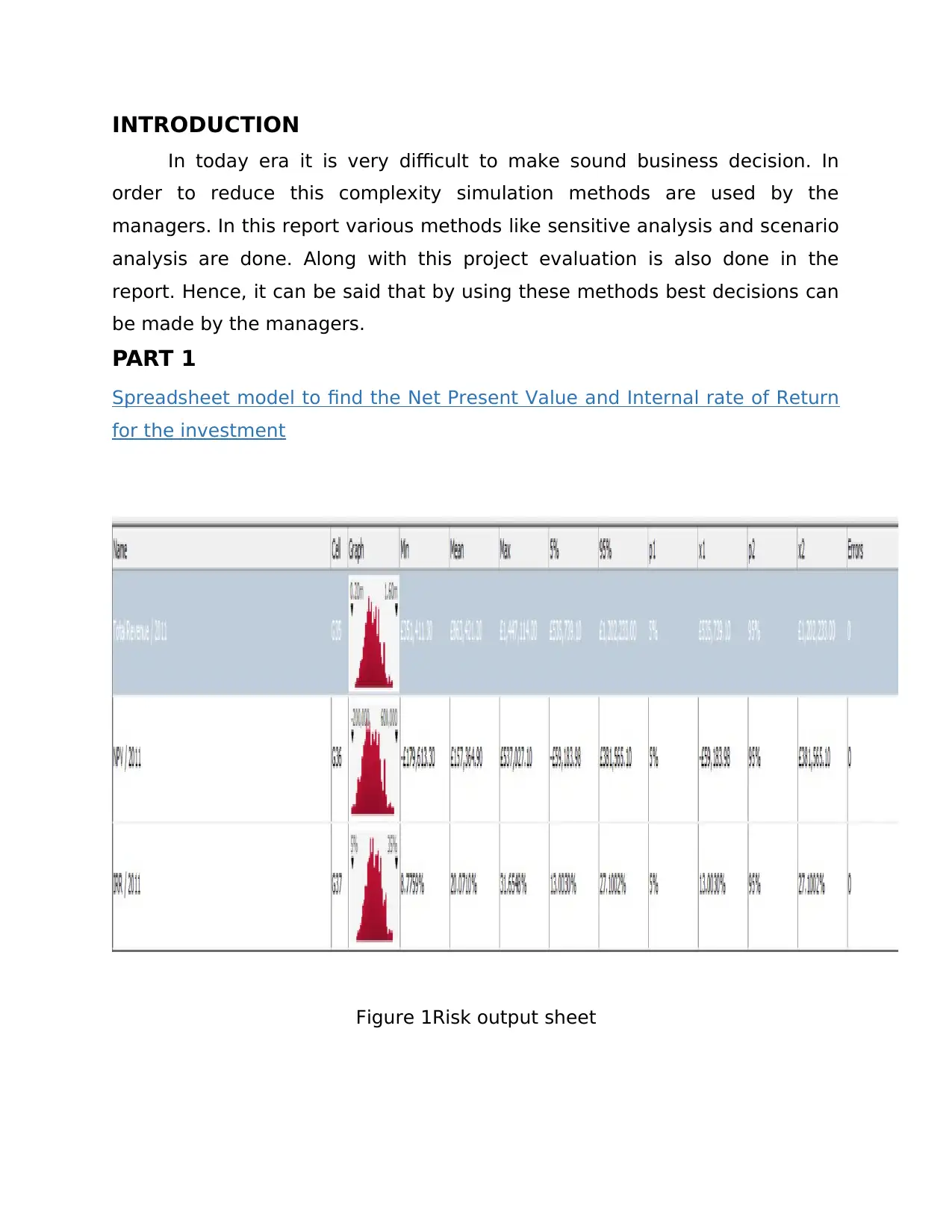

Figure 1Risk output sheet

In today era it is very difficult to make sound business decision. In

order to reduce this complexity simulation methods are used by the

managers. In this report various methods like sensitive analysis and scenario

analysis are done. Along with this project evaluation is also done in the

report. Hence, it can be said that by using these methods best decisions can

be made by the managers.

PART 1

Spreadsheet model to find the Net Present Value and Internal rate of Return

for the investment

Figure 1Risk output sheet

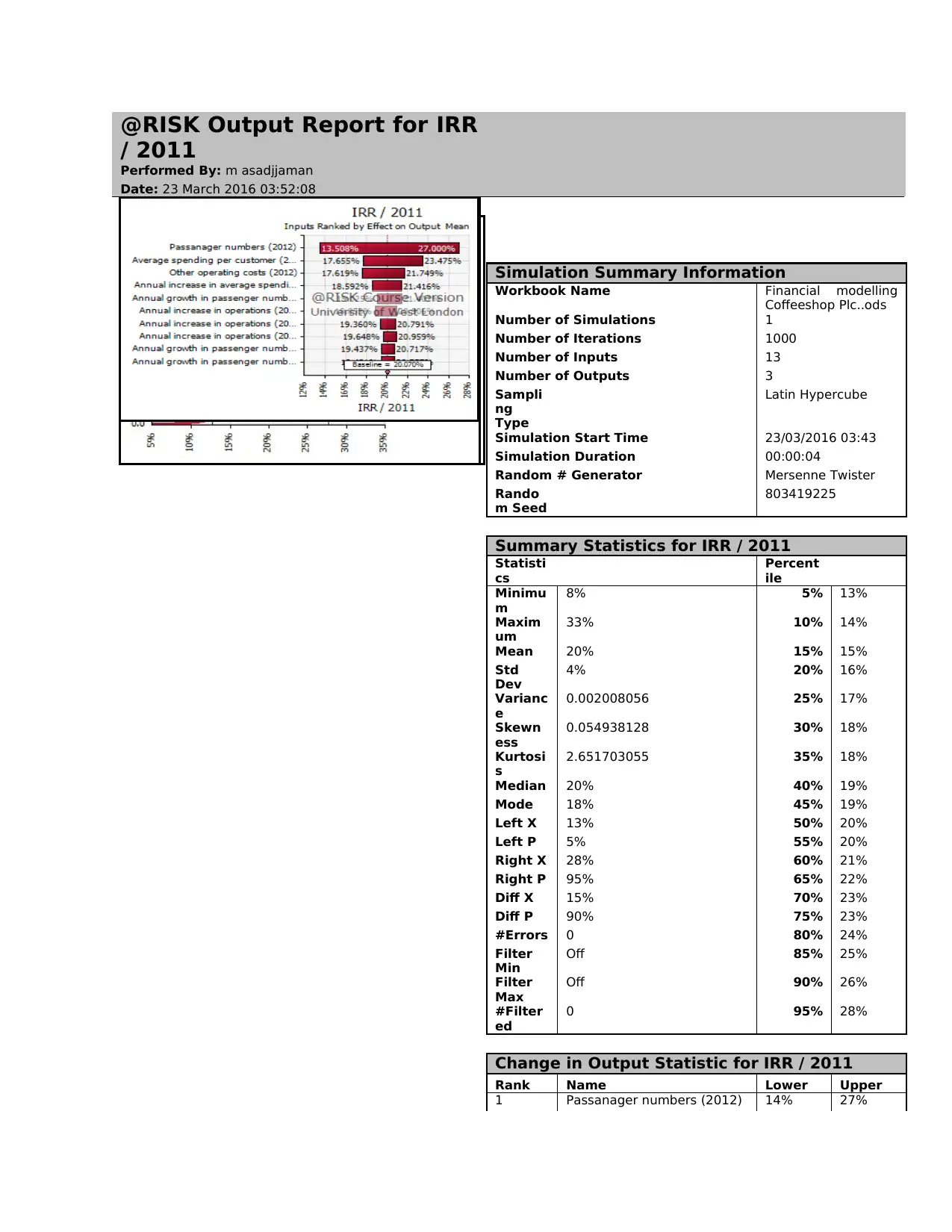

In this attached image results of NPV and IRR are clearly given and helps un

taking decision related to the viability of the project. On the basis of results

produced by the above given table we can see amount that firm may lose in

its business. On the basis of projections financial manager comers to know

about the income that this project can be generate for the firm. The above

given chart shows the maximum, minimum and average return that a firm

can earn on the project during life time of the project. NPV measures the

present value of the project that remain after deducting initial investment

from the present value of the cash flows (Zivot. and Wang, 2007). The cost

of capital for project is 15% which is also discount rate used in the project for

computing present value of the cash flows. On the basis of results produced

by the NPV and IRR best viable can be selected by the firm. Thus, it can be

said that this method help financial managers in selecting most viable

project for the firm. IRR indicate the actual return that a project can earn

on the invested amount. The only difference between ARR and IRR is that in

former method calculation process is tough then latter method of project

evaluation. By using IRR managers can be best decisions related to project

selection. On the basis of analysis of figures given in taqble it can be said

that project is viable for the firm.

@RISK Output Report for

NPV / 2011

Performed By: m asadjjaman

Date: 23 March 2016 03:52:06

Simulation Summary Information

Workbook Name Financial modelling

Coffeeshop Plc..ods

Number of Simulations 1

Number of Iterations 1000

Number of Inputs 13

Number of Outputs 3

Sampli

ng

Type

Latin Hypercube

Simulation Start Time 23/03/2016 03:43

taking decision related to the viability of the project. On the basis of results

produced by the above given table we can see amount that firm may lose in

its business. On the basis of projections financial manager comers to know

about the income that this project can be generate for the firm. The above

given chart shows the maximum, minimum and average return that a firm

can earn on the project during life time of the project. NPV measures the

present value of the project that remain after deducting initial investment

from the present value of the cash flows (Zivot. and Wang, 2007). The cost

of capital for project is 15% which is also discount rate used in the project for

computing present value of the cash flows. On the basis of results produced

by the NPV and IRR best viable can be selected by the firm. Thus, it can be

said that this method help financial managers in selecting most viable

project for the firm. IRR indicate the actual return that a project can earn

on the invested amount. The only difference between ARR and IRR is that in

former method calculation process is tough then latter method of project

evaluation. By using IRR managers can be best decisions related to project

selection. On the basis of analysis of figures given in taqble it can be said

that project is viable for the firm.

@RISK Output Report for

NPV / 2011

Performed By: m asadjjaman

Date: 23 March 2016 03:52:06

Simulation Summary Information

Workbook Name Financial modelling

Coffeeshop Plc..ods

Number of Simulations 1

Number of Iterations 1000

Number of Inputs 13

Number of Outputs 3

Sampli

ng

Type

Latin Hypercube

Simulation Start Time 23/03/2016 03:43

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Simulation Duration 00:00:04

Random # Generator Mersenne Twister

Rando

m

Seed

803419225

Summary Statistics for NPV / 2011

Statisti

cs

Percenti

le

Minimu

m

-£214,755.25 5% -

£66,943.

19

Maxim

um

£595,362.02 10% -

£20,029.

41

Mean £157,676.37 15% £5,431.2

9

Std

Dev

£140,196.45 20% £33,310.

94

Varian

ce

19655043896 25% £58,842.

34

Skewn

ess

0.151804856 30% £79,845.

75

Kurtosi

s

2.676541841 35% £96,933.

25

Median £153,081.26 40% £110,69

6.94

Mode £241,653.18 45% £130,57

4.06

Left X -£66,943.19 50% £153,08

1.26

Left P 5% 55% £168,91

0.07

Right X £402,039.77 60% £194,25

9.25

Right P 95% 65% £215,20

4.96

Diff X £468,982.96 70% £235,13

6.31

Diff P 90% 75% £252,32

1.99

#Error

s

0 80% £281,22

6.24

Filter

Min

Off 85% £308,94

6.36

Filter

Max

Off 90% £340,09

1.57

#Filter

ed

0 95% £402,03

9.77

Change in Output Statistic for NPV / 2011

Rank Name Lower Upper

1 Passanager numbers

(2012)

-

£43,387.

38

£378,06

4.49

2 Average spending per

customer (2012)

£83,252.

77

£264,90

8.48

3 Other operating costs

(2012)

£83,102.

76

£209,85

7.37

4 Annual increase in average

spending (2013 onwards)

£110,26

0.31

£201,07

4.22

5 Annual growth in

passenger numbers (2015)

£124,78

0.21

£200,59

4.02

6 Annual increase in

operations (2015)

£119,73

2.04

£183,21

2.57

7 Annual increase in £135,11 £179,82

Random # Generator Mersenne Twister

Rando

m

Seed

803419225

Summary Statistics for NPV / 2011

Statisti

cs

Percenti

le

Minimu

m

-£214,755.25 5% -

£66,943.

19

Maxim

um

£595,362.02 10% -

£20,029.

41

Mean £157,676.37 15% £5,431.2

9

Std

Dev

£140,196.45 20% £33,310.

94

Varian

ce

19655043896 25% £58,842.

34

Skewn

ess

0.151804856 30% £79,845.

75

Kurtosi

s

2.676541841 35% £96,933.

25

Median £153,081.26 40% £110,69

6.94

Mode £241,653.18 45% £130,57

4.06

Left X -£66,943.19 50% £153,08

1.26

Left P 5% 55% £168,91

0.07

Right X £402,039.77 60% £194,25

9.25

Right P 95% 65% £215,20

4.96

Diff X £468,982.96 70% £235,13

6.31

Diff P 90% 75% £252,32

1.99

#Error

s

0 80% £281,22

6.24

Filter

Min

Off 85% £308,94

6.36

Filter

Max

Off 90% £340,09

1.57

#Filter

ed

0 95% £402,03

9.77

Change in Output Statistic for NPV / 2011

Rank Name Lower Upper

1 Passanager numbers

(2012)

-

£43,387.

38

£378,06

4.49

2 Average spending per

customer (2012)

£83,252.

77

£264,90

8.48

3 Other operating costs

(2012)

£83,102.

76

£209,85

7.37

4 Annual increase in average

spending (2013 onwards)

£110,26

0.31

£201,07

4.22

5 Annual growth in

passenger numbers (2015)

£124,78

0.21

£200,59

4.02

6 Annual increase in

operations (2015)

£119,73

2.04

£183,21

2.57

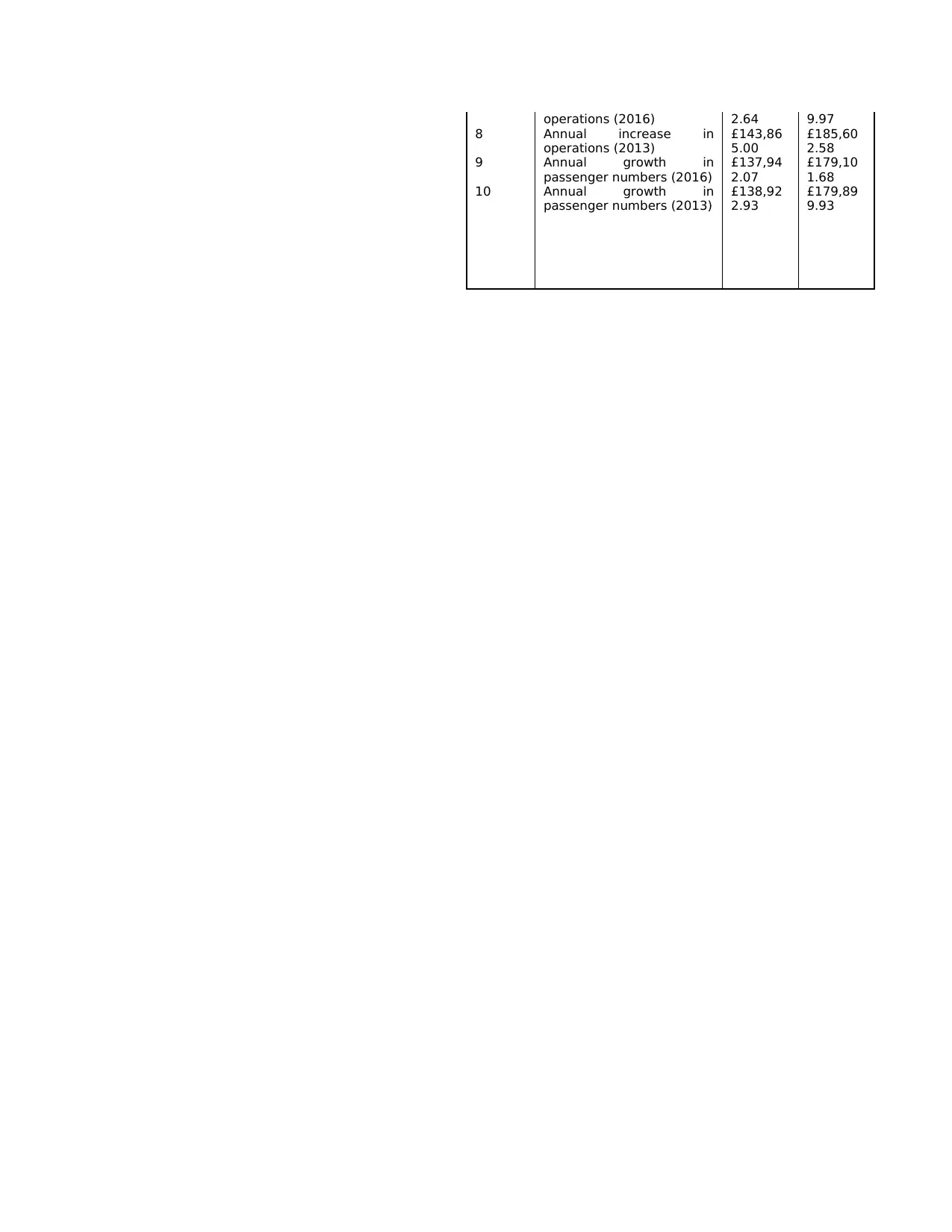

7 Annual increase in £135,11 £179,82

operations (2016) 2.64 9.97

8 Annual increase in

operations (2013)

£143,86

5.00

£185,60

2.58

9 Annual growth in

passenger numbers (2016)

£137,94

2.07

£179,10

1.68

10 Annual growth in

passenger numbers (2013)

£138,92

2.93

£179,89

9.93

8 Annual increase in

operations (2013)

£143,86

5.00

£185,60

2.58

9 Annual growth in

passenger numbers (2016)

£137,94

2.07

£179,10

1.68

10 Annual growth in

passenger numbers (2013)

£138,92

2.93

£179,89

9.93

@RISK Output Report for IRR

/ 2011

Performed By: m asadjjaman

Date: 23 March 2016 03:52:08

Simulation Summary Information

Workbook Name Financial modelling

Coffeeshop Plc..ods

Number of Simulations 1

Number of Iterations 1000

Number of Inputs 13

Number of Outputs 3

Sampli

ng

Type

Latin Hypercube

Simulation Start Time 23/03/2016 03:43

Simulation Duration 00:00:04

Random # Generator Mersenne Twister

Rando

m Seed

803419225

Summary Statistics for IRR / 2011

Statisti

cs

Percent

ile

Minimu

m

8% 5% 13%

Maxim

um

33% 10% 14%

Mean 20% 15% 15%

Std

Dev

4% 20% 16%

Varianc

e

0.002008056 25% 17%

Skewn

ess

0.054938128 30% 18%

Kurtosi

s

2.651703055 35% 18%

Median 20% 40% 19%

Mode 18% 45% 19%

Left X 13% 50% 20%

Left P 5% 55% 20%

Right X 28% 60% 21%

Right P 95% 65% 22%

Diff X 15% 70% 23%

Diff P 90% 75% 23%

#Errors 0 80% 24%

Filter

Min

Off 85% 25%

Filter

Max

Off 90% 26%

#Filter

ed

0 95% 28%

Change in Output Statistic for IRR / 2011

Rank Name Lower Upper

1 Passanager numbers (2012) 14% 27%

/ 2011

Performed By: m asadjjaman

Date: 23 March 2016 03:52:08

Simulation Summary Information

Workbook Name Financial modelling

Coffeeshop Plc..ods

Number of Simulations 1

Number of Iterations 1000

Number of Inputs 13

Number of Outputs 3

Sampli

ng

Type

Latin Hypercube

Simulation Start Time 23/03/2016 03:43

Simulation Duration 00:00:04

Random # Generator Mersenne Twister

Rando

m Seed

803419225

Summary Statistics for IRR / 2011

Statisti

cs

Percent

ile

Minimu

m

8% 5% 13%

Maxim

um

33% 10% 14%

Mean 20% 15% 15%

Std

Dev

4% 20% 16%

Varianc

e

0.002008056 25% 17%

Skewn

ess

0.054938128 30% 18%

Kurtosi

s

2.651703055 35% 18%

Median 20% 40% 19%

Mode 18% 45% 19%

Left X 13% 50% 20%

Left P 5% 55% 20%

Right X 28% 60% 21%

Right P 95% 65% 22%

Diff X 15% 70% 23%

Diff P 90% 75% 23%

#Errors 0 80% 24%

Filter

Min

Off 85% 25%

Filter

Max

Off 90% 26%

#Filter

ed

0 95% 28%

Change in Output Statistic for IRR / 2011

Rank Name Lower Upper

1 Passanager numbers (2012) 14% 27%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 Average spending per

customer (2012)

18% 23%

3 Other operating costs (2012) 18% 22%

4 Annual increase in average

spending (2013 onwards)

19% 21%

5 Annual growth in passenger

numbers (2015)

19% 21%

6 Annual increase in

operations (2015)

19% 21%

7 Annual increase in

operations (2016)

19% 21%

8 Annual increase in

operations (2013)

20% 21%

9 Annual growth in passenger

numbers (2016)

19% 21%

10 Annual growth in passenger

numbers (2013)

19% 21%

PART B

Simulation on proposed project

@RISK Sensitivity

Analysis

Performed By: m asadjjaman

Date: 23 March 2016 01:35:25

Ran

k

For

G35

Ce

ll

Name Description Sheet1!

G35

Total

Revenue /

2011

Correlatio

n Coeff.

Sheet1!

G36

NPV /

2011

Correlatio

n Coeff.

Sheet1!

G37

IRR / 2011

Correlatio

n Coeff.

#1 B5 Passanager numbers (2012) RiskTriang(1800000,2000000,2300000) 0.87 0.88 0.88

#2 B1

4

Average spending per

customer (2012) RiskNormal(5,0.1) 0.31 0.30 0.30

#3 B1

9 Other operating costs (2012) RiskTriang(280000,300000,330000) -

0.19

-

0.20

-

0.19

#4 B2

2

Annual increase in operations

(2015) RiskNormal(0,10,RiskCorrmat(NewMatrix2,3)) 0.18 0.18 0.18

#5 B9 Annual growth in passenger

numbers (2016)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,4)) 0.13 0.12 0.11

#6 B1

5

Annual increase in average

spending (2013 onwards) RiskUniform(0.1,0.2) 0.12 0.09 0.08

#7 B8 Annual growth in passenger

numbers (2015)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,3)) 0.08 0.06 0.06

#8 B2

1

Annual increase in operations

(2014) RiskNormal(0,10,RiskCorrmat(NewMatrix2,2)) 0.06 0.06 0.06

#9 B7 Annual growth in passenger

numbers (2014)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,2)) 0.03 0.02 0.01

#1

0

B2

3

Annual increase in operations

(2016) RiskNormal(0,10,RiskCorrmat(NewMatrix2,4)) -

0.03

-

0.03

-

0.04

#1

1

B2

0

Annual increase in operations

(2013) RiskNormal(0,10,RiskCorrmat(NewMatrix2,1)) -

0.00

-

0.00

-

0.00

customer (2012)

18% 23%

3 Other operating costs (2012) 18% 22%

4 Annual increase in average

spending (2013 onwards)

19% 21%

5 Annual growth in passenger

numbers (2015)

19% 21%

6 Annual increase in

operations (2015)

19% 21%

7 Annual increase in

operations (2016)

19% 21%

8 Annual increase in

operations (2013)

20% 21%

9 Annual growth in passenger

numbers (2016)

19% 21%

10 Annual growth in passenger

numbers (2013)

19% 21%

PART B

Simulation on proposed project

@RISK Sensitivity

Analysis

Performed By: m asadjjaman

Date: 23 March 2016 01:35:25

Ran

k

For

G35

Ce

ll

Name Description Sheet1!

G35

Total

Revenue /

2011

Correlatio

n Coeff.

Sheet1!

G36

NPV /

2011

Correlatio

n Coeff.

Sheet1!

G37

IRR / 2011

Correlatio

n Coeff.

#1 B5 Passanager numbers (2012) RiskTriang(1800000,2000000,2300000) 0.87 0.88 0.88

#2 B1

4

Average spending per

customer (2012) RiskNormal(5,0.1) 0.31 0.30 0.30

#3 B1

9 Other operating costs (2012) RiskTriang(280000,300000,330000) -

0.19

-

0.20

-

0.19

#4 B2

2

Annual increase in operations

(2015) RiskNormal(0,10,RiskCorrmat(NewMatrix2,3)) 0.18 0.18 0.18

#5 B9 Annual growth in passenger

numbers (2016)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,4)) 0.13 0.12 0.11

#6 B1

5

Annual increase in average

spending (2013 onwards) RiskUniform(0.1,0.2) 0.12 0.09 0.08

#7 B8 Annual growth in passenger

numbers (2015)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,3)) 0.08 0.06 0.06

#8 B2

1

Annual increase in operations

(2014) RiskNormal(0,10,RiskCorrmat(NewMatrix2,2)) 0.06 0.06 0.06

#9 B7 Annual growth in passenger

numbers (2014)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,2)) 0.03 0.02 0.01

#1

0

B2

3

Annual increase in operations

(2016) RiskNormal(0,10,RiskCorrmat(NewMatrix2,4)) -

0.03

-

0.03

-

0.04

#1

1

B2

0

Annual increase in operations

(2013) RiskNormal(0,10,RiskCorrmat(NewMatrix2,1)) -

0.00

-

0.00

-

0.00

#1

2 B6 Annual growth in passenger

numbers (2013)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,1)) 0.00

-

0.01

-

0.02

- B1

7 Gross margin RiskUniform(64%,66%) n/a n/a n/a

In this image given above sensitive analysis of NPV and IRR is done for entire

project life. In this report different distribution are used like normal

distribution, triangular distribution and uniform distribution. By using same

from different sides project is evaluated. These distributions indicate the

maximum, average and minimum value of the project that is at risk. These

values are shown for each and every type of distribution. Sensitivity analysis

is used to measure changes that can take place in the specific variable with

change in one variable. By looking at the sensitive table manager get an idea

about the likely changes in the value of specific variable due to change in

other variable (Andersen, Bollerslev, T. and Diebold, 2007). The predictions

made by sensitive analysis help managers in making sound business

decisions. This is because there is tolerance level that manager decide

related to the specific variable. Manager will use that tolerance level for in

order to identify the limit up to which he can accept changes in the specific

variable. In the given table values of correlation is given for different factors

and by using values of correlation impact of input on output can be

determined easily. Means that by using value of correlation the extent to

which specific input can affect output is measured in systematic way

(Example models. 2016). Thus, it can be said that along with sensitive

analysis correlation is a important technique that can be used by the

managers in order to identify impact on one variable if other variable value

get changed with passage of time. Hence, it can be said that both sensitive

analysis and correlation have a due importance for the managers.

2 B6 Annual growth in passenger

numbers (2013)

RiskTriang(1%,1.5%,3%,RiskCorrmat(NewMatri

x1,1)) 0.00

-

0.01

-

0.02

- B1

7 Gross margin RiskUniform(64%,66%) n/a n/a n/a

In this image given above sensitive analysis of NPV and IRR is done for entire

project life. In this report different distribution are used like normal

distribution, triangular distribution and uniform distribution. By using same

from different sides project is evaluated. These distributions indicate the

maximum, average and minimum value of the project that is at risk. These

values are shown for each and every type of distribution. Sensitivity analysis

is used to measure changes that can take place in the specific variable with

change in one variable. By looking at the sensitive table manager get an idea

about the likely changes in the value of specific variable due to change in

other variable (Andersen, Bollerslev, T. and Diebold, 2007). The predictions

made by sensitive analysis help managers in making sound business

decisions. This is because there is tolerance level that manager decide

related to the specific variable. Manager will use that tolerance level for in

order to identify the limit up to which he can accept changes in the specific

variable. In the given table values of correlation is given for different factors

and by using values of correlation impact of input on output can be

determined easily. Means that by using value of correlation the extent to

which specific input can affect output is measured in systematic way

(Example models. 2016). Thus, it can be said that along with sensitive

analysis correlation is a important technique that can be used by the

managers in order to identify impact on one variable if other variable value

get changed with passage of time. Hence, it can be said that both sensitive

analysis and correlation have a due importance for the managers.

@RISK Input

Results

Performed By: m asadjjaman

Date: 23 March 2016 02:23:00

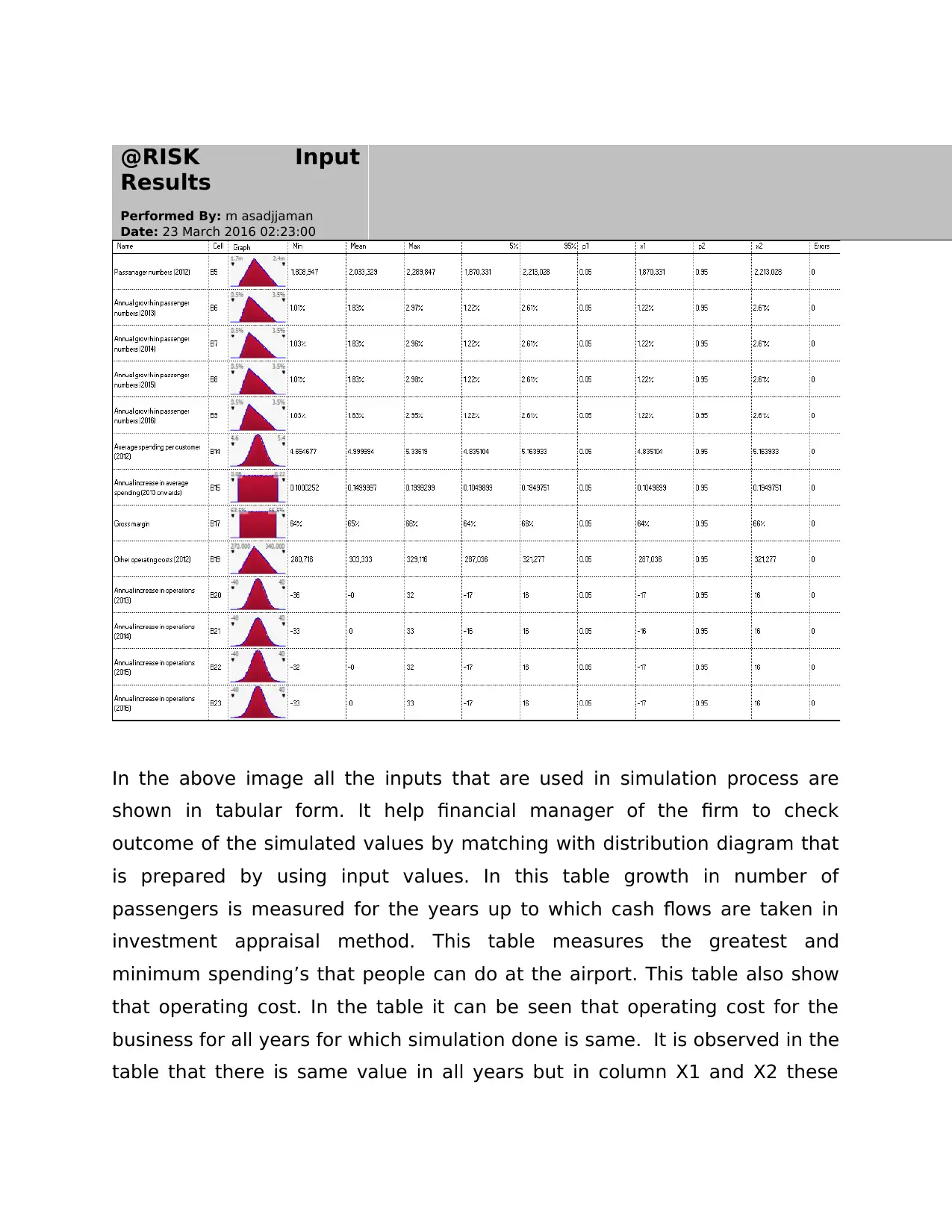

In the above image all the inputs that are used in simulation process are

shown in tabular form. It help financial manager of the firm to check

outcome of the simulated values by matching with distribution diagram that

is prepared by using input values. In this table growth in number of

passengers is measured for the years up to which cash flows are taken in

investment appraisal method. This table measures the greatest and

minimum spending’s that people can do at the airport. This table also show

that operating cost. In the table it can be seen that operating cost for the

business for all years for which simulation done is same. It is observed in the

table that there is same value in all years but in column X1 and X2 these

Results

Performed By: m asadjjaman

Date: 23 March 2016 02:23:00

In the above image all the inputs that are used in simulation process are

shown in tabular form. It help financial manager of the firm to check

outcome of the simulated values by matching with distribution diagram that

is prepared by using input values. In this table growth in number of

passengers is measured for the years up to which cash flows are taken in

investment appraisal method. This table measures the greatest and

minimum spending’s that people can do at the airport. This table also show

that operating cost. In the table it can be seen that operating cost for the

business for all years for which simulation done is same. It is observed in the

table that there is same value in all years but in column X1 and X2 these

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

values are totally different from each other. Apart from this, everything is

same in all remaining columns of table.

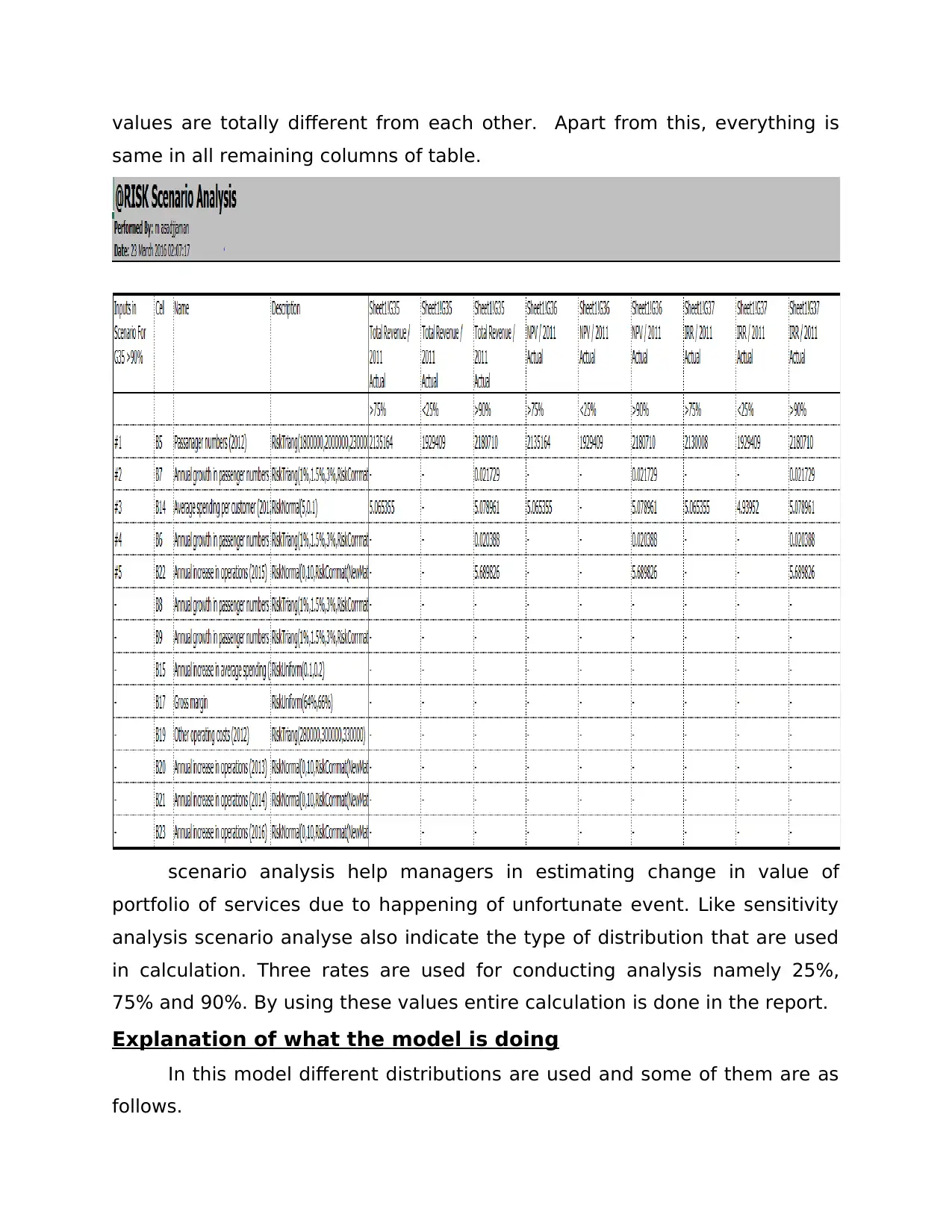

scenario analysis help managers in estimating change in value of

portfolio of services due to happening of unfortunate event. Like sensitivity

analysis scenario analyse also indicate the type of distribution that are used

in calculation. Three rates are used for conducting analysis namely 25%,

75% and 90%. By using these values entire calculation is done in the report.

Explanation of what the model is doing

In this model different distributions are used and some of them are as

follows.

same in all remaining columns of table.

scenario analysis help managers in estimating change in value of

portfolio of services due to happening of unfortunate event. Like sensitivity

analysis scenario analyse also indicate the type of distribution that are used

in calculation. Three rates are used for conducting analysis namely 25%,

75% and 90%. By using these values entire calculation is done in the report.

Explanation of what the model is doing

In this model different distributions are used and some of them are as

follows.

Probability distribution- It helps in measuring uncertainty in the all

variables of the risk analysis (Bielecki. and Rutkowski, 2013).

Normal distribution- it indicate the mean value of the variable and

standard deviation in the variable value from mean.

Uniform distribution- It indicate the values that have equal chance

of occurrence.

Model limitations

The main limitation of this model is that everyone can not apply this

model. Only person that have good knowledge can apply this model

(Wilmott, 2013). Hence, it can be said that this technique is very complex

and it is its main limitation.

CONCLUSION

On the basis of above discussion it is concluded that managers must

different financial modeling techniques in order to select most viable project

for the business. By using these methods various aspects of project can be

measured and good decision can be taken by the manager.

variables of the risk analysis (Bielecki. and Rutkowski, 2013).

Normal distribution- it indicate the mean value of the variable and

standard deviation in the variable value from mean.

Uniform distribution- It indicate the values that have equal chance

of occurrence.

Model limitations

The main limitation of this model is that everyone can not apply this

model. Only person that have good knowledge can apply this model

(Wilmott, 2013). Hence, it can be said that this technique is very complex

and it is its main limitation.

CONCLUSION

On the basis of above discussion it is concluded that managers must

different financial modeling techniques in order to select most viable project

for the business. By using these methods various aspects of project can be

measured and good decision can be taken by the manager.

REFRENCES

Books & journals

Andersen, T.G., Bollerslev, T. and Diebold, F.X., 2007. Roughing it up:

Including jump components in the measurement, modeling, and

forecasting of return volatility. The review of economics and statistics.

89(4). pp.701-720.

Bielecki, T.R. and Rutkowski, M., 2013. Credit risk: modeling, valuation and

hedging. Springer Science & Business Media.

Wilmott, P., 2013. Paul Wilmott on quantitative finance. John Wiley & Sons.

Zivot, E. and Wang, J., 2007. Modeling financial time series with S-Plus® (Vol.

191). Springer Science & Business Media.

Online

Example models. 2016. [Online]. Available through: <

http://www.palisade.com/models/finance.asp>. [Accessed on 23rd March

2016].

Books & journals

Andersen, T.G., Bollerslev, T. and Diebold, F.X., 2007. Roughing it up:

Including jump components in the measurement, modeling, and

forecasting of return volatility. The review of economics and statistics.

89(4). pp.701-720.

Bielecki, T.R. and Rutkowski, M., 2013. Credit risk: modeling, valuation and

hedging. Springer Science & Business Media.

Wilmott, P., 2013. Paul Wilmott on quantitative finance. John Wiley & Sons.

Zivot, E. and Wang, J., 2007. Modeling financial time series with S-Plus® (Vol.

191). Springer Science & Business Media.

Online

Example models. 2016. [Online]. Available through: <

http://www.palisade.com/models/finance.asp>. [Accessed on 23rd March

2016].

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.