Comprehensive Financial Analysis Report: Client Investments

VerifiedAdded on 2022/11/30

|5

|535

|139

Report

AI Summary

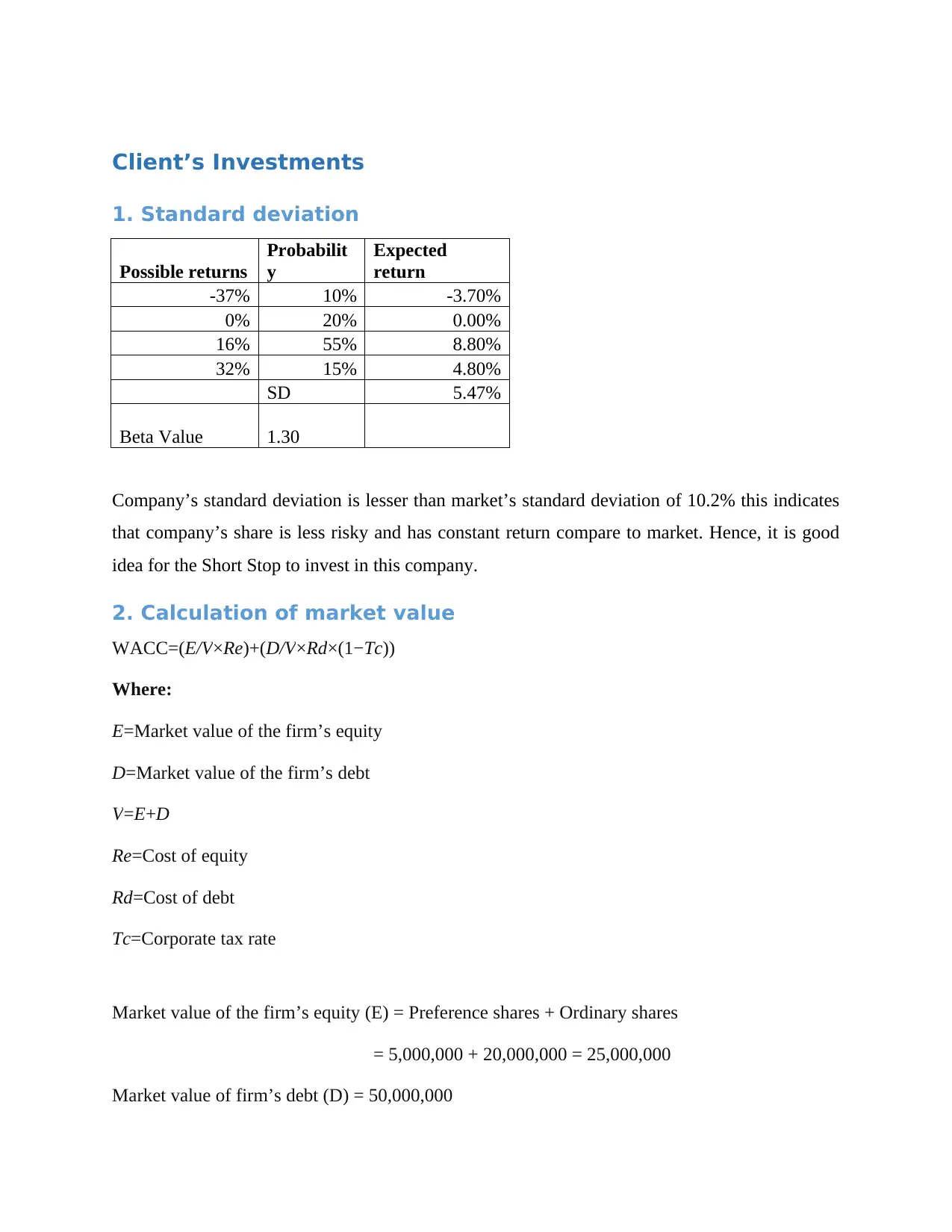

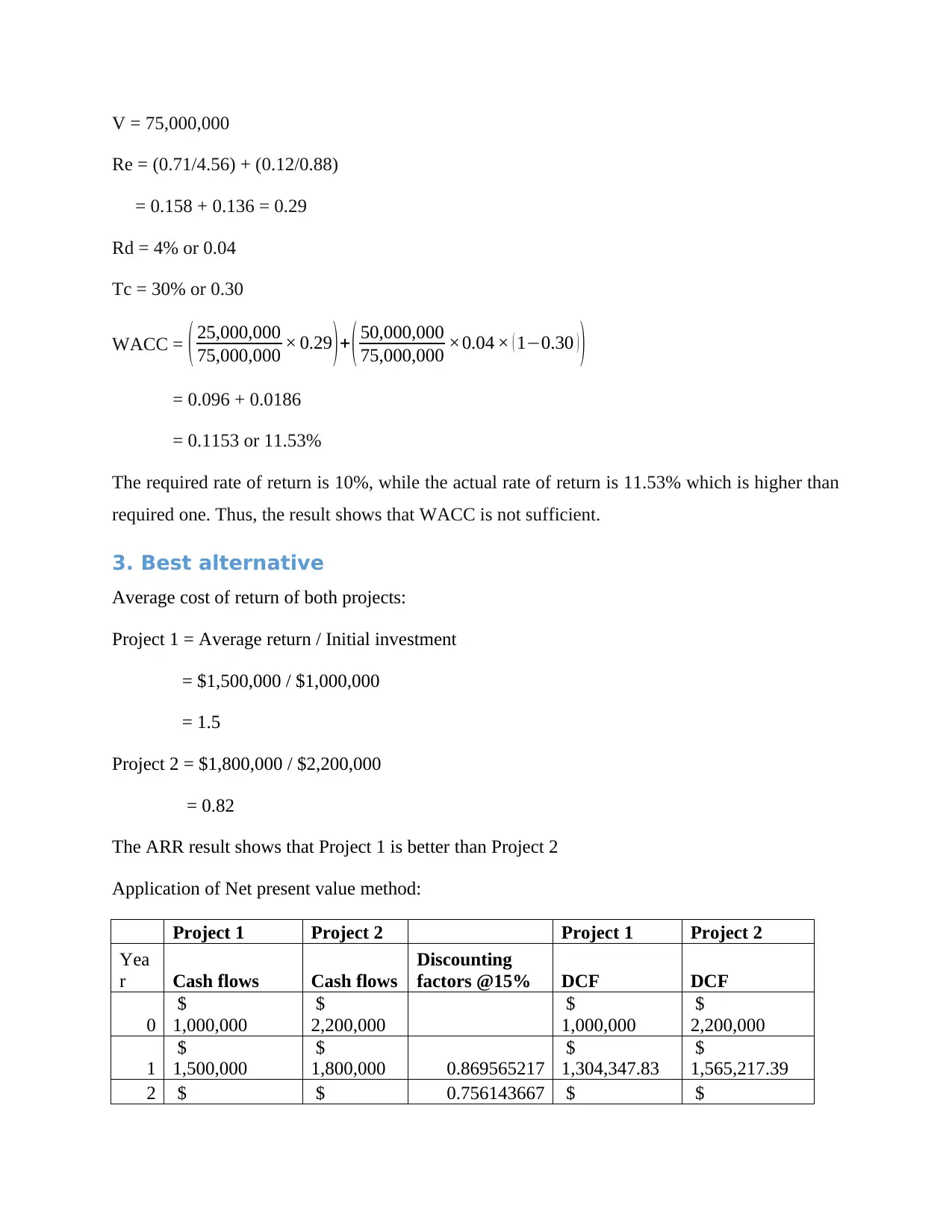

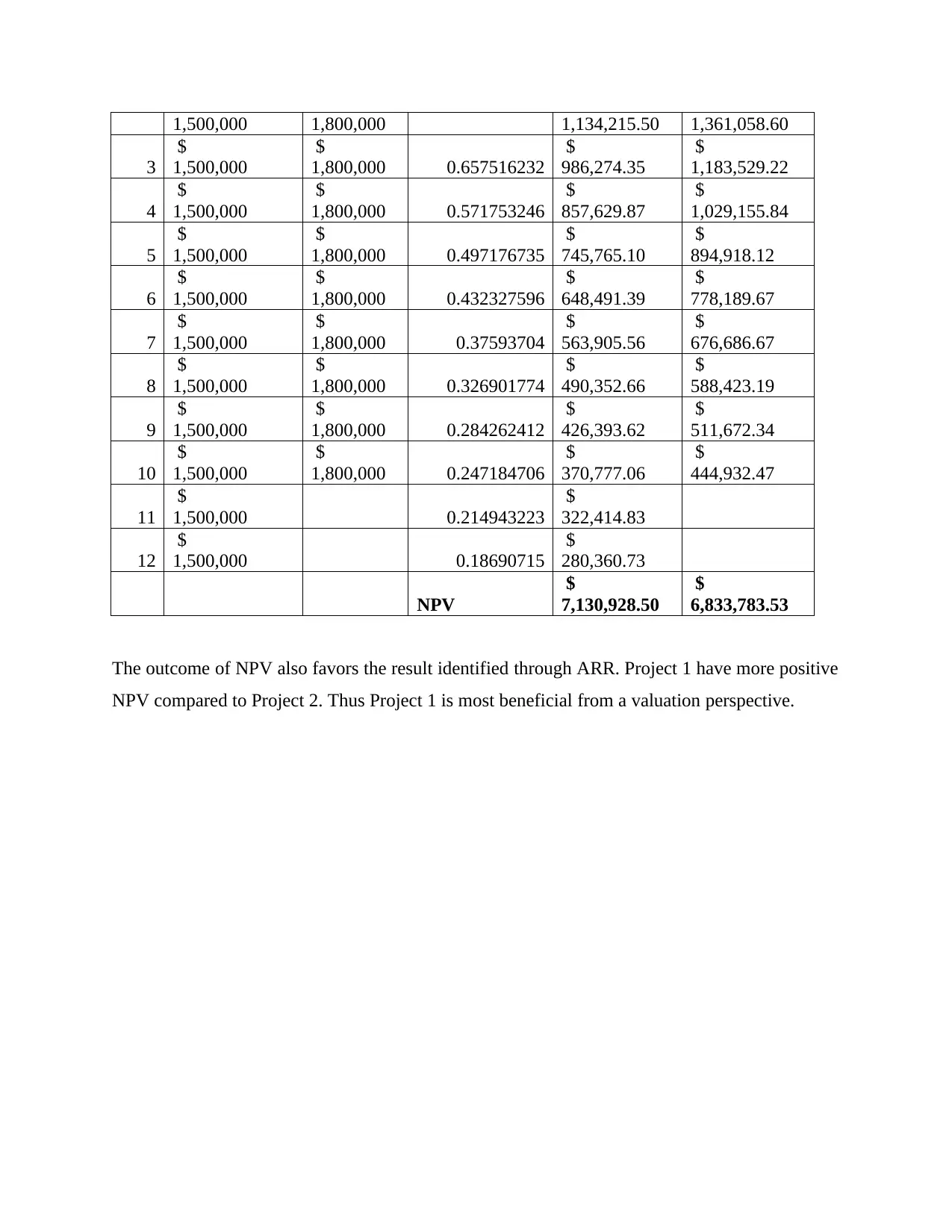

This report provides a financial analysis of a client's investments, focusing on standard deviation, market value calculation, and the evaluation of investment alternatives. The analysis begins with a calculation of standard deviation to assess the risk associated with a company's shares, comparing it to the market's standard deviation to determine its suitability for investment. It then calculates the weighted average cost of capital (WACC) to assess the financial viability of the investment, concluding that the WACC is not sufficient based on the required and actual rates of return. Finally, the report compares two potential projects using the average rate of return (ARR) and net present value (NPV) methods. The ARR analysis suggests Project 1 is superior, a conclusion reinforced by the NPV analysis, which shows Project 1 having a more positive NPV, thus making it the most beneficial from a valuation perspective. The report uses financial data to support its conclusions, providing a clear framework for investment decision-making.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.