Analysis of Financial Performance in Malaysian Retail Sector

VerifiedAdded on 2023/06/03

|20

|3968

|196

AI Summary

The report evaluates investment opportunities in the Malaysian retail sector by analysing the financial condition of Atlan Holdings Berhad and Hai-O-Enterprise Berhad using ratio analysis. It also provides suggestions for changes in financial strategy and investment recommendations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ANALYSIS OF FINANCIAL PERFORMANCE

Analysis of Financial Performance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Analysis of Financial Performance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ANALYSIS OF FINANCIAL PERFORMANCE

Executive Summary:

The report is prepared for evaluating the investment opportunities in the Malaysian retail sector for which

two organisations listed in Bursa Malaysia are chosen. These organisations include Atlan Holdings

Berhad and Hai-O-Enterprise Berhad. It has been found out that Hai-O-Enterprise Berhad has better

financial condition than Atlan Holdings Berhad because of improved profitability, efficiency and leverage

positions. On the other hand, it is found that Atlan is struggling to maintain its competitive position in the

Malaysian retail sector in contrast to Hai-O-Enterprise Berhad due to declining profitability and increased

blockage of working capital in the form of trade receivables. Moreover, the share price analysis clearly

indicates that Hai-O-Enterprise is a better investment opportunity for the investors, as investing in the

shares of the organisation would maximise their overall return on investment.

Executive Summary:

The report is prepared for evaluating the investment opportunities in the Malaysian retail sector for which

two organisations listed in Bursa Malaysia are chosen. These organisations include Atlan Holdings

Berhad and Hai-O-Enterprise Berhad. It has been found out that Hai-O-Enterprise Berhad has better

financial condition than Atlan Holdings Berhad because of improved profitability, efficiency and leverage

positions. On the other hand, it is found that Atlan is struggling to maintain its competitive position in the

Malaysian retail sector in contrast to Hai-O-Enterprise Berhad due to declining profitability and increased

blockage of working capital in the form of trade receivables. Moreover, the share price analysis clearly

indicates that Hai-O-Enterprise is a better investment opportunity for the investors, as investing in the

shares of the organisation would maximise their overall return on investment.

2ANALYSIS OF FINANCIAL PERFORMANCE

Table of Contents

Introduction:................................................................................................................................................3

Analysis of the financial statements using ratio analysis:............................................................................3

Changes in the capital structure:..................................................................................................................6

Evaluation of performance from the viewpoint of the creditors:.................................................................7

Suggestions to changes in financial strategy from the viewpoint of CFO:...................................................7

Share price analysis from the perspective of investors:...............................................................................8

Investment recommendation:.......................................................................................................................9

Conclusion:..................................................................................................................................................9

References:................................................................................................................................................10

Appendices:...............................................................................................................................................12

Table of Contents

Introduction:................................................................................................................................................3

Analysis of the financial statements using ratio analysis:............................................................................3

Changes in the capital structure:..................................................................................................................6

Evaluation of performance from the viewpoint of the creditors:.................................................................7

Suggestions to changes in financial strategy from the viewpoint of CFO:...................................................7

Share price analysis from the perspective of investors:...............................................................................8

Investment recommendation:.......................................................................................................................9

Conclusion:..................................................................................................................................................9

References:................................................................................................................................................10

Appendices:...............................................................................................................................................12

3ANALYSIS OF FINANCIAL PERFORMANCE

Introduction:

The current report aims to analyse the financial markets and investment opportunities in

Malaysia. For meeting the purpose of this assignment, two listed companies in Bursa Malaysia have been

chosen and they include Atlan Holdings Berhad and Hai-O Enterprise Berhad. These two organisations

are operating in the Malaysian retail sector having sound reputation in the market. In order to analyse

investment opportunities, ratio analysis is used for evaluating the financial condition of the two selected

organisations. Based on the outcomes, they are evaluated further from the perspectives of the creditors

and capital structure. After such evaluation, suggestions are provided to both the organisations from the

viewpoints of their CFOs. Finally, share price analysis is conducted to provide investment

recommendations in the two organisations.

Analysis of the financial statements using ratio analysis:

For analysing the financial statements of Atlan Holdings Berhad and Hai-O-Enterprise Berhad,

ratio analysis technique is used, as it provides a complete picture of the financial condition of an

organisation (Brigham et al. 2016). The following types of ratios are used for evaluation of the financial

condition of the two above-mentioned organisations:

Liquidity ratios:

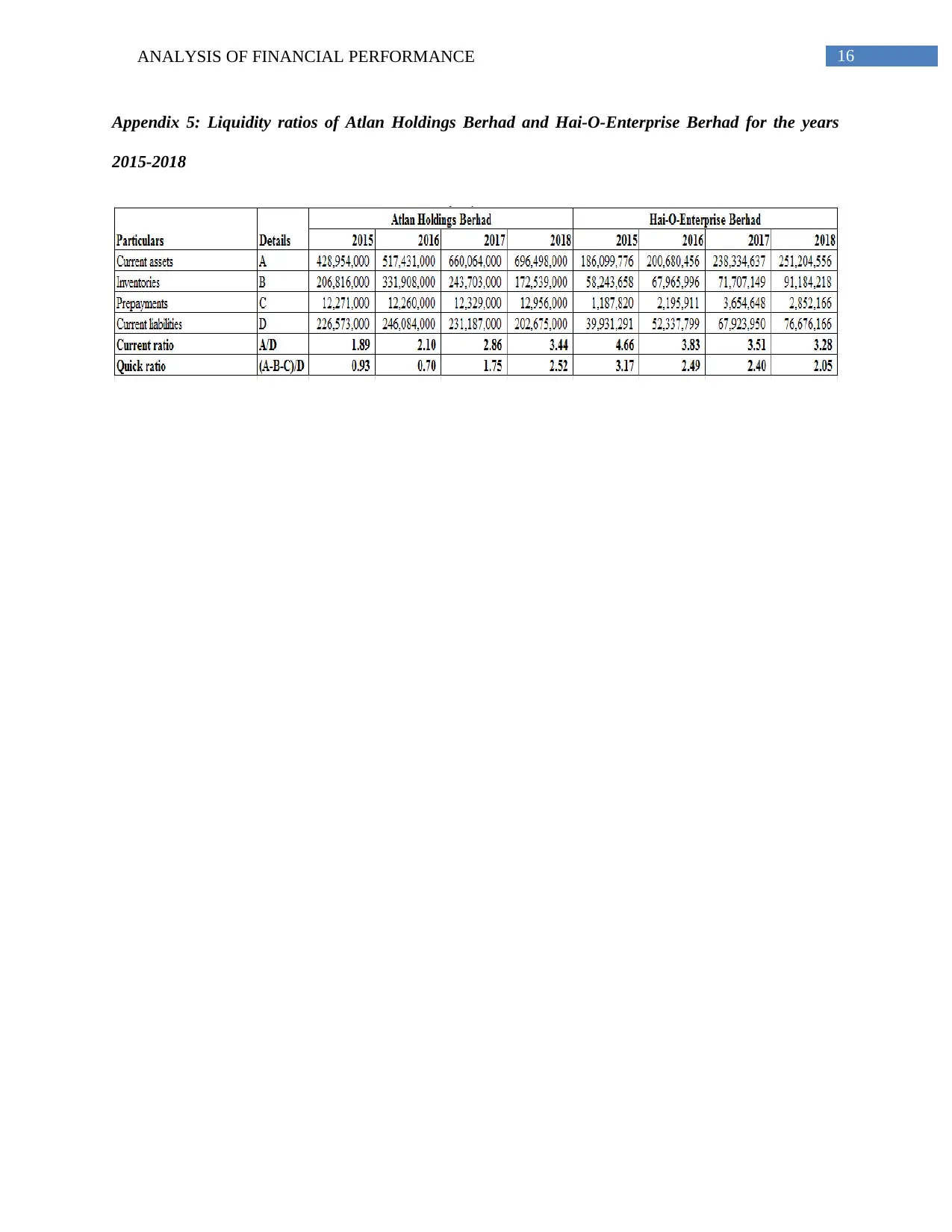

For assessing the liquidity position of Atlan Holdings Berhad and Hai-O-Enterprise Berhad, the

two liquidity ratios used include current ratio and quick ratio (Refer to Appendices, Appendix 5). It has

been found that current ratio is observed to increase from 1.89 in 2015 to 3.44 in 2018 for Atlan Holdings

Berhad, while the same tends to decline from 4.66 in 2015 to 3.28 in 2018. For Atlan, the ratio has

increased due to significant rise in cash and bank balances along with accounts receivable while trade and

other payables have fallen over the years (Atlan.com.my 2018). In case of Hai-O-Enterprise Berhad,

significant rise in trade and other payables is the main reason behind the fall in current ratio. However, it

is noteworthy to mention that the ratio for both companies is well above the ideal standard of 2

Introduction:

The current report aims to analyse the financial markets and investment opportunities in

Malaysia. For meeting the purpose of this assignment, two listed companies in Bursa Malaysia have been

chosen and they include Atlan Holdings Berhad and Hai-O Enterprise Berhad. These two organisations

are operating in the Malaysian retail sector having sound reputation in the market. In order to analyse

investment opportunities, ratio analysis is used for evaluating the financial condition of the two selected

organisations. Based on the outcomes, they are evaluated further from the perspectives of the creditors

and capital structure. After such evaluation, suggestions are provided to both the organisations from the

viewpoints of their CFOs. Finally, share price analysis is conducted to provide investment

recommendations in the two organisations.

Analysis of the financial statements using ratio analysis:

For analysing the financial statements of Atlan Holdings Berhad and Hai-O-Enterprise Berhad,

ratio analysis technique is used, as it provides a complete picture of the financial condition of an

organisation (Brigham et al. 2016). The following types of ratios are used for evaluation of the financial

condition of the two above-mentioned organisations:

Liquidity ratios:

For assessing the liquidity position of Atlan Holdings Berhad and Hai-O-Enterprise Berhad, the

two liquidity ratios used include current ratio and quick ratio (Refer to Appendices, Appendix 5). It has

been found that current ratio is observed to increase from 1.89 in 2015 to 3.44 in 2018 for Atlan Holdings

Berhad, while the same tends to decline from 4.66 in 2015 to 3.28 in 2018. For Atlan, the ratio has

increased due to significant rise in cash and bank balances along with accounts receivable while trade and

other payables have fallen over the years (Atlan.com.my 2018). In case of Hai-O-Enterprise Berhad,

significant rise in trade and other payables is the main reason behind the fall in current ratio. However, it

is noteworthy to mention that the ratio for both companies is well above the ideal standard of 2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ANALYSIS OF FINANCIAL PERFORMANCE

(Buehlmaier and Whited 2018). This implies that both organisations have large amount of idle cash,

which could not be invested to improve existing business operations.

The same trends are observed in case of quick ratio, which is a better measure of liquidity, as it

excludes prepayments and inventories while analysing the liquidity position of an organisation

(Damodaran 2016). In case of Atlan Holdings Berhad, it has minimised its stock holdings over the year,

while Hai-O-Enterprise Berhad has increased its inventory base. Therefore, both the organisations are

needed to minimise their trade receivables so as to increase their cash and bank balances.

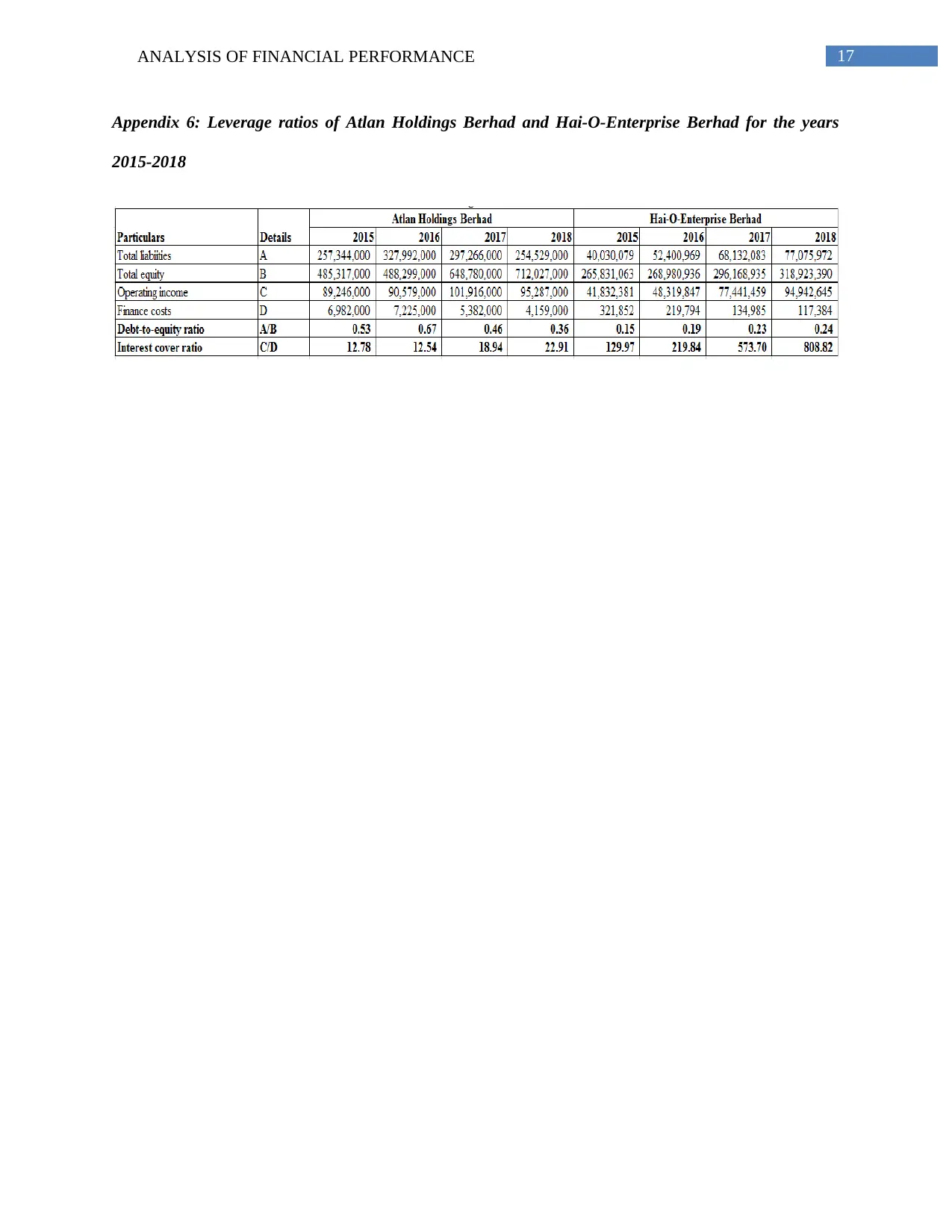

Leverage ratios:

In order to dissect the leverage position of Atlan Holdings Berhad and Hai-O-Enterprise Berhad,

the two liquidity ratios used include debt-to-equity ratio and interest cover ratio (Refer to Appendices,

Appendix 6). For Atlan, debt-to-equity ratio has increased in 2016 after which decline could be observed

consecutively in the next two years. The reason is that the organisation has minimised its debt funding for

avoiding interest payments and it has issued additional equity shares to obtain more funds from the

market. For Hai-O-Enterprise Berhad, ratio has increased over the years from 0.15 in 2015 to 0.24 in

2018 (Hai-o.com.my 2018). However, the ratio is still lower than Atlan, as it has focused on increasing its

retained earnings for future investment operations. A lower ratio is always favourable, as it denotes less

risky position of the organisation (Dokas, Giokas and Tsamis 2014).

On the other hand, interest cover ratio helps in determining whether an organisation possesses the

capability of supporting additional debt. In case of Atlan, the ratio has increased from 12.78 in 2015 to

22.91 in 2018 and for Hai-O-Enterprise; the ratio is significantly higher from 129.97 in 2015 to 808.82 in

2018. The ratio for both the organisations is well above the ideal standard of 1, which denotes that they

have adequate amount of money for settling their interest payments on debt. Therefore, in terms of

leverage, Hai-O-Enterprise has better leverage position than Atlan in the Malaysian retail sector.

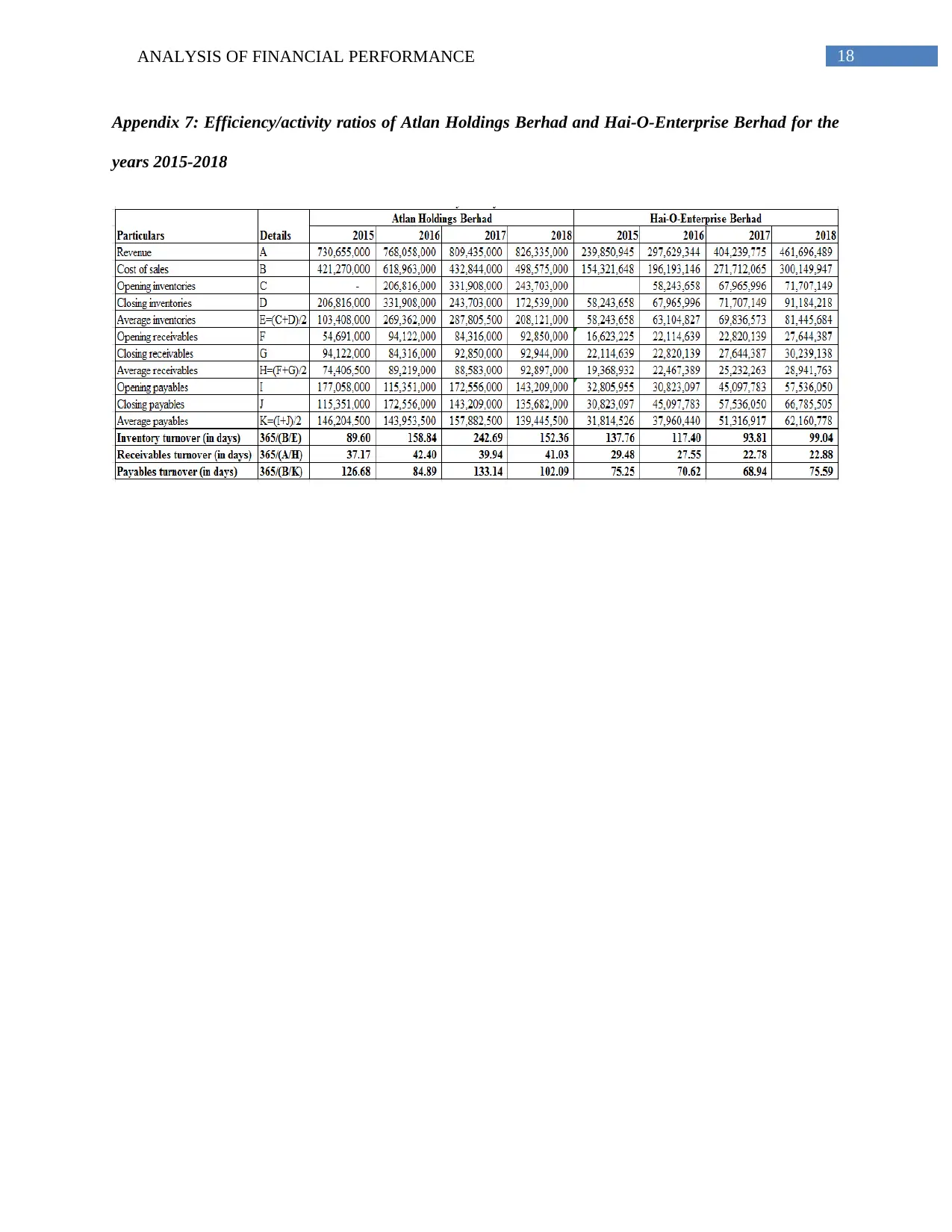

Efficiency/activity ratios:

In order to dissect the efficiency position of Atlan Holdings Berhad and Hai-O-Enterprise

Berhad, the three liquidity ratios used include inventory turnover, receivables turnover and payables

(Buehlmaier and Whited 2018). This implies that both organisations have large amount of idle cash,

which could not be invested to improve existing business operations.

The same trends are observed in case of quick ratio, which is a better measure of liquidity, as it

excludes prepayments and inventories while analysing the liquidity position of an organisation

(Damodaran 2016). In case of Atlan Holdings Berhad, it has minimised its stock holdings over the year,

while Hai-O-Enterprise Berhad has increased its inventory base. Therefore, both the organisations are

needed to minimise their trade receivables so as to increase their cash and bank balances.

Leverage ratios:

In order to dissect the leverage position of Atlan Holdings Berhad and Hai-O-Enterprise Berhad,

the two liquidity ratios used include debt-to-equity ratio and interest cover ratio (Refer to Appendices,

Appendix 6). For Atlan, debt-to-equity ratio has increased in 2016 after which decline could be observed

consecutively in the next two years. The reason is that the organisation has minimised its debt funding for

avoiding interest payments and it has issued additional equity shares to obtain more funds from the

market. For Hai-O-Enterprise Berhad, ratio has increased over the years from 0.15 in 2015 to 0.24 in

2018 (Hai-o.com.my 2018). However, the ratio is still lower than Atlan, as it has focused on increasing its

retained earnings for future investment operations. A lower ratio is always favourable, as it denotes less

risky position of the organisation (Dokas, Giokas and Tsamis 2014).

On the other hand, interest cover ratio helps in determining whether an organisation possesses the

capability of supporting additional debt. In case of Atlan, the ratio has increased from 12.78 in 2015 to

22.91 in 2018 and for Hai-O-Enterprise; the ratio is significantly higher from 129.97 in 2015 to 808.82 in

2018. The ratio for both the organisations is well above the ideal standard of 1, which denotes that they

have adequate amount of money for settling their interest payments on debt. Therefore, in terms of

leverage, Hai-O-Enterprise has better leverage position than Atlan in the Malaysian retail sector.

Efficiency/activity ratios:

In order to dissect the efficiency position of Atlan Holdings Berhad and Hai-O-Enterprise

Berhad, the three liquidity ratios used include inventory turnover, receivables turnover and payables

5ANALYSIS OF FINANCIAL PERFORMANCE

turnover ratios (Refer to Appendices, Appendix 7). Inventory turnover for Atlan is observed to increase

from 2015 to 2017; however, it has fallen in 2018. The reason is that the company has reduced its

inventory base in the year 2018 due to which adequate sales could be generated. On the other hand, the

ratio has fallen from 137.76 days in 2015 to 93.81 days in 2017 for Hai-O-Enterprise Berhad; however, it

has risen again to 99.04 days in 2018. This is because the organisation has experienced an increase in cost

of sales due to which excessive focus has been kept on increasing inventory base, which is lower than the

actual market demand. It is evident that despite such increase, Hai-O-Enterprise Berhad is still managing

to release its inventory at a faster rate than Atlan Holdings Berhad.

Receivables turnover ratio helps in identifying the time taken by an organisation to collect the

amounts owed from the debtors (Hoskin, Fizzell and Cherry 2014). The trend is fluctuating for Atlan

Holdings Berhad and in case of Hai-O-Enterprise Berhad, decline could be observed until 2017 with a

slight decrease in 2018. However, the ratio for Hai-O-Enterprise Berhad is comparatively lower than

Atlan Holdings Berhad, as it has adopted a stringent debtor policy in order to maximise its availability of

working capital.

Payables turnover ratio, on the contrary, is an efficiency ratio that assesses the ability of an

organisation in repaying its debts owed to the suppliers and the creditors (Ibn-Homaid and Tijani 2015).

The trend has been fluctuating for Atlan Holdings Limited and in case of Hai-O-Enterprise Berhad, the

ratio has declined until 2017 followed by an increase in the next year. A higher figure is deemed to be

favourable, as it implies that the organisation has managed to retain cash in hand for a longer timeframe.

However, excessive delay in settling creditor payments might result in loss of trust for the creditors and

they might not be willing to extend payments terms in future (Jordan 2014). Thus, in terms of payables

turnover, Hai-O-Enterprise Berhad is enjoying competitive advantage over Atlan Holdings Berhad in the

retail sector of Malaysia.

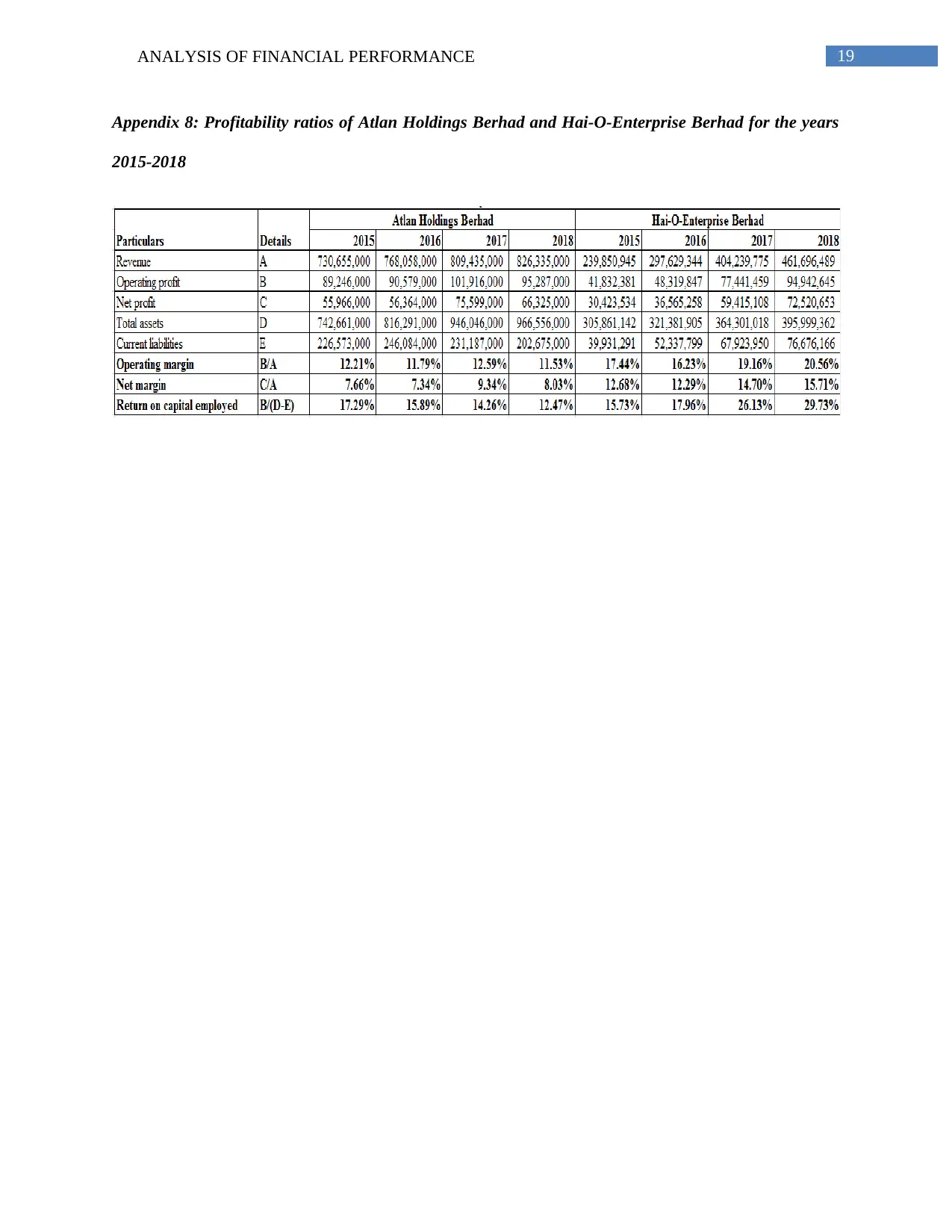

Profitability ratios:

For assessing the profitability position of Atlan Holdings Berhad and Hai-O-Enterprise Berhad,

the two liquidity ratios used include operating margin, net margin and return on capital employed (Refer

turnover ratios (Refer to Appendices, Appendix 7). Inventory turnover for Atlan is observed to increase

from 2015 to 2017; however, it has fallen in 2018. The reason is that the company has reduced its

inventory base in the year 2018 due to which adequate sales could be generated. On the other hand, the

ratio has fallen from 137.76 days in 2015 to 93.81 days in 2017 for Hai-O-Enterprise Berhad; however, it

has risen again to 99.04 days in 2018. This is because the organisation has experienced an increase in cost

of sales due to which excessive focus has been kept on increasing inventory base, which is lower than the

actual market demand. It is evident that despite such increase, Hai-O-Enterprise Berhad is still managing

to release its inventory at a faster rate than Atlan Holdings Berhad.

Receivables turnover ratio helps in identifying the time taken by an organisation to collect the

amounts owed from the debtors (Hoskin, Fizzell and Cherry 2014). The trend is fluctuating for Atlan

Holdings Berhad and in case of Hai-O-Enterprise Berhad, decline could be observed until 2017 with a

slight decrease in 2018. However, the ratio for Hai-O-Enterprise Berhad is comparatively lower than

Atlan Holdings Berhad, as it has adopted a stringent debtor policy in order to maximise its availability of

working capital.

Payables turnover ratio, on the contrary, is an efficiency ratio that assesses the ability of an

organisation in repaying its debts owed to the suppliers and the creditors (Ibn-Homaid and Tijani 2015).

The trend has been fluctuating for Atlan Holdings Limited and in case of Hai-O-Enterprise Berhad, the

ratio has declined until 2017 followed by an increase in the next year. A higher figure is deemed to be

favourable, as it implies that the organisation has managed to retain cash in hand for a longer timeframe.

However, excessive delay in settling creditor payments might result in loss of trust for the creditors and

they might not be willing to extend payments terms in future (Jordan 2014). Thus, in terms of payables

turnover, Hai-O-Enterprise Berhad is enjoying competitive advantage over Atlan Holdings Berhad in the

retail sector of Malaysia.

Profitability ratios:

For assessing the profitability position of Atlan Holdings Berhad and Hai-O-Enterprise Berhad,

the two liquidity ratios used include operating margin, net margin and return on capital employed (Refer

6ANALYSIS OF FINANCIAL PERFORMANCE

to Appendices, Appendix 8). In terms of operating margin, the ratio has been comparatively higher for

Hai-O-Enterprise Berhad, as it has generated income from other sources despite the rise in operating

expenses. On the other hand, Atlan has encountered a considerable increase in raw materials and

consumables used, due to which operating margin has declined in 2018. The situation is found to be

similar for both organisations in terms of net margin as well, which clearly implies that Hai-O-Enterprise

Berhad has generated more profit than Atlan in the Malaysian retail sector. Finally, in terms of return on

capital employed, the ratio has declined over the years for Atlan and the situation is just the opposite for

Hai-O-Enterprise Berhad. This is because the latter has increased its asset base compared to the other,

which resulted in additional return on capital (Miller-Nobles, Mattison and Matsumura 2016). Hence, in

terms of profitability, the position of Hai-O-Enterprise Berhad is found to be better than Atlan in the retail

sector of Malaysia.

Changes in the capital structure:

The capital structure of Atlan Holdings and Hai-O-Enterprise Berhad has been analysed and has

been observed that there have been certain changes in their debt and equity funding proportion. From

analysing the changes in capital structure, it is gathered that there have been certain changes regarding the

ways in which these companies develop growth strategies trough using funds (Zainudin and Hashim

2016). In case of Atlan Holdings it has been observed that the company has made changes in its capital

structure and havedecreased its debt funding in order to avoid its interest payments. This change took

place because of the reason that it issued some additional equity shares in order to attain funds from the

market. However, in case of Hai-O-Enterprise Berhad it has been observed that its capital structure had

changes and focussed on making increased debt funding. However, such change is minor and it does not

indicate that the company can face any financial risk (Vogel 2014). This is because the company is

focussed on increasing its retained earnings for all its future investment business operations.

to Appendices, Appendix 8). In terms of operating margin, the ratio has been comparatively higher for

Hai-O-Enterprise Berhad, as it has generated income from other sources despite the rise in operating

expenses. On the other hand, Atlan has encountered a considerable increase in raw materials and

consumables used, due to which operating margin has declined in 2018. The situation is found to be

similar for both organisations in terms of net margin as well, which clearly implies that Hai-O-Enterprise

Berhad has generated more profit than Atlan in the Malaysian retail sector. Finally, in terms of return on

capital employed, the ratio has declined over the years for Atlan and the situation is just the opposite for

Hai-O-Enterprise Berhad. This is because the latter has increased its asset base compared to the other,

which resulted in additional return on capital (Miller-Nobles, Mattison and Matsumura 2016). Hence, in

terms of profitability, the position of Hai-O-Enterprise Berhad is found to be better than Atlan in the retail

sector of Malaysia.

Changes in the capital structure:

The capital structure of Atlan Holdings and Hai-O-Enterprise Berhad has been analysed and has

been observed that there have been certain changes in their debt and equity funding proportion. From

analysing the changes in capital structure, it is gathered that there have been certain changes regarding the

ways in which these companies develop growth strategies trough using funds (Zainudin and Hashim

2016). In case of Atlan Holdings it has been observed that the company has made changes in its capital

structure and havedecreased its debt funding in order to avoid its interest payments. This change took

place because of the reason that it issued some additional equity shares in order to attain funds from the

market. However, in case of Hai-O-Enterprise Berhad it has been observed that its capital structure had

changes and focussed on making increased debt funding. However, such change is minor and it does not

indicate that the company can face any financial risk (Vogel 2014). This is because the company is

focussed on increasing its retained earnings for all its future investment business operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ANALYSIS OF FINANCIAL PERFORMANCE

Evaluation of performance from the viewpoint of the creditors:

The performance for Atlan Holdings and Hai-O-Enterprise Berhad has been analysed from the

creditors’ point of view. The payables turnover ratio results of these two companies revealed that this

ratio for Atlan Holdings indicates an increasing trend and for Hai-O-Enterprise Berhad Company, this is

observed to be a decreasing trend. In case of Atlan, it can be said that the company is paying its suppliers

in a rapid manner which reveals its improved financial condition (Uechi et al. 2015). The company also

made timely payments after entering into a sales agreement. On the other hand, for Hai-O-Enterprise

Berhad it is evidenced that the company is not that efficient to pay its suppliers on time which signifies its

weakening financial situation. This situation took place as the company’s business activities became slow

and the company is involved in negotiating with its suppliers regarding absorbing some sales and service

tax to deal with weak market condition.

Suggestions to changes in financial strategy from the viewpoint of CFO:

Certain change suggestions regarding financial strategies are offered for Atlan Holdings and Hai-

O-Enterprise Berhad Company in their financial strategies for enhancing their performance position in the

industry. Both the companies recommended shifting its focus from maintaining an increased inventory

and considering maintaining their working capital in cash (Mousa 2015). In case of Atlan Holdings the

company must focus on developing stringent repayment policies for debtors so that they make their

payments on time and do not extend their repayment term on aa regular basis. This can enhance business

everyday business activities of the company.

Evaluation of performance from the viewpoint of the creditors:

The performance for Atlan Holdings and Hai-O-Enterprise Berhad has been analysed from the

creditors’ point of view. The payables turnover ratio results of these two companies revealed that this

ratio for Atlan Holdings indicates an increasing trend and for Hai-O-Enterprise Berhad Company, this is

observed to be a decreasing trend. In case of Atlan, it can be said that the company is paying its suppliers

in a rapid manner which reveals its improved financial condition (Uechi et al. 2015). The company also

made timely payments after entering into a sales agreement. On the other hand, for Hai-O-Enterprise

Berhad it is evidenced that the company is not that efficient to pay its suppliers on time which signifies its

weakening financial situation. This situation took place as the company’s business activities became slow

and the company is involved in negotiating with its suppliers regarding absorbing some sales and service

tax to deal with weak market condition.

Suggestions to changes in financial strategy from the viewpoint of CFO:

Certain change suggestions regarding financial strategies are offered for Atlan Holdings and Hai-

O-Enterprise Berhad Company in their financial strategies for enhancing their performance position in the

industry. Both the companies recommended shifting its focus from maintaining an increased inventory

and considering maintaining their working capital in cash (Mousa 2015). In case of Atlan Holdings the

company must focus on developing stringent repayment policies for debtors so that they make their

payments on time and do not extend their repayment term on aa regular basis. This can enhance business

everyday business activities of the company.

8ANALYSIS OF FINANCIAL PERFORMANCE

Share price analysis from the perspective of investors:

01/01/2014

01/05/2014

01/09/2014

01/01/2015

01/05/2015

01/09/2015

01/01/2016

01/05/2016

01/09/2016

01/01/2017

01/05/2017

01/09/2017

01/01/2018

01/05/2018

01/09/2018

0

1

2

3

4

5

6

Share Price Performance

Share price of Atlan Holdings

Berhad

Share price of Hai-O-Enterprise

Berhad

Figure 1: Share price performance of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the

past four years

(Source: Finance.yahoo.com 2018)

According to the above figure, it has been evaluated that the share price of Atlan has remained

constant for a certain period of time after which it has increased for a smaller timeframe and it has again

declined over the years. However, in case of Hai-O-Enterprise, the trend is observed to be increasing over

time. If the shares of Atlan were purchased in January 2014, the investor would have to incur RM 4.94.

On the current date, the share price of the organisation stands at RM 4.45 and hence, a loss of RM 0.49

would have been incurred. In case of Hai-O-Enterprise, the share price has been RM 1.65 on January

2014, which is now RM 3.60 at the current date and this would lead to a gain of RM 2.95 per share.

Hence, by investing in the shares of Hai-O-Enterprise, the investor could earn profit and the situation is

vice-versa for Atlan.

Share price analysis from the perspective of investors:

01/01/2014

01/05/2014

01/09/2014

01/01/2015

01/05/2015

01/09/2015

01/01/2016

01/05/2016

01/09/2016

01/01/2017

01/05/2017

01/09/2017

01/01/2018

01/05/2018

01/09/2018

0

1

2

3

4

5

6

Share Price Performance

Share price of Atlan Holdings

Berhad

Share price of Hai-O-Enterprise

Berhad

Figure 1: Share price performance of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the

past four years

(Source: Finance.yahoo.com 2018)

According to the above figure, it has been evaluated that the share price of Atlan has remained

constant for a certain period of time after which it has increased for a smaller timeframe and it has again

declined over the years. However, in case of Hai-O-Enterprise, the trend is observed to be increasing over

time. If the shares of Atlan were purchased in January 2014, the investor would have to incur RM 4.94.

On the current date, the share price of the organisation stands at RM 4.45 and hence, a loss of RM 0.49

would have been incurred. In case of Hai-O-Enterprise, the share price has been RM 1.65 on January

2014, which is now RM 3.60 at the current date and this would lead to a gain of RM 2.95 per share.

Hence, by investing in the shares of Hai-O-Enterprise, the investor could earn profit and the situation is

vice-versa for Atlan.

9ANALYSIS OF FINANCIAL PERFORMANCE

Investment recommendation:

The above discussion clearly makes it apparent that Hai-O-Enterprise Berhad is a favourable

investment opportunity for any investor to maximise the level of earnings. This is supported by upward

trend in financial ratios and positive share price performance of the organisation. On the other hand, it is

found that Atlan is struggling to maintain its competitive position in the Malaysian retail sector in contrast

to Hai-O-Enterprise Berhad due to declining profitability and increased blockage of working capital in the

form of trade receivables. Moreover, the share price has declined over the years and therefore, it is

recommended to invest some money in the shares of Hai-O-Enterprise Berhad for maximising return on

investment.

Conclusion:

It is identified from the above evaluation that Hai-O-Enterprise Berhad has better financial

condition than Atlan Holdings Berhad because of improved profitability, efficiency and leverage

positions. The only deficiency is found in the liquidity position and accordingly, recommendations are

provided from the perspective of CFO. Moreover, the share price analysis clearly indicates that Hai-O-

Enterprise is a better investment opportunity for the investors, as investing in the shares of the

organisation would maximise their overall return on investment.

Investment recommendation:

The above discussion clearly makes it apparent that Hai-O-Enterprise Berhad is a favourable

investment opportunity for any investor to maximise the level of earnings. This is supported by upward

trend in financial ratios and positive share price performance of the organisation. On the other hand, it is

found that Atlan is struggling to maintain its competitive position in the Malaysian retail sector in contrast

to Hai-O-Enterprise Berhad due to declining profitability and increased blockage of working capital in the

form of trade receivables. Moreover, the share price has declined over the years and therefore, it is

recommended to invest some money in the shares of Hai-O-Enterprise Berhad for maximising return on

investment.

Conclusion:

It is identified from the above evaluation that Hai-O-Enterprise Berhad has better financial

condition than Atlan Holdings Berhad because of improved profitability, efficiency and leverage

positions. The only deficiency is found in the liquidity position and accordingly, recommendations are

provided from the perspective of CFO. Moreover, the share price analysis clearly indicates that Hai-O-

Enterprise is a better investment opportunity for the investors, as investing in the shares of the

organisation would maximise their overall return on investment.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ANALYSIS OF FINANCIAL PERFORMANCE

References:

Atlan.com.my., 2018. Atlan Holdings Bhd. [online] Available at:

http://www.atlan.com.my/annualreport.html [Accessed 1 Nov. 2018].

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment: Theory And

Practice, Canadian Edition. Nelson Education.

Buehlmaier, M.M. and Whited, T.M., 2018. Are financial constraints priced? Evidence from textual

analysis. The Review of Financial Studies, 31(7), pp.2693-2728.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a financial ratio

based on data envelopment analysis. International Journal of Corporate Finance and Accounting

(IJCFA), 1(1), pp.40-59.

Finance.yahoo.com., 2018. [online] Available at: https://finance.yahoo.com/quote/7668.KL/ [Accessed 1

Nov. 2018].

Finance.yahoo.com., 2018. [online] Available at: https://finance.yahoo.com/quote/7048.KL/ [Accessed 1

Nov. 2018].

Hai-o.com.my., 2018. Hai-O Enterprise Berhad. [online] Available at:

https://www.hai-o.com.my/bursa.php [Accessed 1 Nov. 2018].

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective. Wiley

Global Education.

References:

Atlan.com.my., 2018. Atlan Holdings Bhd. [online] Available at:

http://www.atlan.com.my/annualreport.html [Accessed 1 Nov. 2018].

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment: Theory And

Practice, Canadian Edition. Nelson Education.

Buehlmaier, M.M. and Whited, T.M., 2018. Are financial constraints priced? Evidence from textual

analysis. The Review of Financial Studies, 31(7), pp.2693-2728.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a financial ratio

based on data envelopment analysis. International Journal of Corporate Finance and Accounting

(IJCFA), 1(1), pp.40-59.

Finance.yahoo.com., 2018. [online] Available at: https://finance.yahoo.com/quote/7668.KL/ [Accessed 1

Nov. 2018].

Finance.yahoo.com., 2018. [online] Available at: https://finance.yahoo.com/quote/7048.KL/ [Accessed 1

Nov. 2018].

Hai-o.com.my., 2018. Hai-O Enterprise Berhad. [online] Available at:

https://www.hai-o.com.my/bursa.php [Accessed 1 Nov. 2018].

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective. Wiley

Global Education.

11ANALYSIS OF FINANCIAL PERFORMANCE

Ibn-Homaid, N.T. and Tijani, I.A., 2015. Financial analysis of a construction company in Saudi

Arabia. International Journal of Construction Engineering and Management, 4(3), pp.80-86.

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Miller-Nobles, T.L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial & Managerial

Accounting: The Managerial Chapters. Pearson.

Mousa, G.A., 2015. Financial Ratios versus Data Envelopment Analysis: The Efficiency Assessment of

Banking Sector in Bahrain Bourse. International Journal of Business and Statistical Analysis, 2(2), pp.75-

84.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance ratio

analysis of financial markets. Physica A: Statistical Mechanics and its Applications, 421, pp.488-509.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

Ibn-Homaid, N.T. and Tijani, I.A., 2015. Financial analysis of a construction company in Saudi

Arabia. International Journal of Construction Engineering and Management, 4(3), pp.80-86.

Jordan, B., 2014. Fundamentals of investments. McGraw-Hill Higher Education.

Miller-Nobles, T.L., Mattison, B. and Matsumura, E.M., 2016. Horngren's Financial & Managerial

Accounting: The Managerial Chapters. Pearson.

Mousa, G.A., 2015. Financial Ratios versus Data Envelopment Analysis: The Efficiency Assessment of

Banking Sector in Bahrain Bourse. International Journal of Business and Statistical Analysis, 2(2), pp.75-

84.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance ratio

analysis of financial markets. Physica A: Statistical Mechanics and its Applications, 421, pp.488-509.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

12ANALYSIS OF FINANCIAL PERFORMANCE

Appendices:

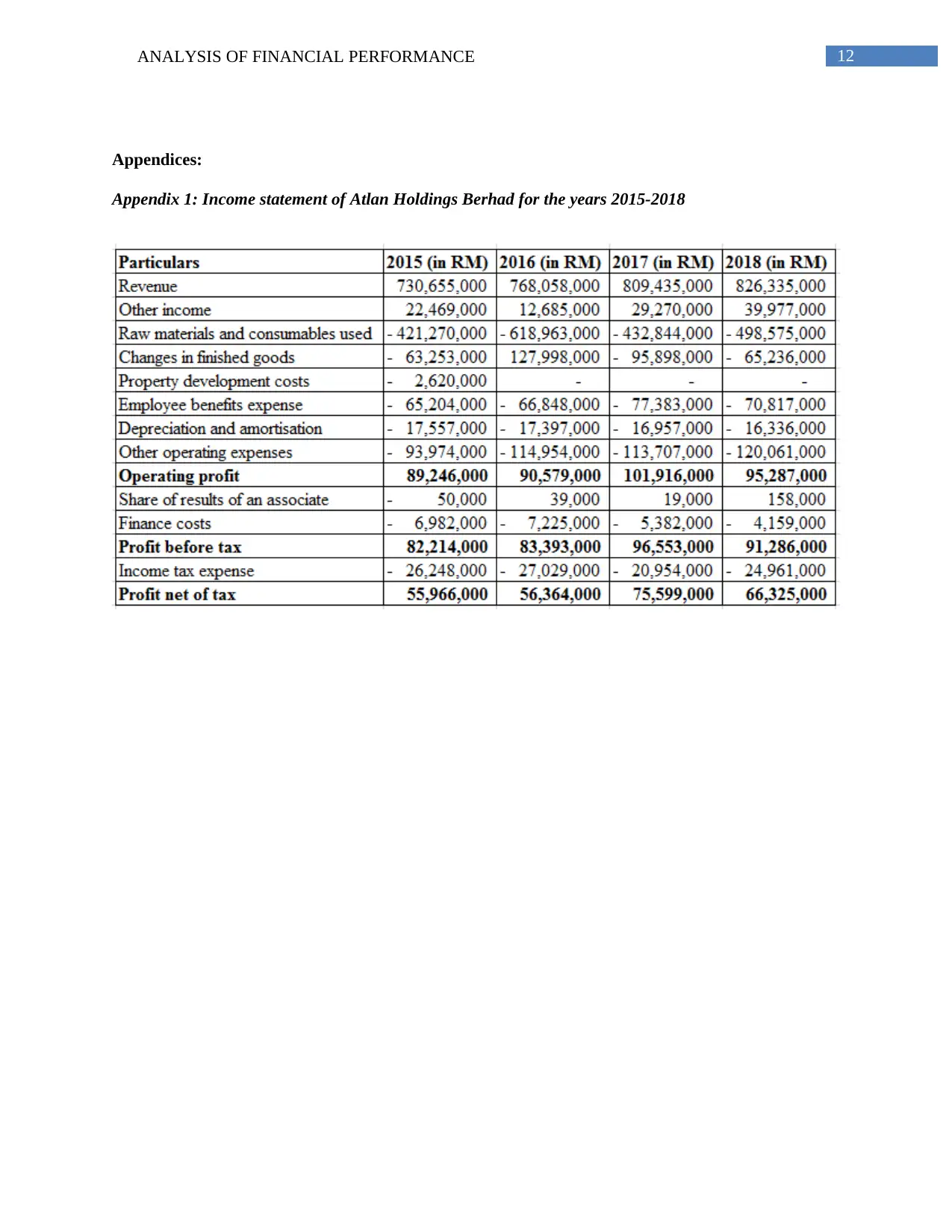

Appendix 1: Income statement of Atlan Holdings Berhad for the years 2015-2018

Appendices:

Appendix 1: Income statement of Atlan Holdings Berhad for the years 2015-2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ANALYSIS OF FINANCIAL PERFORMANCE

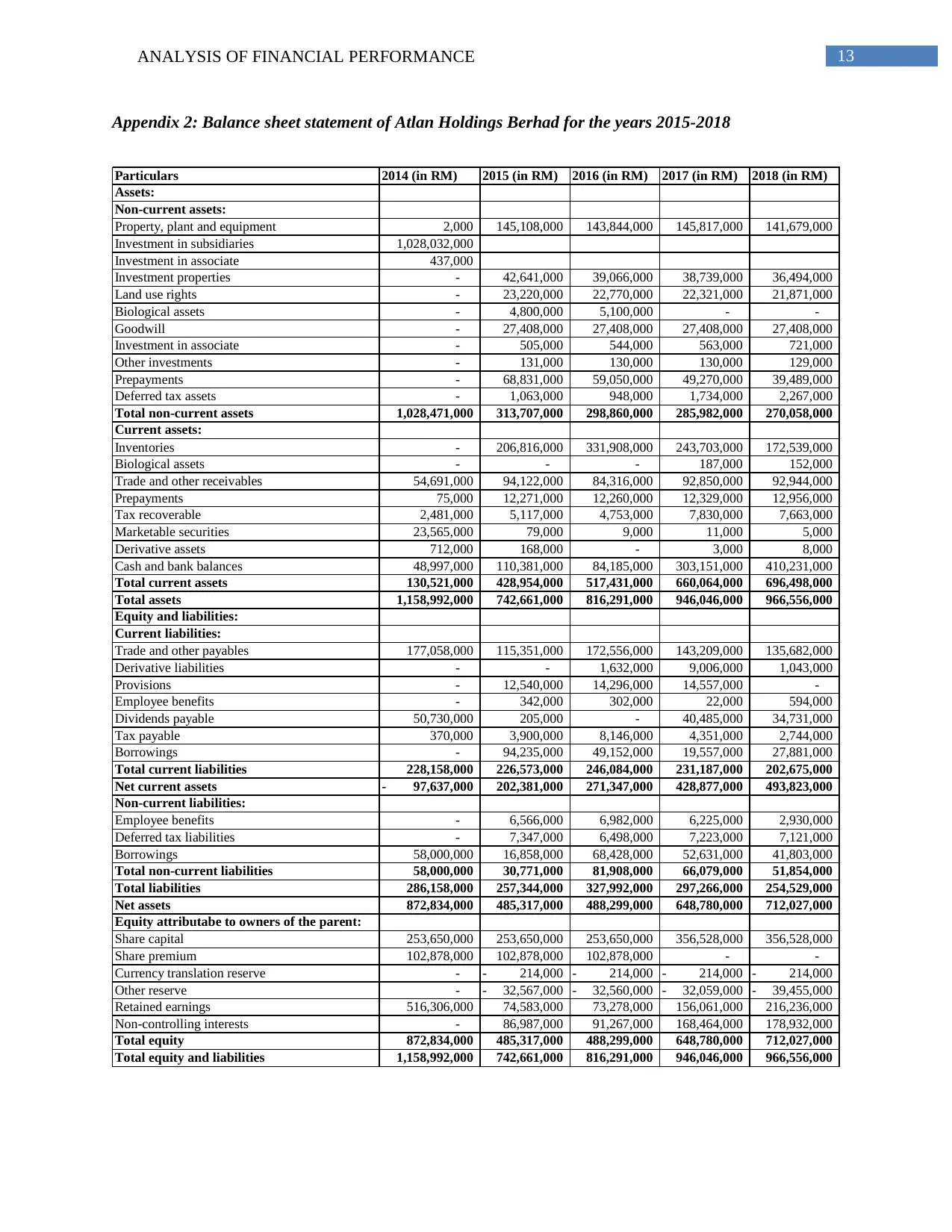

Appendix 2: Balance sheet statement of Atlan Holdings Berhad for the years 2015-2018

Particulars 2014 (in RM) 2015 (in RM) 2016 (in RM) 2017 (in RM) 2018 (in RM)

Assets:

Non-current assets:

Property, plant and equipment 2,000 145,108,000 143,844,000 145,817,000 141,679,000

Investment in subsidiaries 1,028,032,000

Investment in associate 437,000

Investment properties - 42,641,000 39,066,000 38,739,000 36,494,000

Land use rights - 23,220,000 22,770,000 22,321,000 21,871,000

Biological assets - 4,800,000 5,100,000 - -

Goodwill - 27,408,000 27,408,000 27,408,000 27,408,000

Investment in associate - 505,000 544,000 563,000 721,000

Other investments - 131,000 130,000 130,000 129,000

Prepayments - 68,831,000 59,050,000 49,270,000 39,489,000

Deferred tax assets - 1,063,000 948,000 1,734,000 2,267,000

Total non-current assets 1,028,471,000 313,707,000 298,860,000 285,982,000 270,058,000

Current assets:

Inventories - 206,816,000 331,908,000 243,703,000 172,539,000

Biological assets - - - 187,000 152,000

Trade and other receivables 54,691,000 94,122,000 84,316,000 92,850,000 92,944,000

Prepayments 75,000 12,271,000 12,260,000 12,329,000 12,956,000

Tax recoverable 2,481,000 5,117,000 4,753,000 7,830,000 7,663,000

Marketable securities 23,565,000 79,000 9,000 11,000 5,000

Derivative assets 712,000 168,000 - 3,000 8,000

Cash and bank balances 48,997,000 110,381,000 84,185,000 303,151,000 410,231,000

Total current assets 130,521,000 428,954,000 517,431,000 660,064,000 696,498,000

Total assets 1,158,992,000 742,661,000 816,291,000 946,046,000 966,556,000

Equity and liabilities:

Current liabilities:

Trade and other payables 177,058,000 115,351,000 172,556,000 143,209,000 135,682,000

Derivative liabilities - - 1,632,000 9,006,000 1,043,000

Provisions - 12,540,000 14,296,000 14,557,000 -

Employee benefits - 342,000 302,000 22,000 594,000

Dividends payable 50,730,000 205,000 - 40,485,000 34,731,000

Tax payable 370,000 3,900,000 8,146,000 4,351,000 2,744,000

Borrowings - 94,235,000 49,152,000 19,557,000 27,881,000

Total current liabilities 228,158,000 226,573,000 246,084,000 231,187,000 202,675,000

Net current assets 97,637,000- 202,381,000 271,347,000 428,877,000 493,823,000

Non-current liabilities:

Employee benefits - 6,566,000 6,982,000 6,225,000 2,930,000

Deferred tax liabilities - 7,347,000 6,498,000 7,223,000 7,121,000

Borrowings 58,000,000 16,858,000 68,428,000 52,631,000 41,803,000

Total non-current liabilities 58,000,000 30,771,000 81,908,000 66,079,000 51,854,000

Total liabilities 286,158,000 257,344,000 327,992,000 297,266,000 254,529,000

Net assets 872,834,000 485,317,000 488,299,000 648,780,000 712,027,000

Equity attributabe to owners of the parent:

Share capital 253,650,000 253,650,000 253,650,000 356,528,000 356,528,000

Share premium 102,878,000 102,878,000 102,878,000 - -

Currency translation reserve - 214,000- 214,000- 214,000- 214,000-

Other reserve - 32,567,000- 32,560,000- 32,059,000- 39,455,000-

Retained earnings 516,306,000 74,583,000 73,278,000 156,061,000 216,236,000

Non-controlling interests - 86,987,000 91,267,000 168,464,000 178,932,000

Total equity 872,834,000 485,317,000 488,299,000 648,780,000 712,027,000

Total equity and liabilities 1,158,992,000 742,661,000 816,291,000 946,046,000 966,556,000

Appendix 2: Balance sheet statement of Atlan Holdings Berhad for the years 2015-2018

Particulars 2014 (in RM) 2015 (in RM) 2016 (in RM) 2017 (in RM) 2018 (in RM)

Assets:

Non-current assets:

Property, plant and equipment 2,000 145,108,000 143,844,000 145,817,000 141,679,000

Investment in subsidiaries 1,028,032,000

Investment in associate 437,000

Investment properties - 42,641,000 39,066,000 38,739,000 36,494,000

Land use rights - 23,220,000 22,770,000 22,321,000 21,871,000

Biological assets - 4,800,000 5,100,000 - -

Goodwill - 27,408,000 27,408,000 27,408,000 27,408,000

Investment in associate - 505,000 544,000 563,000 721,000

Other investments - 131,000 130,000 130,000 129,000

Prepayments - 68,831,000 59,050,000 49,270,000 39,489,000

Deferred tax assets - 1,063,000 948,000 1,734,000 2,267,000

Total non-current assets 1,028,471,000 313,707,000 298,860,000 285,982,000 270,058,000

Current assets:

Inventories - 206,816,000 331,908,000 243,703,000 172,539,000

Biological assets - - - 187,000 152,000

Trade and other receivables 54,691,000 94,122,000 84,316,000 92,850,000 92,944,000

Prepayments 75,000 12,271,000 12,260,000 12,329,000 12,956,000

Tax recoverable 2,481,000 5,117,000 4,753,000 7,830,000 7,663,000

Marketable securities 23,565,000 79,000 9,000 11,000 5,000

Derivative assets 712,000 168,000 - 3,000 8,000

Cash and bank balances 48,997,000 110,381,000 84,185,000 303,151,000 410,231,000

Total current assets 130,521,000 428,954,000 517,431,000 660,064,000 696,498,000

Total assets 1,158,992,000 742,661,000 816,291,000 946,046,000 966,556,000

Equity and liabilities:

Current liabilities:

Trade and other payables 177,058,000 115,351,000 172,556,000 143,209,000 135,682,000

Derivative liabilities - - 1,632,000 9,006,000 1,043,000

Provisions - 12,540,000 14,296,000 14,557,000 -

Employee benefits - 342,000 302,000 22,000 594,000

Dividends payable 50,730,000 205,000 - 40,485,000 34,731,000

Tax payable 370,000 3,900,000 8,146,000 4,351,000 2,744,000

Borrowings - 94,235,000 49,152,000 19,557,000 27,881,000

Total current liabilities 228,158,000 226,573,000 246,084,000 231,187,000 202,675,000

Net current assets 97,637,000- 202,381,000 271,347,000 428,877,000 493,823,000

Non-current liabilities:

Employee benefits - 6,566,000 6,982,000 6,225,000 2,930,000

Deferred tax liabilities - 7,347,000 6,498,000 7,223,000 7,121,000

Borrowings 58,000,000 16,858,000 68,428,000 52,631,000 41,803,000

Total non-current liabilities 58,000,000 30,771,000 81,908,000 66,079,000 51,854,000

Total liabilities 286,158,000 257,344,000 327,992,000 297,266,000 254,529,000

Net assets 872,834,000 485,317,000 488,299,000 648,780,000 712,027,000

Equity attributabe to owners of the parent:

Share capital 253,650,000 253,650,000 253,650,000 356,528,000 356,528,000

Share premium 102,878,000 102,878,000 102,878,000 - -

Currency translation reserve - 214,000- 214,000- 214,000- 214,000-

Other reserve - 32,567,000- 32,560,000- 32,059,000- 39,455,000-

Retained earnings 516,306,000 74,583,000 73,278,000 156,061,000 216,236,000

Non-controlling interests - 86,987,000 91,267,000 168,464,000 178,932,000

Total equity 872,834,000 485,317,000 488,299,000 648,780,000 712,027,000

Total equity and liabilities 1,158,992,000 742,661,000 816,291,000 946,046,000 966,556,000

14ANALYSIS OF FINANCIAL PERFORMANCE

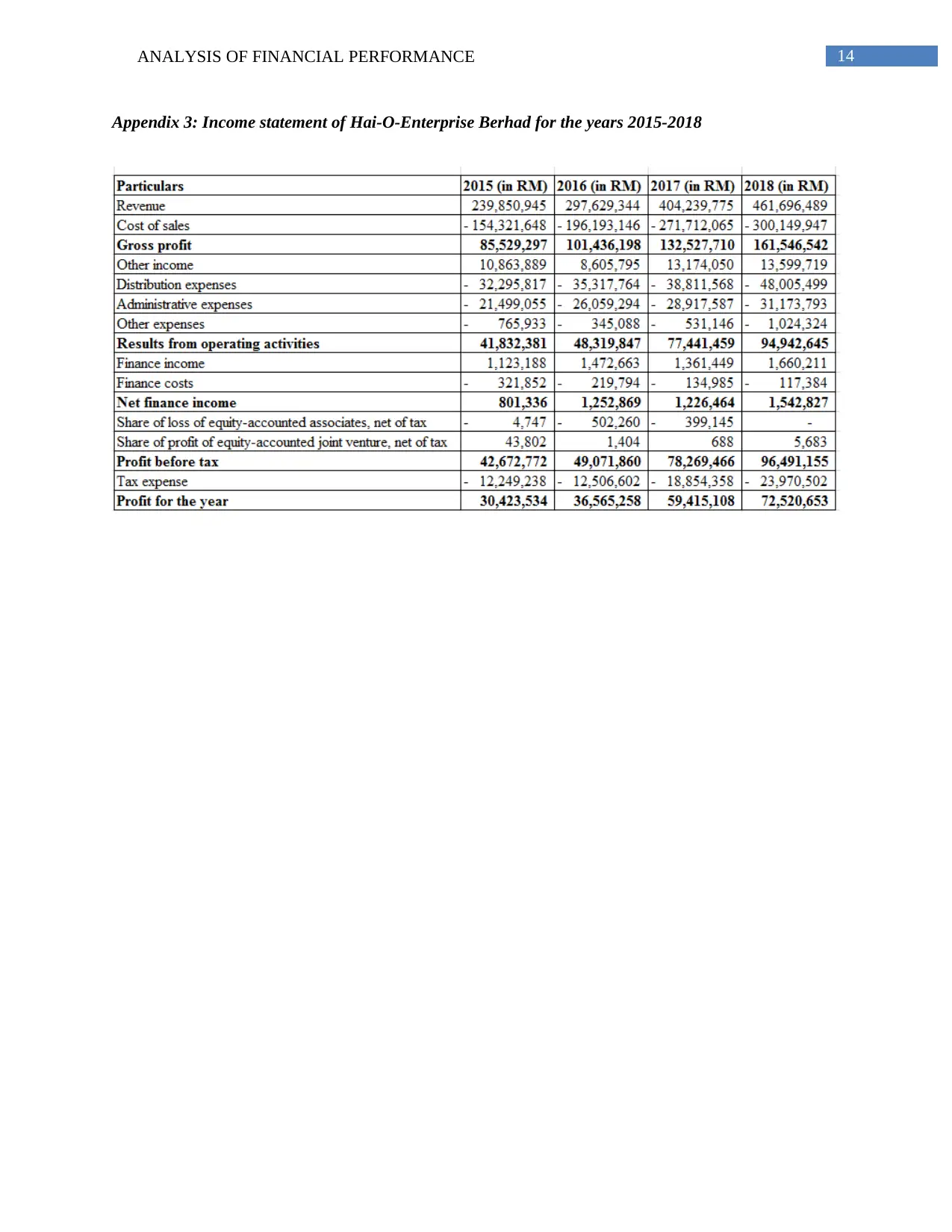

Appendix 3: Income statement of Hai-O-Enterprise Berhad for the years 2015-2018

Appendix 3: Income statement of Hai-O-Enterprise Berhad for the years 2015-2018

15ANALYSIS OF FINANCIAL PERFORMANCE

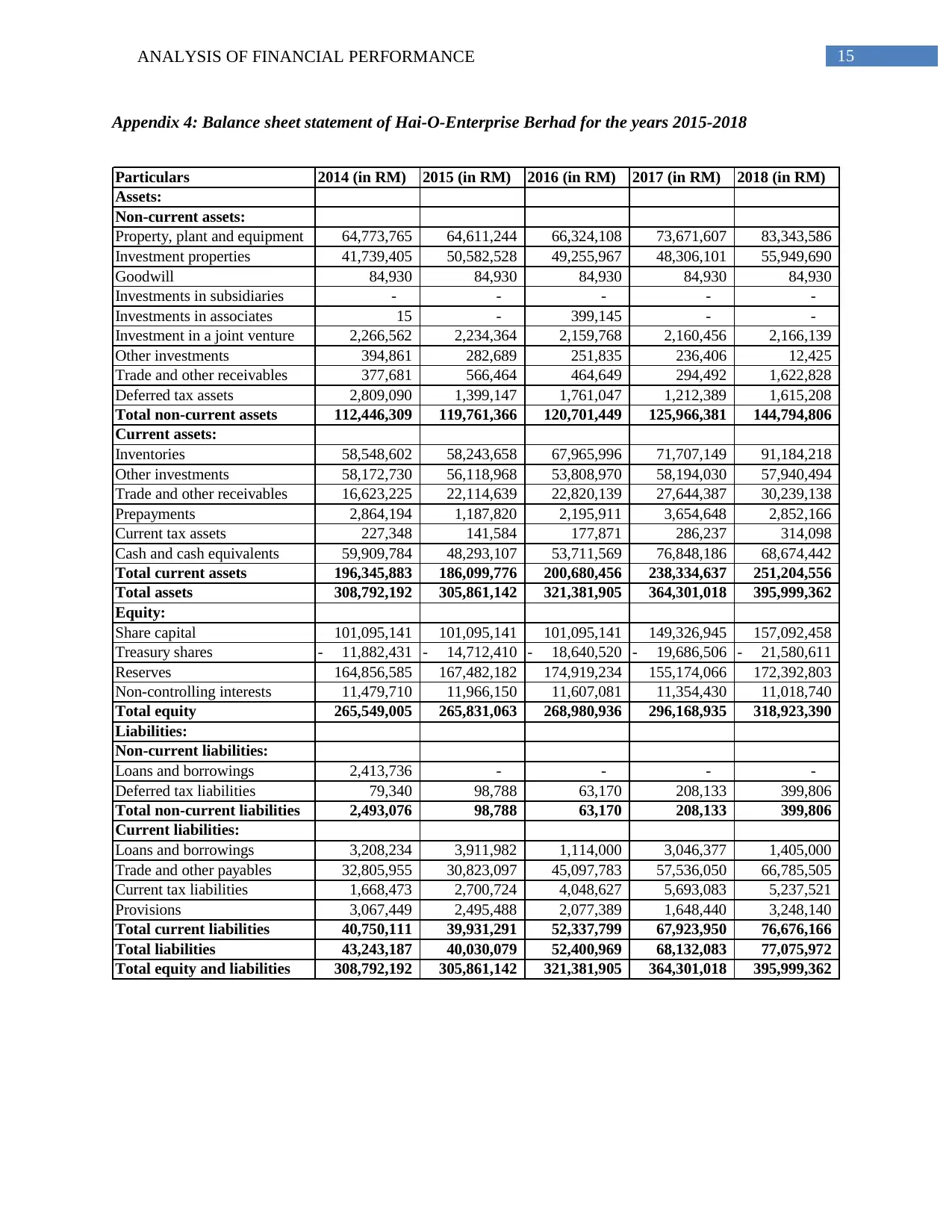

Appendix 4: Balance sheet statement of Hai-O-Enterprise Berhad for the years 2015-2018

Particulars 2014 (in RM) 2015 (in RM) 2016 (in RM) 2017 (in RM) 2018 (in RM)

Assets:

Non-current assets:

Property, plant and equipment 64,773,765 64,611,244 66,324,108 73,671,607 83,343,586

Investment properties 41,739,405 50,582,528 49,255,967 48,306,101 55,949,690

Goodwill 84,930 84,930 84,930 84,930 84,930

Investments in subsidiaries - - - - -

Investments in associates 15 - 399,145 - -

Investment in a joint venture 2,266,562 2,234,364 2,159,768 2,160,456 2,166,139

Other investments 394,861 282,689 251,835 236,406 12,425

Trade and other receivables 377,681 566,464 464,649 294,492 1,622,828

Deferred tax assets 2,809,090 1,399,147 1,761,047 1,212,389 1,615,208

Total non-current assets 112,446,309 119,761,366 120,701,449 125,966,381 144,794,806

Current assets:

Inventories 58,548,602 58,243,658 67,965,996 71,707,149 91,184,218

Other investments 58,172,730 56,118,968 53,808,970 58,194,030 57,940,494

Trade and other receivables 16,623,225 22,114,639 22,820,139 27,644,387 30,239,138

Prepayments 2,864,194 1,187,820 2,195,911 3,654,648 2,852,166

Current tax assets 227,348 141,584 177,871 286,237 314,098

Cash and cash equivalents 59,909,784 48,293,107 53,711,569 76,848,186 68,674,442

Total current assets 196,345,883 186,099,776 200,680,456 238,334,637 251,204,556

Total assets 308,792,192 305,861,142 321,381,905 364,301,018 395,999,362

Equity:

Share capital 101,095,141 101,095,141 101,095,141 149,326,945 157,092,458

Treasury shares 11,882,431- 14,712,410- 18,640,520- 19,686,506- 21,580,611-

Reserves 164,856,585 167,482,182 174,919,234 155,174,066 172,392,803

Non-controlling interests 11,479,710 11,966,150 11,607,081 11,354,430 11,018,740

Total equity 265,549,005 265,831,063 268,980,936 296,168,935 318,923,390

Liabilities:

Non-current liabilities:

Loans and borrowings 2,413,736 - - - -

Deferred tax liabilities 79,340 98,788 63,170 208,133 399,806

Total non-current liabilities 2,493,076 98,788 63,170 208,133 399,806

Current liabilities:

Loans and borrowings 3,208,234 3,911,982 1,114,000 3,046,377 1,405,000

Trade and other payables 32,805,955 30,823,097 45,097,783 57,536,050 66,785,505

Current tax liabilities 1,668,473 2,700,724 4,048,627 5,693,083 5,237,521

Provisions 3,067,449 2,495,488 2,077,389 1,648,440 3,248,140

Total current liabilities 40,750,111 39,931,291 52,337,799 67,923,950 76,676,166

Total liabilities 43,243,187 40,030,079 52,400,969 68,132,083 77,075,972

Total equity and liabilities 308,792,192 305,861,142 321,381,905 364,301,018 395,999,362

Appendix 4: Balance sheet statement of Hai-O-Enterprise Berhad for the years 2015-2018

Particulars 2014 (in RM) 2015 (in RM) 2016 (in RM) 2017 (in RM) 2018 (in RM)

Assets:

Non-current assets:

Property, plant and equipment 64,773,765 64,611,244 66,324,108 73,671,607 83,343,586

Investment properties 41,739,405 50,582,528 49,255,967 48,306,101 55,949,690

Goodwill 84,930 84,930 84,930 84,930 84,930

Investments in subsidiaries - - - - -

Investments in associates 15 - 399,145 - -

Investment in a joint venture 2,266,562 2,234,364 2,159,768 2,160,456 2,166,139

Other investments 394,861 282,689 251,835 236,406 12,425

Trade and other receivables 377,681 566,464 464,649 294,492 1,622,828

Deferred tax assets 2,809,090 1,399,147 1,761,047 1,212,389 1,615,208

Total non-current assets 112,446,309 119,761,366 120,701,449 125,966,381 144,794,806

Current assets:

Inventories 58,548,602 58,243,658 67,965,996 71,707,149 91,184,218

Other investments 58,172,730 56,118,968 53,808,970 58,194,030 57,940,494

Trade and other receivables 16,623,225 22,114,639 22,820,139 27,644,387 30,239,138

Prepayments 2,864,194 1,187,820 2,195,911 3,654,648 2,852,166

Current tax assets 227,348 141,584 177,871 286,237 314,098

Cash and cash equivalents 59,909,784 48,293,107 53,711,569 76,848,186 68,674,442

Total current assets 196,345,883 186,099,776 200,680,456 238,334,637 251,204,556

Total assets 308,792,192 305,861,142 321,381,905 364,301,018 395,999,362

Equity:

Share capital 101,095,141 101,095,141 101,095,141 149,326,945 157,092,458

Treasury shares 11,882,431- 14,712,410- 18,640,520- 19,686,506- 21,580,611-

Reserves 164,856,585 167,482,182 174,919,234 155,174,066 172,392,803

Non-controlling interests 11,479,710 11,966,150 11,607,081 11,354,430 11,018,740

Total equity 265,549,005 265,831,063 268,980,936 296,168,935 318,923,390

Liabilities:

Non-current liabilities:

Loans and borrowings 2,413,736 - - - -

Deferred tax liabilities 79,340 98,788 63,170 208,133 399,806

Total non-current liabilities 2,493,076 98,788 63,170 208,133 399,806

Current liabilities:

Loans and borrowings 3,208,234 3,911,982 1,114,000 3,046,377 1,405,000

Trade and other payables 32,805,955 30,823,097 45,097,783 57,536,050 66,785,505

Current tax liabilities 1,668,473 2,700,724 4,048,627 5,693,083 5,237,521

Provisions 3,067,449 2,495,488 2,077,389 1,648,440 3,248,140

Total current liabilities 40,750,111 39,931,291 52,337,799 67,923,950 76,676,166

Total liabilities 43,243,187 40,030,079 52,400,969 68,132,083 77,075,972

Total equity and liabilities 308,792,192 305,861,142 321,381,905 364,301,018 395,999,362

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16ANALYSIS OF FINANCIAL PERFORMANCE

Appendix 5: Liquidity ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the years

2015-2018

Appendix 5: Liquidity ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the years

2015-2018

17ANALYSIS OF FINANCIAL PERFORMANCE

Appendix 6: Leverage ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the years

2015-2018

Appendix 6: Leverage ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the years

2015-2018

18ANALYSIS OF FINANCIAL PERFORMANCE

Appendix 7: Efficiency/activity ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the

years 2015-2018

Appendix 7: Efficiency/activity ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the

years 2015-2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19ANALYSIS OF FINANCIAL PERFORMANCE

Appendix 8: Profitability ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the years

2015-2018

Appendix 8: Profitability ratios of Atlan Holdings Berhad and Hai-O-Enterprise Berhad for the years

2015-2018

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.