Financial Performance Management: Under Armour vs. Nike Analysis

VerifiedAdded on 2023/06/11

|14

|4336

|328

Report

AI Summary

This report provides a comprehensive financial performance analysis of Under Armour and its closest competitor, Nike, using ratio analysis, a balanced scorecard, and an examination of integrated reporting. The ratio analysis compares the liquidity, working capital, profitability, leverage, and valuation ratios of both companies over two years (2018-2019). The balanced scorecard section critiques the BSC framework and develops a performance evaluation for Under Armour, focusing on financial, customer, internal process, and learning & growth perspectives. The report concludes with a critical analysis of the benefits and challenges of adopting integrated reporting for Under Armour, highlighting the importance of aligning objectives with specific industry segments and customer targets. The analysis draws from financial statements and relevant literature to assess the companies' financial health and strategic positioning.

Financial performance

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1: Financial Performance Using Ratio Analysis..........................................................1

Question 2: Balanced Scorecard..................................................................................................4

Question 3: Integrated Reporting.................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1: Financial Performance Using Ratio Analysis..........................................................1

Question 2: Balanced Scorecard..................................................................................................4

Question 3: Integrated Reporting.................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The analysis is based on a thorough examination of Under Armour's non-financial and

financial performance, and that of its nearest competitor, Nike (Ahmed, Manwani and Ahmed,

2018). Under Armour is a well-known US manufacturer of sports apparel, casual clothing, and

sporting shoes. We chose both of these companies for a financial display relationship since Nike

is the largest participant in the workout gear and apparel industry. The investigation is predicated

on a comprehensive evaluation of the financial ratios of both companies. Comparing at Under

Armour and Nike can help you figure out which company is more financially stable and how

they may benefit by using a balance scorecard and applying marketing strategy into their

business to gain a competitive advantage in the longer run. The report also includes a thorough

examination of the balanced scorecard's effectiveness as a management tool, and also a detailed

discussion of Under Armour's Key Performance Indicators. The Balanced Scorecard is extremely

useful in technique planning and implementation at all stages. It focuses on examining the

previous outcomes of both the financial and customer perspectives to the true reasons in the first

case. It has influenced the outcomes in terms of interior company processes and organisational

ability for development and improvement. The study is also recognized for a thorough

examination of the benefits and challenges of implementing Unified Accounting for Under

Armour.

MAIN BODY

Question 1: Financial Performance Using Ratio Analysis

Under Armour is the primary company chosen for ratio analysis, and its financial

performance is compared to vs. its closest competitor, Nike. Under Armor is a well-known

US manufacturer of sports apparel, casual clothing, and sporting shoes (Alziyadat and Ahmed,

2019). Nike is the largest participant in the workout gear and apparel industry and that is why we

chose both of these companies for a financial report analysis. The financial ratios of Under

Armour and Nike are shown below-

FINANCIAL RATIOS

Particulars Under Armour Nike

2018 2019 2018 2019

Liquidity Ratios

The analysis is based on a thorough examination of Under Armour's non-financial and

financial performance, and that of its nearest competitor, Nike (Ahmed, Manwani and Ahmed,

2018). Under Armour is a well-known US manufacturer of sports apparel, casual clothing, and

sporting shoes. We chose both of these companies for a financial display relationship since Nike

is the largest participant in the workout gear and apparel industry. The investigation is predicated

on a comprehensive evaluation of the financial ratios of both companies. Comparing at Under

Armour and Nike can help you figure out which company is more financially stable and how

they may benefit by using a balance scorecard and applying marketing strategy into their

business to gain a competitive advantage in the longer run. The report also includes a thorough

examination of the balanced scorecard's effectiveness as a management tool, and also a detailed

discussion of Under Armour's Key Performance Indicators. The Balanced Scorecard is extremely

useful in technique planning and implementation at all stages. It focuses on examining the

previous outcomes of both the financial and customer perspectives to the true reasons in the first

case. It has influenced the outcomes in terms of interior company processes and organisational

ability for development and improvement. The study is also recognized for a thorough

examination of the benefits and challenges of implementing Unified Accounting for Under

Armour.

MAIN BODY

Question 1: Financial Performance Using Ratio Analysis

Under Armour is the primary company chosen for ratio analysis, and its financial

performance is compared to vs. its closest competitor, Nike. Under Armor is a well-known

US manufacturer of sports apparel, casual clothing, and sporting shoes (Alziyadat and Ahmed,

2019). Nike is the largest participant in the workout gear and apparel industry and that is why we

chose both of these companies for a financial report analysis. The financial ratios of Under

Armour and Nike are shown below-

FINANCIAL RATIOS

Particulars Under Armour Nike

2018 2019 2018 2019

Liquidity Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

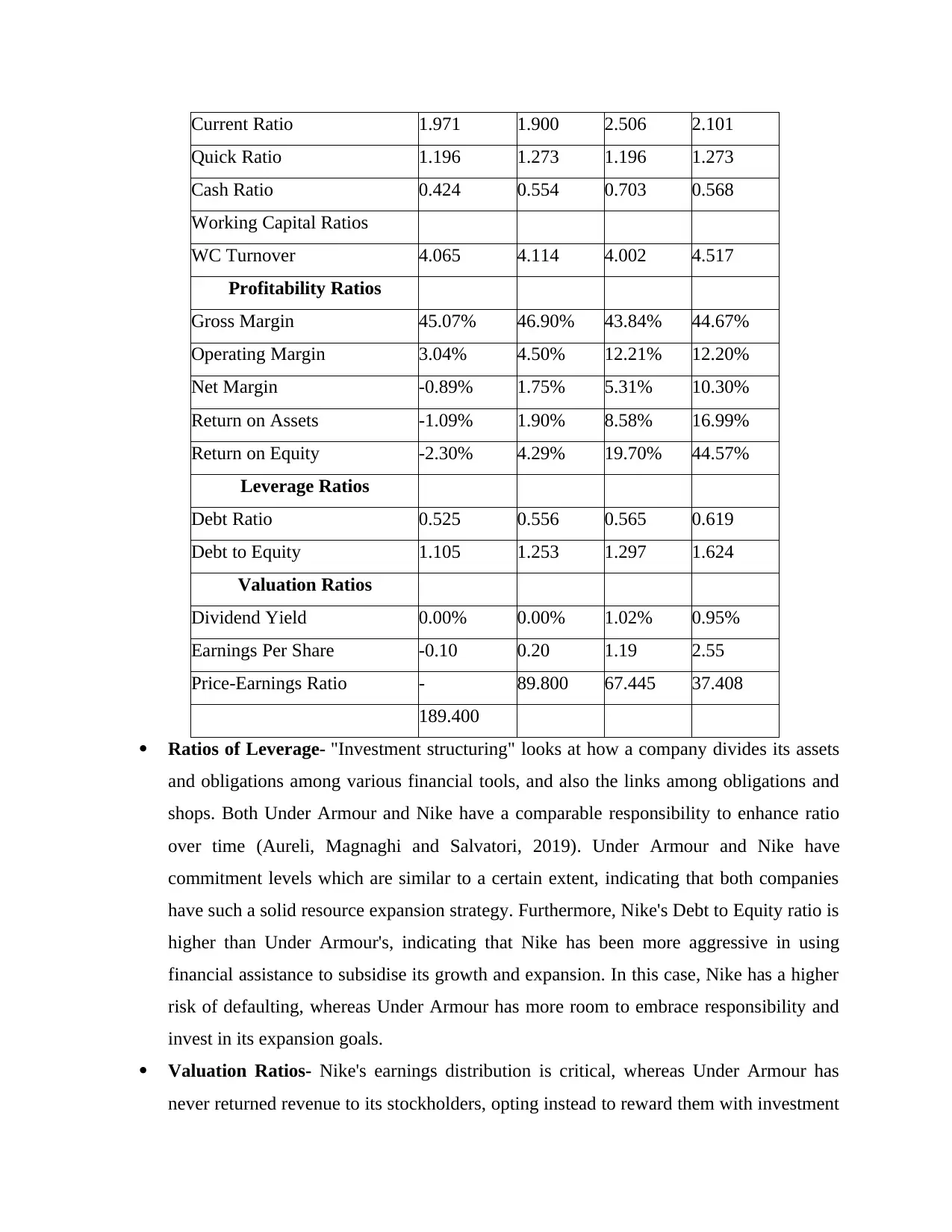

Current Ratio 1.971 1.900 2.506 2.101

Quick Ratio 1.196 1.273 1.196 1.273

Cash Ratio 0.424 0.554 0.703 0.568

Working Capital Ratios

WC Turnover 4.065 4.114 4.002 4.517

Profitability Ratios

Gross Margin 45.07% 46.90% 43.84% 44.67%

Operating Margin 3.04% 4.50% 12.21% 12.20%

Net Margin -0.89% 1.75% 5.31% 10.30%

Return on Assets -1.09% 1.90% 8.58% 16.99%

Return on Equity -2.30% 4.29% 19.70% 44.57%

Leverage Ratios

Debt Ratio 0.525 0.556 0.565 0.619

Debt to Equity 1.105 1.253 1.297 1.624

Valuation Ratios

Dividend Yield 0.00% 0.00% 1.02% 0.95%

Earnings Per Share -0.10 0.20 1.19 2.55

Price-Earnings Ratio - 89.800 67.445 37.408

189.400

Ratios of Leverage- "Investment structuring" looks at how a company divides its assets

and obligations among various financial tools, and also the links among obligations and

shops. Both Under Armour and Nike have a comparable responsibility to enhance ratio

over time (Aureli, Magnaghi and Salvatori, 2019). Under Armour and Nike have

commitment levels which are similar to a certain extent, indicating that both companies

have such a solid resource expansion strategy. Furthermore, Nike's Debt to Equity ratio is

higher than Under Armour's, indicating that Nike has been more aggressive in using

financial assistance to subsidise its growth and expansion. In this case, Nike has a higher

risk of defaulting, whereas Under Armour has more room to embrace responsibility and

invest in its expansion goals.

Valuation Ratios- Nike's earnings distribution is critical, whereas Under Armour has

never returned revenue to its stockholders, opting instead to reward them with investment

Quick Ratio 1.196 1.273 1.196 1.273

Cash Ratio 0.424 0.554 0.703 0.568

Working Capital Ratios

WC Turnover 4.065 4.114 4.002 4.517

Profitability Ratios

Gross Margin 45.07% 46.90% 43.84% 44.67%

Operating Margin 3.04% 4.50% 12.21% 12.20%

Net Margin -0.89% 1.75% 5.31% 10.30%

Return on Assets -1.09% 1.90% 8.58% 16.99%

Return on Equity -2.30% 4.29% 19.70% 44.57%

Leverage Ratios

Debt Ratio 0.525 0.556 0.565 0.619

Debt to Equity 1.105 1.253 1.297 1.624

Valuation Ratios

Dividend Yield 0.00% 0.00% 1.02% 0.95%

Earnings Per Share -0.10 0.20 1.19 2.55

Price-Earnings Ratio - 89.800 67.445 37.408

189.400

Ratios of Leverage- "Investment structuring" looks at how a company divides its assets

and obligations among various financial tools, and also the links among obligations and

shops. Both Under Armour and Nike have a comparable responsibility to enhance ratio

over time (Aureli, Magnaghi and Salvatori, 2019). Under Armour and Nike have

commitment levels which are similar to a certain extent, indicating that both companies

have such a solid resource expansion strategy. Furthermore, Nike's Debt to Equity ratio is

higher than Under Armour's, indicating that Nike has been more aggressive in using

financial assistance to subsidise its growth and expansion. In this case, Nike has a higher

risk of defaulting, whereas Under Armour has more room to embrace responsibility and

invest in its expansion goals.

Valuation Ratios- Nike's earnings distribution is critical, whereas Under Armour has

never returned revenue to its stockholders, opting instead to reward them with investment

recognition. The revenue distribution strategies of the 2 firms are comparable, as

evidenced by their revenue rates. Attributed to the reason that Under Armour does not

generate money, its revenue return is zero, but Nike has a potential revenue return.

Furthermore, the EPS displays how much money buyers earn by investing in the

company. According to the analysis, Nike's EPS is extremely promising, whilst Under

Armour’s EPS has been steadily improving over time. Under Armour's Price-Earnings

Ratio was unfavourable in 2018 as a result of the company's total shortfall (Boyle, Lewis-

Western and Seidel, 2021). Lower transaction growth due to shifting demand in sports

gear, fierce competition, and outlet closures by key suppliers compounded the loss. Yet,

the company made significant progress in 2019, as seen by a similar trajectory in the

company's Price-Earnings ratio. All of Under Armour’s other incentive ratios have

increased dramatically from 2018 to 2019, owing to the company's compensation

announcement shifting from a significant loss to a significant positive.

Ratios of Liquidity- The most common ratios analysed are liquidity levels. It could be

obtained by dividing funds and liquid assets into short-term loans and present obligations.

Major enhancements in the company's excellence of goods and offerings may be

possible. The current and quick ratios of both companies are significantly higher than that

of the standard 1.0, indicating that they will have strong liquidity strength; nevertheless,

Nike outperforms Under Armour in terms of current ratio. In terms of revenue flow,

Under Armour has to strive more to improve its financial condition. This demonstrates

that Under Armour’s long-term share has been falling, whereas its fast-growing share has

already been increasing.

Working Capital Ratios- Nike's working capital overall turnover is significantly greater

than that of Under Armour. Yet, trend analysis suggests that Nike is growing at a

significantly faster pace in terms of working capital turnover. Given this, Under

Armour’s management must adopt some links from Nike's strategy and concentrate on

improving their internal operational competence (Chen, Tan and Fang, 2018).

Profitability Ratios- It was discovered that "The characteristics of financial precision are

linked to an understanding of initial output development in emerging businesses. This is

significant because one of the goals of fiscal reporting is to hold managers accountable to

finance supporters so that investment is allocated efficiently ". In 2018, Under Armour's

evidenced by their revenue rates. Attributed to the reason that Under Armour does not

generate money, its revenue return is zero, but Nike has a potential revenue return.

Furthermore, the EPS displays how much money buyers earn by investing in the

company. According to the analysis, Nike's EPS is extremely promising, whilst Under

Armour’s EPS has been steadily improving over time. Under Armour's Price-Earnings

Ratio was unfavourable in 2018 as a result of the company's total shortfall (Boyle, Lewis-

Western and Seidel, 2021). Lower transaction growth due to shifting demand in sports

gear, fierce competition, and outlet closures by key suppliers compounded the loss. Yet,

the company made significant progress in 2019, as seen by a similar trajectory in the

company's Price-Earnings ratio. All of Under Armour’s other incentive ratios have

increased dramatically from 2018 to 2019, owing to the company's compensation

announcement shifting from a significant loss to a significant positive.

Ratios of Liquidity- The most common ratios analysed are liquidity levels. It could be

obtained by dividing funds and liquid assets into short-term loans and present obligations.

Major enhancements in the company's excellence of goods and offerings may be

possible. The current and quick ratios of both companies are significantly higher than that

of the standard 1.0, indicating that they will have strong liquidity strength; nevertheless,

Nike outperforms Under Armour in terms of current ratio. In terms of revenue flow,

Under Armour has to strive more to improve its financial condition. This demonstrates

that Under Armour’s long-term share has been falling, whereas its fast-growing share has

already been increasing.

Working Capital Ratios- Nike's working capital overall turnover is significantly greater

than that of Under Armour. Yet, trend analysis suggests that Nike is growing at a

significantly faster pace in terms of working capital turnover. Given this, Under

Armour’s management must adopt some links from Nike's strategy and concentrate on

improving their internal operational competence (Chen, Tan and Fang, 2018).

Profitability Ratios- It was discovered that "The characteristics of financial precision are

linked to an understanding of initial output development in emerging businesses. This is

significant because one of the goals of fiscal reporting is to hold managers accountable to

finance supporters so that investment is allocated efficiently ". In 2018, Under Armour's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

return on capital employed was adverse due to a negative gross pay, the company's

largest aggregate loss in ten years. Lower transaction growth due to shifting demand in

sports apparel, fierce competition, and outlet closures by large stores compounded the

disaster. In any event, the organisation made significant progress in 2019, as seen by a

trend in the firm's ROA. All of Under Armour's financial advantage ratios rose

significantly from 2018 to 2019, owing to the company's compensation rationale shifting

from a significant loss to a direct gain. Conversely, Nike has a strong track performance

in terms of output, as evidenced by the advantage ratios above.

Question 2: Balanced Scorecard

Whenever users create a process mapping correctly at the design stage, it shows how the

important goals in another multiple views, i.e. financial and customer, are directly and adversely

influenced by the authorized goals in the first two views. Users set your sights on the golden

Goal on the Strategic Roadmap for the phrase, and you organise initiatives to get the organisation

from which it is to where it wants to be, on a regular basis. In the following scenario, it's critical

that enterprise-level choices and strategies influence and influence multiple tiers of the

organisation (Commerford, Hatfield and Houston, 2018). This is accomplished by cascade the

process down to the lowest tiers, aided by the technique mapping. Each of those departments or

divisions would often use a comparable network mapping to determine which important

objectives apply to them individually. Regardless of the notion that just a few Tactical

Objectives on the Plan Mapping appear to be their direct responsibility, it is prudent for the

primary threshold underneath the Corporate Tier to analyse all Crucial Goal on the Policy Board.

This allows them to concentrate at the same level as the larger organisation. It also enables them

to allocate personal responsibility to employees within respective field of knowledge and

divisions in view of pre-determined goals. For me, such aims are becoming personal goals.

As a result, the institution's goal and purpose become a main focus for all tiers of the

organisation. Because it links to and provides understanding of the specific tasks of

administrative divisions, the balanced scorecard is an indispensable tool for higher-level

planning and implementation. Finally, individuals within the organisation take responsibility of

the objectives and outcomes that serve as a measure of implementation for the 2 components and

individuals. In the mid-1990s, Kaplan and Norton created the Balanced Scorecard approach to

largest aggregate loss in ten years. Lower transaction growth due to shifting demand in

sports apparel, fierce competition, and outlet closures by large stores compounded the

disaster. In any event, the organisation made significant progress in 2019, as seen by a

trend in the firm's ROA. All of Under Armour's financial advantage ratios rose

significantly from 2018 to 2019, owing to the company's compensation rationale shifting

from a significant loss to a direct gain. Conversely, Nike has a strong track performance

in terms of output, as evidenced by the advantage ratios above.

Question 2: Balanced Scorecard

Whenever users create a process mapping correctly at the design stage, it shows how the

important goals in another multiple views, i.e. financial and customer, are directly and adversely

influenced by the authorized goals in the first two views. Users set your sights on the golden

Goal on the Strategic Roadmap for the phrase, and you organise initiatives to get the organisation

from which it is to where it wants to be, on a regular basis. In the following scenario, it's critical

that enterprise-level choices and strategies influence and influence multiple tiers of the

organisation (Commerford, Hatfield and Houston, 2018). This is accomplished by cascade the

process down to the lowest tiers, aided by the technique mapping. Each of those departments or

divisions would often use a comparable network mapping to determine which important

objectives apply to them individually. Regardless of the notion that just a few Tactical

Objectives on the Plan Mapping appear to be their direct responsibility, it is prudent for the

primary threshold underneath the Corporate Tier to analyse all Crucial Goal on the Policy Board.

This allows them to concentrate at the same level as the larger organisation. It also enables them

to allocate personal responsibility to employees within respective field of knowledge and

divisions in view of pre-determined goals. For me, such aims are becoming personal goals.

As a result, the institution's goal and purpose become a main focus for all tiers of the

organisation. Because it links to and provides understanding of the specific tasks of

administrative divisions, the balanced scorecard is an indispensable tool for higher-level

planning and implementation. Finally, individuals within the organisation take responsibility of

the objectives and outcomes that serve as a measure of implementation for the 2 components and

individuals. In the mid-1990s, Kaplan and Norton created the Balanced Scorecard approach to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assist businesses in setting out and analysing organisational results from both a financial and

non-financial perspective.

Many levels of degraded organisations can aid area leaders and officials in identifying the

diverse items which must be able to enhance authoritative implementation.

This is a viewpoint which aids in fully comprehending an organization's actions and goes

totally beyond the common belief that the organisation is self-contained and independent

(Csákné Filep and Karmazin, 2016).

The concept could be quite beneficial to a firm because it focuses on the numerous

actions that must be carried out in order for them to work well. This would be the case

due to the cooperation or integration of various business-related activities.

This is useful for improving methodology because such frameworks could be translated

into implementation standards and goals.

The disadvantages of employing Kaplan and Norton's Balanced Scorecard are as follows:

It would need a decent equilibrium between the 4 groups- financial, customer, interior,

and scholastic and expansion would be tough to complete.

Despite all of the safeguards in place, executive management's primary focus may still be

on financial accomplishment.

It may have an excessive amount of processing references, making it difficult to operate.

In many commercial areas, the focus of businesses and their management is on immediate

manageability and financial rewards, and they frequently overlook long-term marketing tactics

and also the firm's motive and goal. To achieve better financial implementation and a bigger slice

of the bucket, a company should try to turn its objectives and strategies into specific industry

segments and customer targets. Often these organisations' belief that any customer who can pay

is a good customer was rejected by Kaplan and Norton as a short-sighted viewpoint, and they

instead emphasised that the organization's primary focus should be on what to do, as well as

what not to do, when using their receipt assessing structure (Ghesquiere, McAfee and Burnett,

2019). By utilising 4 main methods such as cash, customer, internal understanding, and growth,

the credit cards approach enables the organisation to have a larger and long run perspective than

following the most recent benefits.

Under Armour Balance Score Card-

non-financial perspective.

Many levels of degraded organisations can aid area leaders and officials in identifying the

diverse items which must be able to enhance authoritative implementation.

This is a viewpoint which aids in fully comprehending an organization's actions and goes

totally beyond the common belief that the organisation is self-contained and independent

(Csákné Filep and Karmazin, 2016).

The concept could be quite beneficial to a firm because it focuses on the numerous

actions that must be carried out in order for them to work well. This would be the case

due to the cooperation or integration of various business-related activities.

This is useful for improving methodology because such frameworks could be translated

into implementation standards and goals.

The disadvantages of employing Kaplan and Norton's Balanced Scorecard are as follows:

It would need a decent equilibrium between the 4 groups- financial, customer, interior,

and scholastic and expansion would be tough to complete.

Despite all of the safeguards in place, executive management's primary focus may still be

on financial accomplishment.

It may have an excessive amount of processing references, making it difficult to operate.

In many commercial areas, the focus of businesses and their management is on immediate

manageability and financial rewards, and they frequently overlook long-term marketing tactics

and also the firm's motive and goal. To achieve better financial implementation and a bigger slice

of the bucket, a company should try to turn its objectives and strategies into specific industry

segments and customer targets. Often these organisations' belief that any customer who can pay

is a good customer was rejected by Kaplan and Norton as a short-sighted viewpoint, and they

instead emphasised that the organization's primary focus should be on what to do, as well as

what not to do, when using their receipt assessing structure (Ghesquiere, McAfee and Burnett,

2019). By utilising 4 main methods such as cash, customer, internal understanding, and growth,

the credit cards approach enables the organisation to have a larger and long run perspective than

following the most recent benefits.

Under Armour Balance Score Card-

From a procedural or inner management standpoint- Under Armour’s sensible plan

of operation for productivity and reliability updates should stick to a normal basis. Every

quarter, the number of errors in productivity and sales would be reduced by 3%, and the

system would be evaluated annually for improvements. Under Armour would offer

additional element, such as machinery, and therefore would assess the phases on a case-

by-case situation for changes (Kovalenko, 2019).

Education and Development- It is critical for Under Armour to maintain worker

attrition and maintenance costs minimal. In the athletic apparel sector, Under Armour’s

faith in increases in innovation is critical, and developments in mechanised technology

would continue to progress, putting the company on front of the industry. There would be

town hall-style talks about any advancements which require to be looked out thoroughly

throughout the organisation, and department leaders with collaborators would engage and

be prepared to face all such sorts of feedback.

Shareholders Valuation or Monetary Viewpoint- In terms of earnings and expenses,

the company may need to increase earnings from potential customers by 10% over the

next 2 years. This would be accomplished by aggressively attracting additional clientele

via effective marketing and fresh clothes. All individuals would be held accountable for

providing excellent customer service. The firm's advantage is as important as the use of

gross income to achieve the achievement of the aims and ambitions, and the organisation

would magnify the commercial value and increase advantages by 5% on a regular basis.

From the standpoint of client value- The company would continue to focus on

customer retention and attrition. User engagement is extremely important to the

company, and it plans to increase it by 5% annually for the next 3 years through

providing and collecting data from customer summaries. The divisional managers would

be in charge of collecting user surveys on a monthly basis, compiling statistics, and

reporting to senior management on the results (Lotfi, Salehi and Dashtbayaz, 2021). The

organisation would be supplied data and the customer would be provided a reward for

comparable durations based on the facts obtained in the evaluations, and the development

of customer value would be equated to customer devotion.

of operation for productivity and reliability updates should stick to a normal basis. Every

quarter, the number of errors in productivity and sales would be reduced by 3%, and the

system would be evaluated annually for improvements. Under Armour would offer

additional element, such as machinery, and therefore would assess the phases on a case-

by-case situation for changes (Kovalenko, 2019).

Education and Development- It is critical for Under Armour to maintain worker

attrition and maintenance costs minimal. In the athletic apparel sector, Under Armour’s

faith in increases in innovation is critical, and developments in mechanised technology

would continue to progress, putting the company on front of the industry. There would be

town hall-style talks about any advancements which require to be looked out thoroughly

throughout the organisation, and department leaders with collaborators would engage and

be prepared to face all such sorts of feedback.

Shareholders Valuation or Monetary Viewpoint- In terms of earnings and expenses,

the company may need to increase earnings from potential customers by 10% over the

next 2 years. This would be accomplished by aggressively attracting additional clientele

via effective marketing and fresh clothes. All individuals would be held accountable for

providing excellent customer service. The firm's advantage is as important as the use of

gross income to achieve the achievement of the aims and ambitions, and the organisation

would magnify the commercial value and increase advantages by 5% on a regular basis.

From the standpoint of client value- The company would continue to focus on

customer retention and attrition. User engagement is extremely important to the

company, and it plans to increase it by 5% annually for the next 3 years through

providing and collecting data from customer summaries. The divisional managers would

be in charge of collecting user surveys on a monthly basis, compiling statistics, and

reporting to senior management on the results (Lotfi, Salehi and Dashtbayaz, 2021). The

organisation would be supplied data and the customer would be provided a reward for

comparable durations based on the facts obtained in the evaluations, and the development

of customer value would be equated to customer devotion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 3: Integrated Reporting

By instituting the consequence of both the corporations over a specific duration for

implementation, the connection Under Armour could follow the rules of the integrated report.

The dissolving covering specifies how organization monetary and non-monetary indicators are

presented in a unified statement (Paluri and Mehra, 2016). Those things, for instance, are offered

to provide compelling views to crucial facts like midsized corporate strategy, societal and

organisational constraints connections. Brief, moderate, and far range reporting are a minimum

reaction to the possible outcomes for the connection network, organisation, performance, and

possible outcomes. The IR technique could be beneficial for discussing processes, performance,

potential outcomes, and cells required for accomplishment when utilized in combination. If the

organisation adopts IR, it would be better fiscally sound, and it can offer it the similar treatment

to assist them in attracting more funding supporters.

As a consequence, built-in organisations must present monetary outcomes that are close to

non-performance. This information openness could be perceived as being skewed in the

circumstance based on its viewpoint as well as other downsides. Equally significantly, it is

extremely hazardous and time-consuming to make, gather, and establish data. Several areas are

difficult to comprehend. There's definitely an issue with the thoughts within the capturing

process. As this information spreads the fundamental component in the creation of benefits, the

connection with marketplace abilities is rigorously scrutinised. Its primitive form could cause

significant merger identification issues (Sonnenberg, 2018). Under Armour executives should

confront the initial spectrum in order to retrieve information for assessment preparation. Most

critical data could be shared to groups and accountancy systems. It is under-reporting all of the

great structures and procedures because it allows troubled businesses like Nike to reap the

benefits of it by providing quick and relevant information regarding almost any type of business.

Under Armour's ability to shift its company could be a challenge.

In relation to worker engagement, the concept of a shared statement is fiscal and budgetary

in a particular season. It also has the incredible ability to arrange non-monetary data. This allows

the aid to expand his or her appraisal and relevancy of the content. The strategy section of the

applicable study is, without a question, the well-organized study material. Throughout the period

invested demonstrating, the items are essential. This is critical for each important components

and associated measurement criteria for developing organised summaries. Considering that the

By instituting the consequence of both the corporations over a specific duration for

implementation, the connection Under Armour could follow the rules of the integrated report.

The dissolving covering specifies how organization monetary and non-monetary indicators are

presented in a unified statement (Paluri and Mehra, 2016). Those things, for instance, are offered

to provide compelling views to crucial facts like midsized corporate strategy, societal and

organisational constraints connections. Brief, moderate, and far range reporting are a minimum

reaction to the possible outcomes for the connection network, organisation, performance, and

possible outcomes. The IR technique could be beneficial for discussing processes, performance,

potential outcomes, and cells required for accomplishment when utilized in combination. If the

organisation adopts IR, it would be better fiscally sound, and it can offer it the similar treatment

to assist them in attracting more funding supporters.

As a consequence, built-in organisations must present monetary outcomes that are close to

non-performance. This information openness could be perceived as being skewed in the

circumstance based on its viewpoint as well as other downsides. Equally significantly, it is

extremely hazardous and time-consuming to make, gather, and establish data. Several areas are

difficult to comprehend. There's definitely an issue with the thoughts within the capturing

process. As this information spreads the fundamental component in the creation of benefits, the

connection with marketplace abilities is rigorously scrutinised. Its primitive form could cause

significant merger identification issues (Sonnenberg, 2018). Under Armour executives should

confront the initial spectrum in order to retrieve information for assessment preparation. Most

critical data could be shared to groups and accountancy systems. It is under-reporting all of the

great structures and procedures because it allows troubled businesses like Nike to reap the

benefits of it by providing quick and relevant information regarding almost any type of business.

Under Armour's ability to shift its company could be a challenge.

In relation to worker engagement, the concept of a shared statement is fiscal and budgetary

in a particular season. It also has the incredible ability to arrange non-monetary data. This allows

the aid to expand his or her appraisal and relevancy of the content. The strategy section of the

applicable study is, without a question, the well-organized study material. Throughout the period

invested demonstrating, the items are essential. This is critical for each important components

and associated measurement criteria for developing organised summaries. Considering that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

association is based on the supervisor's connection rather than the division, this is quantifiable.

This document is a broad response to advisers' real-world information requirements. Under

Armour's management division could receive the following advantages by implementing IR

fundamentals:

Current disclosing only provides financial outcomes of financial information, however

integrating specifying provides information regarding relevant facts to enhance control.

It assists in responding to the financial consistency essential for long-term value

building that the existing system cannot provide.

Integrated detailing has recently emerged as a critical requirement for several worldwide

organisations.

It also highlighted concise correlations by providing more facts and expertise than

previous releases (Tumataroa and O'Hare, 2019).

It aids in the creation of considerable value from non-financial data such as licensed

technology, the capital sector, and natural resources.

It provides a longer advantage or a broader area of data than current disclosures, allowing

for the creation and maintenance of value.

With all of it obtained in to consideration, the suggested strengths of integrated detailing

mitigated the price of supplying one more summary in Under Armour, as all of it from the

organisation of details to the investigation and comprehension of statistics will indeed add to the

load on disclosure, but the strengths of synchronised declaring might give the reward

establishment that might easily counterbalanced the expenditure of providing another summary.

As a consequence, Under Armour could use below criteria to create an integrated analysis in

order to enhance the efficiency of its company operational activities:

Comprehensiveness: As being one of the essential principles, preciseness implies that

the merged statement must be brief and straightforward. There must be enough data for

the client to consider the importance in the specifics of the organisational process,

approach, and goals, among other things. Simultaneously, there must be sufficient data

sans unnecessary complexities. Because reaching simplicity must not come at the

expense of other governing concepts and demonstrations, it is critical that the affiliate

adopts a credible approach to its arranged statement.

This document is a broad response to advisers' real-world information requirements. Under

Armour's management division could receive the following advantages by implementing IR

fundamentals:

Current disclosing only provides financial outcomes of financial information, however

integrating specifying provides information regarding relevant facts to enhance control.

It assists in responding to the financial consistency essential for long-term value

building that the existing system cannot provide.

Integrated detailing has recently emerged as a critical requirement for several worldwide

organisations.

It also highlighted concise correlations by providing more facts and expertise than

previous releases (Tumataroa and O'Hare, 2019).

It aids in the creation of considerable value from non-financial data such as licensed

technology, the capital sector, and natural resources.

It provides a longer advantage or a broader area of data than current disclosures, allowing

for the creation and maintenance of value.

With all of it obtained in to consideration, the suggested strengths of integrated detailing

mitigated the price of supplying one more summary in Under Armour, as all of it from the

organisation of details to the investigation and comprehension of statistics will indeed add to the

load on disclosure, but the strengths of synchronised declaring might give the reward

establishment that might easily counterbalanced the expenditure of providing another summary.

As a consequence, Under Armour could use below criteria to create an integrated analysis in

order to enhance the efficiency of its company operational activities:

Comprehensiveness: As being one of the essential principles, preciseness implies that

the merged statement must be brief and straightforward. There must be enough data for

the client to consider the importance in the specifics of the organisational process,

approach, and goals, among other things. Simultaneously, there must be sufficient data

sans unnecessary complexities. Because reaching simplicity must not come at the

expense of other governing concepts and demonstrations, it is critical that the affiliate

adopts a credible approach to its arranged statement.

Reliability: A merged study's stability essential concept relates with the data which is

free of obstacles. A combination of regulatory systems, the existence of external and

inner evaluations, and diverse procedures could all aid in ensuring the accuracy of data.

The processes, method, and process involved of delivering the aggregated statement are

all the responsibility of an organisation's administrative framework.

Materiality: It is likely the basis of every particular core ideas. It implies that the data

connected with a unified analysis provides useful data about the operational activities and

the revenue generation activity over time. It is a link, not a fixed norm. As a result,

associations must carefully identify substantive concerns in order to create an organised

analysis (Zimon and Zimon, 2019). Furthermore, it must be noted that the technical data

provided in the proposed study does not have to be 100% accurate. There must be

transparency about the dual vulnerabilities, possible entrances, and favourable and

unfavourable instances subsequently on in the organisational viewpoint.

Emerging Approach: As a core concept, prospective program incorporates both the

significance of forward-looking data and investigations into the period range across that

the operational basic necessities are established. Aside from thinking on the prospective

and the revenue development procedure in the brief, intermediate, and longer term, it's

critical to establish connections among previous actions and the operational prospective

potential.

CONCLUSION

Relying on the monetary holdings of Under Armour and Nike, we could deduce that they are

performing extremely effectively in the product category and are increasing a portion of their

bucket in the big scheme of things. Advantages from Under Armour suggest a dearth of

financing, although this is a proportional effect of the firm's total shortfall in 2018. In 2019,

Under Armour addressed fundamental issues by combining other good motivations. This must

result to the organisation offering more designing options. Furthermore, Under Armour is urged

to put in more effort in order to improve its financial condition. Furthermore, because to the vast

variations in proportions, Nike, Under Armour's nearest competitor, does have a bunch of

inexhaustible stock. As a result, Under Armour must assess Nike's competitive advantages and

improve. The union could promote an exceptional deal by creating a basically balanced

scorecard in view of Under Armour's Balanced Scorecard evaluation. 4 additional techniques are

free of obstacles. A combination of regulatory systems, the existence of external and

inner evaluations, and diverse procedures could all aid in ensuring the accuracy of data.

The processes, method, and process involved of delivering the aggregated statement are

all the responsibility of an organisation's administrative framework.

Materiality: It is likely the basis of every particular core ideas. It implies that the data

connected with a unified analysis provides useful data about the operational activities and

the revenue generation activity over time. It is a link, not a fixed norm. As a result,

associations must carefully identify substantive concerns in order to create an organised

analysis (Zimon and Zimon, 2019). Furthermore, it must be noted that the technical data

provided in the proposed study does not have to be 100% accurate. There must be

transparency about the dual vulnerabilities, possible entrances, and favourable and

unfavourable instances subsequently on in the organisational viewpoint.

Emerging Approach: As a core concept, prospective program incorporates both the

significance of forward-looking data and investigations into the period range across that

the operational basic necessities are established. Aside from thinking on the prospective

and the revenue development procedure in the brief, intermediate, and longer term, it's

critical to establish connections among previous actions and the operational prospective

potential.

CONCLUSION

Relying on the monetary holdings of Under Armour and Nike, we could deduce that they are

performing extremely effectively in the product category and are increasing a portion of their

bucket in the big scheme of things. Advantages from Under Armour suggest a dearth of

financing, although this is a proportional effect of the firm's total shortfall in 2018. In 2019,

Under Armour addressed fundamental issues by combining other good motivations. This must

result to the organisation offering more designing options. Furthermore, Under Armour is urged

to put in more effort in order to improve its financial condition. Furthermore, because to the vast

variations in proportions, Nike, Under Armour's nearest competitor, does have a bunch of

inexhaustible stock. As a result, Under Armour must assess Nike's competitive advantages and

improve. The union could promote an exceptional deal by creating a basically balanced

scorecard in view of Under Armour's Balanced Scorecard evaluation. 4 additional techniques are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.