Financial Performance Management Report: Ruislip PLC Analysis

VerifiedAdded on 2022/12/28

|12

|2724

|75

Report

AI Summary

This report analyzes the financial performance management of Ruislip PLC, covering key aspects of cost accounting and budgeting. The report begins with a calculation of cost per product for lipstick, lip-balm, and lip-gloss using both labor hour and activity-based costing (ABC) methods. A comparative evaluation of these techniques highlights the advantages of ABC, particularly in accurately allocating overhead costs. Sensitivity analysis is then discussed, emphasizing its role in helping managers navigate uncertainty in decision-making. The report proceeds to calculate and analyze variances for the last month, addressing material usage, mix, and yield variances. It also critiques the current variance reporting system, identifying problems in assessing production manager performance. Finally, the report explores zero-based budgeting (ZBB) and incremental budgeting (IB), comparing their methodologies and evaluating their respective strengths and weaknesses, offering insights into their suitability for different organizational contexts.

FINANCIAL

PERFORMANCE

MANAGEMENT

PERFORMANCE

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Main Body ......................................................................................................................................3

QUESTION 1...................................................................................................................................3

a) Calculation of cost per product on the basis of labour hour...................................................3

b) Estimation of cost per product on the basis of activity based costing approach....................4

c)Evaluation of better technique on the basis of above calculation............................................5

d) discussion of sensitivity analysis helps managers to cope up with uncertainty......................6

QUESTION 2...................................................................................................................................6

a) calculation of variances for the last month.............................................................................6

b) discussion of Problems with current system of calculating and reporting variances for

assessing the performance of the production manager...............................................................8

QUESTION 3...................................................................................................................................9

REFERENCES..............................................................................................................................11

Main Body ......................................................................................................................................3

QUESTION 1...................................................................................................................................3

a) Calculation of cost per product on the basis of labour hour...................................................3

b) Estimation of cost per product on the basis of activity based costing approach....................4

c)Evaluation of better technique on the basis of above calculation............................................5

d) discussion of sensitivity analysis helps managers to cope up with uncertainty......................6

QUESTION 2...................................................................................................................................6

a) calculation of variances for the last month.............................................................................6

b) discussion of Problems with current system of calculating and reporting variances for

assessing the performance of the production manager...............................................................8

QUESTION 3...................................................................................................................................9

REFERENCES..............................................................................................................................11

Main Body

QUESTION 1

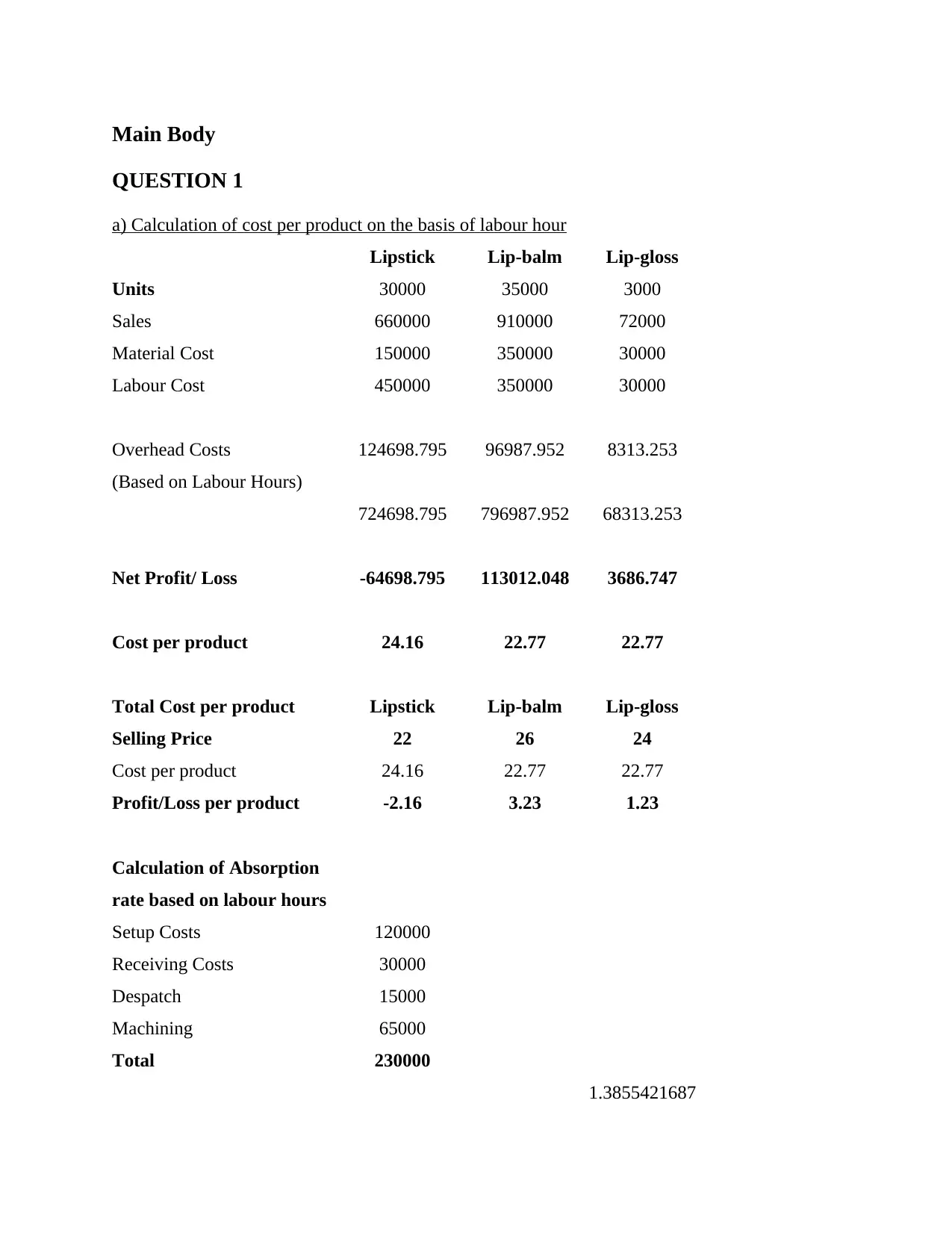

a) Calculation of cost per product on the basis of labour hour

Lipstick Lip-balm Lip-gloss

Units 30000 35000 3000

Sales 660000 910000 72000

Material Cost 150000 350000 30000

Labour Cost 450000 350000 30000

Overhead Costs 124698.795 96987.952 8313.253

(Based on Labour Hours)

724698.795 796987.952 68313.253

Net Profit/ Loss -64698.795 113012.048 3686.747

Cost per product 24.16 22.77 22.77

Total Cost per product Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Cost per product 24.16 22.77 22.77

Profit/Loss per product -2.16 3.23 1.23

Calculation of Absorption

rate based on labour hours

Setup Costs 120000

Receiving Costs 30000

Despatch 15000

Machining 65000

Total 230000

1.3855421687

QUESTION 1

a) Calculation of cost per product on the basis of labour hour

Lipstick Lip-balm Lip-gloss

Units 30000 35000 3000

Sales 660000 910000 72000

Material Cost 150000 350000 30000

Labour Cost 450000 350000 30000

Overhead Costs 124698.795 96987.952 8313.253

(Based on Labour Hours)

724698.795 796987.952 68313.253

Net Profit/ Loss -64698.795 113012.048 3686.747

Cost per product 24.16 22.77 22.77

Total Cost per product Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Cost per product 24.16 22.77 22.77

Profit/Loss per product -2.16 3.23 1.23

Calculation of Absorption

rate based on labour hours

Setup Costs 120000

Receiving Costs 30000

Despatch 15000

Machining 65000

Total 230000

1.3855421687

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Labour Hours 166000

Overhead Cost 230000

Overhead Absorption Rate 230000/166000

(Based on Labour Hours) 1.3855

Lipstick Lip-balm Lip-gloss

Total Labour Hours 90000 70000 6000

Absorption Rate 1.3855 1.3855 1.3855

Overhead Costs 124698.80 96987.95 8313.25

b) Estimation of cost per product on the basis of activity based costing approach

Calculation of Absorption

rate based on labour hours

Setup Costs 120000

Receiving Costs 30000

Despatch 15000

Machining 65000

Total 230000

1.3855421687

Total Labour Hours 166000

Overhead Cost 230000

Overhead Absorption Rate 230000/166000

(Based on Labour Hours) 1.3855

Lipstick Lip-balm Lip-gloss

Total Labour Hours 90000 70000 6000

Absorption Rate 1.3855 1.3855 1.3855

Overhead Costs 124698.80 96987.95 8313.25

Overhead Cost 230000

Overhead Absorption Rate 230000/166000

(Based on Labour Hours) 1.3855

Lipstick Lip-balm Lip-gloss

Total Labour Hours 90000 70000 6000

Absorption Rate 1.3855 1.3855 1.3855

Overhead Costs 124698.80 96987.95 8313.25

b) Estimation of cost per product on the basis of activity based costing approach

Calculation of Absorption

rate based on labour hours

Setup Costs 120000

Receiving Costs 30000

Despatch 15000

Machining 65000

Total 230000

1.3855421687

Total Labour Hours 166000

Overhead Cost 230000

Overhead Absorption Rate 230000/166000

(Based on Labour Hours) 1.3855

Lipstick Lip-balm Lip-gloss

Total Labour Hours 90000 70000 6000

Absorption Rate 1.3855 1.3855 1.3855

Overhead Costs 124698.80 96987.95 8313.25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

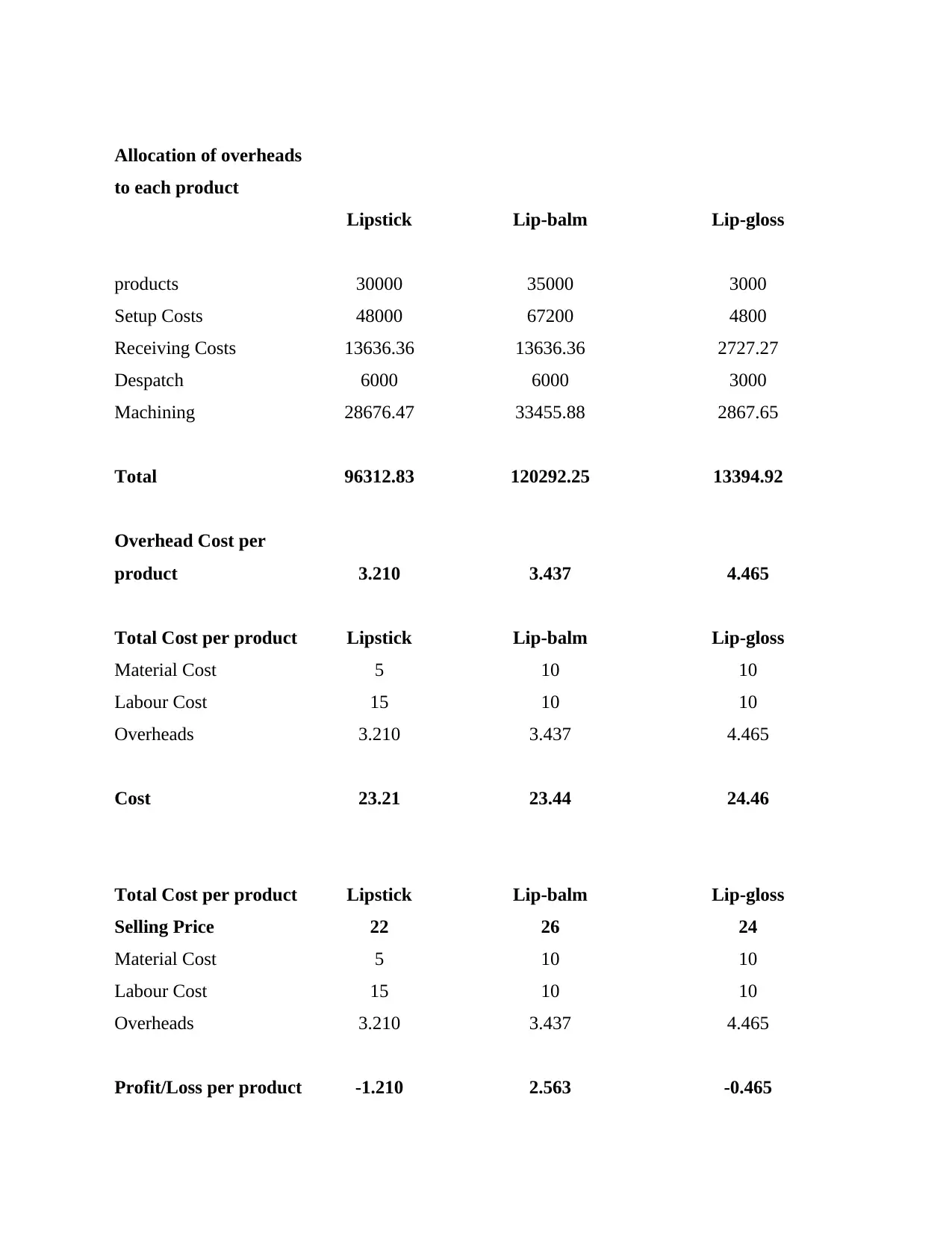

Allocation of overheads

to each product

Lipstick Lip-balm Lip-gloss

products 30000 35000 3000

Setup Costs 48000 67200 4800

Receiving Costs 13636.36 13636.36 2727.27

Despatch 6000 6000 3000

Machining 28676.47 33455.88 2867.65

Total 96312.83 120292.25 13394.92

Overhead Cost per

product 3.210 3.437 4.465

Total Cost per product Lipstick Lip-balm Lip-gloss

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Cost 23.21 23.44 24.46

Total Cost per product Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Profit/Loss per product -1.210 2.563 -0.465

to each product

Lipstick Lip-balm Lip-gloss

products 30000 35000 3000

Setup Costs 48000 67200 4800

Receiving Costs 13636.36 13636.36 2727.27

Despatch 6000 6000 3000

Machining 28676.47 33455.88 2867.65

Total 96312.83 120292.25 13394.92

Overhead Cost per

product 3.210 3.437 4.465

Total Cost per product Lipstick Lip-balm Lip-gloss

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Cost 23.21 23.44 24.46

Total Cost per product Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Profit/Loss per product -1.210 2.563 -0.465

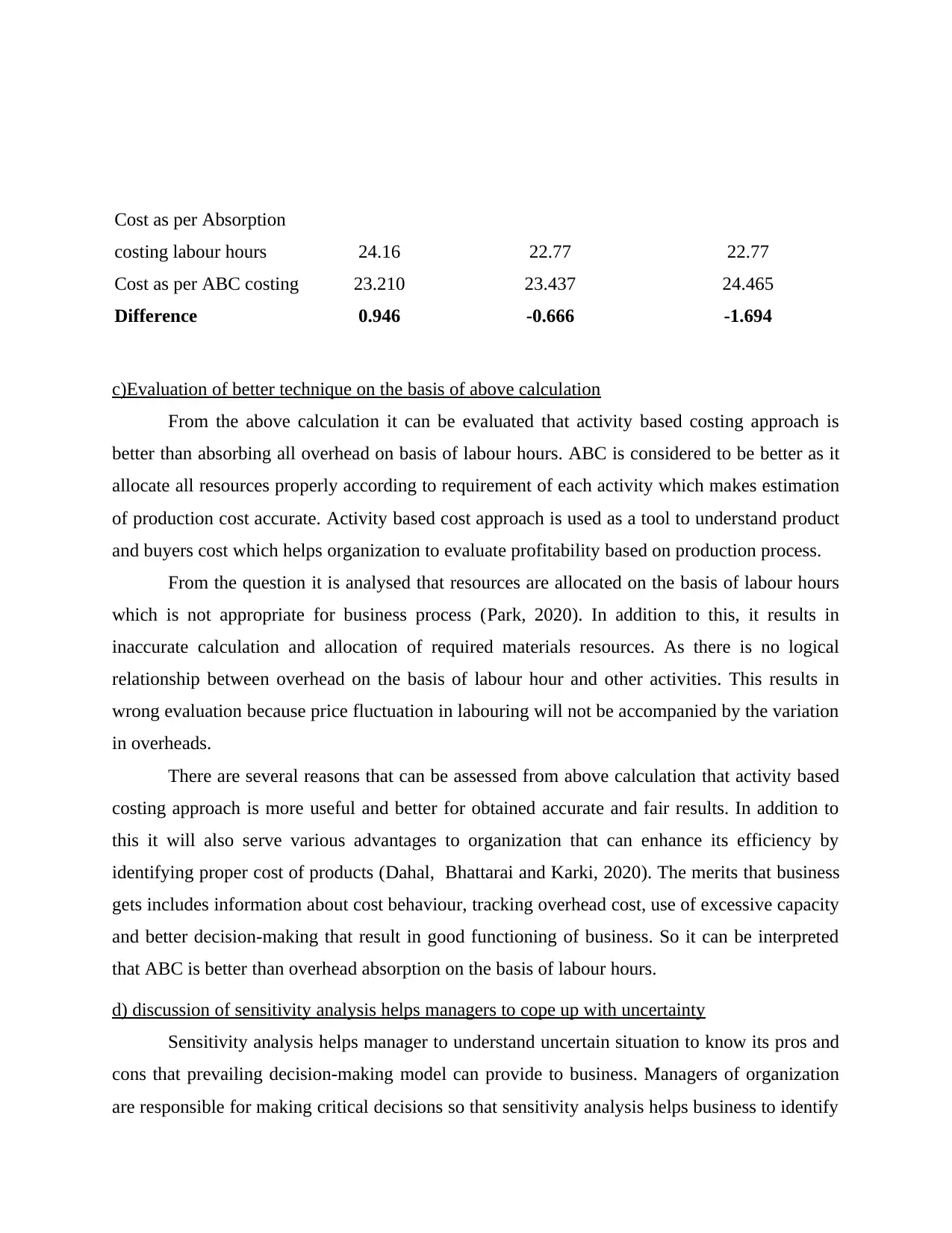

Cost as per Absorption

costing labour hours 24.16 22.77 22.77

Cost as per ABC costing 23.210 23.437 24.465

Difference 0.946 -0.666 -1.694

c)Evaluation of better technique on the basis of above calculation

From the above calculation it can be evaluated that activity based costing approach is

better than absorbing all overhead on basis of labour hours. ABC is considered to be better as it

allocate all resources properly according to requirement of each activity which makes estimation

of production cost accurate. Activity based cost approach is used as a tool to understand product

and buyers cost which helps organization to evaluate profitability based on production process.

From the question it is analysed that resources are allocated on the basis of labour hours

which is not appropriate for business process (Park, 2020). In addition to this, it results in

inaccurate calculation and allocation of required materials resources. As there is no logical

relationship between overhead on the basis of labour hour and other activities. This results in

wrong evaluation because price fluctuation in labouring will not be accompanied by the variation

in overheads.

There are several reasons that can be assessed from above calculation that activity based

costing approach is more useful and better for obtained accurate and fair results. In addition to

this it will also serve various advantages to organization that can enhance its efficiency by

identifying proper cost of products (Dahal, Bhattarai and Karki, 2020). The merits that business

gets includes information about cost behaviour, tracking overhead cost, use of excessive capacity

and better decision-making that result in good functioning of business. So it can be interpreted

that ABC is better than overhead absorption on the basis of labour hours.

d) discussion of sensitivity analysis helps managers to cope up with uncertainty

Sensitivity analysis helps manager to understand uncertain situation to know its pros and

cons that prevailing decision-making model can provide to business. Managers of organization

are responsible for making critical decisions so that sensitivity analysis helps business to identify

costing labour hours 24.16 22.77 22.77

Cost as per ABC costing 23.210 23.437 24.465

Difference 0.946 -0.666 -1.694

c)Evaluation of better technique on the basis of above calculation

From the above calculation it can be evaluated that activity based costing approach is

better than absorbing all overhead on basis of labour hours. ABC is considered to be better as it

allocate all resources properly according to requirement of each activity which makes estimation

of production cost accurate. Activity based cost approach is used as a tool to understand product

and buyers cost which helps organization to evaluate profitability based on production process.

From the question it is analysed that resources are allocated on the basis of labour hours

which is not appropriate for business process (Park, 2020). In addition to this, it results in

inaccurate calculation and allocation of required materials resources. As there is no logical

relationship between overhead on the basis of labour hour and other activities. This results in

wrong evaluation because price fluctuation in labouring will not be accompanied by the variation

in overheads.

There are several reasons that can be assessed from above calculation that activity based

costing approach is more useful and better for obtained accurate and fair results. In addition to

this it will also serve various advantages to organization that can enhance its efficiency by

identifying proper cost of products (Dahal, Bhattarai and Karki, 2020). The merits that business

gets includes information about cost behaviour, tracking overhead cost, use of excessive capacity

and better decision-making that result in good functioning of business. So it can be interpreted

that ABC is better than overhead absorption on the basis of labour hours.

d) discussion of sensitivity analysis helps managers to cope up with uncertainty

Sensitivity analysis helps manager to understand uncertain situation to know its pros and

cons that prevailing decision-making model can provide to business. Managers of organization

are responsible for making critical decisions so that sensitivity analysis helps business to identify

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

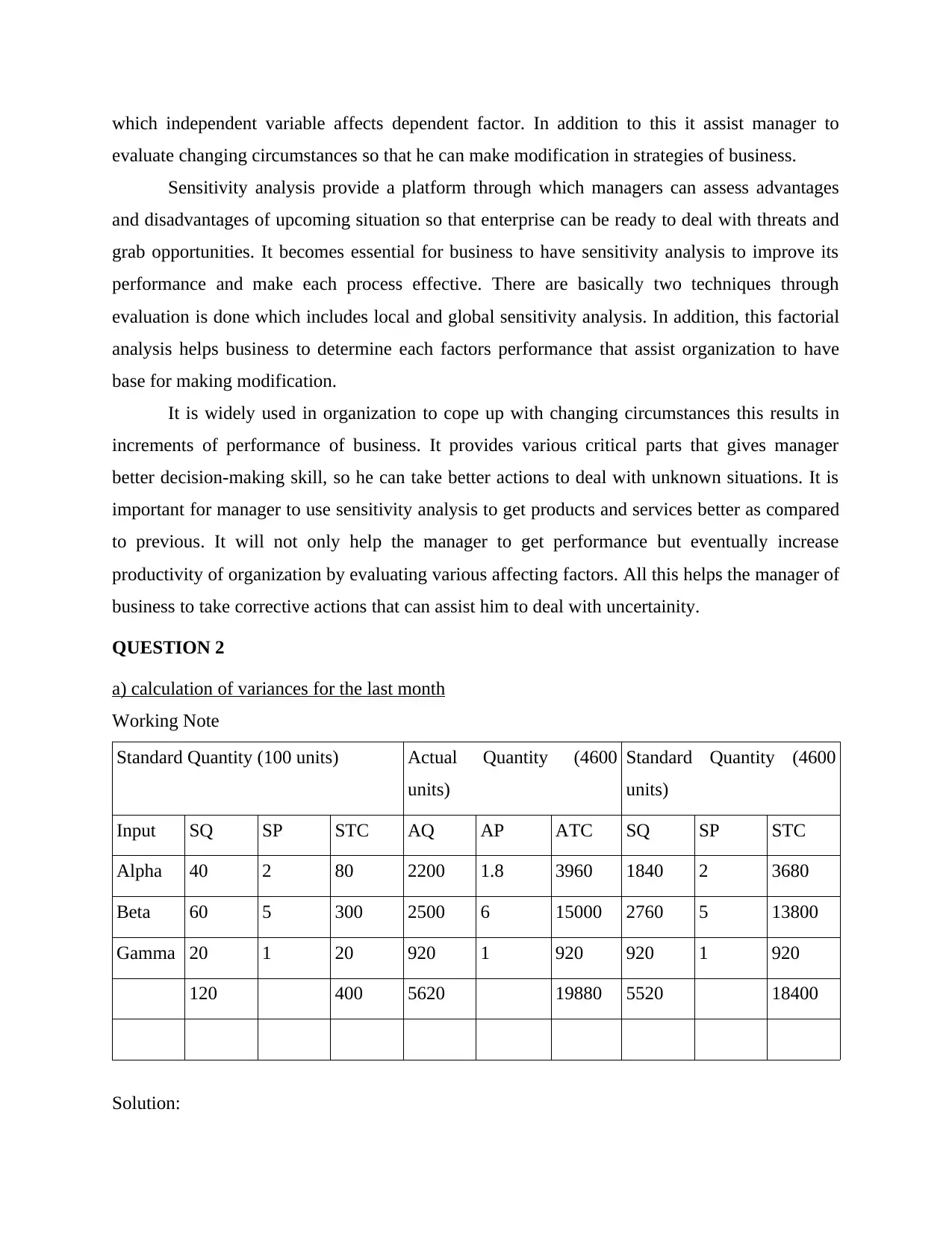

which independent variable affects dependent factor. In addition to this it assist manager to

evaluate changing circumstances so that he can make modification in strategies of business.

Sensitivity analysis provide a platform through which managers can assess advantages

and disadvantages of upcoming situation so that enterprise can be ready to deal with threats and

grab opportunities. It becomes essential for business to have sensitivity analysis to improve its

performance and make each process effective. There are basically two techniques through

evaluation is done which includes local and global sensitivity analysis. In addition, this factorial

analysis helps business to determine each factors performance that assist organization to have

base for making modification.

It is widely used in organization to cope up with changing circumstances this results in

increments of performance of business. It provides various critical parts that gives manager

better decision-making skill, so he can take better actions to deal with unknown situations. It is

important for manager to use sensitivity analysis to get products and services better as compared

to previous. It will not only help the manager to get performance but eventually increase

productivity of organization by evaluating various affecting factors. All this helps the manager of

business to take corrective actions that can assist him to deal with uncertainity.

QUESTION 2

a) calculation of variances for the last month

Working Note

Standard Quantity (100 units) Actual Quantity (4600

units)

Standard Quantity (4600

units)

Input SQ SP STC AQ AP ATC SQ SP STC

Alpha 40 2 80 2200 1.8 3960 1840 2 3680

Beta 60 5 300 2500 6 15000 2760 5 13800

Gamma 20 1 20 920 1 920 920 1 920

120 400 5620 19880 5520 18400

Solution:

evaluate changing circumstances so that he can make modification in strategies of business.

Sensitivity analysis provide a platform through which managers can assess advantages

and disadvantages of upcoming situation so that enterprise can be ready to deal with threats and

grab opportunities. It becomes essential for business to have sensitivity analysis to improve its

performance and make each process effective. There are basically two techniques through

evaluation is done which includes local and global sensitivity analysis. In addition, this factorial

analysis helps business to determine each factors performance that assist organization to have

base for making modification.

It is widely used in organization to cope up with changing circumstances this results in

increments of performance of business. It provides various critical parts that gives manager

better decision-making skill, so he can take better actions to deal with unknown situations. It is

important for manager to use sensitivity analysis to get products and services better as compared

to previous. It will not only help the manager to get performance but eventually increase

productivity of organization by evaluating various affecting factors. All this helps the manager of

business to take corrective actions that can assist him to deal with uncertainity.

QUESTION 2

a) calculation of variances for the last month

Working Note

Standard Quantity (100 units) Actual Quantity (4600

units)

Standard Quantity (4600

units)

Input SQ SP STC AQ AP ATC SQ SP STC

Alpha 40 2 80 2200 1.8 3960 1840 2 3680

Beta 60 5 300 2500 6 15000 2760 5 13800

Gamma 20 1 20 920 1 920 920 1 920

120 400 5620 19880 5520 18400

Solution:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

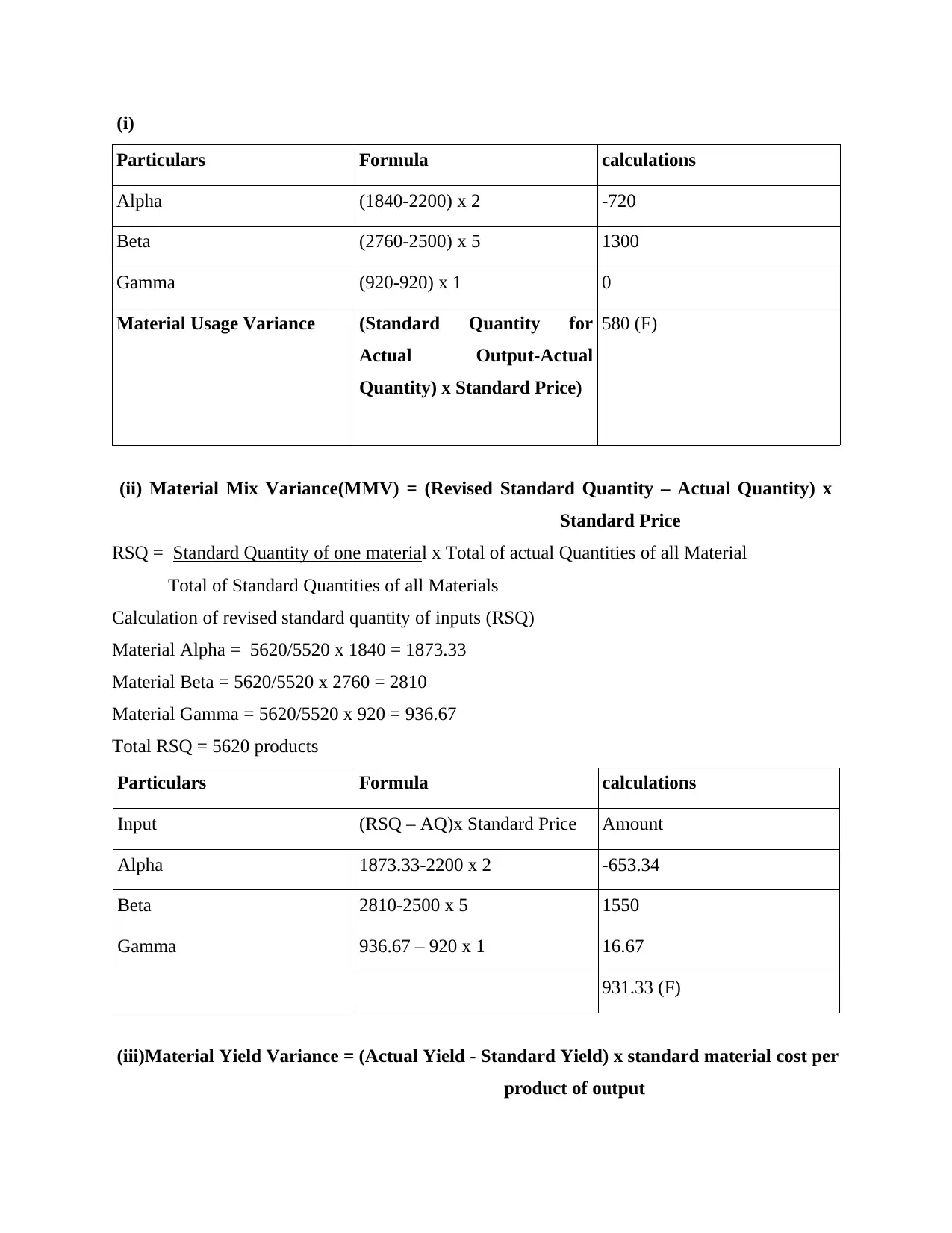

(i)

Particulars Formula calculations

Alpha (1840-2200) x 2 -720

Beta (2760-2500) x 5 1300

Gamma (920-920) x 1 0

Material Usage Variance (Standard Quantity for

Actual Output-Actual

Quantity) x Standard Price)

580 (F)

(ii) Material Mix Variance(MMV) = (Revised Standard Quantity – Actual Quantity) x

Standard Price

RSQ = Standard Quantity of one material x Total of actual Quantities of all Material

Total of Standard Quantities of all Materials

Calculation of revised standard quantity of inputs (RSQ)

Material Alpha = 5620/5520 x 1840 = 1873.33

Material Beta = 5620/5520 x 2760 = 2810

Material Gamma = 5620/5520 x 920 = 936.67

Total RSQ = 5620 products

Particulars Formula calculations

Input (RSQ – AQ)x Standard Price Amount

Alpha 1873.33-2200 x 2 -653.34

Beta 2810-2500 x 5 1550

Gamma 936.67 – 920 x 1 16.67

931.33 (F)

(iii)Material Yield Variance = (Actual Yield - Standard Yield) x standard material cost per

product of output

Particulars Formula calculations

Alpha (1840-2200) x 2 -720

Beta (2760-2500) x 5 1300

Gamma (920-920) x 1 0

Material Usage Variance (Standard Quantity for

Actual Output-Actual

Quantity) x Standard Price)

580 (F)

(ii) Material Mix Variance(MMV) = (Revised Standard Quantity – Actual Quantity) x

Standard Price

RSQ = Standard Quantity of one material x Total of actual Quantities of all Material

Total of Standard Quantities of all Materials

Calculation of revised standard quantity of inputs (RSQ)

Material Alpha = 5620/5520 x 1840 = 1873.33

Material Beta = 5620/5520 x 2760 = 2810

Material Gamma = 5620/5520 x 920 = 936.67

Total RSQ = 5620 products

Particulars Formula calculations

Input (RSQ – AQ)x Standard Price Amount

Alpha 1873.33-2200 x 2 -653.34

Beta 2810-2500 x 5 1550

Gamma 936.67 – 920 x 1 16.67

931.33 (F)

(iii)Material Yield Variance = (Actual Yield - Standard Yield) x standard material cost per

product of output

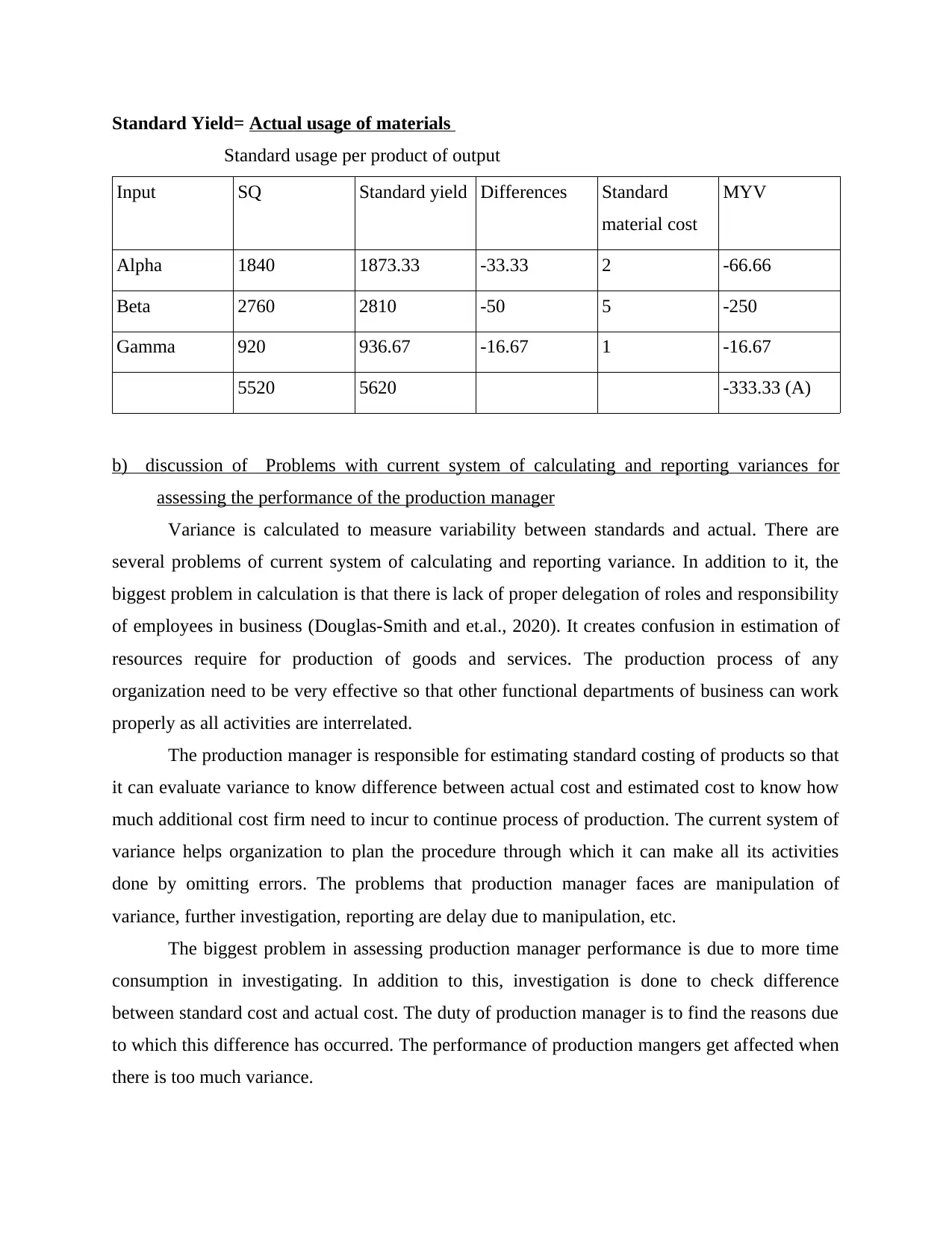

Standard Yield= Actual usage of materials

Standard usage per product of output

Input SQ Standard yield Differences Standard

material cost

MYV

Alpha 1840 1873.33 -33.33 2 -66.66

Beta 2760 2810 -50 5 -250

Gamma 920 936.67 -16.67 1 -16.67

5520 5620 -333.33 (A)

b) discussion of Problems with current system of calculating and reporting variances for

assessing the performance of the production manager

Variance is calculated to measure variability between standards and actual. There are

several problems of current system of calculating and reporting variance. In addition to it, the

biggest problem in calculation is that there is lack of proper delegation of roles and responsibility

of employees in business (Douglas-Smith and et.al., 2020). It creates confusion in estimation of

resources require for production of goods and services. The production process of any

organization need to be very effective so that other functional departments of business can work

properly as all activities are interrelated.

The production manager is responsible for estimating standard costing of products so that

it can evaluate variance to know difference between actual cost and estimated cost to know how

much additional cost firm need to incur to continue process of production. The current system of

variance helps organization to plan the procedure through which it can make all its activities

done by omitting errors. The problems that production manager faces are manipulation of

variance, further investigation, reporting are delay due to manipulation, etc.

The biggest problem in assessing production manager performance is due to more time

consumption in investigating. In addition to this, investigation is done to check difference

between standard cost and actual cost. The duty of production manager is to find the reasons due

to which this difference has occurred. The performance of production mangers get affected when

there is too much variance.

Standard usage per product of output

Input SQ Standard yield Differences Standard

material cost

MYV

Alpha 1840 1873.33 -33.33 2 -66.66

Beta 2760 2810 -50 5 -250

Gamma 920 936.67 -16.67 1 -16.67

5520 5620 -333.33 (A)

b) discussion of Problems with current system of calculating and reporting variances for

assessing the performance of the production manager

Variance is calculated to measure variability between standards and actual. There are

several problems of current system of calculating and reporting variance. In addition to it, the

biggest problem in calculation is that there is lack of proper delegation of roles and responsibility

of employees in business (Douglas-Smith and et.al., 2020). It creates confusion in estimation of

resources require for production of goods and services. The production process of any

organization need to be very effective so that other functional departments of business can work

properly as all activities are interrelated.

The production manager is responsible for estimating standard costing of products so that

it can evaluate variance to know difference between actual cost and estimated cost to know how

much additional cost firm need to incur to continue process of production. The current system of

variance helps organization to plan the procedure through which it can make all its activities

done by omitting errors. The problems that production manager faces are manipulation of

variance, further investigation, reporting are delay due to manipulation, etc.

The biggest problem in assessing production manager performance is due to more time

consumption in investigating. In addition to this, investigation is done to check difference

between standard cost and actual cost. The duty of production manager is to find the reasons due

to which this difference has occurred. The performance of production mangers get affected when

there is too much variance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The variance in price of raw material differs because production managers makes

calculation on the basis of past data and current price of raw material are determine by market

forces. So evaluating performance of production manager on the basis of system of variance is

not appropriate. The production manager can study external forces that affect the variation in

price differentiation to improve its performance. In addition to this, it also helps the managers to

save time which he has to bear in investigation.

Material usage, mix and yield variance makes production process accurate as it helps

manager to evaluate quantity of resources require to produce a single product. In regard to this,

this affect performance of manger positive and negatively both. The preparation of reports get

delay due to more time consumption in investigating reasons due to which changes have

occurred (Apunda and Ndede, 2020). With respect to this using 5 years ago estimation for

calculation of current standard costing can result into lack effect process. So The manager should

change base of standard costing so that he can properly estimate accurate price that doe not differ

much from actual cost of materials.

QUESTION 3

Zero based budgeting (ZBB) is a method used in calculating current year budget from

scratch. In addition to this is prepared by ranking old and new activities according to their

importance (Zero Based Budgeting (ZBB) - Overview & Advantages, 2021). Incremental

budgeting (IB) is technique which is used in preparing budget by making changes in last year's

calculations. In respect to this is made by making addition or reduction in expenses of

organization. Zero based and incremental budgeting are two most commonly used methods that

are implemented by various types of companies. There are various points on basis of which ZBB

and IB are differentiated such as base for budgeting, allocation of resources, wasteful expenses,

innovation, edge of preparation, training and time-consuming. These are the differences that

create quite differentiation between zero base budgeting and incremental budgeting.

In zero based budgeting managers require skill knowledge that prepared proper budget

for organization (Hastings, 2021). The biggest disadvantage of zero based budgeting is lack

expertise due to managers that are not properly trained and qualified. Additionally, it results in

more time consumption at each activity of enterprise because managers do not have much

practical knowledge of changing circumstances of business that reduces chance of expansion.

calculation on the basis of past data and current price of raw material are determine by market

forces. So evaluating performance of production manager on the basis of system of variance is

not appropriate. The production manager can study external forces that affect the variation in

price differentiation to improve its performance. In addition to this, it also helps the managers to

save time which he has to bear in investigation.

Material usage, mix and yield variance makes production process accurate as it helps

manager to evaluate quantity of resources require to produce a single product. In regard to this,

this affect performance of manger positive and negatively both. The preparation of reports get

delay due to more time consumption in investigating reasons due to which changes have

occurred (Apunda and Ndede, 2020). With respect to this using 5 years ago estimation for

calculation of current standard costing can result into lack effect process. So The manager should

change base of standard costing so that he can properly estimate accurate price that doe not differ

much from actual cost of materials.

QUESTION 3

Zero based budgeting (ZBB) is a method used in calculating current year budget from

scratch. In addition to this is prepared by ranking old and new activities according to their

importance (Zero Based Budgeting (ZBB) - Overview & Advantages, 2021). Incremental

budgeting (IB) is technique which is used in preparing budget by making changes in last year's

calculations. In respect to this is made by making addition or reduction in expenses of

organization. Zero based and incremental budgeting are two most commonly used methods that

are implemented by various types of companies. There are various points on basis of which ZBB

and IB are differentiated such as base for budgeting, allocation of resources, wasteful expenses,

innovation, edge of preparation, training and time-consuming. These are the differences that

create quite differentiation between zero base budgeting and incremental budgeting.

In zero based budgeting managers require skill knowledge that prepared proper budget

for organization (Hastings, 2021). The biggest disadvantage of zero based budgeting is lack

expertise due to managers that are not properly trained and qualified. Additionally, it results in

more time consumption at each activity of enterprise because managers do not have much

practical knowledge of changing circumstances of business that reduces chance of expansion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are several disadvantages of zero based budgeting which makes it unsuitable for firm.

Another drawback of ZBB is rigid as firm can not find this method suitable in every situation.

It's another demit is that its not appropriate in determining short term goals of organization.

Whereas incremental budgets are not that much adequate and fair to enhance efficiency

of business. In addition to this, IB assumes that all the activities and expenditures previously

identified are still required without evaluating current need of business. Further it enhances and

promotes the unnecessary expenses of business that is the biggest disadvantage of the IB. The

reason behind this is that all the departments of company tend to spend all monetary resources

which is allocated to respective managers. Furthermore, it discourages innovation of

organization because it just believes in making modification in old statements rather than trying

new structure. With respect to this enterprises fail to account changes according to external

factors that can affect firm. It also leads in wastage of resources of business as no proper

evaluation is exerted at initial stage of year which eventually result in variance of actual from

standards. In this type of budgeting system there are several unreal assumptions that reduce

effectiveness and efficiency of business (Ibrahim, 2019). Incremental budgeting can give adverse

effect on business concern in case of long term. In regard to this it hampers the potential growth

of firm which makes business.

There are various drawbacks of both incremental and zero based budgeting which makes

these techniques unsuitable for planning, coordinating and controlling. In addition to this,

organization always makes planning for its operations with help of formulating budget. As

budget gives estimated cost which helps business to identify limits of resources so that it can

arrange materials for its operations of business in specified time. It will lead to efficient

functioning of enterprise. IB and ZBB fails in formulating proper budget plan for firm .In

addition to this when an organization is unable to plan its required resources. It creates confusion

in managers of departments which result in lack of coordination and control n business

processes. It is very essential to have proper coordination among departments of businesses for

smooth functioning of firm (Miller, 2018). As the managers are departments are not qualified, so

they fail to establish good control over business activities.

These are the reason that proves that neither ZBB and IB provide perfect toll for

planning, coordinating and controlling.

Another drawback of ZBB is rigid as firm can not find this method suitable in every situation.

It's another demit is that its not appropriate in determining short term goals of organization.

Whereas incremental budgets are not that much adequate and fair to enhance efficiency

of business. In addition to this, IB assumes that all the activities and expenditures previously

identified are still required without evaluating current need of business. Further it enhances and

promotes the unnecessary expenses of business that is the biggest disadvantage of the IB. The

reason behind this is that all the departments of company tend to spend all monetary resources

which is allocated to respective managers. Furthermore, it discourages innovation of

organization because it just believes in making modification in old statements rather than trying

new structure. With respect to this enterprises fail to account changes according to external

factors that can affect firm. It also leads in wastage of resources of business as no proper

evaluation is exerted at initial stage of year which eventually result in variance of actual from

standards. In this type of budgeting system there are several unreal assumptions that reduce

effectiveness and efficiency of business (Ibrahim, 2019). Incremental budgeting can give adverse

effect on business concern in case of long term. In regard to this it hampers the potential growth

of firm which makes business.

There are various drawbacks of both incremental and zero based budgeting which makes

these techniques unsuitable for planning, coordinating and controlling. In addition to this,

organization always makes planning for its operations with help of formulating budget. As

budget gives estimated cost which helps business to identify limits of resources so that it can

arrange materials for its operations of business in specified time. It will lead to efficient

functioning of enterprise. IB and ZBB fails in formulating proper budget plan for firm .In

addition to this when an organization is unable to plan its required resources. It creates confusion

in managers of departments which result in lack of coordination and control n business

processes. It is very essential to have proper coordination among departments of businesses for

smooth functioning of firm (Miller, 2018). As the managers are departments are not qualified, so

they fail to establish good control over business activities.

These are the reason that proves that neither ZBB and IB provide perfect toll for

planning, coordinating and controlling.

REFERENCES

Books and Journals

Apunda, M. A. and Ndede, F. W., 2020. The effect of adoption of management accounting

practices on financial performance of commercial parastatals in Kenya. International

Academic Journal of Economics and Finance. 3(6). pp.119-130.

Dahal, R. K., Bhattarai, G. and Karki, D., 2020. Management Accounting Techniques on

Rationalize Decisions in the Nepalese Listed Manufacturing Companies. Researcher: A

Research Journal of Culture and Society. 4(1). pp.112-128.

Douglas-Smith, D. and et.al., 2020. Certain trends in uncertainty and sensitivity analysis: An

overview of software tools and techniques. Environmental Modelling & Software. 124.

p.104588.

Hastings, N.A.J., 2021. Maintenance organization and budget. In Physical Asset

Management (pp. 381-408). Springer, Cham.

Ibrahim, M.M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Miller, G., 2018. Performance based budgeting. Routledge.

Park, S., 2020. Managerial Accounting for Decision Making (Vol. 7). Seohee Academy.

Online

Zero Based Budgeting (ZBB) - Overview & Advantages. 2021. Online. Available through:

<https://cleartax.in/s/zero-based-budgeting>.

Books and Journals

Apunda, M. A. and Ndede, F. W., 2020. The effect of adoption of management accounting

practices on financial performance of commercial parastatals in Kenya. International

Academic Journal of Economics and Finance. 3(6). pp.119-130.

Dahal, R. K., Bhattarai, G. and Karki, D., 2020. Management Accounting Techniques on

Rationalize Decisions in the Nepalese Listed Manufacturing Companies. Researcher: A

Research Journal of Culture and Society. 4(1). pp.112-128.

Douglas-Smith, D. and et.al., 2020. Certain trends in uncertainty and sensitivity analysis: An

overview of software tools and techniques. Environmental Modelling & Software. 124.

p.104588.

Hastings, N.A.J., 2021. Maintenance organization and budget. In Physical Asset

Management (pp. 381-408). Springer, Cham.

Ibrahim, M.M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Miller, G., 2018. Performance based budgeting. Routledge.

Park, S., 2020. Managerial Accounting for Decision Making (Vol. 7). Seohee Academy.

Online

Zero Based Budgeting (ZBB) - Overview & Advantages. 2021. Online. Available through:

<https://cleartax.in/s/zero-based-budgeting>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.