Detailed Financial Performance Analysis Report: Tesco & Sainsbury

VerifiedAdded on 2022/12/16

|17

|4331

|1

Report

AI Summary

This report presents a comprehensive financial performance analysis of Tesco and Sainsbury, two prominent companies in the grocery retail sector. The analysis begins with a detailed examination of financial ratios, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, price-earnings ratio, and earnings per share, comparing their performance over the years 2018 and 2019. The report then delves into the application of the balanced scorecard framework, evaluating its perspectives and outlining its advantages and disadvantages for strategic management. Finally, the report explores the adoption of integrated reporting (IR), discussing its benefits and challenges for the selected organizations. The report aims to provide insights into the financial health and performance of Tesco and Sainsbury using various analytical tools and frameworks.

Financial

Performance

Analysis

Performance

Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Ratio analysis for businesses:......................................................................................................3

TASK 2............................................................................................................................................8

Balance score card:......................................................................................................................8

TASK 3..........................................................................................................................................11

Integrated reporting:..................................................................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Ratio analysis for businesses:......................................................................................................3

TASK 2............................................................................................................................................8

Balance score card:......................................................................................................................8

TASK 3..........................................................................................................................................11

Integrated reporting:..................................................................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The aspects in which a firm controls and tracks financial statements within an entity are

referred to as financial performance management (Gartenberg, Prat and Serafeim, 2019).

Financial performance management's key objective is to equate real outcomes to projections and

predictions and make corrections as required. Firms are well able to accomplish their targets by

help of proper management of outcomes. Basically, financial performance is a subjective

indicator of a company's ability to produce money from its primary mode of operation. The

concept is often used as a broad indicator of a company's overall financial performance over

time. The report is based on different kinds of tasks which have been performed. The main

organization which has been chosen for report is Tesco. This company was founded in year 1919

and operates at a global level. This company offers different kinds of grocery items with wider

portfolio of products. The objective of project report is to analyze financial performance of

chosen company with financial and non-financial aspects. There are three main tasks in report

under which first task is based on analyzing financial performance of company by help of ratio

analysis. In the second task, detailed analysis of balance scorecard matrix has been done. In the

end of report, critical analysis of the benefits and challenges of adopting Integrated Reporting

(IR) for selected organization has been done.

TASK 1

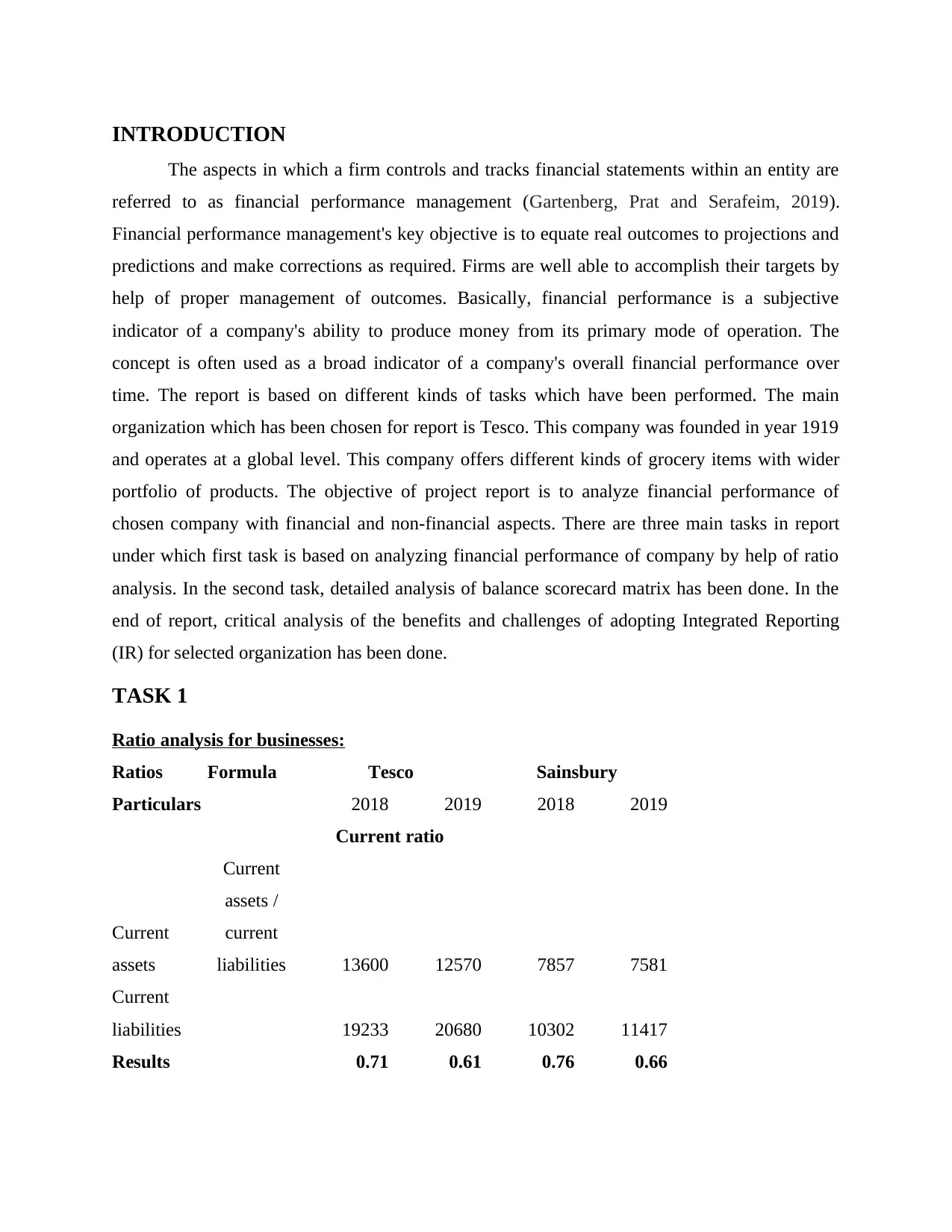

Ratio analysis for businesses:

Ratios Formula Tesco Sainsbury

Particulars 2018 2019 2018 2019

Current ratio

Current

assets

Current

assets /

current

liabilities 13600 12570 7857 7581

Current

liabilities 19233 20680 10302 11417

Results 0.71 0.61 0.76 0.66

The aspects in which a firm controls and tracks financial statements within an entity are

referred to as financial performance management (Gartenberg, Prat and Serafeim, 2019).

Financial performance management's key objective is to equate real outcomes to projections and

predictions and make corrections as required. Firms are well able to accomplish their targets by

help of proper management of outcomes. Basically, financial performance is a subjective

indicator of a company's ability to produce money from its primary mode of operation. The

concept is often used as a broad indicator of a company's overall financial performance over

time. The report is based on different kinds of tasks which have been performed. The main

organization which has been chosen for report is Tesco. This company was founded in year 1919

and operates at a global level. This company offers different kinds of grocery items with wider

portfolio of products. The objective of project report is to analyze financial performance of

chosen company with financial and non-financial aspects. There are three main tasks in report

under which first task is based on analyzing financial performance of company by help of ratio

analysis. In the second task, detailed analysis of balance scorecard matrix has been done. In the

end of report, critical analysis of the benefits and challenges of adopting Integrated Reporting

(IR) for selected organization has been done.

TASK 1

Ratio analysis for businesses:

Ratios Formula Tesco Sainsbury

Particulars 2018 2019 2018 2019

Current ratio

Current

assets

Current

assets /

current

liabilities 13600 12570 7857 7581

Current

liabilities 19233 20680 10302 11417

Results 0.71 0.61 0.76 0.66

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

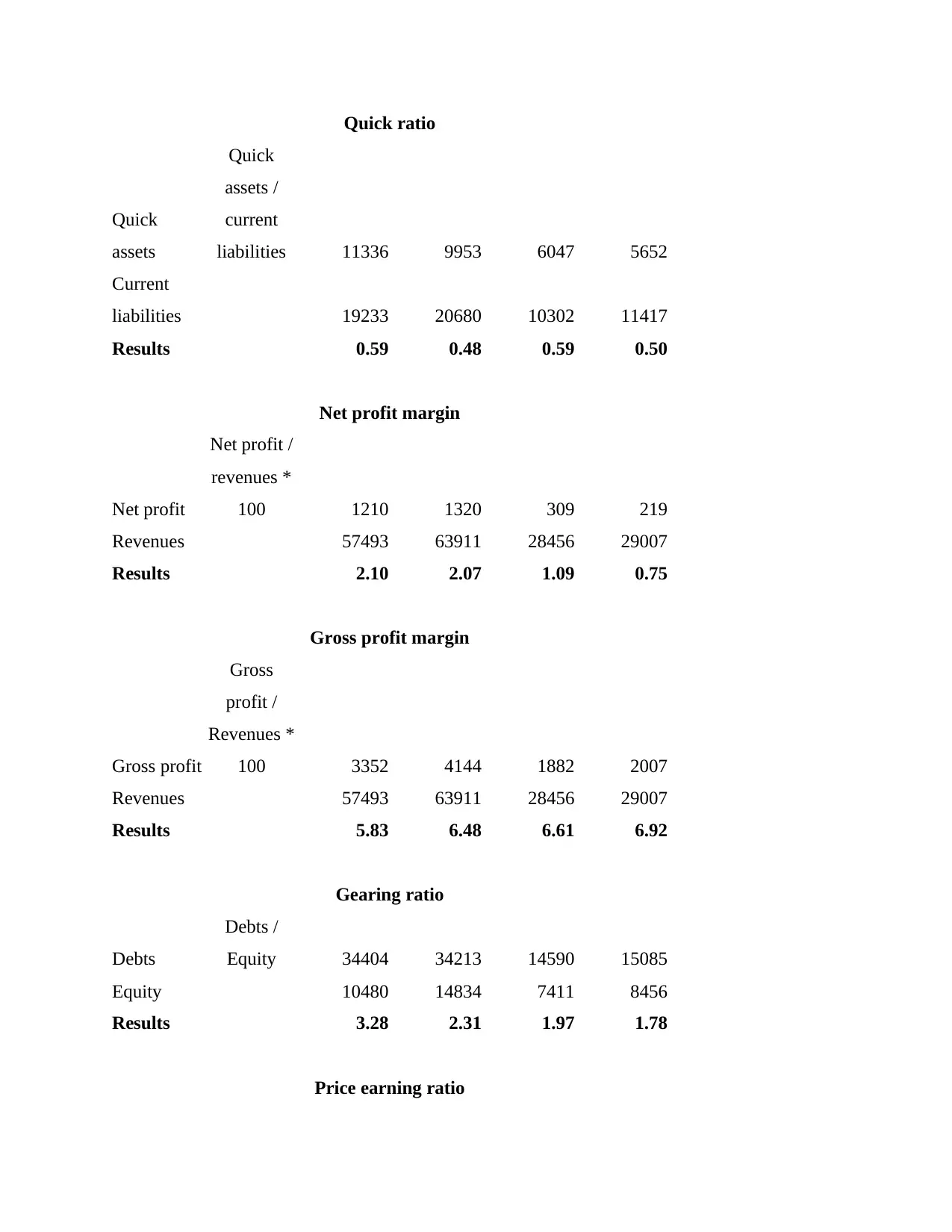

Quick ratio

Quick

assets

Quick

assets /

current

liabilities 11336 9953 6047 5652

Current

liabilities 19233 20680 10302 11417

Results 0.59 0.48 0.59 0.50

Net profit margin

Net profit

Net profit /

revenues *

100 1210 1320 309 219

Revenues 57493 63911 28456 29007

Results 2.10 2.07 1.09 0.75

Gross profit margin

Gross profit

Gross

profit /

Revenues *

100 3352 4144 1882 2007

Revenues 57493 63911 28456 29007

Results 5.83 6.48 6.61 6.92

Gearing ratio

Debts

Debts /

Equity 34404 34213 14590 15085

Equity 10480 14834 7411 8456

Results 3.28 2.31 1.97 1.78

Price earning ratio

Quick

assets

Quick

assets /

current

liabilities 11336 9953 6047 5652

Current

liabilities 19233 20680 10302 11417

Results 0.59 0.48 0.59 0.50

Net profit margin

Net profit

Net profit /

revenues *

100 1210 1320 309 219

Revenues 57493 63911 28456 29007

Results 2.10 2.07 1.09 0.75

Gross profit margin

Gross profit

Gross

profit /

Revenues *

100 3352 4144 1882 2007

Revenues 57493 63911 28456 29007

Results 5.83 6.48 6.61 6.92

Gearing ratio

Debts

Debts /

Equity 34404 34213 14590 15085

Equity 10480 14834 7411 8456

Results 3.28 2.31 1.97 1.78

Price earning ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

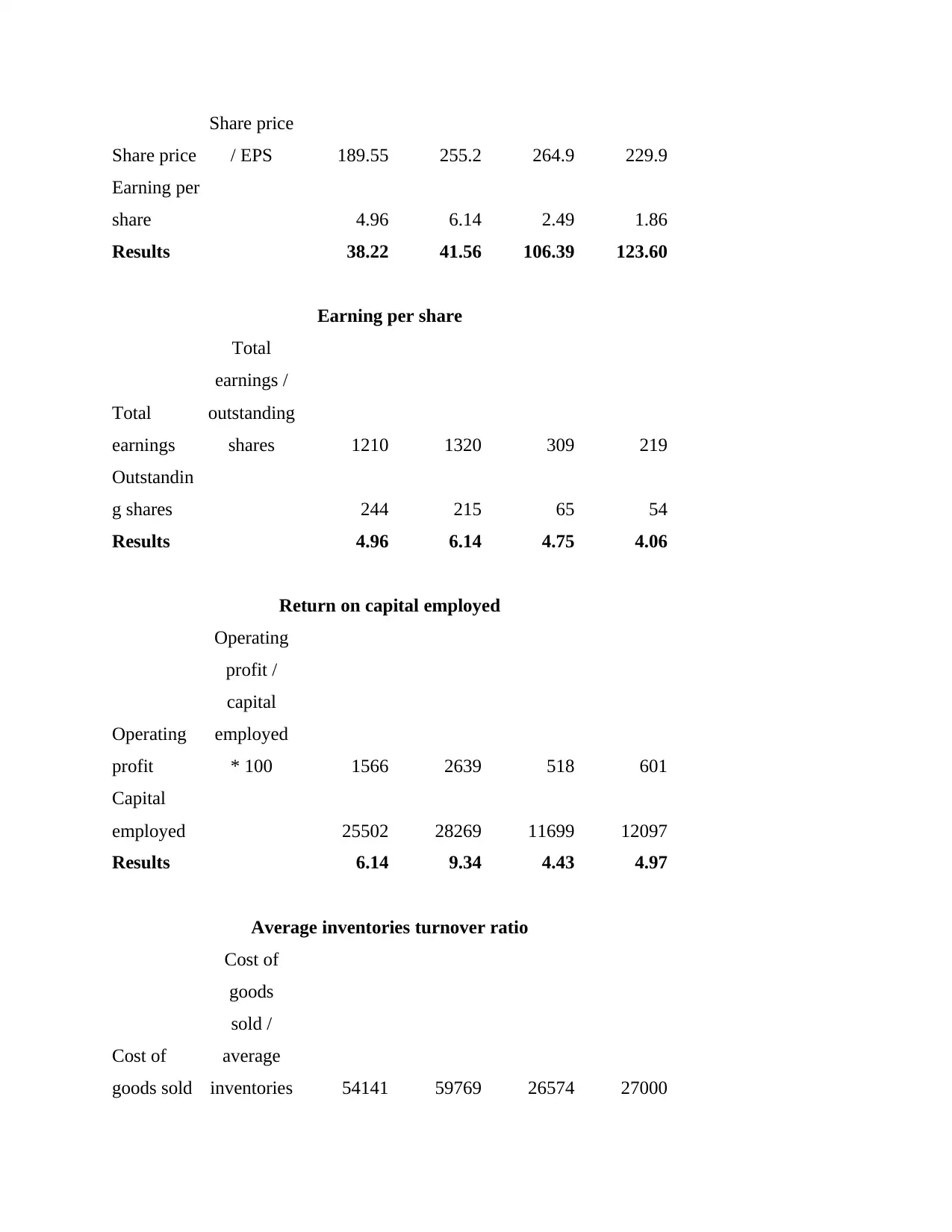

Share price

Share price

/ EPS 189.55 255.2 264.9 229.9

Earning per

share 4.96 6.14 2.49 1.86

Results 38.22 41.56 106.39 123.60

Earning per share

Total

earnings

Total

earnings /

outstanding

shares 1210 1320 309 219

Outstandin

g shares 244 215 65 54

Results 4.96 6.14 4.75 4.06

Return on capital employed

Operating

profit

Operating

profit /

capital

employed

* 100 1566 2639 518 601

Capital

employed 25502 28269 11699 12097

Results 6.14 9.34 4.43 4.97

Average inventories turnover ratio

Cost of

goods sold

Cost of

goods

sold /

average

inventories 54141 59769 26574 27000

Share price

/ EPS 189.55 255.2 264.9 229.9

Earning per

share 4.96 6.14 2.49 1.86

Results 38.22 41.56 106.39 123.60

Earning per share

Total

earnings

Total

earnings /

outstanding

shares 1210 1320 309 219

Outstandin

g shares 244 215 65 54

Results 4.96 6.14 4.75 4.06

Return on capital employed

Operating

profit

Operating

profit /

capital

employed

* 100 1566 2639 518 601

Capital

employed 25502 28269 11699 12097

Results 6.14 9.34 4.43 4.97

Average inventories turnover ratio

Cost of

goods sold

Cost of

goods

sold /

average

inventories 54141 59769 26574 27000

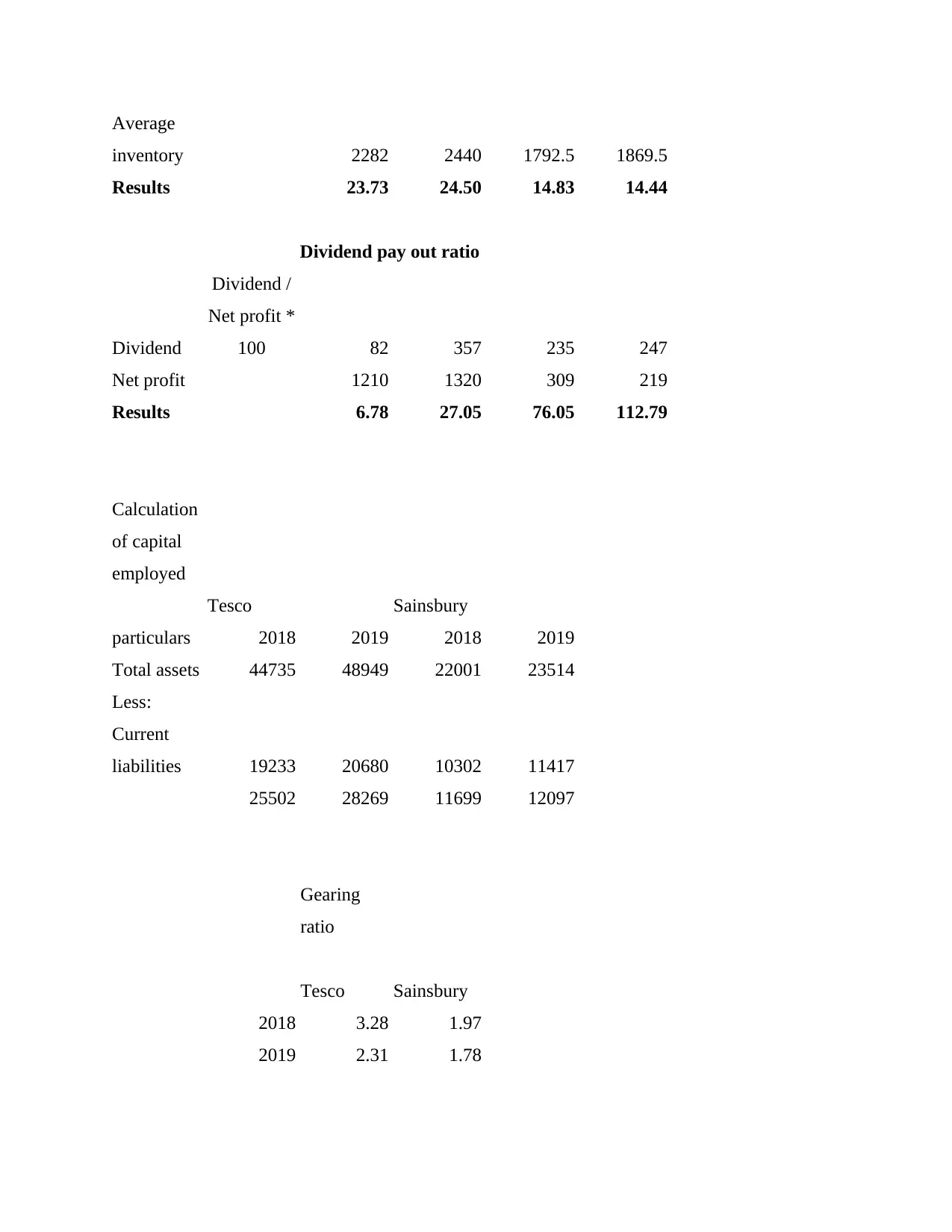

Average

inventory 2282 2440 1792.5 1869.5

Results 23.73 24.50 14.83 14.44

Dividend pay out ratio

Dividend

Dividend /

Net profit *

100 82 357 235 247

Net profit 1210 1320 309 219

Results 6.78 27.05 76.05 112.79

Calculation

of capital

employed

Tesco Sainsbury

particulars 2018 2019 2018 2019

Total assets 44735 48949 22001 23514

Less:

Current

liabilities 19233 20680 10302 11417

25502 28269 11699 12097

Gearing

ratio

Tesco Sainsbury

2018 3.28 1.97

2019 2.31 1.78

inventory 2282 2440 1792.5 1869.5

Results 23.73 24.50 14.83 14.44

Dividend pay out ratio

Dividend

Dividend /

Net profit *

100 82 357 235 247

Net profit 1210 1320 309 219

Results 6.78 27.05 76.05 112.79

Calculation

of capital

employed

Tesco Sainsbury

particulars 2018 2019 2018 2019

Total assets 44735 48949 22001 23514

Less:

Current

liabilities 19233 20680 10302 11417

25502 28269 11699 12097

Gearing

ratio

Tesco Sainsbury

2018 3.28 1.97

2019 2.31 1.78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current ratio: It is about which views how much ability businesses has for paying debt.

It is about current assets, current liability. It is about which views how much cash businesses has

for pay debt. It is known for working capital ratio. This data is about Tesco, Sainsbury. This data

views about Tesco has 0.71 for 2018, 0.61 for 2019. Sainsbury has 0.76 for 2018, 0.66 for 2019.

It is about Sainsbury has better performance for 2018, 2019.

Quick ratio: It is about which views how much cash businesses have for pay debt. It

includes liquid assets which is cash, it not includes inventory, prepaid expense for pay debt (Le,

Du and Tran, 2018). It is about how much ability businesses has for pay debt. This is about

Tesco, Sainsbury. This data views about Tesco 0.59 for 2018, 0.48 for 2019. Sainsbury has 0.59

for 2018, 0.50 for 2019. it is about Sainsbury has more cash for pay it debt. Sainsbury has better

performance which helps for generating more profit.

Gross profit ratio: It is about which views how much profit businesses generate for

gross profit by sale. It views relation for gross profit, sale. It is about profit which businesses

generate for their sale. This is about Tesco, Sainsbury. This data views about Tesco has 5.83 for

2018, 6.48 for 2019. Sainsbury has 6.61 for 2018, 6.92 for 2019. it is about Sainsbury has better

performance for 2018, 2019.

Net profit ratio: It is about which views how much profit businesses generate for net

profit by sale. It views relation for net profit, sale. It is about profit which businesses generate for

their sale. This is about Tesco, Sainsbury. This data views about Tesco 2.10 for 2018, 2.07 for

2019. Sainsbury has 1.09 for 2018, 0.75 for 2019. Tesco has better performance for 2018, 2019.

Gearing ratio: It is about which views equity, debt, fund which borrow by the

businesses. Gearing ratio is financial ratio which helps for knowing businesses leverage, amount

for fund borrow by investor which helps for running businesses activities. It is about equity, debt,

fund which businesses borrow for generating profit. It is about Tesco, Sainsbury. Tesco has 3.28

for 2018, 2.31 for 2019. Sainsbury has 1.97 for 2018, 1.78 for 2019. Tesco has better

performance for the 2018, 2019.

Price earnings ratio: It is about how much amount investor invests for businesses for

achieving businesses earning. This is price earnings ratio which views various prices. It is about

which views how much investor willing for pay for earning. This is about Tesco, Sainsbury.

Tesco has 38.22 for 2018, 41.56 for 2019. Sainsbury has 109.39 for 2018, 123.60 for 2019.

Sainsbury has better performance for 2018, 2019.

It is about current assets, current liability. It is about which views how much cash businesses has

for pay debt. It is known for working capital ratio. This data is about Tesco, Sainsbury. This data

views about Tesco has 0.71 for 2018, 0.61 for 2019. Sainsbury has 0.76 for 2018, 0.66 for 2019.

It is about Sainsbury has better performance for 2018, 2019.

Quick ratio: It is about which views how much cash businesses have for pay debt. It

includes liquid assets which is cash, it not includes inventory, prepaid expense for pay debt (Le,

Du and Tran, 2018). It is about how much ability businesses has for pay debt. This is about

Tesco, Sainsbury. This data views about Tesco 0.59 for 2018, 0.48 for 2019. Sainsbury has 0.59

for 2018, 0.50 for 2019. it is about Sainsbury has more cash for pay it debt. Sainsbury has better

performance which helps for generating more profit.

Gross profit ratio: It is about which views how much profit businesses generate for

gross profit by sale. It views relation for gross profit, sale. It is about profit which businesses

generate for their sale. This is about Tesco, Sainsbury. This data views about Tesco has 5.83 for

2018, 6.48 for 2019. Sainsbury has 6.61 for 2018, 6.92 for 2019. it is about Sainsbury has better

performance for 2018, 2019.

Net profit ratio: It is about which views how much profit businesses generate for net

profit by sale. It views relation for net profit, sale. It is about profit which businesses generate for

their sale. This is about Tesco, Sainsbury. This data views about Tesco 2.10 for 2018, 2.07 for

2019. Sainsbury has 1.09 for 2018, 0.75 for 2019. Tesco has better performance for 2018, 2019.

Gearing ratio: It is about which views equity, debt, fund which borrow by the

businesses. Gearing ratio is financial ratio which helps for knowing businesses leverage, amount

for fund borrow by investor which helps for running businesses activities. It is about equity, debt,

fund which businesses borrow for generating profit. It is about Tesco, Sainsbury. Tesco has 3.28

for 2018, 2.31 for 2019. Sainsbury has 1.97 for 2018, 1.78 for 2019. Tesco has better

performance for the 2018, 2019.

Price earnings ratio: It is about how much amount investor invests for businesses for

achieving businesses earning. This is price earnings ratio which views various prices. It is about

which views how much investor willing for pay for earning. This is about Tesco, Sainsbury.

Tesco has 38.22 for 2018, 41.56 for 2019. Sainsbury has 109.39 for 2018, 123.60 for 2019.

Sainsbury has better performance for 2018, 2019.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Earning per share: It is about how much profit businesses earn for their share. It views

business profit which it earns for share (Alexander, 2018). It is about which views how much

profit businesses earn for share which it gives for shareholder. It is about Tesco, Sainsbury.

Tesco has 4.96 for 2018, 6.14 for 2019. Sainsbury has 4.75 for 2018, 4.06 for 2019. Tesco has

better performance for 2018, 2019 for businesses.

TASK 2

Balance score card:

Balanced Scorecard- Balanced Scorecard refers to a framework in which the

implementation and management of the strategy can be done so that the measures are taken in

order to boost the overall level of performance effectively and efficiently in the right manner

(Albuhisi and Abdallah, 2018). Therefore, it is important for the organizations that the use of this

particular framework can be made so that the attainment of the short-term, medium-term and

long-term goals and objectives can be made in a proper manner. This model was developed by

Kaplan and Norton in the year 1992 and is one of the most famous frameworks which are used in

order to assess the overall level of performance effectively and efficiently and therefore help in

the attainment of the goals and objectives.

In the context of Tesco and Sainsbury's it is an important system which is required to be

implemented within the processes and systems and therefore this will help the management in

ensuring that the strategic implementation can be made effectively and efficiently. Therefore, the

use of this system is essential for both of the organizations because through it the measurement

of the overall performance level has to be done and therefore the attainment of the goals and

objectives in the future can be made.

There are multiple perspectives which are concerned with the Balanced Scorecard. The

analysis of these particular perspectives can be explained in the following manner-

Financial- These are the higher-level of financial perspectives which are required to be

considered by the organizations and therefore this can be quite helpful for them in ensuring that

they can manage their position of funds in the right manner (Maqbool and Zameer, 2018). This

will be helpful in the attainment of the overall goals and objectives. Here, the management of

Tesco and Sainsbury does both have to consider these perspectives and this will lead towards the

better management of the finances within both of the companies.

business profit which it earns for share (Alexander, 2018). It is about which views how much

profit businesses earn for share which it gives for shareholder. It is about Tesco, Sainsbury.

Tesco has 4.96 for 2018, 6.14 for 2019. Sainsbury has 4.75 for 2018, 4.06 for 2019. Tesco has

better performance for 2018, 2019 for businesses.

TASK 2

Balance score card:

Balanced Scorecard- Balanced Scorecard refers to a framework in which the

implementation and management of the strategy can be done so that the measures are taken in

order to boost the overall level of performance effectively and efficiently in the right manner

(Albuhisi and Abdallah, 2018). Therefore, it is important for the organizations that the use of this

particular framework can be made so that the attainment of the short-term, medium-term and

long-term goals and objectives can be made in a proper manner. This model was developed by

Kaplan and Norton in the year 1992 and is one of the most famous frameworks which are used in

order to assess the overall level of performance effectively and efficiently and therefore help in

the attainment of the goals and objectives.

In the context of Tesco and Sainsbury's it is an important system which is required to be

implemented within the processes and systems and therefore this will help the management in

ensuring that the strategic implementation can be made effectively and efficiently. Therefore, the

use of this system is essential for both of the organizations because through it the measurement

of the overall performance level has to be done and therefore the attainment of the goals and

objectives in the future can be made.

There are multiple perspectives which are concerned with the Balanced Scorecard. The

analysis of these particular perspectives can be explained in the following manner-

Financial- These are the higher-level of financial perspectives which are required to be

considered by the organizations and therefore this can be quite helpful for them in ensuring that

they can manage their position of funds in the right manner (Maqbool and Zameer, 2018). This

will be helpful in the attainment of the overall goals and objectives. Here, the management of

Tesco and Sainsbury does both have to consider these perspectives and this will lead towards the

better management of the finances within both of the companies.

Customer- These are the perspectives which are directly linked with the customers of the

organization. Therefore, it is crucial for the firms that they are able to give adequate importance

to the customers and thus in this way it can be helpful for the management of both Tesco and

Sainsbury's so that they can make sure that the application of a wide range of strategies and

methods can be made so that the satisfaction level of the customers can be enhance in a right

manner.

Internal processes- These are the wide range of measures which are required to be

undertaken so that the organizations can make sure that the improvement in the overall level of

internal processes can be made effectively and efficiently (Mahrani and Soewarno, 2018). Thus,

in this way it can be said that for both Tesco and Sainsbury's it is important that the internal

processes can be given priority so that the attainment of a higher-level of performance can be

done in a proper manner. Therefore, for the overall level of improvement in both of the

companies it is crucial to bring improvement in these processes.

Organizational capacity- These are the wide range of measures which can be

undertaken in order to ensure that there can be a substantial increase in the overall organizational

capacity. Thus, In this way it can be said that the management of Tesco and Sainsbury's are

required to make sure that they are able to bring an overall level of improvement in the

organizational capacity in a proper manner.

There are various types of advantages and disadvantages of making the use of the

Balanced Scorecard Model. Therefore, In this way there are following advantages and

disadvantages of making the use of this particular model-

Advantages-

Visual picture of the strategy- The use of the Balanced Scorecard model can be made in

order to ensure that a visual picture of the strategy can be made effectively and

efficiently. Thus, In this way the managers of Tesco and Sainsbury's are able to make

sure that they can provide an appropriate picture of the strategy they will use.

Easier data collection- Use of the Balanced Scorecard model is quite helpful in ensuring

that the data collection can be done effectively and efficiently. Therefore, for the

managers of Tesco and Sainsbury's it will be helpful in ensuring that the collection of the

data can be done in a proper way.

organization. Therefore, it is crucial for the firms that they are able to give adequate importance

to the customers and thus in this way it can be helpful for the management of both Tesco and

Sainsbury's so that they can make sure that the application of a wide range of strategies and

methods can be made so that the satisfaction level of the customers can be enhance in a right

manner.

Internal processes- These are the wide range of measures which are required to be

undertaken so that the organizations can make sure that the improvement in the overall level of

internal processes can be made effectively and efficiently (Mahrani and Soewarno, 2018). Thus,

in this way it can be said that for both Tesco and Sainsbury's it is important that the internal

processes can be given priority so that the attainment of a higher-level of performance can be

done in a proper manner. Therefore, for the overall level of improvement in both of the

companies it is crucial to bring improvement in these processes.

Organizational capacity- These are the wide range of measures which can be

undertaken in order to ensure that there can be a substantial increase in the overall organizational

capacity. Thus, In this way it can be said that the management of Tesco and Sainsbury's are

required to make sure that they are able to bring an overall level of improvement in the

organizational capacity in a proper manner.

There are various types of advantages and disadvantages of making the use of the

Balanced Scorecard Model. Therefore, In this way there are following advantages and

disadvantages of making the use of this particular model-

Advantages-

Visual picture of the strategy- The use of the Balanced Scorecard model can be made in

order to ensure that a visual picture of the strategy can be made effectively and

efficiently. Thus, In this way the managers of Tesco and Sainsbury's are able to make

sure that they can provide an appropriate picture of the strategy they will use.

Easier data collection- Use of the Balanced Scorecard model is quite helpful in ensuring

that the data collection can be done effectively and efficiently. Therefore, for the

managers of Tesco and Sainsbury's it will be helpful in ensuring that the collection of the

data can be done in a proper way.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Easier strategy reporting- Balanced Scorecard model is helpful in leading towards

easier strategy reporting (Chen, 2018). In the context of Tesco and Sainsbury's, it can be

helpful so that the strategy reports can be prepared properly and therefore the appropriate

actions can be taken accordingly.

Easier to train- Using Balanced Scorecard model can help a lot in ensuring that the

training can be provided in an appropriate manner. For the management of Tesco and

Sainsbury's, this can be quite useful so that the proper training is provided to the various

types of employees.

Disadvantages-

Less focus on the external factors and competitors- The use of Balanced Scorecard

model leads towards less focus on the external factors and competitors. This is so because

the use of this model is helpful for the analysis of the internal situation within an

organization. Thus, In Tesco and Sainsbury's this creates a disadvantage.

Lack of risk analysis- With the use of Balanced Scorecard model there is a very less

focus of the organizations on the overall risk analysis (Chowdhury, Rana, Akter and

Hoque, 2018). This is so because using this model can lead towards improper assessment

of the level of risks which are present within the company. Therefore, In Tesco and

Sainsbury's a disadvantage is created due to this particular reason.

Strategy Map/KPIs are hard to maintain- Using the Balanced Scorecard model can

create a lot of problems and difficulties because the Strategy Map and KPIs cannot be

maintained easily within the organization. Thus, In this way the management of Tesco

and Sainsbury's can find it difficult to appropriately make the use of Strategies effectively

and efficiently.

Cannot work without cultural shifts- The use of the Balanced Scorecard model is not

helpful when the organization's employees are not cooperating in the cultural shift. In this

way, the managers of Tesco and Sainsbury's can find it difficult because their employees

will have to adjust according to the change which is required to be implemented within

the organization.

easier strategy reporting (Chen, 2018). In the context of Tesco and Sainsbury's, it can be

helpful so that the strategy reports can be prepared properly and therefore the appropriate

actions can be taken accordingly.

Easier to train- Using Balanced Scorecard model can help a lot in ensuring that the

training can be provided in an appropriate manner. For the management of Tesco and

Sainsbury's, this can be quite useful so that the proper training is provided to the various

types of employees.

Disadvantages-

Less focus on the external factors and competitors- The use of Balanced Scorecard

model leads towards less focus on the external factors and competitors. This is so because

the use of this model is helpful for the analysis of the internal situation within an

organization. Thus, In Tesco and Sainsbury's this creates a disadvantage.

Lack of risk analysis- With the use of Balanced Scorecard model there is a very less

focus of the organizations on the overall risk analysis (Chowdhury, Rana, Akter and

Hoque, 2018). This is so because using this model can lead towards improper assessment

of the level of risks which are present within the company. Therefore, In Tesco and

Sainsbury's a disadvantage is created due to this particular reason.

Strategy Map/KPIs are hard to maintain- Using the Balanced Scorecard model can

create a lot of problems and difficulties because the Strategy Map and KPIs cannot be

maintained easily within the organization. Thus, In this way the management of Tesco

and Sainsbury's can find it difficult to appropriately make the use of Strategies effectively

and efficiently.

Cannot work without cultural shifts- The use of the Balanced Scorecard model is not

helpful when the organization's employees are not cooperating in the cultural shift. In this

way, the managers of Tesco and Sainsbury's can find it difficult because their employees

will have to adjust according to the change which is required to be implemented within

the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

Integrated reporting:

Integrated reporting is about which is corporate communication which is process for

communication, which is about value creation (Bontis, Ciambotti, Palazzi and Sgro 2018).

Integrated report is concise communication about how businesses strategy, governance,

performance lead for creation for value for short, medium, long. It is about integrated views for

business performance for both financial, value relevant data. Integrated reporting gives greater

context for performance data which views relevant information which fit for businesses which

helps businesses for strategic decision making. It is about while communication views

performance by IR it will be benefit for shareholders, it is necessary for them to gives financial

capital allocation. IR helps for financial, sustainability. It is framework which investor,

shareholder using for running businesses activities. Capitalism is about efficient allocation for

capital for return for investor.

Integrated reporting refers to the coordination between the company and the production process.

There is succinct detail about how corporate management, governance and results contribute for

the short and long-term objectives (Cho, Chung and Young, 2019). The portrayal in single

instance of the enterprise's financial as well as non results. In the light of non-financial data like

the way companies perform the economic, social, and leadership criteria, this is more useful.

This will help to assess the key market performance and productivity of the shareholders and the

various parties involved. This is crucial in assessing the organization's longevity and overall

success. It aims to improve the development of reports in order to provide holistic reporting in

order to provide business value. Many considerations other than the financial facets of the

business often take this into consideration. The IIRC, the world's powerful association of

regulators, investors and enterprises, supports this in order to exchange more information on

business reporting developments. In the form of the Tesco survey, the proposal for businesses to

understand the problem in several respects depends not only on a corporate report.

It is about which businesses manage for financial capital which investor gives for

generate value for generate by other financial data, trademark, natural resource. IR is about

growing realization which is for wide range factor which view for value businesses, these are

financial, tangible for nature which is easy for account for financial statements while intellectual

capital, competition. IR is growing which is for wide range for element for value for the

Integrated reporting:

Integrated reporting is about which is corporate communication which is process for

communication, which is about value creation (Bontis, Ciambotti, Palazzi and Sgro 2018).

Integrated report is concise communication about how businesses strategy, governance,

performance lead for creation for value for short, medium, long. It is about integrated views for

business performance for both financial, value relevant data. Integrated reporting gives greater

context for performance data which views relevant information which fit for businesses which

helps businesses for strategic decision making. It is about while communication views

performance by IR it will be benefit for shareholders, it is necessary for them to gives financial

capital allocation. IR helps for financial, sustainability. It is framework which investor,

shareholder using for running businesses activities. Capitalism is about efficient allocation for

capital for return for investor.

Integrated reporting refers to the coordination between the company and the production process.

There is succinct detail about how corporate management, governance and results contribute for

the short and long-term objectives (Cho, Chung and Young, 2019). The portrayal in single

instance of the enterprise's financial as well as non results. In the light of non-financial data like

the way companies perform the economic, social, and leadership criteria, this is more useful.

This will help to assess the key market performance and productivity of the shareholders and the

various parties involved. This is crucial in assessing the organization's longevity and overall

success. It aims to improve the development of reports in order to provide holistic reporting in

order to provide business value. Many considerations other than the financial facets of the

business often take this into consideration. The IIRC, the world's powerful association of

regulators, investors and enterprises, supports this in order to exchange more information on

business reporting developments. In the form of the Tesco survey, the proposal for businesses to

understand the problem in several respects depends not only on a corporate report.

It is about which businesses manage for financial capital which investor gives for

generate value for generate by other financial data, trademark, natural resource. IR is about

growing realization which is for wide range factor which view for value businesses, these are

financial, tangible for nature which is easy for account for financial statements while intellectual

capital, competition. IR is growing which is for wide range for element for value for the

businesses. These are financial for nature which is easy for account for financial statements

which is about intellectual capital, competition. IR which broad, large consequences for decision

for businesses which is base for factor, in order for create sustains value for businesses. IR

enable for businesses for communicate for clear, articulate way how it is for resource, which is

using for generate value which helps investor for manage risk, allocate resource for most

efficiently. It is necessary, for increasing reporting for financial data for ecological data.

Integrated report is about which is necessary communication about how businesses strategy,

governance, performance generate for investor, shareholder for businesses. It helps businesses

for improving their communication for various activities.

It is about achieving knowledge about businesses which helps for better performance

which helps for higher profitability for businesses (Paniagua, Rivelles and Sapena, 2018). In

context to Tesco, Sainsbury these businesses using IR for knowing how businesses has better

performance. It views about various activities for the businesses. It is about which businesses

using for their strategic decision. This is about businesses using these data for knowing for

investor about businesses strategy. Investor is who invest their fund for running activities for

businesses. Investor views businesses strategy which helps for knowhow businesses has better

performance. Investor views how businesses using fund which helps them for generating profit.

IR is about which helps for knowhow businesses generate their profitability. Investor using these

data for knowing how much profitability businesses generate for running their activities. These

businesses using financial statement which includes cash flow. Balance sheet, income statement.

Cash flow which includes cash outflow, inflow for various activities which includes operating,

investing, financial activities for businesses.

Benefits-

• This aims to demonstrate seriously the enterprise to have sustainability in its main market. This

is beneficial in Tesco to increase the company's net profits. •• It also helps communicate the

environmental and societal impacts of the company's activities, which contribute to minimising

the organization's influence and dedication. In Tesco, this allows forming the main form of

productivity in order to manage many other advantages and has the right outcomes. This explains

how the organisation needs to learn and is helpful in achieving improved results (Kim, Kim and

Qian, 2018).

which is about intellectual capital, competition. IR which broad, large consequences for decision

for businesses which is base for factor, in order for create sustains value for businesses. IR

enable for businesses for communicate for clear, articulate way how it is for resource, which is

using for generate value which helps investor for manage risk, allocate resource for most

efficiently. It is necessary, for increasing reporting for financial data for ecological data.

Integrated report is about which is necessary communication about how businesses strategy,

governance, performance generate for investor, shareholder for businesses. It helps businesses

for improving their communication for various activities.

It is about achieving knowledge about businesses which helps for better performance

which helps for higher profitability for businesses (Paniagua, Rivelles and Sapena, 2018). In

context to Tesco, Sainsbury these businesses using IR for knowing how businesses has better

performance. It views about various activities for the businesses. It is about which businesses

using for their strategic decision. This is about businesses using these data for knowing for

investor about businesses strategy. Investor is who invest their fund for running activities for

businesses. Investor views businesses strategy which helps for knowhow businesses has better

performance. Investor views how businesses using fund which helps them for generating profit.

IR is about which helps for knowhow businesses generate their profitability. Investor using these

data for knowing how much profitability businesses generate for running their activities. These

businesses using financial statement which includes cash flow. Balance sheet, income statement.

Cash flow which includes cash outflow, inflow for various activities which includes operating,

investing, financial activities for businesses.

Benefits-

• This aims to demonstrate seriously the enterprise to have sustainability in its main market. This

is beneficial in Tesco to increase the company's net profits. •• It also helps communicate the

environmental and societal impacts of the company's activities, which contribute to minimising

the organization's influence and dedication. In Tesco, this allows forming the main form of

productivity in order to manage many other advantages and has the right outcomes. This explains

how the organisation needs to learn and is helpful in achieving improved results (Kim, Kim and

Qian, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.