Financial Performance Management

VerifiedAdded on 2022/12/28

|11

|2362

|67

AI Summary

This document discusses the concept of financial performance management and its significance in organizations. It covers various methods of calculating and analyzing financial performance, including per unit cost calculation based on labor hours and ABC method. The document also explores the evaluation of results using labor hours and ABC approach, as well as the use of sensitivity analysis in coping with uncertainties. Additionally, it addresses the calculation of variances and the problems with the current system of calculating and reporting variances. Lastly, it evaluates the effectiveness of zero-based budgeting and incremental budgeting in preparation, organization, and control.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial performance

management

management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

(a) Calculation of per unit cost on the basis of labour hours.......................................................1

(b) Calculation per unit cost on basis of ABC method................................................................2

(c) Evaluation of results as per labour hours and ABC approach................................................4

QUESTION 2..................................................................................................................................6

QUESTION 3..................................................................................................................................8

Evaluation of neither ZBB nor the IB delivers the impeccable toll for preparation organisation

and control...................................................................................................................................8

CONCLUSION................................................................................................................................9

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

(a) Calculation of per unit cost on the basis of labour hours.......................................................1

(b) Calculation per unit cost on basis of ABC method................................................................2

(c) Evaluation of results as per labour hours and ABC approach................................................4

QUESTION 2..................................................................................................................................6

QUESTION 3..................................................................................................................................8

Evaluation of neither ZBB nor the IB delivers the impeccable toll for preparation organisation

and control...................................................................................................................................8

CONCLUSION................................................................................................................................9

INTRODUCTION

Financial results analysis is a continuous real economy, which makes learning and

expansion at any level important. This is really a quantitative calculation, which each

organization carries out in an effective way to run its operations. Manager uses this definition in

order to predict economic expansion and organizational health for a certain span. There are

various ways to calculate and analyse financial performance. The quarterly earnings may begin

to be closer looked at and decreased successfully by investment analysts. This article focuses on

value accounting focused mostly on costing and accrual accounting framework. This research

involves the introduction of the estimation framework for management support and the

calculation of various material variances. There are also analyses of the issues about the new

system and variability in calculating efficiency. At the close of the study, ZBB and incremental

financial planning are discussed extensively.

QUESTION 1

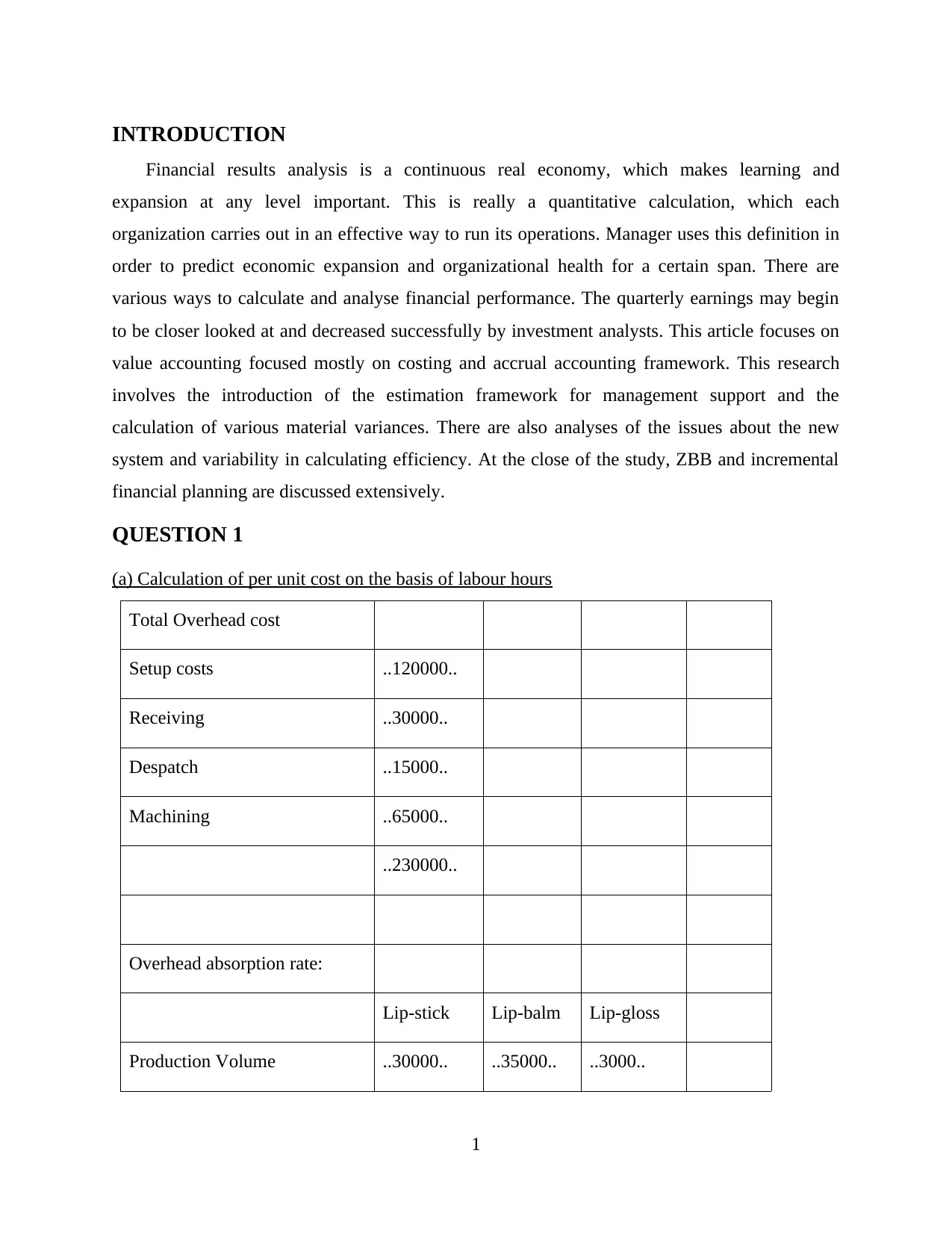

(a) Calculation of per unit cost on the basis of labour hours

Total Overhead cost

Setup costs ..120000..

Receiving ..30000..

Despatch ..15000..

Machining ..65000..

..230000..

Overhead absorption rate:

Lip-stick Lip-balm Lip-gloss

Production Volume ..30000.. ..35000.. ..3000..

1

Financial results analysis is a continuous real economy, which makes learning and

expansion at any level important. This is really a quantitative calculation, which each

organization carries out in an effective way to run its operations. Manager uses this definition in

order to predict economic expansion and organizational health for a certain span. There are

various ways to calculate and analyse financial performance. The quarterly earnings may begin

to be closer looked at and decreased successfully by investment analysts. This article focuses on

value accounting focused mostly on costing and accrual accounting framework. This research

involves the introduction of the estimation framework for management support and the

calculation of various material variances. There are also analyses of the issues about the new

system and variability in calculating efficiency. At the close of the study, ZBB and incremental

financial planning are discussed extensively.

QUESTION 1

(a) Calculation of per unit cost on the basis of labour hours

Total Overhead cost

Setup costs ..120000..

Receiving ..30000..

Despatch ..15000..

Machining ..65000..

..230000..

Overhead absorption rate:

Lip-stick Lip-balm Lip-gloss

Production Volume ..30000.. ..35000.. ..3000..

1

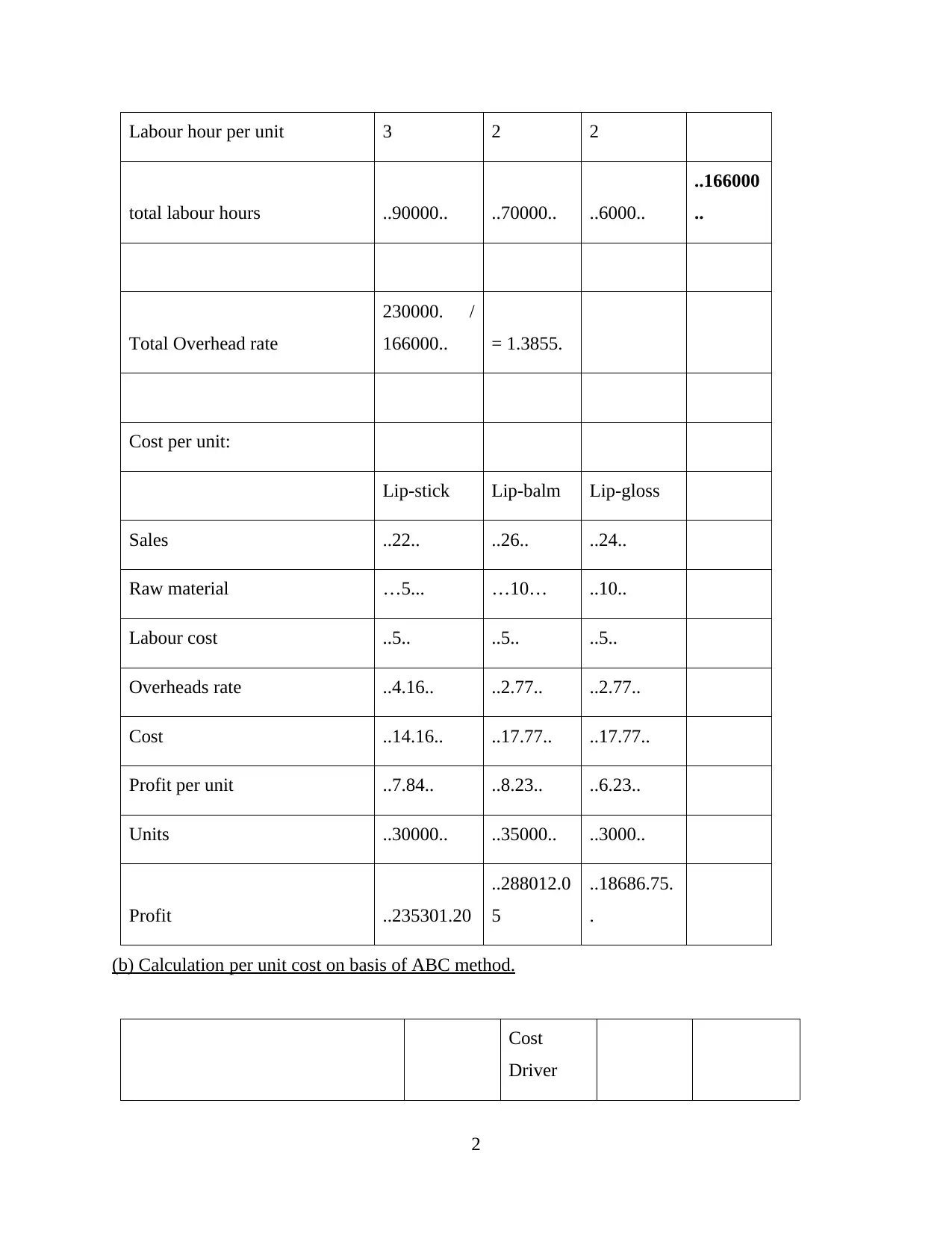

Labour hour per unit 3 2 2

total labour hours ..90000.. ..70000.. ..6000..

..166000

..

Total Overhead rate

230000. /

166000.. = 1.3855.

Cost per unit:

Lip-stick Lip-balm Lip-gloss

Sales ..22.. ..26.. ..24..

Raw material …5... …10… ..10..

Labour cost ..5.. ..5.. ..5..

Overheads rate ..4.16.. ..2.77.. ..2.77..

Cost ..14.16.. ..17.77.. ..17.77..

Profit per unit ..7.84.. ..8.23.. ..6.23..

Units ..30000.. ..35000.. ..3000..

Profit ..235301.20

..288012.0

5

..18686.75.

.

(b) Calculation per unit cost on basis of ABC method.

Cost

Driver

2

total labour hours ..90000.. ..70000.. ..6000..

..166000

..

Total Overhead rate

230000. /

166000.. = 1.3855.

Cost per unit:

Lip-stick Lip-balm Lip-gloss

Sales ..22.. ..26.. ..24..

Raw material …5... …10… ..10..

Labour cost ..5.. ..5.. ..5..

Overheads rate ..4.16.. ..2.77.. ..2.77..

Cost ..14.16.. ..17.77.. ..17.77..

Profit per unit ..7.84.. ..8.23.. ..6.23..

Units ..30000.. ..35000.. ..3000..

Profit ..235301.20

..288012.0

5

..18686.75.

.

(b) Calculation per unit cost on basis of ABC method.

Cost

Driver

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

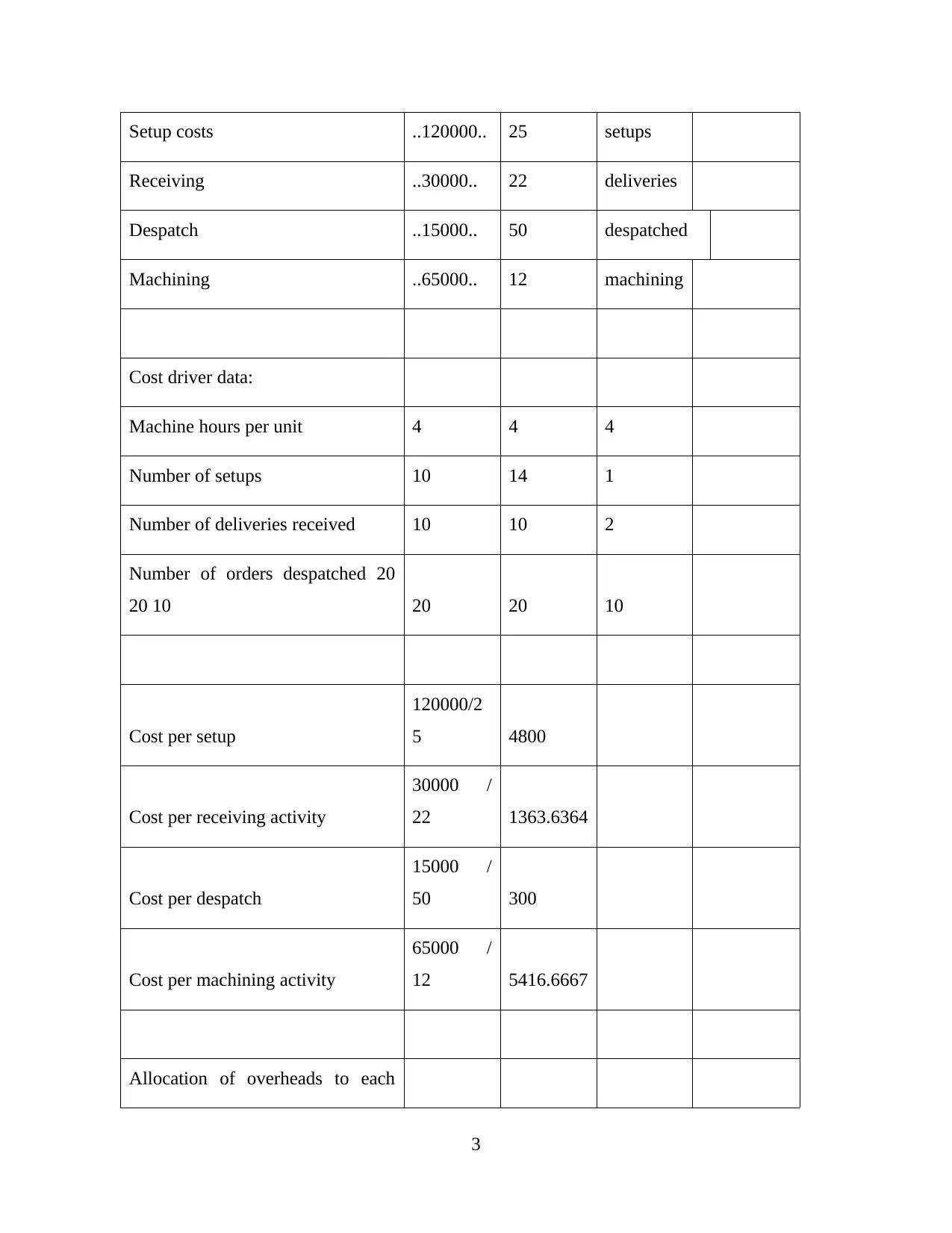

Setup costs ..120000.. 25 setups

Receiving ..30000.. 22 deliveries

Despatch ..15000.. 50 despatched

Machining ..65000.. 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12 5416.6667

Allocation of overheads to each

3

Receiving ..30000.. 22 deliveries

Despatch ..15000.. 50 despatched

Machining ..65000.. 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12 5416.6667

Allocation of overheads to each

3

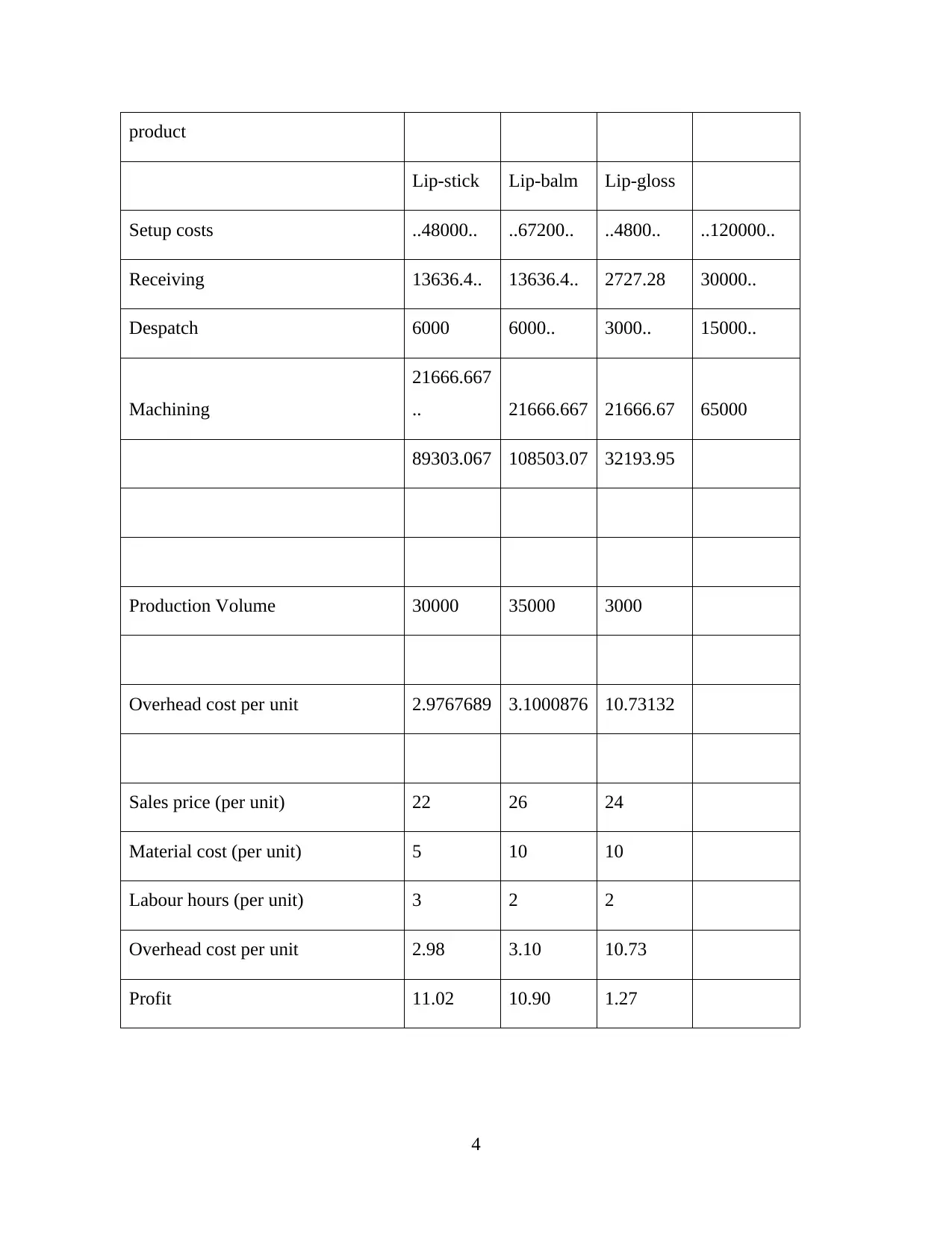

product

Lip-stick Lip-balm Lip-gloss

Setup costs ..48000.. ..67200.. ..4800.. ..120000..

Receiving 13636.4.. 13636.4.. 2727.28 30000..

Despatch 6000 6000.. 3000.. 15000..

Machining

21666.667

.. 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

4

Lip-stick Lip-balm Lip-gloss

Setup costs ..48000.. ..67200.. ..4800.. ..120000..

Receiving 13636.4.. 13636.4.. 2727.28 30000..

Despatch 6000 6000.. 3000.. 15000..

Machining

21666.667

.. 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

4

(c) Evaluation of results as per labour hours and ABC approach.

The next calculation evaluated the use of various work hour procedures and ABC costs

approaches each unit for quality. This is from the approximate results of 7.84, 8.23 and 6.23

every hour by both processes. However, in understanding the complexities, the results are 11, 02,

10, 90, and 1.27 at the same time. Different substance and quantity concentrations are calculated

and determined by 2 techniques. In the 3 schemes, 235301, 288012 and 18686 are the

absorbance value. For ABC, profit margins are 11.02, 10.90 and 1.27 independently.

Without the use of the consumption price, inventory control charges, such as fixed

operational costs, shall comprise energy charges and the lack of factory inventory. Multiple

expenditure, namely facilities manager salaries and business tax, include direct inventory, work,

and capital expenditure. These products help to determine real competitiveness and lower sales

value. In this method, variable production is allocated as either a product cost and helps to

determine the product portfolio. In contrast, the amount of absorption provides a bad evaluation

of the actual production cost of every other product.

Application focused on activities is then used to delegate production costs to them with

reliable tasks. All estimates of expenses are based on uncommon intellectual integrity. The

definition is based on negative steps to minimize operational costs. ABC works well under

conventional conditions where understanding a lot of sensors and devices is also not easy. For

instance, there is no concentrated value in the atmosphere where development cycles are

reduced. Many information requests mainly concentrate on the ABC process that is very much

effective. Activity-based cost estimation offers a concise method of costing products/services,

which leads to more exact price choices. It solid examples of costs and the motorists as well as

makes it much more accessible and extremely expensive and invaluable to add activities that can

be reduced or eliminated by management. ABC allows an efficient operating expense obstacle to

identify better ways to allocate and eliminate overhead costs. Also it allows for better assessment

of product and brand profit margins. It promotes methods like continuous improvements and

balanced scorecard for organizational performance. If a business may be using the standardized

ABC system to decide that detailed details is not required just after decision has been made. At

just the end including its method, this system is cantered on the procedure and gathers cost

benefit research that is mainly based on preference and approves costs and deliver advantageous

5

The next calculation evaluated the use of various work hour procedures and ABC costs

approaches each unit for quality. This is from the approximate results of 7.84, 8.23 and 6.23

every hour by both processes. However, in understanding the complexities, the results are 11, 02,

10, 90, and 1.27 at the same time. Different substance and quantity concentrations are calculated

and determined by 2 techniques. In the 3 schemes, 235301, 288012 and 18686 are the

absorbance value. For ABC, profit margins are 11.02, 10.90 and 1.27 independently.

Without the use of the consumption price, inventory control charges, such as fixed

operational costs, shall comprise energy charges and the lack of factory inventory. Multiple

expenditure, namely facilities manager salaries and business tax, include direct inventory, work,

and capital expenditure. These products help to determine real competitiveness and lower sales

value. In this method, variable production is allocated as either a product cost and helps to

determine the product portfolio. In contrast, the amount of absorption provides a bad evaluation

of the actual production cost of every other product.

Application focused on activities is then used to delegate production costs to them with

reliable tasks. All estimates of expenses are based on uncommon intellectual integrity. The

definition is based on negative steps to minimize operational costs. ABC works well under

conventional conditions where understanding a lot of sensors and devices is also not easy. For

instance, there is no concentrated value in the atmosphere where development cycles are

reduced. Many information requests mainly concentrate on the ABC process that is very much

effective. Activity-based cost estimation offers a concise method of costing products/services,

which leads to more exact price choices. It solid examples of costs and the motorists as well as

makes it much more accessible and extremely expensive and invaluable to add activities that can

be reduced or eliminated by management. ABC allows an efficient operating expense obstacle to

identify better ways to allocate and eliminate overhead costs. Also it allows for better assessment

of product and brand profit margins. It promotes methods like continuous improvements and

balanced scorecard for organizational performance. If a business may be using the standardized

ABC system to decide that detailed details is not required just after decision has been made. At

just the end including its method, this system is cantered on the procedure and gathers cost

benefit research that is mainly based on preference and approves costs and deliver advantageous

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information for enhanced efficiency. Furthermore, the overall analysis uses activity-based

methods for critical evaluation.

(d) Sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis is a model of outcomes that alter knowledge and forecast expected cash

flows that depend heavily on future activities, revenues, behaviours and purchases. In complex

algorithms, the stream can control the estimation value. Any input data may be omitted and

additional data processing and analyses carried out. On the basis of the report. This is related to

the outcomes under which all inconsistencies of data and design must be removed before

spending volume and space to collect extra production data and measure the performance of the

measurement unit, if not required. A number of advantages for policymakers are the behaviour

of sensitivity analysis. It is first and foremost a thorough examination of all of the other

variables. As the assumptions are far more thorough, they could be much more dependable.

Furthermore, it accelerates to determine where changes need to be made in long term. Finally, it

enables the ability to decide on firms, the economy or one’s investment funds soundly. This

research explains the key independent variables which influence individual event activities. A

methodology for using candidate models must be planned for the analysis, which is concerned

with an internal expression alteration known as an input issue.

The fundamental model is divided into a mathematical model that can be used to interpret effects

based on the number of variables. This analytical research focuses on multiple variables, which

influence the outcomes by producing a series of variables. The analyst investigates the critical

impact on the target of the change and output signal. Sensitivity for improving the securities of

human groups can be calculated and includes market profits, portfolio forecasts, the number of

competitive competitors and the influence of various factors on share prices. The prices of the

assets are measured and optimized by picking multiple theories and adding several parameters.

This assessment helps managers to assess the different elements, including the reduction in

investment costs, that will impact outcomes. This will have an effect on potential sales and

evaluation to resolve the risks of a new business entity until a sensitivity study has been

completed. The Middle is a way to analyse circumstances in a particular way. It attempts to

determine the magnitude of the operating risk, and helps to assess the performance in compliance

with the input accuracy.

6

methods for critical evaluation.

(d) Sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis is a model of outcomes that alter knowledge and forecast expected cash

flows that depend heavily on future activities, revenues, behaviours and purchases. In complex

algorithms, the stream can control the estimation value. Any input data may be omitted and

additional data processing and analyses carried out. On the basis of the report. This is related to

the outcomes under which all inconsistencies of data and design must be removed before

spending volume and space to collect extra production data and measure the performance of the

measurement unit, if not required. A number of advantages for policymakers are the behaviour

of sensitivity analysis. It is first and foremost a thorough examination of all of the other

variables. As the assumptions are far more thorough, they could be much more dependable.

Furthermore, it accelerates to determine where changes need to be made in long term. Finally, it

enables the ability to decide on firms, the economy or one’s investment funds soundly. This

research explains the key independent variables which influence individual event activities. A

methodology for using candidate models must be planned for the analysis, which is concerned

with an internal expression alteration known as an input issue.

The fundamental model is divided into a mathematical model that can be used to interpret effects

based on the number of variables. This analytical research focuses on multiple variables, which

influence the outcomes by producing a series of variables. The analyst investigates the critical

impact on the target of the change and output signal. Sensitivity for improving the securities of

human groups can be calculated and includes market profits, portfolio forecasts, the number of

competitive competitors and the influence of various factors on share prices. The prices of the

assets are measured and optimized by picking multiple theories and adding several parameters.

This assessment helps managers to assess the different elements, including the reduction in

investment costs, that will impact outcomes. This will have an effect on potential sales and

evaluation to resolve the risks of a new business entity until a sensitivity study has been

completed. The Middle is a way to analyse circumstances in a particular way. It attempts to

determine the magnitude of the operating risk, and helps to assess the performance in compliance

with the input accuracy.

6

QUESTION 2

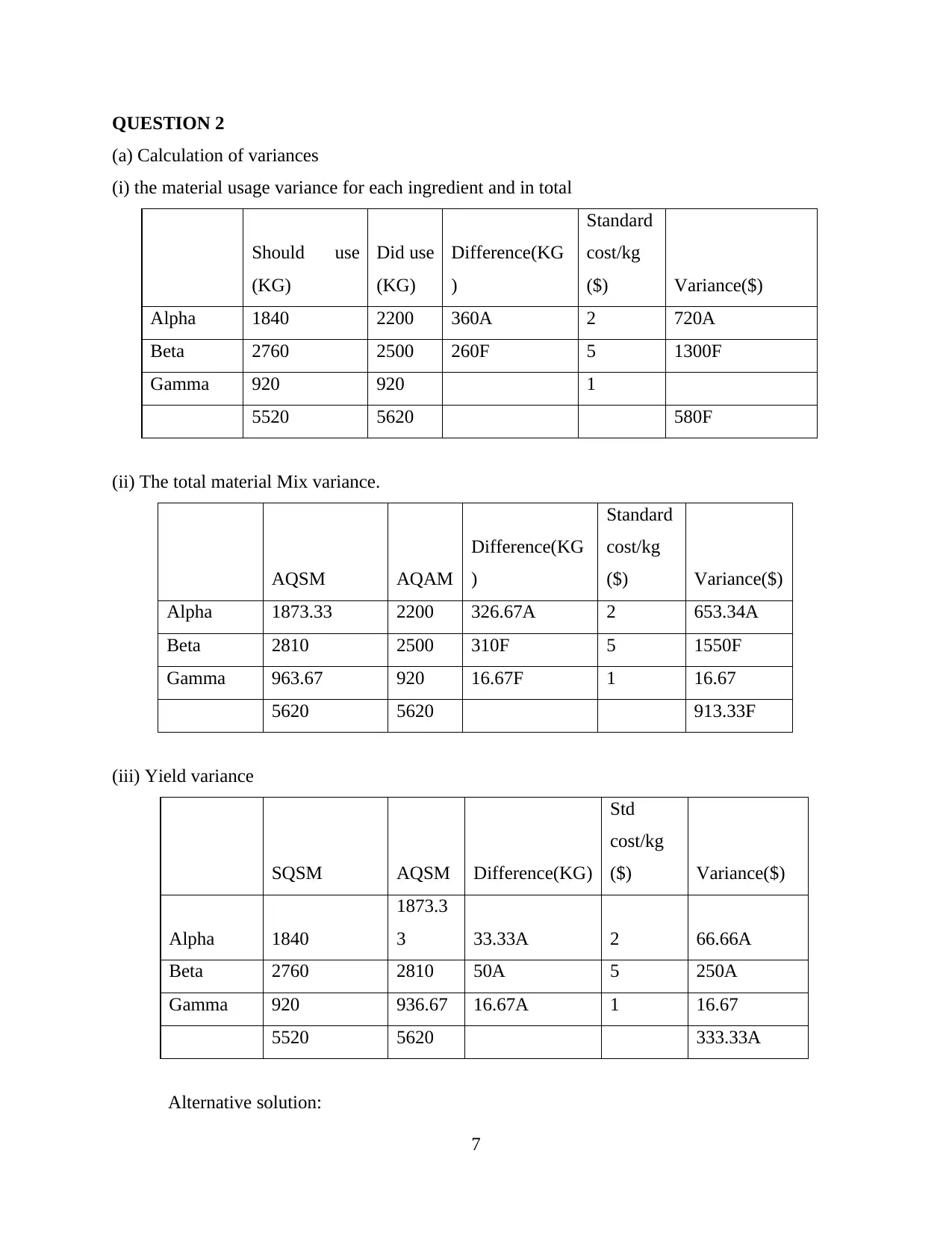

(a) Calculation of variances

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

7

(a) Calculation of variances

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

7

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Problems with current system of calculating and reporting variances

According to the report, the raw materials differ from outside the manufacturing range and are

mainly responsible for this buying manager. The daily combination is not taken into account

along with the production manager of the company. Different variances are analysed but cannot

be detected in the government. It is necessary to plan variations so they won't measure them.

Price and productivity ratios of three items are being modified and prices are being used

according to yield mix specifications.

Consistency changes and prices of basic mixtures and goods have not changed over the course of

5 years. The foundation of many variances and the creation of outdated expectations is becoming

the rationale for the conduct of control activities. Since Kappa has no reactions and opinions due

to less real photos and it becomes an excuse for the success of the production manager. Kappa co

does not influence many variants, which are cost-conscious and self-satisfying.

QUESTION 3

Evaluation of neither ZBB nor the IB delivers the impeccable toll for preparation organisation

and control

ZBB budget control is a zero-income spending plan which is not related to the existing

estimate. The purpose of this proposal is to calculate the yearly budgets. This allows the

organisation, rather than the original, to consider the entire amount. It must be determined and

the coordination and communication of the company must be improved. It helps the company to

save even more money and to generate income by evaluating the additional spending in the

business that can be removed. On the other extreme, the investment spending appears to lie

inside the expected budget again from overall budget and contains the amount of the rise in the

budget preparation period. Businesses may end competitors in this framework or profit from

genuine equality among divisions but adjust the same amount as in the last year.

The zero-based cash management doesn't quite consider current year expenditures, starting

from the start and then also, in comparison to the expenses of that year, the resources attributed

to each segment are measured whereas the client ’s requirements is planned to run for this year

8

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Problems with current system of calculating and reporting variances

According to the report, the raw materials differ from outside the manufacturing range and are

mainly responsible for this buying manager. The daily combination is not taken into account

along with the production manager of the company. Different variances are analysed but cannot

be detected in the government. It is necessary to plan variations so they won't measure them.

Price and productivity ratios of three items are being modified and prices are being used

according to yield mix specifications.

Consistency changes and prices of basic mixtures and goods have not changed over the course of

5 years. The foundation of many variances and the creation of outdated expectations is becoming

the rationale for the conduct of control activities. Since Kappa has no reactions and opinions due

to less real photos and it becomes an excuse for the success of the production manager. Kappa co

does not influence many variants, which are cost-conscious and self-satisfying.

QUESTION 3

Evaluation of neither ZBB nor the IB delivers the impeccable toll for preparation organisation

and control

ZBB budget control is a zero-income spending plan which is not related to the existing

estimate. The purpose of this proposal is to calculate the yearly budgets. This allows the

organisation, rather than the original, to consider the entire amount. It must be determined and

the coordination and communication of the company must be improved. It helps the company to

save even more money and to generate income by evaluating the additional spending in the

business that can be removed. On the other extreme, the investment spending appears to lie

inside the expected budget again from overall budget and contains the amount of the rise in the

budget preparation period. Businesses may end competitors in this framework or profit from

genuine equality among divisions but adjust the same amount as in the last year.

The zero-based cash management doesn't quite consider current year expenditures, starting

from the start and then also, in comparison to the expenses of that year, the resources attributed

to each segment are measured whereas the client ’s requirements is planned to run for this year

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

from the Spending plan focus of previous year. A cumulative sum for certain business operations

in the interest of the company is designed for ZBB. It takes some time because this strategy starts

at around nil and needs some time for the expenditure to be planned during all current

operations. The budgetary projections take a little longer to prepare since the current budget has

been calculated from the existing estimate. This spending plan needs budgetary skills and

information, and it is easy to proceed gradually, because budgeting process learning is not

involved. The spending plan as well takes into account the expenses involved in developing the

expenditures as it will start and thus does not actually involve any expense for drafting the

expenses. Null-based financial planning reduces challenges and high uncertainty in operational

activities by calculating basic spending, and in a procedure in accelerated aspects doesn't really

give close attention towards this point as it contributes or deletes from of the original proposal.

CONCLUSION

According to the main report, an effective financial planning approach has been believed to

monitor and analyse the financial performance of an individual. The management's primary

rationale for comparing and approximating existing costs and making adjustments accordingly.

Examination of variances in material and task variances in this analysis using a variety of

approaches to efficiently produce various effects.

9

in the interest of the company is designed for ZBB. It takes some time because this strategy starts

at around nil and needs some time for the expenditure to be planned during all current

operations. The budgetary projections take a little longer to prepare since the current budget has

been calculated from the existing estimate. This spending plan needs budgetary skills and

information, and it is easy to proceed gradually, because budgeting process learning is not

involved. The spending plan as well takes into account the expenses involved in developing the

expenditures as it will start and thus does not actually involve any expense for drafting the

expenses. Null-based financial planning reduces challenges and high uncertainty in operational

activities by calculating basic spending, and in a procedure in accelerated aspects doesn't really

give close attention towards this point as it contributes or deletes from of the original proposal.

CONCLUSION

According to the main report, an effective financial planning approach has been believed to

monitor and analyse the financial performance of an individual. The management's primary

rationale for comparing and approximating existing costs and making adjustments accordingly.

Examination of variances in material and task variances in this analysis using a variety of

approaches to efficiently produce various effects.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.