Financial Performance Management Report: Ruislip PLC Analysis, FNN6800

VerifiedAdded on 2022/12/28

|13

|2675

|49

Report

AI Summary

This report analyzes the financial performance of Ruislip PLC, covering various aspects of financial management. It begins with the calculation of cost per unit using both labor hours and activity-based costing approaches, comparing the results and highlighting the advantages of activity-based costing. The report then delves into variance analysis, calculating material usage, mix, and yield variances, while also discussing the shortcomings of the current variance reporting system. Furthermore, the report critically examines zero-based budgeting (ZBB) and incremental budgeting (IB), concluding that neither method provides a perfect tool for planning, coordination, and control. Sensitivity analysis is also discussed as a tool to cope with uncertainties. The report utilizes data provided in the assignment brief, including production volumes, sales prices, material costs, and labor hours to perform the financial analysis and provide recommendations.

Financial Performance

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................4

QUESTION 1.................................................................................................................................................4

(a) Calculate cost per unit on basis of labor hours...................................................................................4

(b) Calculate cost per unit on basis of activity based costing approach...................................................5

(c) Analysis results on basis of labor hours and activity based costing approach....................................7

(d) Sensitivity analysis help managers to cope with uncertainties ..........................................................8

QUESTION 2.................................................................................................................................................8

(a) Calculation of variances......................................................................................................................8

(b) Problems with current system of calculating and reporting variances...............................................9

QUESTION 3...............................................................................................................................................10

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination and

control...................................................................................................................................................10

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................12

INTRODUCTION...........................................................................................................................................4

QUESTION 1.................................................................................................................................................4

(a) Calculate cost per unit on basis of labor hours...................................................................................4

(b) Calculate cost per unit on basis of activity based costing approach...................................................5

(c) Analysis results on basis of labor hours and activity based costing approach....................................7

(d) Sensitivity analysis help managers to cope with uncertainties ..........................................................8

QUESTION 2.................................................................................................................................................8

(a) Calculation of variances......................................................................................................................8

(b) Problems with current system of calculating and reporting variances...............................................9

QUESTION 3...............................................................................................................................................10

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination and

control...................................................................................................................................................10

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial Performance is large framework which is used by the entity for financial

objectives and achieved for financial risk management. In the procedure analyzing of all

outcomes that important for firm policies as well as operations in monetary terms. In a business

entity identify different types of financial activity that impact on the business positive and

negative. Thus, it is required top manage these activities in proper manner (Zhou, Mavondo, and

Saunders, 2019). For this apply the concept of financial performance management and measure

firm’s overall financial health in specified period of time. This report based on the financial

performance activities and consist of different methods that use for the calculations. Along with

apply sensitivity analysis for reduce uncertainties and select right method for the calculations. At

the end of the report analysis of different budgeting method like Zero based budgeting and

incremental budgeting to conduct business operations.

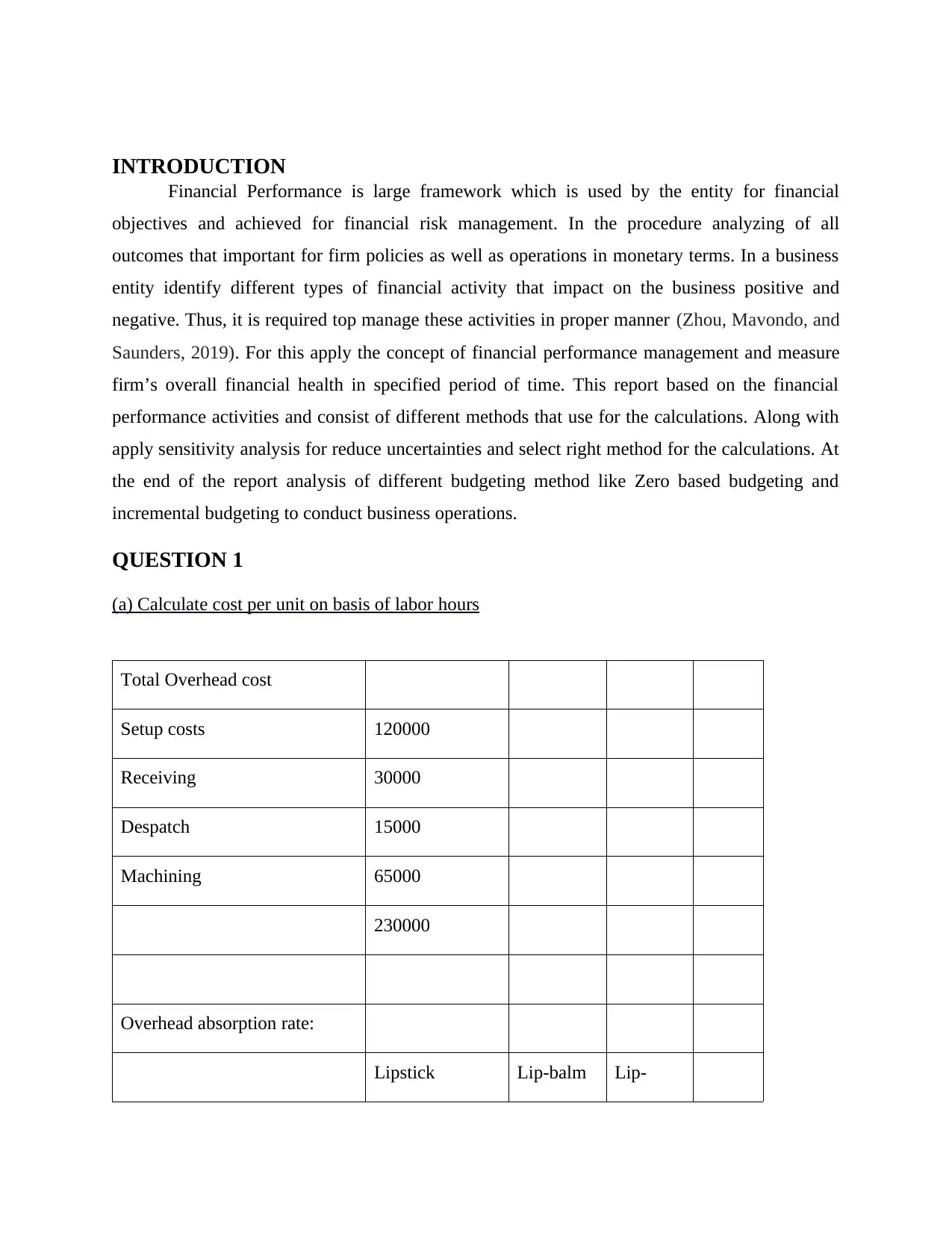

QUESTION 1

(a) Calculate cost per unit on basis of labor hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Lipstick Lip-balm Lip-

Financial Performance is large framework which is used by the entity for financial

objectives and achieved for financial risk management. In the procedure analyzing of all

outcomes that important for firm policies as well as operations in monetary terms. In a business

entity identify different types of financial activity that impact on the business positive and

negative. Thus, it is required top manage these activities in proper manner (Zhou, Mavondo, and

Saunders, 2019). For this apply the concept of financial performance management and measure

firm’s overall financial health in specified period of time. This report based on the financial

performance activities and consist of different methods that use for the calculations. Along with

apply sensitivity analysis for reduce uncertainties and select right method for the calculations. At

the end of the report analysis of different budgeting method like Zero based budgeting and

incremental budgeting to conduct business operations.

QUESTION 1

(a) Calculate cost per unit on basis of labor hours

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Lipstick Lip-balm Lip-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

gloss

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000

16600

0

Total Overhead rate

230000 /

166000 = 1.3855

Cost per unit:

Lipstick Lip-balm

Lip-

gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Units 30000 35000 3000

Profit 235301.20 288012.05 18686.75

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000

16600

0

Total Overhead rate

230000 /

166000 = 1.3855

Cost per unit:

Lipstick Lip-balm

Lip-

gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Units 30000 35000 3000

Profit 235301.20 288012.05 18686.75

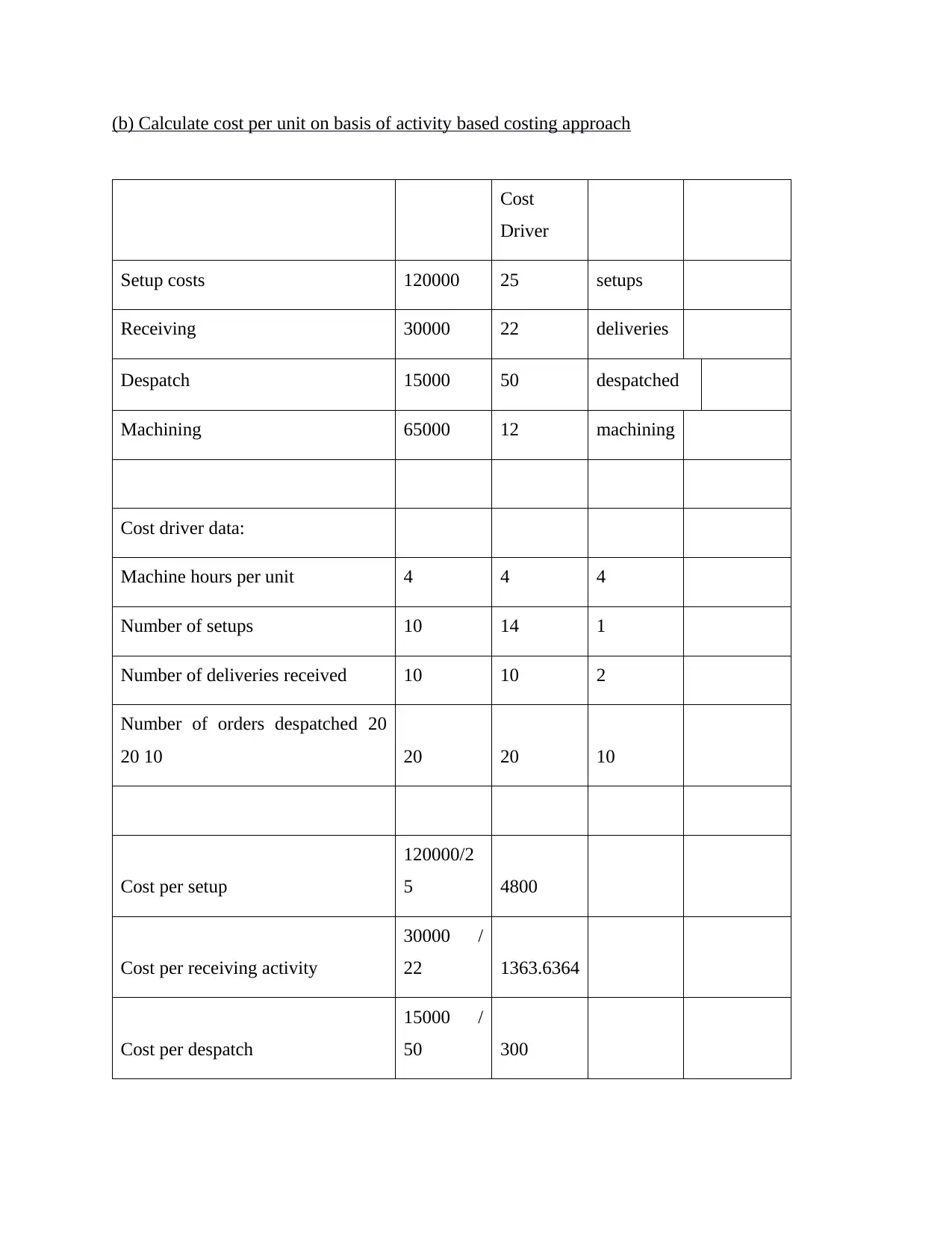

(b) Calculate cost per unit on basis of activity based costing approach

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12 machining

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20

20 10 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22 1363.6364

Cost per despatch

15000 /

50 300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

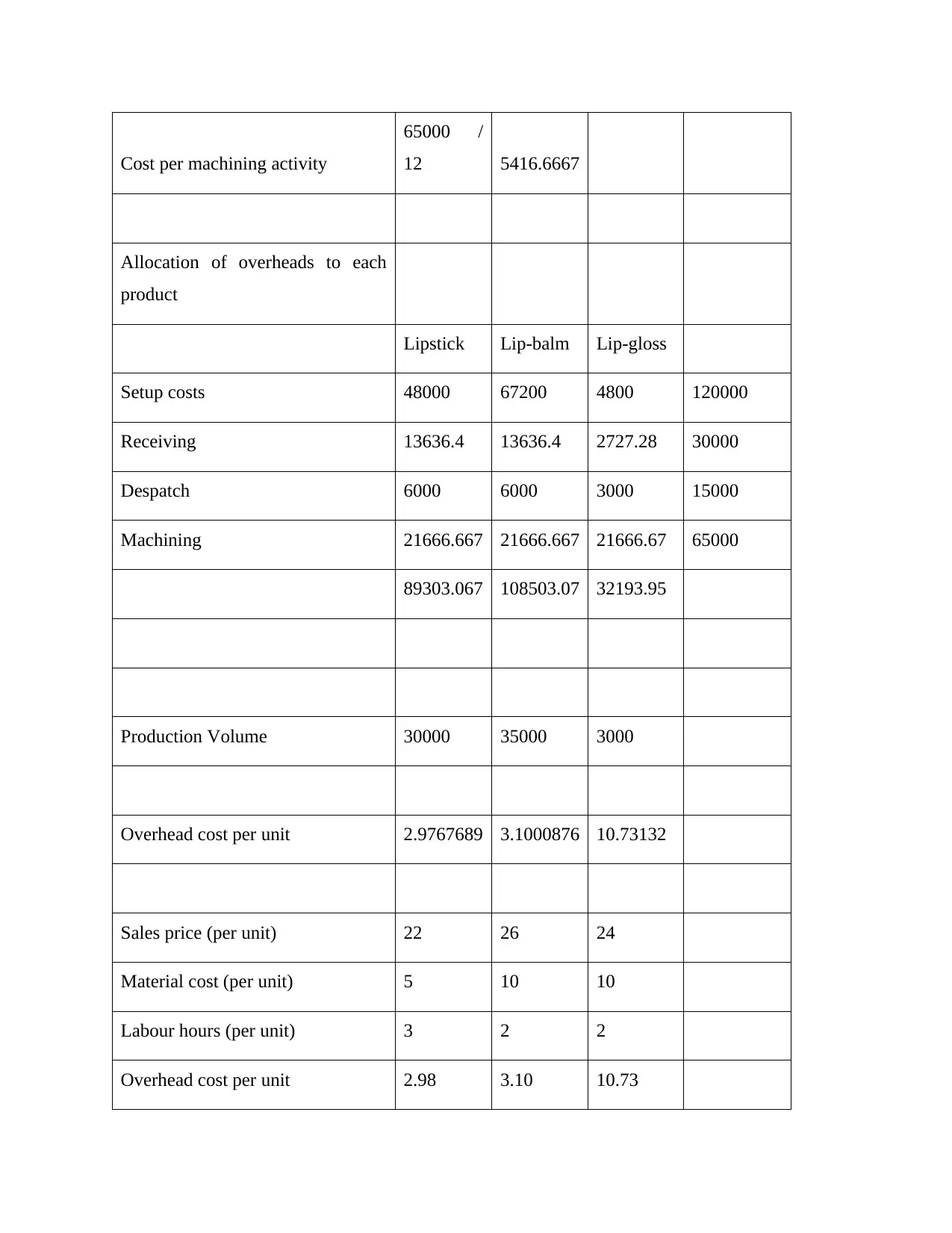

Cost per machining activity

65000 /

12 5416.6667

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

65000 /

12 5416.6667

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800 120000

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining 21666.667 21666.667 21666.67 65000

89303.067 108503.07 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit 2.9767689 3.1000876 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit 11.02 10.90 1.27

(c) Analysis results on basis of labor hours and activity based costing approach

As per the computation it is analyzed that for the calculation of cost per unit use two

methods which are labor hours and activity based costing approach. From the both methods get

different results and identify differences in profitability because of changes in absorption cost.

On the bases of labor hour get results of 7.84, 8.23 and 6.23 continuously and by the method of

activity based costing get results of 11.02, 10.09 and 1.27 respectively.

Labor hour mainly used for the industry labor intensive and identified skills, semi skills

and unskilled people. In this methods consist of all the activities that related with labor like direct

labor, materials and various types of expenditure such as, direct as well as indirect expenditure. It

is easy method that supports in effective sales price of items on the other side absorption costing

needed to provide fixed production overheads to recognize expenses of each item (Wang, Akbar

and Akbar, 2020).

Activity based costing methods is use by the entity for analysis reliable overhead cost by

attributed them to operations. After the allocation specify the cost objectives to manage all

operational activities. The main objective of this technique to reduce the cost at the time of

manufacturing that helps to generate more profitability in positive manner. Id entity installed

ABC system so it carries out effective results and take right decision on right time. Such as, after

the overall analysis it is understanding that activity based method is most effective method that

should use by the company for comprehensive analysis (Su, Liu and Teng, 2020).

(d) Sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis is the technique identify uncertainty in the mathematical model which

impact input variables into output variables. This analysis helps in various situations forecasting

share prices in the market of companies which are listed on stock exchange and determine

interest rates which acts on bond prices. Sensitivity analysis is based on historical data. It helps

investors to ascertain different changes on their investment return. It is useful to predict and

make decisions about business operations, wealth and investment.

(c) Analysis results on basis of labor hours and activity based costing approach

As per the computation it is analyzed that for the calculation of cost per unit use two

methods which are labor hours and activity based costing approach. From the both methods get

different results and identify differences in profitability because of changes in absorption cost.

On the bases of labor hour get results of 7.84, 8.23 and 6.23 continuously and by the method of

activity based costing get results of 11.02, 10.09 and 1.27 respectively.

Labor hour mainly used for the industry labor intensive and identified skills, semi skills

and unskilled people. In this methods consist of all the activities that related with labor like direct

labor, materials and various types of expenditure such as, direct as well as indirect expenditure. It

is easy method that supports in effective sales price of items on the other side absorption costing

needed to provide fixed production overheads to recognize expenses of each item (Wang, Akbar

and Akbar, 2020).

Activity based costing methods is use by the entity for analysis reliable overhead cost by

attributed them to operations. After the allocation specify the cost objectives to manage all

operational activities. The main objective of this technique to reduce the cost at the time of

manufacturing that helps to generate more profitability in positive manner. Id entity installed

ABC system so it carries out effective results and take right decision on right time. Such as, after

the overall analysis it is understanding that activity based method is most effective method that

should use by the company for comprehensive analysis (Su, Liu and Teng, 2020).

(d) Sensitivity analysis help managers to cope with uncertainties

Sensitivity analysis is the technique identify uncertainty in the mathematical model which

impact input variables into output variables. This analysis helps in various situations forecasting

share prices in the market of companies which are listed on stock exchange and determine

interest rates which acts on bond prices. Sensitivity analysis is based on historical data. It helps

investors to ascertain different changes on their investment return. It is useful to predict and

make decisions about business operations, wealth and investment.

Sensitivity analysis helps managers to make strategic decisions and improve past

performance of the business to reduce uncertainty in the company. This analysis is determined

by manager before accomplish a new project. It assess risk in a new project which involved risk

in a project. This helps managers to solve the problems in changes of any variables with affect

the profit of the company. This evaluation helps manager to identify the inaccuracy in data which

impacts the outcome of model. Managers can cope up with the uncertainties in identifying key

assumptions, optimizing resource allocation which increase the input variations. It analyse the

variables and financial aspects are ascertained the way that changes one variable and impact final

outcome. It is the tool to assess the uncertainty analysis to make policy decisions which are

based on assumptions related to input variables which are used in mathematical calculations. If

manager determine uncertainty in asset which can be figure out when they analyse profits and

return of the company.(Bendickson and Chandler, 2019)

QUESTION 2

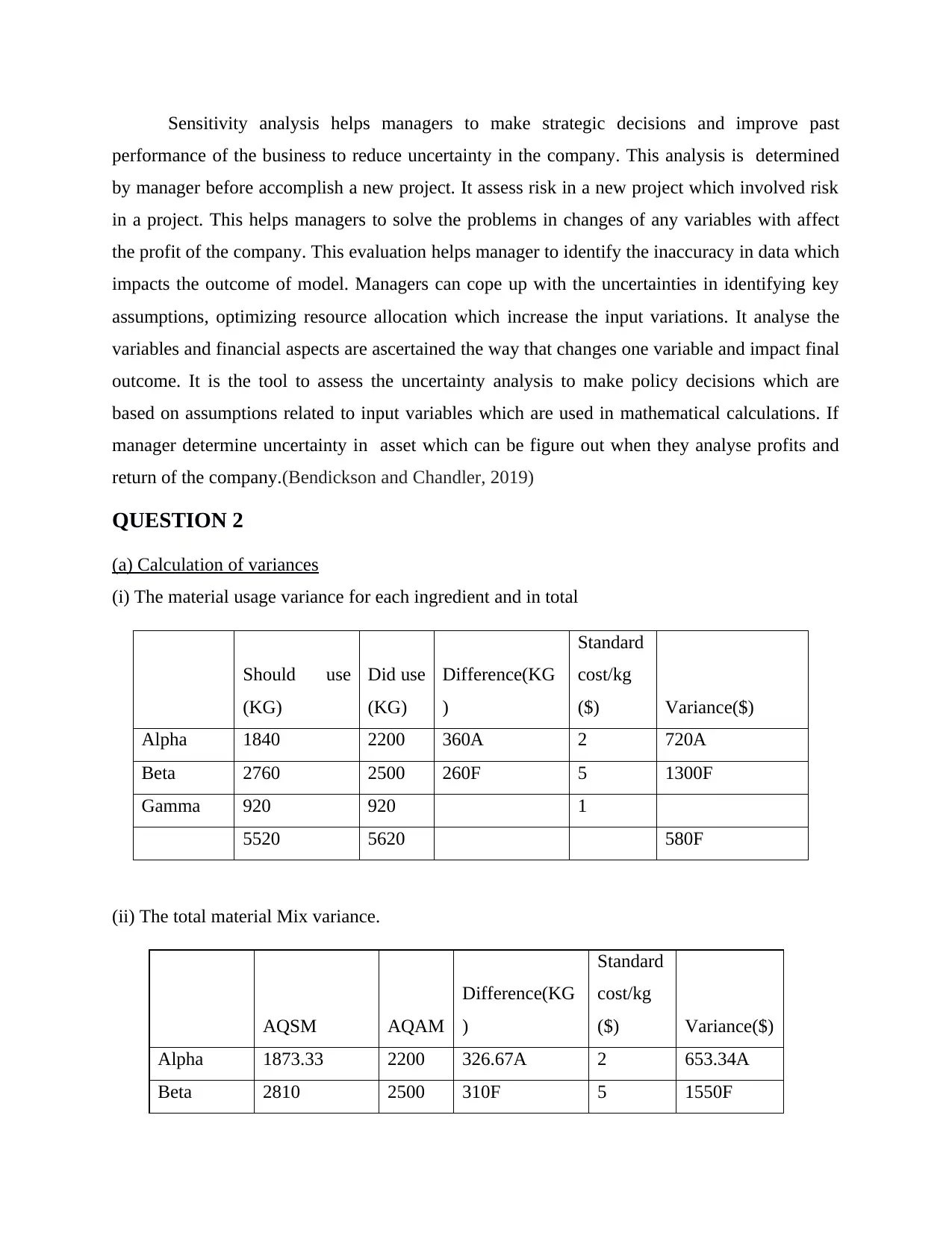

(a) Calculation of variances

(i) The material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

performance of the business to reduce uncertainty in the company. This analysis is determined

by manager before accomplish a new project. It assess risk in a new project which involved risk

in a project. This helps managers to solve the problems in changes of any variables with affect

the profit of the company. This evaluation helps manager to identify the inaccuracy in data which

impacts the outcome of model. Managers can cope up with the uncertainties in identifying key

assumptions, optimizing resource allocation which increase the input variations. It analyse the

variables and financial aspects are ascertained the way that changes one variable and impact final

outcome. It is the tool to assess the uncertainty analysis to make policy decisions which are

based on assumptions related to input variables which are used in mathematical calculations. If

manager determine uncertainty in asset which can be figure out when they analyse profits and

return of the company.(Bendickson and Chandler, 2019)

QUESTION 2

(a) Calculation of variances

(i) The material usage variance for each ingredient and in total

Should use

(KG)

Did use

(KG)

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gamma 920 920 1

5520 5620 580F

(ii) The total material Mix variance.

AQSM AQAM

Difference(KG

)

Standard

cost/kg

($) Variance($)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

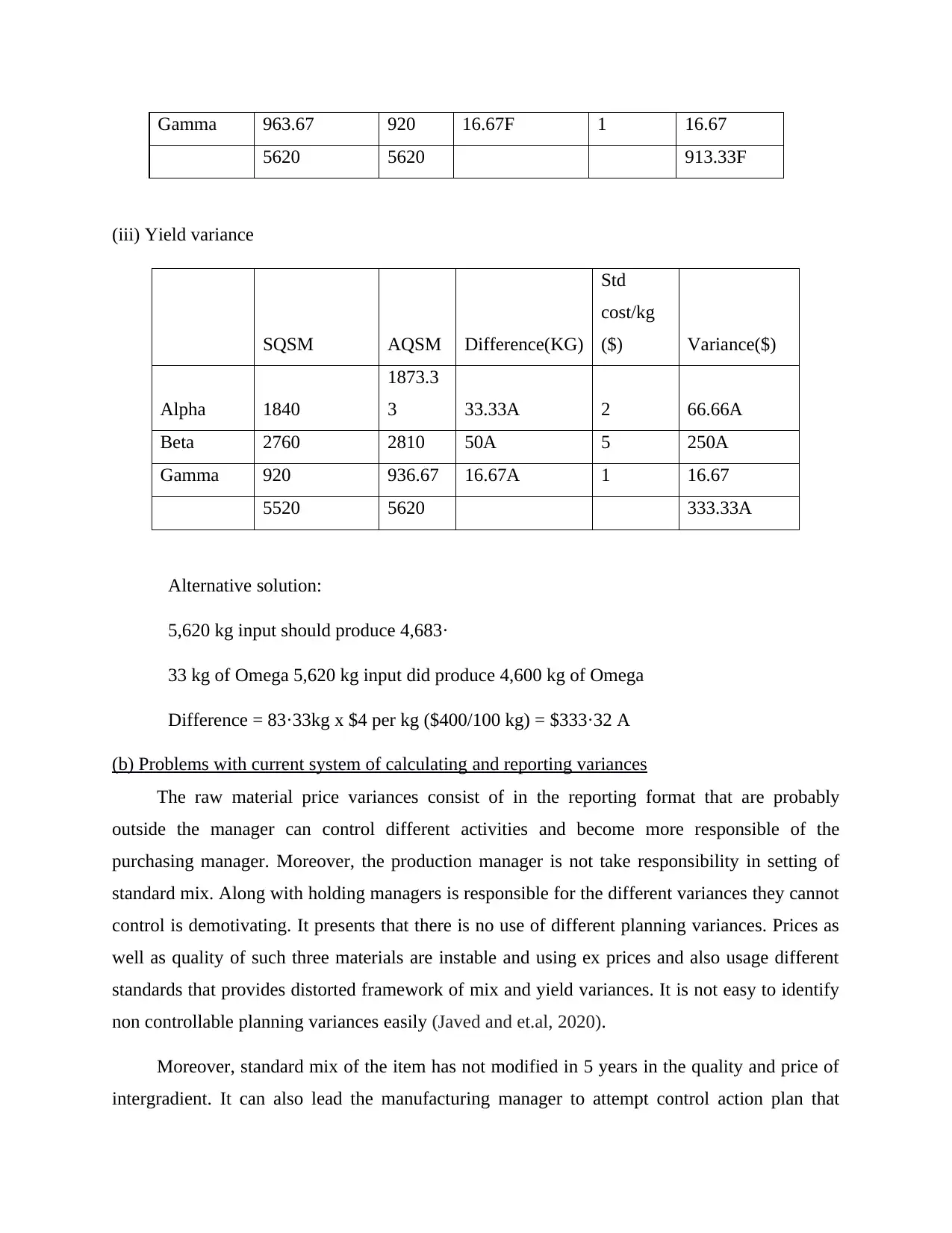

Gamma 963.67 920 16.67F 1 16.67

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Problems with current system of calculating and reporting variances

The raw material price variances consist of in the reporting format that are probably

outside the manager can control different activities and become more responsible of the

purchasing manager. Moreover, the production manager is not take responsibility in setting of

standard mix. Along with holding managers is responsible for the different variances they cannot

control is demotivating. It presents that there is no use of different planning variances. Prices as

well as quality of such three materials are instable and using ex prices and also usage different

standards that provides distorted framework of mix and yield variances. It is not easy to identify

non controllable planning variances easily (Javed and et.al, 2020).

Moreover, standard mix of the item has not modified in 5 years in the quality and price of

intergradient. It can also lead the manufacturing manager to attempt control action plan that

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM Difference(KG)

Std

cost/kg

($) Variance($)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamma 920 936.67 16.67A 1 16.67

5520 5620 333.33A

Alternative solution:

5,620 kg input should produce 4,683·

33 kg of Omega 5,620 kg input did produce 4,600 kg of Omega

Difference = 83·33kg x $4 per kg ($400/100 kg) = $333·32 A

(b) Problems with current system of calculating and reporting variances

The raw material price variances consist of in the reporting format that are probably

outside the manager can control different activities and become more responsible of the

purchasing manager. Moreover, the production manager is not take responsibility in setting of

standard mix. Along with holding managers is responsible for the different variances they cannot

control is demotivating. It presents that there is no use of different planning variances. Prices as

well as quality of such three materials are instable and using ex prices and also usage different

standards that provides distorted framework of mix and yield variances. It is not easy to identify

non controllable planning variances easily (Javed and et.al, 2020).

Moreover, standard mix of the item has not modified in 5 years in the quality and price of

intergradient. It can also lead the manufacturing manager to attempt control action plan that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depend on the different variances and it is computed on basis of different standards that are out

of date. In the context of kappa Co does not provide any feedback and commentary in regard of

business because of lacking of true picture is taking by production manager’s performance.

There is also not following particular procedure for variance calculation. As Kappa Co does not

presents to place more advantage on the variances and the production manager do not encourage

to control cost and become complacent that could negatively impact on Kappa Company overall.

QUESTION 3

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination

and control

Zero base budgeting: Zero base budgeting is the approach for making budget for

expenses for the functions for the company which helps for analyses the needs for the company

which helps for the profits. It helps for the strategic goals which are includes for budgeting

process for the functional areas for the company it includes various expenses which company

makes for it for running its activities (Gao, Yang and Hafsi, 2019). These budgets help

companies for its better performance which helps for higher profitability for the businesses. It

helps for lower costs which helps for higher profitability for the businesses. It is the method for

the giving funds for better performance for the company. It helps for final performance for the

company's business strategies, it helps for collaboration for the company, it helps for the

improvement for performance, it helps for higher profitability, it avoids traditional budgeting.

The company's use it for making its strategies better which helps its for its higher profitability.

These budgeting helps companies for their higher profits. Incremental budgeting analyses

expenses which are views additional, zero base budgeting includes various expenses which are

includes for the activities which runs for the company. It helps for running activities for the

company which helps for better performance which helps for the higher profitability for the

businesses. Company's use it for their better performance for now its various costs which

includes for its activities which helps it for making decisions. The company use the various costs

for its profitability which businesses includes for their performance which views profits for the

businesses. It helps businesses for the making financial statements for it which views its

expenses, income, profits, liabilities, assets for the company. Incremental budget includes those

values which are includes for the additional, zero base budget includes various values for the

of date. In the context of kappa Co does not provide any feedback and commentary in regard of

business because of lacking of true picture is taking by production manager’s performance.

There is also not following particular procedure for variance calculation. As Kappa Co does not

presents to place more advantage on the variances and the production manager do not encourage

to control cost and become complacent that could negatively impact on Kappa Company overall.

QUESTION 3

Critically discussed neither ZBB nor the IB provides the perfect toll for planning coordination

and control

Zero base budgeting: Zero base budgeting is the approach for making budget for

expenses for the functions for the company which helps for analyses the needs for the company

which helps for the profits. It helps for the strategic goals which are includes for budgeting

process for the functional areas for the company it includes various expenses which company

makes for it for running its activities (Gao, Yang and Hafsi, 2019). These budgets help

companies for its better performance which helps for higher profitability for the businesses. It

helps for lower costs which helps for higher profitability for the businesses. It is the method for

the giving funds for better performance for the company. It helps for final performance for the

company's business strategies, it helps for collaboration for the company, it helps for the

improvement for performance, it helps for higher profitability, it avoids traditional budgeting.

The company's use it for making its strategies better which helps its for its higher profitability.

These budgeting helps companies for their higher profits. Incremental budgeting analyses

expenses which are views additional, zero base budgeting includes various expenses which are

includes for the activities which runs for the company. It helps for running activities for the

company which helps for better performance which helps for the higher profitability for the

businesses. Company's use it for their better performance for now its various costs which

includes for its activities which helps it for making decisions. The company use the various costs

for its profitability which businesses includes for their performance which views profits for the

businesses. It helps businesses for the making financial statements for it which views its

expenses, income, profits, liabilities, assets for the company. Incremental budget includes those

values which are includes for the additional, zero base budget includes various values for the

company's activities. It includes various expenses for the company’s profits which helps for

better performance for higher profitability for the businesses (Ramli, Latan and Solovida, 2019).

Incremental budget: This is part of budgeting method in which manager formulate

budget on the basis of adding increment of amount or value in the data of previous budget. These

types of budget are mainly concern with the incremental amount of values. Resource are

allocated on the basis of reviewing previous data. incremental budget is focus on control and

eliminate cost of spending of wastage of business activities thus on the basis of that resource are

distributed by recognize value of changes.

It is considering as one of the useful budget which help in provide accurate business

information related with future. These types of budget are generally formulated for organizations

which run their business in international market. The main advantage of formulation of this

budget is that manager able to effectively and accurately show the real value of performs acre.

By formulation of this budget manager able to find stable result as well as control conflicts arises

due to mismanagement of business activities (Van Vu and et.al, 2018).

Incremental budget is prepared after recognize changes in value and items thus it provides

accurate and reliable information.

CONCLUSION

As per the above report it has been analyzed that financial performance management is

important term of any organization that utilized to effectively manage all the business activities.

There is calculation cost per unit by different methods and analysis results and get that activity

based costing approach is good that helps to conduct business activities and carry out outcomes

properly. Along with it is identified that incremental budget used by the organizations in broad

manner to predict future profit and expenses.

better performance for higher profitability for the businesses (Ramli, Latan and Solovida, 2019).

Incremental budget: This is part of budgeting method in which manager formulate

budget on the basis of adding increment of amount or value in the data of previous budget. These

types of budget are mainly concern with the incremental amount of values. Resource are

allocated on the basis of reviewing previous data. incremental budget is focus on control and

eliminate cost of spending of wastage of business activities thus on the basis of that resource are

distributed by recognize value of changes.

It is considering as one of the useful budget which help in provide accurate business

information related with future. These types of budget are generally formulated for organizations

which run their business in international market. The main advantage of formulation of this

budget is that manager able to effectively and accurately show the real value of performs acre.

By formulation of this budget manager able to find stable result as well as control conflicts arises

due to mismanagement of business activities (Van Vu and et.al, 2018).

Incremental budget is prepared after recognize changes in value and items thus it provides

accurate and reliable information.

CONCLUSION

As per the above report it has been analyzed that financial performance management is

important term of any organization that utilized to effectively manage all the business activities.

There is calculation cost per unit by different methods and analysis results and get that activity

based costing approach is good that helps to conduct business activities and carry out outcomes

properly. Along with it is identified that incremental budget used by the organizations in broad

manner to predict future profit and expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.