FNN6800: Financial Performance Management Assignment Report Analysis

VerifiedAdded on 2022/12/28

|10

|2590

|1

Report

AI Summary

This report analyzes financial performance management, addressing key concepts like absorption rates, cost per unit calculations, and overhead allocation methods. It examines different costing approaches, including labor hour-based absorption and activity-based costing, comparing their effectiveness and implications on product profitability. The report further explores variance analysis, including material usage, mix, and yield variances, with a focus on standard costing systems and their limitations. It also covers sensitivity analysis, margin of safety, and the application of zero-based budgeting versus incremental budgeting, evaluating their respective advantages and disadvantages in different business contexts. The report incorporates calculations, tables, and variance analysis to provide a comprehensive understanding of financial performance management principles.

FINANCIAL PERFORMANCE

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................1

a)..................................................................................................................................................1

b)..................................................................................................................................................1

c)..................................................................................................................................................2

d) .................................................................................................................................................3

QUESTION 2...................................................................................................................................4

a)..................................................................................................................................................4

b) .................................................................................................................................................5

QUESTION 3 ..................................................................................................................................6

a)..................................................................................................................................................6

REFERENCES................................................................................................................................8

QUESTION 1...................................................................................................................................1

a)..................................................................................................................................................1

b)..................................................................................................................................................1

c)..................................................................................................................................................2

d) .................................................................................................................................................3

QUESTION 2...................................................................................................................................4

a)..................................................................................................................................................4

b) .................................................................................................................................................5

QUESTION 3 ..................................................................................................................................6

a)..................................................................................................................................................6

REFERENCES................................................................................................................................8

QUESTION 1

a)

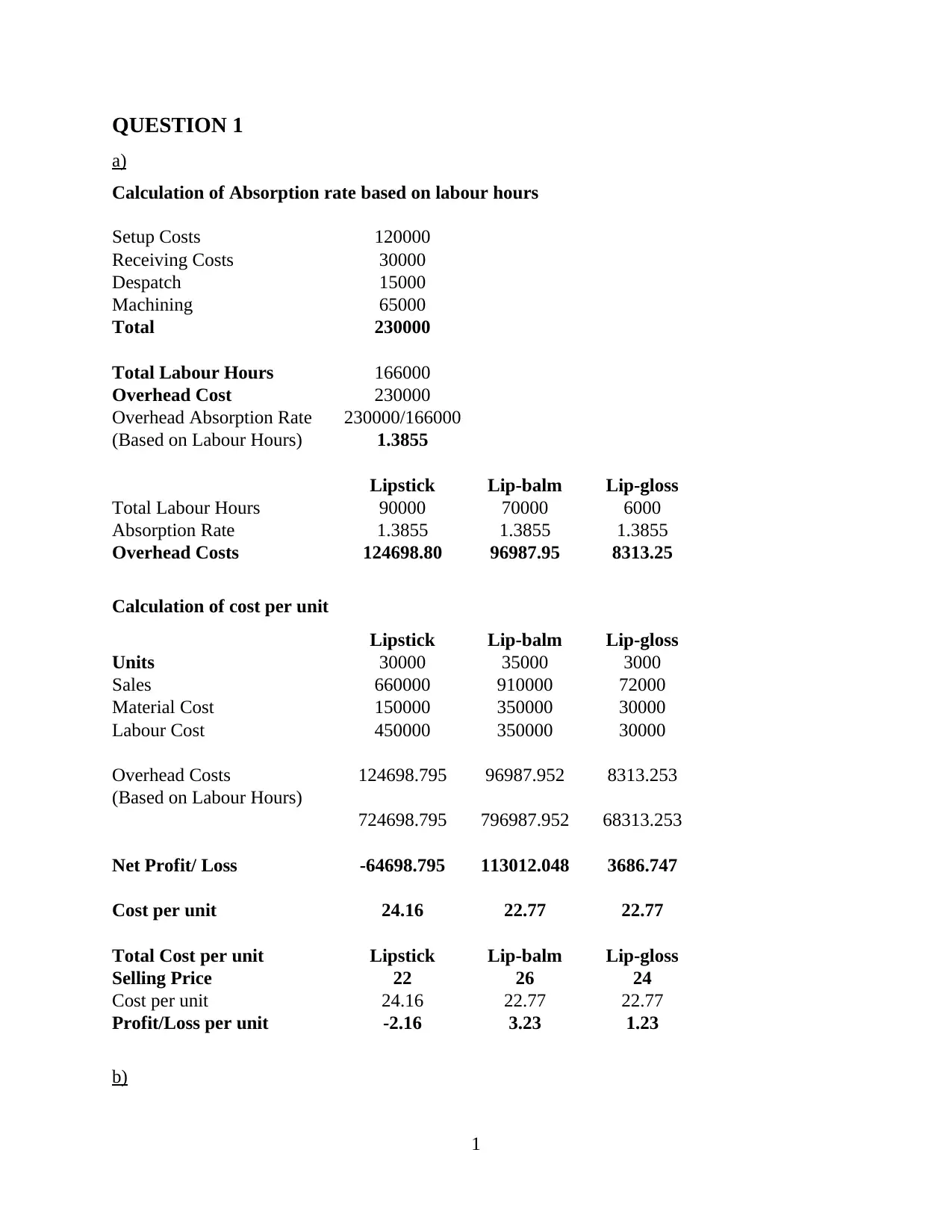

Calculation of Absorption rate based on labour hours

Setup Costs 120000

Receiving Costs 30000

Despatch 15000

Machining 65000

Total 230000

Total Labour Hours 166000

Overhead Cost 230000

Overhead Absorption Rate 230000/166000

(Based on Labour Hours) 1.3855

Lipstick Lip-balm Lip-gloss

Total Labour Hours 90000 70000 6000

Absorption Rate 1.3855 1.3855 1.3855

Overhead Costs 124698.80 96987.95 8313.25

Calculation of cost per unit

Lipstick Lip-balm Lip-gloss

Units 30000 35000 3000

Sales 660000 910000 72000

Material Cost 150000 350000 30000

Labour Cost 450000 350000 30000

Overhead Costs 124698.795 96987.952 8313.253

(Based on Labour Hours)

724698.795 796987.952 68313.253

Net Profit/ Loss -64698.795 113012.048 3686.747

Cost per unit 24.16 22.77 22.77

Total Cost per unit Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Cost per unit 24.16 22.77 22.77

Profit/Loss per unit -2.16 3.23 1.23

b)

1

a)

Calculation of Absorption rate based on labour hours

Setup Costs 120000

Receiving Costs 30000

Despatch 15000

Machining 65000

Total 230000

Total Labour Hours 166000

Overhead Cost 230000

Overhead Absorption Rate 230000/166000

(Based on Labour Hours) 1.3855

Lipstick Lip-balm Lip-gloss

Total Labour Hours 90000 70000 6000

Absorption Rate 1.3855 1.3855 1.3855

Overhead Costs 124698.80 96987.95 8313.25

Calculation of cost per unit

Lipstick Lip-balm Lip-gloss

Units 30000 35000 3000

Sales 660000 910000 72000

Material Cost 150000 350000 30000

Labour Cost 450000 350000 30000

Overhead Costs 124698.795 96987.952 8313.253

(Based on Labour Hours)

724698.795 796987.952 68313.253

Net Profit/ Loss -64698.795 113012.048 3686.747

Cost per unit 24.16 22.77 22.77

Total Cost per unit Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Cost per unit 24.16 22.77 22.77

Profit/Loss per unit -2.16 3.23 1.23

b)

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

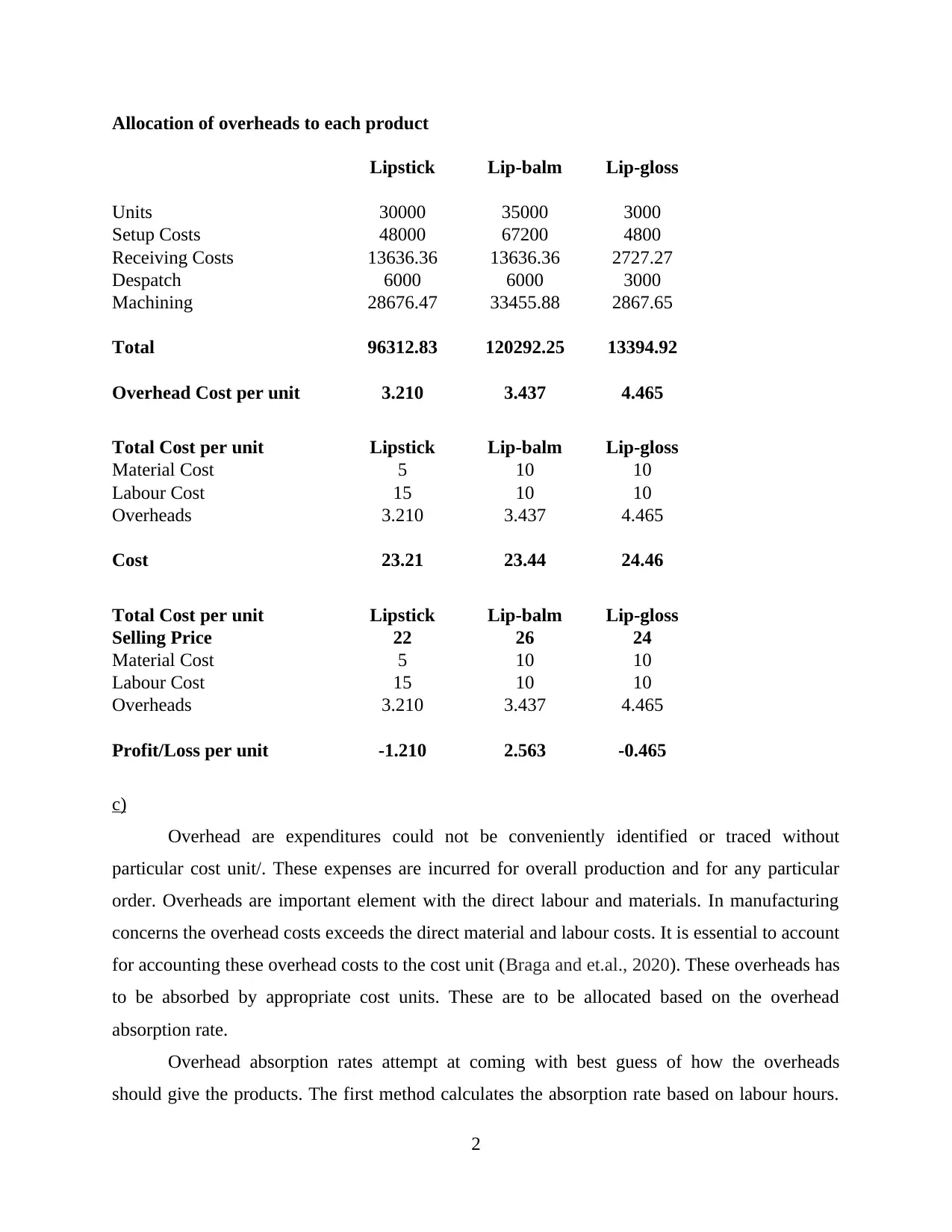

Allocation of overheads to each product

Lipstick Lip-balm Lip-gloss

Units 30000 35000 3000

Setup Costs 48000 67200 4800

Receiving Costs 13636.36 13636.36 2727.27

Despatch 6000 6000 3000

Machining 28676.47 33455.88 2867.65

Total 96312.83 120292.25 13394.92

Overhead Cost per unit 3.210 3.437 4.465

Total Cost per unit Lipstick Lip-balm Lip-gloss

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Cost 23.21 23.44 24.46

Total Cost per unit Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Profit/Loss per unit -1.210 2.563 -0.465

c)

Overhead are expenditures could not be conveniently identified or traced without

particular cost unit/. These expenses are incurred for overall production and for any particular

order. Overheads are important element with the direct labour and materials. In manufacturing

concerns the overhead costs exceeds the direct material and labour costs. It is essential to account

for accounting these overhead costs to the cost unit (Braga and et.al., 2020). These overheads has

to be absorbed by appropriate cost units. These are to be allocated based on the overhead

absorption rate.

Overhead absorption rates attempt at coming with best guess of how the overheads

should give the products. The first method calculates the absorption rate based on labour hours.

2

Lipstick Lip-balm Lip-gloss

Units 30000 35000 3000

Setup Costs 48000 67200 4800

Receiving Costs 13636.36 13636.36 2727.27

Despatch 6000 6000 3000

Machining 28676.47 33455.88 2867.65

Total 96312.83 120292.25 13394.92

Overhead Cost per unit 3.210 3.437 4.465

Total Cost per unit Lipstick Lip-balm Lip-gloss

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Cost 23.21 23.44 24.46

Total Cost per unit Lipstick Lip-balm Lip-gloss

Selling Price 22 26 24

Material Cost 5 10 10

Labour Cost 15 10 10

Overheads 3.210 3.437 4.465

Profit/Loss per unit -1.210 2.563 -0.465

c)

Overhead are expenditures could not be conveniently identified or traced without

particular cost unit/. These expenses are incurred for overall production and for any particular

order. Overheads are important element with the direct labour and materials. In manufacturing

concerns the overhead costs exceeds the direct material and labour costs. It is essential to account

for accounting these overhead costs to the cost unit (Braga and et.al., 2020). These overheads has

to be absorbed by appropriate cost units. These are to be allocated based on the overhead

absorption rate.

Overhead absorption rates attempt at coming with best guess of how the overheads

should give the products. The first method calculates the absorption rate based on labour hours.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The first method do not consider other cost driver that are essential part of the cost. This do not

make proper allocation of costs based on the cost drivers. While on the other activity based

costing method allocates overhead costs based on determining the cost pools and cost drivers. It

ensures that costs are allocated to the products based on the activities and units. Absorption rate

is calculated considering the cost driver. The absorption rate is calculated for each product. It

makes more appropriate allocation of the overhead costs to each product.

The costs under the labour hour rates provides single rate for all the units. This rate is

applied to all the units based on their labour hours. The cost per unit has been 24.16, 22.77 and

22.77. This is inadequate allocation while the activity based costing method calculates absorption

rates for every product (Parikh and Japee, 2018). As it involves all the cost drivers for allocation

of the costs. This method is considered more better.

d)

Sensitivity analysis is used for determining how the independent variable values would

impact the particular dependent variables under the given assumptions is described as the

sensitivity analysis. It is used on one or more variables in the specific range, like effect of labour

rate on price of product.

Sensitivity analysis is is largely used tool by the managers and professions for preparing

strategic plans and for decision making. The sensitivity analysis is also known as what if analysis

which is used by the managers for identifying how outcome would change if original predicted

figures are not achieved or there is change in the underlying assumption. In relation with CVP,

the sensitivity analysis identifies how the operating income change if predicted data for selling

price, variable cost, fixed costs or other costs are not achieved (Geiszler, Baker and Lippitt,

2017). Sensitivity over different outcomes broadens the managers perspectives as what might

actually occurs before they makes the cost commitments.

One of objective of the management accounting aims at analysing and evaluating effect

of the variables like prices, volume and the cost structure on profits of company. CVP analysis

could help company to assess what if scenario for developing better understanding of the

performance in long run.

Margin of Safety

3

make proper allocation of costs based on the cost drivers. While on the other activity based

costing method allocates overhead costs based on determining the cost pools and cost drivers. It

ensures that costs are allocated to the products based on the activities and units. Absorption rate

is calculated considering the cost driver. The absorption rate is calculated for each product. It

makes more appropriate allocation of the overhead costs to each product.

The costs under the labour hour rates provides single rate for all the units. This rate is

applied to all the units based on their labour hours. The cost per unit has been 24.16, 22.77 and

22.77. This is inadequate allocation while the activity based costing method calculates absorption

rates for every product (Parikh and Japee, 2018). As it involves all the cost drivers for allocation

of the costs. This method is considered more better.

d)

Sensitivity analysis is used for determining how the independent variable values would

impact the particular dependent variables under the given assumptions is described as the

sensitivity analysis. It is used on one or more variables in the specific range, like effect of labour

rate on price of product.

Sensitivity analysis is is largely used tool by the managers and professions for preparing

strategic plans and for decision making. The sensitivity analysis is also known as what if analysis

which is used by the managers for identifying how outcome would change if original predicted

figures are not achieved or there is change in the underlying assumption. In relation with CVP,

the sensitivity analysis identifies how the operating income change if predicted data for selling

price, variable cost, fixed costs or other costs are not achieved (Geiszler, Baker and Lippitt,

2017). Sensitivity over different outcomes broadens the managers perspectives as what might

actually occurs before they makes the cost commitments.

One of objective of the management accounting aims at analysing and evaluating effect

of the variables like prices, volume and the cost structure on profits of company. CVP analysis

could help company to assess what if scenario for developing better understanding of the

performance in long run.

Margin of Safety

3

Margin of safety is important components of CVP analysis. It is described as different

between actual sales and break even sales. It could be measured as coarse measure of the risk.

Result of dynamic corporate environment, the certain events could influence actual sales of

company in the manner that could lead to decline than original budgeted sales (VanderWeele and

Ding, 2017). It plays vital role in determining extent of loss company may suffer.

QUESTION 2

a)

Standard Qty (100 units) Actual Qty (4600 units) Standard Qty (4600 units)

Input SQ SP STC AQ AP ATC SQ SP STC

Alpha 40 2 80 2200 1.8 3960 1840 2 3680

Beta 60 5 300 2500 6 15000 2760 5 13800

Gamma 20 1 20 920 1 920 920 1 920

120 400 5620 19880 5520 18400

i) Material Usage Variance = (Standard Quantity for Actual Output-Actual Quantity) x

Standard Price

Alpha (1840-2200) x 2 -720

Beta (2760-2500) x 5 1300

Gamma (920-920) x 1 0

580 (F)

ii) Material Mix Variance(MMV) = (Revised Standard Quantity – Actual Quantity)*

Standard Price

RSQ = Standard Quantity of one material x Total of actual Quantities of all Material

Total of Standard Quantities of all Materials

Material Alpha = 5620/5520 x 1840 = 1873.33

Material Beta = 5620/5520 x 2760 = 2810

Material Gamma = 5620/5520 x 920 = 936.67

Input (RSQ – AQ)x Standard Price Amount

Alpha 1873.33-2200 x 2 -653.34

Beta 2810-2500 x 5 1550

4

between actual sales and break even sales. It could be measured as coarse measure of the risk.

Result of dynamic corporate environment, the certain events could influence actual sales of

company in the manner that could lead to decline than original budgeted sales (VanderWeele and

Ding, 2017). It plays vital role in determining extent of loss company may suffer.

QUESTION 2

a)

Standard Qty (100 units) Actual Qty (4600 units) Standard Qty (4600 units)

Input SQ SP STC AQ AP ATC SQ SP STC

Alpha 40 2 80 2200 1.8 3960 1840 2 3680

Beta 60 5 300 2500 6 15000 2760 5 13800

Gamma 20 1 20 920 1 920 920 1 920

120 400 5620 19880 5520 18400

i) Material Usage Variance = (Standard Quantity for Actual Output-Actual Quantity) x

Standard Price

Alpha (1840-2200) x 2 -720

Beta (2760-2500) x 5 1300

Gamma (920-920) x 1 0

580 (F)

ii) Material Mix Variance(MMV) = (Revised Standard Quantity – Actual Quantity)*

Standard Price

RSQ = Standard Quantity of one material x Total of actual Quantities of all Material

Total of Standard Quantities of all Materials

Material Alpha = 5620/5520 x 1840 = 1873.33

Material Beta = 5620/5520 x 2760 = 2810

Material Gamma = 5620/5520 x 920 = 936.67

Input (RSQ – AQ)x Standard Price Amount

Alpha 1873.33-2200 x 2 -653.34

Beta 2810-2500 x 5 1550

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gamma 936.67- 920 x 1 16.67

931.33 (F)

iii)Material Yield Variance = (Actual Yield - Standard Yield) x standard material cost per

unit of output

Standard Yield= Actual usage of materials

Standard usage per unit of output

Input SQ Standard

yield

Differences Standard

material cost

MYV

Alpha 1840 1873.33 -33.33 2 -66.66

Beta 2760 2810 -50 5 -250

Gamma 920 936.67 -16.67 1 -16.67

5520 5620 -333.33 (A)

b)

Kappa Co produces Omega which is animal feed produced using three products which

are Alpha, Beta and Gamma. Company is currently using standard costing for monitoring the

costs. The standard costing method is effective and useful method which is used by many of the

organisations. The process involves loss of materials due to evaporation from heating. As these

are agriculture products prices and quality varies every year of the products. Standard prices in

the budget are set taking average prices range for last 5 years. Standard mix are set by finance

department.

In the current process production manager receives the operating cost statement

containing variances of material, price, usage, labour and efficiency (VanderWeele and Ding,

2017). There is no reasons stated for the difference and variation between the actual and standard

products.

In standard costing system company is not able to set the standard figures accurately as

they are not able to find the actual prices. There is considerable level of variation between the

quality and prices. It affects the budgets prepared by the company. This method do not consider

the loss from evaporation in variance calculation. This causes high variation between the actual

and budgeted figures. It do not allows the business to identify the actual variances.

Also as the company sets the standards taking average of 5 years it is not able to get the prices

near the standard or actual. It do not allow to make relevant standards for the product and

services. Due to these reasons there is significant variation between the actual and standard

5

931.33 (F)

iii)Material Yield Variance = (Actual Yield - Standard Yield) x standard material cost per

unit of output

Standard Yield= Actual usage of materials

Standard usage per unit of output

Input SQ Standard

yield

Differences Standard

material cost

MYV

Alpha 1840 1873.33 -33.33 2 -66.66

Beta 2760 2810 -50 5 -250

Gamma 920 936.67 -16.67 1 -16.67

5520 5620 -333.33 (A)

b)

Kappa Co produces Omega which is animal feed produced using three products which

are Alpha, Beta and Gamma. Company is currently using standard costing for monitoring the

costs. The standard costing method is effective and useful method which is used by many of the

organisations. The process involves loss of materials due to evaporation from heating. As these

are agriculture products prices and quality varies every year of the products. Standard prices in

the budget are set taking average prices range for last 5 years. Standard mix are set by finance

department.

In the current process production manager receives the operating cost statement

containing variances of material, price, usage, labour and efficiency (VanderWeele and Ding,

2017). There is no reasons stated for the difference and variation between the actual and standard

products.

In standard costing system company is not able to set the standard figures accurately as

they are not able to find the actual prices. There is considerable level of variation between the

quality and prices. It affects the budgets prepared by the company. This method do not consider

the loss from evaporation in variance calculation. This causes high variation between the actual

and budgeted figures. It do not allows the business to identify the actual variances.

Also as the company sets the standards taking average of 5 years it is not able to get the prices

near the standard or actual. It do not allow to make relevant standards for the product and

services. Due to these reasons there is significant variation between the actual and standard

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

figures. Company is also not able to identify the actual reasons for the differences between the

budgeted and actual figures.

The method is useful for costing of product, for cost control and to make the decisions.

The issue with the process is that it very labour intensive, time consuming and it is expensive.

The controversial materiality limit for the variances could be controversial. Management has

business has responsibility to determine material or for unusual variance (VanderWeele and

Ding, 2017). The materiality includes the individual judgement, conflicts or many problems that

could arise in making the materiality limits. Also in the present case workers are not reporting

the reasons for these variances. This do not allow the managers to know the main reason of these

differences. Without identifying the variances corrective actions could not be taken. This do not

allow to assess the actual performance of production manager.

QUESTION 3

a)

Zero Based Budgeting refers to method where the budget is prepared taking zero base

that means that each new budget will be prepared from scratch and no previous data will be used

in the current budget (Zero Based Budgeting, 2021). Each function is assess for determining the

individual needs in the operations and business activities. This method is used by firm which

have product which are prone to high degree of changes. It is not useful for the production

process that do not see changes over short period of time (Saha and et.al., 2021). Management is

required to provide the justify the addition of every item in the budget. As the each item is

entered after analysing them it makes it time and more cost consuming method. This budgeting

method is expensive and requires considerable attention of the managers over each item included

in budget.

Incremental budgeting on the other is budget which is prepared on basis of the previous

budget or actual performance adding the incremental values. The addition is made to both

revenue targets and the resource allocation. It is also known as the traditional budgeting method

which is used by majority of the organisations. This method is easy and simple as compared with

other method and is therefore used by many firms. The management by analysing the current

scenarios such as prices, inflation, supply demand, economic factors and other things to

determine the increments to be made in the budget (May, 2017). It is done using different tools

6

budgeted and actual figures.

The method is useful for costing of product, for cost control and to make the decisions.

The issue with the process is that it very labour intensive, time consuming and it is expensive.

The controversial materiality limit for the variances could be controversial. Management has

business has responsibility to determine material or for unusual variance (VanderWeele and

Ding, 2017). The materiality includes the individual judgement, conflicts or many problems that

could arise in making the materiality limits. Also in the present case workers are not reporting

the reasons for these variances. This do not allow the managers to know the main reason of these

differences. Without identifying the variances corrective actions could not be taken. This do not

allow to assess the actual performance of production manager.

QUESTION 3

a)

Zero Based Budgeting refers to method where the budget is prepared taking zero base

that means that each new budget will be prepared from scratch and no previous data will be used

in the current budget (Zero Based Budgeting, 2021). Each function is assess for determining the

individual needs in the operations and business activities. This method is used by firm which

have product which are prone to high degree of changes. It is not useful for the production

process that do not see changes over short period of time (Saha and et.al., 2021). Management is

required to provide the justify the addition of every item in the budget. As the each item is

entered after analysing them it makes it time and more cost consuming method. This budgeting

method is expensive and requires considerable attention of the managers over each item included

in budget.

Incremental budgeting on the other is budget which is prepared on basis of the previous

budget or actual performance adding the incremental values. The addition is made to both

revenue targets and the resource allocation. It is also known as the traditional budgeting method

which is used by majority of the organisations. This method is easy and simple as compared with

other method and is therefore used by many firms. The management by analysing the current

scenarios such as prices, inflation, supply demand, economic factors and other things to

determine the increments to be made in the budget (May, 2017). It is done using different tools

6

for preparing the budget. This method is used where the business do not have much changes and

follows a constant method of cost allocation and resource allocation.

However there is significant difference between the two methods:

Application: Incremental budget is used commonly under budgeting by the management as it is

simple and easy to understand. It provides achievable target without involving cost of

formulating it. ZBB on other is more time consuming and complicated method. As each activity

needs to allocate costs from the scratch, targets are re-evaluated than just revising.

Primary focus: Main focus is on activities which are essential for the organisation. It requires

time and resources, as used at the strategic level for setting the budgets which are congruent

with vision of organisation. Primary focus of traditional budgeting is on regular activities which

do not require high professional expertise. The budgeting could be applied at operational and

management levels where variable does not differs from actuals quickly.

Cost Analysis: ZBB works for minimising chances of the risk and errors in activity. It evaluated

every expense and process from the base and aims at mitigating chances of the non value adding

expenditures to be occurred. It results in enhancing effectiveness and efficiency of the

procedures and operations. On other incremental budget do not involve high expertise to general

processes included in task other than adding or subtracting from previous results which makes it

difficulty to mitigate identifying the wasteful expenses (Rubin and Abramson, 2018).

Resource Allocation: Both human and financial resources are essential for making ZBB.

Management of the company require the professional and the relevant experience, knowledge

and the skills for preparing such budgets. In incremental budgeting the budgets are simple to

prepare as it does not requires the specialist knowledge or skills. It could also be prepared with

managers having basic knowledge of the tasks and activities.

It could be said that both the method are used by the organisation due to their

effectiveness but than also they fail to perfectly plan the future processes and expenditures. It

requires significant coordination of all the departments for implementation and controlling the

costs. Both these budgets fail to do this therefore are not highly effective budgeting methods.

7

follows a constant method of cost allocation and resource allocation.

However there is significant difference between the two methods:

Application: Incremental budget is used commonly under budgeting by the management as it is

simple and easy to understand. It provides achievable target without involving cost of

formulating it. ZBB on other is more time consuming and complicated method. As each activity

needs to allocate costs from the scratch, targets are re-evaluated than just revising.

Primary focus: Main focus is on activities which are essential for the organisation. It requires

time and resources, as used at the strategic level for setting the budgets which are congruent

with vision of organisation. Primary focus of traditional budgeting is on regular activities which

do not require high professional expertise. The budgeting could be applied at operational and

management levels where variable does not differs from actuals quickly.

Cost Analysis: ZBB works for minimising chances of the risk and errors in activity. It evaluated

every expense and process from the base and aims at mitigating chances of the non value adding

expenditures to be occurred. It results in enhancing effectiveness and efficiency of the

procedures and operations. On other incremental budget do not involve high expertise to general

processes included in task other than adding or subtracting from previous results which makes it

difficulty to mitigate identifying the wasteful expenses (Rubin and Abramson, 2018).

Resource Allocation: Both human and financial resources are essential for making ZBB.

Management of the company require the professional and the relevant experience, knowledge

and the skills for preparing such budgets. In incremental budgeting the budgets are simple to

prepare as it does not requires the specialist knowledge or skills. It could also be prepared with

managers having basic knowledge of the tasks and activities.

It could be said that both the method are used by the organisation due to their

effectiveness but than also they fail to perfectly plan the future processes and expenditures. It

requires significant coordination of all the departments for implementation and controlling the

costs. Both these budgets fail to do this therefore are not highly effective budgeting methods.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Braga, G. H. R., and et.al., 2020 Measurement of costs of quality in wood plywood production

by the ABC (Activity Based Costing) costing method and by Absorption.

Geiszler, M., Baker, K. and Lippitt, J., 2017. Variable Activity‐Based Costing and Decision

Making. Journal of Corporate Accounting & Finance. 28(5). pp.45-52.

Jere, H., 2017. An evaluation of variance analysis as a function of internal control (Case study of

Losave Investments)(Doctoral dissertation, BUSE).

May, A. U., 2017. Traditional budgeting in today’s business environment. Journal of Applied

Finance & Banking. 7(3). pp.111-120.

Parikh, C. N. and Japee, G.P., ACTIVITY BASED COSTING–A TOOL OF ACCURATE

COSTING.

Rubin, G. D. and Abramson, R. G., 2018. Creating value through incremental innovation:

Managing culture, structure, and process. Radiology. 288(2). pp.330-340.

Saha, R. and et.al., 2021. Integrated economic design of quality control and maintenance

management: Implications for managing manufacturing process. International Journal of

System Assurance Engineering and Management. pp.1-18.

VanderWeele, T. J. and Ding, P., 2017. Sensitivity analysis in observational research:

introducing the E-value. Annals of internal medicine. 167(4). pp.268-274.

Online

Zero Based Budgeting. 2021. Online. Available through:

<https://efinancemanagement.com/budgeting/zero-based>.

8

Books and Journals

Braga, G. H. R., and et.al., 2020 Measurement of costs of quality in wood plywood production

by the ABC (Activity Based Costing) costing method and by Absorption.

Geiszler, M., Baker, K. and Lippitt, J., 2017. Variable Activity‐Based Costing and Decision

Making. Journal of Corporate Accounting & Finance. 28(5). pp.45-52.

Jere, H., 2017. An evaluation of variance analysis as a function of internal control (Case study of

Losave Investments)(Doctoral dissertation, BUSE).

May, A. U., 2017. Traditional budgeting in today’s business environment. Journal of Applied

Finance & Banking. 7(3). pp.111-120.

Parikh, C. N. and Japee, G.P., ACTIVITY BASED COSTING–A TOOL OF ACCURATE

COSTING.

Rubin, G. D. and Abramson, R. G., 2018. Creating value through incremental innovation:

Managing culture, structure, and process. Radiology. 288(2). pp.330-340.

Saha, R. and et.al., 2021. Integrated economic design of quality control and maintenance

management: Implications for managing manufacturing process. International Journal of

System Assurance Engineering and Management. pp.1-18.

VanderWeele, T. J. and Ding, P., 2017. Sensitivity analysis in observational research:

introducing the E-value. Annals of internal medicine. 167(4). pp.268-274.

Online

Zero Based Budgeting. 2021. Online. Available through:

<https://efinancemanagement.com/budgeting/zero-based>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.