Comparative Financial Analysis and Valuation of Tesco PLC

VerifiedAdded on 2021/02/20

|13

|3554

|245

Report

AI Summary

This report provides a detailed financial analysis of Tesco PLC, a major player in the grocery retail sector, comparing its performance to its competitor, Morrisons. The analysis encompasses a review of the statement of financial position, income statements, and a comprehensive ratio analysis, including liquidity, profitability, and solvency criteria. The report calculates Tesco's value using asset-based valuation, the Price-Earnings (P/E) ratio method, and a dividend valuation model, employing the Capital Asset Pricing Model (CAPM) to estimate the required return. The report also discusses the limitations of the comparison and valuation methodologies, offering a critical evaluation of the approaches used. The conclusion summarizes the key findings regarding Tesco's financial health and performance relative to its competitor.

Finance.

Table of Contents

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

2.1 Analysis of financial performance of Tesco compared to its competitor Morrisons:..........3

2.2 Company Valuation:.............................................................................................................6

2.3 Capital Structure..................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

TASK...............................................................................................................................................3

2.1 Analysis of financial performance of Tesco compared to its competitor Morrisons:..........3

2.2 Company Valuation:.............................................................................................................6

2.3 Capital Structure..................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Finance is a life line for a business organisation as it provides funds to such company for

smoothly running its operations effectively and efficiently. It is concerned with art of money

management by allocating assets and liabilities in right direction in conducting business

(Buchner and et.al., 2014). For understanding of such topic, company named TESCO Plc is

chosen which is engaged in providing groceries items through general merchandise retail

business and UK based multinational company. This report provides evaluation of financial

statements of above mentioned company by making comparison with another competitor named

Morrisons. Information about the capital structure is also provided in such report along with

valuation of such company's shares.

TASK

2.1 Analysis of financial performance of Tesco compared to its competitor Morrisons:

A. Analysis of statement of financial position:

Tesco has reported in year 2018 total assets amounting GBP 44862 million whereas

company's total liabilities are GBP 34382 millions. While on other hand Morrisons has reported

assets of GBP 9667 million and overall liabilities amounting GBP 5122 million in year 2018.

Which indicates that Tesco has is performing at larger scale as compare to it's competitor

Morrisons. Tesco has wide range of resources and gaining competitive advantages (About

financial statement of Tesco. 2019). Tesco has shareholder's fund amounting GBP 10480 million

while Morrisons has reported shareholder's fund of GBP 4545 million indicating that Tesco's

funding structure is more efficient as compare to Morrisons. Tesco's current assets are GBP

13726 millions and current liabilities are GBP 19238 million. On other hand Morrisons current

assets are of GBP 1278 millions and current liabilities are of GBP 3081.

B. Analysis of Income Statements:

Tesco's revenue in year 2018 as per reported income statement is GBP 57491 million

whereas Morrisons has reported overall revenue of GBP 17262 million in year 2018, it indicates

that Tesco is mre efficient to generate revenue as comparison of it's competitor. Operating

income of Tesco is 1564 million in year 2018 whereas GBP 439 million showing that Tesco has

more efficient in providing operating income. Tesco's net profit is 1206 million in year 2018

while Morrison's net profit in year 2018 is GBP 311 million (About financial statement of

Finance is a life line for a business organisation as it provides funds to such company for

smoothly running its operations effectively and efficiently. It is concerned with art of money

management by allocating assets and liabilities in right direction in conducting business

(Buchner and et.al., 2014). For understanding of such topic, company named TESCO Plc is

chosen which is engaged in providing groceries items through general merchandise retail

business and UK based multinational company. This report provides evaluation of financial

statements of above mentioned company by making comparison with another competitor named

Morrisons. Information about the capital structure is also provided in such report along with

valuation of such company's shares.

TASK

2.1 Analysis of financial performance of Tesco compared to its competitor Morrisons:

A. Analysis of statement of financial position:

Tesco has reported in year 2018 total assets amounting GBP 44862 million whereas

company's total liabilities are GBP 34382 millions. While on other hand Morrisons has reported

assets of GBP 9667 million and overall liabilities amounting GBP 5122 million in year 2018.

Which indicates that Tesco has is performing at larger scale as compare to it's competitor

Morrisons. Tesco has wide range of resources and gaining competitive advantages (About

financial statement of Tesco. 2019). Tesco has shareholder's fund amounting GBP 10480 million

while Morrisons has reported shareholder's fund of GBP 4545 million indicating that Tesco's

funding structure is more efficient as compare to Morrisons. Tesco's current assets are GBP

13726 millions and current liabilities are GBP 19238 million. On other hand Morrisons current

assets are of GBP 1278 millions and current liabilities are of GBP 3081.

B. Analysis of Income Statements:

Tesco's revenue in year 2018 as per reported income statement is GBP 57491 million

whereas Morrisons has reported overall revenue of GBP 17262 million in year 2018, it indicates

that Tesco is mre efficient to generate revenue as comparison of it's competitor. Operating

income of Tesco is 1564 million in year 2018 whereas GBP 439 million showing that Tesco has

more efficient in providing operating income. Tesco's net profit is 1206 million in year 2018

while Morrison's net profit in year 2018 is GBP 311 million (About financial statement of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

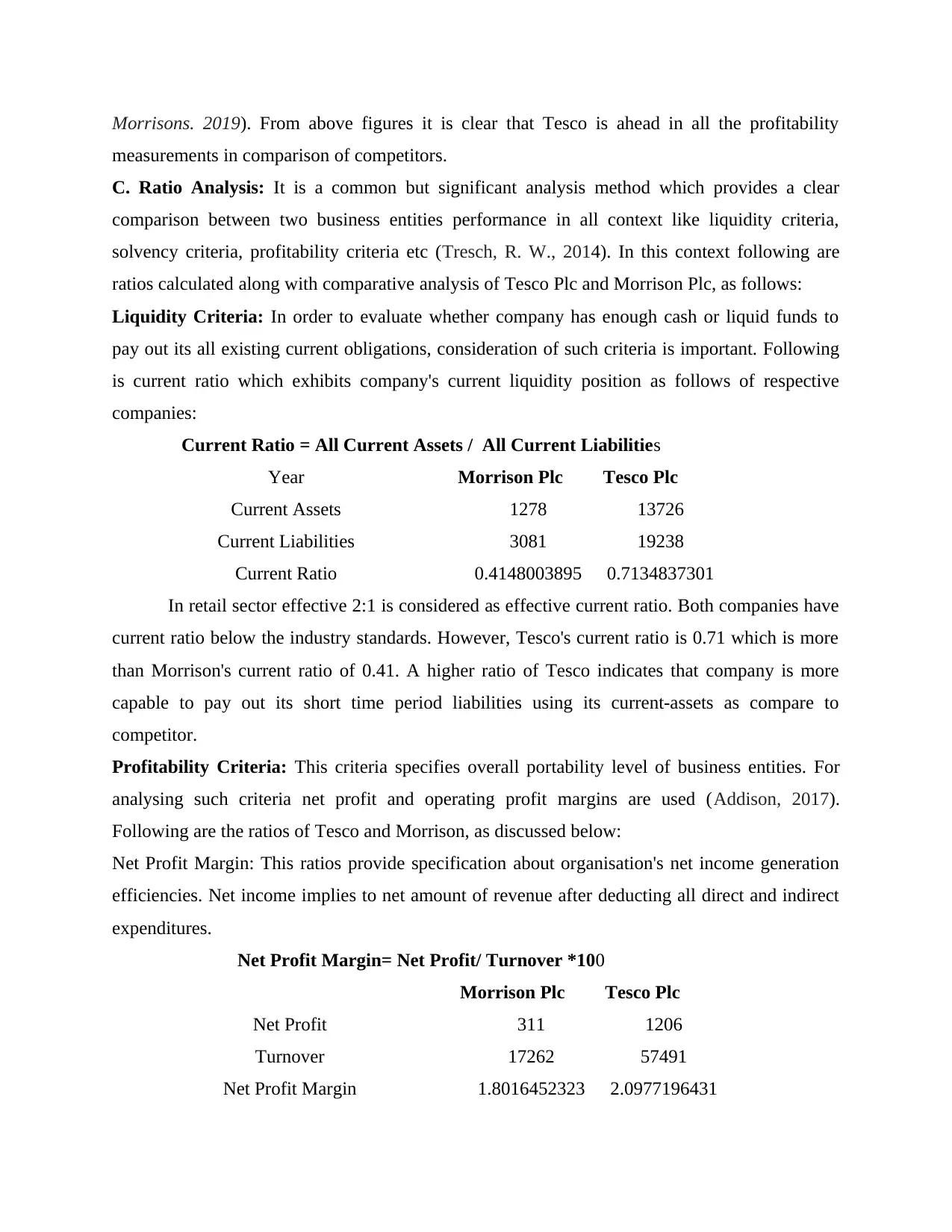

Morrisons. 2019). From above figures it is clear that Tesco is ahead in all the profitability

measurements in comparison of competitors.

C. Ratio Analysis: It is a common but significant analysis method which provides a clear

comparison between two business entities performance in all context like liquidity criteria,

solvency criteria, profitability criteria etc (Tresch, R. W., 2014). In this context following are

ratios calculated along with comparative analysis of Tesco Plc and Morrison Plc, as follows:

Liquidity Criteria: In order to evaluate whether company has enough cash or liquid funds to

pay out its all existing current obligations, consideration of such criteria is important. Following

is current ratio which exhibits company's current liquidity position as follows of respective

companies:

Current Ratio = All Current Assets / All Current Liabilities

Year Morrison Plc Tesco Plc

Current Assets 1278 13726

Current Liabilities 3081 19238

Current Ratio 0.4148003895 0.7134837301

In retail sector effective 2:1 is considered as effective current ratio. Both companies have

current ratio below the industry standards. However, Tesco's current ratio is 0.71 which is more

than Morrison's current ratio of 0.41. A higher ratio of Tesco indicates that company is more

capable to pay out its short time period liabilities using its current-assets as compare to

competitor.

Profitability Criteria: This criteria specifies overall portability level of business entities. For

analysing such criteria net profit and operating profit margins are used (Addison, 2017).

Following are the ratios of Tesco and Morrison, as discussed below:

Net Profit Margin: This ratios provide specification about organisation's net income generation

efficiencies. Net income implies to net amount of revenue after deducting all direct and indirect

expenditures.

Net Profit Margin= Net Profit/ Turnover *100

Morrison Plc Tesco Plc

Net Profit 311 1206

Turnover 17262 57491

Net Profit Margin 1.8016452323 2.0977196431

measurements in comparison of competitors.

C. Ratio Analysis: It is a common but significant analysis method which provides a clear

comparison between two business entities performance in all context like liquidity criteria,

solvency criteria, profitability criteria etc (Tresch, R. W., 2014). In this context following are

ratios calculated along with comparative analysis of Tesco Plc and Morrison Plc, as follows:

Liquidity Criteria: In order to evaluate whether company has enough cash or liquid funds to

pay out its all existing current obligations, consideration of such criteria is important. Following

is current ratio which exhibits company's current liquidity position as follows of respective

companies:

Current Ratio = All Current Assets / All Current Liabilities

Year Morrison Plc Tesco Plc

Current Assets 1278 13726

Current Liabilities 3081 19238

Current Ratio 0.4148003895 0.7134837301

In retail sector effective 2:1 is considered as effective current ratio. Both companies have

current ratio below the industry standards. However, Tesco's current ratio is 0.71 which is more

than Morrison's current ratio of 0.41. A higher ratio of Tesco indicates that company is more

capable to pay out its short time period liabilities using its current-assets as compare to

competitor.

Profitability Criteria: This criteria specifies overall portability level of business entities. For

analysing such criteria net profit and operating profit margins are used (Addison, 2017).

Following are the ratios of Tesco and Morrison, as discussed below:

Net Profit Margin: This ratios provide specification about organisation's net income generation

efficiencies. Net income implies to net amount of revenue after deducting all direct and indirect

expenditures.

Net Profit Margin= Net Profit/ Turnover *100

Morrison Plc Tesco Plc

Net Profit 311 1206

Turnover 17262 57491

Net Profit Margin 1.8016452323 2.0977196431

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

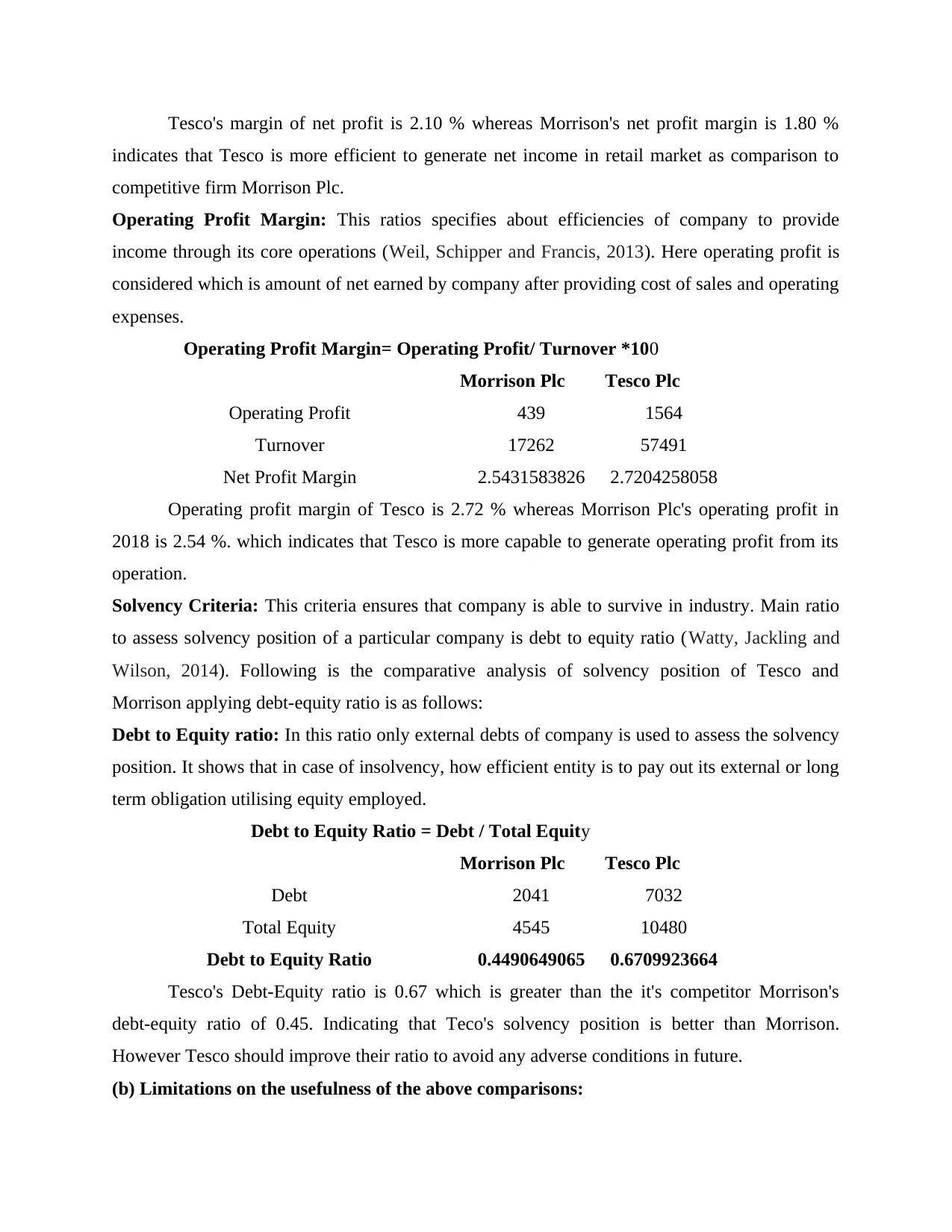

Tesco's margin of net profit is 2.10 % whereas Morrison's net profit margin is 1.80 %

indicates that Tesco is more efficient to generate net income in retail market as comparison to

competitive firm Morrison Plc.

Operating Profit Margin: This ratios specifies about efficiencies of company to provide

income through its core operations (Weil, Schipper and Francis, 2013). Here operating profit is

considered which is amount of net earned by company after providing cost of sales and operating

expenses.

Operating Profit Margin= Operating Profit/ Turnover *100

Morrison Plc Tesco Plc

Operating Profit 439 1564

Turnover 17262 57491

Net Profit Margin 2.5431583826 2.7204258058

Operating profit margin of Tesco is 2.72 % whereas Morrison Plc's operating profit in

2018 is 2.54 %. which indicates that Tesco is more capable to generate operating profit from its

operation.

Solvency Criteria: This criteria ensures that company is able to survive in industry. Main ratio

to assess solvency position of a particular company is debt to equity ratio (Watty, Jackling and

Wilson, 2014). Following is the comparative analysis of solvency position of Tesco and

Morrison applying debt-equity ratio is as follows:

Debt to Equity ratio: In this ratio only external debts of company is used to assess the solvency

position. It shows that in case of insolvency, how efficient entity is to pay out its external or long

term obligation utilising equity employed.

Debt to Equity Ratio = Debt / Total Equity

Morrison Plc Tesco Plc

Debt 2041 7032

Total Equity 4545 10480

Debt to Equity Ratio 0.4490649065 0.6709923664

Tesco's Debt-Equity ratio is 0.67 which is greater than the it's competitor Morrison's

debt-equity ratio of 0.45. Indicating that Teco's solvency position is better than Morrison.

However Tesco should improve their ratio to avoid any adverse conditions in future.

(b) Limitations on the usefulness of the above comparisons:

indicates that Tesco is more efficient to generate net income in retail market as comparison to

competitive firm Morrison Plc.

Operating Profit Margin: This ratios specifies about efficiencies of company to provide

income through its core operations (Weil, Schipper and Francis, 2013). Here operating profit is

considered which is amount of net earned by company after providing cost of sales and operating

expenses.

Operating Profit Margin= Operating Profit/ Turnover *100

Morrison Plc Tesco Plc

Operating Profit 439 1564

Turnover 17262 57491

Net Profit Margin 2.5431583826 2.7204258058

Operating profit margin of Tesco is 2.72 % whereas Morrison Plc's operating profit in

2018 is 2.54 %. which indicates that Tesco is more capable to generate operating profit from its

operation.

Solvency Criteria: This criteria ensures that company is able to survive in industry. Main ratio

to assess solvency position of a particular company is debt to equity ratio (Watty, Jackling and

Wilson, 2014). Following is the comparative analysis of solvency position of Tesco and

Morrison applying debt-equity ratio is as follows:

Debt to Equity ratio: In this ratio only external debts of company is used to assess the solvency

position. It shows that in case of insolvency, how efficient entity is to pay out its external or long

term obligation utilising equity employed.

Debt to Equity Ratio = Debt / Total Equity

Morrison Plc Tesco Plc

Debt 2041 7032

Total Equity 4545 10480

Debt to Equity Ratio 0.4490649065 0.6709923664

Tesco's Debt-Equity ratio is 0.67 which is greater than the it's competitor Morrison's

debt-equity ratio of 0.45. Indicating that Teco's solvency position is better than Morrison.

However Tesco should improve their ratio to avoid any adverse conditions in future.

(b) Limitations on the usefulness of the above comparisons:

1. Analysis of reported information does not provides clear picture as it does not combines

effect of external factors such as inflation rate, economic stability of industry.

2. Only quantitative aspects and variables are taken in comparisons, and qualitative aspects

or facts are completely ignored (Collis, Holt and Hussey, 2017).

3. Year data is commonly used in such comparisons so these do not provides a current and

updated performance of company.

4. An organisation can alter its actual operational structure in order to manipulate to such

extent that ratios measured in several time period ago and compared to today's same ratio

would yield or lead to a misleading conclusion.

2.2 Company Valuation:

(a) Calculate of value of Tesco though different methods:

Asset Based Valuation: Asset-based valuation is indeed a method of enterprise valuation which,

after deduction of obligations, concentrates on the worth of a company's assets or the fair value

of all its total assets (Ainsworth and Deines, 2019). Under this method company's net assets

value is considered as value of of company. It is simple method as it considers company's net

worth or shareholder fund as value of company.

Asset Based Valuation of Tesco Plc

2019-02

Amount

Assets

GBP in Million except per

share data

Current assets

Cash

Cash and other cash equivalent items 2916

Investments: Short-term 457

Total cash 3373

Stock 2617

Other current assets 6678

Total current assets 12668

Non-current assets

Property, plant and equipment

effect of external factors such as inflation rate, economic stability of industry.

2. Only quantitative aspects and variables are taken in comparisons, and qualitative aspects

or facts are completely ignored (Collis, Holt and Hussey, 2017).

3. Year data is commonly used in such comparisons so these do not provides a current and

updated performance of company.

4. An organisation can alter its actual operational structure in order to manipulate to such

extent that ratios measured in several time period ago and compared to today's same ratio

would yield or lead to a misleading conclusion.

2.2 Company Valuation:

(a) Calculate of value of Tesco though different methods:

Asset Based Valuation: Asset-based valuation is indeed a method of enterprise valuation which,

after deduction of obligations, concentrates on the worth of a company's assets or the fair value

of all its total assets (Ainsworth and Deines, 2019). Under this method company's net assets

value is considered as value of of company. It is simple method as it considers company's net

worth or shareholder fund as value of company.

Asset Based Valuation of Tesco Plc

2019-02

Amount

Assets

GBP in Million except per

share data

Current assets

Cash

Cash and other cash equivalent items 2916

Investments: Short-term 457

Total cash 3373

Stock 2617

Other current assets 6678

Total current assets 12668

Non-current assets

Property, plant and equipment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

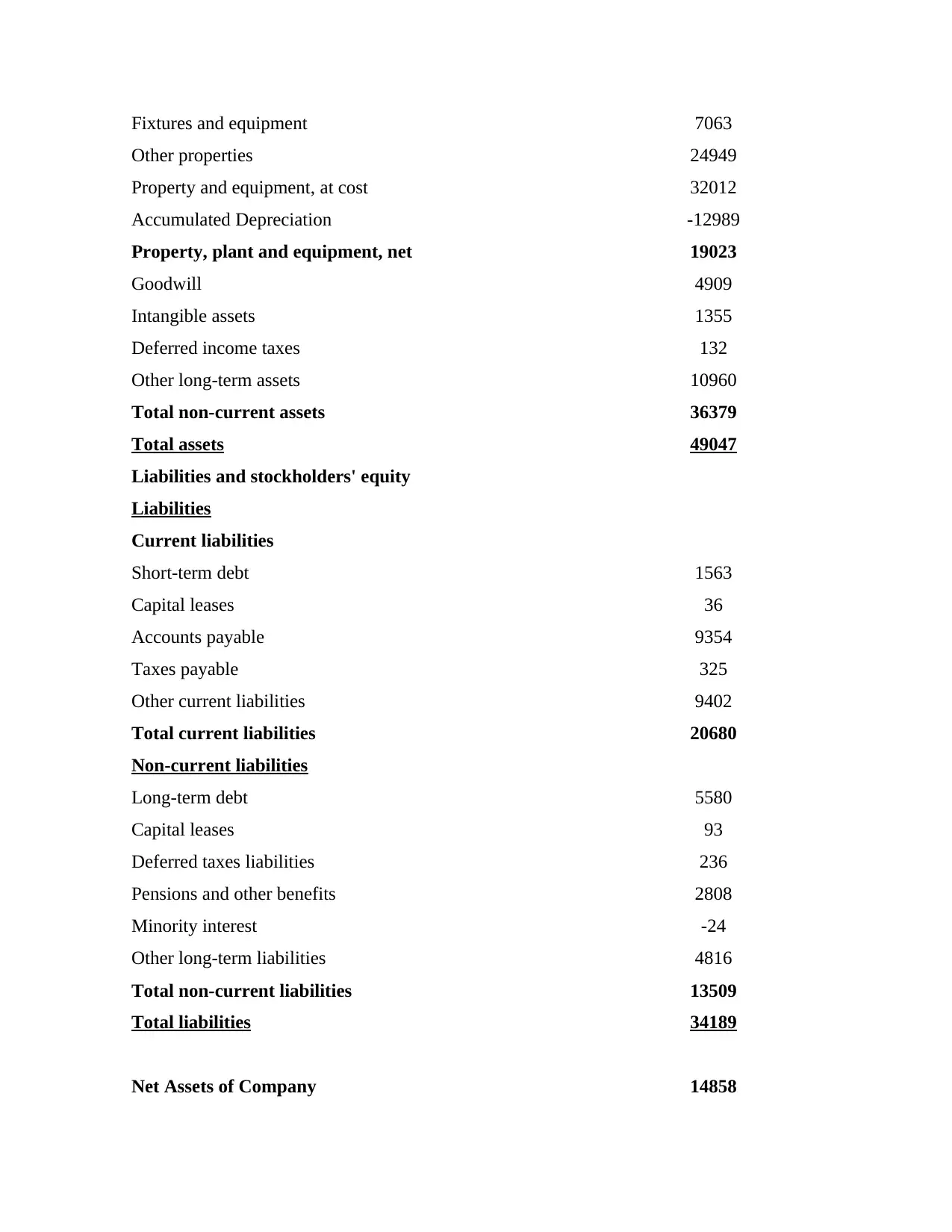

Fixtures and equipment 7063

Other properties 24949

Property and equipment, at cost 32012

Accumulated Depreciation -12989

Property, plant and equipment, net 19023

Goodwill 4909

Intangible assets 1355

Deferred income taxes 132

Other long-term assets 10960

Total non-current assets 36379

Total assets 49047

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 1563

Capital leases 36

Accounts payable 9354

Taxes payable 325

Other current liabilities 9402

Total current liabilities 20680

Non-current liabilities

Long-term debt 5580

Capital leases 93

Deferred taxes liabilities 236

Pensions and other benefits 2808

Minority interest -24

Other long-term liabilities 4816

Total non-current liabilities 13509

Total liabilities 34189

Net Assets of Company 14858

Other properties 24949

Property and equipment, at cost 32012

Accumulated Depreciation -12989

Property, plant and equipment, net 19023

Goodwill 4909

Intangible assets 1355

Deferred income taxes 132

Other long-term assets 10960

Total non-current assets 36379

Total assets 49047

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 1563

Capital leases 36

Accounts payable 9354

Taxes payable 325

Other current liabilities 9402

Total current liabilities 20680

Non-current liabilities

Long-term debt 5580

Capital leases 93

Deferred taxes liabilities 236

Pensions and other benefits 2808

Minority interest -24

Other long-term liabilities 4816

Total non-current liabilities 13509

Total liabilities 34189

Net Assets of Company 14858

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

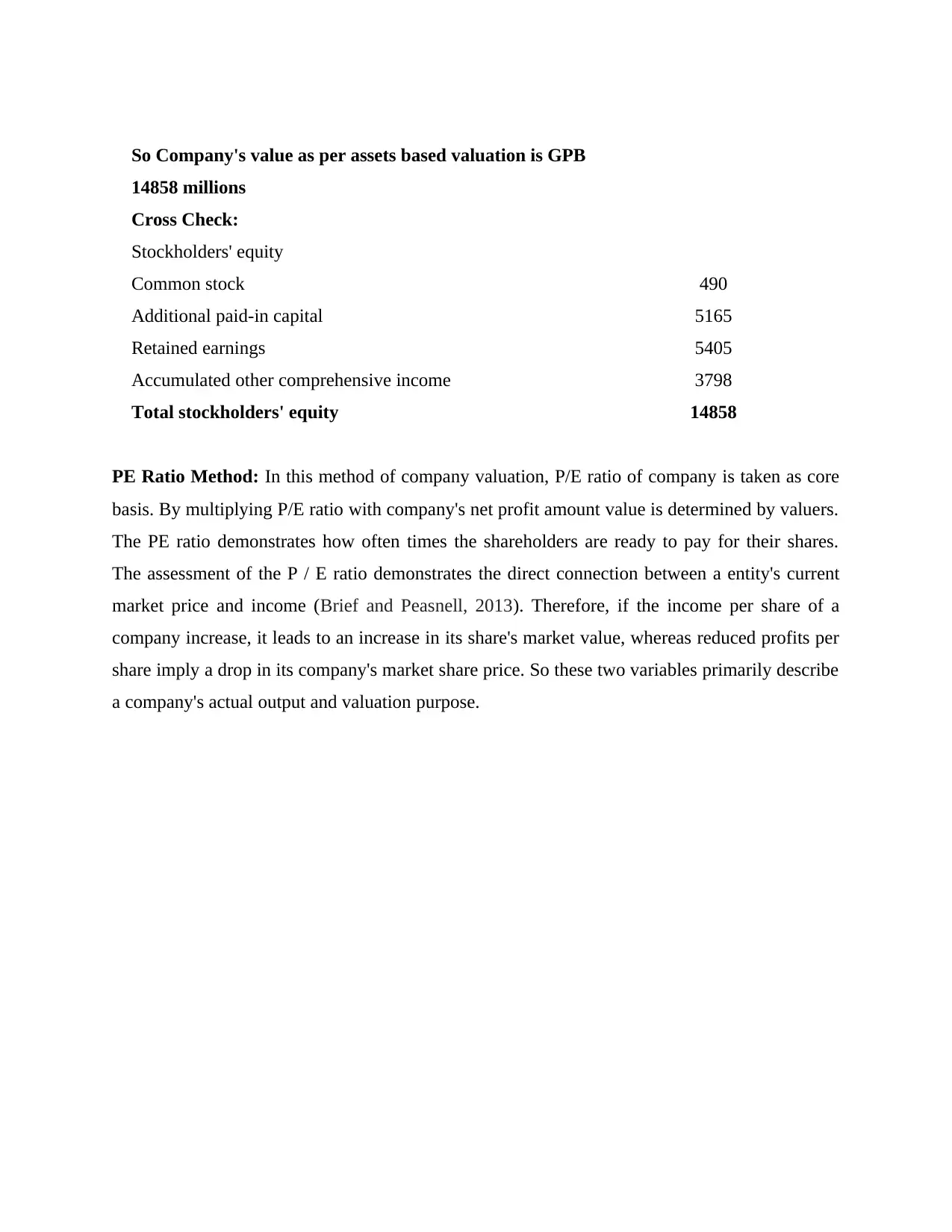

So Company's value as per assets based valuation is GPB

14858 millions

Cross Check:

Stockholders' equity

Common stock 490

Additional paid-in capital 5165

Retained earnings 5405

Accumulated other comprehensive income 3798

Total stockholders' equity 14858

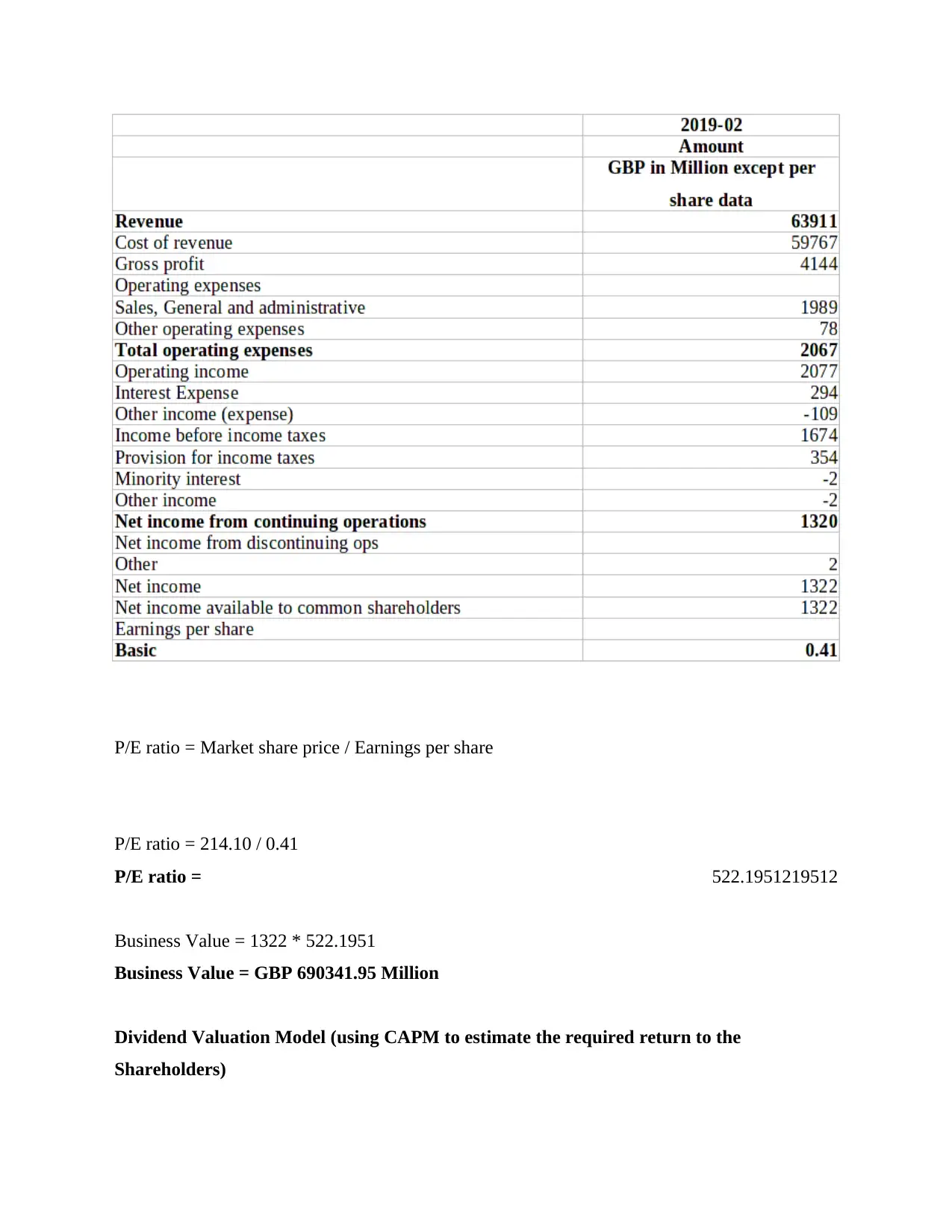

PE Ratio Method: In this method of company valuation, P/E ratio of company is taken as core

basis. By multiplying P/E ratio with company's net profit amount value is determined by valuers.

The PE ratio demonstrates how often times the shareholders are ready to pay for their shares.

The assessment of the P / E ratio demonstrates the direct connection between a entity's current

market price and income (Brief and Peasnell, 2013). Therefore, if the income per share of a

company increase, it leads to an increase in its share's market value, whereas reduced profits per

share imply a drop in its company's market share price. So these two variables primarily describe

a company's actual output and valuation purpose.

14858 millions

Cross Check:

Stockholders' equity

Common stock 490

Additional paid-in capital 5165

Retained earnings 5405

Accumulated other comprehensive income 3798

Total stockholders' equity 14858

PE Ratio Method: In this method of company valuation, P/E ratio of company is taken as core

basis. By multiplying P/E ratio with company's net profit amount value is determined by valuers.

The PE ratio demonstrates how often times the shareholders are ready to pay for their shares.

The assessment of the P / E ratio demonstrates the direct connection between a entity's current

market price and income (Brief and Peasnell, 2013). Therefore, if the income per share of a

company increase, it leads to an increase in its share's market value, whereas reduced profits per

share imply a drop in its company's market share price. So these two variables primarily describe

a company's actual output and valuation purpose.

P/E ratio = Market share price / Earnings per share

P/E ratio = 214.10 / 0.41

P/E ratio = 522.1951219512

Business Value = 1322 * 522.1951

Business Value = GBP 690341.95 Million

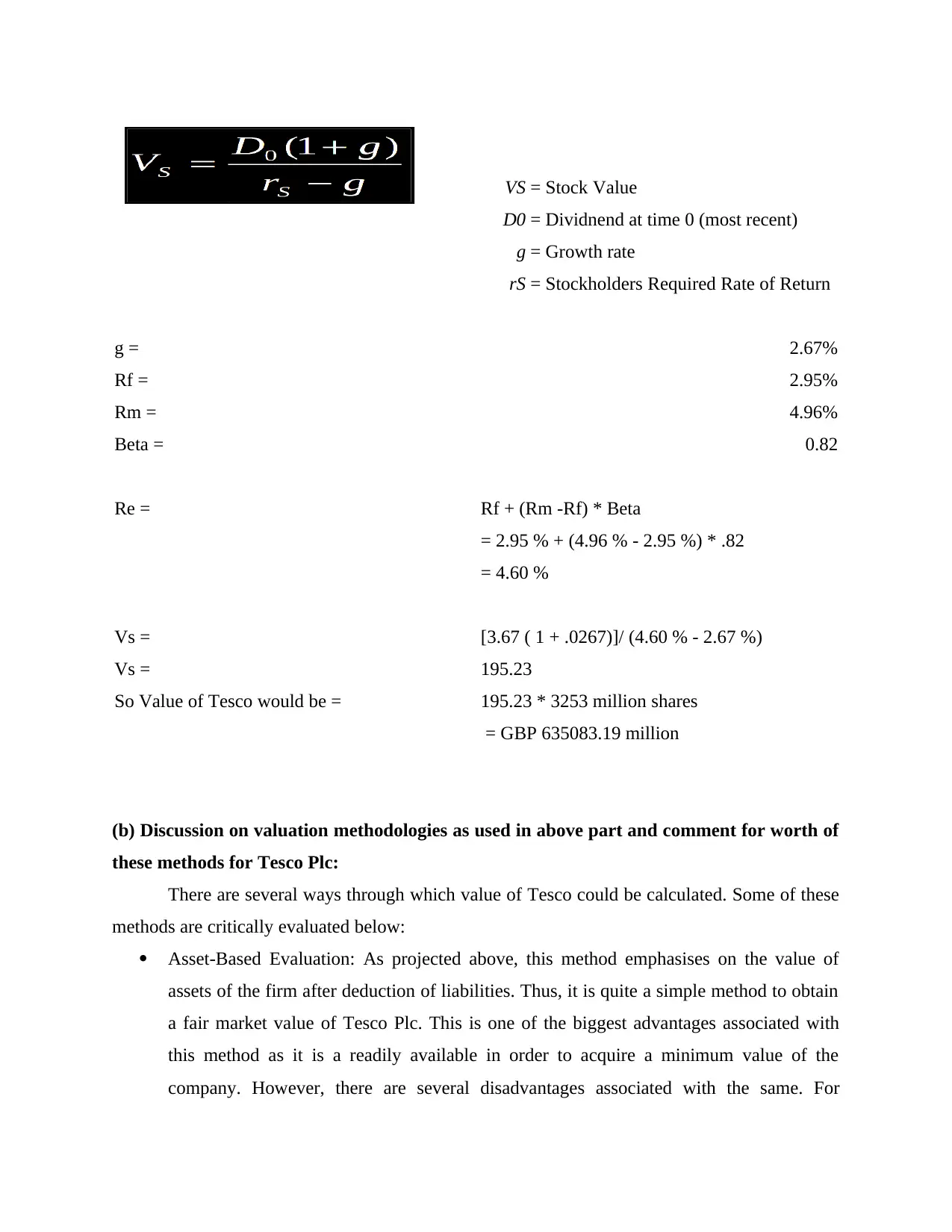

Dividend Valuation Model (using CAPM to estimate the required return to the

Shareholders)

P/E ratio = 214.10 / 0.41

P/E ratio = 522.1951219512

Business Value = 1322 * 522.1951

Business Value = GBP 690341.95 Million

Dividend Valuation Model (using CAPM to estimate the required return to the

Shareholders)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VS = Stock Value

D0 = Dividnend at time 0 (most recent)

g = Growth rate

rS = Stockholders Required Rate of Return

g = 2.67%

Rf = 2.95%

Rm = 4.96%

Beta = 0.82

Re = Rf + (Rm -Rf) * Beta

= 2.95 % + (4.96 % - 2.95 %) * .82

= 4.60 %

Vs = [3.67 ( 1 + .0267)]/ (4.60 % - 2.67 %)

Vs = 195.23

So Value of Tesco would be = 195.23 * 3253 million shares

= GBP 635083.19 million

(b) Discussion on valuation methodologies as used in above part and comment for worth of

these methods for Tesco Plc:

There are several ways through which value of Tesco could be calculated. Some of these

methods are critically evaluated below:

Asset-Based Evaluation: As projected above, this method emphasises on the value of

assets of the firm after deduction of liabilities. Thus, it is quite a simple method to obtain

a fair market value of Tesco Plc. This is one of the biggest advantages associated with

this method as it is a readily available in order to acquire a minimum value of the

company. However, there are several disadvantages associated with the same. For

D0 = Dividnend at time 0 (most recent)

g = Growth rate

rS = Stockholders Required Rate of Return

g = 2.67%

Rf = 2.95%

Rm = 4.96%

Beta = 0.82

Re = Rf + (Rm -Rf) * Beta

= 2.95 % + (4.96 % - 2.95 %) * .82

= 4.60 %

Vs = [3.67 ( 1 + .0267)]/ (4.60 % - 2.67 %)

Vs = 195.23

So Value of Tesco would be = 195.23 * 3253 million shares

= GBP 635083.19 million

(b) Discussion on valuation methodologies as used in above part and comment for worth of

these methods for Tesco Plc:

There are several ways through which value of Tesco could be calculated. Some of these

methods are critically evaluated below:

Asset-Based Evaluation: As projected above, this method emphasises on the value of

assets of the firm after deduction of liabilities. Thus, it is quite a simple method to obtain

a fair market value of Tesco Plc. This is one of the biggest advantages associated with

this method as it is a readily available in order to acquire a minimum value of the

company. However, there are several disadvantages associated with the same. For

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

instance, it ignores valuation of intangible assets like intellectual property. Moreover,

premature valuation might be performed due to depreciation (Gitman, Juchau and

Flanagan, 2015).

Dividend Valuation Method: This method determines the overall value of stock, as

displayed above. It's biggest advantage is that it is quite risk-free as well as it removes

subjectivity from equation. However, it is only applied on stocks that pay dividends

within the company, as well as does not undertake non-dividend factors into account.

P/E Ratio: The Price/Earning ratio helps in valuing an organisation by measuring its

current share price relative to its per-share earnings. It is quite an effective method which

allows the company to measure degree of confidence which investors have on firm's

future, which helps the firm in identifying its appropriate value. However, at company

level, it could easily be manipulated, compared to other metrics like dividend and cash

flow. Moreover, it enhances risk as earnings are a single factor used for valuation.

Thus, out of all the methods, P/E Ratio seems to be the best method for the company to

ensure appropriate valuation of Tesco Plc in comparison to other factors as it could be applied

effectively on the earnings of the firm, which is a fair base for its valuation.

2.3 Capital Structure

A. Cost of Debt:

Cost of debt may be defined an effective rate of interest which a company pay to its

debt-holder for providing funds in the form of debt to the company. In calculating the cost of

debt, company calculates such cost after tax and this is so because of payment of interest of debt,

company saves its profits from the taxes (Atrill, McLaney and Harvey, 2014). Hence, for

calculating the net cost of capital which is real cost of raising funds through debt, it is required to

calculate rate of interest after tax. Calculations of cost of convertible debt for absolute company

is as follows:

Given:

Particulars

Interest rate on convertible bond before tax 8.00%

Corporate Tax 19.00%

8% Convertible bonds 750000

premature valuation might be performed due to depreciation (Gitman, Juchau and

Flanagan, 2015).

Dividend Valuation Method: This method determines the overall value of stock, as

displayed above. It's biggest advantage is that it is quite risk-free as well as it removes

subjectivity from equation. However, it is only applied on stocks that pay dividends

within the company, as well as does not undertake non-dividend factors into account.

P/E Ratio: The Price/Earning ratio helps in valuing an organisation by measuring its

current share price relative to its per-share earnings. It is quite an effective method which

allows the company to measure degree of confidence which investors have on firm's

future, which helps the firm in identifying its appropriate value. However, at company

level, it could easily be manipulated, compared to other metrics like dividend and cash

flow. Moreover, it enhances risk as earnings are a single factor used for valuation.

Thus, out of all the methods, P/E Ratio seems to be the best method for the company to

ensure appropriate valuation of Tesco Plc in comparison to other factors as it could be applied

effectively on the earnings of the firm, which is a fair base for its valuation.

2.3 Capital Structure

A. Cost of Debt:

Cost of debt may be defined an effective rate of interest which a company pay to its

debt-holder for providing funds in the form of debt to the company. In calculating the cost of

debt, company calculates such cost after tax and this is so because of payment of interest of debt,

company saves its profits from the taxes (Atrill, McLaney and Harvey, 2014). Hence, for

calculating the net cost of capital which is real cost of raising funds through debt, it is required to

calculate rate of interest after tax. Calculations of cost of convertible debt for absolute company

is as follows:

Given:

Particulars

Interest rate on convertible bond before tax 8.00%

Corporate Tax 19.00%

8% Convertible bonds 750000

Formula: Cost of debt = Interest Expense (1-Tax rate)

Cost of debt (%) = 8%(1 - 0.19)

= 6.48%

Cost of debt (In £) = 750,000* 6.48%

= 48,600

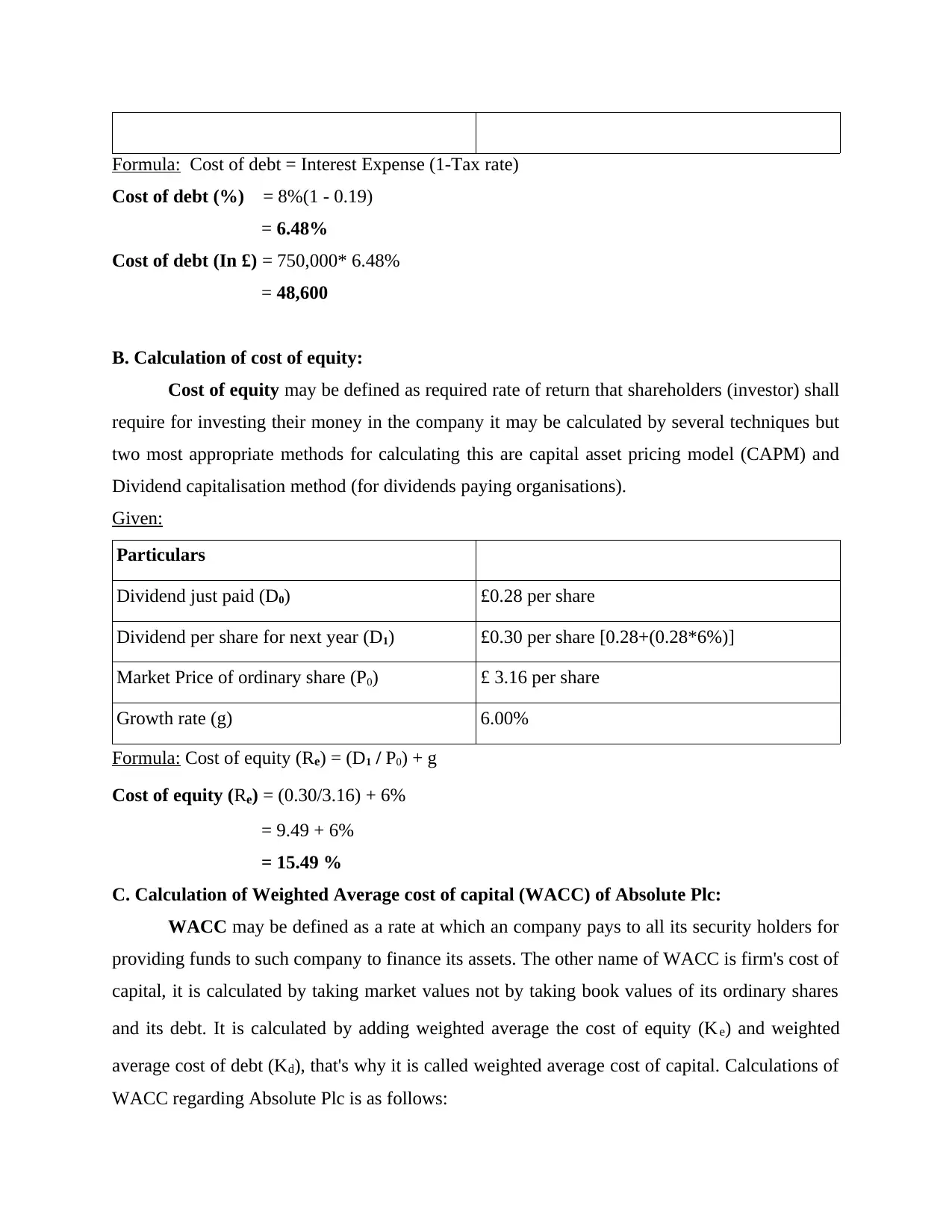

B. Calculation of cost of equity:

Cost of equity may be defined as required rate of return that shareholders (investor) shall

require for investing their money in the company it may be calculated by several techniques but

two most appropriate methods for calculating this are capital asset pricing model (CAPM) and

Dividend capitalisation method (for dividends paying organisations).

Given:

Particulars

Dividend just paid (D0) £0.28 per share

Dividend per share for next year (D1) £0.30 per share [0.28+(0.28*6%)]

Market Price of ordinary share (P0) £ 3.16 per share

Growth rate (g) 6.00%

Formula: Cost of equity (Re) = (D1 / P0) + g

Cost of equity (Re) = (0.30/3.16) + 6%

= 9.49 + 6%

= 15.49 %

C. Calculation of Weighted Average cost of capital (WACC) of Absolute Plc:

WACC may be defined as a rate at which an company pays to all its security holders for

providing funds to such company to finance its assets. The other name of WACC is firm's cost of

capital, it is calculated by taking market values not by taking book values of its ordinary shares

and its debt. It is calculated by adding weighted average the cost of equity (Ke) and weighted

average cost of debt (Kd), that's why it is called weighted average cost of capital. Calculations of

WACC regarding Absolute Plc is as follows:

Cost of debt (%) = 8%(1 - 0.19)

= 6.48%

Cost of debt (In £) = 750,000* 6.48%

= 48,600

B. Calculation of cost of equity:

Cost of equity may be defined as required rate of return that shareholders (investor) shall

require for investing their money in the company it may be calculated by several techniques but

two most appropriate methods for calculating this are capital asset pricing model (CAPM) and

Dividend capitalisation method (for dividends paying organisations).

Given:

Particulars

Dividend just paid (D0) £0.28 per share

Dividend per share for next year (D1) £0.30 per share [0.28+(0.28*6%)]

Market Price of ordinary share (P0) £ 3.16 per share

Growth rate (g) 6.00%

Formula: Cost of equity (Re) = (D1 / P0) + g

Cost of equity (Re) = (0.30/3.16) + 6%

= 9.49 + 6%

= 15.49 %

C. Calculation of Weighted Average cost of capital (WACC) of Absolute Plc:

WACC may be defined as a rate at which an company pays to all its security holders for

providing funds to such company to finance its assets. The other name of WACC is firm's cost of

capital, it is calculated by taking market values not by taking book values of its ordinary shares

and its debt. It is calculated by adding weighted average the cost of equity (Ke) and weighted

average cost of debt (Kd), that's why it is called weighted average cost of capital. Calculations of

WACC regarding Absolute Plc is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.