Investment Analysis for Louis and Larissa

VerifiedAdded on 2020/05/28

|15

|4089

|222

AI Summary

This assignment provides an analysis of suitable investment products for Louis and Larissa, considering their financial goals and risk tolerance. It compares Vanguard and Russell Investments Diversified 50 Fund Class A Units, highlighting the costs, features, and investment objectives of each product. The analysis concludes with a recommendation favoring Vanguard based on its lower costs and alignment with the couple's needs. Additionally, the document explores the concept of gearing in investments and explains how positive gearing can benefit Louis and Larissa.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL PLANNING

Financial Planning

Name of the Student:

Name of the University:

Author’s Note:

Financial Planning

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

FINANCIAL PLANNING

Covering Letter

Louis and Larissa Edberg

Address Line: 22 Curve Street Hill Rise Victoria 3888

Dear Louis and Larissa,

I am highly obliged that you have given me the opportunity to have a meeting with you and

forward with the recommendations that have been framed in accordance to the information

that have been forwarded to me. These data would be helpful in undertaking investments

effectively and the income and the returns that would be received will be helpful in

improving your lifestyle and even life after post retirement.

The Risk Profile answers and the Fact Finder provided during the meeting has been very

helpful in as an effective knowledge about the current goals, objectives and the current

scenario that is existent and the mindset towards security, returns, risks and volatility.

The results that would be gathered can be used for the purpose of framing the SoA. This

report would act as a record that can be taken as an advice by you and your family thereby

would be helpful in attaining the individual circumstances and goals that even includes the

fees, interests and any other costs that have an influence over the advice.

In case there are any transformations in the lifestyle with the advent of time then, additional

advices can be given with the help of which the sustainable lifestyle can be maintained. I

therefore look forward to help you in any other advices and incorporation of the strategies

and the plans and thereby able to provide continuous assistance and services. The services

FINANCIAL PLANNING

Covering Letter

Louis and Larissa Edberg

Address Line: 22 Curve Street Hill Rise Victoria 3888

Dear Louis and Larissa,

I am highly obliged that you have given me the opportunity to have a meeting with you and

forward with the recommendations that have been framed in accordance to the information

that have been forwarded to me. These data would be helpful in undertaking investments

effectively and the income and the returns that would be received will be helpful in

improving your lifestyle and even life after post retirement.

The Risk Profile answers and the Fact Finder provided during the meeting has been very

helpful in as an effective knowledge about the current goals, objectives and the current

scenario that is existent and the mindset towards security, returns, risks and volatility.

The results that would be gathered can be used for the purpose of framing the SoA. This

report would act as a record that can be taken as an advice by you and your family thereby

would be helpful in attaining the individual circumstances and goals that even includes the

fees, interests and any other costs that have an influence over the advice.

In case there are any transformations in the lifestyle with the advent of time then, additional

advices can be given with the help of which the sustainable lifestyle can be maintained. I

therefore look forward to help you in any other advices and incorporation of the strategies

and the plans and thereby able to provide continuous assistance and services. The services

2

FINANCIAL PLANNING

and the recommendations that have been given are in compliance with the requirements of

ASIC.

Regards

John Johnson

Signature

Financial Adviser

FINANCIAL PLANNING

and the recommendations that have been given are in compliance with the requirements of

ASIC.

Regards

John Johnson

Signature

Financial Adviser

3

FINANCIAL PLANNING

Executive Summary

The executive summary is actually a small synopsis that would be provided to the

couple by the financial consultant. The summary is actually the scenario, the goals and

objectives and the strategies that would be suggested thereby able to meet the goals and

objectives. The optimum result for the couple can be projected from the strategy

implementation and technique that has been used. The couple requires understanding and

going through the executive summary and gain effective understanding about the advices that

has been provided and being able to ascertain whether the goals and objectives have been

attained. There is adequate information which would permit the couple to undertake decisions

by observing the risks that are associated to it. The associated fees are even disclosed. The

information that has been provided in jotted down in a clear language with an absence of any

terminology and is suitable to their extent of the financial knowledge.

Personal Situation

By assessing the present condition, Louis and Larissa Edberg are married for a long

tenure and are both 48 years old. They have their home in Victoria and have two dependent

children Michael and Meena. Louis and Larissa have been working full time and earn

significant amount of money Louis has a yearly income of $ 180,000 and on the other hand

his wife Larissa has an annual income of $ 30,000. The couple, each one of them have super

life contribution that have a current value of $300,000 for Louis and $50,000 for Larissa

each. The house they reside in has existing mortgage and they have the idea of repaying their

mortgage before they retire. The couple have a holiday home for themselves where they

reside on family vacations and this holiday home has an existing mortgage as well. The

couple have the idea of using their holiday home for investment purpose if they desire. The

couple are aged 48 years and therefore have nearing the age of retiring and therefore they are

FINANCIAL PLANNING

Executive Summary

The executive summary is actually a small synopsis that would be provided to the

couple by the financial consultant. The summary is actually the scenario, the goals and

objectives and the strategies that would be suggested thereby able to meet the goals and

objectives. The optimum result for the couple can be projected from the strategy

implementation and technique that has been used. The couple requires understanding and

going through the executive summary and gain effective understanding about the advices that

has been provided and being able to ascertain whether the goals and objectives have been

attained. There is adequate information which would permit the couple to undertake decisions

by observing the risks that are associated to it. The associated fees are even disclosed. The

information that has been provided in jotted down in a clear language with an absence of any

terminology and is suitable to their extent of the financial knowledge.

Personal Situation

By assessing the present condition, Louis and Larissa Edberg are married for a long

tenure and are both 48 years old. They have their home in Victoria and have two dependent

children Michael and Meena. Louis and Larissa have been working full time and earn

significant amount of money Louis has a yearly income of $ 180,000 and on the other hand

his wife Larissa has an annual income of $ 30,000. The couple, each one of them have super

life contribution that have a current value of $300,000 for Louis and $50,000 for Larissa

each. The house they reside in has existing mortgage and they have the idea of repaying their

mortgage before they retire. The couple have a holiday home for themselves where they

reside on family vacations and this holiday home has an existing mortgage as well. The

couple have the idea of using their holiday home for investment purpose if they desire. The

couple are aged 48 years and therefore have nearing the age of retiring and therefore they are

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

FINANCIAL PLANNING

looking to undertake investments in the managed funds in order to secure long term capital

growth and income which they can make use of one they retire. This income would be

helpful in maintaining their current lifestyle even after retirement. These are the factors due

to which the couple are seeking advice that would assist them in taking up investments .that

are suitable for them and thereby gain additional income from the same for the purpose of

retirement.

Goals and Objectives

The couple Louis and Larissa like any other couple are looking for long term

generation of income with the help of which they would have a secured future and would not

have to think about wealth once they retire. Risk is a key factor and therefore they are in the

idea of looking into the investments that would provide them with significant amount of

income and the level of risk would be moderate if the income return is able to mitigate the

risk. The couple are in the idea of paying out the mortgage for their house and the holiday

home that they have within the next 5 years. They are even in the idea of constructing wealth

with an idea of getting $200,000 invested in the next 10 years’ time. This amount would be in

terms with the present value of dollar. The couple even have the aim of reducing their level of

taxes wherever possible. They even want to acquire a car for themselves within the next 5

year with the help of the returns that would be attained from the investments. They would

even want to continue their charitable donations till they can and wants to have an

expenditure of $5,000 per annum. Their children are still dependent and therefore want to

save a significant amount of cash that they can make use of for meeting the expenses of their

children. Hence, they want to save money in order to pay for the university fees for their

children who have been projected to $50,000 for each of their children in the time period of

next 10 years and value is estimated in the current term of dollar. Larissa even has the aim of

increasing her income by completing her nursing degree and thereby has estimated that her

FINANCIAL PLANNING

looking to undertake investments in the managed funds in order to secure long term capital

growth and income which they can make use of one they retire. This income would be

helpful in maintaining their current lifestyle even after retirement. These are the factors due

to which the couple are seeking advice that would assist them in taking up investments .that

are suitable for them and thereby gain additional income from the same for the purpose of

retirement.

Goals and Objectives

The couple Louis and Larissa like any other couple are looking for long term

generation of income with the help of which they would have a secured future and would not

have to think about wealth once they retire. Risk is a key factor and therefore they are in the

idea of looking into the investments that would provide them with significant amount of

income and the level of risk would be moderate if the income return is able to mitigate the

risk. The couple are in the idea of paying out the mortgage for their house and the holiday

home that they have within the next 5 years. They are even in the idea of constructing wealth

with an idea of getting $200,000 invested in the next 10 years’ time. This amount would be in

terms with the present value of dollar. The couple even have the aim of reducing their level of

taxes wherever possible. They even want to acquire a car for themselves within the next 5

year with the help of the returns that would be attained from the investments. They would

even want to continue their charitable donations till they can and wants to have an

expenditure of $5,000 per annum. Their children are still dependent and therefore want to

save a significant amount of cash that they can make use of for meeting the expenses of their

children. Hence, they want to save money in order to pay for the university fees for their

children who have been projected to $50,000 for each of their children in the time period of

next 10 years and value is estimated in the current term of dollar. Larissa even has the aim of

increasing her income by completing her nursing degree and thereby has estimated that her

5

FINANCIAL PLANNING

income would get increased to $60,000 per annum. The most significant goal of the couple

has been to make sure that their wishes that have been expressed are fulfilled even after the

pass away. The couple are not in the idea of investing into superannuation and any other

estate planning as the couple have existing superannuation and holiday home and therefore

focus should be given on the investments.

The goals and objectives can be classified in accordance to the short, medium and

long term aspects.

Short Term Objectives

To reduce taxation where possible

To make charitable donations of $5,000 per annum

Medium Term Objectives

To pay off house and holiday home in 5 years.

To acquire a new car every 5 years

Long Term Objectives

To build wealth with a goal of $200,000 invested in 10 years’ time (today’s dollars

terms)

To save to pay for children’s university degrees (estimated at $50,000 each) in 10

years’ time (today’s dollars terms)

To ensure that their wishes are carried out when they pass away

Appropriate Recommendations to meet the goal

FINANCIAL PLANNING

income would get increased to $60,000 per annum. The most significant goal of the couple

has been to make sure that their wishes that have been expressed are fulfilled even after the

pass away. The couple are not in the idea of investing into superannuation and any other

estate planning as the couple have existing superannuation and holiday home and therefore

focus should be given on the investments.

The goals and objectives can be classified in accordance to the short, medium and

long term aspects.

Short Term Objectives

To reduce taxation where possible

To make charitable donations of $5,000 per annum

Medium Term Objectives

To pay off house and holiday home in 5 years.

To acquire a new car every 5 years

Long Term Objectives

To build wealth with a goal of $200,000 invested in 10 years’ time (today’s dollars

terms)

To save to pay for children’s university degrees (estimated at $50,000 each) in 10

years’ time (today’s dollars terms)

To ensure that their wishes are carried out when they pass away

Appropriate Recommendations to meet the goal

6

FINANCIAL PLANNING

There are several recommendations that can be given in accordance to the goals and

objectives that have been highlighted earlier. They are as follows:

Wealth Protection

The protection of debt can be initiated with the knowledge of reducing level of debt

by taking assistive actions and thereby protecting their wealth. The wealth protection can be

undertaken with the help of effective assessment of the portfolio of the investments with

respect to the market which has a tendency to change.

Wealth Accumulation

In order to accumulate wealth, the couple needs to make use of the effective earnings

from their deposits and thereby increasing their income and therefore the client is in need of

investing in funds after maturity in distinct managed fund investments like in shares and

bonds and even in products of managed funds that would invest their money and saves time

of the couple of looking into their investments from time to time.

Estate Planning

The couple have two mortgages out of which one of the mortgage for the house where

they currently reside and another for a holiday home that they have. They want to pay out the

mortgage within 5 years’ time and thereby wants to pay their debt off before retirement. The

couple in order to increase their income can even opt for giving out the holiday home for rent

purpose to visitors as a holiday home with the help of which the couple can earn additional

income. This additional income can be helpful to meet the goals and objectives that have

been discussed earlier.

Projected Results of the Recommendations

FINANCIAL PLANNING

There are several recommendations that can be given in accordance to the goals and

objectives that have been highlighted earlier. They are as follows:

Wealth Protection

The protection of debt can be initiated with the knowledge of reducing level of debt

by taking assistive actions and thereby protecting their wealth. The wealth protection can be

undertaken with the help of effective assessment of the portfolio of the investments with

respect to the market which has a tendency to change.

Wealth Accumulation

In order to accumulate wealth, the couple needs to make use of the effective earnings

from their deposits and thereby increasing their income and therefore the client is in need of

investing in funds after maturity in distinct managed fund investments like in shares and

bonds and even in products of managed funds that would invest their money and saves time

of the couple of looking into their investments from time to time.

Estate Planning

The couple have two mortgages out of which one of the mortgage for the house where

they currently reside and another for a holiday home that they have. They want to pay out the

mortgage within 5 years’ time and thereby wants to pay their debt off before retirement. The

couple in order to increase their income can even opt for giving out the holiday home for rent

purpose to visitors as a holiday home with the help of which the couple can earn additional

income. This additional income can be helpful to meet the goals and objectives that have

been discussed earlier.

Projected Results of the Recommendations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL PLANNING

There are scope of several projections in accordance to the future expenditure that

needs to be regarded like the legislation associated to income tax, the rate of taxes, rate of the

investment returns and the level of inflation so that effective suggestions can be given. The

significant transformations in these components would helpful for reflective effects on the

future strategy and the financial position. It is essential to appreciate the projections and

thereby can act a guideline and the projected outcome may not be assumed with the level of

certainty.

The recommended and the projected outcomes discloses that the development of the

investment portfolio that consists of the several investments in the shares and equities and

also in certain bonds that can lead to the increase in the level of earnings and income that

would improve the financial scenario of the couple. The recommendations are inclusive of

undertaking investments in various bonds and shares so that the risk that is present is

distributed evenly with the help of which the level of income gets increased. There has been

an observation that the couple do not insurance for themselves and therefore should look to

purchase insurances for them in order to mitigate the risk of financial distress in case any

unprecedented things arises and even after death. In case of death, their spouse would receive

financial remuneration and thereby would be able to improve the financial scenario of their

family. Insurance can even be taken for the house and the holiday home with the help of

which these assets can be secured as well. The couple have car of their own and therefore

should look to purchase insurance for their car as well. The couple have the intention of

saving money so that they can pay for the university expenses of their children and therefore

even look to undertake comparison of the various products that are available to them in the

market. The process of comparison would be helpful in understanding the product that is

appropriate for them.

FINANCIAL PLANNING

There are scope of several projections in accordance to the future expenditure that

needs to be regarded like the legislation associated to income tax, the rate of taxes, rate of the

investment returns and the level of inflation so that effective suggestions can be given. The

significant transformations in these components would helpful for reflective effects on the

future strategy and the financial position. It is essential to appreciate the projections and

thereby can act a guideline and the projected outcome may not be assumed with the level of

certainty.

The recommended and the projected outcomes discloses that the development of the

investment portfolio that consists of the several investments in the shares and equities and

also in certain bonds that can lead to the increase in the level of earnings and income that

would improve the financial scenario of the couple. The recommendations are inclusive of

undertaking investments in various bonds and shares so that the risk that is present is

distributed evenly with the help of which the level of income gets increased. There has been

an observation that the couple do not insurance for themselves and therefore should look to

purchase insurances for them in order to mitigate the risk of financial distress in case any

unprecedented things arises and even after death. In case of death, their spouse would receive

financial remuneration and thereby would be able to improve the financial scenario of their

family. Insurance can even be taken for the house and the holiday home with the help of

which these assets can be secured as well. The couple have car of their own and therefore

should look to purchase insurance for their car as well. The couple have the intention of

saving money so that they can pay for the university expenses of their children and therefore

even look to undertake comparison of the various products that are available to them in the

market. The process of comparison would be helpful in understanding the product that is

appropriate for them.

8

FINANCIAL PLANNING

The product disclosure statement and the investment plans need to be assessed by

undertaking a comparison with the past performances of the selected products thereby having

an idea about the present performance of the products and therefore aids in the undertaking of

the investment decisions. The statements are even assessed and compared with the disclosed

reports by the couple and the financial adviser in order to have some knowledge about the

various disclosure statement of the product.

The information that is quantitative in nature that has been gained from the data given

in the statements and thereby several changes that are taking in the economy and the market

so that effective developments can be taken by assistance of the products that would be

recommended to the couple.

Risk Profile

Risks related to investment can be explained as the likelihood and the probability of

the losses that can be incurred in association to the anticipated returns on any specific

investment. It is simply a measure of the extent of the uncertainty of accomplishing the

returns according to the expectations of the investors. It is the level of the unprecedented

results that needs to be realised. Risk has been a key aspect in the evaluation of the prospects

of an investment. Most of the shareholders and the investors while undertaking an investment

look for the kind of investments that have less amount of risks. The lower amount of

investment risks makes the investment much more attractive and lucrative. On the other hand,

the thumb rule has been that increased risks leads to enhanced returns.

The risk profile of the couple have been understood by gaining an idea of the

questions that have been answered by them. The risk profile has been constructed by

considering the investment strategy that is apt in accordance to the distinct circumstances that

has been concluded in the Risk Profile Questionnaire with the help of meaningful and precise

FINANCIAL PLANNING

The product disclosure statement and the investment plans need to be assessed by

undertaking a comparison with the past performances of the selected products thereby having

an idea about the present performance of the products and therefore aids in the undertaking of

the investment decisions. The statements are even assessed and compared with the disclosed

reports by the couple and the financial adviser in order to have some knowledge about the

various disclosure statement of the product.

The information that is quantitative in nature that has been gained from the data given

in the statements and thereby several changes that are taking in the economy and the market

so that effective developments can be taken by assistance of the products that would be

recommended to the couple.

Risk Profile

Risks related to investment can be explained as the likelihood and the probability of

the losses that can be incurred in association to the anticipated returns on any specific

investment. It is simply a measure of the extent of the uncertainty of accomplishing the

returns according to the expectations of the investors. It is the level of the unprecedented

results that needs to be realised. Risk has been a key aspect in the evaluation of the prospects

of an investment. Most of the shareholders and the investors while undertaking an investment

look for the kind of investments that have less amount of risks. The lower amount of

investment risks makes the investment much more attractive and lucrative. On the other hand,

the thumb rule has been that increased risks leads to enhanced returns.

The risk profile of the couple have been understood by gaining an idea of the

questions that have been answered by them. The risk profile has been constructed by

considering the investment strategy that is apt in accordance to the distinct circumstances that

has been concluded in the Risk Profile Questionnaire with the help of meaningful and precise

9

FINANCIAL PLANNING

assessment of the eagerness to accept the risk. The questionnaire that has been given answers

to the experiences, values and attitude. The couple are in the idea of undertaking investments

that would provide long term returns which would be for 5-7 years. The couple are even in

the intention of the being comfortable with this trade off in order to compete with the

inflation. They have significant amount of experience in the investment scenario and

therefore understand the importance of diversification. The most aggressive investments that

they have undertaken is the managed funds. They are very patient as an investor as in case of

decline in the investment portfolio they would be wait for the investment to recover as they

have the intention of long term benefits from the investments. The couple have their focus on

the capital growth and would like to reinvest the income that is generated by them. As their

aim has been to gain significant amount of income after their time of retirement, they are not

in the requirement of liquidity and therefore does not need to maintain easy access to the

funds that have been invested. The comfortable mix of the couple has been that they prefer

prospectively increased returns that would provide optimum saving of tax even though this

would mean increased risk and volatility. The volatility that is existent in the investment

values is acceptable given the increased term of the objectives of the capital growth.

The assessment of the risk profile of the couple has compelled to take the decision

that the couple are balanced investors. They are in the idea of having a balanced portfolio that

would work towards medium to long term financial objectives and therefore require

investment strategy which would cope with the impacts that can take place due to inflation

and tax. The couple accepts calculative risks in order to gain effective amount of returns. The

eagerness to grant the portfolio volatility and their return for the potentiality of the higher

returns. They would even want to generate capital growth and income in accordance to the

timeframe of the investment after paying out for the expenses that have been identified. The

appropriate allocation of the assets involves the allocating their investment in the

FINANCIAL PLANNING

assessment of the eagerness to accept the risk. The questionnaire that has been given answers

to the experiences, values and attitude. The couple are in the idea of undertaking investments

that would provide long term returns which would be for 5-7 years. The couple are even in

the intention of the being comfortable with this trade off in order to compete with the

inflation. They have significant amount of experience in the investment scenario and

therefore understand the importance of diversification. The most aggressive investments that

they have undertaken is the managed funds. They are very patient as an investor as in case of

decline in the investment portfolio they would be wait for the investment to recover as they

have the intention of long term benefits from the investments. The couple have their focus on

the capital growth and would like to reinvest the income that is generated by them. As their

aim has been to gain significant amount of income after their time of retirement, they are not

in the requirement of liquidity and therefore does not need to maintain easy access to the

funds that have been invested. The comfortable mix of the couple has been that they prefer

prospectively increased returns that would provide optimum saving of tax even though this

would mean increased risk and volatility. The volatility that is existent in the investment

values is acceptable given the increased term of the objectives of the capital growth.

The assessment of the risk profile of the couple has compelled to take the decision

that the couple are balanced investors. They are in the idea of having a balanced portfolio that

would work towards medium to long term financial objectives and therefore require

investment strategy which would cope with the impacts that can take place due to inflation

and tax. The couple accepts calculative risks in order to gain effective amount of returns. The

eagerness to grant the portfolio volatility and their return for the potentiality of the higher

returns. They would even want to generate capital growth and income in accordance to the

timeframe of the investment after paying out for the expenses that have been identified. The

appropriate allocation of the assets involves the allocating their investment in the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

FINANCIAL PLANNING

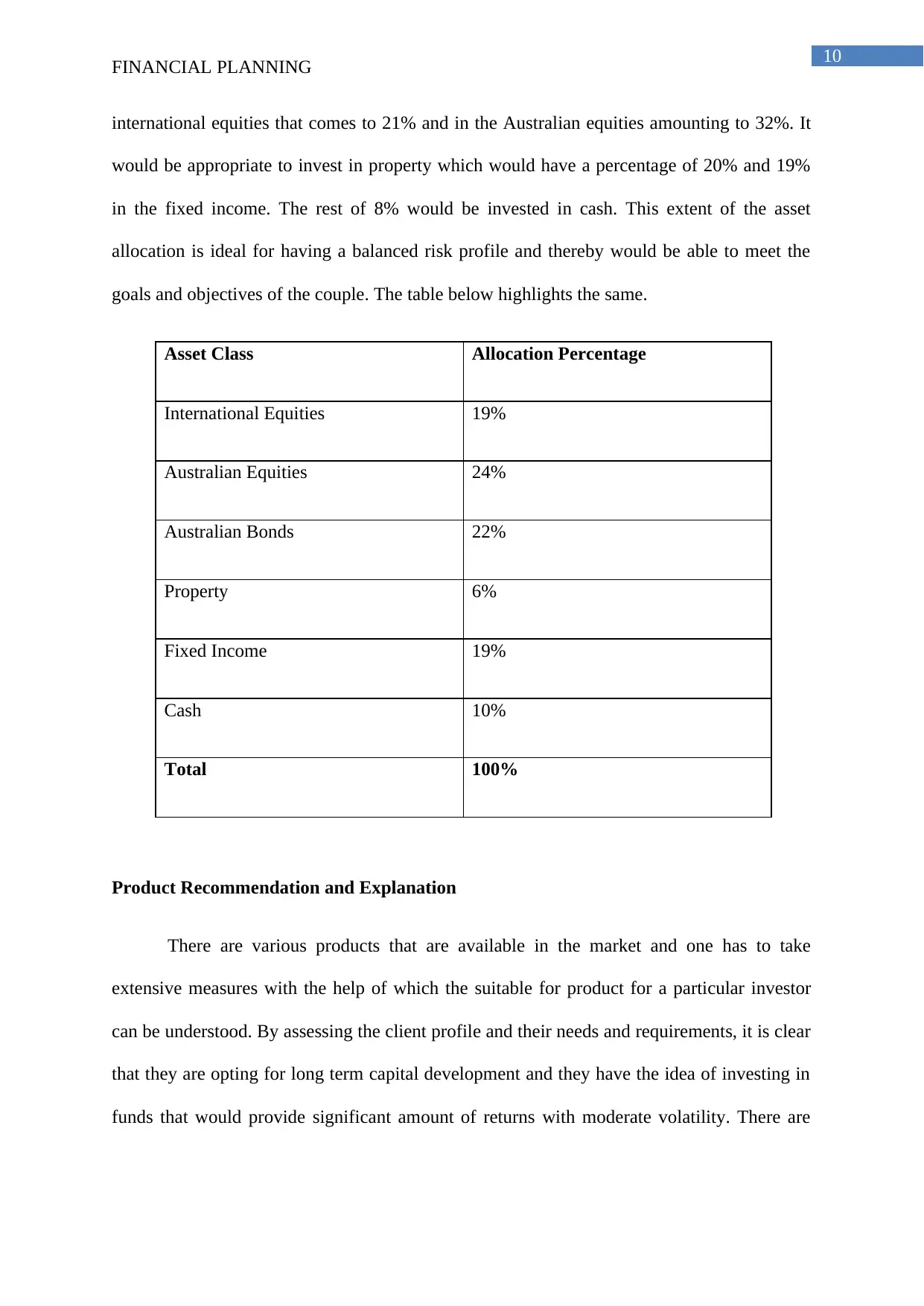

international equities that comes to 21% and in the Australian equities amounting to 32%. It

would be appropriate to invest in property which would have a percentage of 20% and 19%

in the fixed income. The rest of 8% would be invested in cash. This extent of the asset

allocation is ideal for having a balanced risk profile and thereby would be able to meet the

goals and objectives of the couple. The table below highlights the same.

Asset Class Allocation Percentage

International Equities 19%

Australian Equities 24%

Australian Bonds 22%

Property 6%

Fixed Income 19%

Cash 10%

Total 100%

Product Recommendation and Explanation

There are various products that are available in the market and one has to take

extensive measures with the help of which the suitable for product for a particular investor

can be understood. By assessing the client profile and their needs and requirements, it is clear

that they are opting for long term capital development and they have the idea of investing in

funds that would provide significant amount of returns with moderate volatility. There are

FINANCIAL PLANNING

international equities that comes to 21% and in the Australian equities amounting to 32%. It

would be appropriate to invest in property which would have a percentage of 20% and 19%

in the fixed income. The rest of 8% would be invested in cash. This extent of the asset

allocation is ideal for having a balanced risk profile and thereby would be able to meet the

goals and objectives of the couple. The table below highlights the same.

Asset Class Allocation Percentage

International Equities 19%

Australian Equities 24%

Australian Bonds 22%

Property 6%

Fixed Income 19%

Cash 10%

Total 100%

Product Recommendation and Explanation

There are various products that are available in the market and one has to take

extensive measures with the help of which the suitable for product for a particular investor

can be understood. By assessing the client profile and their needs and requirements, it is clear

that they are opting for long term capital development and they have the idea of investing in

funds that would provide significant amount of returns with moderate volatility. There are

11

FINANCIAL PLANNING

two investment products that are recommended to the couple and one has been the Russell

Investment Fund and the other has been Vanguard Investment.

When coming to the factor for investment, it is hard to determine a trend. Therefore

this company has concentrated on developing strategic allocation of the assets by

constructing a framework for the investment strategy that would be suitable for the risk

profile of the investors and thereby giving out a solid base for the investors to attain their

expectations and goals. The company generally invests in long term funds as they have the

idea that markets are volatile and is dependent on the various external factors like the

political, economic and social. Hence, it becomes difficult to understand the market activities

and therefore long term investments are important. The long term investments can be useful

for attaining the goals and objectives of the investor. The company even diversifies their

products and thereby distributing the risks that are existent with investments. The associated

costs are significantly low and have a product disclosure statement that explains the asset

allocation to the customers effectively. The asset allocation is distributed in such a manner,

that changes can be made in accordance to the requirement of the client. The risks that are

associated with the investments have been laid down in an effective manner so that

discrepancies are present in the mind of the customers. There are various products that are

offered by the firm and the one that is suitable for the client can be recommended for

purchase.

Russell Investment Management Ltd on the other hand, is a company that provides

operations in accordance to the operations of the fund in line with the Corporations Act

20011. The product disclosure statement of the product explains the process with the help of

which the funds work by explaining the process of investing and the fees that are associated

with it. The process of withdrawing the investment is even laid down so that the customers

can have an idea about the process and thereby complete their business with the company

FINANCIAL PLANNING

two investment products that are recommended to the couple and one has been the Russell

Investment Fund and the other has been Vanguard Investment.

When coming to the factor for investment, it is hard to determine a trend. Therefore

this company has concentrated on developing strategic allocation of the assets by

constructing a framework for the investment strategy that would be suitable for the risk

profile of the investors and thereby giving out a solid base for the investors to attain their

expectations and goals. The company generally invests in long term funds as they have the

idea that markets are volatile and is dependent on the various external factors like the

political, economic and social. Hence, it becomes difficult to understand the market activities

and therefore long term investments are important. The long term investments can be useful

for attaining the goals and objectives of the investor. The company even diversifies their

products and thereby distributing the risks that are existent with investments. The associated

costs are significantly low and have a product disclosure statement that explains the asset

allocation to the customers effectively. The asset allocation is distributed in such a manner,

that changes can be made in accordance to the requirement of the client. The risks that are

associated with the investments have been laid down in an effective manner so that

discrepancies are present in the mind of the customers. There are various products that are

offered by the firm and the one that is suitable for the client can be recommended for

purchase.

Russell Investment Management Ltd on the other hand, is a company that provides

operations in accordance to the operations of the fund in line with the Corporations Act

20011. The product disclosure statement of the product explains the process with the help of

which the funds work by explaining the process of investing and the fees that are associated

with it. The process of withdrawing the investment is even laid down so that the customers

can have an idea about the process and thereby complete their business with the company

12

FINANCIAL PLANNING

effectively. There can be circumstances where suspension of the transactions can be

understood as such circumstances can arise. The distribution of the funds that would be

undertaken by the firm is laid down to the client. The risk associated with the managed

investment schemes is even explained and thereby the client would be able to understand

their level of returns due to the risk that is associated with the investments. The benefits of

investing in the funds are addressed and their unique selling proposition to the quality of the

ingredients, effective incorporation and management of the multi-asset solutions are

highlighted to the client.

By examining the product that have been offered by the two companies, it is

suggested that investment product of Vanguard is ideal for Louis and Larissa as the goals and

objectives that they have would met by investing in Vanguard’s product. Vanguard Life

Strategy Balanced Fund is ideal for the couple rather than Russell Investments Diversified 50

Fund Class A Units. Vanguard Life Strategy Balanced Fund is actively associated for the

investments that balanced risk profile investors want to undertake. This product effectively

has a strategic allocation of the assets that ranges from 20-24% for Australian shares, 15-19%

from International Shares, 18-22% for Australian fixed interest, Properties within 1-5%.

These are the aspects where the couple wants to undertake investments and therefore this

product is ideally suitable for them. The product being focused on the balanced investors

have the minimum amount of risk with significant amount of stable returns with probabilities

of higher returns when the market is performing exceedingly well. There are certain chances

of the loss of capital but the level of capital growth is significantly higher if the investment is

maintained for a longer time period. The minimum suggested investment frame for this

product is 5 years and this is ideally suited for them. The fees associated with this product is

reasonable as well and this would reduce the investment expense for the couple.

FINANCIAL PLANNING

effectively. There can be circumstances where suspension of the transactions can be

understood as such circumstances can arise. The distribution of the funds that would be

undertaken by the firm is laid down to the client. The risk associated with the managed

investment schemes is even explained and thereby the client would be able to understand

their level of returns due to the risk that is associated with the investments. The benefits of

investing in the funds are addressed and their unique selling proposition to the quality of the

ingredients, effective incorporation and management of the multi-asset solutions are

highlighted to the client.

By examining the product that have been offered by the two companies, it is

suggested that investment product of Vanguard is ideal for Louis and Larissa as the goals and

objectives that they have would met by investing in Vanguard’s product. Vanguard Life

Strategy Balanced Fund is ideal for the couple rather than Russell Investments Diversified 50

Fund Class A Units. Vanguard Life Strategy Balanced Fund is actively associated for the

investments that balanced risk profile investors want to undertake. This product effectively

has a strategic allocation of the assets that ranges from 20-24% for Australian shares, 15-19%

from International Shares, 18-22% for Australian fixed interest, Properties within 1-5%.

These are the aspects where the couple wants to undertake investments and therefore this

product is ideally suitable for them. The product being focused on the balanced investors

have the minimum amount of risk with significant amount of stable returns with probabilities

of higher returns when the market is performing exceedingly well. There are certain chances

of the loss of capital but the level of capital growth is significantly higher if the investment is

maintained for a longer time period. The minimum suggested investment frame for this

product is 5 years and this is ideally suited for them. The fees associated with this product is

reasonable as well and this would reduce the investment expense for the couple.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

FINANCIAL PLANNING

On the other hand, Russell Investments Diversified 50 Fund Class A Units is a good

product as well but there are certain traits that are not ideal for Louis and Larissa. The

associated costs for this product is relatively higher and the asset allocation investment has

been different with respect to the requirement of the client. There is no specific balanced

product that the client can purchase and therefore the risks associated with the product would

be a bit higher than Vanguard. Therefore, Vanguard is suggested for the client.

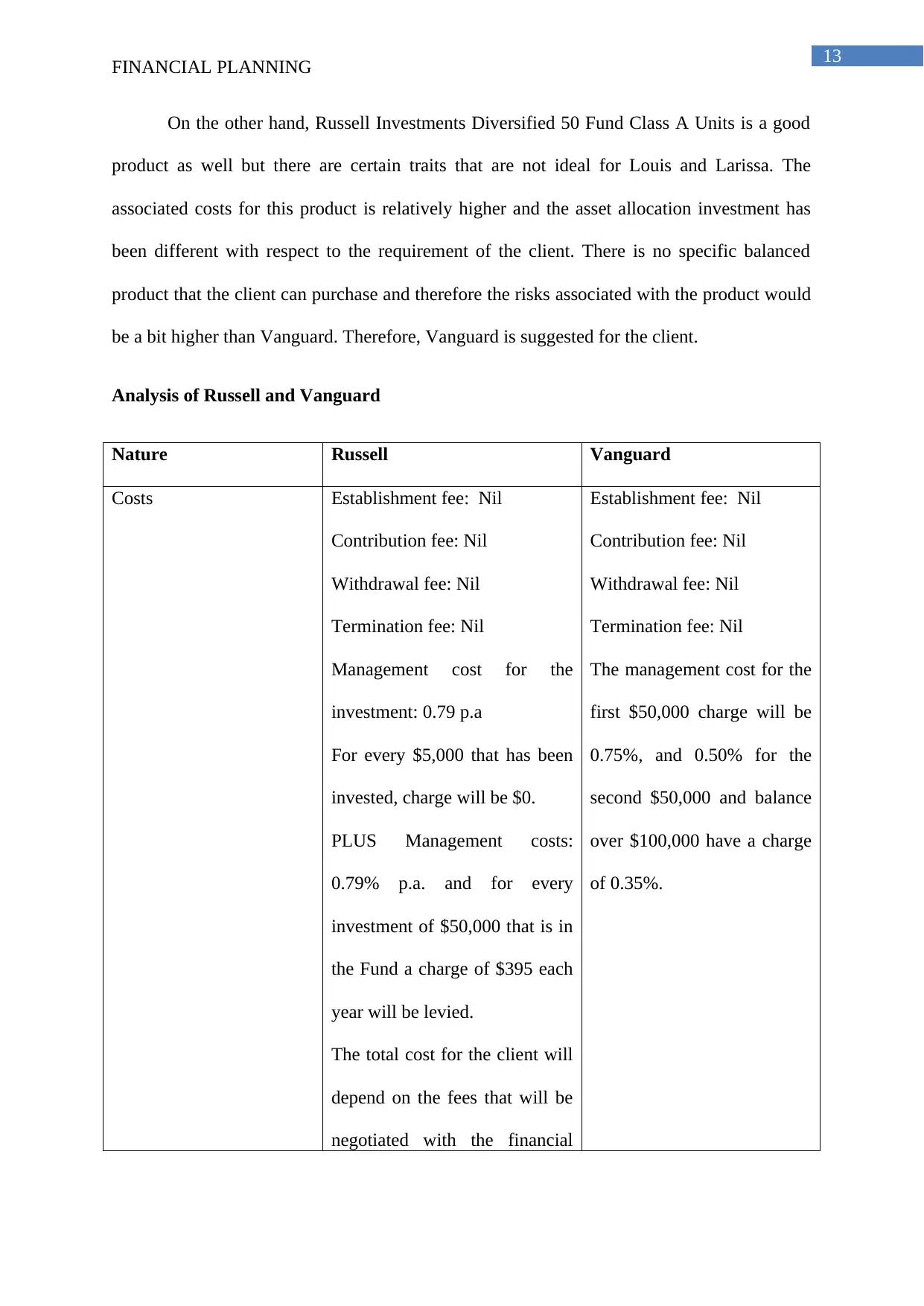

Analysis of Russell and Vanguard

Nature Russell Vanguard

Costs Establishment fee: Nil

Contribution fee: Nil

Withdrawal fee: Nil

Termination fee: Nil

Management cost for the

investment: 0.79 p.a

For every $5,000 that has been

invested, charge will be $0.

PLUS Management costs:

0.79% p.a. and for every

investment of $50,000 that is in

the Fund a charge of $395 each

year will be levied.

The total cost for the client will

depend on the fees that will be

negotiated with the financial

Establishment fee: Nil

Contribution fee: Nil

Withdrawal fee: Nil

Termination fee: Nil

The management cost for the

first $50,000 charge will be

0.75%, and 0.50% for the

second $50,000 and balance

over $100,000 have a charge

of 0.35%.

FINANCIAL PLANNING

On the other hand, Russell Investments Diversified 50 Fund Class A Units is a good

product as well but there are certain traits that are not ideal for Louis and Larissa. The

associated costs for this product is relatively higher and the asset allocation investment has

been different with respect to the requirement of the client. There is no specific balanced

product that the client can purchase and therefore the risks associated with the product would

be a bit higher than Vanguard. Therefore, Vanguard is suggested for the client.

Analysis of Russell and Vanguard

Nature Russell Vanguard

Costs Establishment fee: Nil

Contribution fee: Nil

Withdrawal fee: Nil

Termination fee: Nil

Management cost for the

investment: 0.79 p.a

For every $5,000 that has been

invested, charge will be $0.

PLUS Management costs:

0.79% p.a. and for every

investment of $50,000 that is in

the Fund a charge of $395 each

year will be levied.

The total cost for the client will

depend on the fees that will be

negotiated with the financial

Establishment fee: Nil

Contribution fee: Nil

Withdrawal fee: Nil

Termination fee: Nil

The management cost for the

first $50,000 charge will be

0.75%, and 0.50% for the

second $50,000 and balance

over $100,000 have a charge

of 0.35%.

14

FINANCIAL PLANNING

adviser.

Features Actively managed,

multi-asset solutions

Quality Ingredients

Effective

Implementation

Competitive long

term performance

Diversification

Tax Efficiency

Lost cost of investing

Investment Objectives The investment objective of the

fund involves the development

of the expected returns with

lower amount of risks

Increase invested returns

with diversification of the

investment in various

products and thereby

reducing the level of risk.

Gearing in investments

The process of gearing explains the level of the debt of an investment that is

associated with the equity and is addressed in the form of percentage. It is a measure for the

financial leverage of an investment and explains the extent to which the activities are funded.

Gearing is borrowing to invest and in other terms undertaking investments in the leveraged

assets. It is helpful in transforming the extent of risk in the investment strategy. The risks

associated with gearing involves the risk in the cash, shares, fixed interest and properties. In

accordance to the requirement and objective of the client, there has been an observation that

interest and other costs are lower than the income received from the investment. Therefore,

the couple can undertake positive gearing with the help of which they can claim for

deductions in the taxes for the costs and the interests with respect to the income from

investment. The taxable income would be subjective to income tax at the marginal tax rate.

FINANCIAL PLANNING

adviser.

Features Actively managed,

multi-asset solutions

Quality Ingredients

Effective

Implementation

Competitive long

term performance

Diversification

Tax Efficiency

Lost cost of investing

Investment Objectives The investment objective of the

fund involves the development

of the expected returns with

lower amount of risks

Increase invested returns

with diversification of the

investment in various

products and thereby

reducing the level of risk.

Gearing in investments

The process of gearing explains the level of the debt of an investment that is

associated with the equity and is addressed in the form of percentage. It is a measure for the

financial leverage of an investment and explains the extent to which the activities are funded.

Gearing is borrowing to invest and in other terms undertaking investments in the leveraged

assets. It is helpful in transforming the extent of risk in the investment strategy. The risks

associated with gearing involves the risk in the cash, shares, fixed interest and properties. In

accordance to the requirement and objective of the client, there has been an observation that

interest and other costs are lower than the income received from the investment. Therefore,

the couple can undertake positive gearing with the help of which they can claim for

deductions in the taxes for the costs and the interests with respect to the income from

investment. The taxable income would be subjective to income tax at the marginal tax rate.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.