Analyzing Financial Plans: Budgeting and Cost Management Strategies

VerifiedAdded on 2023/06/13

|9

|1618

|468

Case Study

AI Summary

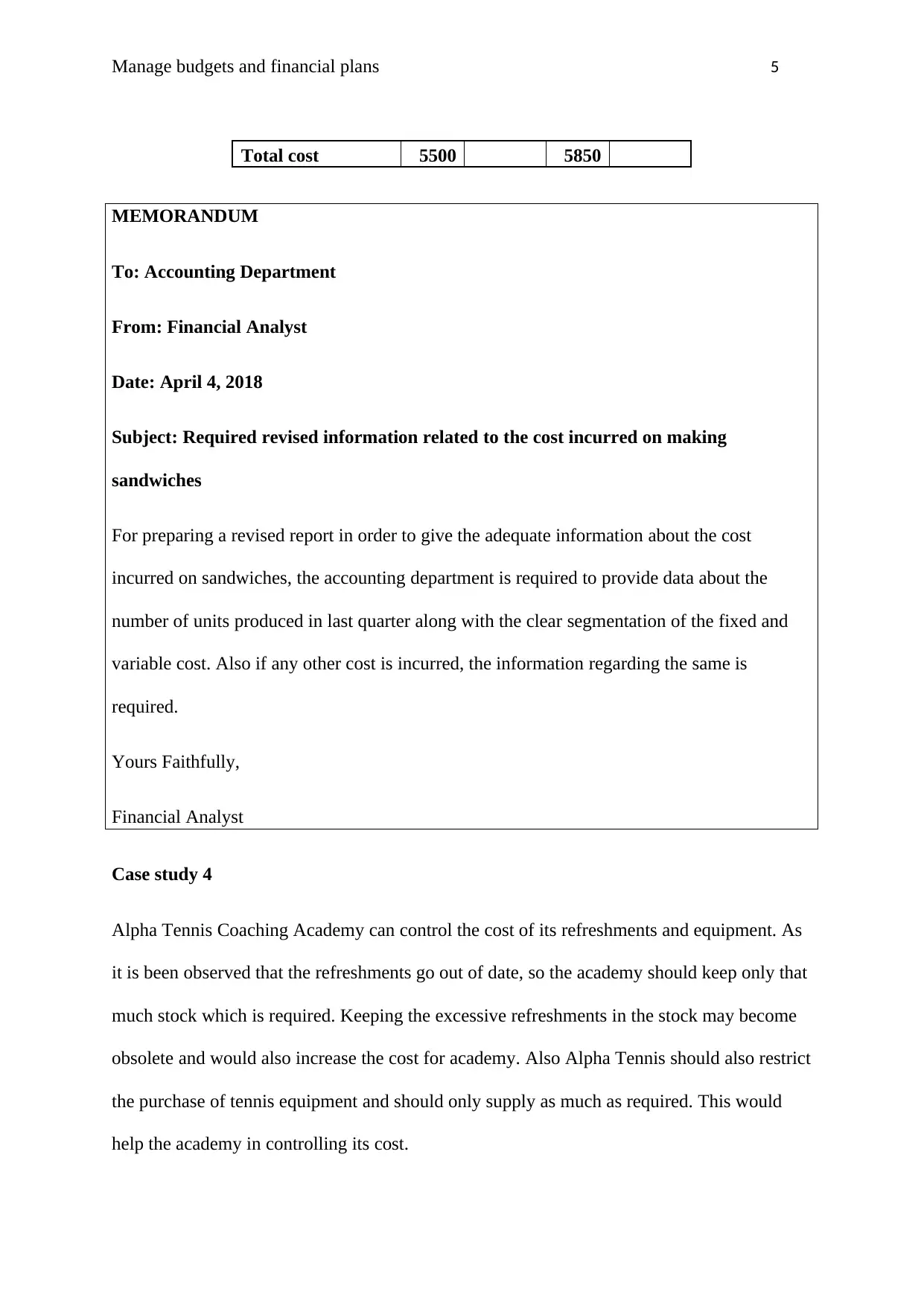

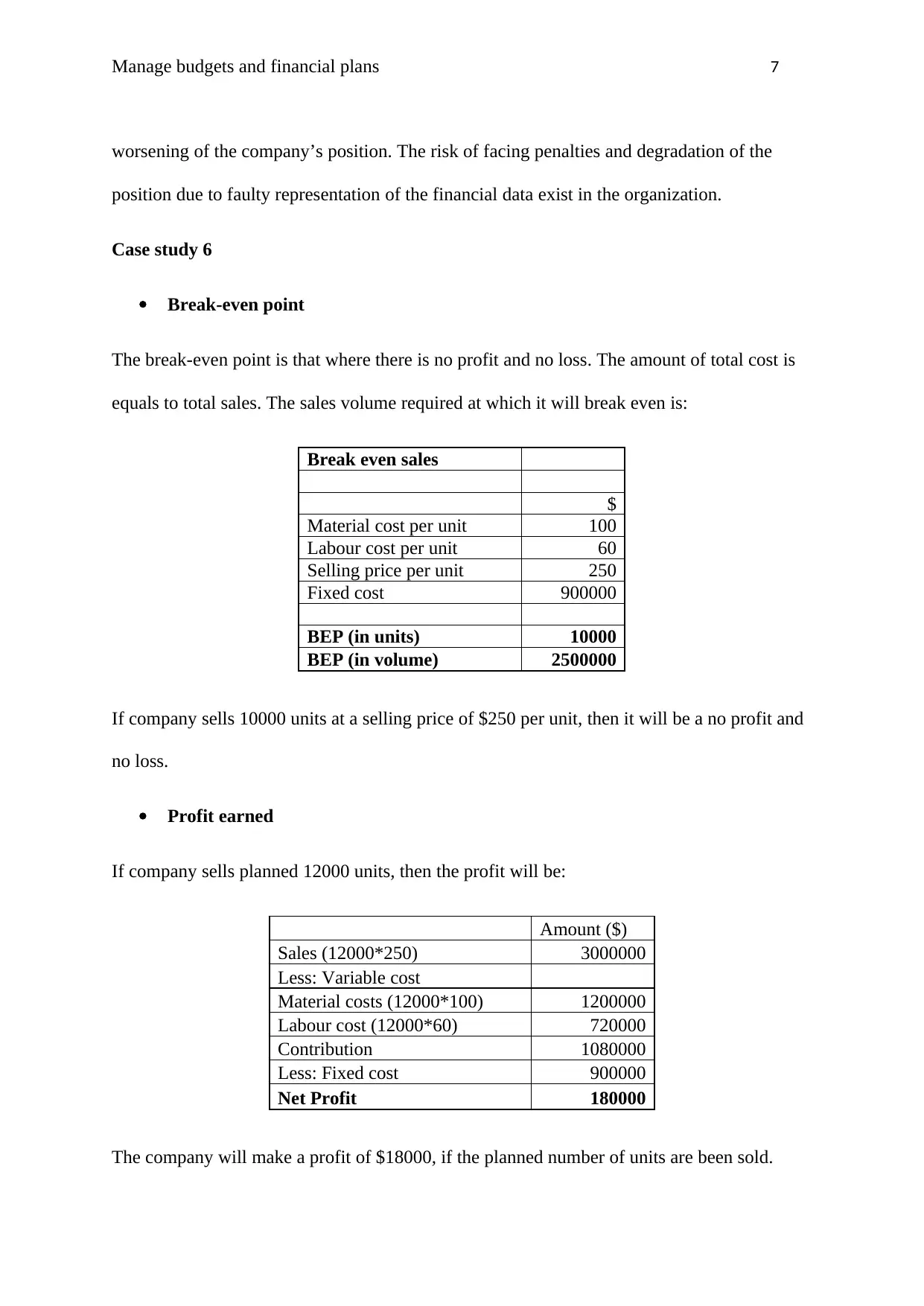

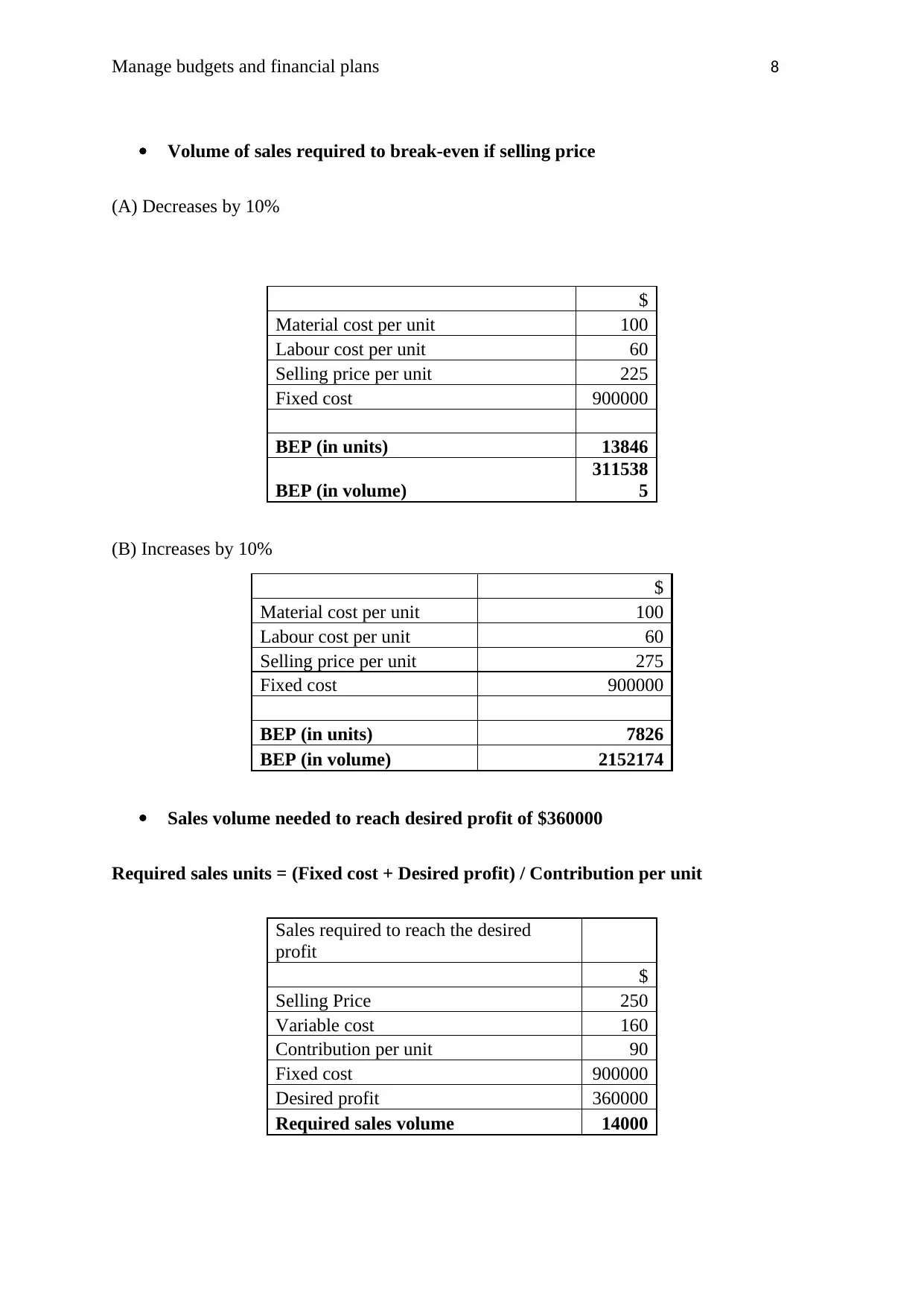

This assignment presents a series of case studies focused on financial planning and cost management. The first case examines a business facing losses and considers the viability of closing a department. The second case involves bifurcating expenses into fixed and variable costs to improve financial reporting and contribution margin analysis. The third case scrutinizes the cost analysis of sandwich production, emphasizing the need for detailed unit cost information and expense categorization. The fourth case discusses cost control strategies for a tennis academy, differentiating between controllable and uncontrollable costs. The fifth case explores the application of International Accounting Standards (IAS) 19 and IAS 2 regarding employee benefits and inventory costing, respectively, highlighting the risks of non-compliance. Finally, the sixth case involves break-even point analysis and profit calculation based on varying sales volumes and pricing scenarios. The analysis provides insights into effective budgeting, financial planning, and cost management strategies, while stressing the importance of accurate financial reporting and compliance with accounting standards. Desklib offers a wealth of resources for students seeking to deepen their understanding of these critical areas.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.