Financial Planning Statement of Advice

VerifiedAdded on 2023/01/13

|23

|4824

|90

AI Summary

This document provides a statement of advice for financial planning, including recommendations for investment in equity and superannuation. It discusses the goals and objectives of the investors, risk profile assessment, and the benefits and risks associated with the advice. Suitable for investors looking to minimize risk and maximize returns.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL PLANNING -

STATEMENT OF ADVICE

STATEMENT OF ADVICE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Compliance......................................................................................................................................1

Scope of advice...........................................................................................................................1

Goal and objectives clearly set out..............................................................................................2

Risk profile assessment and explanation.....................................................................................3

Benefits of advice........................................................................................................................4

Risk associated with advice........................................................................................................6

Suitability of advice for the investor...........................................................................................6

Recommendations............................................................................................................................7

Recommendation appropriate to goal and objectives.................................................................7

Discussion on superannuation.....................................................................................................8

Discussion on investment property.............................................................................................8

Financial projections...................................................................................................................9

Feedback from financial planner...................................................................................................14

SOA...........................................................................................................................................14

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................................21

Table 1Percentage share in the investment avenues........................................................................4

Table 2Projected income statement.................................................................................................9

Table 3Expected return percentage...............................................................................................10

Table 4Annual income on investment...........................................................................................11

Table 5Return on investment.........................................................................................................11

Table 6Projected balance sheet......................................................................................................13

INTRODUCTION...........................................................................................................................1

Compliance......................................................................................................................................1

Scope of advice...........................................................................................................................1

Goal and objectives clearly set out..............................................................................................2

Risk profile assessment and explanation.....................................................................................3

Benefits of advice........................................................................................................................4

Risk associated with advice........................................................................................................6

Suitability of advice for the investor...........................................................................................6

Recommendations............................................................................................................................7

Recommendation appropriate to goal and objectives.................................................................7

Discussion on superannuation.....................................................................................................8

Discussion on investment property.............................................................................................8

Financial projections...................................................................................................................9

Feedback from financial planner...................................................................................................14

SOA...........................................................................................................................................14

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................................21

Table 1Percentage share in the investment avenues........................................................................4

Table 2Projected income statement.................................................................................................9

Table 3Expected return percentage...............................................................................................10

Table 4Annual income on investment...........................................................................................11

Table 5Return on investment.........................................................................................................11

Table 6Projected balance sheet......................................................................................................13

INTRODUCTION

Financial planning is the process of approximation of the capital which is required and determining its competition. The overall file is

based upon the case scenario in which Hamish and Harriet wants to invest the amount in appropriate place. Further, the current report

will describe the scope of advice, goals and objectives which are clearly set for Hamish and Harrirt using SMART tool. Moreover,

study will describe risk profile assessment and explanation and explain why given advice is best for client. Report also recommended

advice related to superannuation and investment on property by defining financial projections. Lastly, report will also prepare and

submit statement of advice and also provide statement of advice that meet all the legal requirements.

Compliance

Scope of advice

Hamish and Harriet intend to make investment in the financial instruments so that their financial needs can be fulfilled and

regular income can be obtained after retirement. Both investors are couple and are moderate risk investor. Thus, they can take medium

risk. Both intend to earn return more than average return but at low risk. Thus, by considering this factor entire investment planning

will be done. As part of scope of advice 60% investment will be made on risky assets and 40% investment will be made on the non-

risky assets (Duffy, 2018). In this regard varied instruments will be taken into account. As part of risky assets equity is taken into

account and along with-it investment will also be made on the exchange traded funds as well as mutual fund schemes that are 60%

equity and 20% debt oriented. On side of safe heaven investment total sum 20% investment will be made in the debt oriented mutual

fund schemes. Thus, it can be said that scope of advice is wide and investment will be made on the multiple securities and by doing so

risk will be minimized and profit will be maximized to the maximum possible extent.

1

Financial planning is the process of approximation of the capital which is required and determining its competition. The overall file is

based upon the case scenario in which Hamish and Harriet wants to invest the amount in appropriate place. Further, the current report

will describe the scope of advice, goals and objectives which are clearly set for Hamish and Harrirt using SMART tool. Moreover,

study will describe risk profile assessment and explanation and explain why given advice is best for client. Report also recommended

advice related to superannuation and investment on property by defining financial projections. Lastly, report will also prepare and

submit statement of advice and also provide statement of advice that meet all the legal requirements.

Compliance

Scope of advice

Hamish and Harriet intend to make investment in the financial instruments so that their financial needs can be fulfilled and

regular income can be obtained after retirement. Both investors are couple and are moderate risk investor. Thus, they can take medium

risk. Both intend to earn return more than average return but at low risk. Thus, by considering this factor entire investment planning

will be done. As part of scope of advice 60% investment will be made on risky assets and 40% investment will be made on the non-

risky assets (Duffy, 2018). In this regard varied instruments will be taken into account. As part of risky assets equity is taken into

account and along with-it investment will also be made on the exchange traded funds as well as mutual fund schemes that are 60%

equity and 20% debt oriented. On side of safe heaven investment total sum 20% investment will be made in the debt oriented mutual

fund schemes. Thus, it can be said that scope of advice is wide and investment will be made on the multiple securities and by doing so

risk will be minimized and profit will be maximized to the maximum possible extent.

1

Goal and objectives clearly set out

On detail interview of Hamish and Harriet it is identified that after making investment in two to five years both wants to make use

of the investment or superannuation funds. Both investors understand the inflation factor which they need to account while preparing

to make investment and due to this reason, their main aim is to make investment on the financial instruments which lead to moderate

risk and good amount of return. Client main objective is to make diversified investment. Client main aim is to earn medium profit and

he do not intend to pull investment back just after facing loss. Client understand that it has to wait for profit for short time period even

he faces loss on investment. SMART objectives are prepared by the most of the business firms and two of its components are given

below. Measurable: It is very important to determine actions that will be taken to achieve target. In this stage financial planner have

to set some of benchmarks against which performance is measured and accordingly step is taken to handle the situation.

Investment will be mad in the equity, mutual funds, exchange traded funds, fixed deposits and superannuation funds. In order

to make objective measurable return on overall portfolio is determined and return on each individual security is also

ascertained. Return on overall portfolio is expected to be 10%. On other hand, return on mutual fund is expected to be 6%.

This is because it will include both debt and equity schemes. Debt schemes of mutual fund generate low return on the

investment amount and equity generate moderate to high return (Fuertes and Gimeno, 2017). However, on mutual fund

investor may earn profit and loss both. Thus, it is expected that return on mutual fund may lie somewhere to 5% to 6%.

Exchange traded funds are another option where investment will be made. ETF will be one which is based on the specific

sector or index and it equity based. Return of 7% is expected on ETF because stock market generates good amount of return

and in case market generate positive return then in that case 7% return may be earned on the equity investment. Investment

will also be made on the bank fixed deposits and property. In most of banks interest rate of 2% is paid by the banks which is

very low and due to this reason by considering investor risk behaviour small amount of investment will be made in the fixed

deposits.

2

On detail interview of Hamish and Harriet it is identified that after making investment in two to five years both wants to make use

of the investment or superannuation funds. Both investors understand the inflation factor which they need to account while preparing

to make investment and due to this reason, their main aim is to make investment on the financial instruments which lead to moderate

risk and good amount of return. Client main objective is to make diversified investment. Client main aim is to earn medium profit and

he do not intend to pull investment back just after facing loss. Client understand that it has to wait for profit for short time period even

he faces loss on investment. SMART objectives are prepared by the most of the business firms and two of its components are given

below. Measurable: It is very important to determine actions that will be taken to achieve target. In this stage financial planner have

to set some of benchmarks against which performance is measured and accordingly step is taken to handle the situation.

Investment will be mad in the equity, mutual funds, exchange traded funds, fixed deposits and superannuation funds. In order

to make objective measurable return on overall portfolio is determined and return on each individual security is also

ascertained. Return on overall portfolio is expected to be 10%. On other hand, return on mutual fund is expected to be 6%.

This is because it will include both debt and equity schemes. Debt schemes of mutual fund generate low return on the

investment amount and equity generate moderate to high return (Fuertes and Gimeno, 2017). However, on mutual fund

investor may earn profit and loss both. Thus, it is expected that return on mutual fund may lie somewhere to 5% to 6%.

Exchange traded funds are another option where investment will be made. ETF will be one which is based on the specific

sector or index and it equity based. Return of 7% is expected on ETF because stock market generates good amount of return

and in case market generate positive return then in that case 7% return may be earned on the equity investment. Investment

will also be made on the bank fixed deposits and property. In most of banks interest rate of 2% is paid by the banks which is

very low and due to this reason by considering investor risk behaviour small amount of investment will be made in the fixed

deposits.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Specific: Main aim of the overall investment is to generate specific percentage of the return for the investor which must be

nearby to 11%. So, that they can get sufficient amount as income post retirement every month from the investment. Investor is

moderate risk taker and due to this reason 40% investment will be made on debt and 60% in equity. By doing so to some

extent capital protection will be ensured which is also matter of concern for the investors. Investors already states that if loss is

observed on investment then in that case they can wait for profit. Thus, considering risk appetite of the investors 40:60 ratio is

followed as investment strategy. Further, in each category whether it is equity or debt multiple investments will be made in the

varied securities so that loss can be minimized and profit can be maximized. Time: Investment will be made for 7 years because after that both will retire and will need additional source of income.

According to allocation of investment up to 7 years like systematic investment plan (SIP) investment will be made in the

financial instruments. So that return can be maximized on the investment amount.

Risk profile assessment and explanation

In order to access player risk profile multiple factors, need to be considered. Level of risk that an individual can take depends on

the financial position of the investor. Hence, in order to determine appropriate risk level for individual it is inevitable to evaluate

assets of the investor. Some of the points that are taken into account to prepare risk profile of the investors are explained below. Residential property: Investors own residential property valued at $5,50,000 if loan is not considered. This indicate investor

financially are strong. Cash and bank deposits: Liquid cash is very low, valued at $14000. Thus, majority of cash is blocked on fixed assets and due

to availability of less cash investor can afford to take moderate risk. Managed fund: Managed fun valued at $85000 which is higher amount and indicate that investor already make investment in

varied securities. Superannuation client and partner: Investment amount is $270000 and $100000.

3

nearby to 11%. So, that they can get sufficient amount as income post retirement every month from the investment. Investor is

moderate risk taker and due to this reason 40% investment will be made on debt and 60% in equity. By doing so to some

extent capital protection will be ensured which is also matter of concern for the investors. Investors already states that if loss is

observed on investment then in that case they can wait for profit. Thus, considering risk appetite of the investors 40:60 ratio is

followed as investment strategy. Further, in each category whether it is equity or debt multiple investments will be made in the

varied securities so that loss can be minimized and profit can be maximized. Time: Investment will be made for 7 years because after that both will retire and will need additional source of income.

According to allocation of investment up to 7 years like systematic investment plan (SIP) investment will be made in the

financial instruments. So that return can be maximized on the investment amount.

Risk profile assessment and explanation

In order to access player risk profile multiple factors, need to be considered. Level of risk that an individual can take depends on

the financial position of the investor. Hence, in order to determine appropriate risk level for individual it is inevitable to evaluate

assets of the investor. Some of the points that are taken into account to prepare risk profile of the investors are explained below. Residential property: Investors own residential property valued at $5,50,000 if loan is not considered. This indicate investor

financially are strong. Cash and bank deposits: Liquid cash is very low, valued at $14000. Thus, majority of cash is blocked on fixed assets and due

to availability of less cash investor can afford to take moderate risk. Managed fund: Managed fun valued at $85000 which is higher amount and indicate that investor already make investment in

varied securities. Superannuation client and partner: Investment amount is $270000 and $100000.

3

All these things that asset value is very high and investor can afford to take medium risk because of less availability of cash.

Otherwise finally investors are very strong. Cumulative income of both on yearly basis is $170000. In two to five years investors are

planning to make use of the superannuation funds. Investors intend to take moderate risk by considering inflation factors. Apart from

this, as mentioned earlier investors already make heavy investment in the multiple securities and due to this reason, they understand

importance of diversification. This is the reason due to which investors are prepared to take moderate risk. They strongly believed that

diversification will minimize risk and required rate of return will be gained by following this strategy.

Investors prefer to make investment in property because its value increase consistently and is safe investment which reflect that

investors are risk conscious and freely would not prefer to take risk on investment.

Thus, on analysis of the overall risk profile of the investors it can be said that financially they are sound and intend to earn

good return at moderate risk.

Benefits of advice

As mentioned earlier that main aim of the investor is to earn good amount of return by taking moderate risk. It is to advisable to

the investors that they must make investment in diversified manner in specific proportion across varied financial instruments so that

loss faced on single security can be covered by the profit gained on other one. Investor also understand this concept. Benefit of this

idea will be that target return will be gained while minimizing risk in the investment.

Table 1Percentage share in the investment avenues

Investment avenues

Percentage

share

Equity 60%

Shares 20%

ETF 20%

4

Otherwise finally investors are very strong. Cumulative income of both on yearly basis is $170000. In two to five years investors are

planning to make use of the superannuation funds. Investors intend to take moderate risk by considering inflation factors. Apart from

this, as mentioned earlier investors already make heavy investment in the multiple securities and due to this reason, they understand

importance of diversification. This is the reason due to which investors are prepared to take moderate risk. They strongly believed that

diversification will minimize risk and required rate of return will be gained by following this strategy.

Investors prefer to make investment in property because its value increase consistently and is safe investment which reflect that

investors are risk conscious and freely would not prefer to take risk on investment.

Thus, on analysis of the overall risk profile of the investors it can be said that financially they are sound and intend to earn

good return at moderate risk.

Benefits of advice

As mentioned earlier that main aim of the investor is to earn good amount of return by taking moderate risk. It is to advisable to

the investors that they must make investment in diversified manner in specific proportion across varied financial instruments so that

loss faced on single security can be covered by the profit gained on other one. Investor also understand this concept. Benefit of this

idea will be that target return will be gained while minimizing risk in the investment.

Table 1Percentage share in the investment avenues

Investment avenues

Percentage

share

Equity 60%

Shares 20%

ETF 20%

4

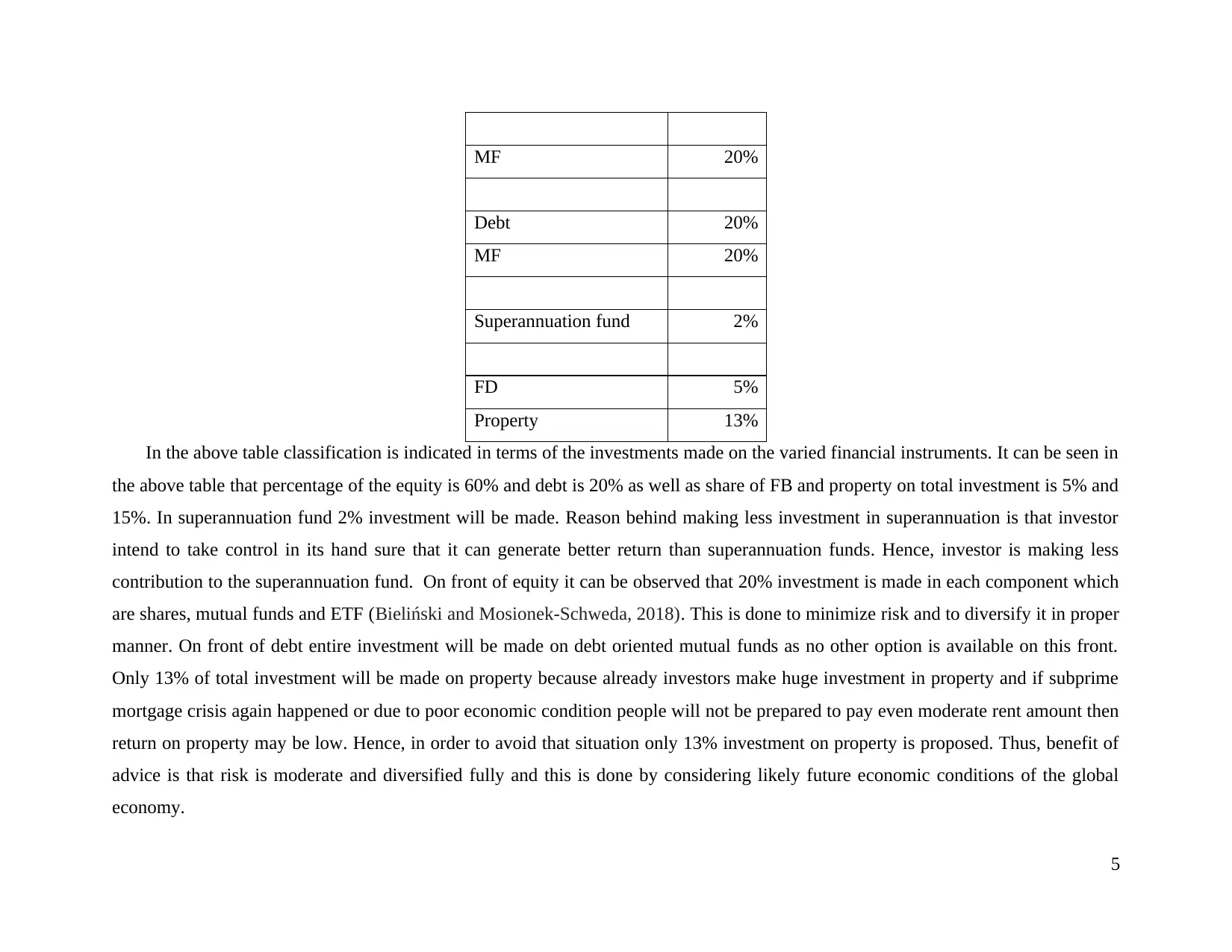

MF 20%

Debt 20%

MF 20%

Superannuation fund 2%

FD 5%

Property 13%

In the above table classification is indicated in terms of the investments made on the varied financial instruments. It can be seen in

the above table that percentage of the equity is 60% and debt is 20% as well as share of FB and property on total investment is 5% and

15%. In superannuation fund 2% investment will be made. Reason behind making less investment in superannuation is that investor

intend to take control in its hand sure that it can generate better return than superannuation funds. Hence, investor is making less

contribution to the superannuation fund. On front of equity it can be observed that 20% investment is made in each component which

are shares, mutual funds and ETF (Bieliński and Mosionek-Schweda, 2018). This is done to minimize risk and to diversify it in proper

manner. On front of debt entire investment will be made on debt oriented mutual funds as no other option is available on this front.

Only 13% of total investment will be made on property because already investors make huge investment in property and if subprime

mortgage crisis again happened or due to poor economic condition people will not be prepared to pay even moderate rent amount then

return on property may be low. Hence, in order to avoid that situation only 13% investment on property is proposed. Thus, benefit of

advice is that risk is moderate and diversified fully and this is done by considering likely future economic conditions of the global

economy.

5

Debt 20%

MF 20%

Superannuation fund 2%

FD 5%

Property 13%

In the above table classification is indicated in terms of the investments made on the varied financial instruments. It can be seen in

the above table that percentage of the equity is 60% and debt is 20% as well as share of FB and property on total investment is 5% and

15%. In superannuation fund 2% investment will be made. Reason behind making less investment in superannuation is that investor

intend to take control in its hand sure that it can generate better return than superannuation funds. Hence, investor is making less

contribution to the superannuation fund. On front of equity it can be observed that 20% investment is made in each component which

are shares, mutual funds and ETF (Bieliński and Mosionek-Schweda, 2018). This is done to minimize risk and to diversify it in proper

manner. On front of debt entire investment will be made on debt oriented mutual funds as no other option is available on this front.

Only 13% of total investment will be made on property because already investors make huge investment in property and if subprime

mortgage crisis again happened or due to poor economic condition people will not be prepared to pay even moderate rent amount then

return on property may be low. Hence, in order to avoid that situation only 13% investment on property is proposed. Thus, benefit of

advice is that risk is moderate and diversified fully and this is done by considering likely future economic conditions of the global

economy.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk associated with advice

Every attempt is made to control risk but still risk is associated with the advice. One of the major risk is that if global economic

conditions will not be good and major global economies will observe decline in their growth rate then in that case stock market will

surely decline. In case such kind of situation stocks, mutual funds and exchange traded funds may give poor performance and

ultimately 60% of overall investment may generate heavy loss to the business. Moreover, demand of property may also decline. Thus,

it is very important to ensure that time to time if required investment percentage is changed. However, if global economic condition

remains good and only problem is observed in the domestic economy then that case small jerks can be observed but overall required

return can be earned. So, if situation remain as discussed return may decline slightly not moderately. These are the one of the major

risk associated with the advice.

Suitability of advice for the investor

Advise is in best interest of client because it intend to earn moderate return by taking less risk. Portfolio managers in order to

minimize risk and to earn moderate return usually make investment in multiple securities so that loss faced on investment can be

covered from the profit gained on other investments. This strategy is same followed in case of current investors. Thus, advice given to

the investor best suits to them. 60% investment is made in equity and 20% in debt as well as 2% in superannuation and 5% in FD as

well as 13% in property. All these instruments or investment avenues risk and return profile is quite different and due to this reason in

same situation all these will react in different manner due to which risk in some securities will be high, medium and low (Acharya and

Ryan, 2016). Ultimately, up to particular level risk will be minimized which will lead to earning of moderate amount of profit on the

invested amount. Thus, in this way risk will be minimized and profit will be moderate. Hence, in this way advice is suitable for the

investors.

6

Every attempt is made to control risk but still risk is associated with the advice. One of the major risk is that if global economic

conditions will not be good and major global economies will observe decline in their growth rate then in that case stock market will

surely decline. In case such kind of situation stocks, mutual funds and exchange traded funds may give poor performance and

ultimately 60% of overall investment may generate heavy loss to the business. Moreover, demand of property may also decline. Thus,

it is very important to ensure that time to time if required investment percentage is changed. However, if global economic condition

remains good and only problem is observed in the domestic economy then that case small jerks can be observed but overall required

return can be earned. So, if situation remain as discussed return may decline slightly not moderately. These are the one of the major

risk associated with the advice.

Suitability of advice for the investor

Advise is in best interest of client because it intend to earn moderate return by taking less risk. Portfolio managers in order to

minimize risk and to earn moderate return usually make investment in multiple securities so that loss faced on investment can be

covered from the profit gained on other investments. This strategy is same followed in case of current investors. Thus, advice given to

the investor best suits to them. 60% investment is made in equity and 20% in debt as well as 2% in superannuation and 5% in FD as

well as 13% in property. All these instruments or investment avenues risk and return profile is quite different and due to this reason in

same situation all these will react in different manner due to which risk in some securities will be high, medium and low (Acharya and

Ryan, 2016). Ultimately, up to particular level risk will be minimized which will lead to earning of moderate amount of profit on the

invested amount. Thus, in this way risk will be minimized and profit will be moderate. Hence, in this way advice is suitable for the

investors.

6

Recommendations

Recommendation appropriate to goal and objectives

As Hamish and Harriet make an investment in their financial instrument, that is why, it is recommended to them to invest their

amount in equity and superannuation. It so because they are medium risk taker and if they get good amount of return from equity then

it is consider another additional source of income after their retirement. Further, it is also recommended to both that if they invest the

amount in superannuation then it will be more beneficial for them because when they get any loss from equity then they have another

income source option. Therefore, it is analyzed that investing in these two will be more beneficial and also, helps to minimize the risk

level.

The main goal of Hamish and Harriet is to invest the amount in superannuation because that amount will be converted into

pension and this will be further help them in their any emergency situation. On the other hand, their main aim is to generate specific

percentage of return for the investor which is near by 11%. it is so because they will get sufficient income as their post retirement.

Hence, it is recommended to Hamish and Harriet to invest the amount in superannuation because it Is tax effective saving method and

it is actually designed for the people to become self- sufficient when they retire (Cummings, 2016). Or else, investing less amount on

superannuation will help to generate better results and this in turn provide better income even after their retirement.

Overall, it is analyzed that investing the amount in multiple securities will help to manage risk and also earn moderate return. It

is so because loss faced on investment can be easily covered from profit gained from the other investment. Therefore, further, it is

recommended to both Hamish and Harriet that they may also invest some amount on residential property because it will help to gain

good amount in near future because amount on property will definitely increases in near future. Though there are many risk associated

with it but investing good amount in equity i.e. 60%, superannuation i.e. 2% and 13% on investment. So that when the amount is

invested in this will be more beneficial, as they are low risk taker and If due to poor economic condition, they face any loss then they

have another option of income which will definitely support them. In this way, they will easily meet with their aim and objectives.

7

Recommendation appropriate to goal and objectives

As Hamish and Harriet make an investment in their financial instrument, that is why, it is recommended to them to invest their

amount in equity and superannuation. It so because they are medium risk taker and if they get good amount of return from equity then

it is consider another additional source of income after their retirement. Further, it is also recommended to both that if they invest the

amount in superannuation then it will be more beneficial for them because when they get any loss from equity then they have another

income source option. Therefore, it is analyzed that investing in these two will be more beneficial and also, helps to minimize the risk

level.

The main goal of Hamish and Harriet is to invest the amount in superannuation because that amount will be converted into

pension and this will be further help them in their any emergency situation. On the other hand, their main aim is to generate specific

percentage of return for the investor which is near by 11%. it is so because they will get sufficient income as their post retirement.

Hence, it is recommended to Hamish and Harriet to invest the amount in superannuation because it Is tax effective saving method and

it is actually designed for the people to become self- sufficient when they retire (Cummings, 2016). Or else, investing less amount on

superannuation will help to generate better results and this in turn provide better income even after their retirement.

Overall, it is analyzed that investing the amount in multiple securities will help to manage risk and also earn moderate return. It

is so because loss faced on investment can be easily covered from profit gained from the other investment. Therefore, further, it is

recommended to both Hamish and Harriet that they may also invest some amount on residential property because it will help to gain

good amount in near future because amount on property will definitely increases in near future. Though there are many risk associated

with it but investing good amount in equity i.e. 60%, superannuation i.e. 2% and 13% on investment. So that when the amount is

invested in this will be more beneficial, as they are low risk taker and If due to poor economic condition, they face any loss then they

have another option of income which will definitely support them. In this way, they will easily meet with their aim and objectives.

7

Discussion on superannuation

Superannuation is consider one of the best way for Australians to save money for their retirement such that employer should

have to pay 9.5% of their salary into super fund. Further, this money is also deposited into superannuation account which is further

invested and the growth is also reinvested in order to balance grow. In the same way, as per the case scenario it is better for Hamish

and Harriet to invest $2 lac 70 thousand in superannuation because when super fund started paying an allocated pension then, there is

no tax on capital gains or income. Such that if before the age of 60, retirement starts, then super funds will be responsible for the tax of

around 15% of the assessable amount (Bui, Sarath and Ahmed, 2016).

Moreover, while investing 2% into such amount will be more beneficial because it also helps to protect from bankruptcy. Such

that in future when someone have claim on both Hamish and Harriet, at that time, super benefits will be protected up to Reasonable

Benefit Limit of individual's pension. Therefore, this also allow business owners and individuals to protect their assets otherwise it

may be seized by creditors at the time of bankruptcy. Therefore, it also reflected that when investor chooses this option then it will

help to get more better value in near future.

It is also reflected that it is recommended to Hamish and Harriet that invest the amount on superannuation because it make

sure that money goes where the investor want and thus it turn to pay less amount on the investment ( Kingston and Thorp, 2019).

Therefore, it is analyzed that investing into superannuation will leads to cheaper insurance cover in many cases and also assist to

enhance their overall income. Moreover, when investor invest some amount in superannuation, then it will assist to use that money in

emergency situation such that they may also withdraw amount whenever find any financial hardship. This in turn, help them to

overcome any financial issues as well.

Discussion on investment property

It is also recommended to Hamish and Harriet, to invest in property and it is recommended them to invest around 13% of the

total amount because it is analyzed that investing in this will help to generate more income in near future. Such that both Hamish and

Harriet, may invest in refurbishment of their residential property and then also charge high amount of rate as well (Mackenzie, 2017).

8

Superannuation is consider one of the best way for Australians to save money for their retirement such that employer should

have to pay 9.5% of their salary into super fund. Further, this money is also deposited into superannuation account which is further

invested and the growth is also reinvested in order to balance grow. In the same way, as per the case scenario it is better for Hamish

and Harriet to invest $2 lac 70 thousand in superannuation because when super fund started paying an allocated pension then, there is

no tax on capital gains or income. Such that if before the age of 60, retirement starts, then super funds will be responsible for the tax of

around 15% of the assessable amount (Bui, Sarath and Ahmed, 2016).

Moreover, while investing 2% into such amount will be more beneficial because it also helps to protect from bankruptcy. Such

that in future when someone have claim on both Hamish and Harriet, at that time, super benefits will be protected up to Reasonable

Benefit Limit of individual's pension. Therefore, this also allow business owners and individuals to protect their assets otherwise it

may be seized by creditors at the time of bankruptcy. Therefore, it also reflected that when investor chooses this option then it will

help to get more better value in near future.

It is also reflected that it is recommended to Hamish and Harriet that invest the amount on superannuation because it make

sure that money goes where the investor want and thus it turn to pay less amount on the investment ( Kingston and Thorp, 2019).

Therefore, it is analyzed that investing into superannuation will leads to cheaper insurance cover in many cases and also assist to

enhance their overall income. Moreover, when investor invest some amount in superannuation, then it will assist to use that money in

emergency situation such that they may also withdraw amount whenever find any financial hardship. This in turn, help them to

overcome any financial issues as well.

Discussion on investment property

It is also recommended to Hamish and Harriet, to invest in property and it is recommended them to invest around 13% of the

total amount because it is analyzed that investing in this will help to generate more income in near future. Such that both Hamish and

Harriet, may invest in refurbishment of their residential property and then also charge high amount of rate as well (Mackenzie, 2017).

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

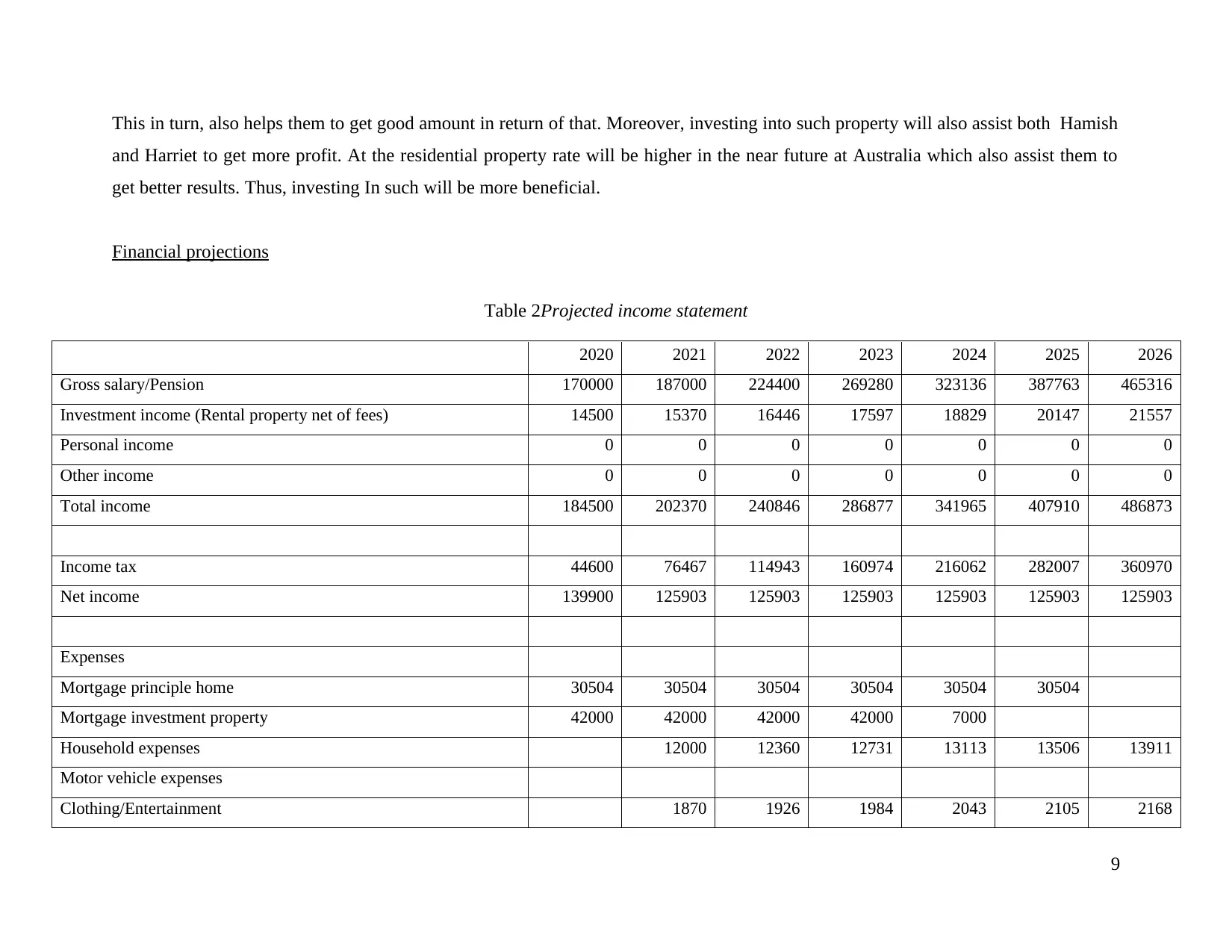

This in turn, also helps them to get good amount in return of that. Moreover, investing into such property will also assist both Hamish

and Harriet to get more profit. At the residential property rate will be higher in the near future at Australia which also assist them to

get better results. Thus, investing In such will be more beneficial.

Financial projections

Table 2Projected income statement

2020 2021 2022 2023 2024 2025 2026

Gross salary/Pension 170000 187000 224400 269280 323136 387763 465316

Investment income (Rental property net of fees) 14500 15370 16446 17597 18829 20147 21557

Personal income 0 0 0 0 0 0 0

Other income 0 0 0 0 0 0 0

Total income 184500 202370 240846 286877 341965 407910 486873

Income tax 44600 76467 114943 160974 216062 282007 360970

Net income 139900 125903 125903 125903 125903 125903 125903

Expenses

Mortgage principle home 30504 30504 30504 30504 30504 30504

Mortgage investment property 42000 42000 42000 42000 7000

Household expenses 12000 12360 12731 13113 13506 13911

Motor vehicle expenses

Clothing/Entertainment 1870 1926 1984 2043 2105 2168

9

and Harriet to get more profit. At the residential property rate will be higher in the near future at Australia which also assist them to

get better results. Thus, investing In such will be more beneficial.

Financial projections

Table 2Projected income statement

2020 2021 2022 2023 2024 2025 2026

Gross salary/Pension 170000 187000 224400 269280 323136 387763 465316

Investment income (Rental property net of fees) 14500 15370 16446 17597 18829 20147 21557

Personal income 0 0 0 0 0 0 0

Other income 0 0 0 0 0 0 0

Total income 184500 202370 240846 286877 341965 407910 486873

Income tax 44600 76467 114943 160974 216062 282007 360970

Net income 139900 125903 125903 125903 125903 125903 125903

Expenses

Mortgage principle home 30504 30504 30504 30504 30504 30504

Mortgage investment property 42000 42000 42000 42000 7000

Household expenses 12000 12360 12731 13113 13506 13911

Motor vehicle expenses

Clothing/Entertainment 1870 1926 1984 2043 2105 2168

9

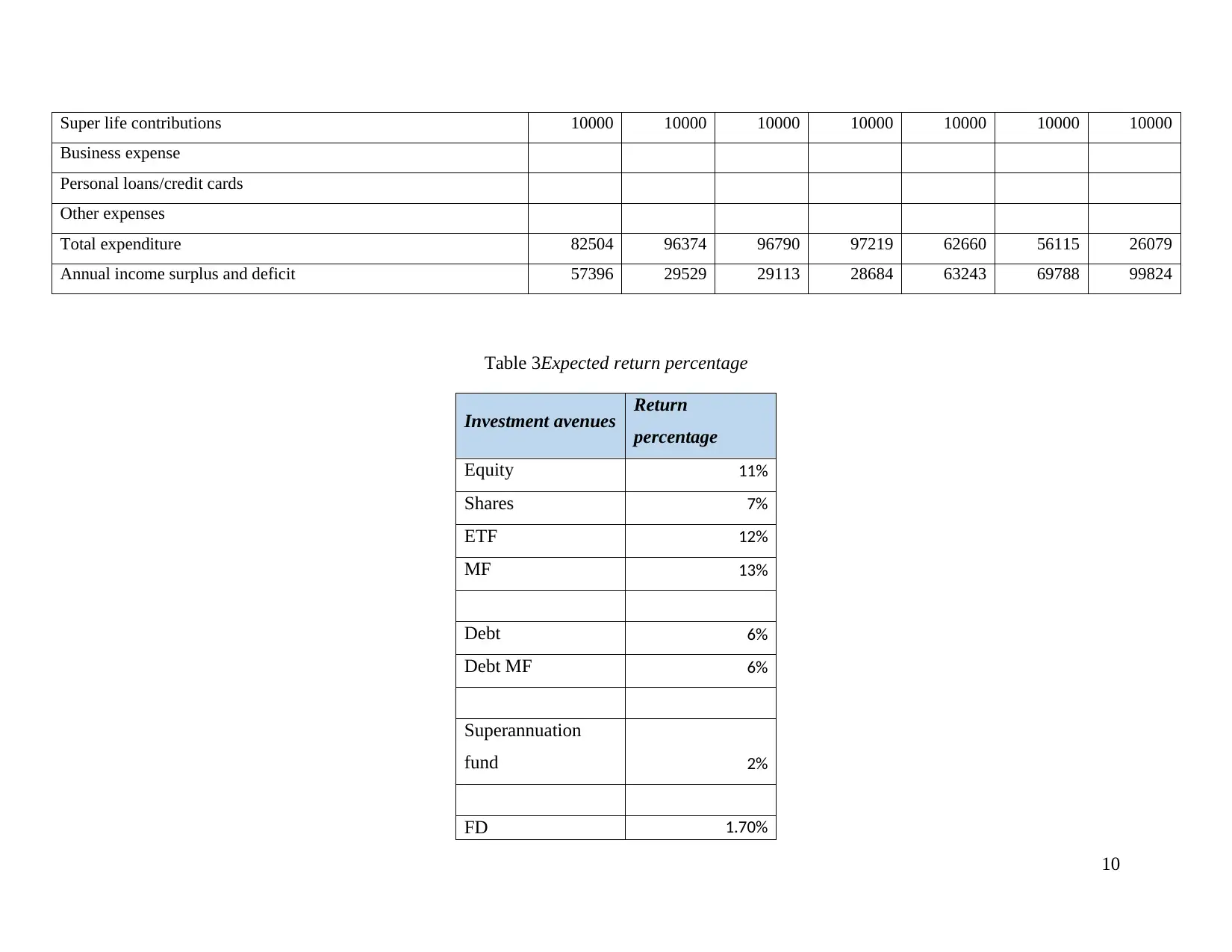

Super life contributions 10000 10000 10000 10000 10000 10000 10000

Business expense

Personal loans/credit cards

Other expenses

Total expenditure 82504 96374 96790 97219 62660 56115 26079

Annual income surplus and deficit 57396 29529 29113 28684 63243 69788 99824

Table 3Expected return percentage

Investment avenues Return

percentage

Equity 11%

Shares 7%

ETF 12%

MF 13%

Debt 6%

Debt MF 6%

Superannuation

fund 2%

FD 1.70%

10

Business expense

Personal loans/credit cards

Other expenses

Total expenditure 82504 96374 96790 97219 62660 56115 26079

Annual income surplus and deficit 57396 29529 29113 28684 63243 69788 99824

Table 3Expected return percentage

Investment avenues Return

percentage

Equity 11%

Shares 7%

ETF 12%

MF 13%

Debt 6%

Debt MF 6%

Superannuation

fund 2%

FD 1.70%

10

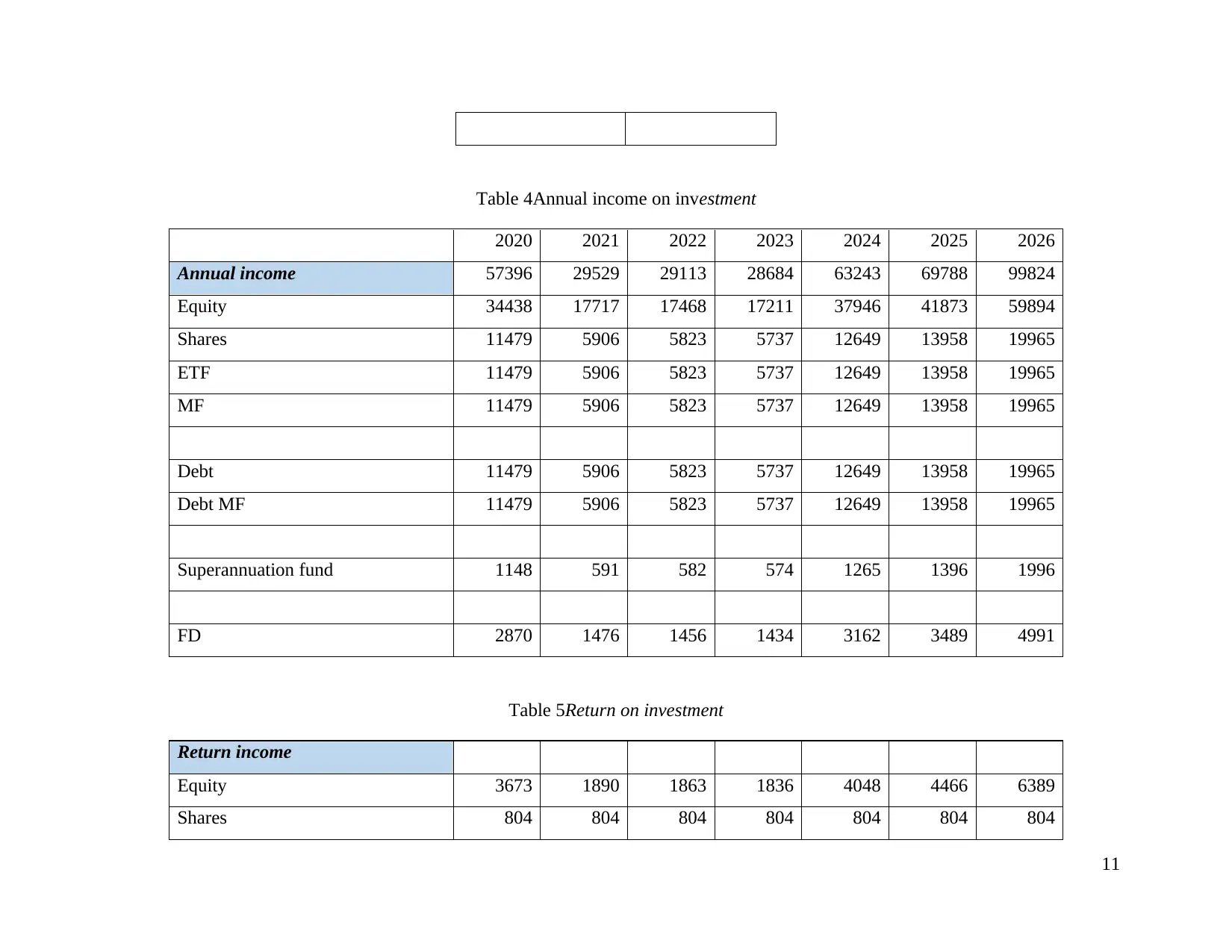

Table 4Annual income on investment

2020 2021 2022 2023 2024 2025 2026

Annual income 57396 29529 29113 28684 63243 69788 99824

Equity 34438 17717 17468 17211 37946 41873 59894

Shares 11479 5906 5823 5737 12649 13958 19965

ETF 11479 5906 5823 5737 12649 13958 19965

MF 11479 5906 5823 5737 12649 13958 19965

Debt 11479 5906 5823 5737 12649 13958 19965

Debt MF 11479 5906 5823 5737 12649 13958 19965

Superannuation fund 1148 591 582 574 1265 1396 1996

FD 2870 1476 1456 1434 3162 3489 4991

Table 5Return on investment

Return income

Equity 3673 1890 1863 1836 4048 4466 6389

Shares 804 804 804 804 804 804 804

11

2020 2021 2022 2023 2024 2025 2026

Annual income 57396 29529 29113 28684 63243 69788 99824

Equity 34438 17717 17468 17211 37946 41873 59894

Shares 11479 5906 5823 5737 12649 13958 19965

ETF 11479 5906 5823 5737 12649 13958 19965

MF 11479 5906 5823 5737 12649 13958 19965

Debt 11479 5906 5823 5737 12649 13958 19965

Debt MF 11479 5906 5823 5737 12649 13958 19965

Superannuation fund 1148 591 582 574 1265 1396 1996

FD 2870 1476 1456 1434 3162 3489 4991

Table 5Return on investment

Return income

Equity 3673 1890 1863 1836 4048 4466 6389

Shares 804 804 804 804 804 804 804

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ETF 1378 709 699 688 1518 1675 2595

MF 1492 768 757 746 1644 1814 2595

Debt 689 354 349 344 759 837 1198

Debt MF 689 354 349 344 759 837 1198

Superannuation fund 23 12 12 11 25 28 40

FD 49 25 25 24 54 59 85

Return total 4434 2281 2249 2216 4886 5391 7711

12

MF 1492 768 757 746 1644 1814 2595

Debt 689 354 349 344 759 837 1198

Debt MF 689 354 349 344 759 837 1198

Superannuation fund 23 12 12 11 25 28 40

FD 49 25 25 24 54 59 85

Return total 4434 2281 2249 2216 4886 5391 7711

12

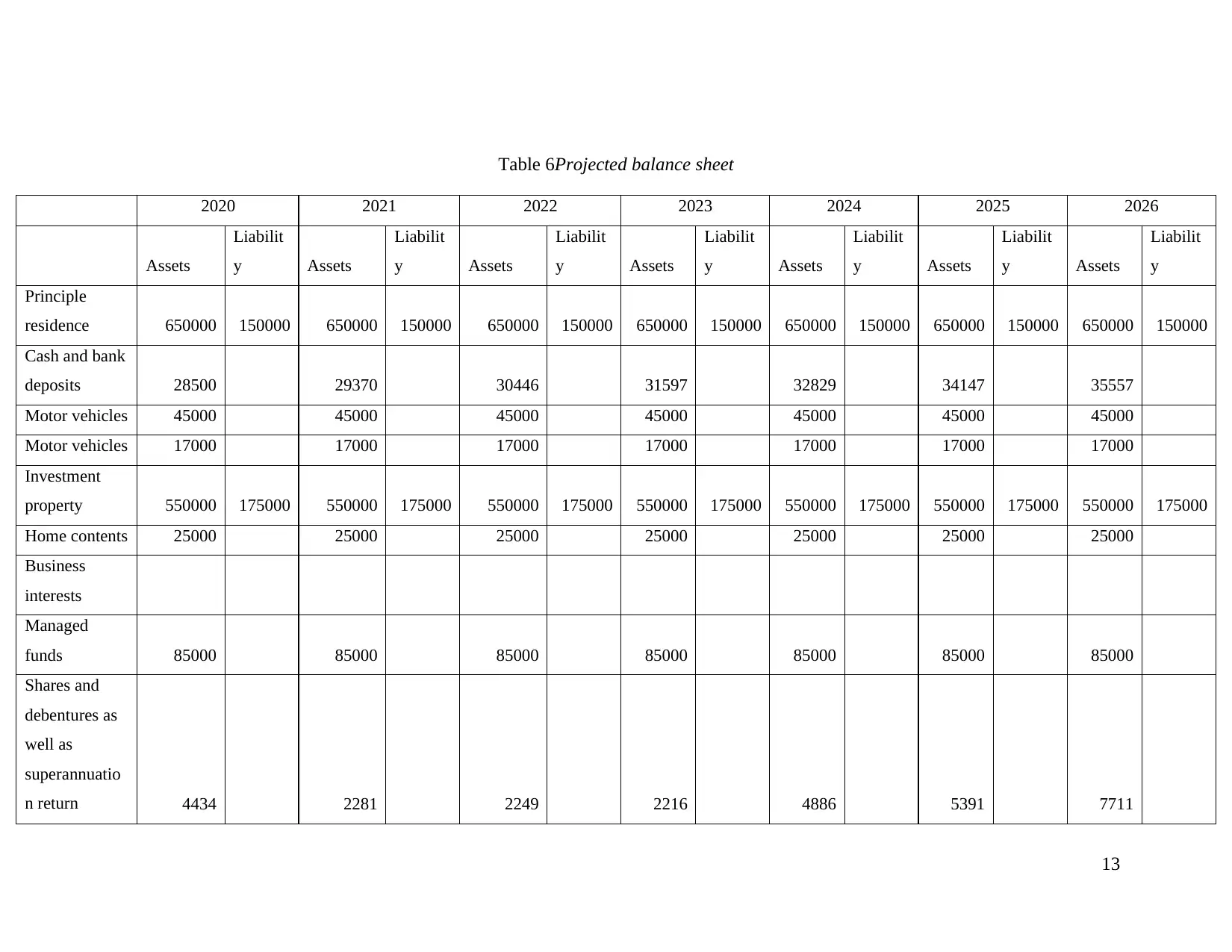

Table 6Projected balance sheet

2020 2021 2022 2023 2024 2025 2026

Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y

Principle

residence 650000 150000 650000 150000 650000 150000 650000 150000 650000 150000 650000 150000 650000 150000

Cash and bank

deposits 28500 29370 30446 31597 32829 34147 35557

Motor vehicles 45000 45000 45000 45000 45000 45000 45000

Motor vehicles 17000 17000 17000 17000 17000 17000 17000

Investment

property 550000 175000 550000 175000 550000 175000 550000 175000 550000 175000 550000 175000 550000 175000

Home contents 25000 25000 25000 25000 25000 25000 25000

Business

interests

Managed

funds 85000 85000 85000 85000 85000 85000 85000

Shares and

debentures as

well as

superannuatio

n return 4434 2281 2249 2216 4886 5391 7711

13

2020 2021 2022 2023 2024 2025 2026

Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y Assets

Liabilit

y

Principle

residence 650000 150000 650000 150000 650000 150000 650000 150000 650000 150000 650000 150000 650000 150000

Cash and bank

deposits 28500 29370 30446 31597 32829 34147 35557

Motor vehicles 45000 45000 45000 45000 45000 45000 45000

Motor vehicles 17000 17000 17000 17000 17000 17000 17000

Investment

property 550000 175000 550000 175000 550000 175000 550000 175000 550000 175000 550000 175000 550000 175000

Home contents 25000 25000 25000 25000 25000 25000 25000

Business

interests

Managed

funds 85000 85000 85000 85000 85000 85000 85000

Shares and

debentures as

well as

superannuatio

n return 4434 2281 2249 2216 4886 5391 7711

13

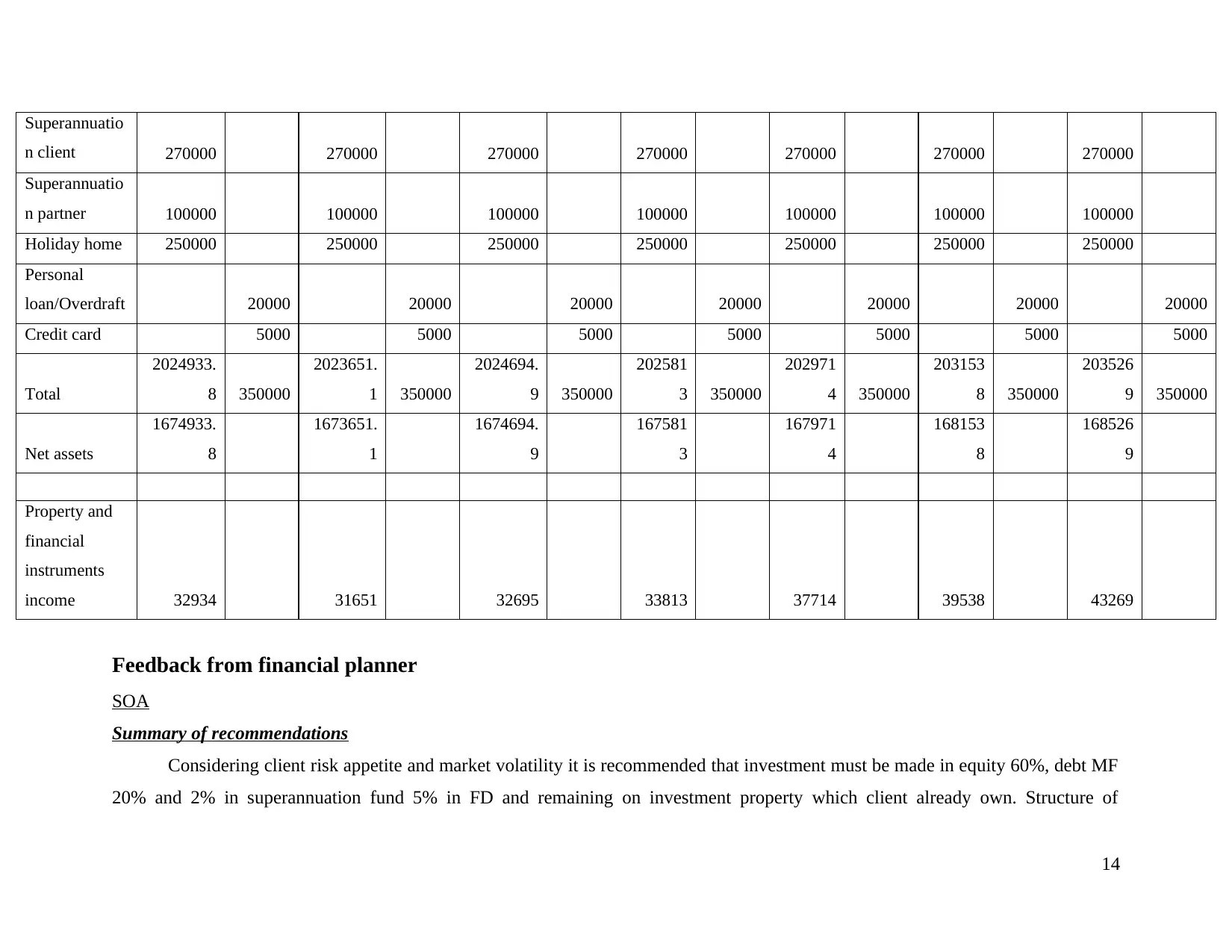

Superannuatio

n client 270000 270000 270000 270000 270000 270000 270000

Superannuatio

n partner 100000 100000 100000 100000 100000 100000 100000

Holiday home 250000 250000 250000 250000 250000 250000 250000

Personal

loan/Overdraft 20000 20000 20000 20000 20000 20000 20000

Credit card 5000 5000 5000 5000 5000 5000 5000

Total

2024933.

8 350000

2023651.

1 350000

2024694.

9 350000

202581

3 350000

202971

4 350000

203153

8 350000

203526

9 350000

Net assets

1674933.

8

1673651.

1

1674694.

9

167581

3

167971

4

168153

8

168526

9

Property and

financial

instruments

income 32934 31651 32695 33813 37714 39538 43269

Feedback from financial planner

SOA

Summary of recommendations

Considering client risk appetite and market volatility it is recommended that investment must be made in equity 60%, debt MF

20% and 2% in superannuation fund 5% in FD and remaining on investment property which client already own. Structure of

14

n client 270000 270000 270000 270000 270000 270000 270000

Superannuatio

n partner 100000 100000 100000 100000 100000 100000 100000

Holiday home 250000 250000 250000 250000 250000 250000 250000

Personal

loan/Overdraft 20000 20000 20000 20000 20000 20000 20000

Credit card 5000 5000 5000 5000 5000 5000 5000

Total

2024933.

8 350000

2023651.

1 350000

2024694.

9 350000

202581

3 350000

202971

4 350000

203153

8 350000

203526

9 350000

Net assets

1674933.

8

1673651.

1

1674694.

9

167581

3

167971

4

168153

8

168526

9

Property and

financial

instruments

income 32934 31651 32695 33813 37714 39538 43269

Feedback from financial planner

SOA

Summary of recommendations

Considering client risk appetite and market volatility it is recommended that investment must be made in equity 60%, debt MF

20% and 2% in superannuation fund 5% in FD and remaining on investment property which client already own. Structure of

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

investment will assist investor to earn higher return on moderate investment. Renovation and furnishing of investment property will be

done on regular basis of liquidity can be enhanced even during investment time period.

Client needs

What we discussed? Explanations on advice

To pay all mortgage amount till retirement and buy a new car and

visit any tourist place as well as developing source of income.

By considering client need and risk-taking behaviour

emphasis is given on property where small expenditure

will be made on renovation and furnishing. Considering

inflation rate and furnishing factor rent amount will be

increased by 7% each year for seven-year duration. This

will generate regular income.

Stock and relevant financial instruments if hold for long

term generate better returns may be 20% to 25%. Thus,

60% investment made in equity.

To prepare safe zone 27% investment is made on debt so

that capital can protected in investment.

15

done on regular basis of liquidity can be enhanced even during investment time period.

Client needs

What we discussed? Explanations on advice

To pay all mortgage amount till retirement and buy a new car and

visit any tourist place as well as developing source of income.

By considering client need and risk-taking behaviour

emphasis is given on property where small expenditure

will be made on renovation and furnishing. Considering

inflation rate and furnishing factor rent amount will be

increased by 7% each year for seven-year duration. This

will generate regular income.

Stock and relevant financial instruments if hold for long

term generate better returns may be 20% to 25%. Thus,

60% investment made in equity.

To prepare safe zone 27% investment is made on debt so

that capital can protected in investment.

15

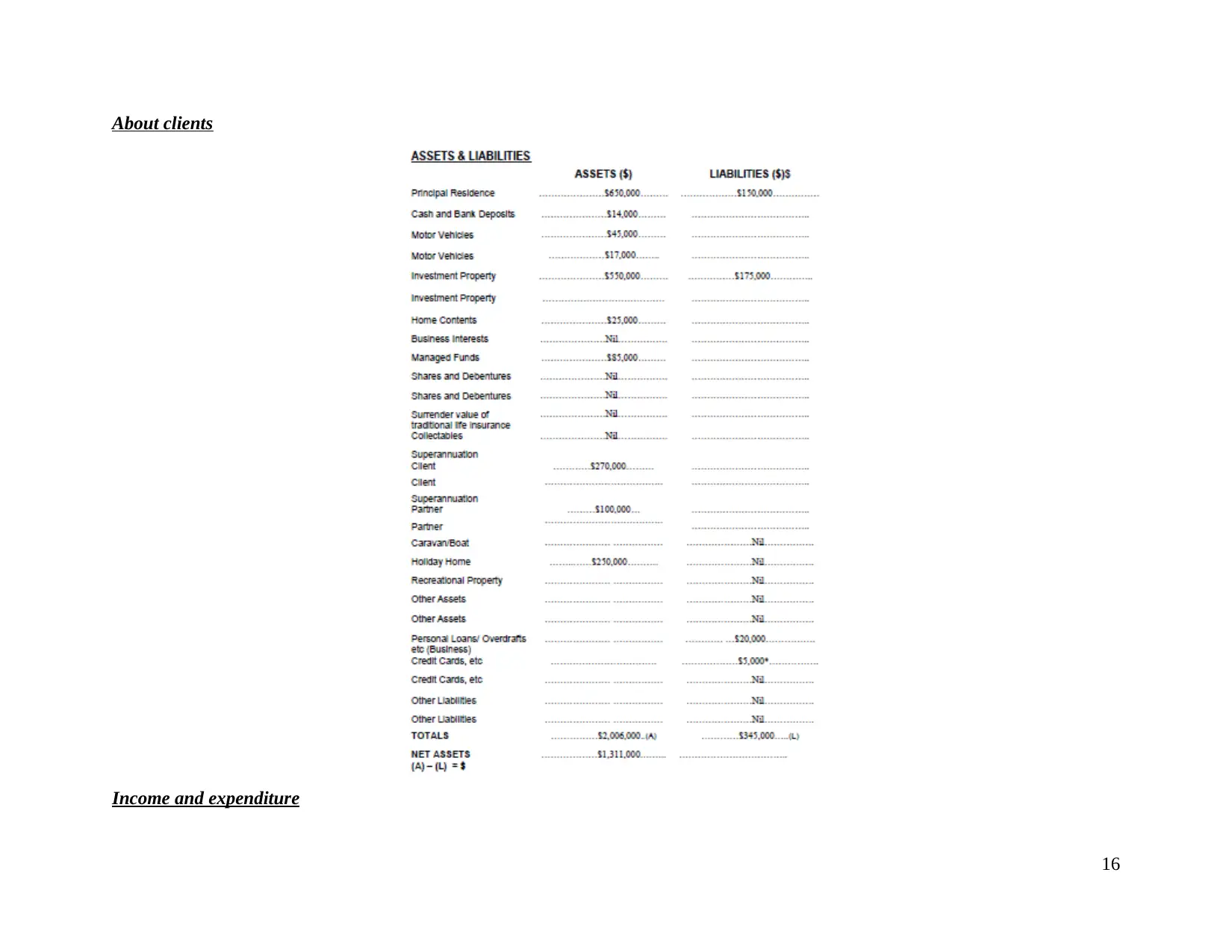

About clients

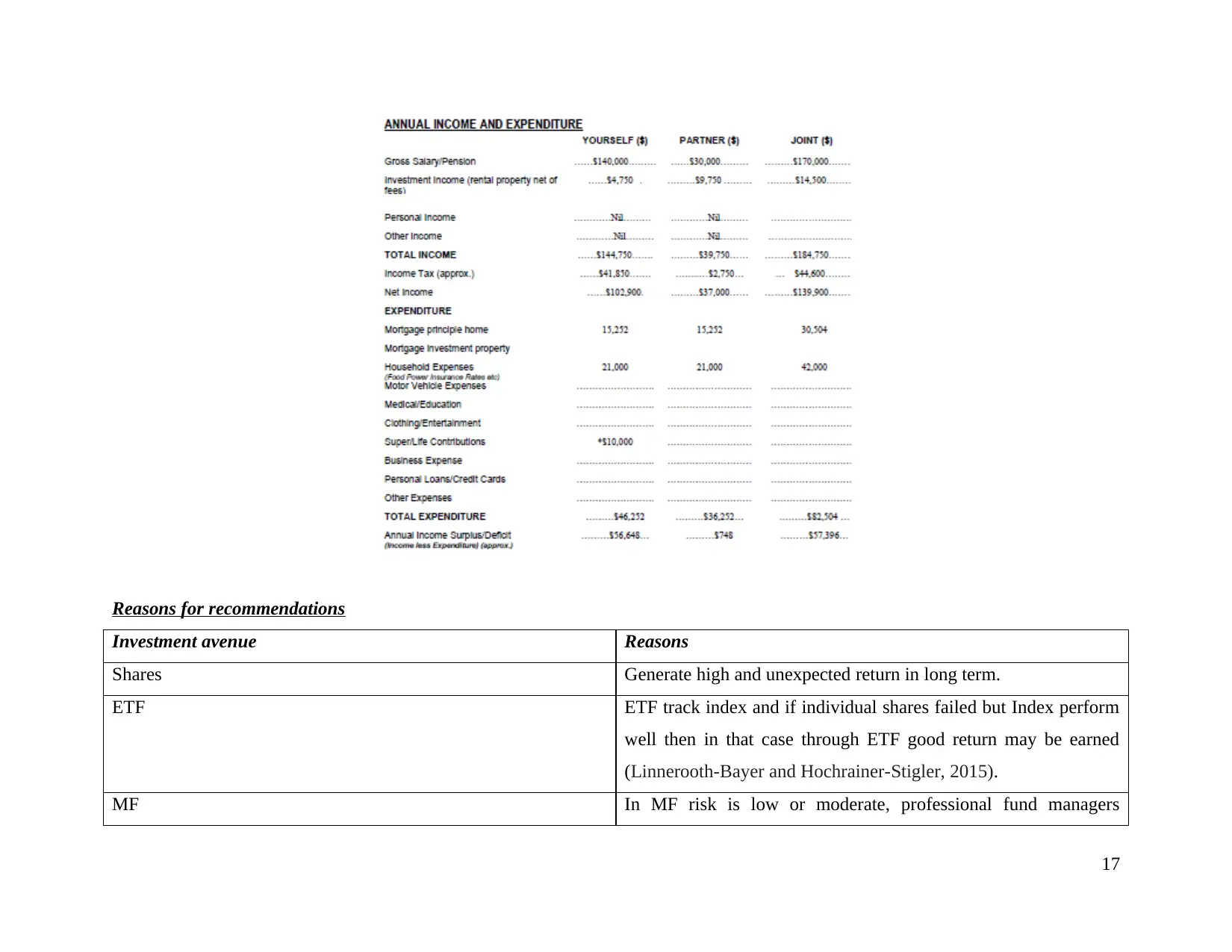

Income and expenditure

16

Income and expenditure

16

Reasons for recommendations

Investment avenue Reasons

Shares Generate high and unexpected return in long term.

ETF ETF track index and if individual shares failed but Index perform

well then in that case through ETF good return may be earned

(Linnerooth-Bayer and Hochrainer-Stigler, 2015).

MF In MF risk is low or moderate, professional fund managers

17

Investment avenue Reasons

Shares Generate high and unexpected return in long term.

ETF ETF track index and if individual shares failed but Index perform

well then in that case through ETF good return may be earned

(Linnerooth-Bayer and Hochrainer-Stigler, 2015).

MF In MF risk is low or moderate, professional fund managers

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manage fund and through investment in derivative minimize loss

on portfolio. Thus, better returns are earned in MF and is safe

then equity.

Debt MF Debt MF generate fixed percentage of return and if investment is

made on Junk bonds through it higher return can be expected.

Superannuation fund Only 2% is invested because return is low but safe haven for

investors.

Fixed deposits FD guarantee fixed return and safe investment. Investor is able to

take moderate risk and due to this reason 5% of fund is invested

in FD.

Property 13% is invested in real estate because it consistently generates

good return for the investors in past years. Moreover, client

already have investment property (Finke, M.S. Howe and Huston,

2017). By renovation more rent can be earned through property.

Hence, 13% is invested in property.

Consequence of advice

40% investment is made on capital protection assets and remaining on risky assets which contain some high or moderate risky asset in

equity. Thus, at low risk higher profit will be earned nearby to 33% ROI.

Investment 769415

Return 251614

Return % 33%

18

on portfolio. Thus, better returns are earned in MF and is safe

then equity.

Debt MF Debt MF generate fixed percentage of return and if investment is

made on Junk bonds through it higher return can be expected.

Superannuation fund Only 2% is invested because return is low but safe haven for

investors.

Fixed deposits FD guarantee fixed return and safe investment. Investor is able to

take moderate risk and due to this reason 5% of fund is invested

in FD.

Property 13% is invested in real estate because it consistently generates

good return for the investors in past years. Moreover, client

already have investment property (Finke, M.S. Howe and Huston,

2017). By renovation more rent can be earned through property.

Hence, 13% is invested in property.

Consequence of advice

40% investment is made on capital protection assets and remaining on risky assets which contain some high or moderate risky asset in

equity. Thus, at low risk higher profit will be earned nearby to 33% ROI.

Investment 769415

Return 251614

Return % 33%

18

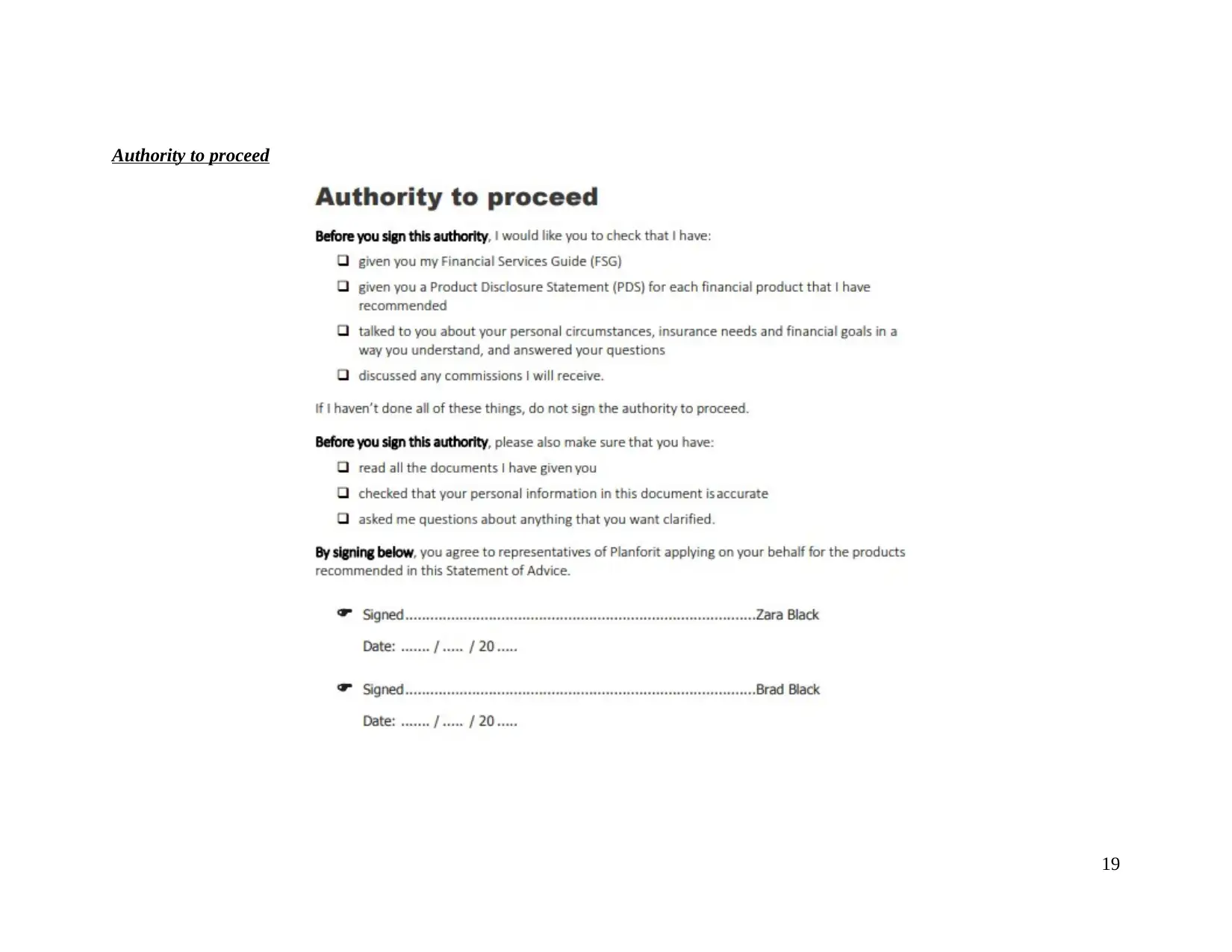

Authority to proceed

19

19

CONCLUSION

By summing up above report it has been concluded that both Hamish and Harriet may invest their amount on equity (60%),

residential property (13%) and superannuation (2%) that will help to generate more profit even after their retirement. Further, it is also

concluded that to make financial planning better, it is essential to consider all the key element and analyze future benefits as well.

Lastly, report concluded that all the risk should be analyzed before making any investment and also develop proper planning for the

same.

20

By summing up above report it has been concluded that both Hamish and Harriet may invest their amount on equity (60%),

residential property (13%) and superannuation (2%) that will help to generate more profit even after their retirement. Further, it is also

concluded that to make financial planning better, it is essential to consider all the key element and analyze future benefits as well.

Lastly, report concluded that all the risk should be analyzed before making any investment and also develop proper planning for the

same.

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Acharya, V.V. and Ryan, S.G., 2016. Banks’ financial reporting and financial system stability. Journal of Accounting Research. 54(2).

pp.277-340.

Bieliński, T. and Mosionek-Schweda, M., 2018. Green Bonds as a financial instrument for environmental projects funding. Unia

Europejska. Pl. 248(1). pp.13-21.

Bui, Y. H., Sarath, D. and Ahmed, A.D., 2016. Efficiency of Australian superannuation funds: a comparative assessment. Journal of

Economic Studies.

Cummings, J. R., 2016. Effect of fund size on the performance of Australian superannuation funds. Accounting & Finance. 56(3).

pp.695-725.

Duffy, D.J., 2018. Financial Instrument Pricing Using C++. John Wiley & Sons.

Finke, M.S., Howe, J.S. and Huston, S.J., 2017. Old age and the decline in financial literacy. Management Science. 63(1). pp.213-230.

Fuertes, A. and Gimeno, R., 2017. Inflation expectation indicators based on financial instrument prices. Banco de Espana Article. 16.

p.17.

Linnerooth-Bayer, J. and Hochrainer-Stigler, S., 2015. Financial instruments for disaster risk management and climate change

adaptation. Climatic Change. 133(1). pp.85-100.

Mackenzie, G., 2017. Superannuation tax reform: The new fairness measures. Tax Specialist, 21(2), p.73.

Kingston, G. and Thorp, S., 2019. Superannuation in Australia: A Survey of the Literature. Economic Record.95(308). pp.141-160.

21

Books and Journals

Acharya, V.V. and Ryan, S.G., 2016. Banks’ financial reporting and financial system stability. Journal of Accounting Research. 54(2).

pp.277-340.

Bieliński, T. and Mosionek-Schweda, M., 2018. Green Bonds as a financial instrument for environmental projects funding. Unia

Europejska. Pl. 248(1). pp.13-21.

Bui, Y. H., Sarath, D. and Ahmed, A.D., 2016. Efficiency of Australian superannuation funds: a comparative assessment. Journal of

Economic Studies.

Cummings, J. R., 2016. Effect of fund size on the performance of Australian superannuation funds. Accounting & Finance. 56(3).

pp.695-725.

Duffy, D.J., 2018. Financial Instrument Pricing Using C++. John Wiley & Sons.

Finke, M.S., Howe, J.S. and Huston, S.J., 2017. Old age and the decline in financial literacy. Management Science. 63(1). pp.213-230.

Fuertes, A. and Gimeno, R., 2017. Inflation expectation indicators based on financial instrument prices. Banco de Espana Article. 16.

p.17.

Linnerooth-Bayer, J. and Hochrainer-Stigler, S., 2015. Financial instruments for disaster risk management and climate change

adaptation. Climatic Change. 133(1). pp.85-100.

Mackenzie, G., 2017. Superannuation tax reform: The new fairness measures. Tax Specialist, 21(2), p.73.

Kingston, G. and Thorp, S., 2019. Superannuation in Australia: A Survey of the Literature. Economic Record.95(308). pp.141-160.

21

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.