Financial Problems Analysis: Finance Assignment for [University Name]

VerifiedAdded on 2020/04/07

|30

|4155

|82

Homework Assignment

AI Summary

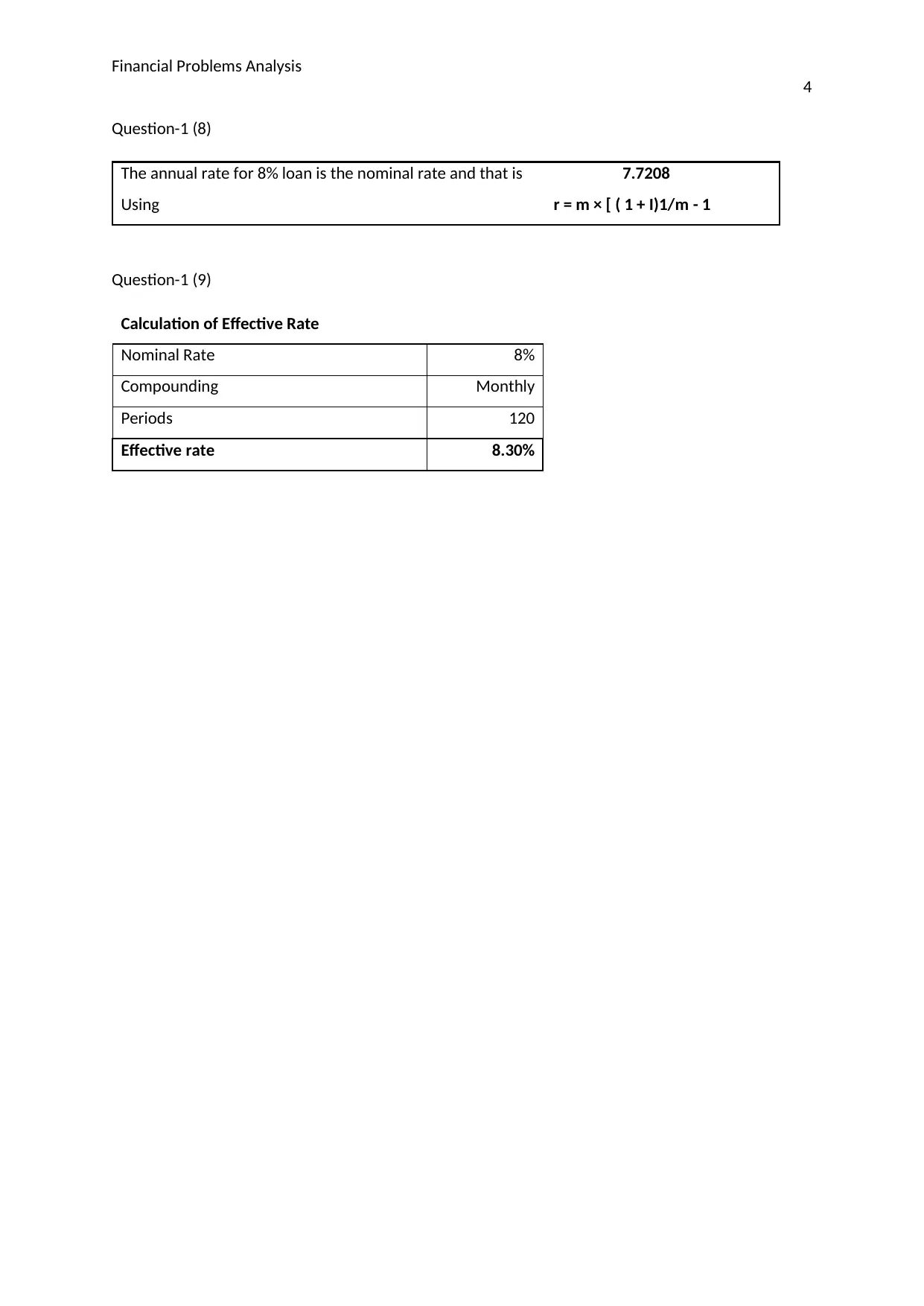

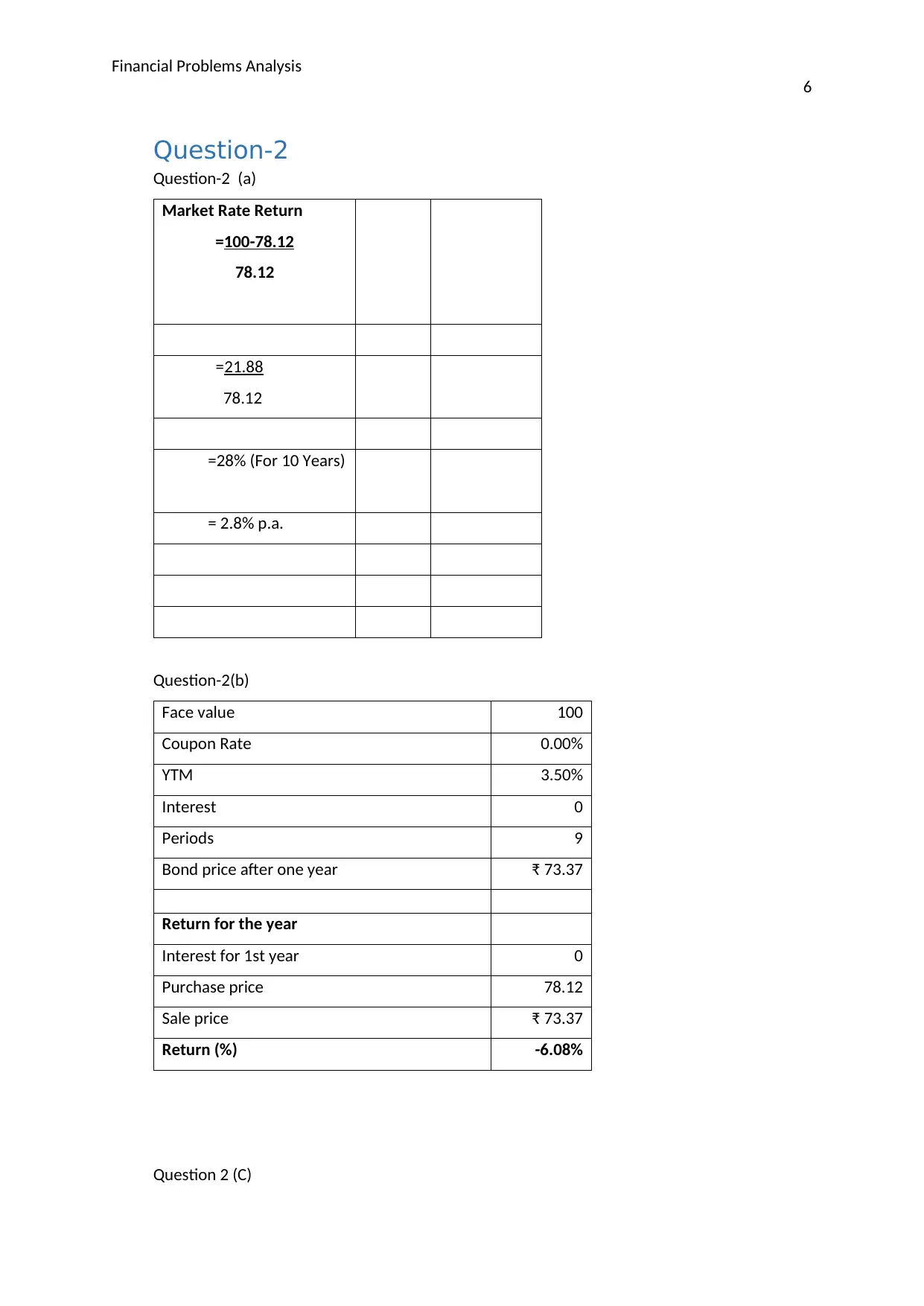

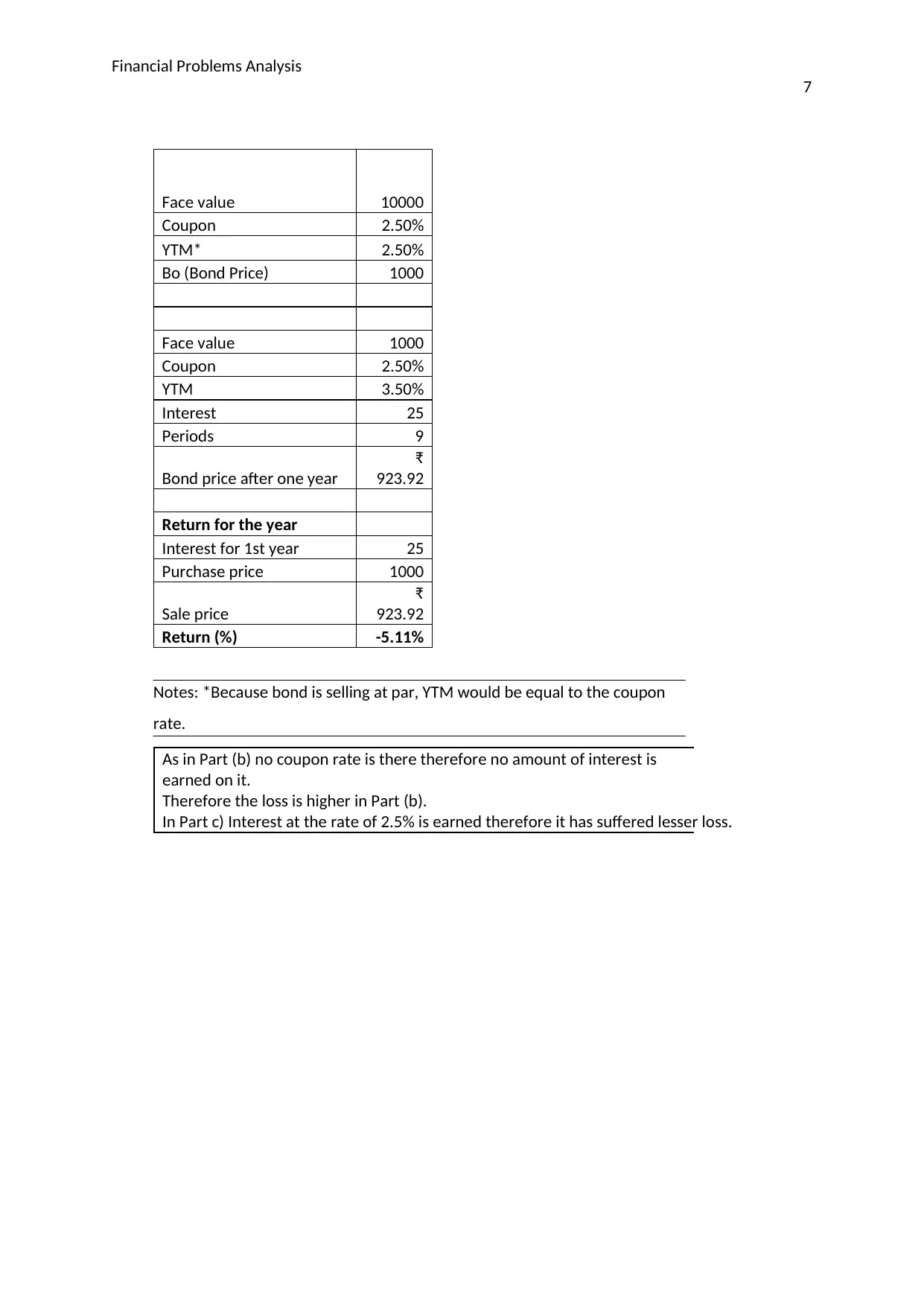

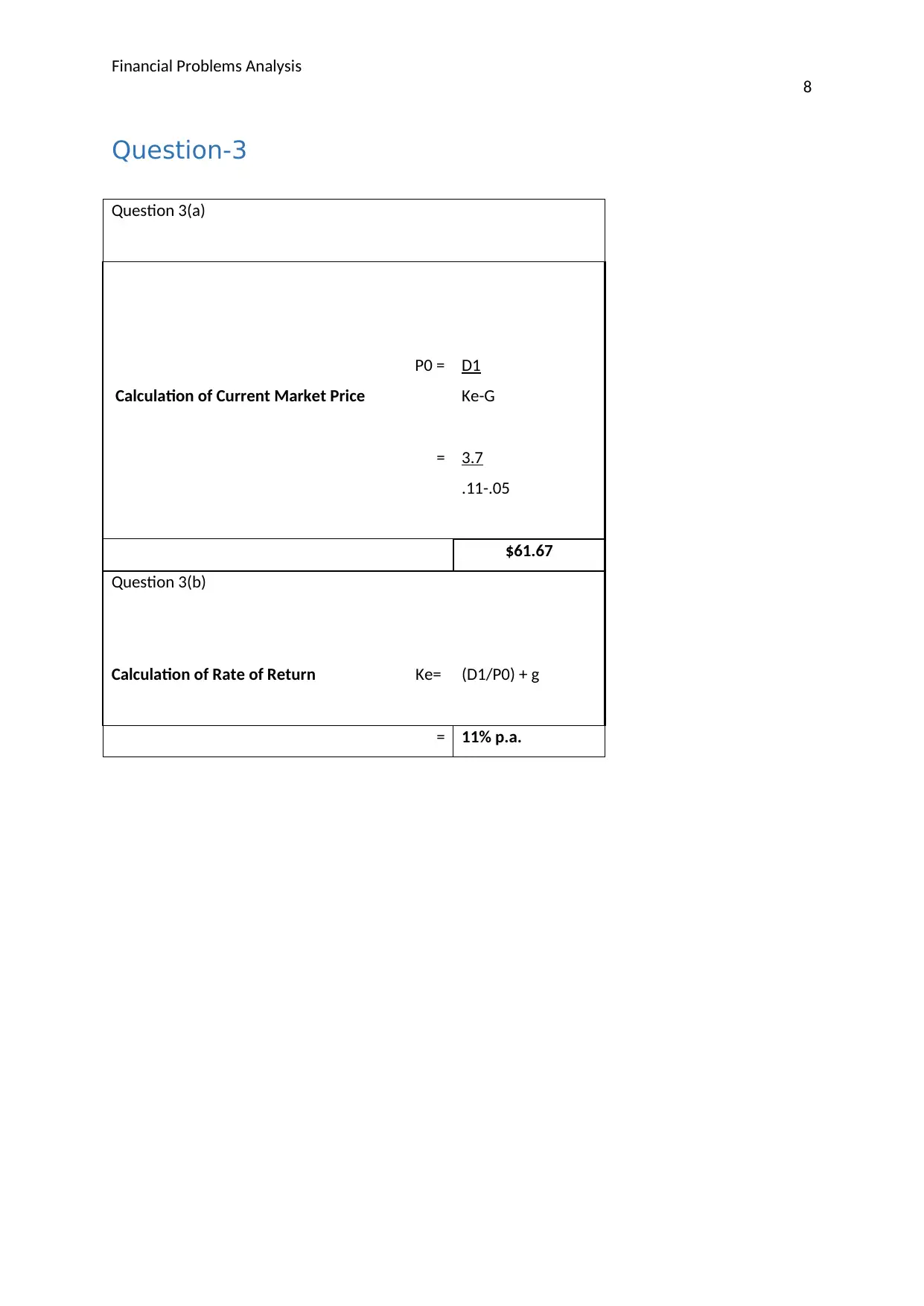

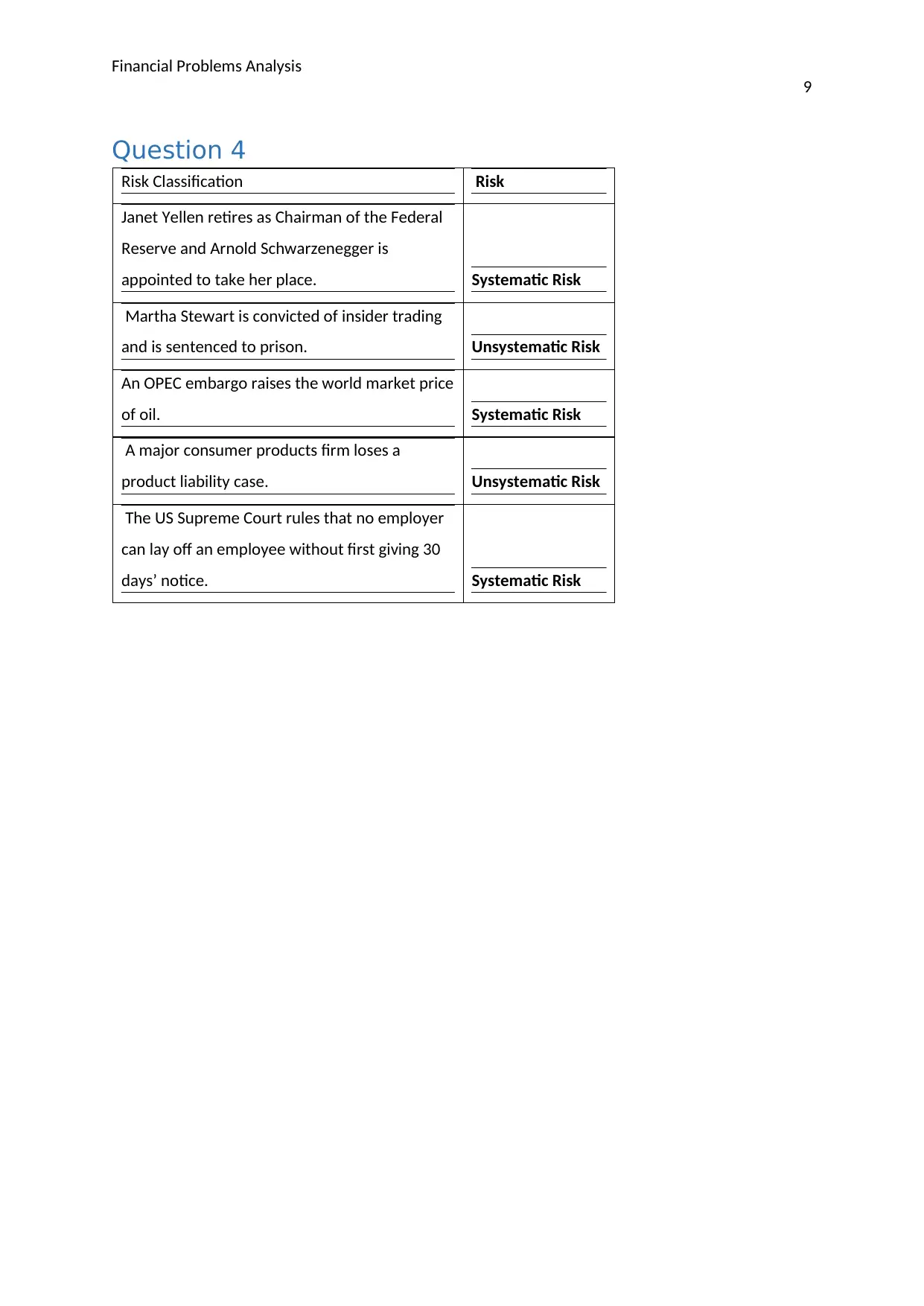

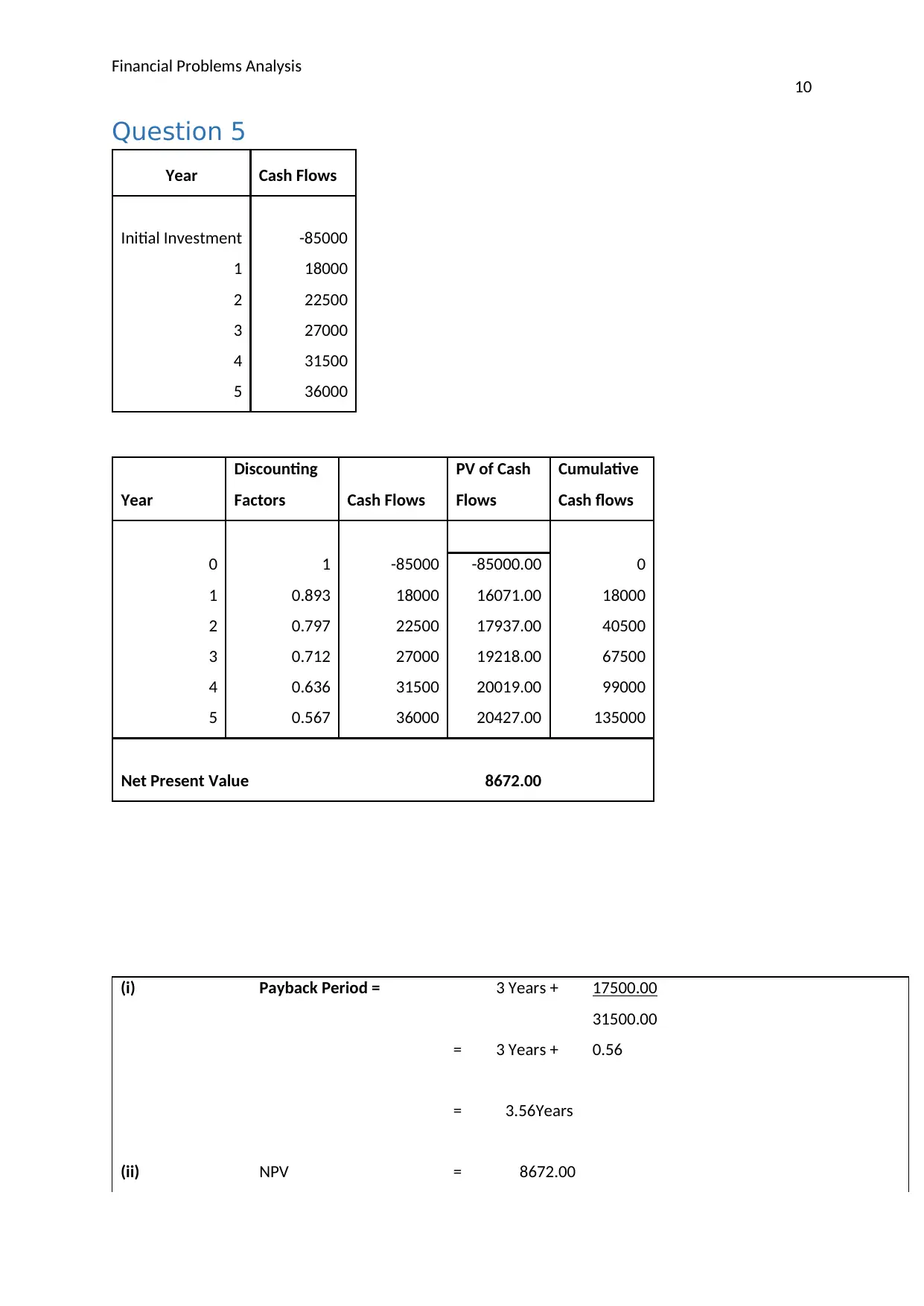

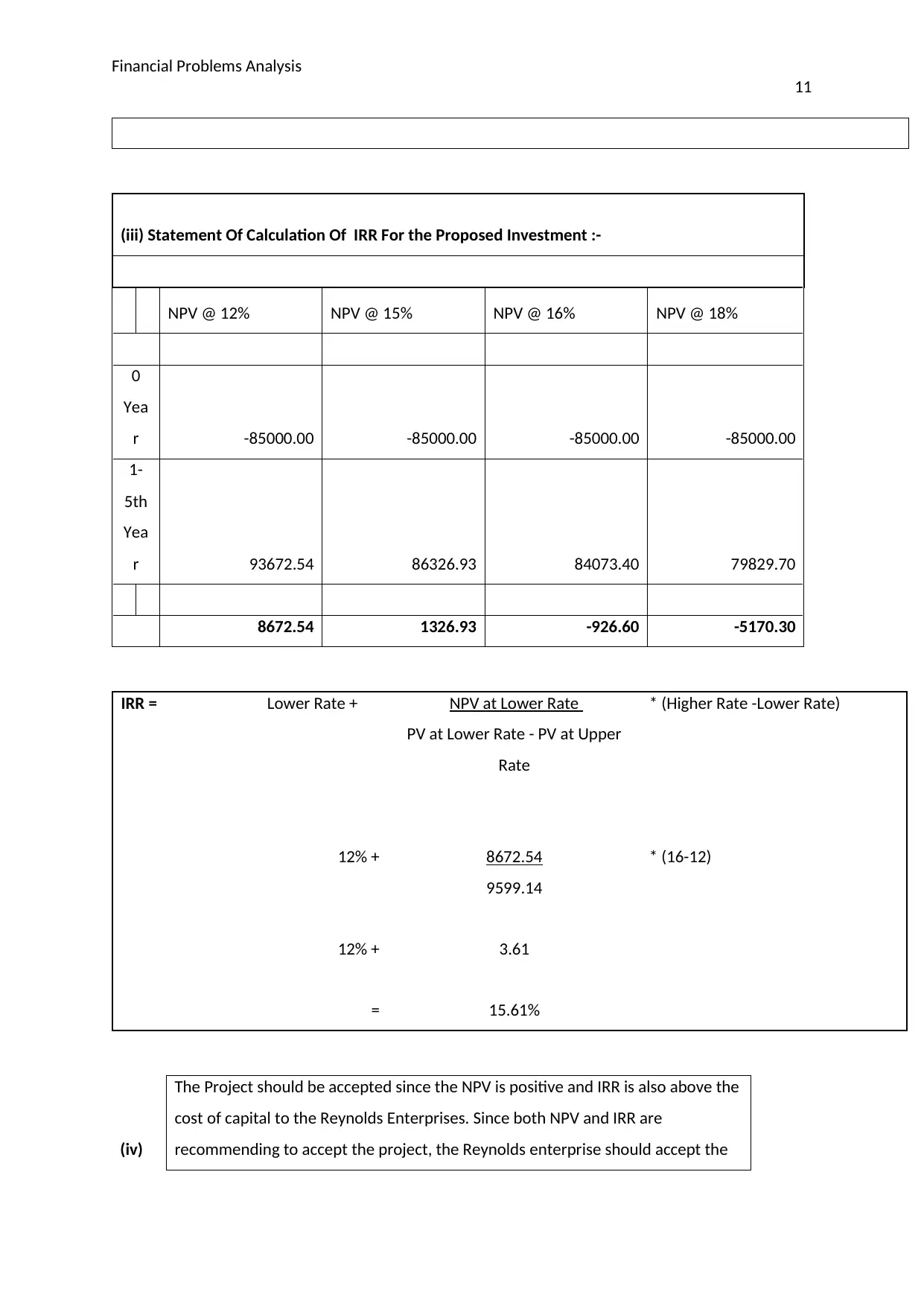

This assignment provides a comprehensive analysis of various financial problems. It begins with detailed calculations related to loan installments, interest, and refinancing decisions. The document then delves into bond valuation, exploring market returns and the impact of coupon rates on bond prices. Capital budgeting techniques, including payback period, NPV, and IRR, are applied to evaluate investment projects. Risk classification and its impact on financial decisions are also discussed. Furthermore, the assignment analyzes the impact of different investment strategies, and offers solutions for the renovation vs. replacement of an asset. Finally, the assignment concludes with an analysis of financial ratios and portfolio management using the CAPM model, offering valuable insights into company valuation and investment strategies.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.