Stock Portfolio Performance Analysis

VerifiedAdded on 2020/01/28

|9

|1063

|69

Homework Assignment

AI Summary

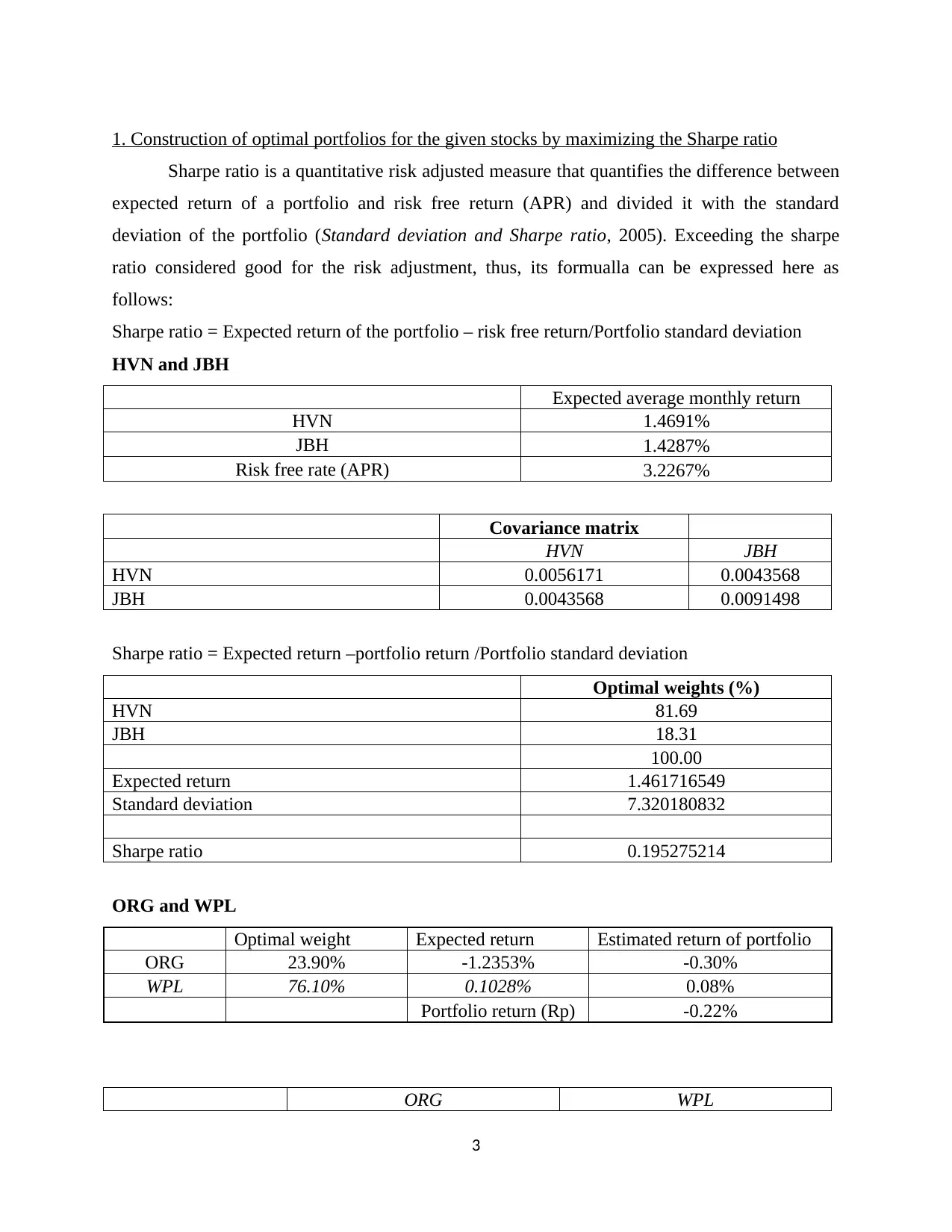

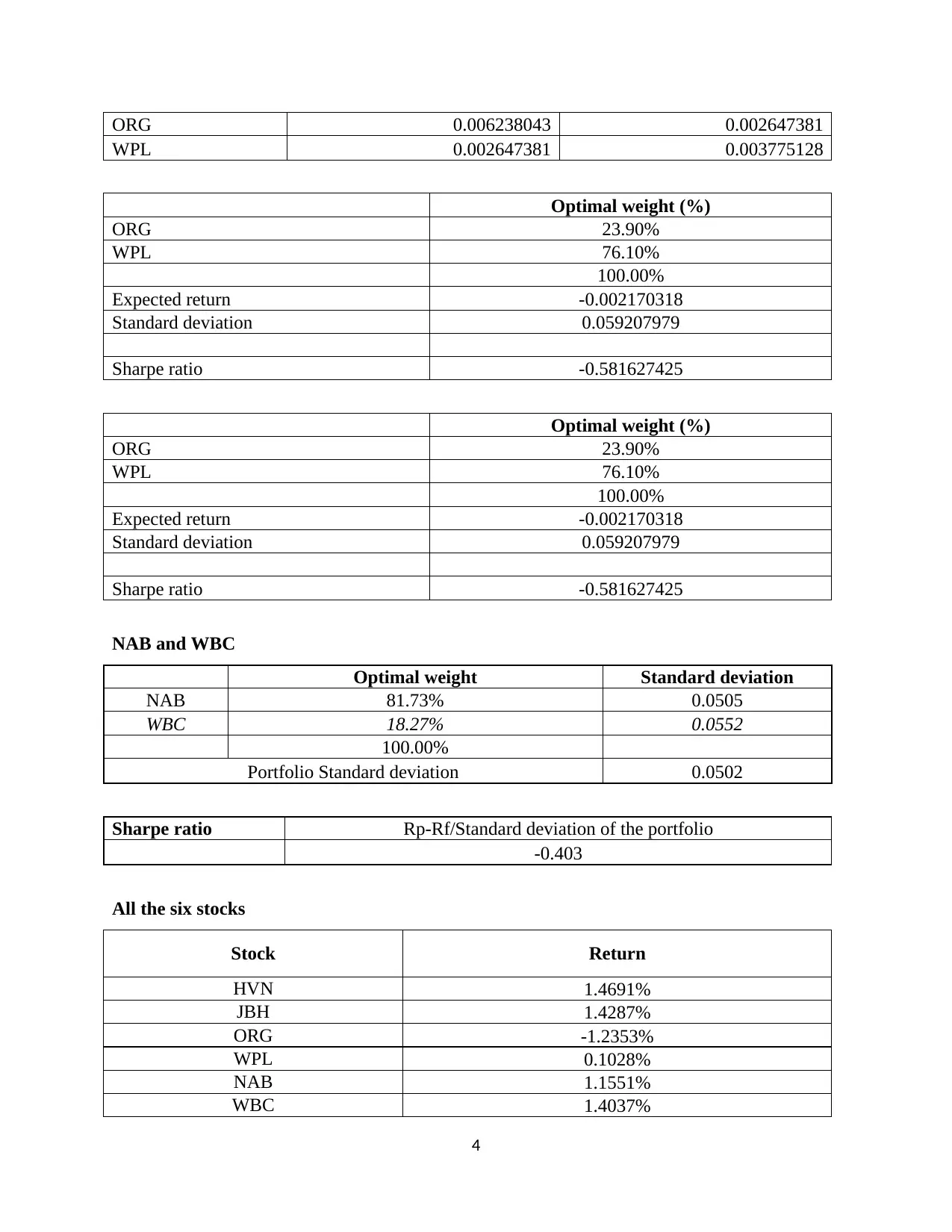

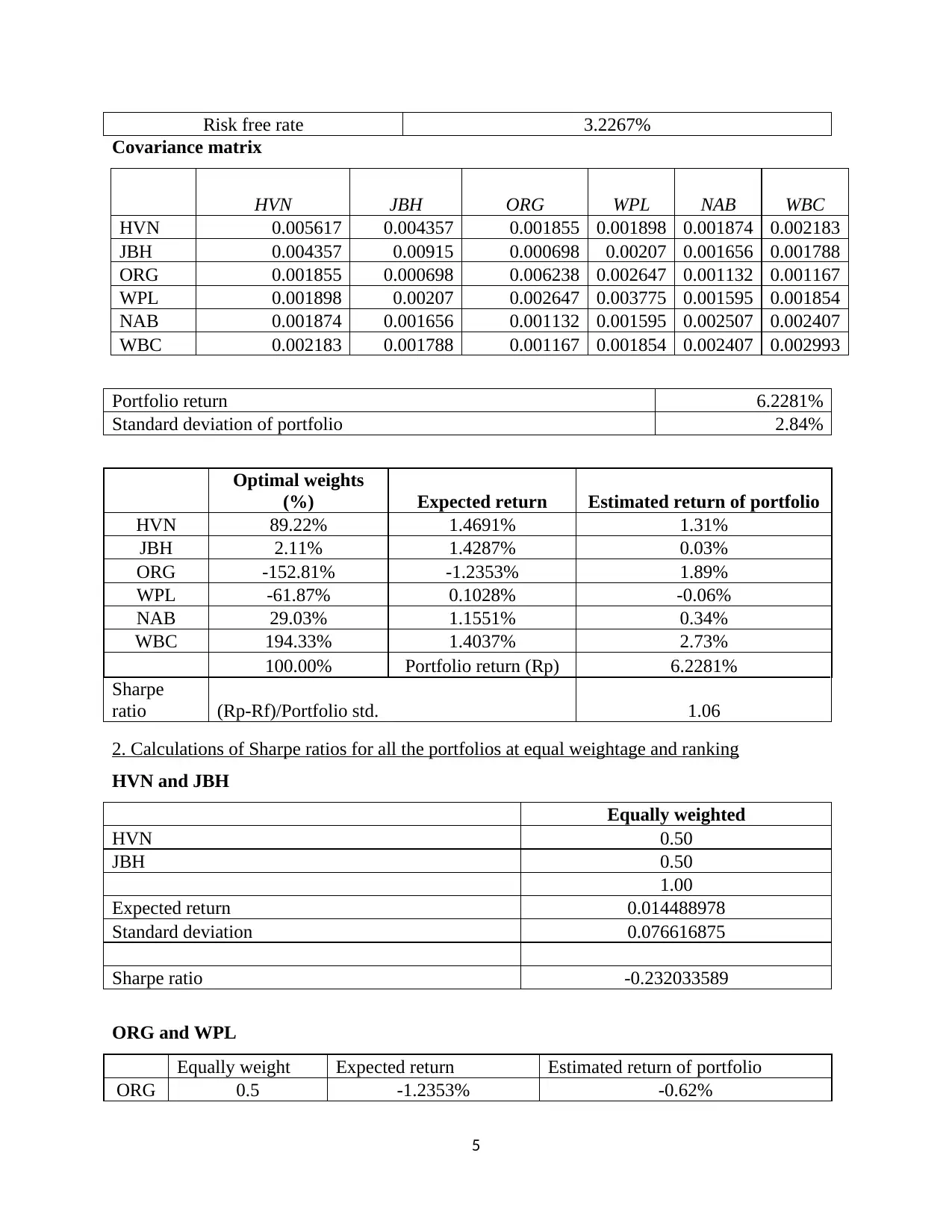

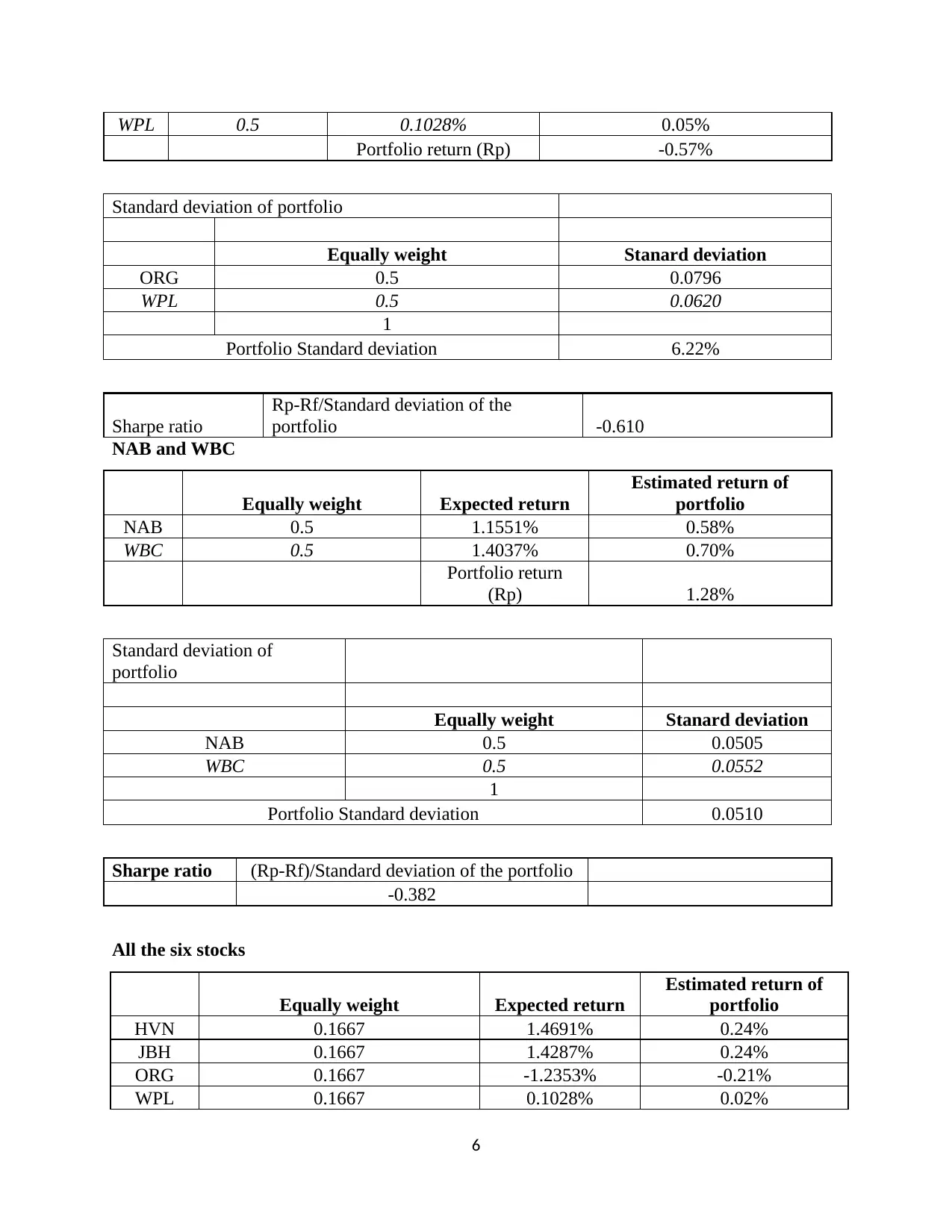

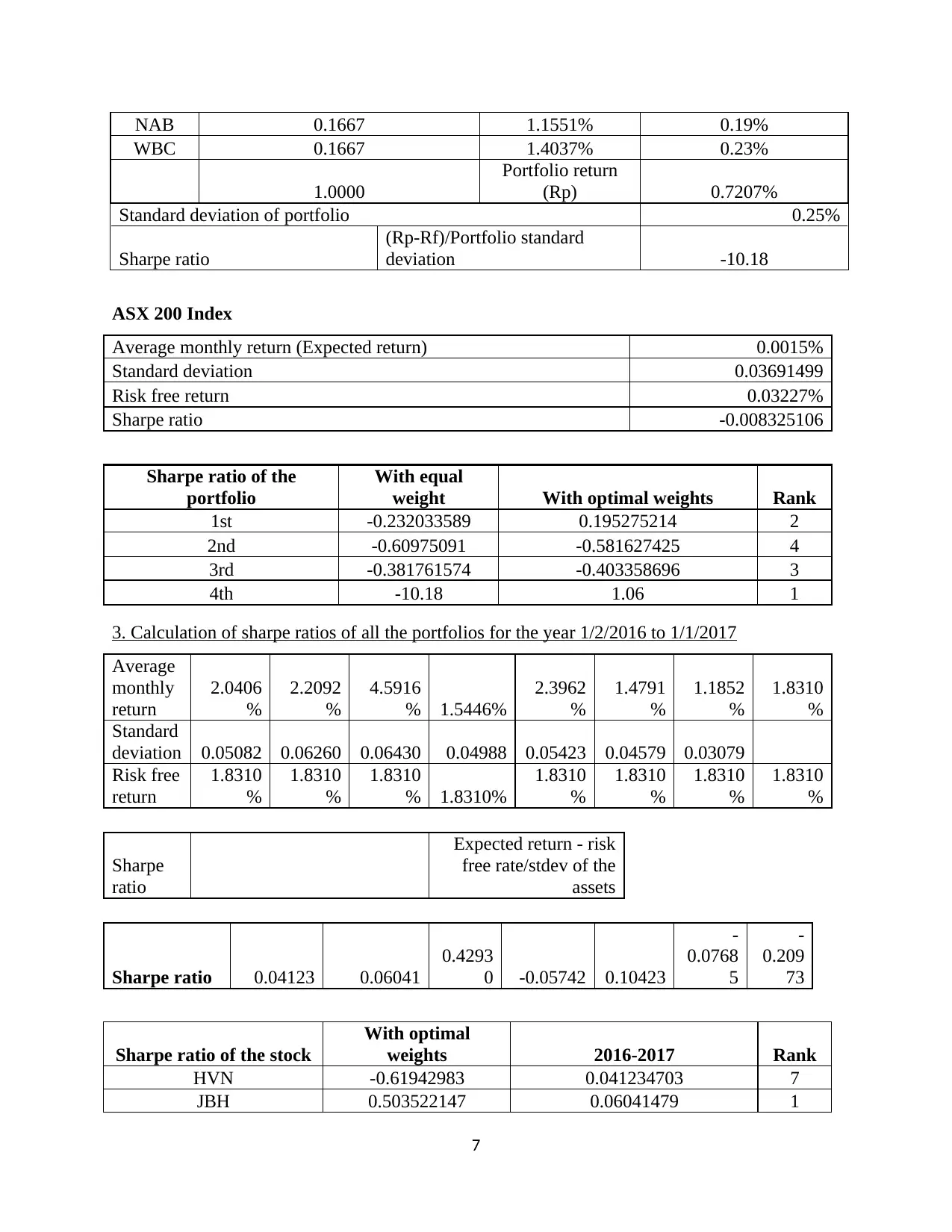

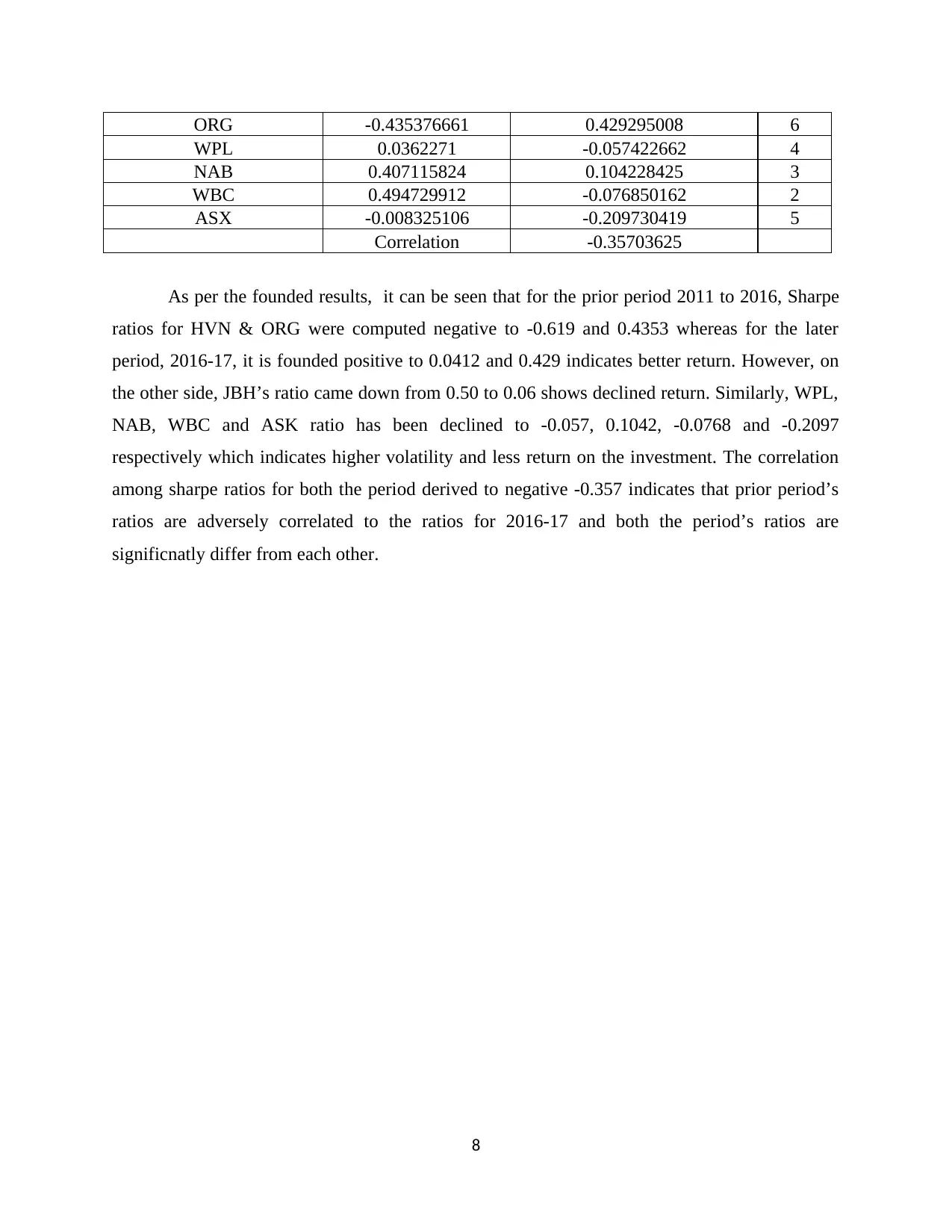

This assignment analyzes the performance of a stock portfolio across two periods (2011-2016 and 2016-2017) using the Sharpe ratio as a measure of risk-adjusted return. It examines individual stock performances (HVN, JBH, ORG, WPL, NAB, WBC, ASX) and their optimal weights for portfolio diversification. The analysis also includes correlation between Sharpe ratios across periods to understand performance trends and identify potential risks.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.