Financial Evaluation Report for BIA Ltd. Rebranding Project Assessment

VerifiedAdded on 2022/12/27

|20

|3480

|1

Report

AI Summary

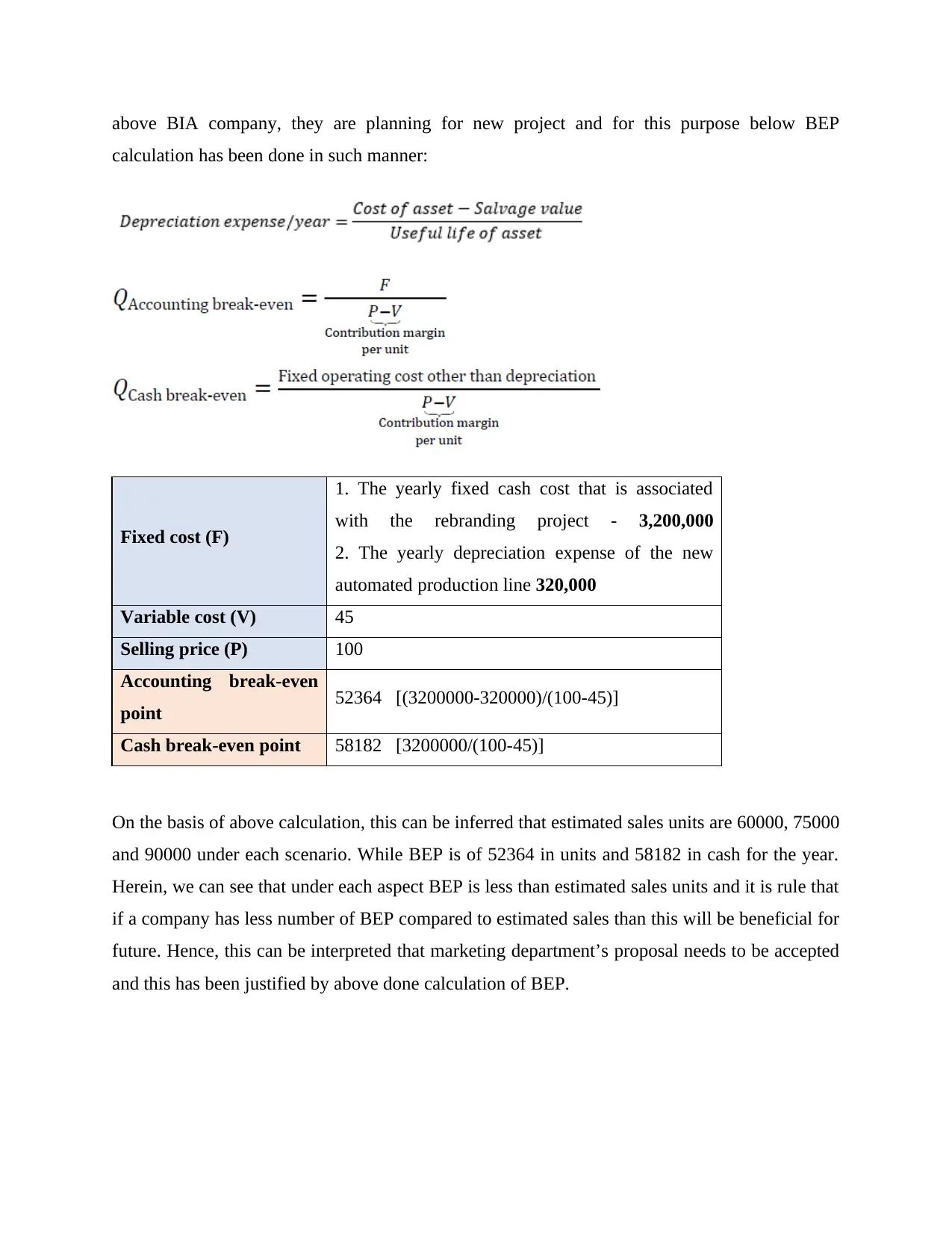

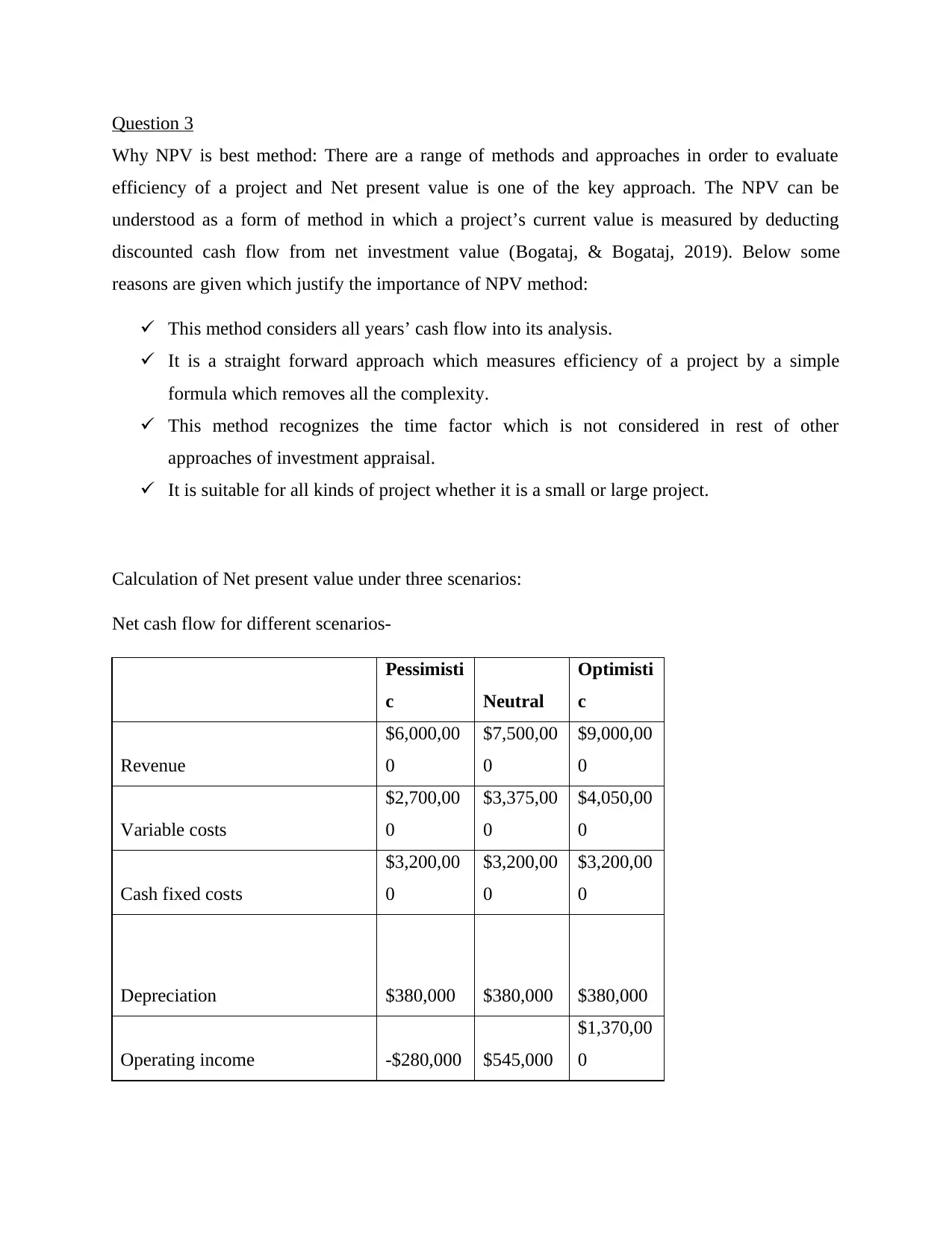

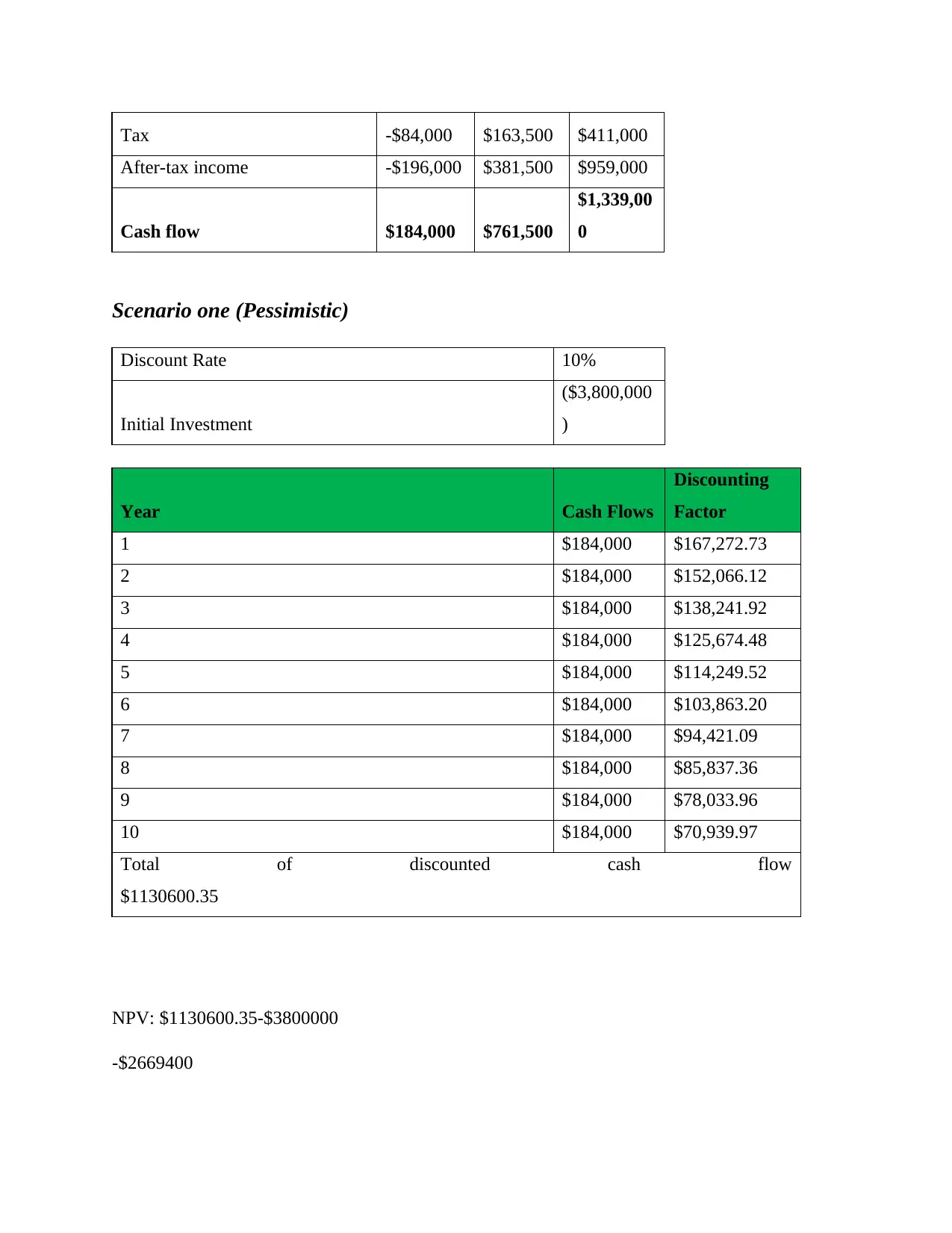

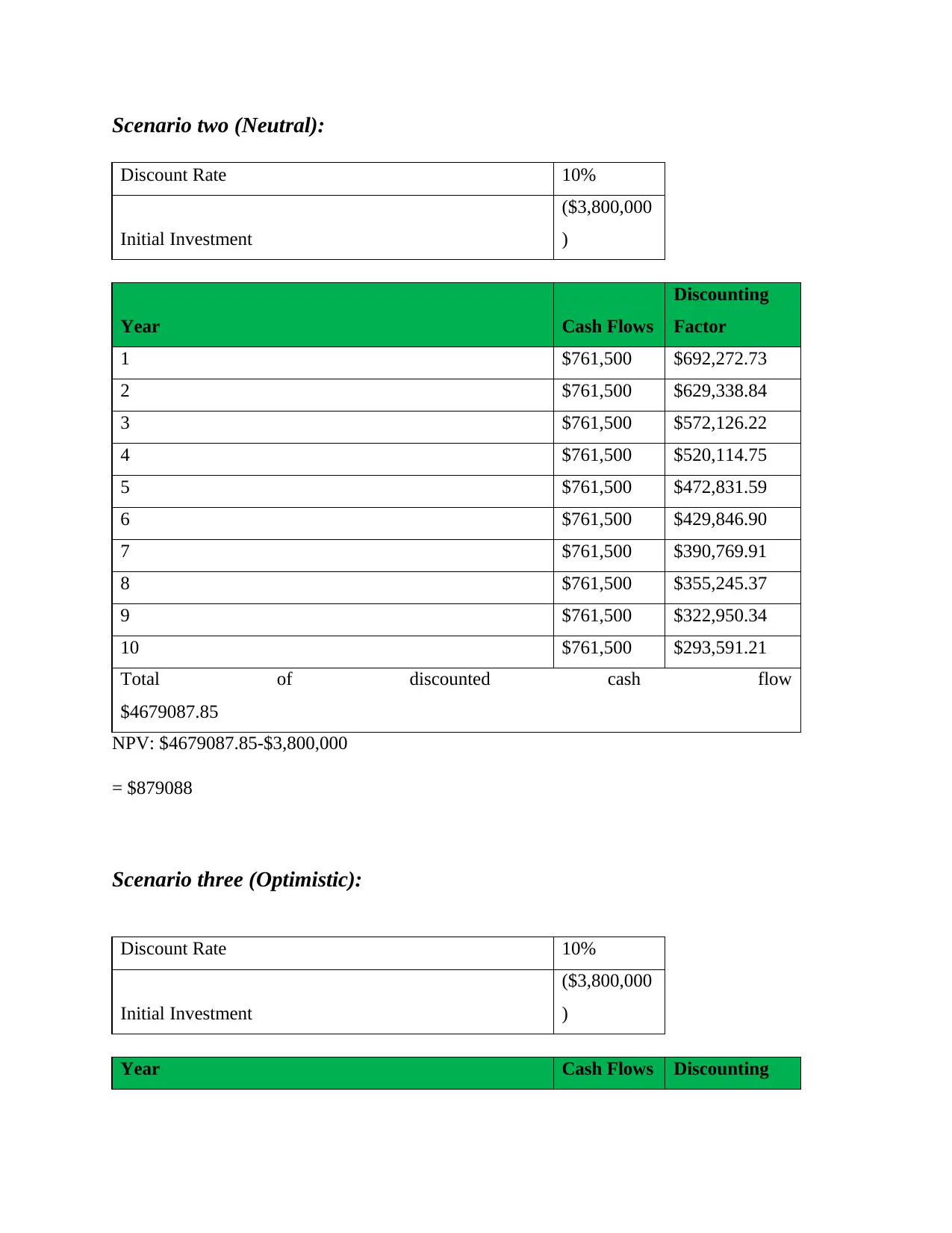

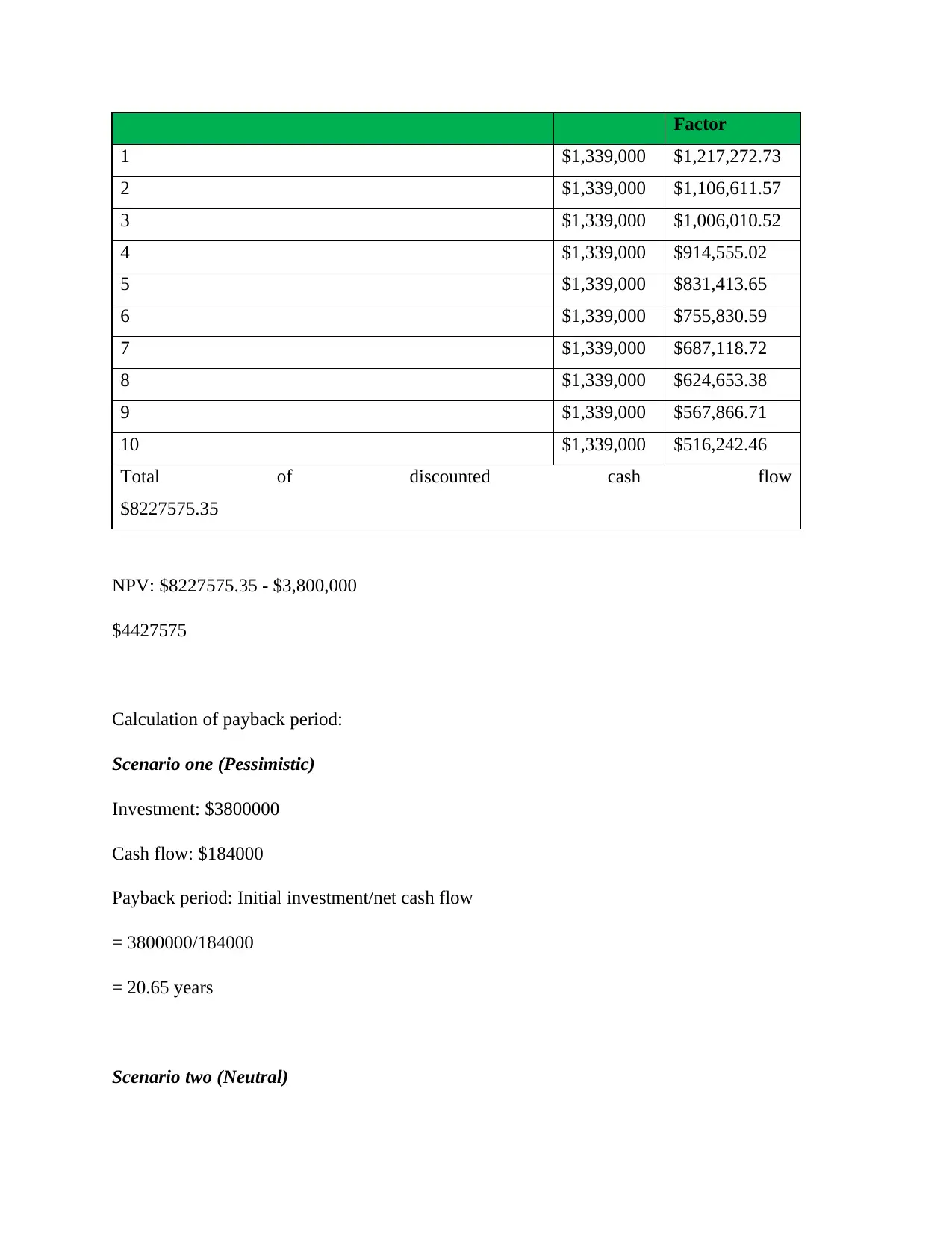

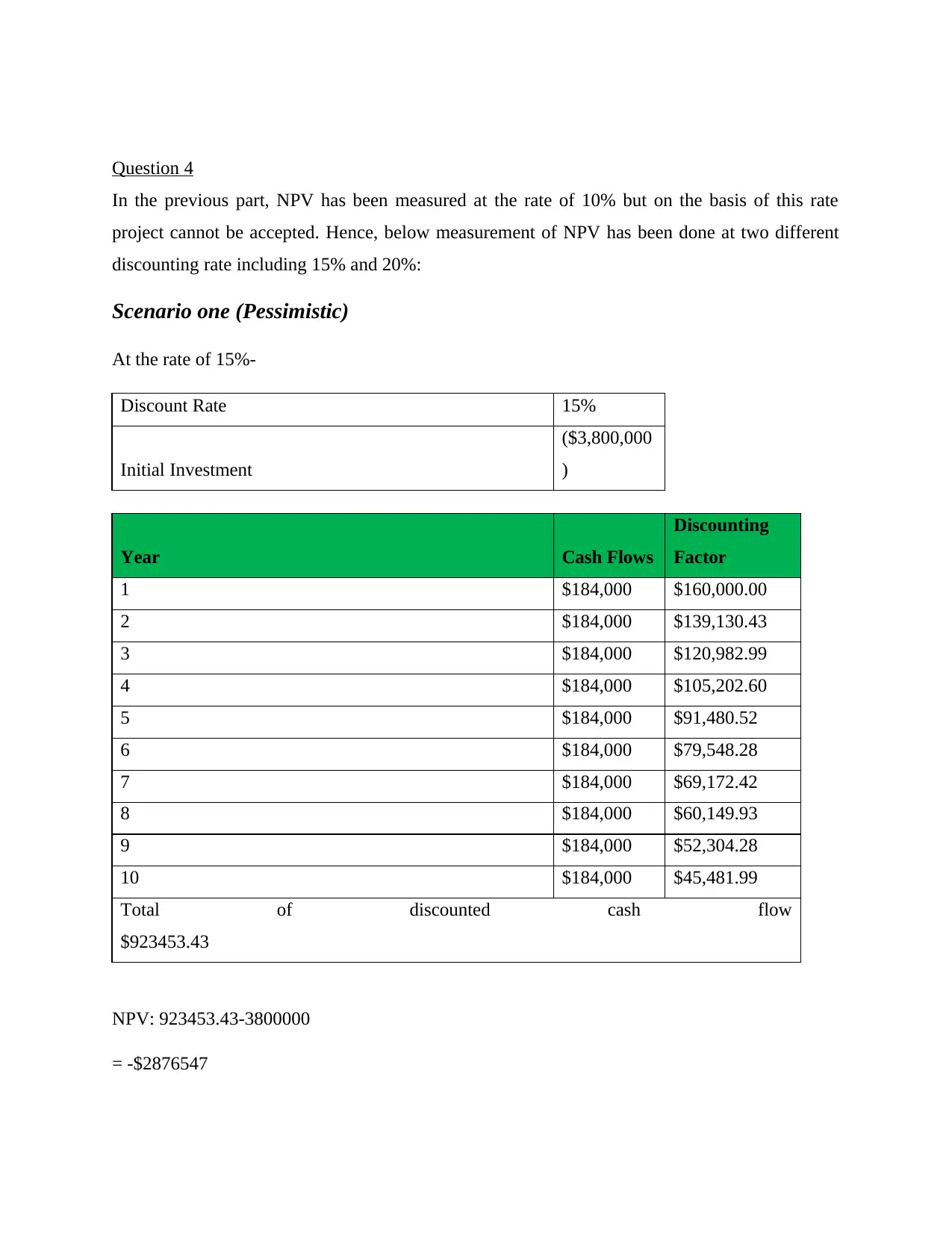

This report provides a detailed financial evaluation of BIA Ltd.'s rebranding project. It begins with an executive summary, followed by an introduction that outlines the company's situation and the report's objectives. The main body addresses key financial concepts, including the cash conversion cycle, break-even analysis, and investment appraisal techniques (NPV and payback period) under optimistic, neutral, and pessimistic scenarios. The report calculates the cash conversion cycle, break-even points, and assesses the project's viability through NPV and payback period methods at different discount rates. The findings indicate that the project is viable under most scenarios, with the report concluding with comments on the company's capital structure, and limitations. The report uses financial ratios and investment appraisal techniques to determine the project's feasibility and offers recommendations for financing options. The report is a comprehensive financial analysis of the rebranding project, covering various financial aspects and providing a clear assessment of its viability.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.