Financial Report: Analysis of Financial Statements and Ratios

VerifiedAdded on 2022/12/30

|16

|2542

|62

AI Summary

This financial report provides an overview of financial statement preparation, analysis, and ratio interpretation. It covers the difference between financial and management accounting and explores the importance of various ratios such as current ratio, quick ratio, gross profit ratio, and net profit ratio. The report also includes a case study on Lucky House Limited and its financial performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Report

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

TASK 1............................................................................................................................................1

A) Two branches of accounting and explain the difference between the financial and

management ................................................................................................................................1

Journal entry and prepare of trial balance ...................................................................................3

Task 2...............................................................................................................................................8

A. Statement of Profit and Loss and Statement of Financial Position.........................................8

Ratio analysis and interpretation ...............................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

Books and Journals ...................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

TASK 1............................................................................................................................................1

A) Two branches of accounting and explain the difference between the financial and

management ................................................................................................................................1

Journal entry and prepare of trial balance ...................................................................................3

Task 2...............................................................................................................................................8

A. Statement of Profit and Loss and Statement of Financial Position.........................................8

Ratio analysis and interpretation ...............................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

Books and Journals ...................................................................................................................12

INTRODUCTION

Financial report means report made for the preparation of the financial statements which

is very important for the analysing of the organization performance, through this they determine

the position in the market place through the use of the decision which is make by the manager

after analysing all the balance sheet and income statements. It is the formal records of the

financial activities and position of the business, person and entities. It is made in the structured

way which ids very easy to understand for the investors and analyst. This report is based on the

making of the income statement, making journals and balance sheet (Burkhanov, 2020). There is

the analysis of the ratio for determine the comparison of the two company regarding their

position and performance to convey the financial activities for giving the financial affairs. In this

there is the requirement of the financial statement analysis of the company to determine the

analysis of the company.

MAIN BODY

TASK 1

A) Two branches of accounting and explain the difference between the financial and

management

In the accounting, there is the internal auditor and chief financial officer for evaluate the

positions of the company in the working business. It is used for all branch public sector, non

profit sector and technological developments. There are different types of branch is there-

Financial accounting- it is the systematic method used for recording the business

transactions for the recording of the accounting principles for calculation of the profit and

loss and accurate picture of the balance sheet during the period which is benefit for the

calculation of the trail balance, balance sheet which is based on the financial accounting

principles. It is useful for the creditors, banks and financial status. It involves recording f

the transactions in a day which is remain in the historical for generating the past, it

involves in generating financial statements which is prepared according to the generally

accepted accounting principles (GAAP) for the calculation of the various tax which is

based on the various bank balances and tax based records. This the external regulations

1

Financial report means report made for the preparation of the financial statements which

is very important for the analysing of the organization performance, through this they determine

the position in the market place through the use of the decision which is make by the manager

after analysing all the balance sheet and income statements. It is the formal records of the

financial activities and position of the business, person and entities. It is made in the structured

way which ids very easy to understand for the investors and analyst. This report is based on the

making of the income statement, making journals and balance sheet (Burkhanov, 2020). There is

the analysis of the ratio for determine the comparison of the two company regarding their

position and performance to convey the financial activities for giving the financial affairs. In this

there is the requirement of the financial statement analysis of the company to determine the

analysis of the company.

MAIN BODY

TASK 1

A) Two branches of accounting and explain the difference between the financial and

management

In the accounting, there is the internal auditor and chief financial officer for evaluate the

positions of the company in the working business. It is used for all branch public sector, non

profit sector and technological developments. There are different types of branch is there-

Financial accounting- it is the systematic method used for recording the business

transactions for the recording of the accounting principles for calculation of the profit and

loss and accurate picture of the balance sheet during the period which is benefit for the

calculation of the trail balance, balance sheet which is based on the financial accounting

principles. It is useful for the creditors, banks and financial status. It involves recording f

the transactions in a day which is remain in the historical for generating the past, it

involves in generating financial statements which is prepared according to the generally

accepted accounting principles (GAAP) for the calculation of the various tax which is

based on the various bank balances and tax based records. This the external regulations

1

for the internal employees to make analyse and make financial decisions for used in the

purpose.

Cost accounting- Cost accounting refers to the branch of Accounting in which the

estimation of overall level of costs can be done highly effectively and efficiently. Thus in

this way the use of different types of methods can be made so that the costs are reduced

which will help in achieving financial goals and objectives (Farre-Mensa and Ljungqvist,

2016).

Difference between Financial accounting and Management accounting

Basis Financial accounting Management

accounting

Usage Financial accounting

puts its focus on

making the use of

financial facts, data and

information so that the

financial goals and

objectives can be

attained.

Management

accounting ensures that

the use of techniques

and methods can be

made so that the

problems can be

solved.

Time Period Financial accounting is

used to examine the

result of the

transactions which

have been done so that

a proper analysis and

interpretation can be

done.

Management

accounting is used in

order to forecast the

results of the future in

the right manner.

User groups of Financial accounting-

Shareholders- The shareholders are the users of the information which is provided by

the Financial accounting. Thus in this way they can make sure that they get valuable

insights into the operations and functioning of the organization in the right manner. This

2

purpose.

Cost accounting- Cost accounting refers to the branch of Accounting in which the

estimation of overall level of costs can be done highly effectively and efficiently. Thus in

this way the use of different types of methods can be made so that the costs are reduced

which will help in achieving financial goals and objectives (Farre-Mensa and Ljungqvist,

2016).

Difference between Financial accounting and Management accounting

Basis Financial accounting Management

accounting

Usage Financial accounting

puts its focus on

making the use of

financial facts, data and

information so that the

financial goals and

objectives can be

attained.

Management

accounting ensures that

the use of techniques

and methods can be

made so that the

problems can be

solved.

Time Period Financial accounting is

used to examine the

result of the

transactions which

have been done so that

a proper analysis and

interpretation can be

done.

Management

accounting is used in

order to forecast the

results of the future in

the right manner.

User groups of Financial accounting-

Shareholders- The shareholders are the users of the information which is provided by

the Financial accounting. Thus in this way they can make sure that they get valuable

insights into the operations and functioning of the organization in the right manner. This

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

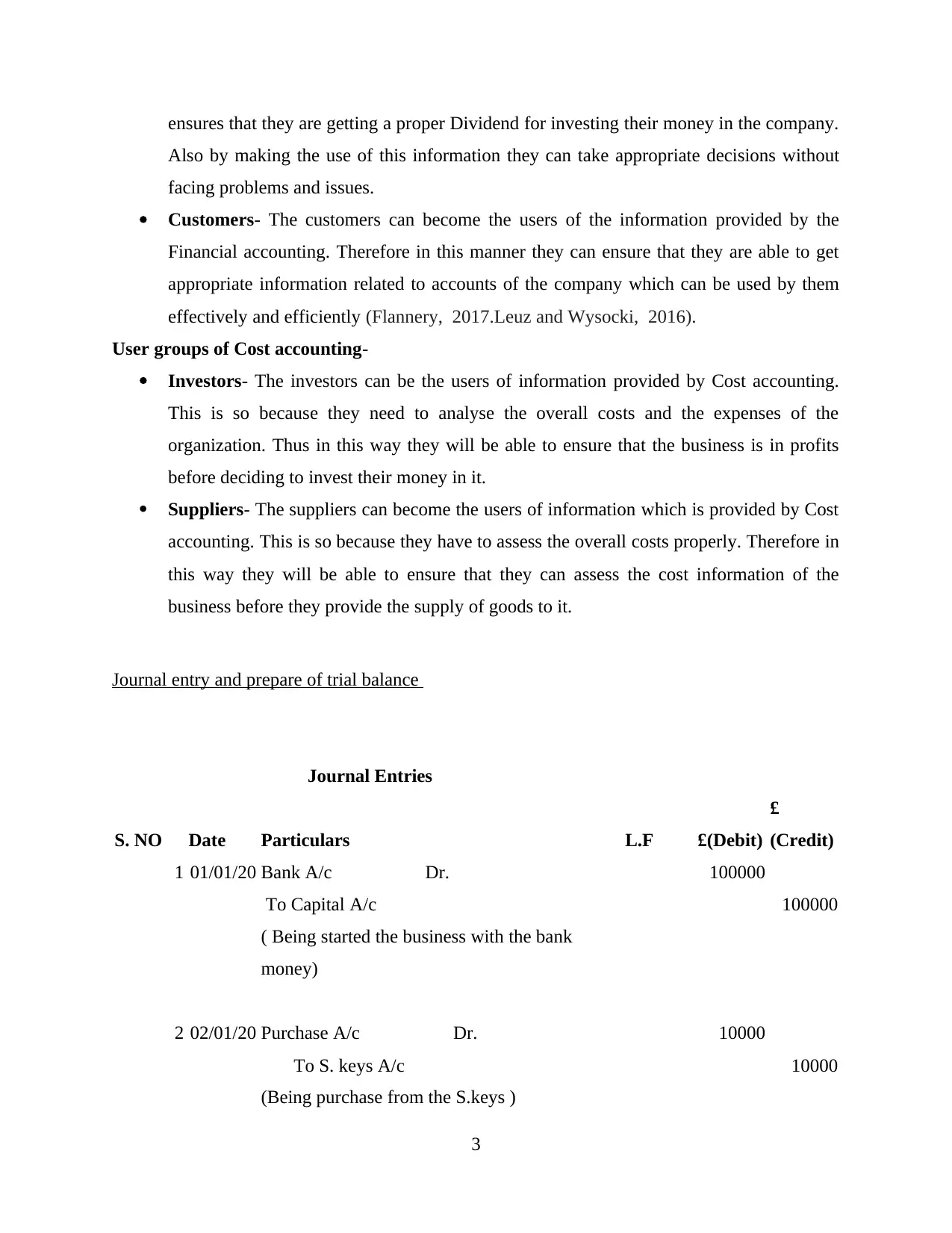

ensures that they are getting a proper Dividend for investing their money in the company.

Also by making the use of this information they can take appropriate decisions without

facing problems and issues.

Customers- The customers can become the users of the information provided by the

Financial accounting. Therefore in this manner they can ensure that they are able to get

appropriate information related to accounts of the company which can be used by them

effectively and efficiently (Flannery, 2017.Leuz and Wysocki, 2016).

User groups of Cost accounting-

Investors- The investors can be the users of information provided by Cost accounting.

This is so because they need to analyse the overall costs and the expenses of the

organization. Thus in this way they will be able to ensure that the business is in profits

before deciding to invest their money in it.

Suppliers- The suppliers can become the users of information which is provided by Cost

accounting. This is so because they have to assess the overall costs properly. Therefore in

this way they will be able to ensure that they can assess the cost information of the

business before they provide the supply of goods to it.

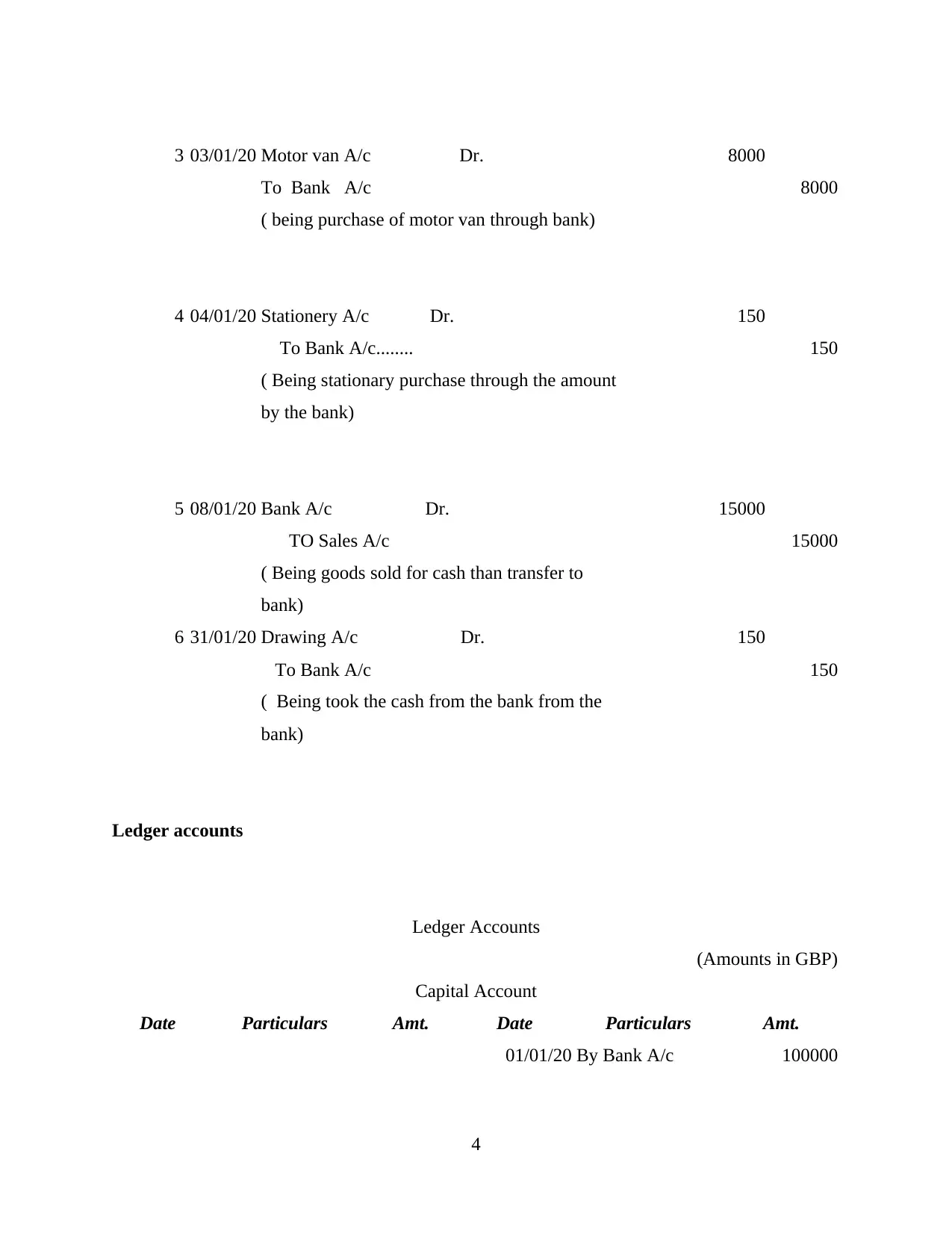

Journal entry and prepare of trial balance

Journal Entries

S. NO Date Particulars L.F £(Debit)

£

(Credit)

1 01/01/20 Bank A/c Dr. 100000

To Capital A/c 100000

( Being started the business with the bank

money)

2 02/01/20 Purchase A/c Dr. 10000

To S. keys A/c 10000

(Being purchase from the S.keys )

3

Also by making the use of this information they can take appropriate decisions without

facing problems and issues.

Customers- The customers can become the users of the information provided by the

Financial accounting. Therefore in this manner they can ensure that they are able to get

appropriate information related to accounts of the company which can be used by them

effectively and efficiently (Flannery, 2017.Leuz and Wysocki, 2016).

User groups of Cost accounting-

Investors- The investors can be the users of information provided by Cost accounting.

This is so because they need to analyse the overall costs and the expenses of the

organization. Thus in this way they will be able to ensure that the business is in profits

before deciding to invest their money in it.

Suppliers- The suppliers can become the users of information which is provided by Cost

accounting. This is so because they have to assess the overall costs properly. Therefore in

this way they will be able to ensure that they can assess the cost information of the

business before they provide the supply of goods to it.

Journal entry and prepare of trial balance

Journal Entries

S. NO Date Particulars L.F £(Debit)

£

(Credit)

1 01/01/20 Bank A/c Dr. 100000

To Capital A/c 100000

( Being started the business with the bank

money)

2 02/01/20 Purchase A/c Dr. 10000

To S. keys A/c 10000

(Being purchase from the S.keys )

3

3 03/01/20 Motor van A/c Dr. 8000

To Bank A/c 8000

( being purchase of motor van through bank)

4 04/01/20 Stationery A/c Dr. 150

To Bank A/c........ 150

( Being stationary purchase through the amount

by the bank)

5 08/01/20 Bank A/c Dr. 15000

TO Sales A/c 15000

( Being goods sold for cash than transfer to

bank)

6 31/01/20 Drawing A/c Dr. 150

To Bank A/c 150

( Being took the cash from the bank from the

bank)

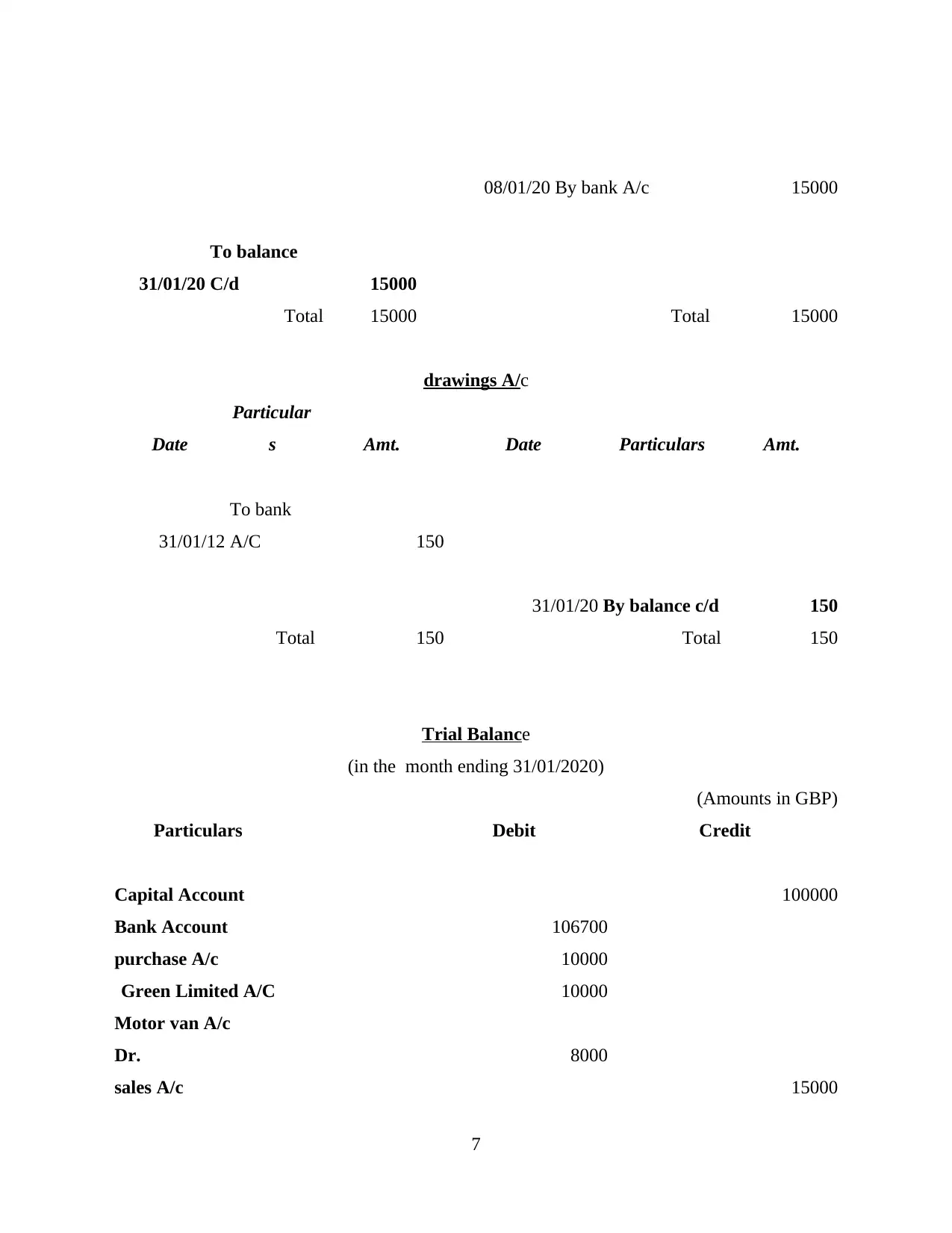

Ledger accounts

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

01/01/20 By Bank A/c 100000

4

To Bank A/c 8000

( being purchase of motor van through bank)

4 04/01/20 Stationery A/c Dr. 150

To Bank A/c........ 150

( Being stationary purchase through the amount

by the bank)

5 08/01/20 Bank A/c Dr. 15000

TO Sales A/c 15000

( Being goods sold for cash than transfer to

bank)

6 31/01/20 Drawing A/c Dr. 150

To Bank A/c 150

( Being took the cash from the bank from the

bank)

Ledger accounts

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amt. Date Particulars Amt.

01/01/20 By Bank A/c 100000

4

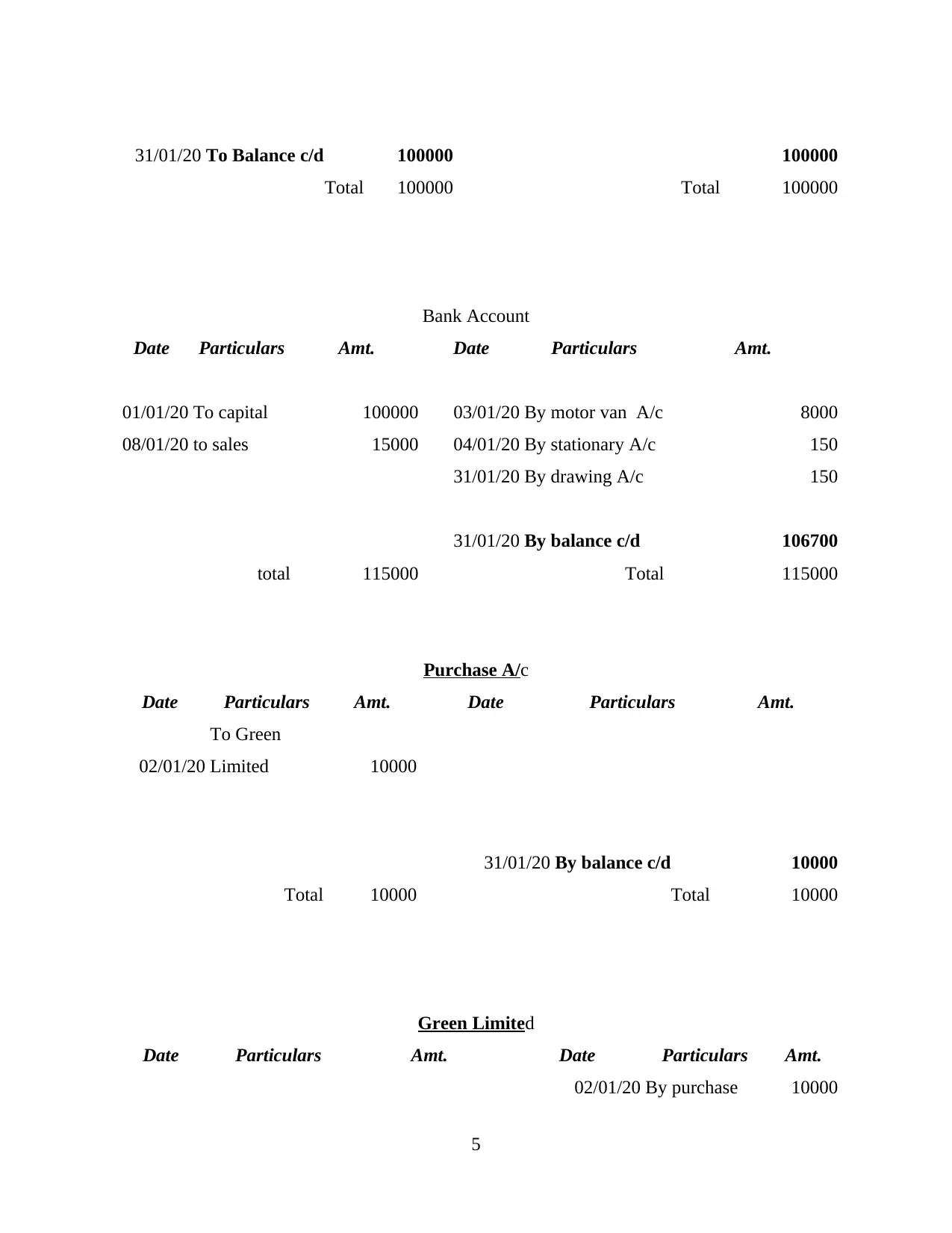

31/01/20 To Balance c/d 100000 100000

Total 100000 Total 100000

Bank Account

Date Particulars Amt. Date Particulars Amt.

01/01/20 To capital 100000 03/01/20 By motor van A/c 8000

08/01/20 to sales 15000 04/01/20 By stationary A/c 150

31/01/20 By drawing A/c 150

31/01/20 By balance c/d 106700

total 115000 Total 115000

Purchase A/c

Date Particulars Amt. Date Particulars Amt.

02/01/20

To Green

Limited 10000

31/01/20 By balance c/d 10000

Total 10000 Total 10000

Green Limited

Date Particulars Amt. Date Particulars Amt.

02/01/20 By purchase 10000

5

Total 100000 Total 100000

Bank Account

Date Particulars Amt. Date Particulars Amt.

01/01/20 To capital 100000 03/01/20 By motor van A/c 8000

08/01/20 to sales 15000 04/01/20 By stationary A/c 150

31/01/20 By drawing A/c 150

31/01/20 By balance c/d 106700

total 115000 Total 115000

Purchase A/c

Date Particulars Amt. Date Particulars Amt.

02/01/20

To Green

Limited 10000

31/01/20 By balance c/d 10000

Total 10000 Total 10000

Green Limited

Date Particulars Amt. Date Particulars Amt.

02/01/20 By purchase 10000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A/c

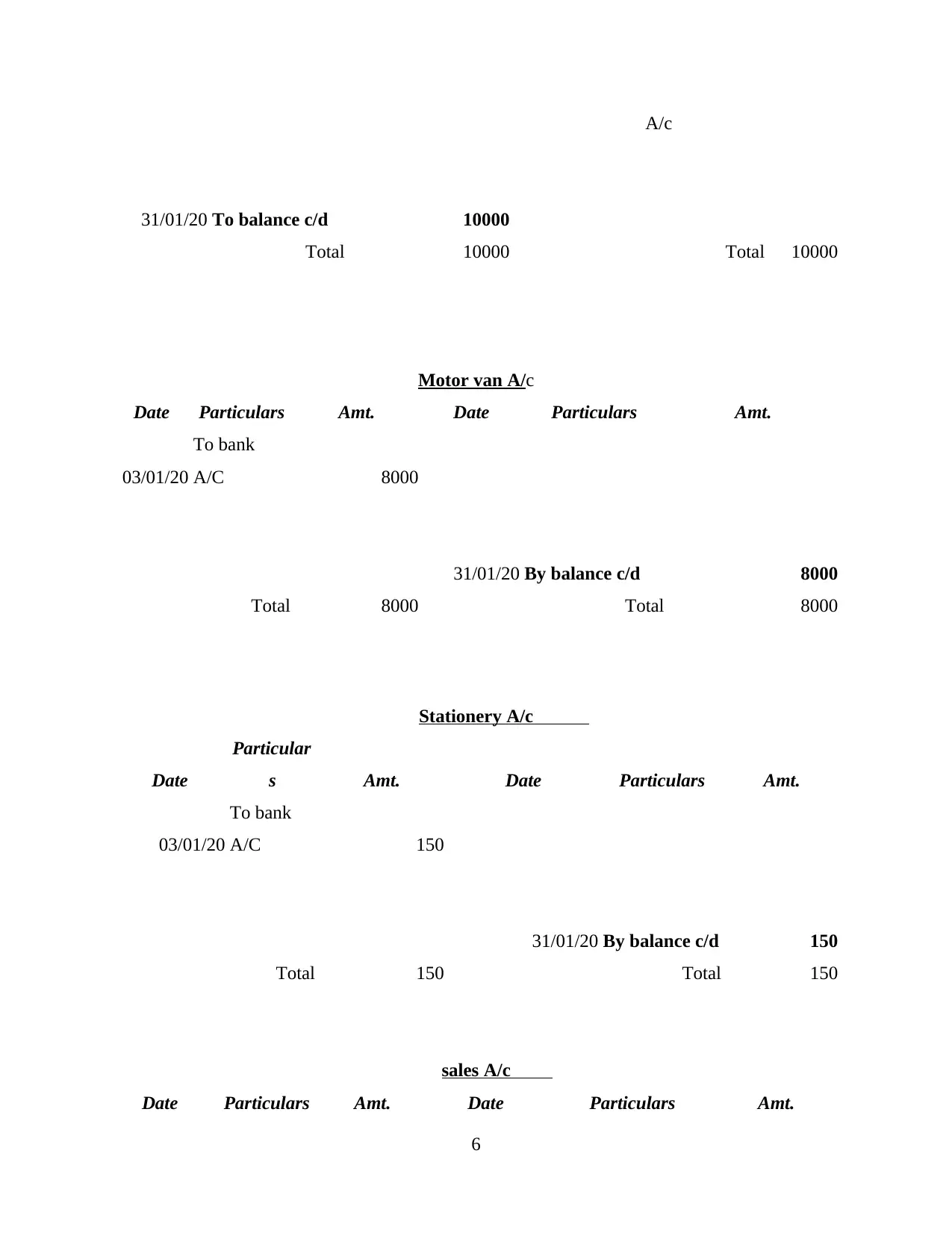

31/01/20 To balance c/d 10000

Total 10000 Total 10000

Motor van A/c

Date Particulars Amt. Date Particulars Amt.

03/01/20

To bank

A/C 8000

31/01/20 By balance c/d 8000

Total 8000 Total 8000

Stationery A/c

Date

Particular

s Amt. Date Particulars Amt.

03/01/20

To bank

A/C 150

31/01/20 By balance c/d 150

Total 150 Total 150

sales A/c

Date Particulars Amt. Date Particulars Amt.

6

31/01/20 To balance c/d 10000

Total 10000 Total 10000

Motor van A/c

Date Particulars Amt. Date Particulars Amt.

03/01/20

To bank

A/C 8000

31/01/20 By balance c/d 8000

Total 8000 Total 8000

Stationery A/c

Date

Particular

s Amt. Date Particulars Amt.

03/01/20

To bank

A/C 150

31/01/20 By balance c/d 150

Total 150 Total 150

sales A/c

Date Particulars Amt. Date Particulars Amt.

6

08/01/20 By bank A/c 15000

31/01/20

To balance

C/d 15000

Total 15000 Total 15000

drawings A/c

Date

Particular

s Amt. Date Particulars Amt.

31/01/12

To bank

A/C 150

31/01/20 By balance c/d 150

Total 150 Total 150

Trial Balance

(in the month ending 31/01/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 100000

Bank Account 106700

purchase A/c 10000

Green Limited A/C 10000

Motor van A/c

Dr. 8000

sales A/c 15000

7

31/01/20

To balance

C/d 15000

Total 15000 Total 15000

drawings A/c

Date

Particular

s Amt. Date Particulars Amt.

31/01/12

To bank

A/C 150

31/01/20 By balance c/d 150

Total 150 Total 150

Trial Balance

(in the month ending 31/01/2020)

(Amounts in GBP)

Particulars Debit Credit

Capital Account 100000

Bank Account 106700

purchase A/c 10000

Green Limited A/C 10000

Motor van A/c

Dr. 8000

sales A/c 15000

7

Stationery A/c 150

drawings A/c 150

Suspense A/c 20000

Total 135000 135000

8

drawings A/c 150

Suspense A/c 20000

Total 135000 135000

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

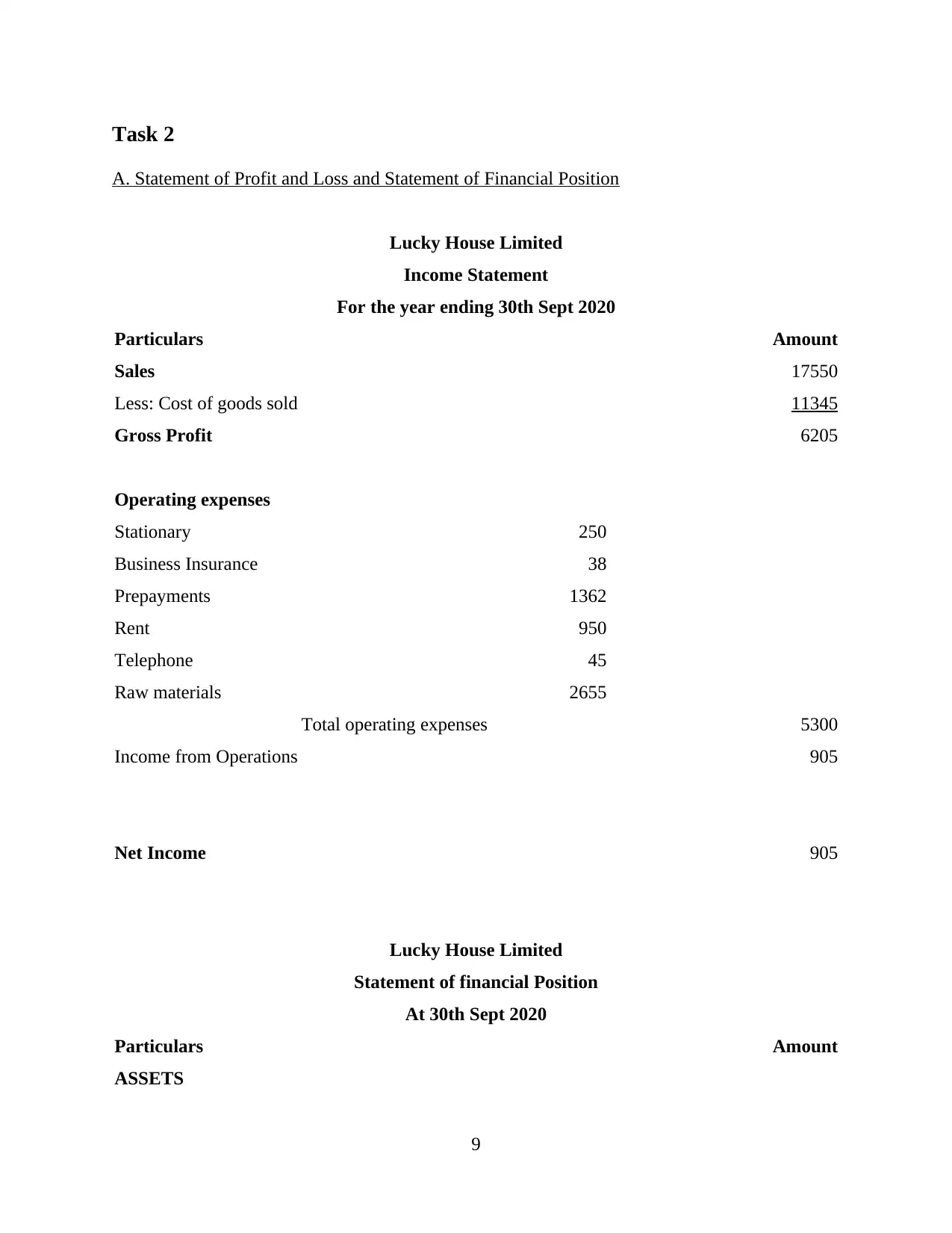

Task 2

A. Statement of Profit and Loss and Statement of Financial Position

Lucky House Limited

Income Statement

For the year ending 30th Sept 2020

Particulars Amount

Sales 17550

Less: Cost of goods sold 11345

Gross Profit 6205

Operating expenses

Stationary 250

Business Insurance 38

Prepayments 1362

Rent 950

Telephone 45

Raw materials 2655

Total operating expenses 5300

Income from Operations 905

Net Income 905

Lucky House Limited

Statement of financial Position

At 30th Sept 2020

Particulars Amount

ASSETS

9

A. Statement of Profit and Loss and Statement of Financial Position

Lucky House Limited

Income Statement

For the year ending 30th Sept 2020

Particulars Amount

Sales 17550

Less: Cost of goods sold 11345

Gross Profit 6205

Operating expenses

Stationary 250

Business Insurance 38

Prepayments 1362

Rent 950

Telephone 45

Raw materials 2655

Total operating expenses 5300

Income from Operations 905

Net Income 905

Lucky House Limited

Statement of financial Position

At 30th Sept 2020

Particulars Amount

ASSETS

9

Non-current Assets:

Machine 8100

Current Assets:

Cash at bank 5850

Accounts Receivable 4500

Total Assets 18450

LIABILITIES

Non-current Liabilities:

Current Liabilities:

Accounts Payable 6545

Total Liabilities 6545

Net Assets 11905

EQUITY

Capital Account 15000

Less: Drawings -4000

Add: Profit 905

Total Equity 11905

B. Statement of Cash Flow

Cash Flow Statement

Lucky House Limited

For the year ended September, 2020

Particulars Amount

10

Machine 8100

Current Assets:

Cash at bank 5850

Accounts Receivable 4500

Total Assets 18450

LIABILITIES

Non-current Liabilities:

Current Liabilities:

Accounts Payable 6545

Total Liabilities 6545

Net Assets 11905

EQUITY

Capital Account 15000

Less: Drawings -4000

Add: Profit 905

Total Equity 11905

B. Statement of Cash Flow

Cash Flow Statement

Lucky House Limited

For the year ended September, 2020

Particulars Amount

10

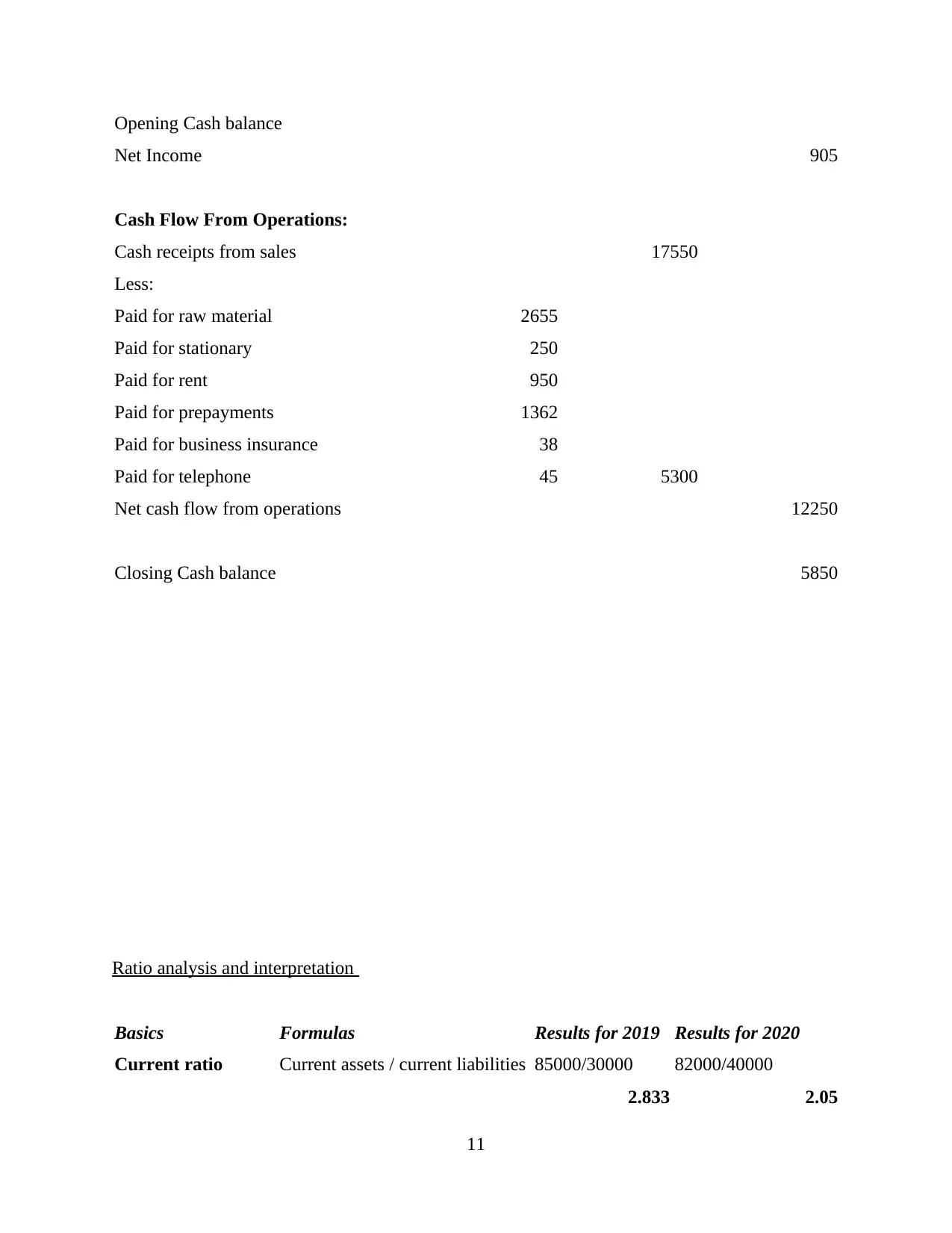

Opening Cash balance

Net Income 905

Cash Flow From Operations:

Cash receipts from sales 17550

Less:

Paid for raw material 2655

Paid for stationary 250

Paid for rent 950

Paid for prepayments 1362

Paid for business insurance 38

Paid for telephone 45 5300

Net cash flow from operations 12250

Closing Cash balance 5850

Ratio analysis and interpretation

Basics Formulas Results for 2019 Results for 2020

Current ratio Current assets / current liabilities 85000/30000 82000/40000

2.833 2.05

11

Net Income 905

Cash Flow From Operations:

Cash receipts from sales 17550

Less:

Paid for raw material 2655

Paid for stationary 250

Paid for rent 950

Paid for prepayments 1362

Paid for business insurance 38

Paid for telephone 45 5300

Net cash flow from operations 12250

Closing Cash balance 5850

Ratio analysis and interpretation

Basics Formulas Results for 2019 Results for 2020

Current ratio Current assets / current liabilities 85000/30000 82000/40000

2.833 2.05

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

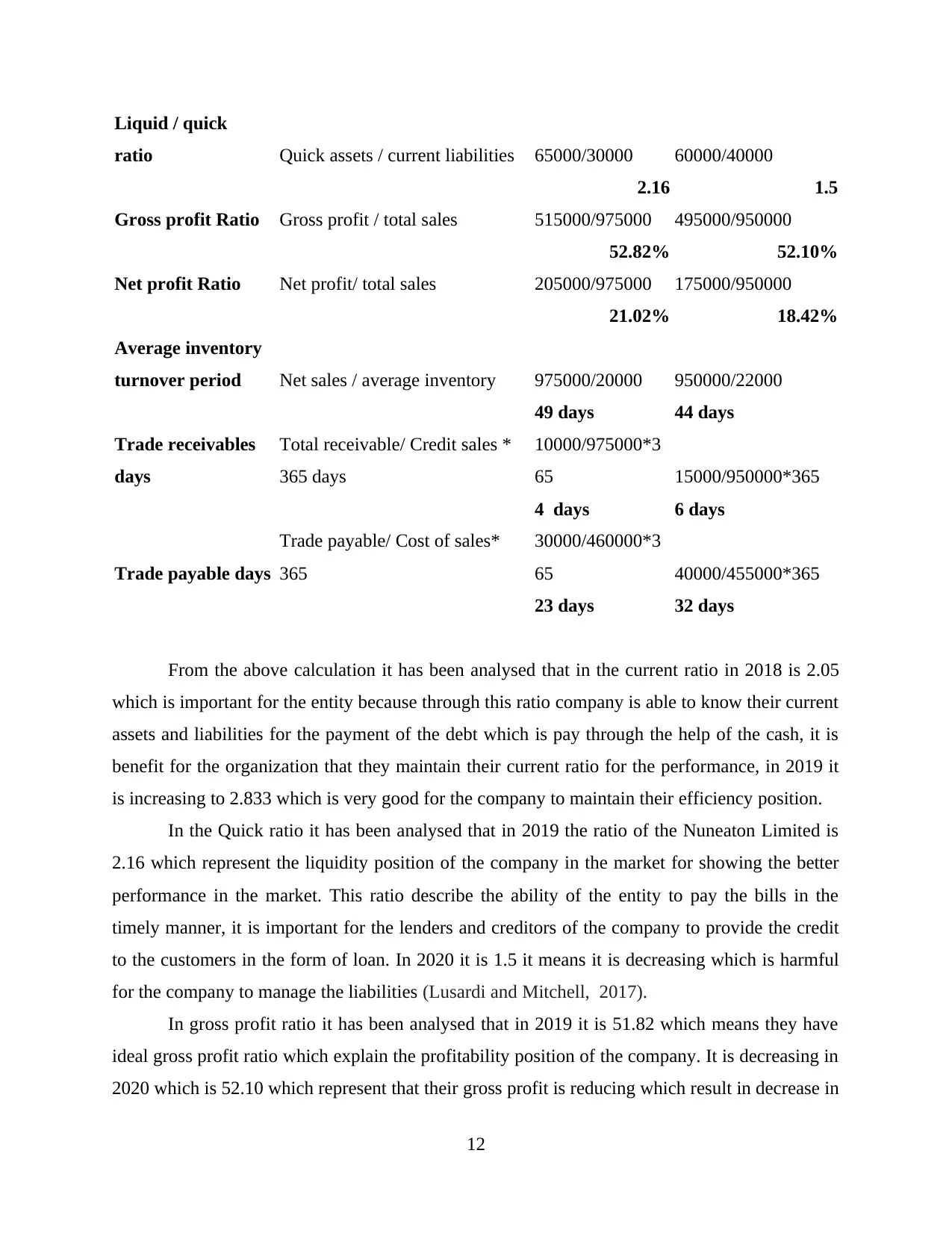

Liquid / quick

ratio Quick assets / current liabilities 65000/30000 60000/40000

2.16 1.5

Gross profit Ratio Gross profit / total sales 515000/975000 495000/950000

52.82% 52.10%

Net profit Ratio Net profit/ total sales 205000/975000 175000/950000

21.02% 18.42%

Average inventory

turnover period Net sales / average inventory 975000/20000 950000/22000

49 days 44 days

Trade receivables

days

Total receivable/ Credit sales *

365 days

10000/975000*3

65 15000/950000*365

4 days 6 days

Trade payable days

Trade payable/ Cost of sales*

365

30000/460000*3

65 40000/455000*365

23 days 32 days

From the above calculation it has been analysed that in the current ratio in 2018 is 2.05

which is important for the entity because through this ratio company is able to know their current

assets and liabilities for the payment of the debt which is pay through the help of the cash, it is

benefit for the organization that they maintain their current ratio for the performance, in 2019 it

is increasing to 2.833 which is very good for the company to maintain their efficiency position.

In the Quick ratio it has been analysed that in 2019 the ratio of the Nuneaton Limited is

2.16 which represent the liquidity position of the company in the market for showing the better

performance in the market. This ratio describe the ability of the entity to pay the bills in the

timely manner, it is important for the lenders and creditors of the company to provide the credit

to the customers in the form of loan. In 2020 it is 1.5 it means it is decreasing which is harmful

for the company to manage the liabilities (Lusardi and Mitchell, 2017).

In gross profit ratio it has been analysed that in 2019 it is 51.82 which means they have

ideal gross profit ratio which explain the profitability position of the company. It is decreasing in

2020 which is 52.10 which represent that their gross profit is reducing which result in decrease in

12

ratio Quick assets / current liabilities 65000/30000 60000/40000

2.16 1.5

Gross profit Ratio Gross profit / total sales 515000/975000 495000/950000

52.82% 52.10%

Net profit Ratio Net profit/ total sales 205000/975000 175000/950000

21.02% 18.42%

Average inventory

turnover period Net sales / average inventory 975000/20000 950000/22000

49 days 44 days

Trade receivables

days

Total receivable/ Credit sales *

365 days

10000/975000*3

65 15000/950000*365

4 days 6 days

Trade payable days

Trade payable/ Cost of sales*

365

30000/460000*3

65 40000/455000*365

23 days 32 days

From the above calculation it has been analysed that in the current ratio in 2018 is 2.05

which is important for the entity because through this ratio company is able to know their current

assets and liabilities for the payment of the debt which is pay through the help of the cash, it is

benefit for the organization that they maintain their current ratio for the performance, in 2019 it

is increasing to 2.833 which is very good for the company to maintain their efficiency position.

In the Quick ratio it has been analysed that in 2019 the ratio of the Nuneaton Limited is

2.16 which represent the liquidity position of the company in the market for showing the better

performance in the market. This ratio describe the ability of the entity to pay the bills in the

timely manner, it is important for the lenders and creditors of the company to provide the credit

to the customers in the form of loan. In 2020 it is 1.5 it means it is decreasing which is harmful

for the company to manage the liabilities (Lusardi and Mitchell, 2017).

In gross profit ratio it has been analysed that in 2019 it is 51.82 which means they have

ideal gross profit ratio which explain the profitability position of the company. It is decreasing in

2020 which is 52.10 which represent that their gross profit is reducing which result in decrease in

12

the sales of the company. Through this investor invest less amount in the company because their

profit is low.

In the Net profit ratio it has been interpreted that in 2019 it is 21.02% which represent

that it determine the profitability position of the company in the market, through this

organization is able to use this ratio for increase the sales, in 2020 it is reduce to 18.42% which

harm the entity because there is reduction in the ratio of the profit which also reduce the

profitability position in the market (Talbot and Boiral, 2018).

In the Average inventory turnover period, it has been interpreted that in 2019 it is 49 days

which show the management of the inventory for the organization which is important for

maintaining the raw materials and finished goods which is their essential part for their regular

activities, in 2020 it is 44 days which means there is the decrease in the inventory turnover

period which mean they are not able to maintain their inventory in the proper way.

In the trade receivables period, it has been analysed that in 2019 it is 4 days which means

there debtor ratio is good they can collect the money from the debtor in the fastest rate which is

very important for the proper management. In the 2020 it is 6 days which means they are not

able to collect money from the debtor in the efficient way in the fastest way which decrease their

cash management in the proper way.

In the trade payable period, it has been interpreted that in 2019 it is 23 days which means

company is able to pay the debt in short period of time but in 2020 it is increasing to 32 days

which means entity is not able to pay to creditors in the fastest way which effect the performance

of their in terms of liquidity and efficiency. It also effect the profitability of the company in the

productive manner (Smets, 2018).

CONCLUSION

From the above report it has been concluded that financial report refers to the analysis of

the financial statements and position of the company in the market. In this report there is the

analysis of the ratio and branch of the accounting and users for the management accounting.

REFERENCES

Books and Journals

Burkhanov, A., 2020. Indicators to assess financial security of the banks.Архив научных

исследований. (27).

13

profit is low.

In the Net profit ratio it has been interpreted that in 2019 it is 21.02% which represent

that it determine the profitability position of the company in the market, through this

organization is able to use this ratio for increase the sales, in 2020 it is reduce to 18.42% which

harm the entity because there is reduction in the ratio of the profit which also reduce the

profitability position in the market (Talbot and Boiral, 2018).

In the Average inventory turnover period, it has been interpreted that in 2019 it is 49 days

which show the management of the inventory for the organization which is important for

maintaining the raw materials and finished goods which is their essential part for their regular

activities, in 2020 it is 44 days which means there is the decrease in the inventory turnover

period which mean they are not able to maintain their inventory in the proper way.

In the trade receivables period, it has been analysed that in 2019 it is 4 days which means

there debtor ratio is good they can collect the money from the debtor in the fastest rate which is

very important for the proper management. In the 2020 it is 6 days which means they are not

able to collect money from the debtor in the efficient way in the fastest way which decrease their

cash management in the proper way.

In the trade payable period, it has been interpreted that in 2019 it is 23 days which means

company is able to pay the debt in short period of time but in 2020 it is increasing to 32 days

which means entity is not able to pay to creditors in the fastest way which effect the performance

of their in terms of liquidity and efficiency. It also effect the profitability of the company in the

productive manner (Smets, 2018).

CONCLUSION

From the above report it has been concluded that financial report refers to the analysis of

the financial statements and position of the company in the market. In this report there is the

analysis of the ratio and branch of the accounting and users for the management accounting.

REFERENCES

Books and Journals

Burkhanov, A., 2020. Indicators to assess financial security of the banks.Архив научных

исследований. (27).

13

Farre-Mensa, J. and Ljungqvist, A., 2016. Do measures of financial constraints measure financial

constraints?.The Review of Financial Studies. 29(2). pp.271-308.

Flannery, M. J., 2017. Stabilizing large financial institutions with contingent capital certificates.

InThe Most Important Concepts in Finance. Edward Elgar Publishing.

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research.Journal of accounting

research. 54(2). pp.525-622.

Lusardi, A. and Mitchell, O.S., 2017. How ordinary consumers make complex economic

decisions: Financial literacy and retirement readiness.Quarterly Journal of Finance.

7(03). p.1750008.

Smets, F., 2018. Financial stability and monetary policy: How closely interlinked?.35th issue

(June 2014) of the International Journal of Central Banking.

Talbot, D. and Boiral, O., 2018. GHG reporting and impression management: An assessment of

sustainability reports from the energy sector.Journal of Business Ethics.147(2). pp.367-

383.

14

constraints?.The Review of Financial Studies. 29(2). pp.271-308.

Flannery, M. J., 2017. Stabilizing large financial institutions with contingent capital certificates.

InThe Most Important Concepts in Finance. Edward Elgar Publishing.

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research.Journal of accounting

research. 54(2). pp.525-622.

Lusardi, A. and Mitchell, O.S., 2017. How ordinary consumers make complex economic

decisions: Financial literacy and retirement readiness.Quarterly Journal of Finance.

7(03). p.1750008.

Smets, F., 2018. Financial stability and monetary policy: How closely interlinked?.35th issue

(June 2014) of the International Journal of Central Banking.

Talbot, D. and Boiral, O., 2018. GHG reporting and impression management: An assessment of

sustainability reports from the energy sector.Journal of Business Ethics.147(2). pp.367-

383.

14

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.