Financial Reporting: Analysis of Financial Statements and IFRS

VerifiedAdded on 2020/06/04

|10

|3155

|58

Report

AI Summary

This report provides a detailed analysis of financial reporting, emphasizing its context, purpose, and the conceptual and regulatory framework. It explores the key principles, stakeholders, and the value of financial reporting in meeting organizational objectives. The report includes an examination of the format of income statements and balance sheets as per IAS 1, along with the uses of financial statements in measuring company performance. It also highlights the differences between IAS and IFRS, the benefits of IFRS adoption, and factors affecting its compliance. The analysis extends to ratio analysis of Tesco, providing insights into gross profit, net profit, current, and debt-equity ratios. The report concludes with a summary of the key findings and implications of financial reporting practices, with the goal of assisting students in understanding the intricacies of financial reporting and its importance in business decision-making.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Context and purpose of financial reporting.....................................................................................1

Conceptual and regulatory framework as well as their requirements and key principles...............1

Main stakeholders of company and way in which they benefit from financial information...........2

Value of financial reporting for meeting organization objectives and growth................................3

Format of income statement and balance sheet as per IAS 1..........................................................3

Uses of company financial statements to meausre company performance.....................................5

Difference between IAS and IFRS..................................................................................................6

Benefits of using IFRS.....................................................................................................................6

Compliance of IFRS and factors in nation that may affect its compliance.....................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Table 1Income statement.................................................................................................................3

Table 2Balance sheet.......................................................................................................................4

Table 3Ratio analysis of Tesco........................................................................................................5

INTRODUCTION...........................................................................................................................1

Context and purpose of financial reporting.....................................................................................1

Conceptual and regulatory framework as well as their requirements and key principles...............1

Main stakeholders of company and way in which they benefit from financial information...........2

Value of financial reporting for meeting organization objectives and growth................................3

Format of income statement and balance sheet as per IAS 1..........................................................3

Uses of company financial statements to meausre company performance.....................................5

Difference between IAS and IFRS..................................................................................................6

Benefits of using IFRS.....................................................................................................................6

Compliance of IFRS and factors in nation that may affect its compliance.....................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Table 1Income statement.................................................................................................................3

Table 2Balance sheet.......................................................................................................................4

Table 3Ratio analysis of Tesco........................................................................................................5

INTRODUCTION

Financial reporting is give due importance by the firms in their busines. This is because it

assist them in making busines decisions more accurately. In the current report detail discussion is

carried out on financial reporting and in this regard its significence is discussed. Apart from this,

varied benefits of adopting IFRS are discussed in the report. By making changes in trial balance

income statement and balance sheet is prepared in the report. At end of the research study,

conclusion section is prepared and in this way research study is carried out.

Context and purpose of financial reporting

Financial reporting refers to the reports that are generated quarterly and annually for the

stakeholders and buisness firms. In financial reporting varied statements are prepared like

income statement, balance sheet and cash flow statement. All these statements have due

importance for the firms and their stakeholders because these statements reflect the current

condition of the busines firm and its strong as well as weak points. It is very important to work

on all these areas because by doing so weak point can be converted in to strong one (Beyer and

et.al., 2010). Financial reporting help managers in spoting areas where they must work and assist

shareholders in deciding whether they must make investment further in the firm or exit from

same. Main purpose of financial reporting is to keep informed managers and other stakeholders

about company condition and to assist them in making strategic business decisions. On basis of

identified weak point managers can determine strategic direction in which business need to be

taken so that maximum profit can be earned and loss can be minimized in the business. It can be

said that there is huge significence of financial reporting for the business firms.

Conceptual and regulatory framework as well as their requirements and key

principles

Conceptual and regulatory framework is prepared because they determine that in which

manner different elements need to be reported in the company accounts like income statement

and balanced. Rules that need to be followed to prepare these statements is also determined and

this ensured that computation is done in accurate manner and comparison can be made between

firms fairly as well as their performance can be measured accurately. Thus, there is huge

significence of conceptual and regulatory framework. Qualitative characteristics make financial

information reliable in nature. It can be observed that there are some of qualitative characteristics

1 | P a g e

Financial reporting is give due importance by the firms in their busines. This is because it

assist them in making busines decisions more accurately. In the current report detail discussion is

carried out on financial reporting and in this regard its significence is discussed. Apart from this,

varied benefits of adopting IFRS are discussed in the report. By making changes in trial balance

income statement and balance sheet is prepared in the report. At end of the research study,

conclusion section is prepared and in this way research study is carried out.

Context and purpose of financial reporting

Financial reporting refers to the reports that are generated quarterly and annually for the

stakeholders and buisness firms. In financial reporting varied statements are prepared like

income statement, balance sheet and cash flow statement. All these statements have due

importance for the firms and their stakeholders because these statements reflect the current

condition of the busines firm and its strong as well as weak points. It is very important to work

on all these areas because by doing so weak point can be converted in to strong one (Beyer and

et.al., 2010). Financial reporting help managers in spoting areas where they must work and assist

shareholders in deciding whether they must make investment further in the firm or exit from

same. Main purpose of financial reporting is to keep informed managers and other stakeholders

about company condition and to assist them in making strategic business decisions. On basis of

identified weak point managers can determine strategic direction in which business need to be

taken so that maximum profit can be earned and loss can be minimized in the business. It can be

said that there is huge significence of financial reporting for the business firms.

Conceptual and regulatory framework as well as their requirements and key

principles

Conceptual and regulatory framework is prepared because they determine that in which

manner different elements need to be reported in the company accounts like income statement

and balanced. Rules that need to be followed to prepare these statements is also determined and

this ensured that computation is done in accurate manner and comparison can be made between

firms fairly as well as their performance can be measured accurately. Thus, there is huge

significence of conceptual and regulatory framework. Qualitative characteristics make financial

information reliable in nature. It can be observed that there are some of qualitative characteristics

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

like understandability, relevance reliability and comparability (Li, 2010). This means that

financial information which is prepared must be understandable in nature. In other words it must

be prepared in such a manner that one on taking single look at statement easily comprehend it.

Other major characteristic of financial information is that financial information that is included

in statement must be relevant. Such kind of facts must not be included in statements that have no

significent use for investors. Facts covered in financial information must be reliable in nature

which means that all these facts must be authentic figures which are computed after following

relevant guidelines. Financial information must be comparable in nature and it must be possible

to compare it with other company financial statements. Thus, firms must follow IFRS principles

and accordingly should prepare income statement and balance sheet so that easily comparison

can be made between firms. It can be said that stong compliance with these principles ensured

that true and fair information will be available to customers at workplace.

Main stakeholders of company and way in which they benefit from financial

information

Stakeholders are the entities that support an organization in number of ways by

partcipating in decision making process and making available important resources which benefit

an organization. There are number of stakeholders of the firm that require financial information

and same are explained below. Managers: These are the one of the main stakeholders of the business firm as they play

an active role in decision making process that is going on in organization (Armstrong,

Guay and Weber,2010). Managers needed company information or financial statements

like income statement and balance sheet in order to find out areas where they need to

make lots of efforts in order to improve organization performance in terms of effeciency

and productivity at workplace. Suppliers: These are those entities that supply raw material to the business firm.

Sometimes these firms supply these materials on credit basis to the company and in this

way give support to them. Suppliers need company financials in order to identify days

within which firm make payment to suppliers on usual basis. On this basis suppliers

decide whether to give raw material to company on credit basis or not. Shareholders: These are those entities that make investment in any company shares and

provide capital to it. These shareholders needed company information in order to

2 | P a g e

financial information which is prepared must be understandable in nature. In other words it must

be prepared in such a manner that one on taking single look at statement easily comprehend it.

Other major characteristic of financial information is that financial information that is included

in statement must be relevant. Such kind of facts must not be included in statements that have no

significent use for investors. Facts covered in financial information must be reliable in nature

which means that all these facts must be authentic figures which are computed after following

relevant guidelines. Financial information must be comparable in nature and it must be possible

to compare it with other company financial statements. Thus, firms must follow IFRS principles

and accordingly should prepare income statement and balance sheet so that easily comparison

can be made between firms. It can be said that stong compliance with these principles ensured

that true and fair information will be available to customers at workplace.

Main stakeholders of company and way in which they benefit from financial

information

Stakeholders are the entities that support an organization in number of ways by

partcipating in decision making process and making available important resources which benefit

an organization. There are number of stakeholders of the firm that require financial information

and same are explained below. Managers: These are the one of the main stakeholders of the business firm as they play

an active role in decision making process that is going on in organization (Armstrong,

Guay and Weber,2010). Managers needed company information or financial statements

like income statement and balance sheet in order to find out areas where they need to

make lots of efforts in order to improve organization performance in terms of effeciency

and productivity at workplace. Suppliers: These are those entities that supply raw material to the business firm.

Sometimes these firms supply these materials on credit basis to the company and in this

way give support to them. Suppliers need company financials in order to identify days

within which firm make payment to suppliers on usual basis. On this basis suppliers

decide whether to give raw material to company on credit basis or not. Shareholders: These are those entities that make investment in any company shares and

provide capital to it. These shareholders needed company information in order to

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

determine whether they must further make investment in firm or exit same from the

company (Barth. and Landsman, 2010). Shareholders do fundamental analysis of the

company and by doing so identify company strong and weak point. On this basis, they

make their investment decisions. Employees: Employees needed company information in order to identify whether same is

on growth track or facing huge problem in the business. It can be said that employees

required financial information less then other stakeholders.

Value of financial reporting for meeting organization objectives and growth

In order to achieve organization objectives and growth there is huge importance of

financial reporting for the firms. This is because in order to achieve growth firms need to work in

specific direction. That area may be business expansion or internal weak area of the company. It

is the financial reporting that help managers in identifying that in which geographic area higher

amount of sales is made. In that specific area business firm decide to make investment. On other

hand, financial reports also reflect the weak area of the firm (Chen and et.al., 2011). Weak area

may be lack of control on expenses in the business. If such kind of things are revealed by

financial report managers can work on that specific area and can prepare plan to ensure that

objectives will be achieved and growth will be obtained in the business. It can be said that there

is huge value of financial reporting because it help them a lot to make decisions that will pave a

way of growth for the firm. In financial reports multiple sort of information are included like

geographical segmentation of revenue and cost analysis etc. All these facts and information are

taken in to account by managers to make strong busines decisions.

Format of income statement and balance sheet as per IAS 1

Table 1Income statement

Revenue 285100

Cost of sales 191700

Gross profit 93400

Operating expenses 39500

Rental income from investment properties 1600

Bank interest 1030

Preference dividend 1330

Ordinary dividend 5340

Deferred taxation 6900

3 | P a g e

company (Barth. and Landsman, 2010). Shareholders do fundamental analysis of the

company and by doing so identify company strong and weak point. On this basis, they

make their investment decisions. Employees: Employees needed company information in order to identify whether same is

on growth track or facing huge problem in the business. It can be said that employees

required financial information less then other stakeholders.

Value of financial reporting for meeting organization objectives and growth

In order to achieve organization objectives and growth there is huge importance of

financial reporting for the firms. This is because in order to achieve growth firms need to work in

specific direction. That area may be business expansion or internal weak area of the company. It

is the financial reporting that help managers in identifying that in which geographic area higher

amount of sales is made. In that specific area business firm decide to make investment. On other

hand, financial reports also reflect the weak area of the firm (Chen and et.al., 2011). Weak area

may be lack of control on expenses in the business. If such kind of things are revealed by

financial report managers can work on that specific area and can prepare plan to ensure that

objectives will be achieved and growth will be obtained in the business. It can be said that there

is huge value of financial reporting because it help them a lot to make decisions that will pave a

way of growth for the firm. In financial reports multiple sort of information are included like

geographical segmentation of revenue and cost analysis etc. All these facts and information are

taken in to account by managers to make strong busines decisions.

Format of income statement and balance sheet as per IAS 1

Table 1Income statement

Revenue 285100

Cost of sales 191700

Gross profit 93400

Operating expenses 39500

Rental income from investment properties 1600

Bank interest 1030

Preference dividend 1330

Ordinary dividend 5340

Deferred taxation 6900

3 | P a g e

Depreciation 8450

Retained earnings 32450

Table 2Balance sheet

Assets

Trade receivables 18000

Investment property at valuation 18000

Land and property at valuation 78750

Plant and equipment at cost 3200

Closing inventory 14000

Bank 1200

133150

Liability

Trade payables 15700

Revaluation reserve 46000

105 redeemable preference shares 13300

Ordinary share capital 26700

Retained earnings 32450

133150

Statement of cash flow wide variety of information then income statement and balance

sheet because in the statement of cash flow varied information are covered related to operating,

investing and financing activity. It can be observed that in statement of income only information

related to divided and interest payment as well as received is given. It can be said that scope of

information covered in income statement is less. Hence, there is less similarity between

statement of income and cash flow statement. On other hand, in case of statement of financial

position and cash flow statement there are similarities to some extent (Altamuro. and Beatty,

2010). This is because in case statement of financial position information related to investment

made in fixed assets and securities are covered. Moreover, infomration related to change in

working capital are directly given in the balance sheet. Apart from this, in balance sheet sources

from which fund is raised is revealed and payments that are made are also reflected if liability of

multiple years are compared with each other. In case of cash flow statement all these facts are

already given and due to this reason it can be said that there is high degree of similarity between

cash flow statement and balance sheet. In other words, it can be said that in cash flow statement

information related to operating activities are also covered which is not observed in case of

4 | P a g e

Retained earnings 32450

Table 2Balance sheet

Assets

Trade receivables 18000

Investment property at valuation 18000

Land and property at valuation 78750

Plant and equipment at cost 3200

Closing inventory 14000

Bank 1200

133150

Liability

Trade payables 15700

Revaluation reserve 46000

105 redeemable preference shares 13300

Ordinary share capital 26700

Retained earnings 32450

133150

Statement of cash flow wide variety of information then income statement and balance

sheet because in the statement of cash flow varied information are covered related to operating,

investing and financing activity. It can be observed that in statement of income only information

related to divided and interest payment as well as received is given. It can be said that scope of

information covered in income statement is less. Hence, there is less similarity between

statement of income and cash flow statement. On other hand, in case of statement of financial

position and cash flow statement there are similarities to some extent (Altamuro. and Beatty,

2010). This is because in case statement of financial position information related to investment

made in fixed assets and securities are covered. Moreover, infomration related to change in

working capital are directly given in the balance sheet. Apart from this, in balance sheet sources

from which fund is raised is revealed and payments that are made are also reflected if liability of

multiple years are compared with each other. In case of cash flow statement all these facts are

already given and due to this reason it can be said that there is high degree of similarity between

cash flow statement and balance sheet. In other words, it can be said that in cash flow statement

information related to operating activities are also covered which is not observed in case of

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

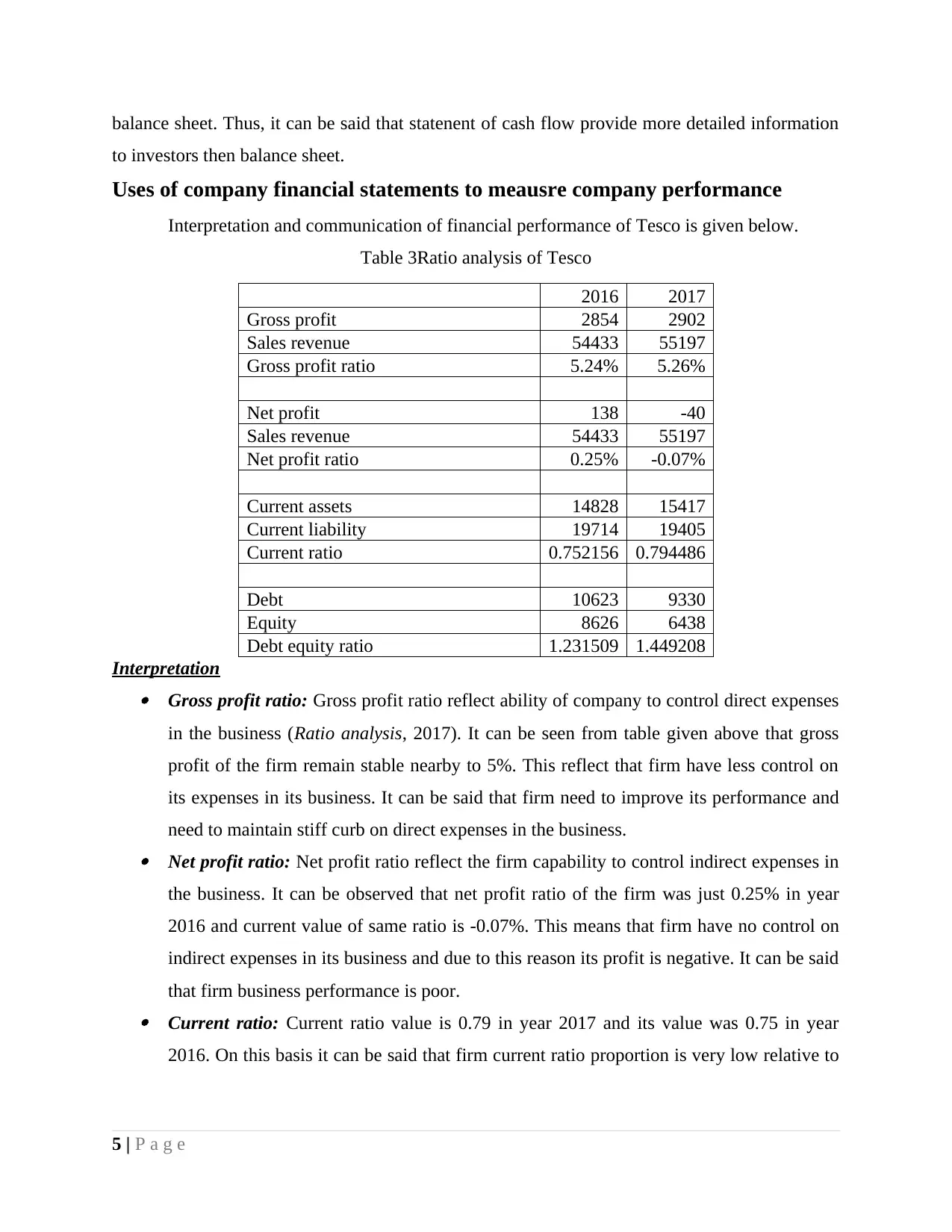

balance sheet. Thus, it can be said that statenent of cash flow provide more detailed information

to investors then balance sheet.

Uses of company financial statements to meausre company performance

Interpretation and communication of financial performance of Tesco is given below.

Table 3Ratio analysis of Tesco

2016 2017

Gross profit 2854 2902

Sales revenue 54433 55197

Gross profit ratio 5.24% 5.26%

Net profit 138 -40

Sales revenue 54433 55197

Net profit ratio 0.25% -0.07%

Current assets 14828 15417

Current liability 19714 19405

Current ratio 0.752156 0.794486

Debt 10623 9330

Equity 8626 6438

Debt equity ratio 1.231509 1.449208

Interpretation Gross profit ratio: Gross profit ratio reflect ability of company to control direct expenses

in the business (Ratio analysis, 2017). It can be seen from table given above that gross

profit of the firm remain stable nearby to 5%. This reflect that firm have less control on

its expenses in its business. It can be said that firm need to improve its performance and

need to maintain stiff curb on direct expenses in the business. Net profit ratio: Net profit ratio reflect the firm capability to control indirect expenses in

the business. It can be observed that net profit ratio of the firm was just 0.25% in year

2016 and current value of same ratio is -0.07%. This means that firm have no control on

indirect expenses in its business and due to this reason its profit is negative. It can be said

that firm business performance is poor. Current ratio: Current ratio value is 0.79 in year 2017 and its value was 0.75 in year

2016. On this basis it can be said that firm current ratio proportion is very low relative to

5 | P a g e

to investors then balance sheet.

Uses of company financial statements to meausre company performance

Interpretation and communication of financial performance of Tesco is given below.

Table 3Ratio analysis of Tesco

2016 2017

Gross profit 2854 2902

Sales revenue 54433 55197

Gross profit ratio 5.24% 5.26%

Net profit 138 -40

Sales revenue 54433 55197

Net profit ratio 0.25% -0.07%

Current assets 14828 15417

Current liability 19714 19405

Current ratio 0.752156 0.794486

Debt 10623 9330

Equity 8626 6438

Debt equity ratio 1.231509 1.449208

Interpretation Gross profit ratio: Gross profit ratio reflect ability of company to control direct expenses

in the business (Ratio analysis, 2017). It can be seen from table given above that gross

profit of the firm remain stable nearby to 5%. This reflect that firm have less control on

its expenses in its business. It can be said that firm need to improve its performance and

need to maintain stiff curb on direct expenses in the business. Net profit ratio: Net profit ratio reflect the firm capability to control indirect expenses in

the business. It can be observed that net profit ratio of the firm was just 0.25% in year

2016 and current value of same ratio is -0.07%. This means that firm have no control on

indirect expenses in its business and due to this reason its profit is negative. It can be said

that firm business performance is poor. Current ratio: Current ratio value is 0.79 in year 2017 and its value was 0.75 in year

2016. On this basis it can be said that firm current ratio proportion is very low relative to

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

current liability. It can be said that it is very hard task for the company to pay all its

current liabilities on time by using current assets. Debt equity ratio: Debt equity ratio value is 1.23 in year 2016 and 1.44 in 2017. It can be

said that proportion of debt is greater then equity value and it can be assumed thart firm

need to make its capital structure balanced.

Difference between IAS and IFRS

There is differencen between IAS and IFRS in many ways as former one stand for

International accounting standards and IFRS stand for international financial reporting standard.

One of the major difference between IAS and IFRS is that many times provisions of both comes

in contradiction with each other. In such kind of situation preference is given to provision of

IFRS then IAS (Chen. and et.al., 2010). Other major difference between IAS and IFRS is that

standards of former one were published between 1973 and 2001. On other hand, in case of IFRS

all standards were published after 2001. Third difference between IAS and IFRS is that IAS were

issued by IASC whereas IFRS were issued by IASB. Other difference that can be observed

between IAS and IFRS is that in international accounting standard only standards are given and

reporting is not done. Whereas, in case of IFRS standards are also given and it is also clarified

that in what manner financial reporting must be done. It can be said that there is huge difference

between IAS and IFRS and latter one cover latest principles of reporting which make IFRS more

popular between accounting experts then IAS.

Benefits of using IFRS Focus on investors: IFRS standards of financial reporting are prepared by considering

investors and format of income statement, balance sheet and cash flow statement is

simplified. Due to this reason it can be said that IFRS have number of benefits for

investors. Loss recognition timeliness: Identification of loss immediately is the one of the key

feature of IFRS as it helps stakeholders in evaluating firm performance at fast rate. It can

be said that transparency increased in operations due to usage of IFRS. This is the one of

the major strength of IFRS for the business firms (Costello, 2011). Comparability: IFRS convergence takes place in EU and due to this reason comparability

of financial statememnts increased at fast rate. It can be said that IFRS adoption increased

6 | P a g e

current liabilities on time by using current assets. Debt equity ratio: Debt equity ratio value is 1.23 in year 2016 and 1.44 in 2017. It can be

said that proportion of debt is greater then equity value and it can be assumed thart firm

need to make its capital structure balanced.

Difference between IAS and IFRS

There is differencen between IAS and IFRS in many ways as former one stand for

International accounting standards and IFRS stand for international financial reporting standard.

One of the major difference between IAS and IFRS is that many times provisions of both comes

in contradiction with each other. In such kind of situation preference is given to provision of

IFRS then IAS (Chen. and et.al., 2010). Other major difference between IAS and IFRS is that

standards of former one were published between 1973 and 2001. On other hand, in case of IFRS

all standards were published after 2001. Third difference between IAS and IFRS is that IAS were

issued by IASC whereas IFRS were issued by IASB. Other difference that can be observed

between IAS and IFRS is that in international accounting standard only standards are given and

reporting is not done. Whereas, in case of IFRS standards are also given and it is also clarified

that in what manner financial reporting must be done. It can be said that there is huge difference

between IAS and IFRS and latter one cover latest principles of reporting which make IFRS more

popular between accounting experts then IAS.

Benefits of using IFRS Focus on investors: IFRS standards of financial reporting are prepared by considering

investors and format of income statement, balance sheet and cash flow statement is

simplified. Due to this reason it can be said that IFRS have number of benefits for

investors. Loss recognition timeliness: Identification of loss immediately is the one of the key

feature of IFRS as it helps stakeholders in evaluating firm performance at fast rate. It can

be said that transparency increased in operations due to usage of IFRS. This is the one of

the major strength of IFRS for the business firms (Costello, 2011). Comparability: IFRS convergence takes place in EU and due to this reason comparability

of financial statememnts increased at fast rate. It can be said that IFRS adoption increased

6 | P a g e

at fast rate in EU and due to increase in comparability it become more easy for investors

to make business decisions. Standardization of accounting and financial reporting: In IFRS standardization of

accounting and financial reporting happened. There are clearly determined rules and

regulations that need to be followed while preparing financial statements. It can be said

that standardization and wide adoption are other major benefits of financial reporting.

Compliance of IFRS and factors in nation that may affect its compliance

Across the globe firms are complying with IFRS and increasingly adopted it to ensure

that accounting is done in better way and facts as well as information are provided to

stakeholders in legitimate manner. However, there are some barriers in the nation which are

preventing adoption of IFRS in the nations. This is because in every nation there are already

determined rules in regulations. It is very hard task to replace entire accounting system

overnight. Hence, it is very time consuming and expensive task to match country accounting

standards with IFRS standards and making changes in it accordingly (McGuire, Omer and Sharp,

2011). Due to adoption of IFRS by replacing nation accounting standards accounting differences

are observed. Alongwith this, reporting difference, tax difference, effect on statutory reporting

and effect on regulatory reporting is also observed. It can be said that due to such kind of

changes that can be observed in entire accounting and taxation system (barrier) nations abstained

from adoption of IFRS for accounting and reporting purpose.

CONCLUSION

On basis of above discussion it is concluded that there is significent importance of

financial reporting for the firms. This is because it assist them in making business decisions. It is

also concluded that there is significent importance of IFRS for the firms and it make reporting of

results much better and ensure that on taking single look on statements they will be able to make

better decisions. It is also concluded that some of the factors like need to change entire

accounting system is the one of the factor that prevent adoption of IFRS in business.

7 | P a g e

to make business decisions. Standardization of accounting and financial reporting: In IFRS standardization of

accounting and financial reporting happened. There are clearly determined rules and

regulations that need to be followed while preparing financial statements. It can be said

that standardization and wide adoption are other major benefits of financial reporting.

Compliance of IFRS and factors in nation that may affect its compliance

Across the globe firms are complying with IFRS and increasingly adopted it to ensure

that accounting is done in better way and facts as well as information are provided to

stakeholders in legitimate manner. However, there are some barriers in the nation which are

preventing adoption of IFRS in the nations. This is because in every nation there are already

determined rules in regulations. It is very hard task to replace entire accounting system

overnight. Hence, it is very time consuming and expensive task to match country accounting

standards with IFRS standards and making changes in it accordingly (McGuire, Omer and Sharp,

2011). Due to adoption of IFRS by replacing nation accounting standards accounting differences

are observed. Alongwith this, reporting difference, tax difference, effect on statutory reporting

and effect on regulatory reporting is also observed. It can be said that due to such kind of

changes that can be observed in entire accounting and taxation system (barrier) nations abstained

from adoption of IFRS for accounting and reporting purpose.

CONCLUSION

On basis of above discussion it is concluded that there is significent importance of

financial reporting for the firms. This is because it assist them in making business decisions. It is

also concluded that there is significent importance of IFRS for the firms and it make reporting of

results much better and ensure that on taking single look on statements they will be able to make

better decisions. It is also concluded that some of the factors like need to change entire

accounting system is the one of the factor that prevent adoption of IFRS in business.

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Agoglia, C.P., Doupnik, T.S. and Tsakumis, G.T., 2011. Principles-based versus rules-based

accounting standards: The influence of standard precision and audit committee strength

on financial reporting decisions. The Accounting Review. 86(3). pp.747-767.

Altamuro, J. and Beatty, A., 2010. How does internal control regulation affect financial

reporting?. Journal of accounting and Economics. 49(1). pp.58-74.

Armstrong, C.S., Guay, W.R. and Weber, J.P., 2010. The role of information and financial

reporting in corporate governance and debt contracting. Journal of Accounting and

Economics. 50(2). pp.179-234.

Barth, M.E. and Landsman, W.R., 2010. How did financial reporting contribute to the financial

crisis?. European accounting review. 19(3). pp.399-423.

Beyer, A., and et.al., 2010. The financial reporting environment: Review of the recent

literature. Journal of accounting and economics. 50(2). pp.296-343.

Chen, F. and et.al., 2011. Financial reporting quality and investment efficiency of private firms

in emerging markets. The accounting review. 86(4). pp.1255-1288.

Chen, H. and et.al., 2010. The role of international financial reporting standards in accounting

quality: Evidence from the European Union. Journal of International Financial

Management & Accounting. 21(3). pp.220-278.

Costello, A.M., 2011. The impact of financial reporting quality on debt contracting: Evidence

from internal control weakness reports. Journal of Accounting Research. 49(1). pp.97-

136.

Li, S., 2010. Does mandatory adoption of International Financial Reporting Standards in the

European Union reduce the cost of equity capital?. The accounting review. 85(2). pp.607-

636.

McGuire, S.T., Omer, T.C. and Sharp, N.Y., 2011. The impact of religion on financial reporting

irregularities. The Accounting Review. 87(2). pp.645-673.

Online

Ratio analysis, 2017. [Online]. Available through:<

http://www.zenwealth.com/businessfinanceonline/RA/RatioAnalysis.html>.

8 | P a g e

Books and Journals

Agoglia, C.P., Doupnik, T.S. and Tsakumis, G.T., 2011. Principles-based versus rules-based

accounting standards: The influence of standard precision and audit committee strength

on financial reporting decisions. The Accounting Review. 86(3). pp.747-767.

Altamuro, J. and Beatty, A., 2010. How does internal control regulation affect financial

reporting?. Journal of accounting and Economics. 49(1). pp.58-74.

Armstrong, C.S., Guay, W.R. and Weber, J.P., 2010. The role of information and financial

reporting in corporate governance and debt contracting. Journal of Accounting and

Economics. 50(2). pp.179-234.

Barth, M.E. and Landsman, W.R., 2010. How did financial reporting contribute to the financial

crisis?. European accounting review. 19(3). pp.399-423.

Beyer, A., and et.al., 2010. The financial reporting environment: Review of the recent

literature. Journal of accounting and economics. 50(2). pp.296-343.

Chen, F. and et.al., 2011. Financial reporting quality and investment efficiency of private firms

in emerging markets. The accounting review. 86(4). pp.1255-1288.

Chen, H. and et.al., 2010. The role of international financial reporting standards in accounting

quality: Evidence from the European Union. Journal of International Financial

Management & Accounting. 21(3). pp.220-278.

Costello, A.M., 2011. The impact of financial reporting quality on debt contracting: Evidence

from internal control weakness reports. Journal of Accounting Research. 49(1). pp.97-

136.

Li, S., 2010. Does mandatory adoption of International Financial Reporting Standards in the

European Union reduce the cost of equity capital?. The accounting review. 85(2). pp.607-

636.

McGuire, S.T., Omer, T.C. and Sharp, N.Y., 2011. The impact of religion on financial reporting

irregularities. The Accounting Review. 87(2). pp.645-673.

Online

Ratio analysis, 2017. [Online]. Available through:<

http://www.zenwealth.com/businessfinanceonline/RA/RatioAnalysis.html>.

8 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.